Financial Analysis and Acquisition Recommendation: Deepwater Ltd

VerifiedAdded on 2020/06/03

|14

|2914

|173

Report

AI Summary

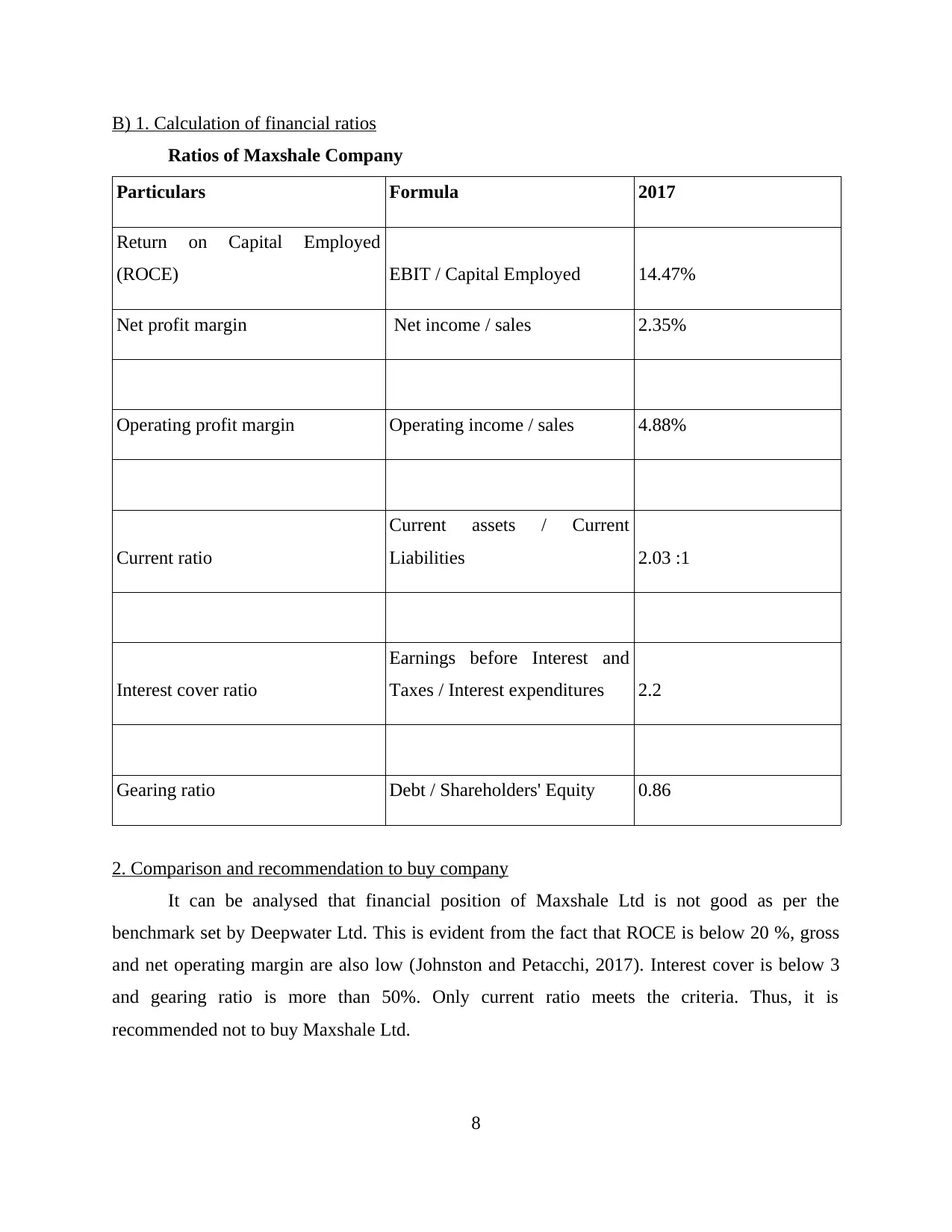

This report provides a comprehensive financial analysis of Deepwater Ltd, focusing on its performance and the potential acquisition of Maxshale Ltd. It begins with an executive summary highlighting the importance of financial statement analysis for making informed decisions, followed by an introduction outlining the context of the acquisition. The report is divided into five parts, covering topics such as transaction descriptions, tangible and intangible assets, trend analysis of revenue and profits, application of financial techniques, financial performance indicators, and calculation of financial ratios. The analysis includes computations of gross profit margin, trend analysis, and the impact of changes in operating costs on profitability. The report also examines cash flow statements, working capital improvements, and the specific components that have improved Deepwater Ltd's cash position. Finally, it includes a comparison of Maxshale Ltd's financial position and a recommendation regarding the acquisition, concluding that it is not recommended to buy Maxshale Ltd. The report uses various financial techniques and ratios to assess the financial health of the company and provides insights for making informed investment decisions. The report emphasizes the importance of financial analysis in the context of business acquisitions and strategic planning.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.