Financial Statement Analysis and Ratio Comparison Report

VerifiedAdded on 2020/01/28

|13

|3727

|273

Report

AI Summary

This report presents a detailed analysis of financial statements, encompassing the preparation of an adjusted trial balance, a statement of comprehensive income, and a balance sheet for Weather and Sons. It also includes working notes that elaborate on specific calculations, such as prepaid expenses, depreciation, and accruals. Furthermore, the report extends to financial ratio analysis, specifically focusing on comparing the performance of Ryanair and EasyJet. The analysis involves creating ratio tables for the years 2013, 2014, and 2015, providing insights into the financial health and operational efficiency of the selected companies. The report aims to provide a thorough understanding of financial statement preparation and the application of financial ratios in performance evaluation.

Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Question1.........................................................................................................................................3

a) Preparing adjusted trial balance...................................................................................................3

b) Preparation of the statement of comprehensive income.............................................................6

c.) Preparation of balance sheet.......................................................................................................7

TASK 2...............................................................................................................................................10

Question 2......................................................................................................................................10

Produce the 2013, 2014 and 2015 ratio tables for the Ryanair and Easy Jet and the comparison of

performance of the selected companies.........................................................................................10

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Question1.........................................................................................................................................3

a) Preparing adjusted trial balance...................................................................................................3

b) Preparation of the statement of comprehensive income.............................................................6

c.) Preparation of balance sheet.......................................................................................................7

TASK 2...............................................................................................................................................10

Question 2......................................................................................................................................10

Produce the 2013, 2014 and 2015 ratio tables for the Ryanair and Easy Jet and the comparison of

performance of the selected companies.........................................................................................10

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION

Accounting is the systematic and comprehensive recording of financial transaction related to

a business. It is a process of analysing, summarizing and reporting of transaction. It is regard as a

“Language of the business” which assists the companies to convey right and accurate financial

information to external parties in order to enhance brand image in front on the stakeholders

(Zimmerman and Yahya-Zadeh, 2011). All business and economical decision making are based on

financial statement which is the outcome of accounting information system. Without keeping a

proper account, the objective will not be achieved in the right manner. Accounting is a basic need of

a business organization to find out where the business stands in the market in terms of financial

aspect (Accounting- Need And Importance, 2016). It delivers a great essence of providing the basis

for planning and budgeting at the time of dealing and measuring economic activities and

communicating financial information to the users for decision making process.

TASK 1

Accounting can be categorized into different areas like financial, management, auditing,

taxation accounting etc. This division is based on several functions and related powers to these

various streams. Profession of accounting include private and public accounting categorize (Kaplan

and Atkinson, 2015). Private accounting is employed by an organization in order to keep record of

daily transactions. On the other hand, public accountants appoint by the government itself with the

aim of auditing. These types of accountants know with the name of external auditors and they are

protecting the interest of the shareholders. Public accountants need to follow all regulations and

rules of government in right way. For presenting the financial information of a business, a company

use different kinds of methods and format. The basic and common methods are income statements

and balance sheet (Horngren, Sundem, Schatzberg and Burgstahler, 2013). Along with this, trail

balance also used by the firms in order to deliver financial information to the shareholders.

Question1

a) Preparing adjusted trial balance

Trial balance is a list of closing balance of ledger accounts on a particular date. It can be

considered as a first stage of preparation of financial statements. Generally, it prepares at the end of

accounting period which assist in drafting of financial statement (What is a trial balance?, 2016).

With the help of this, it is easy for the organizations to ensure that every debit entry recorded

against a corresponding credit entry in the accounts book. During this process, a double entry

concept of accounting follows. It is important to resolve the differences in trial balance because

3

Accounting is the systematic and comprehensive recording of financial transaction related to

a business. It is a process of analysing, summarizing and reporting of transaction. It is regard as a

“Language of the business” which assists the companies to convey right and accurate financial

information to external parties in order to enhance brand image in front on the stakeholders

(Zimmerman and Yahya-Zadeh, 2011). All business and economical decision making are based on

financial statement which is the outcome of accounting information system. Without keeping a

proper account, the objective will not be achieved in the right manner. Accounting is a basic need of

a business organization to find out where the business stands in the market in terms of financial

aspect (Accounting- Need And Importance, 2016). It delivers a great essence of providing the basis

for planning and budgeting at the time of dealing and measuring economic activities and

communicating financial information to the users for decision making process.

TASK 1

Accounting can be categorized into different areas like financial, management, auditing,

taxation accounting etc. This division is based on several functions and related powers to these

various streams. Profession of accounting include private and public accounting categorize (Kaplan

and Atkinson, 2015). Private accounting is employed by an organization in order to keep record of

daily transactions. On the other hand, public accountants appoint by the government itself with the

aim of auditing. These types of accountants know with the name of external auditors and they are

protecting the interest of the shareholders. Public accountants need to follow all regulations and

rules of government in right way. For presenting the financial information of a business, a company

use different kinds of methods and format. The basic and common methods are income statements

and balance sheet (Horngren, Sundem, Schatzberg and Burgstahler, 2013). Along with this, trail

balance also used by the firms in order to deliver financial information to the shareholders.

Question1

a) Preparing adjusted trial balance

Trial balance is a list of closing balance of ledger accounts on a particular date. It can be

considered as a first stage of preparation of financial statements. Generally, it prepares at the end of

accounting period which assist in drafting of financial statement (What is a trial balance?, 2016).

With the help of this, it is easy for the organizations to ensure that every debit entry recorded

against a corresponding credit entry in the accounts book. During this process, a double entry

concept of accounting follows. It is important to resolve the differences in trial balance because

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

after preparing financial statement, rectification of differences or errors cannot be easy tasks. Trail

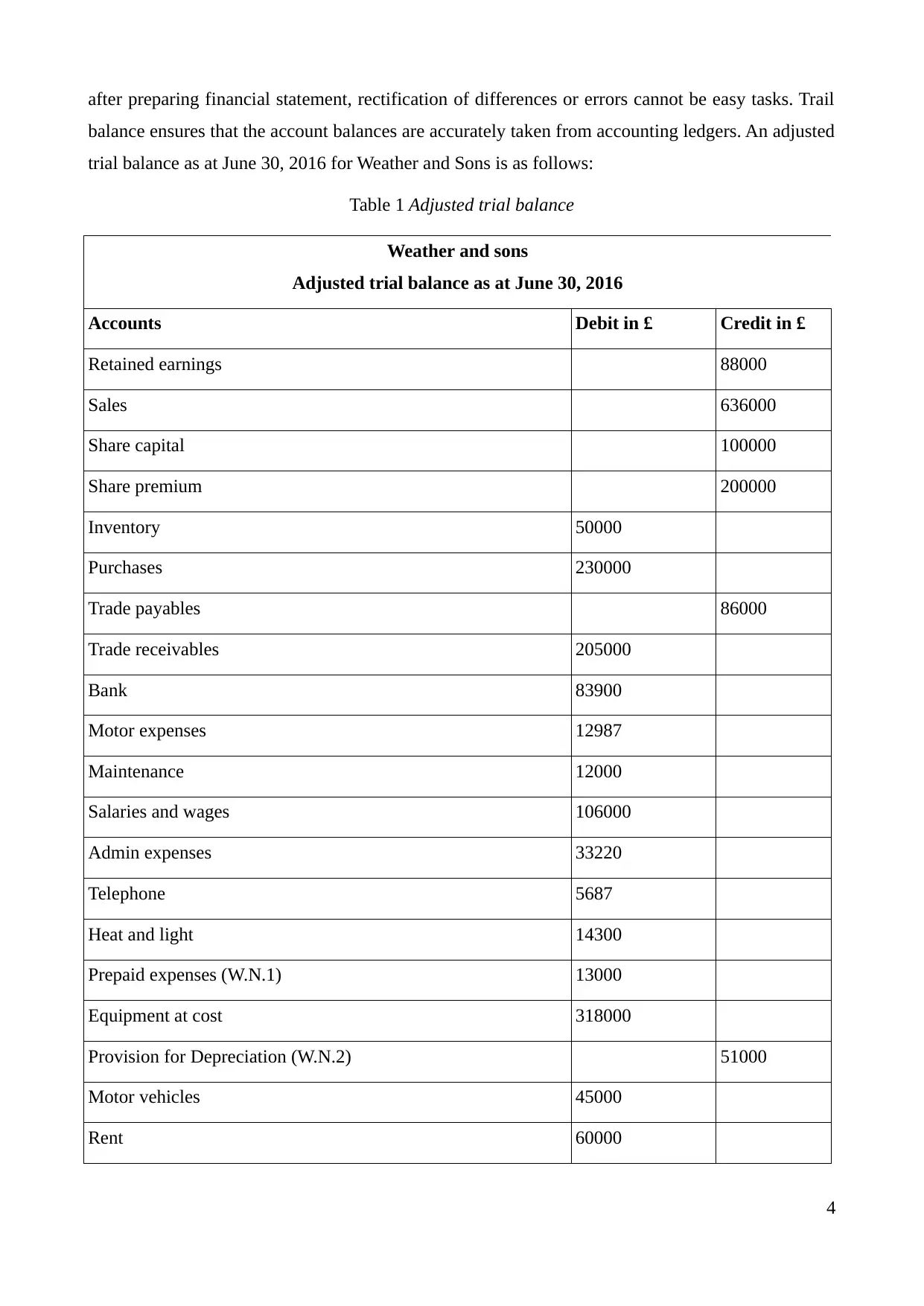

balance ensures that the account balances are accurately taken from accounting ledgers. An adjusted

trial balance as at June 30, 2016 for Weather and Sons is as follows:

Table 1 Adjusted trial balance

Weather and sons

Adjusted trial balance as at June 30, 2016

Accounts Debit in £ Credit in £

Retained earnings 88000

Sales 636000

Share capital 100000

Share premium 200000

Inventory 50000

Purchases 230000

Trade payables 86000

Trade receivables 205000

Bank 83900

Motor expenses 12987

Maintenance 12000

Salaries and wages 106000

Admin expenses 33220

Telephone 5687

Heat and light 14300

Prepaid expenses (W.N.1) 13000

Equipment at cost 318000

Provision for Depreciation (W.N.2) 51000

Motor vehicles 45000

Rent 60000

4

balance ensures that the account balances are accurately taken from accounting ledgers. An adjusted

trial balance as at June 30, 2016 for Weather and Sons is as follows:

Table 1 Adjusted trial balance

Weather and sons

Adjusted trial balance as at June 30, 2016

Accounts Debit in £ Credit in £

Retained earnings 88000

Sales 636000

Share capital 100000

Share premium 200000

Inventory 50000

Purchases 230000

Trade payables 86000

Trade receivables 205000

Bank 83900

Motor expenses 12987

Maintenance 12000

Salaries and wages 106000

Admin expenses 33220

Telephone 5687

Heat and light 14300

Prepaid expenses (W.N.1) 13000

Equipment at cost 318000

Provision for Depreciation (W.N.2) 51000

Motor vehicles 45000

Rent 60000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

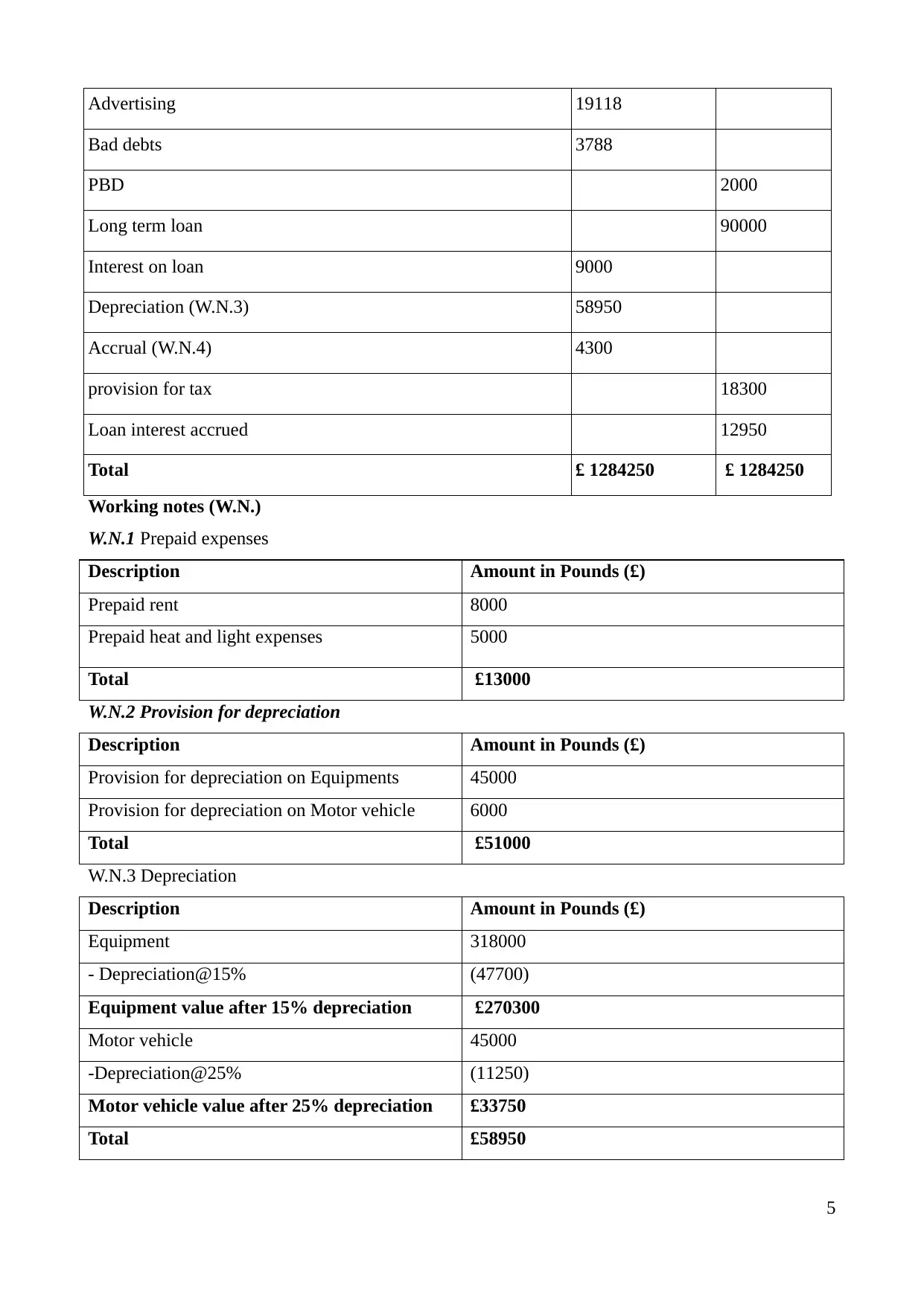

Advertising 19118

Bad debts 3788

PBD 2000

Long term loan 90000

Interest on loan 9000

Depreciation (W.N.3) 58950

Accrual (W.N.4) 4300

provision for tax 18300

Loan interest accrued 12950

Total £ 1284250 £ 1284250

Working notes (W.N.)

W.N.1 Prepaid expenses

Description Amount in Pounds (£)

Prepaid rent 8000

Prepaid heat and light expenses 5000

Total £13000

W.N.2 Provision for depreciation

Description Amount in Pounds (£)

Provision for depreciation on Equipments 45000

Provision for depreciation on Motor vehicle 6000

Total £51000

W.N.3 Depreciation

Description Amount in Pounds (£)

Equipment 318000

- Depreciation@15% (47700)

Equipment value after 15% depreciation £270300

Motor vehicle 45000

-Depreciation@25% (11250)

Motor vehicle value after 25% depreciation £33750

Total £58950

5

Bad debts 3788

PBD 2000

Long term loan 90000

Interest on loan 9000

Depreciation (W.N.3) 58950

Accrual (W.N.4) 4300

provision for tax 18300

Loan interest accrued 12950

Total £ 1284250 £ 1284250

Working notes (W.N.)

W.N.1 Prepaid expenses

Description Amount in Pounds (£)

Prepaid rent 8000

Prepaid heat and light expenses 5000

Total £13000

W.N.2 Provision for depreciation

Description Amount in Pounds (£)

Provision for depreciation on Equipments 45000

Provision for depreciation on Motor vehicle 6000

Total £51000

W.N.3 Depreciation

Description Amount in Pounds (£)

Equipment 318000

- Depreciation@15% (47700)

Equipment value after 15% depreciation £270300

Motor vehicle 45000

-Depreciation@25% (11250)

Motor vehicle value after 25% depreciation £33750

Total £58950

5

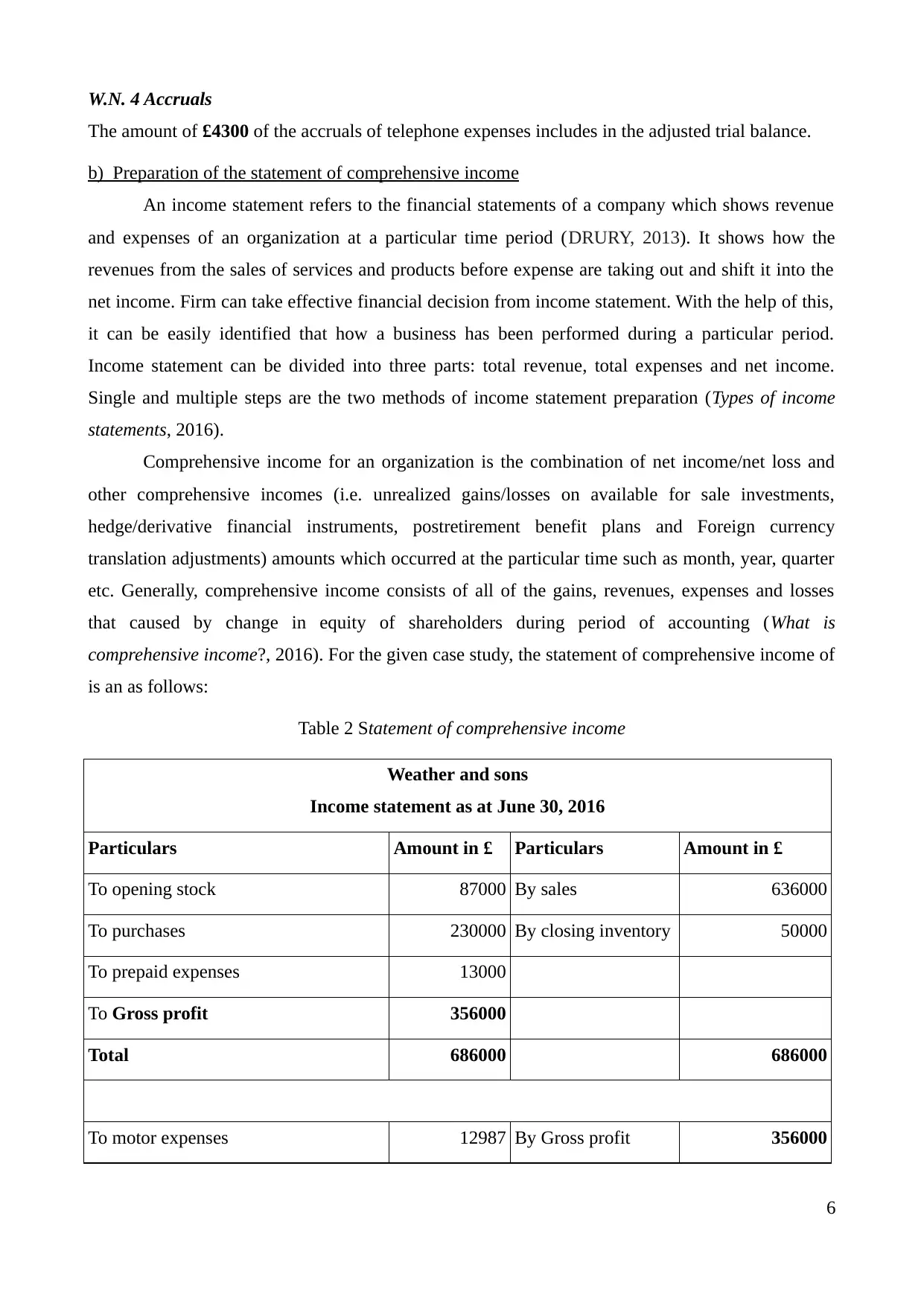

W.N. 4 Accruals

The amount of £4300 of the accruals of telephone expenses includes in the adjusted trial balance.

b) Preparation of the statement of comprehensive income

An income statement refers to the financial statements of a company which shows revenue

and expenses of an organization at a particular time period (DRURY, 2013). It shows how the

revenues from the sales of services and products before expense are taking out and shift it into the

net income. Firm can take effective financial decision from income statement. With the help of this,

it can be easily identified that how a business has been performed during a particular period.

Income statement can be divided into three parts: total revenue, total expenses and net income.

Single and multiple steps are the two methods of income statement preparation (Types of income

statements, 2016).

Comprehensive income for an organization is the combination of net income/net loss and

other comprehensive incomes (i.e. unrealized gains/losses on available for sale investments,

hedge/derivative financial instruments, postretirement benefit plans and Foreign currency

translation adjustments) amounts which occurred at the particular time such as month, year, quarter

etc. Generally, comprehensive income consists of all of the gains, revenues, expenses and losses

that caused by change in equity of shareholders during period of accounting (What is

comprehensive income?, 2016). For the given case study, the statement of comprehensive income of

is an as follows:

Table 2 Statement of comprehensive income

Weather and sons

Income statement as at June 30, 2016

Particulars Amount in £ Particulars Amount in £

To opening stock 87000 By sales 636000

To purchases 230000 By closing inventory 50000

To prepaid expenses 13000

To Gross profit 356000

Total 686000 686000

To motor expenses 12987 By Gross profit 356000

6

The amount of £4300 of the accruals of telephone expenses includes in the adjusted trial balance.

b) Preparation of the statement of comprehensive income

An income statement refers to the financial statements of a company which shows revenue

and expenses of an organization at a particular time period (DRURY, 2013). It shows how the

revenues from the sales of services and products before expense are taking out and shift it into the

net income. Firm can take effective financial decision from income statement. With the help of this,

it can be easily identified that how a business has been performed during a particular period.

Income statement can be divided into three parts: total revenue, total expenses and net income.

Single and multiple steps are the two methods of income statement preparation (Types of income

statements, 2016).

Comprehensive income for an organization is the combination of net income/net loss and

other comprehensive incomes (i.e. unrealized gains/losses on available for sale investments,

hedge/derivative financial instruments, postretirement benefit plans and Foreign currency

translation adjustments) amounts which occurred at the particular time such as month, year, quarter

etc. Generally, comprehensive income consists of all of the gains, revenues, expenses and losses

that caused by change in equity of shareholders during period of accounting (What is

comprehensive income?, 2016). For the given case study, the statement of comprehensive income of

is an as follows:

Table 2 Statement of comprehensive income

Weather and sons

Income statement as at June 30, 2016

Particulars Amount in £ Particulars Amount in £

To opening stock 87000 By sales 636000

To purchases 230000 By closing inventory 50000

To prepaid expenses 13000

To Gross profit 356000

Total 686000 686000

To motor expenses 12987 By Gross profit 356000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

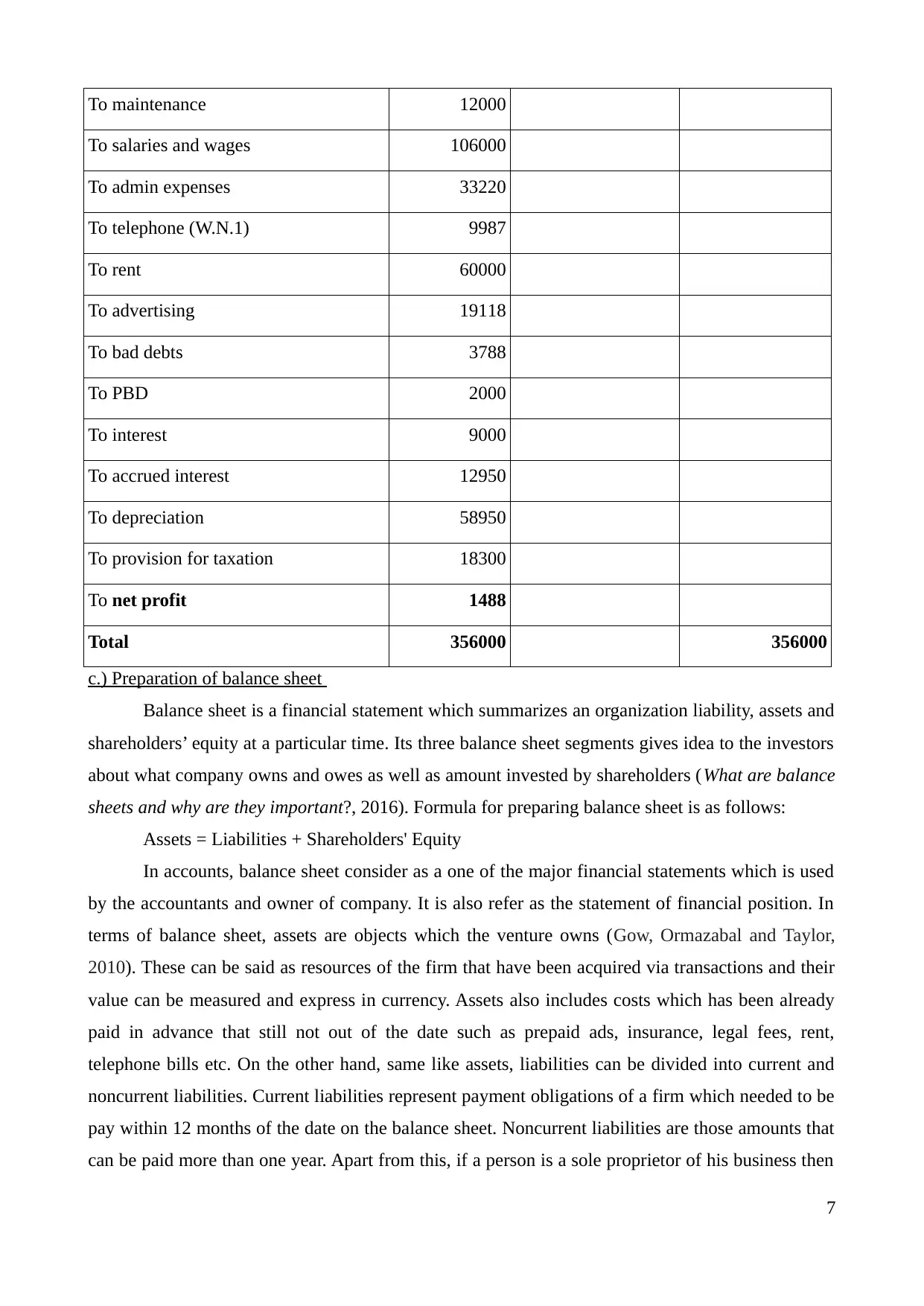

To maintenance 12000

To salaries and wages 106000

To admin expenses 33220

To telephone (W.N.1) 9987

To rent 60000

To advertising 19118

To bad debts 3788

To PBD 2000

To interest 9000

To accrued interest 12950

To depreciation 58950

To provision for taxation 18300

To net profit 1488

Total 356000 356000

c.) Preparation of balance sheet

Balance sheet is a financial statement which summarizes an organization liability, assets and

shareholders’ equity at a particular time. Its three balance sheet segments gives idea to the investors

about what company owns and owes as well as amount invested by shareholders (What are balance

sheets and why are they important?, 2016). Formula for preparing balance sheet is as follows:

Assets = Liabilities + Shareholders' Equity

In accounts, balance sheet consider as a one of the major financial statements which is used

by the accountants and owner of company. It is also refer as the statement of financial position. In

terms of balance sheet, assets are objects which the venture owns (Gow, Ormazabal and Taylor,

2010). These can be said as resources of the firm that have been acquired via transactions and their

value can be measured and express in currency. Assets also includes costs which has been already

paid in advance that still not out of the date such as prepaid ads, insurance, legal fees, rent,

telephone bills etc. On the other hand, same like assets, liabilities can be divided into current and

noncurrent liabilities. Current liabilities represent payment obligations of a firm which needed to be

pay within 12 months of the date on the balance sheet. Noncurrent liabilities are those amounts that

can be paid more than one year. Apart from this, if a person is a sole proprietor of his business then

7

To salaries and wages 106000

To admin expenses 33220

To telephone (W.N.1) 9987

To rent 60000

To advertising 19118

To bad debts 3788

To PBD 2000

To interest 9000

To accrued interest 12950

To depreciation 58950

To provision for taxation 18300

To net profit 1488

Total 356000 356000

c.) Preparation of balance sheet

Balance sheet is a financial statement which summarizes an organization liability, assets and

shareholders’ equity at a particular time. Its three balance sheet segments gives idea to the investors

about what company owns and owes as well as amount invested by shareholders (What are balance

sheets and why are they important?, 2016). Formula for preparing balance sheet is as follows:

Assets = Liabilities + Shareholders' Equity

In accounts, balance sheet consider as a one of the major financial statements which is used

by the accountants and owner of company. It is also refer as the statement of financial position. In

terms of balance sheet, assets are objects which the venture owns (Gow, Ormazabal and Taylor,

2010). These can be said as resources of the firm that have been acquired via transactions and their

value can be measured and express in currency. Assets also includes costs which has been already

paid in advance that still not out of the date such as prepaid ads, insurance, legal fees, rent,

telephone bills etc. On the other hand, same like assets, liabilities can be divided into current and

noncurrent liabilities. Current liabilities represent payment obligations of a firm which needed to be

pay within 12 months of the date on the balance sheet. Noncurrent liabilities are those amounts that

can be paid more than one year. Apart from this, if a person is a sole proprietor of his business then

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

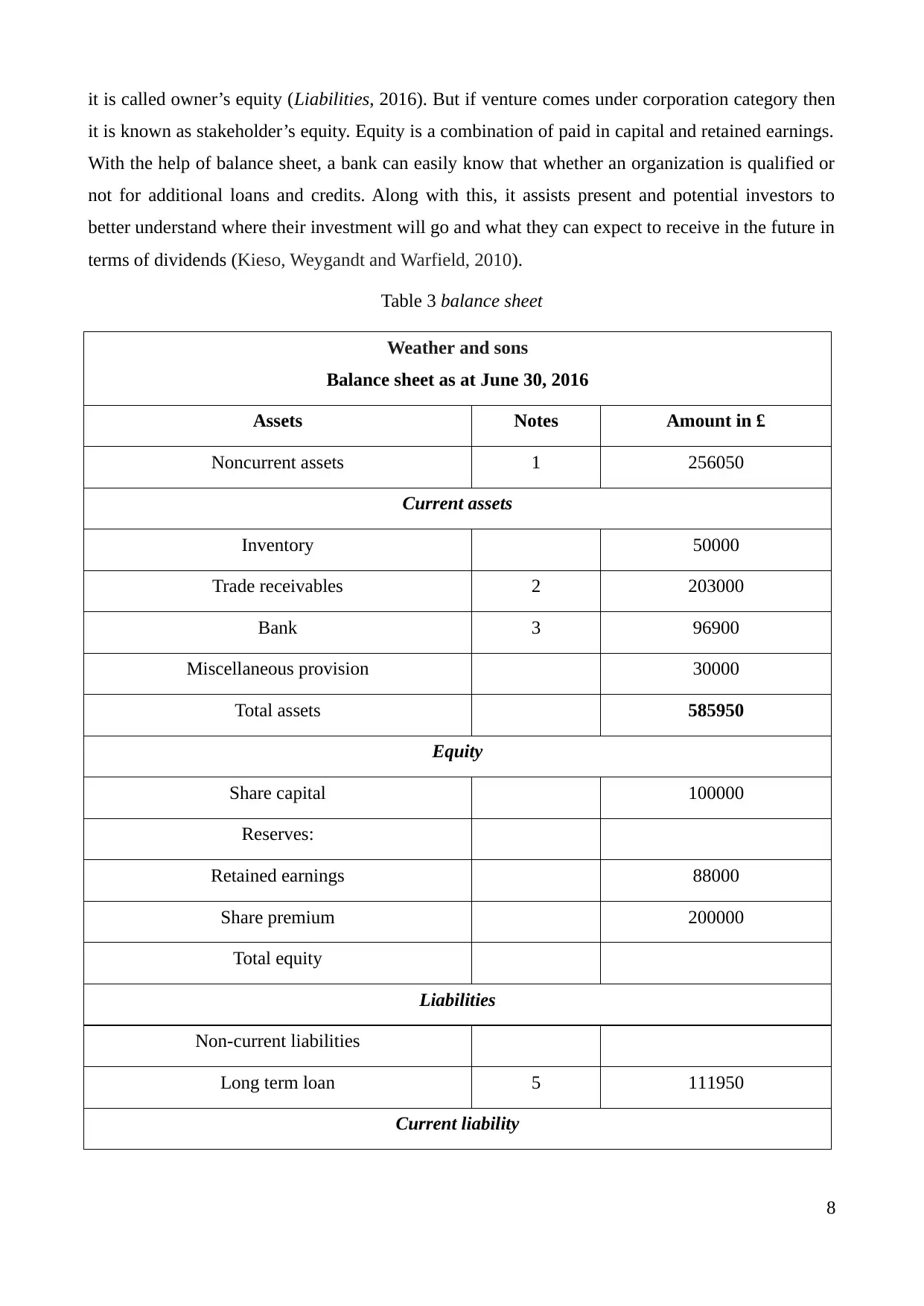

it is called owner’s equity (Liabilities, 2016). But if venture comes under corporation category then

it is known as stakeholder’s equity. Equity is a combination of paid in capital and retained earnings.

With the help of balance sheet, a bank can easily know that whether an organization is qualified or

not for additional loans and credits. Along with this, it assists present and potential investors to

better understand where their investment will go and what they can expect to receive in the future in

terms of dividends (Kieso, Weygandt and Warfield, 2010).

Table 3 balance sheet

Weather and sons

Balance sheet as at June 30, 2016

Assets Notes Amount in £

Noncurrent assets 1 256050

Current assets

Inventory 50000

Trade receivables 2 203000

Bank 3 96900

Miscellaneous provision 30000

Total assets 585950

Equity

Share capital 100000

Reserves:

Retained earnings 88000

Share premium 200000

Total equity

Liabilities

Non-current liabilities

Long term loan 5 111950

Current liability

8

it is known as stakeholder’s equity. Equity is a combination of paid in capital and retained earnings.

With the help of balance sheet, a bank can easily know that whether an organization is qualified or

not for additional loans and credits. Along with this, it assists present and potential investors to

better understand where their investment will go and what they can expect to receive in the future in

terms of dividends (Kieso, Weygandt and Warfield, 2010).

Table 3 balance sheet

Weather and sons

Balance sheet as at June 30, 2016

Assets Notes Amount in £

Noncurrent assets 1 256050

Current assets

Inventory 50000

Trade receivables 2 203000

Bank 3 96900

Miscellaneous provision 30000

Total assets 585950

Equity

Share capital 100000

Reserves:

Retained earnings 88000

Share premium 200000

Total equity

Liabilities

Non-current liabilities

Long term loan 5 111950

Current liability

8

Trade payables 86000

Total equity and liability 585950

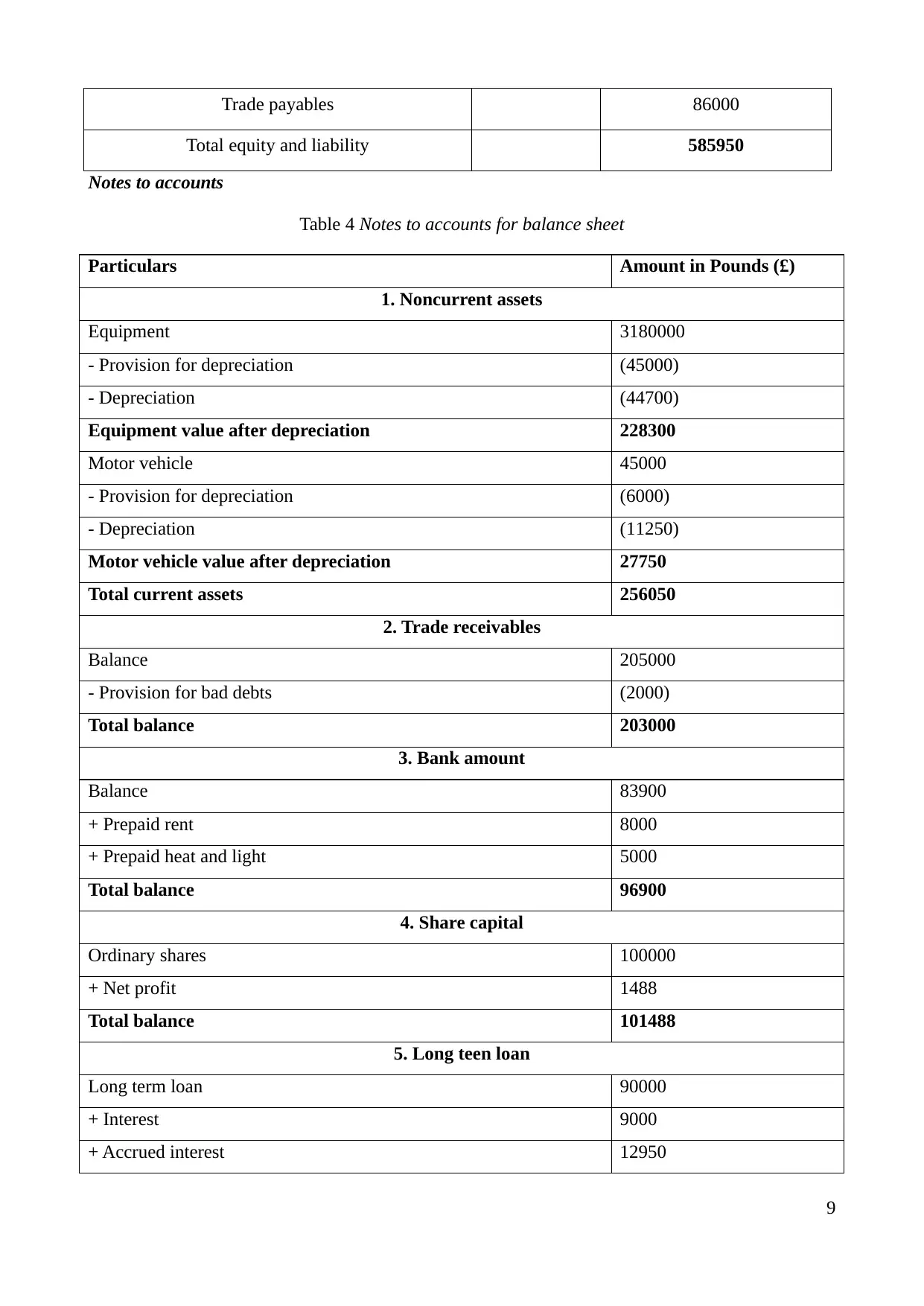

Notes to accounts

Table 4 Notes to accounts for balance sheet

Particulars Amount in Pounds (£)

1. Noncurrent assets

Equipment 3180000

- Provision for depreciation (45000)

- Depreciation (44700)

Equipment value after depreciation 228300

Motor vehicle 45000

- Provision for depreciation (6000)

- Depreciation (11250)

Motor vehicle value after depreciation 27750

Total current assets 256050

2. Trade receivables

Balance 205000

- Provision for bad debts (2000)

Total balance 203000

3. Bank amount

Balance 83900

+ Prepaid rent 8000

+ Prepaid heat and light 5000

Total balance 96900

4. Share capital

Ordinary shares 100000

+ Net profit 1488

Total balance 101488

5. Long teen loan

Long term loan 90000

+ Interest 9000

+ Accrued interest 12950

9

Total equity and liability 585950

Notes to accounts

Table 4 Notes to accounts for balance sheet

Particulars Amount in Pounds (£)

1. Noncurrent assets

Equipment 3180000

- Provision for depreciation (45000)

- Depreciation (44700)

Equipment value after depreciation 228300

Motor vehicle 45000

- Provision for depreciation (6000)

- Depreciation (11250)

Motor vehicle value after depreciation 27750

Total current assets 256050

2. Trade receivables

Balance 205000

- Provision for bad debts (2000)

Total balance 203000

3. Bank amount

Balance 83900

+ Prepaid rent 8000

+ Prepaid heat and light 5000

Total balance 96900

4. Share capital

Ordinary shares 100000

+ Net profit 1488

Total balance 101488

5. Long teen loan

Long term loan 90000

+ Interest 9000

+ Accrued interest 12950

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total balance 111950

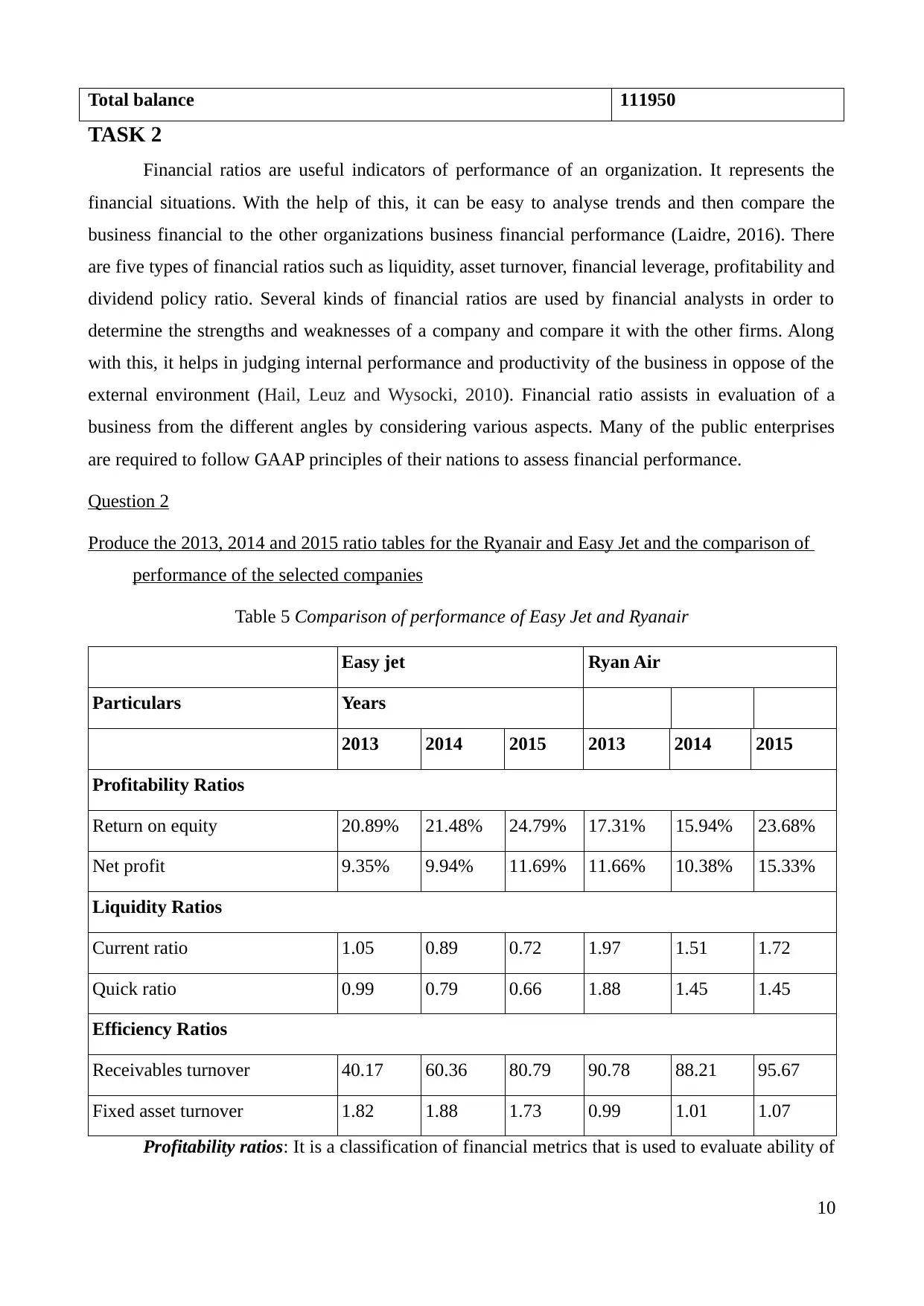

TASK 2

Financial ratios are useful indicators of performance of an organization. It represents the

financial situations. With the help of this, it can be easy to analyse trends and then compare the

business financial to the other organizations business financial performance (Laidre, 2016). There

are five types of financial ratios such as liquidity, asset turnover, financial leverage, profitability and

dividend policy ratio. Several kinds of financial ratios are used by financial analysts in order to

determine the strengths and weaknesses of a company and compare it with the other firms. Along

with this, it helps in judging internal performance and productivity of the business in oppose of the

external environment (Hail, Leuz and Wysocki, 2010). Financial ratio assists in evaluation of a

business from the different angles by considering various aspects. Many of the public enterprises

are required to follow GAAP principles of their nations to assess financial performance.

Question 2

Produce the 2013, 2014 and 2015 ratio tables for the Ryanair and Easy Jet and the comparison of

performance of the selected companies

Table 5 Comparison of performance of Easy Jet and Ryanair

Easy jet Ryan Air

Particulars Years

2013 2014 2015 2013 2014 2015

Profitability Ratios

Return on equity 20.89% 21.48% 24.79% 17.31% 15.94% 23.68%

Net profit 9.35% 9.94% 11.69% 11.66% 10.38% 15.33%

Liquidity Ratios

Current ratio 1.05 0.89 0.72 1.97 1.51 1.72

Quick ratio 0.99 0.79 0.66 1.88 1.45 1.45

Efficiency Ratios

Receivables turnover 40.17 60.36 80.79 90.78 88.21 95.67

Fixed asset turnover 1.82 1.88 1.73 0.99 1.01 1.07

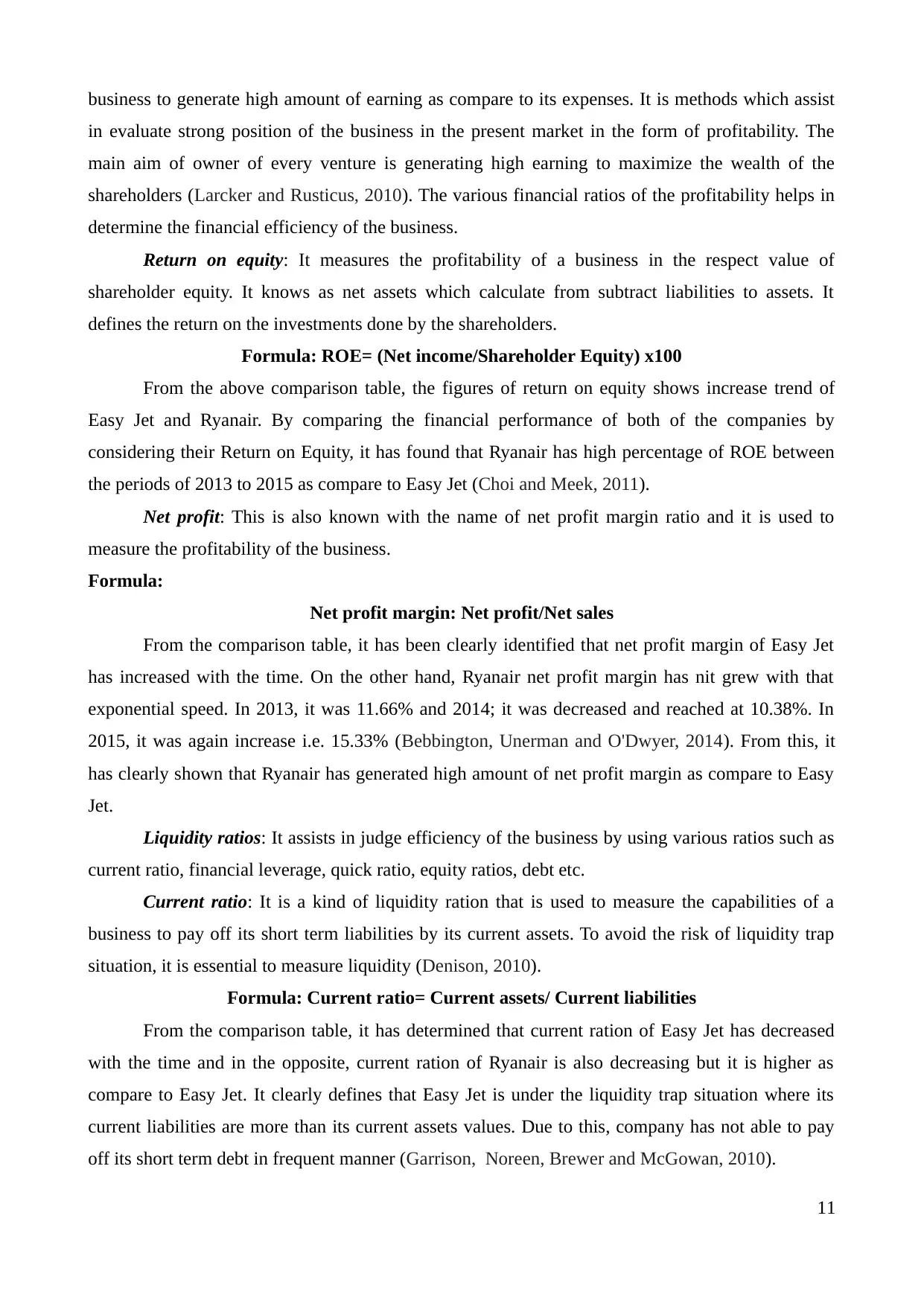

Profitability ratios: It is a classification of financial metrics that is used to evaluate ability of

10

TASK 2

Financial ratios are useful indicators of performance of an organization. It represents the

financial situations. With the help of this, it can be easy to analyse trends and then compare the

business financial to the other organizations business financial performance (Laidre, 2016). There

are five types of financial ratios such as liquidity, asset turnover, financial leverage, profitability and

dividend policy ratio. Several kinds of financial ratios are used by financial analysts in order to

determine the strengths and weaknesses of a company and compare it with the other firms. Along

with this, it helps in judging internal performance and productivity of the business in oppose of the

external environment (Hail, Leuz and Wysocki, 2010). Financial ratio assists in evaluation of a

business from the different angles by considering various aspects. Many of the public enterprises

are required to follow GAAP principles of their nations to assess financial performance.

Question 2

Produce the 2013, 2014 and 2015 ratio tables for the Ryanair and Easy Jet and the comparison of

performance of the selected companies

Table 5 Comparison of performance of Easy Jet and Ryanair

Easy jet Ryan Air

Particulars Years

2013 2014 2015 2013 2014 2015

Profitability Ratios

Return on equity 20.89% 21.48% 24.79% 17.31% 15.94% 23.68%

Net profit 9.35% 9.94% 11.69% 11.66% 10.38% 15.33%

Liquidity Ratios

Current ratio 1.05 0.89 0.72 1.97 1.51 1.72

Quick ratio 0.99 0.79 0.66 1.88 1.45 1.45

Efficiency Ratios

Receivables turnover 40.17 60.36 80.79 90.78 88.21 95.67

Fixed asset turnover 1.82 1.88 1.73 0.99 1.01 1.07

Profitability ratios: It is a classification of financial metrics that is used to evaluate ability of

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business to generate high amount of earning as compare to its expenses. It is methods which assist

in evaluate strong position of the business in the present market in the form of profitability. The

main aim of owner of every venture is generating high earning to maximize the wealth of the

shareholders (Larcker and Rusticus, 2010). The various financial ratios of the profitability helps in

determine the financial efficiency of the business.

Return on equity: It measures the profitability of a business in the respect value of

shareholder equity. It knows as net assets which calculate from subtract liabilities to assets. It

defines the return on the investments done by the shareholders.

Formula: ROE= (Net income/Shareholder Equity) x100

From the above comparison table, the figures of return on equity shows increase trend of

Easy Jet and Ryanair. By comparing the financial performance of both of the companies by

considering their Return on Equity, it has found that Ryanair has high percentage of ROE between

the periods of 2013 to 2015 as compare to Easy Jet (Choi and Meek, 2011).

Net profit: This is also known with the name of net profit margin ratio and it is used to

measure the profitability of the business.

Formula:

Net profit margin: Net profit/Net sales

From the comparison table, it has been clearly identified that net profit margin of Easy Jet

has increased with the time. On the other hand, Ryanair net profit margin has nit grew with that

exponential speed. In 2013, it was 11.66% and 2014; it was decreased and reached at 10.38%. In

2015, it was again increase i.e. 15.33% (Bebbington, Unerman and O'Dwyer, 2014). From this, it

has clearly shown that Ryanair has generated high amount of net profit margin as compare to Easy

Jet.

Liquidity ratios: It assists in judge efficiency of the business by using various ratios such as

current ratio, financial leverage, quick ratio, equity ratios, debt etc.

Current ratio: It is a kind of liquidity ration that is used to measure the capabilities of a

business to pay off its short term liabilities by its current assets. To avoid the risk of liquidity trap

situation, it is essential to measure liquidity (Denison, 2010).

Formula: Current ratio= Current assets/ Current liabilities

From the comparison table, it has determined that current ration of Easy Jet has decreased

with the time and in the opposite, current ration of Ryanair is also decreasing but it is higher as

compare to Easy Jet. It clearly defines that Easy Jet is under the liquidity trap situation where its

current liabilities are more than its current assets values. Due to this, company has not able to pay

off its short term debt in frequent manner (Garrison, Noreen, Brewer and McGowan, 2010).

11

in evaluate strong position of the business in the present market in the form of profitability. The

main aim of owner of every venture is generating high earning to maximize the wealth of the

shareholders (Larcker and Rusticus, 2010). The various financial ratios of the profitability helps in

determine the financial efficiency of the business.

Return on equity: It measures the profitability of a business in the respect value of

shareholder equity. It knows as net assets which calculate from subtract liabilities to assets. It

defines the return on the investments done by the shareholders.

Formula: ROE= (Net income/Shareholder Equity) x100

From the above comparison table, the figures of return on equity shows increase trend of

Easy Jet and Ryanair. By comparing the financial performance of both of the companies by

considering their Return on Equity, it has found that Ryanair has high percentage of ROE between

the periods of 2013 to 2015 as compare to Easy Jet (Choi and Meek, 2011).

Net profit: This is also known with the name of net profit margin ratio and it is used to

measure the profitability of the business.

Formula:

Net profit margin: Net profit/Net sales

From the comparison table, it has been clearly identified that net profit margin of Easy Jet

has increased with the time. On the other hand, Ryanair net profit margin has nit grew with that

exponential speed. In 2013, it was 11.66% and 2014; it was decreased and reached at 10.38%. In

2015, it was again increase i.e. 15.33% (Bebbington, Unerman and O'Dwyer, 2014). From this, it

has clearly shown that Ryanair has generated high amount of net profit margin as compare to Easy

Jet.

Liquidity ratios: It assists in judge efficiency of the business by using various ratios such as

current ratio, financial leverage, quick ratio, equity ratios, debt etc.

Current ratio: It is a kind of liquidity ration that is used to measure the capabilities of a

business to pay off its short term liabilities by its current assets. To avoid the risk of liquidity trap

situation, it is essential to measure liquidity (Denison, 2010).

Formula: Current ratio= Current assets/ Current liabilities

From the comparison table, it has determined that current ration of Easy Jet has decreased

with the time and in the opposite, current ration of Ryanair is also decreasing but it is higher as

compare to Easy Jet. It clearly defines that Easy Jet is under the liquidity trap situation where its

current liabilities are more than its current assets values. Due to this, company has not able to pay

off its short term debt in frequent manner (Garrison, Noreen, Brewer and McGowan, 2010).

11

Quick ratio: It is common and most important method to measure financial performance of

a company. Under this, total amount of cash + marketable securities+ accounts receivables to the

amount of current liabilities compares.

Formula: Quick ratio= Cash and cash equivalents+ Marketable securities+ Accounts

receivables Current liabilities

From the comparison table of two organization, it has been explored that quick ratio of Easy

Jet and Ryanair decreases. This reflects the shortage of the company to pay off its short term

liabilities (Lennox, Francis and Wang, 2011).

Efficiency ratios: The aim of this method to analyse the future efficiency of a business in

various aspects. It includes various ratios such as trade receivables, fixed asset turnover, inventory

turnover and asset turnover.

Receivables turnover: The receivable turnover of the Easy jet company reflects that there is

a strong capability of the firm to control over recovery of the payments from the debtors. This trend

increases every year by 20%. But in the case Ryanair, this trend has increased or decreased with the

time.

Fixed asset turnover: The following trend of the Easy Jet has decreased and in the opposite,

Ryanair trend has increased with the time (Zimmerman and Yahya-Zadeh, 2011).

CONCLUSION

From the above study it has been concluded that the accounting has played an important role

in every organization. It has used to keep the records of all kind of transactions in right format.

There have various methods and techniques have available by which a performance of a company

can be evaluated by considering many aspects.

12

a company. Under this, total amount of cash + marketable securities+ accounts receivables to the

amount of current liabilities compares.

Formula: Quick ratio= Cash and cash equivalents+ Marketable securities+ Accounts

receivables Current liabilities

From the comparison table of two organization, it has been explored that quick ratio of Easy

Jet and Ryanair decreases. This reflects the shortage of the company to pay off its short term

liabilities (Lennox, Francis and Wang, 2011).

Efficiency ratios: The aim of this method to analyse the future efficiency of a business in

various aspects. It includes various ratios such as trade receivables, fixed asset turnover, inventory

turnover and asset turnover.

Receivables turnover: The receivable turnover of the Easy jet company reflects that there is

a strong capability of the firm to control over recovery of the payments from the debtors. This trend

increases every year by 20%. But in the case Ryanair, this trend has increased or decreased with the

time.

Fixed asset turnover: The following trend of the Easy Jet has decreased and in the opposite,

Ryanair trend has increased with the time (Zimmerman and Yahya-Zadeh, 2011).

CONCLUSION

From the above study it has been concluded that the accounting has played an important role

in every organization. It has used to keep the records of all kind of transactions in right format.

There have various methods and techniques have available by which a performance of a company

can be evaluated by considering many aspects.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.