Qantas Airways Financial Report Analysis: Corporate Accounting

VerifiedAdded on 2021/05/27

|15

|2691

|480

Report

AI Summary

This report provides a comprehensive analysis of Qantas Airways' financial statements, focusing on corporate accounting principles. The analysis includes a detailed examination of the cash flow statement, breaking down operating, investing, and financing activities for the years 2015-2017. It explores the items included in each category and explains the trends observed. The report also delves into the statement of comprehensive income, outlining items that may or may not be reclassified to profit or loss, and examines the statutory profit and exchange differences. Furthermore, it analyzes the company's tax expenditure, including the calculation of income tax and deferred tax assets/liabilities, and reconciles income tax expense with income tax payable. The report highlights the differences between income tax expenses and cash payments for income tax, providing a thorough understanding of Qantas Airways' financial performance and accounting practices.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

University Name

Student Name

Authors’ Note

Corporate Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

CORPORATE ACCOUNTING

Table of Contents

Answer i)....................................................................................................................................2

Answer ii)...................................................................................................................................4

Answer iii)..................................................................................................................................5

Answer iv)..................................................................................................................................6

Answer v)...................................................................................................................................6

Answer vi)..................................................................................................................................6

Answer vii).................................................................................................................................7

Answer viii)................................................................................................................................7

Answer ix)..................................................................................................................................8

Answer x)...................................................................................................................................8

Answer xi)..................................................................................................................................9

References................................................................................................................................10

Appendix..................................................................................................................................12

CORPORATE ACCOUNTING

Table of Contents

Answer i)....................................................................................................................................2

Answer ii)...................................................................................................................................4

Answer iii)..................................................................................................................................5

Answer iv)..................................................................................................................................6

Answer v)...................................................................................................................................6

Answer vi)..................................................................................................................................6

Answer vii).................................................................................................................................7

Answer viii)................................................................................................................................7

Answer ix)..................................................................................................................................8

Answer x)...................................................................................................................................8

Answer xi)..................................................................................................................................9

References................................................................................................................................10

Appendix..................................................................................................................................12

3

CORPORATE ACCOUNTING

The company chosen for the current study is Qantas Airways. Qantas Airways is largest

airline in Australia in terms of size of fleet, intercontinental flights and global destinations

and is regarded as the flag carrier of the nation Australia. This is a publicly traded company

and is listed in the Australian Stock Exchange.

Answer i)

The items that are included in the cash flow statement of the firm can be categorised under

three different heads namely, financing, investing as well as operating activities. The list of

items that are mentioned under the heading of “cash flow for the purpose of operating

activities comprises of depreciation, specific adjustments in earnings, changes in accounts

receivables, inventory along with changes in the company’s liability (Siew 2015). As per the

annual report of the firm, the flows of cash from operating activities include receipts of cash

from particularly customers, disbursements of cash to different suppliers as well as

employees. In addition to this, there are payments of cash to different employees for various

redundancies as well as associated costs, payments of cash to firm’s employees for

particularly Wage Freeze Bonus as well as Record Results Bonus. Also, flow of cash from

operations also includes interests received and paid, dividends received for investments as

well as payments of income taxes. Thereafter, the items included under Qantas’s investing

activities include disbursements for particularly plant, property along with equipments (also

known as PPE), disbursements for interests and capitalised on specific assets, disbursements

for investments (considered under method of equity), earnings generated from sale of PPE

and net repayment of company’s loans. Furthermore, the list of items under the financing

actions of the firm Qantas Airways include payments for particularly buy back of shares,

disbursements for return of capital, treasury shares and pay offs of different borrowings.

Also, proceeds generated from the borrowings are also included under this head. Further, this

CORPORATE ACCOUNTING

The company chosen for the current study is Qantas Airways. Qantas Airways is largest

airline in Australia in terms of size of fleet, intercontinental flights and global destinations

and is regarded as the flag carrier of the nation Australia. This is a publicly traded company

and is listed in the Australian Stock Exchange.

Answer i)

The items that are included in the cash flow statement of the firm can be categorised under

three different heads namely, financing, investing as well as operating activities. The list of

items that are mentioned under the heading of “cash flow for the purpose of operating

activities comprises of depreciation, specific adjustments in earnings, changes in accounts

receivables, inventory along with changes in the company’s liability (Siew 2015). As per the

annual report of the firm, the flows of cash from operating activities include receipts of cash

from particularly customers, disbursements of cash to different suppliers as well as

employees. In addition to this, there are payments of cash to different employees for various

redundancies as well as associated costs, payments of cash to firm’s employees for

particularly Wage Freeze Bonus as well as Record Results Bonus. Also, flow of cash from

operations also includes interests received and paid, dividends received for investments as

well as payments of income taxes. Thereafter, the items included under Qantas’s investing

activities include disbursements for particularly plant, property along with equipments (also

known as PPE), disbursements for interests and capitalised on specific assets, disbursements

for investments (considered under method of equity), earnings generated from sale of PPE

and net repayment of company’s loans. Furthermore, the list of items under the financing

actions of the firm Qantas Airways include payments for particularly buy back of shares,

disbursements for return of capital, treasury shares and pay offs of different borrowings.

Also, proceeds generated from the borrowings are also included under this head. Further, this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

CORPORATE ACCOUNTING

section includes net receipts for varied aircraft security deposits as well as hedges associated

to debt, dividend payments to firm’s shareholders as well as non-controlling interests.

It can also be hereby mentioned that the net cash used for the three different kinds of

activities of the firm are also included in this assertion along with cash as well as cash

equivalents registered at the closing of the year (Miao et al. 2016).

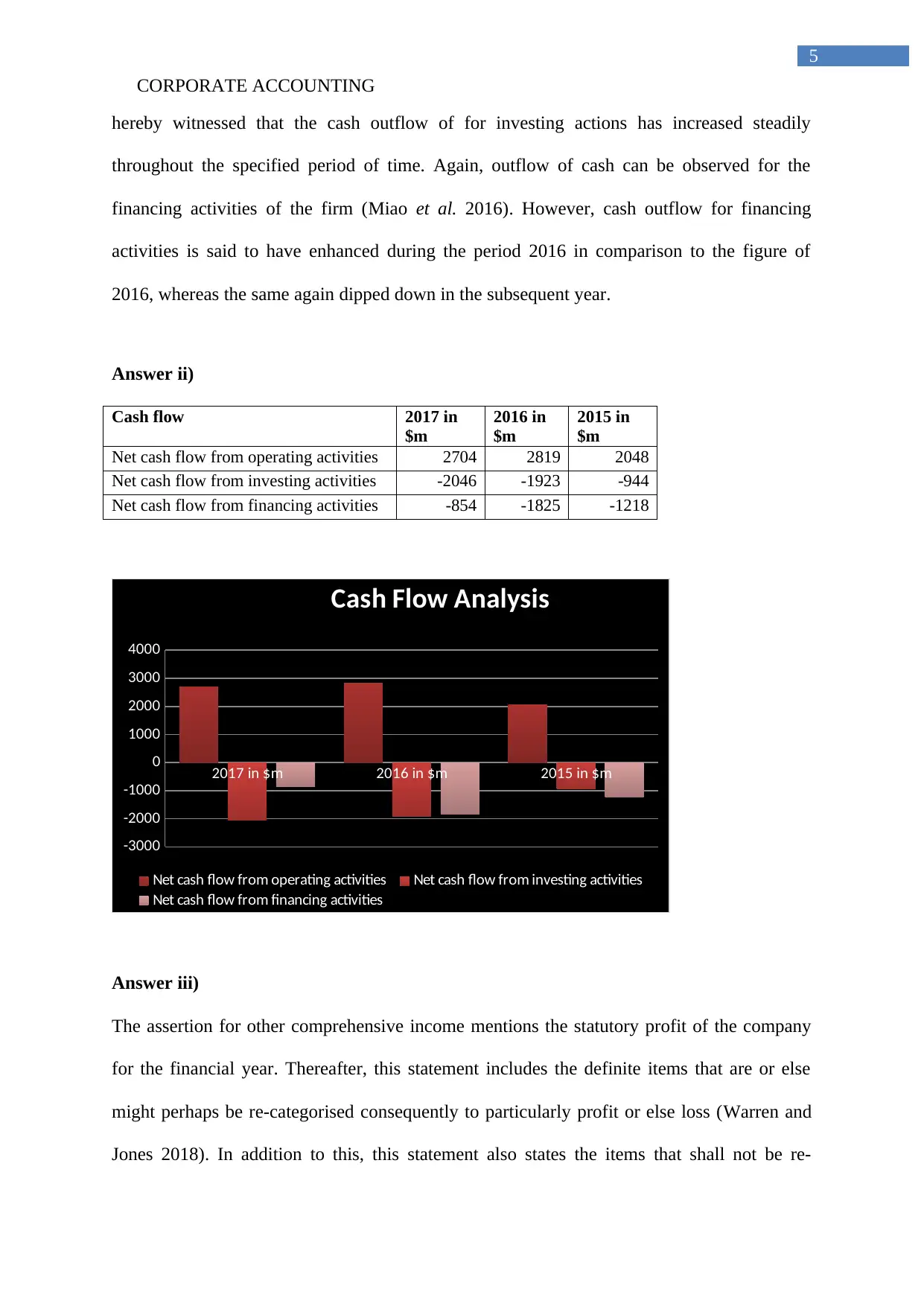

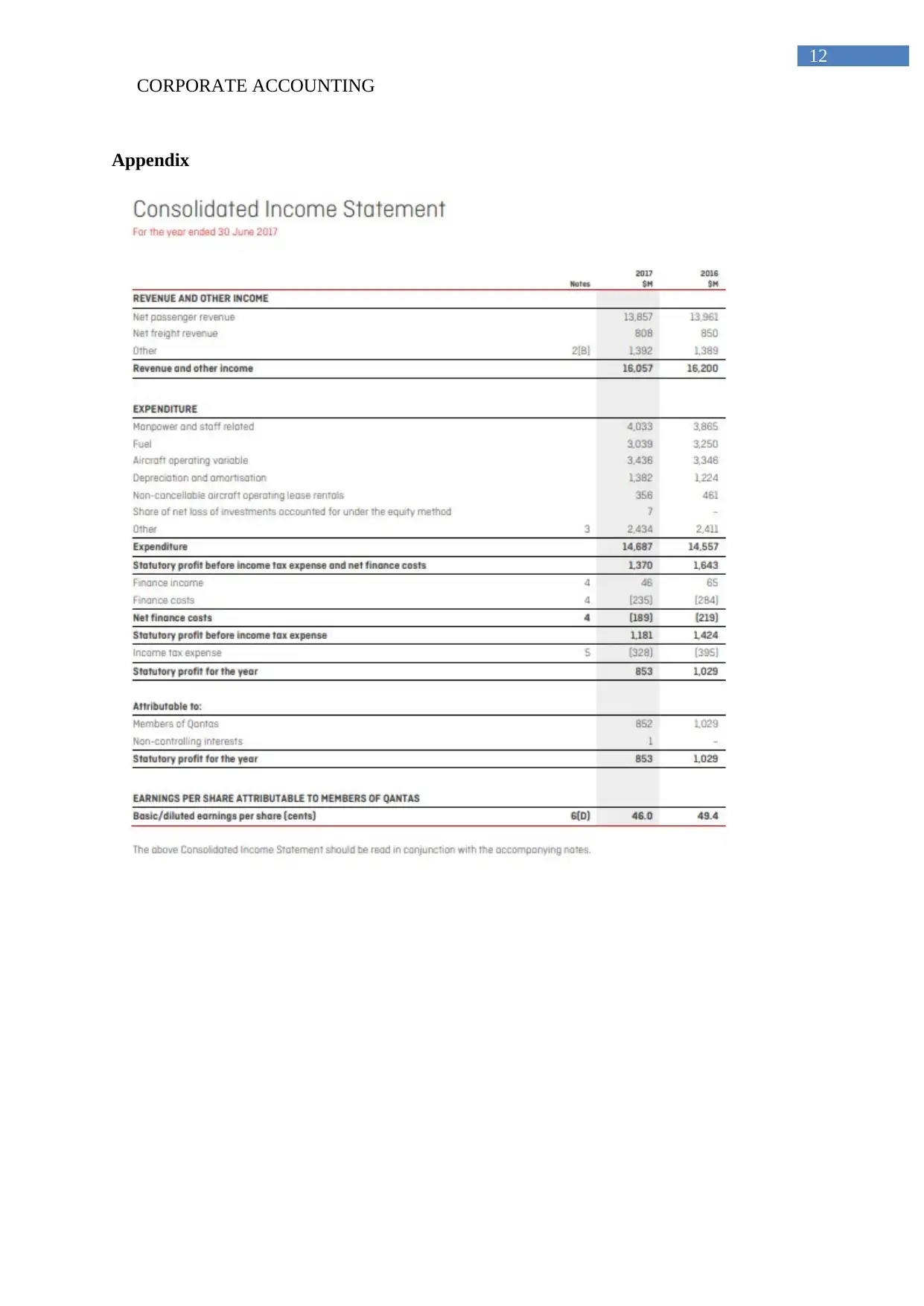

Analysis of the cash flow statement reveals that the cash flow used in operating actions is

registered to be AUD2704 million in 2017 in comparison to AUD 2819 million in 2016,

replicating a decline in the inflow of cash from operating activities. This is mainly due to

decrease in receipts of cash from customers, decline in receipt of interests along with increase

in payments of cash to firm’s employees for wage freeze bonus and increase in tax paid.

Again , cash flow from particularly investing activities shows increase in cash outflow of the

firm from (AUD 1923 million) to (AUD 2046 million). This is mainly due to sharp decline in

the proceeds of the firm from the disposal of its PPE. Again, evaluation of the assertion

replicates decrease in cash outflow for financing actions in the year 2017 to (AUD 854

million) as compared to the year ago figure of (AUD 1825 million). As such, this is primarily

owing to decline in the payments for the buyback of shares as well as repayment of

borrowings (Miao et al. 2016). Finally, the cash as well as cash equivalents of the firm

Qantas Airways recorded at the closing of the year is registered to be AUD 1775 million in

2017 as compared to AUD 1980 million registered in the year 2016.

Graphical and tabular presentation of the cash flow of the firm Qantas Airways for the past

three years are presented below. The net inflow of the company’s cash for operating activities

can be observed to have escalated during the period 2016 as compared to the year ago period,

while the same reflects a sharp decline in the following year that is during the year 2017.

However, outflow of cash has been registered for the investing activities. However, it can be

CORPORATE ACCOUNTING

section includes net receipts for varied aircraft security deposits as well as hedges associated

to debt, dividend payments to firm’s shareholders as well as non-controlling interests.

It can also be hereby mentioned that the net cash used for the three different kinds of

activities of the firm are also included in this assertion along with cash as well as cash

equivalents registered at the closing of the year (Miao et al. 2016).

Analysis of the cash flow statement reveals that the cash flow used in operating actions is

registered to be AUD2704 million in 2017 in comparison to AUD 2819 million in 2016,

replicating a decline in the inflow of cash from operating activities. This is mainly due to

decrease in receipts of cash from customers, decline in receipt of interests along with increase

in payments of cash to firm’s employees for wage freeze bonus and increase in tax paid.

Again , cash flow from particularly investing activities shows increase in cash outflow of the

firm from (AUD 1923 million) to (AUD 2046 million). This is mainly due to sharp decline in

the proceeds of the firm from the disposal of its PPE. Again, evaluation of the assertion

replicates decrease in cash outflow for financing actions in the year 2017 to (AUD 854

million) as compared to the year ago figure of (AUD 1825 million). As such, this is primarily

owing to decline in the payments for the buyback of shares as well as repayment of

borrowings (Miao et al. 2016). Finally, the cash as well as cash equivalents of the firm

Qantas Airways recorded at the closing of the year is registered to be AUD 1775 million in

2017 as compared to AUD 1980 million registered in the year 2016.

Graphical and tabular presentation of the cash flow of the firm Qantas Airways for the past

three years are presented below. The net inflow of the company’s cash for operating activities

can be observed to have escalated during the period 2016 as compared to the year ago period,

while the same reflects a sharp decline in the following year that is during the year 2017.

However, outflow of cash has been registered for the investing activities. However, it can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

CORPORATE ACCOUNTING

hereby witnessed that the cash outflow of for investing actions has increased steadily

throughout the specified period of time. Again, outflow of cash can be observed for the

financing activities of the firm (Miao et al. 2016). However, cash outflow for financing

activities is said to have enhanced during the period 2016 in comparison to the figure of

2016, whereas the same again dipped down in the subsequent year.

Answer ii)

Cash flow 2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating activities 2704 2819 2048

Net cash flow from investing activities -2046 -1923 -944

Net cash flow from financing activities -854 -1825 -1218

2017 in $m 2016 in $m 2015 in $m

-3000

-2000

-1000

0

1000

2000

3000

4000

Cash Flow Analysis

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Answer iii)

The assertion for other comprehensive income mentions the statutory profit of the company

for the financial year. Thereafter, this statement includes the definite items that are or else

might perhaps be re-categorised consequently to particularly profit or else loss (Warren and

Jones 2018). In addition to this, this statement also states the items that shall not be re-

CORPORATE ACCOUNTING

hereby witnessed that the cash outflow of for investing actions has increased steadily

throughout the specified period of time. Again, outflow of cash can be observed for the

financing activities of the firm (Miao et al. 2016). However, cash outflow for financing

activities is said to have enhanced during the period 2016 in comparison to the figure of

2016, whereas the same again dipped down in the subsequent year.

Answer ii)

Cash flow 2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating activities 2704 2819 2048

Net cash flow from investing activities -2046 -1923 -944

Net cash flow from financing activities -854 -1825 -1218

2017 in $m 2016 in $m 2015 in $m

-3000

-2000

-1000

0

1000

2000

3000

4000

Cash Flow Analysis

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Answer iii)

The assertion for other comprehensive income mentions the statutory profit of the company

for the financial year. Thereafter, this statement includes the definite items that are or else

might perhaps be re-categorised consequently to particularly profit or else loss (Warren and

Jones 2018). In addition to this, this statement also states the items that shall not be re-

6

CORPORATE ACCOUNTING

classified to firm’s profit or else loss. Thereafter, this assertion mentions the other

comprehensive earning/loss for the particular year and the total figure for the same (Warren

and Jones 2018). However, the items that are included in the items that might be reclassified

include effectual fraction of changes in particularly fair value of mainly hedges of flow of

cash, transfer of reserve of hedges, recognition of particularly effectual hedge of cash flow,

translation of foreign currency of different controlled entities and translation of specific

investments that is mainly accounted under equity method along with share of various other

comprehensive income else loss of definite investments considered under equity mechanism.

The total comprehensive income of the firm Qantas Airways is recorded to be AUD 1033 in

the financial year 2017 and AUD 850 million in 2016, replicating an increase in the same.

Answer iv)

Statutory profit for the current year is observed to decrease to AUD 853 million in the year

2017 while the same is recorded to be AUD 1029 million in 2016. The exchange differences

can be observed from the effective changes in fair value of hedges of flow of cash. In this

segment there is an outflow amounting to (AUD 187 million) in 2016 that turned to inflow

amounting to AUD 46 million.

Answer v)

Fundamentally, comprehensive statement of earnings is chiefly used for enumerating all the

changes and transformations in interests of different owners (Ijiri 2018). As such, this

considers income together with expenditure of the firm that are necessarily not realised and is

chiefly used for varied derivative instruments, effective changes in mainly fair value of

hedging of flow of cash (considered net of amount of tax), transfer of reserve of hedge to

chiefly consolidated earning statement (considered net of amount of tax). Also, this statement

takes in recognition of effective hedging of flow of cash on specified capitalised asset (that is

CORPORATE ACCOUNTING

classified to firm’s profit or else loss. Thereafter, this assertion mentions the other

comprehensive earning/loss for the particular year and the total figure for the same (Warren

and Jones 2018). However, the items that are included in the items that might be reclassified

include effectual fraction of changes in particularly fair value of mainly hedges of flow of

cash, transfer of reserve of hedges, recognition of particularly effectual hedge of cash flow,

translation of foreign currency of different controlled entities and translation of specific

investments that is mainly accounted under equity method along with share of various other

comprehensive income else loss of definite investments considered under equity mechanism.

The total comprehensive income of the firm Qantas Airways is recorded to be AUD 1033 in

the financial year 2017 and AUD 850 million in 2016, replicating an increase in the same.

Answer iv)

Statutory profit for the current year is observed to decrease to AUD 853 million in the year

2017 while the same is recorded to be AUD 1029 million in 2016. The exchange differences

can be observed from the effective changes in fair value of hedges of flow of cash. In this

segment there is an outflow amounting to (AUD 187 million) in 2016 that turned to inflow

amounting to AUD 46 million.

Answer v)

Fundamentally, comprehensive statement of earnings is chiefly used for enumerating all the

changes and transformations in interests of different owners (Ijiri 2018). As such, this

considers income together with expenditure of the firm that are necessarily not realised and is

chiefly used for varied derivative instruments, effective changes in mainly fair value of

hedging of flow of cash (considered net of amount of tax), transfer of reserve of hedge to

chiefly consolidated earning statement (considered net of amount of tax). Also, this statement

takes in recognition of effective hedging of flow of cash on specified capitalised asset (that is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

CORPORATE ACCOUNTING

again net of amount of tax). In addition to this, this assertion of comprehensive earning also

reveals net transformation in company’s reserve of essentially hedge for specifically time

value of definite options (also considered net of amount of tax) (Maas et al. 2016).

Additionally, this pronouncement also comprises of details of translation of foreign currency,

translation of foreign currency of essentially investment that is taken in under specifically

equity method as well as shares of different other comprehensive gains otherwise losses for

investment enumerated under the equity method.

Answer vi)

The tax expenditure of the company Qantas Airways is recorded to be (AUD328 million in

2017 and (AUD 395 million). Particularly, expenditure for income tax uses domestic rate of

corporate tax of roughly 30%. Together with this, statutory profit before income tax are

essentially adjusted for mainly non-assessable dividends, diverse non-deductible shares of

chiefly net loss for necessarily investments under system of equity, different non-deductible

losses necessarily for foreign branches together with controlled entity losses (Miao et al.

2016). In addition to this, adjustments also take account of utilization of previously

unrecognized capital losses, diverse non-assessable profits on specifically sale of PPE along

with other non-assessable items together with provisions from earlier period.

Answer vii)

The income tax for the firm Qantas Airways is necessarily calculated by using specified tax

rate that are necessarily enforced considerably by the declaration on financial position.

Thorough study of the yearly report of then firm reveals that the present expenditure of the

firm on particularly tax in the year 2017 was registered to be (AUD 328 million) while the

same was recorded to be (AUD 395 million) in the year 2016. Therefore, it cannot be

CORPORATE ACCOUNTING

again net of amount of tax). In addition to this, this assertion of comprehensive earning also

reveals net transformation in company’s reserve of essentially hedge for specifically time

value of definite options (also considered net of amount of tax) (Maas et al. 2016).

Additionally, this pronouncement also comprises of details of translation of foreign currency,

translation of foreign currency of essentially investment that is taken in under specifically

equity method as well as shares of different other comprehensive gains otherwise losses for

investment enumerated under the equity method.

Answer vi)

The tax expenditure of the company Qantas Airways is recorded to be (AUD328 million in

2017 and (AUD 395 million). Particularly, expenditure for income tax uses domestic rate of

corporate tax of roughly 30%. Together with this, statutory profit before income tax are

essentially adjusted for mainly non-assessable dividends, diverse non-deductible shares of

chiefly net loss for necessarily investments under system of equity, different non-deductible

losses necessarily for foreign branches together with controlled entity losses (Miao et al.

2016). In addition to this, adjustments also take account of utilization of previously

unrecognized capital losses, diverse non-assessable profits on specifically sale of PPE along

with other non-assessable items together with provisions from earlier period.

Answer vii)

The income tax for the firm Qantas Airways is necessarily calculated by using specified tax

rate that are necessarily enforced considerably by the declaration on financial position.

Thorough study of the yearly report of then firm reveals that the present expenditure of the

firm on particularly tax in the year 2017 was registered to be (AUD 328 million) while the

same was recorded to be (AUD 395 million) in the year 2016. Therefore, it cannot be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE ACCOUNTING

evaluated whether numerals for income tax expenses are similar to that rate of tax times

overall earnings (Siew 2015).

Answer viii)

It can be hereby observed from the annual report of the firm Qantas Airways that the deferred

tax (assets/liabilities) stands at (AUD 353 million) in the year 2017 whereas the same is

recorded to be AUD 39 million. In essence, deferred tax is mainly recognized with regard to

temporary differences between carrying amounts of assets else wise liabilities for particularly

financial reporting cause and the overall amount used for the purpose of taxation (Miao et al.

2016). In particular, deferred tax assets are essentially recognized for particularly unused tax

losses; credit for necessarily tax together with temporary differences to the specific point that

it becomes plausible that taxable earning in the future period against which they can be used

(Miglani et al. 2015).

Answer ix)

Expenditure for income tax for period 2017 as documented in the financial statement of the

firm stands at (AUD 328 million) and income tax expenditure was observed to be (AUD 395

million) during the period 2016. Nonetheless, the figure for the firm’s income tax payable is

recorded to be (AUD 4 million). Essentially, this replicates a reconciliation of particularly

income tax expenditure of the corporation Qantas Airways to income tax payable. This

process of reconciliation includes adjustments for chiefly temporary differences. Essentially,

adjustments carried out for temporary differences take in adjustments for particularly

inventories, PPE, revenue earned by the firm in advance period along with payables (Reid

and Myddelton 2017). Also, there is adjustments regarding firm’s interests bearing liabilities,

diverse financial assets, varied provisions, varied other items along with previous period

differences. In essence, temporary differences is documented to be AUD 167 million in the

CORPORATE ACCOUNTING

evaluated whether numerals for income tax expenses are similar to that rate of tax times

overall earnings (Siew 2015).

Answer viii)

It can be hereby observed from the annual report of the firm Qantas Airways that the deferred

tax (assets/liabilities) stands at (AUD 353 million) in the year 2017 whereas the same is

recorded to be AUD 39 million. In essence, deferred tax is mainly recognized with regard to

temporary differences between carrying amounts of assets else wise liabilities for particularly

financial reporting cause and the overall amount used for the purpose of taxation (Miao et al.

2016). In particular, deferred tax assets are essentially recognized for particularly unused tax

losses; credit for necessarily tax together with temporary differences to the specific point that

it becomes plausible that taxable earning in the future period against which they can be used

(Miglani et al. 2015).

Answer ix)

Expenditure for income tax for period 2017 as documented in the financial statement of the

firm stands at (AUD 328 million) and income tax expenditure was observed to be (AUD 395

million) during the period 2016. Nonetheless, the figure for the firm’s income tax payable is

recorded to be (AUD 4 million). Essentially, this replicates a reconciliation of particularly

income tax expenditure of the corporation Qantas Airways to income tax payable. This

process of reconciliation includes adjustments for chiefly temporary differences. Essentially,

adjustments carried out for temporary differences take in adjustments for particularly

inventories, PPE, revenue earned by the firm in advance period along with payables (Reid

and Myddelton 2017). Also, there is adjustments regarding firm’s interests bearing liabilities,

diverse financial assets, varied provisions, varied other items along with previous period

differences. In essence, temporary differences is documented to be AUD 167 million in the

9

CORPORATE ACCOUNTING

period 2017 as compared to the previous period’s (AUD 18 million). Finally, after the

adjustments the tax payable is enumerated to be (AUD 4 million).

Answer x)

Critical evaluation of annual financial assertion of the firm Qantas Airways reflects that

income tax expenses presented in the income statement is not similar to that of payment of

income tax reflected in the declaration on flow of cash. In essence, disbursements for income

tax necessarily take in impact of income tax of particular losses otherwise gains related to

financing actions so that cash flow enumerated after tax is reflected in the sub totals of net

cash flow (Saeidi et al. 2015). Again, conversely, expenses of the firm on particularly

taxation are necessarily the particular amount that represents costs for tax.

Answer xi)

Founded on thorough analysis of annual report, it can be hereby identified that for the firm

Qantas Airways there is essentially a charge for current taxation on firm’s earnings. In

essence, this is primarily based on company’s adjusted profits that are primarily attributable

for any kind of disapproved otherwise non-assessable item. In addition to this, there also exist

notes for the financial declarations presented by the firm that help in comprehending

reconciliation of expenses on income tax to payable tax. Fundamentally, this sort of

reconciliation presents specific information to varied users as regards enumeration of this sort

of income tax expenses (Schaltegger and Burritt2017). Therefore, the most remarkable part in

relation to realisation of expenses of income tax is basically reconciliation of numerous

temporary differences and ny sort of net loss that is borne particularly after tax on firm’s

earnings.

CORPORATE ACCOUNTING

period 2017 as compared to the previous period’s (AUD 18 million). Finally, after the

adjustments the tax payable is enumerated to be (AUD 4 million).

Answer x)

Critical evaluation of annual financial assertion of the firm Qantas Airways reflects that

income tax expenses presented in the income statement is not similar to that of payment of

income tax reflected in the declaration on flow of cash. In essence, disbursements for income

tax necessarily take in impact of income tax of particular losses otherwise gains related to

financing actions so that cash flow enumerated after tax is reflected in the sub totals of net

cash flow (Saeidi et al. 2015). Again, conversely, expenses of the firm on particularly

taxation are necessarily the particular amount that represents costs for tax.

Answer xi)

Founded on thorough analysis of annual report, it can be hereby identified that for the firm

Qantas Airways there is essentially a charge for current taxation on firm’s earnings. In

essence, this is primarily based on company’s adjusted profits that are primarily attributable

for any kind of disapproved otherwise non-assessable item. In addition to this, there also exist

notes for the financial declarations presented by the firm that help in comprehending

reconciliation of expenses on income tax to payable tax. Fundamentally, this sort of

reconciliation presents specific information to varied users as regards enumeration of this sort

of income tax expenses (Schaltegger and Burritt2017). Therefore, the most remarkable part in

relation to realisation of expenses of income tax is basically reconciliation of numerous

temporary differences and ny sort of net loss that is borne particularly after tax on firm’s

earnings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

CORPORATE ACCOUNTING

References

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-515.

Miglani, S., Ahmed, K., and Henry, D. 2015. Voluntary corporate governance structure and

financial distress: evidence from Australia. Journal of Contemporary Accounting &

Economics, 11(1), 18-30.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., and Saaeidi, S. A. 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of

competitive advantage, reputation, and customer satisfaction. Journal of Business

Research, 68(2), 341-350.

Schaltegger, S., and Burritt, R. 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Siew, R.Y., 2015. A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

CORPORATE ACCOUNTING

References

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-515.

Miglani, S., Ahmed, K., and Henry, D. 2015. Voluntary corporate governance structure and

financial distress: evidence from Australia. Journal of Contemporary Accounting &

Economics, 11(1), 18-30.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., and Saaeidi, S. A. 2015. How does corporate

social responsibility contribute to firm financial performance? The mediating role of

competitive advantage, reputation, and customer satisfaction. Journal of Business

Research, 68(2), 341-350.

Schaltegger, S., and Burritt, R. 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Siew, R.Y., 2015. A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

CORPORATE ACCOUNTING

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

CORPORATE ACCOUNTING

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

12

CORPORATE ACCOUNTING

Appendix

CORPORATE ACCOUNTING

Appendix

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.