Accounting Report: Financial Statement Analysis of Hydan Co. 2017

VerifiedAdded on 2022/08/12

|15

|501

|18

Report

AI Summary

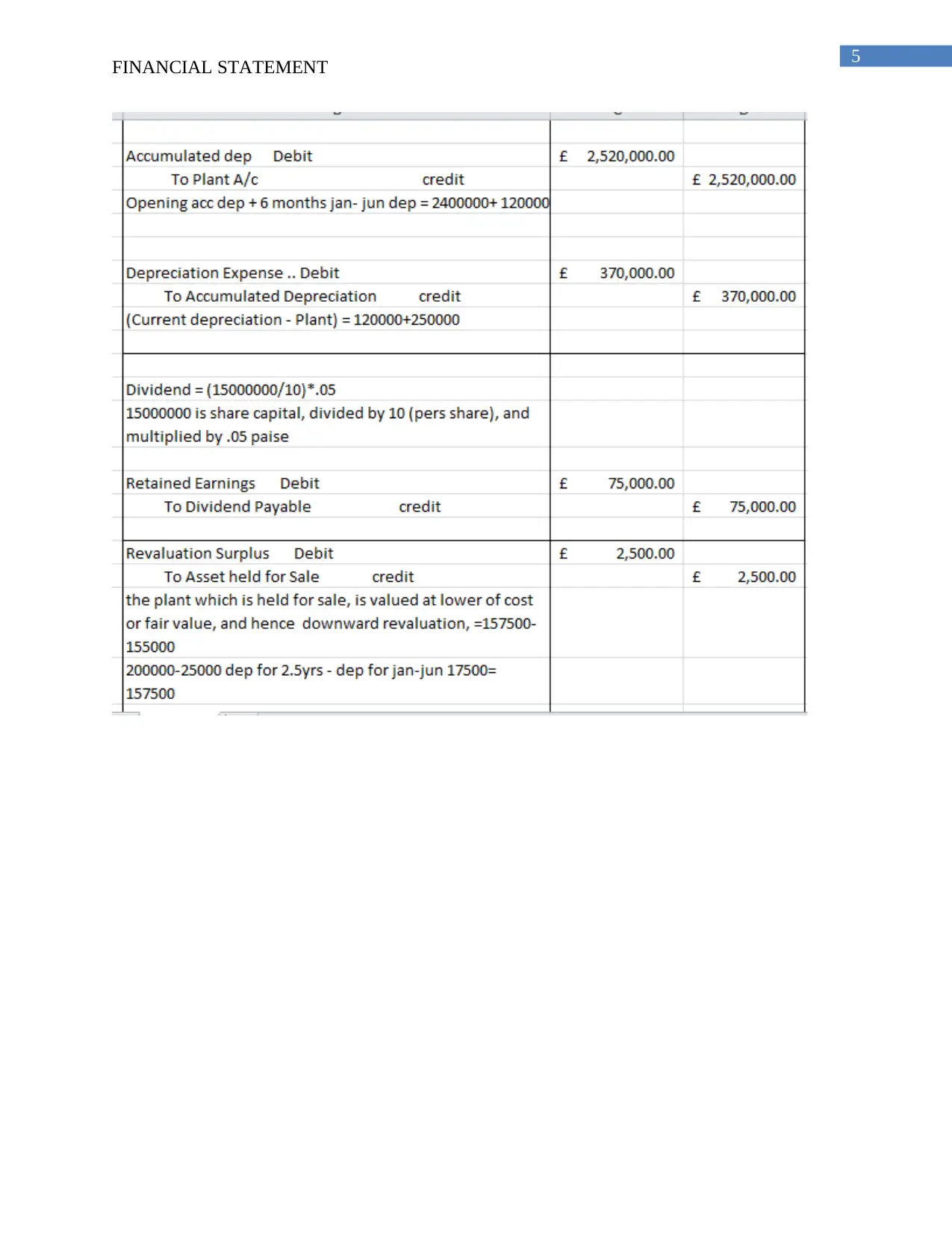

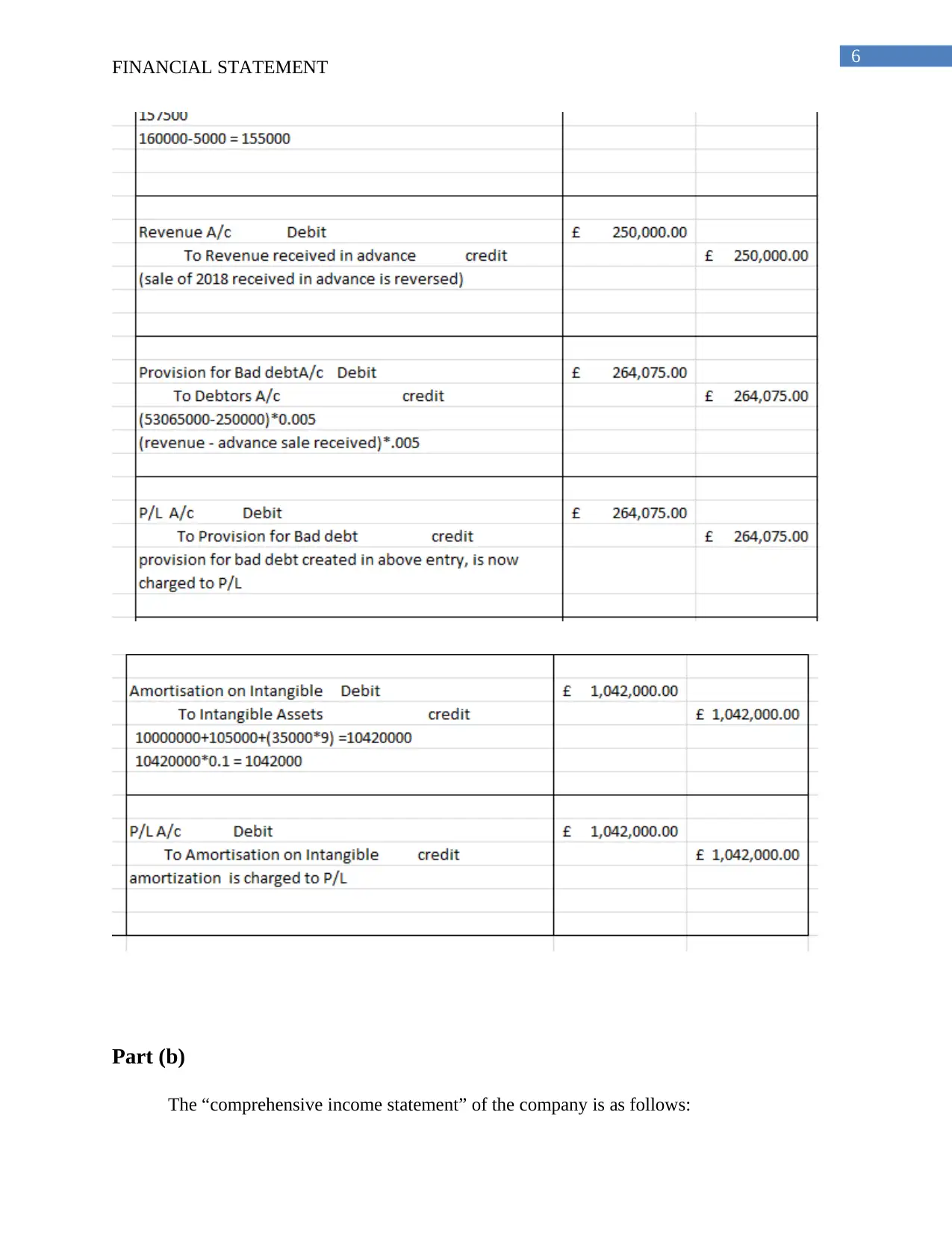

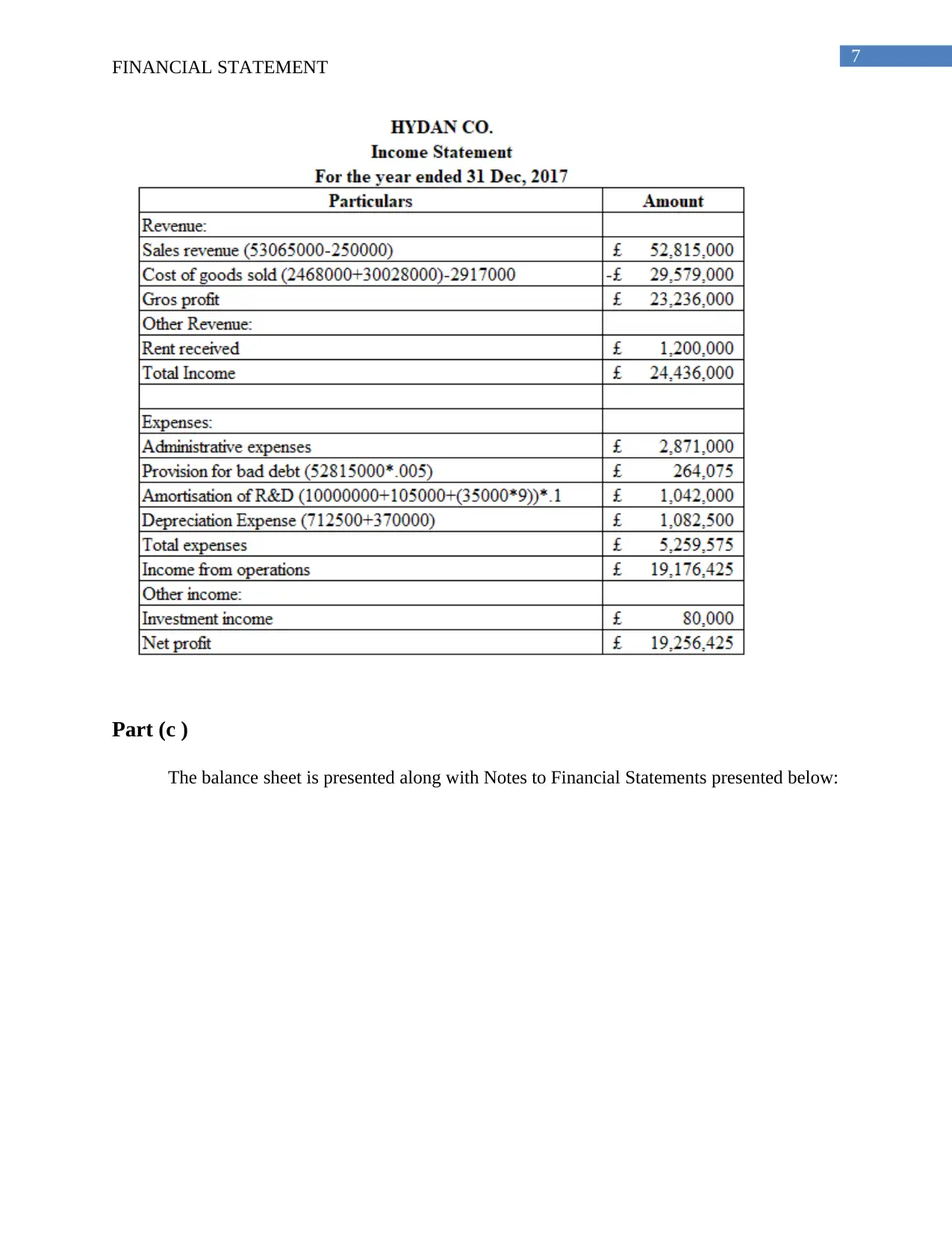

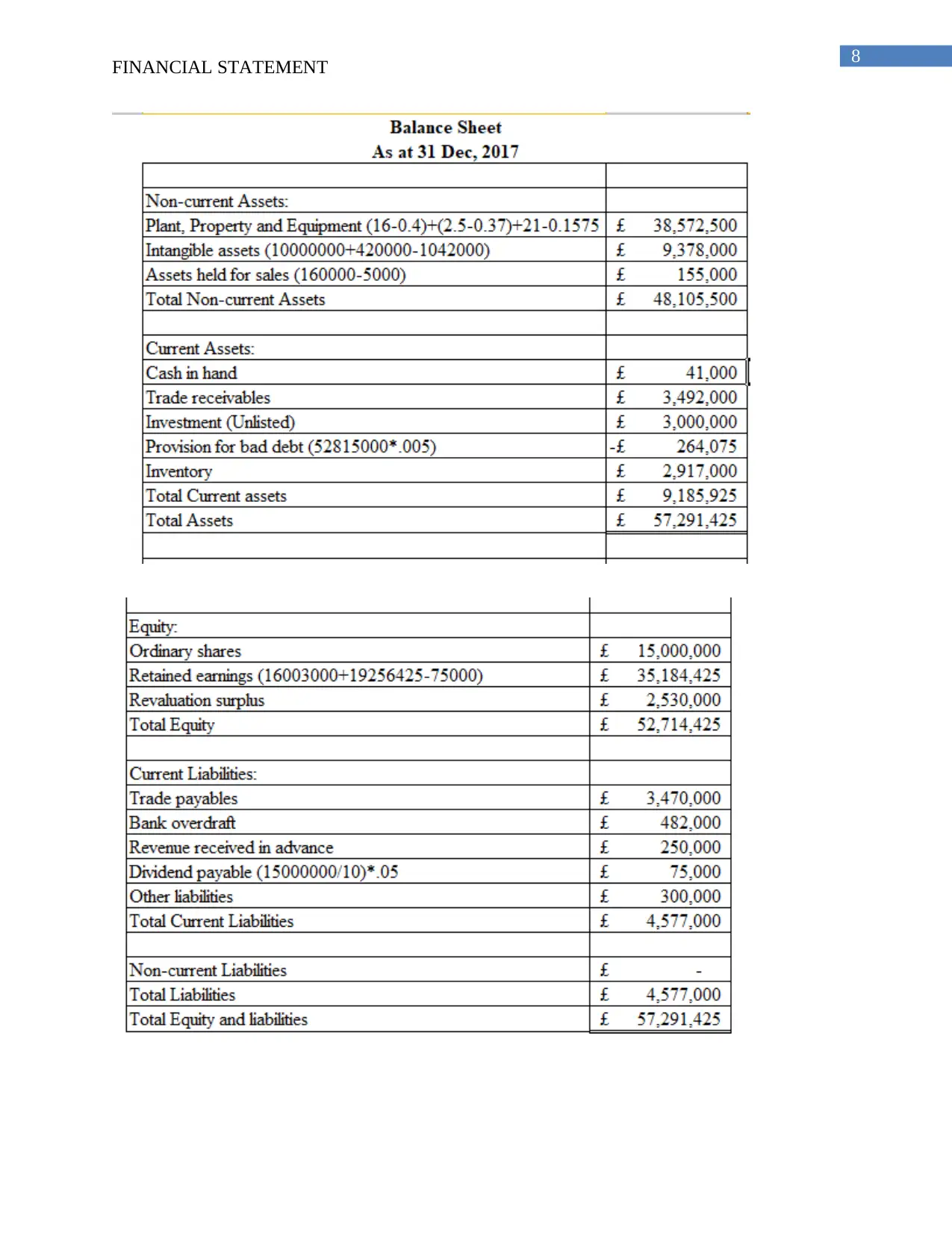

This report presents a financial statement analysis of Hydan Co. for the year 2017. It begins with an executive summary and table of contents, followed by an introduction that outlines the scope of the report. The report delves into the journal entries, comprehensive income statement, and balance sheet. It also explores the concept of depreciation, detailing the factors influencing the useful life of assets. Additionally, the report compares and contrasts the cost and revaluation models as per IAS 16, highlighting the implications of each method. The conclusion summarizes the key findings and allows the company to choose their preferred valuation method. The report also includes a list of references.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.