Comprehensive Financial Statement Analysis and Preparation Report

VerifiedAdded on 2021/06/15

|8

|2096

|37

Report

AI Summary

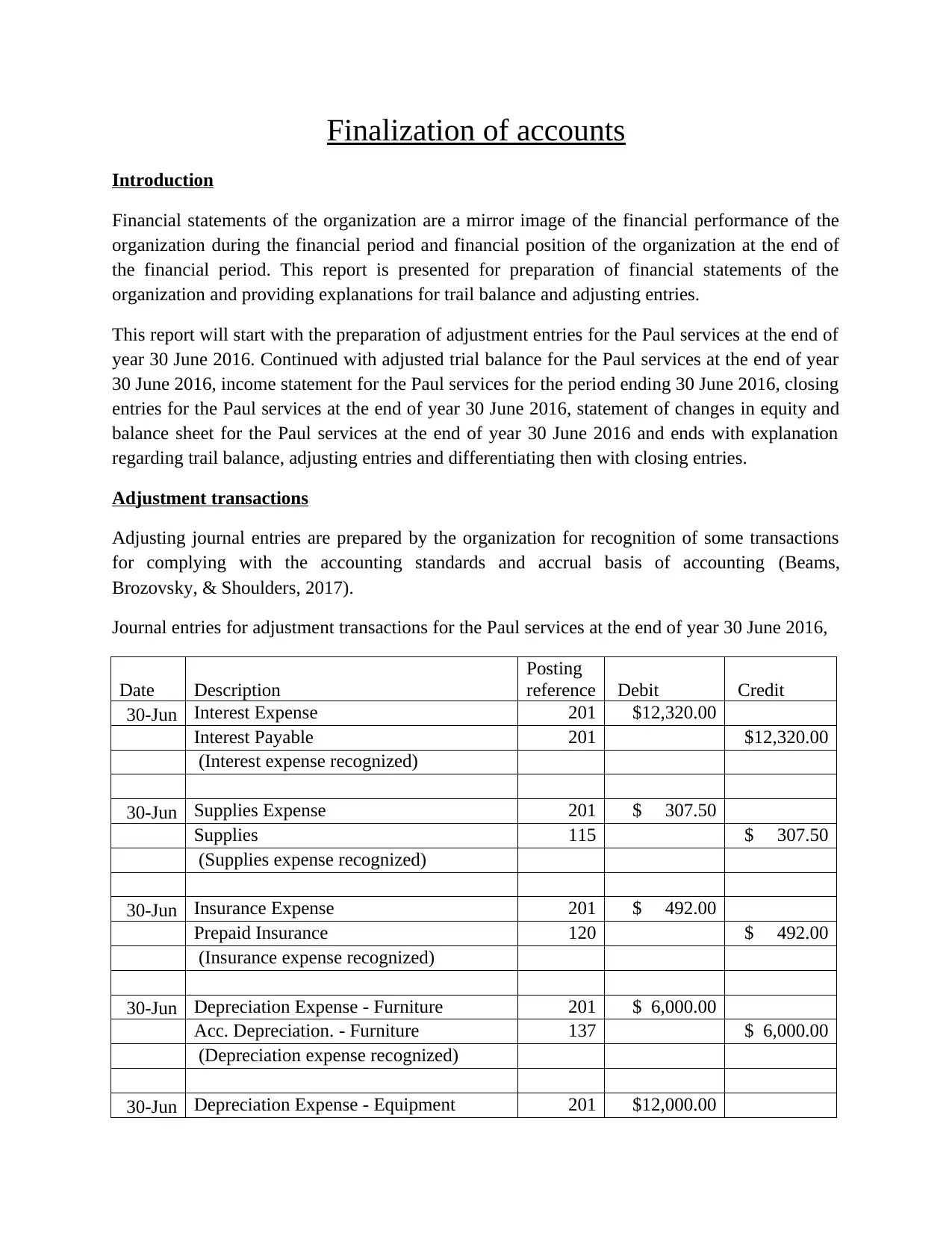

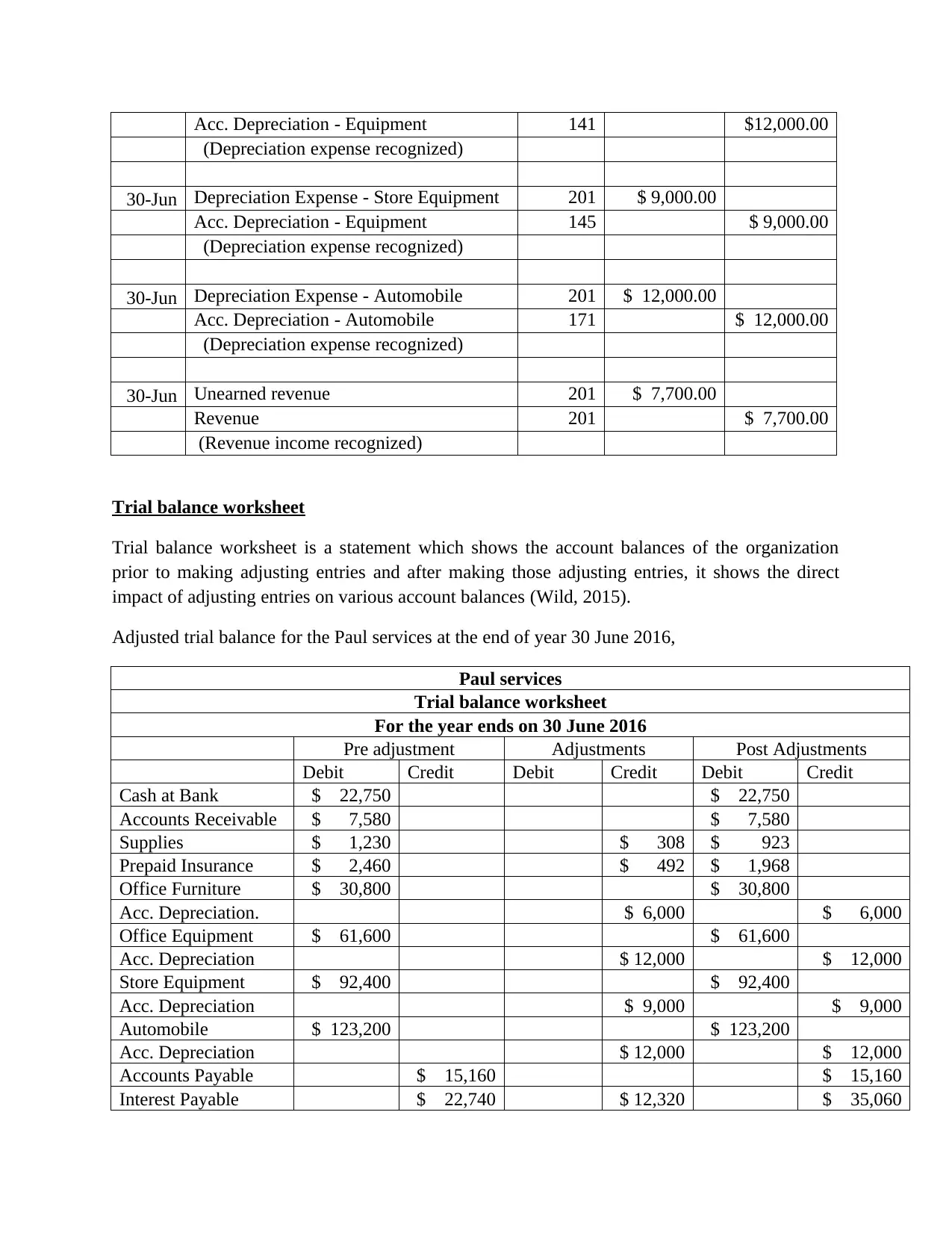

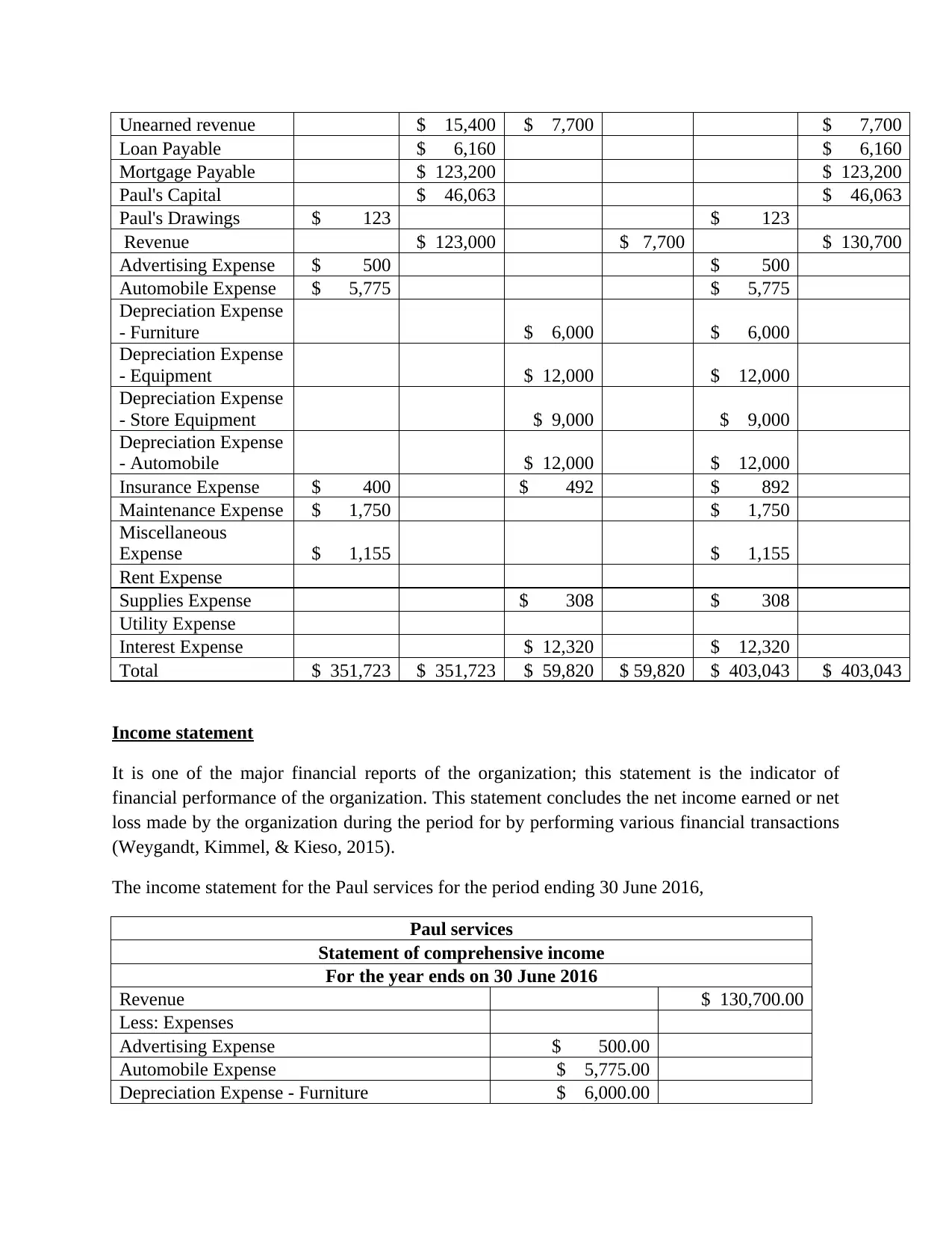

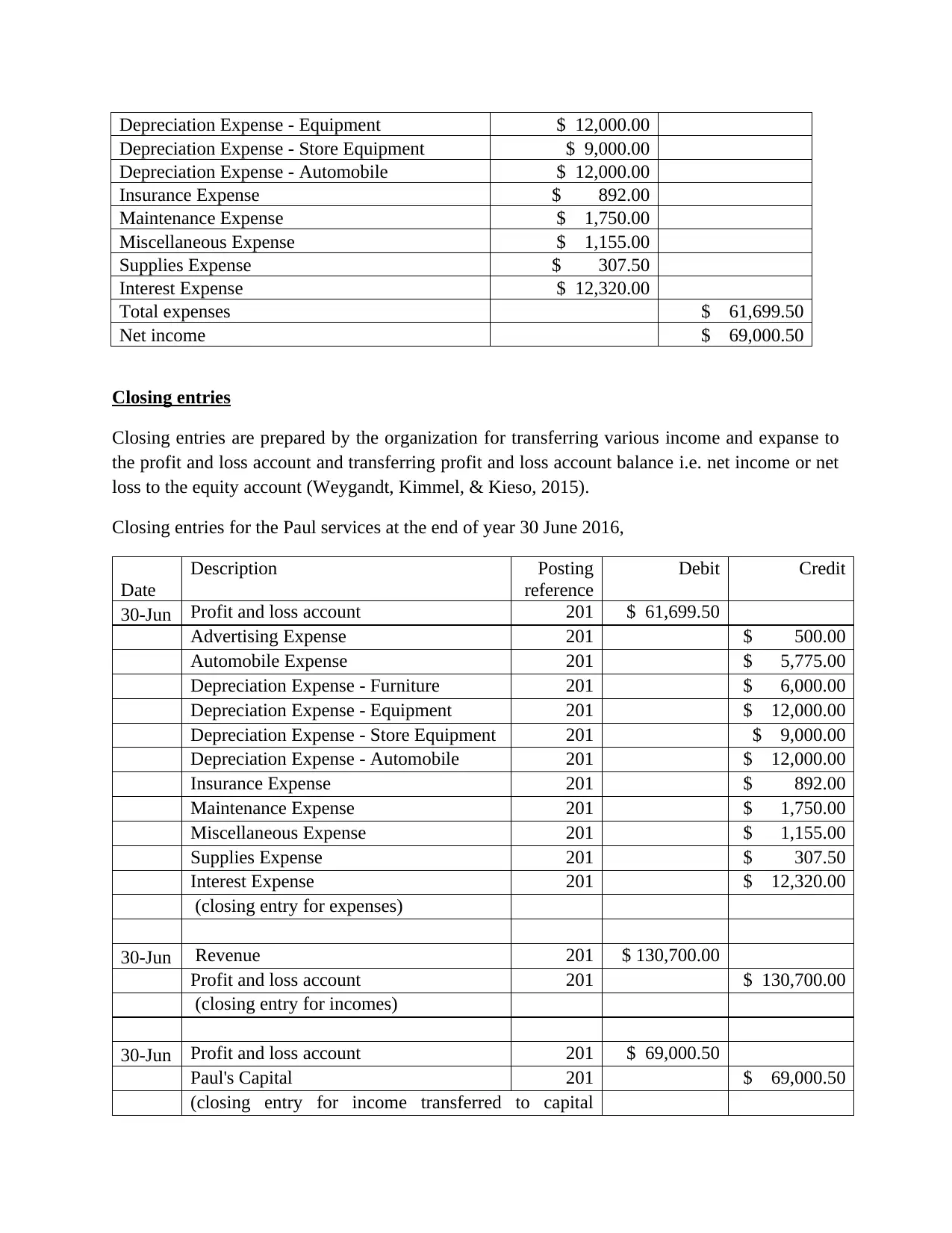

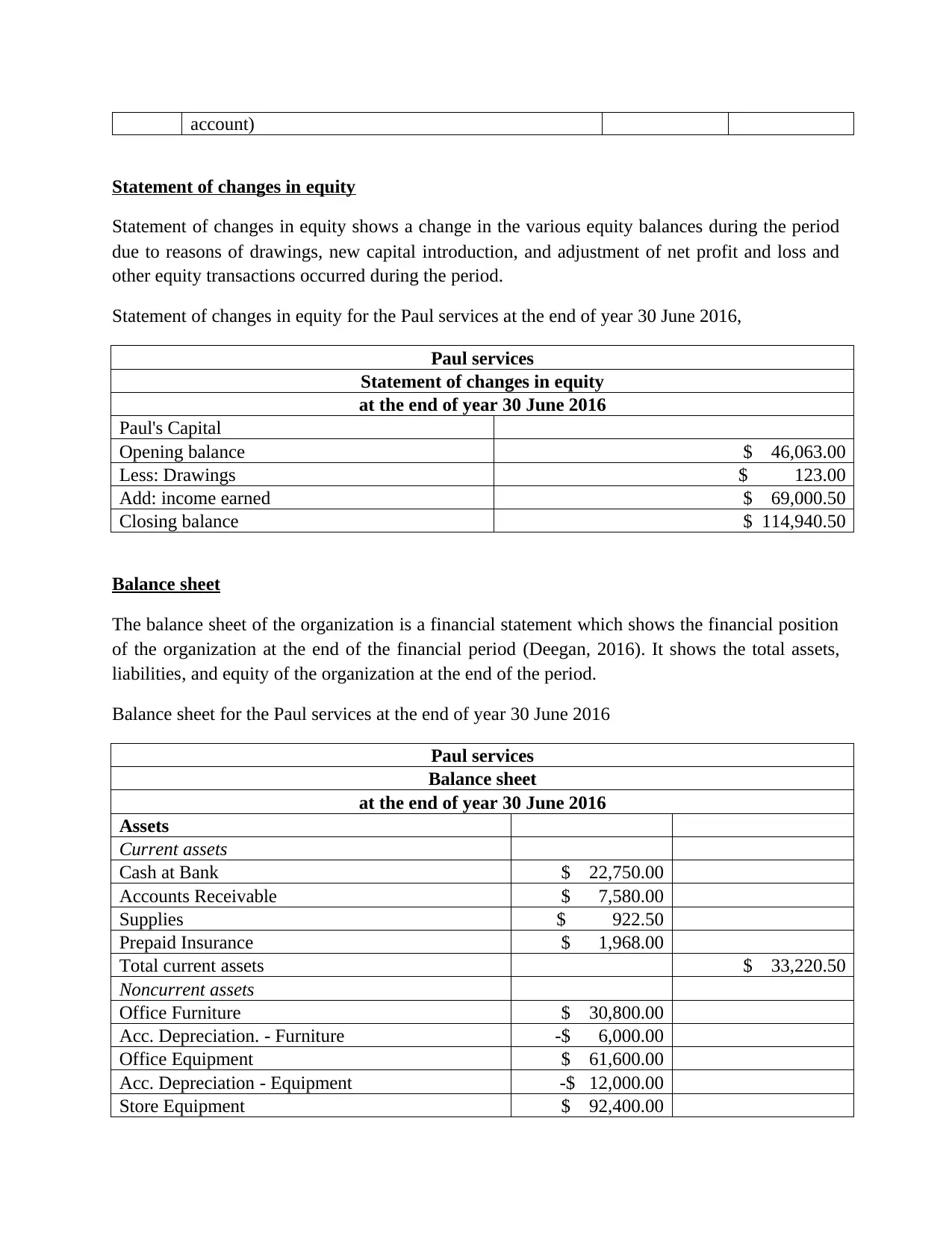

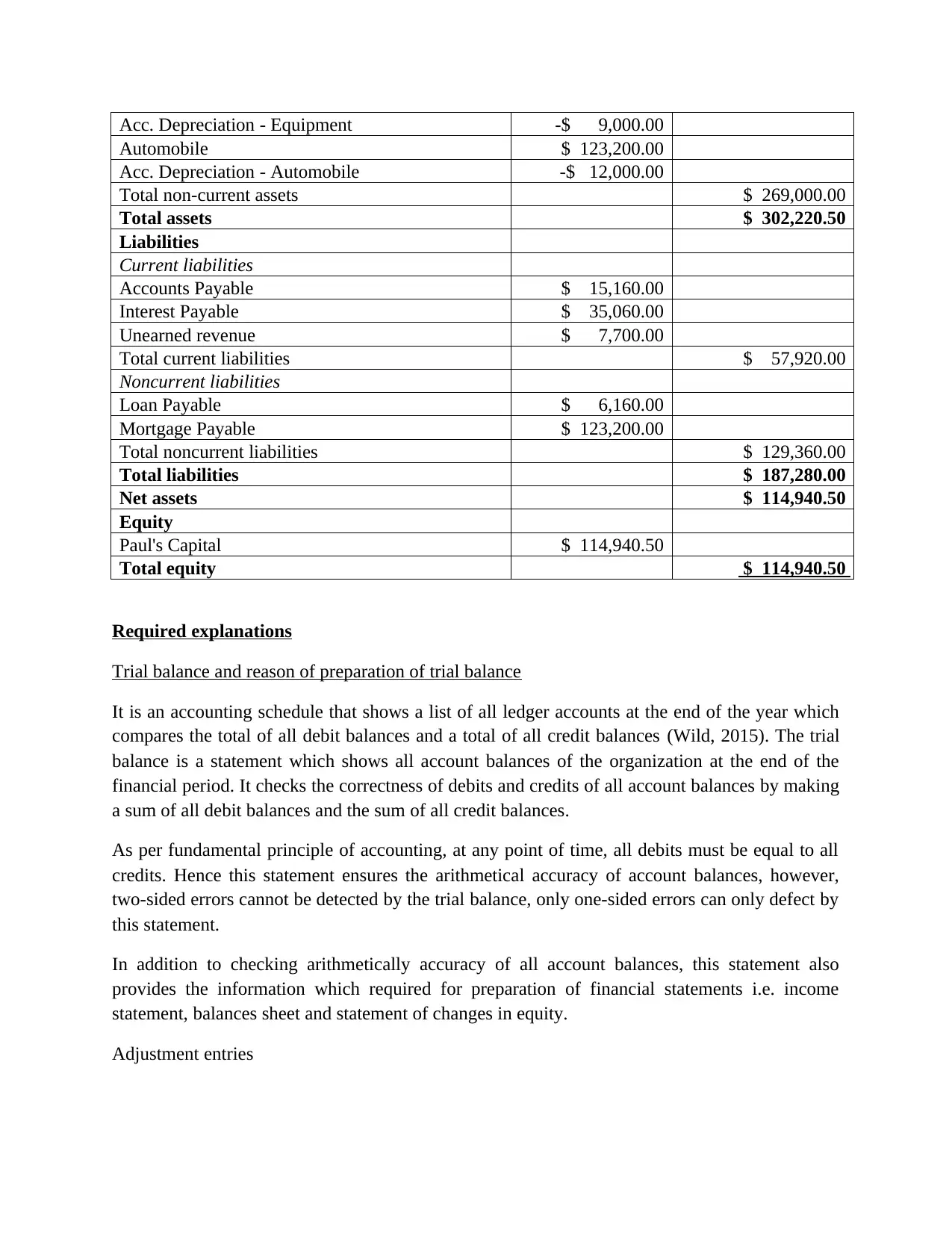

This report details the process of finalizing accounts for Paul Services, encompassing the preparation of financial statements for the period ending June 30, 2016. It begins with adjusting entries, followed by an adjusted trial balance, an income statement, and closing entries. The report also includes a statement of changes in equity and a balance sheet, providing a comprehensive overview of the company's financial performance and position. Key aspects such as trial balance preparation, adjusting entries, and the distinction between adjusting and closing entries are thoroughly explained, offering insights into accounting principles and practices. The report utilizes standard accounting practices to demonstrate the financial health of the organization. It provides a detailed breakdown of various financial statements, including the income statement, balance sheet, and statement of changes in equity, which are crucial for understanding the company's financial performance and position.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.