Corporate Accounting: Analysis of Financial Statements - Simrex

VerifiedAdded on 2023/06/06

|14

|1578

|362

Report

AI Summary

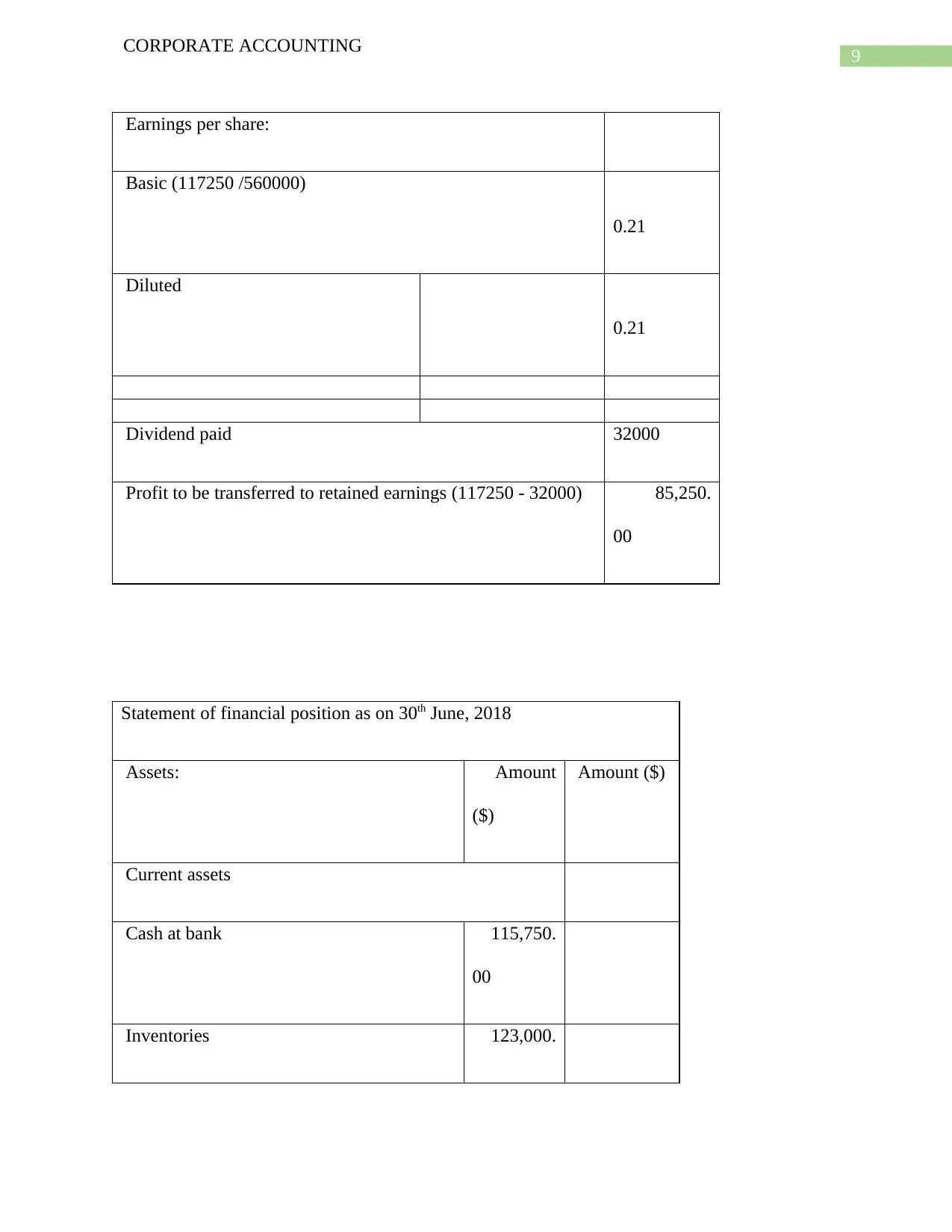

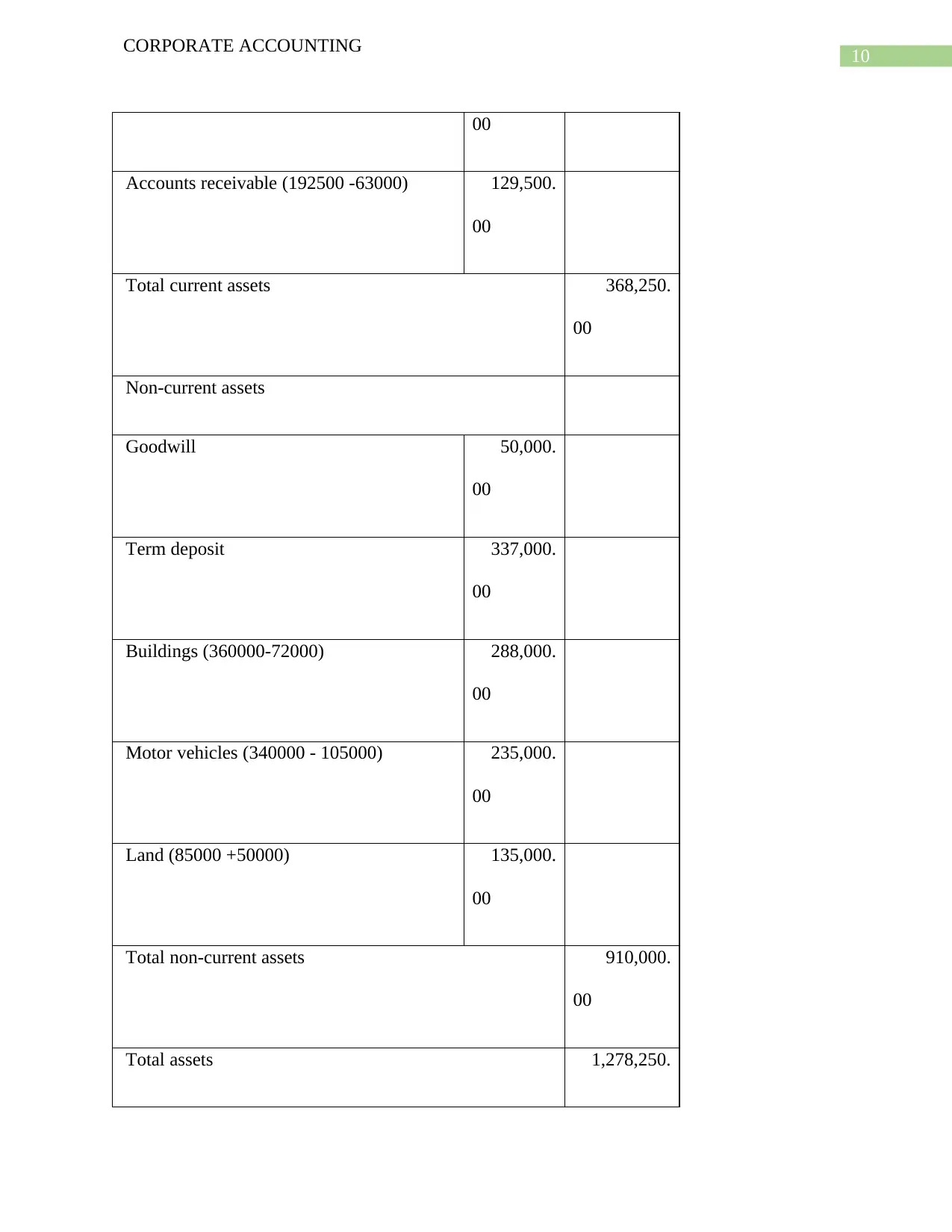

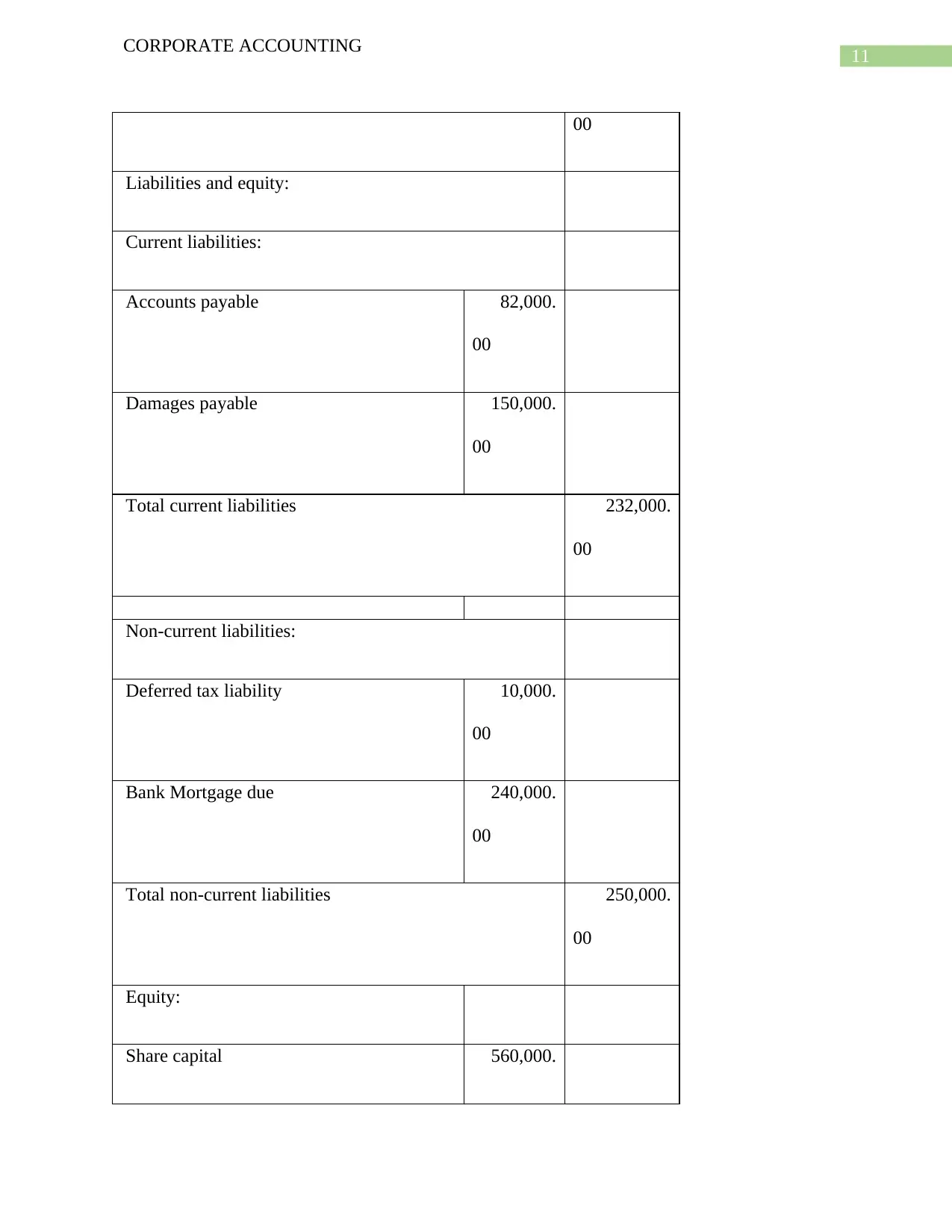

This report provides a comprehensive analysis of Simrex Limited's financial statements, including journal entries, a statement of financial position, a statement of profit and loss, and a statement of changes in equity. It covers key aspects of corporate accounting, such as segment reporting, exceptional items, significant events, income and expenditure recognition, income tax expenses, earnings per share, working capital, accounts receivable, inventories, and accounts payable. The analysis highlights the company's profitability, financial position, and significant events impacting its performance, such as damages and bad debt. The report also includes detailed notes to the financial accounts, providing additional context and explanations.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.