Financial Statement Analysis of Wesfarmers Half-Year Report - Finance

VerifiedAdded on 2021/05/27

|28

|7393

|200

Project

AI Summary

This project presents a comprehensive financial statement analysis of Wesfarmers' half-year report. It begins by evaluating changes in strategy and competitive strategy analysis based on the half-yearly results, including the identification of yields from share investments. The analysis then delves into operating, investment, and financial management decomposition, assessing key financial ratios and their implications. The project also includes an evaluation of the sustainable growth rate and cash flow statements, alongside forecasting for the company. Furthermore, the project explores the impact of the half-year report on share prices and concludes with a reflective section discussing the student's learning experience, the evolving understanding of financial ratios, and the interrelationships among them. The analysis utilizes the provided financial data to assess the company's performance, investment potential, and financial health.

Running head: FINANCIAL STATEMENT ANALYSIS

Financial Statement Analysis

Name of the Student:

Name of the University:

Authors Note:

Financial Statement Analysis

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMENT ANALYSIS

1

Table of Contents

Part 1 of Assignment 2:..............................................................................................................3

1.a) Evaluating any change in strategy analysis based on half-yearly results:..........................3

1.b) Evaluating the change in competitive strategy analysis based on half-yearly results:.......3

1.c.i) Identifying the yield based on half-yearly report by using the shares purchased on 28

March:........................................................................................................................................4

1.c.i) Identifying and comparing the current half-yearly yield with full year yield:.................4

Part 2 of Assignment 2:..............................................................................................................5

2.a Evaluating and assessing the operating Management Decomposition:................................5

2.b Assessing and reporting Investment management decomposition:.....................................7

2.c Assessing and reporting Financial management decomposition:.........................................9

2.d Evaluating and reporting sustainable growth rate:.............................................................12

2.e Evaluating the cash flow statement:...................................................................................13

3.a Identifying the forecast for the company:..........................................................................15

3.b Evaluating and discussing the appropriate forecast strategy:............................................16

3.c Depicting the cash flow forecast, which analysing the statement:.....................................16

4.a Identifying the change in share price within 7 days of half-year report release:...............18

4.b Identifying the change in share price within 31- December and half-year report release: 19

4.c Identifying the change in share price between the half-year report release and 30 April:.20

Part 3 of Assignment 2: Reflective Thinking...........................................................................21

5.a Analysing and discussing on each of the three analyses and how the knowledge changed:

..................................................................................................................................................21

5.b Evaluating how my knowledge improved after receiving feedback from requirement 1:.22

5.c Evaluating how the perception altered regarding the purpose of ratios:............................23

1

Table of Contents

Part 1 of Assignment 2:..............................................................................................................3

1.a) Evaluating any change in strategy analysis based on half-yearly results:..........................3

1.b) Evaluating the change in competitive strategy analysis based on half-yearly results:.......3

1.c.i) Identifying the yield based on half-yearly report by using the shares purchased on 28

March:........................................................................................................................................4

1.c.i) Identifying and comparing the current half-yearly yield with full year yield:.................4

Part 2 of Assignment 2:..............................................................................................................5

2.a Evaluating and assessing the operating Management Decomposition:................................5

2.b Assessing and reporting Investment management decomposition:.....................................7

2.c Assessing and reporting Financial management decomposition:.........................................9

2.d Evaluating and reporting sustainable growth rate:.............................................................12

2.e Evaluating the cash flow statement:...................................................................................13

3.a Identifying the forecast for the company:..........................................................................15

3.b Evaluating and discussing the appropriate forecast strategy:............................................16

3.c Depicting the cash flow forecast, which analysing the statement:.....................................16

4.a Identifying the change in share price within 7 days of half-year report release:...............18

4.b Identifying the change in share price within 31- December and half-year report release: 19

4.c Identifying the change in share price between the half-year report release and 30 April:.20

Part 3 of Assignment 2: Reflective Thinking...........................................................................21

5.a Analysing and discussing on each of the three analyses and how the knowledge changed:

..................................................................................................................................................21

5.b Evaluating how my knowledge improved after receiving feedback from requirement 1:.22

5.c Evaluating how the perception altered regarding the purpose of ratios:............................23

FINANCIAL STATEMENT ANALYSIS

2

5.d Evaluating how the perception of interrelationship among financial ratios and company’s

financial position changed:......................................................................................................23

Reference and Bibliography:....................................................................................................25

2

5.d Evaluating how the perception of interrelationship among financial ratios and company’s

financial position changed:......................................................................................................23

Reference and Bibliography:....................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL STATEMENT ANALYSIS

3

Part 1 of Assignment 2:

1.a) Evaluating any change in strategy analysis based on half-yearly results:

After evaluating the half yearly results of Wesfarmers the strategy analysis used for

the previous assessment needs to be changed, as compared to previous year the organization

incurred losses for the half yearly period. Furthermore, the strategy analysis used needs to be

altered to identify the accurate investment opportunity, as the organization is not able to

generate a higher profit from their operations. moreover, it could be clearly seen that the

strategy-based analysis has not allowed the investor to identify the adequate company for

investment, as the results of Wesfarmers declined during the half yearly period. The net profit

value of Wesfarmers relatively declined from 4.52% in 2016 half yearly report to 0.59% in

2017 half yearly report. This drastic decline in the net profit obtained by the organization has

relatively portrayed the insignificance of strategy analysis used in evaluating the performance

of the organization. The company was not able to provide and deliver the anticipated returns

to the investors (Alin-Eliodor 2014).

1.b) Evaluating the change in competitive strategy analysis based on half-yearly results:

From the evaluation of the half yearly report it could be identified that changes in

competitive strategy analysis would be beneficial for identifying the adequate investment

opportunity, as Wesfarmers was not able to deliver the required returns. The financial

viability of Wesfarmers mainly declined during 2017 half yearly report. where the profits

declined exponentially. The changes in competitive and strategy analysis would eventually

help in identifying the adequate investment opportunity who is overall profit increasing and

are not hindered by other external factors. The competitive strategy did not help with the

investor in detecting the investment opportunity and select the adequate company whose

3

Part 1 of Assignment 2:

1.a) Evaluating any change in strategy analysis based on half-yearly results:

After evaluating the half yearly results of Wesfarmers the strategy analysis used for

the previous assessment needs to be changed, as compared to previous year the organization

incurred losses for the half yearly period. Furthermore, the strategy analysis used needs to be

altered to identify the accurate investment opportunity, as the organization is not able to

generate a higher profit from their operations. moreover, it could be clearly seen that the

strategy-based analysis has not allowed the investor to identify the adequate company for

investment, as the results of Wesfarmers declined during the half yearly period. The net profit

value of Wesfarmers relatively declined from 4.52% in 2016 half yearly report to 0.59% in

2017 half yearly report. This drastic decline in the net profit obtained by the organization has

relatively portrayed the insignificance of strategy analysis used in evaluating the performance

of the organization. The company was not able to provide and deliver the anticipated returns

to the investors (Alin-Eliodor 2014).

1.b) Evaluating the change in competitive strategy analysis based on half-yearly results:

From the evaluation of the half yearly report it could be identified that changes in

competitive strategy analysis would be beneficial for identifying the adequate investment

opportunity, as Wesfarmers was not able to deliver the required returns. The financial

viability of Wesfarmers mainly declined during 2017 half yearly report. where the profits

declined exponentially. The changes in competitive and strategy analysis would eventually

help in identifying the adequate investment opportunity who is overall profit increasing and

are not hindered by other external factors. The competitive strategy did not help with the

investor in detecting the investment opportunity and select the adequate company whose

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMENT ANALYSIS

4

overall profit will increase in future. On the contrary, the selected companies overall net

profits directly declined during the half yearly period, which directly nullified the

significance of competitive strategy analysis (Wahlen, Baginski and Bradsha 2014).

1.c.i) Identifying the yield based on half-yearly report by using the shares purchased on

28 March:

Particulars Value

Share price on 28 March 2018 41.80

Number of shares 598.09

Investment Amount 25,000.00

Dividends half yearly (31-12-17) 1.03

Dividend received 616.03

Yield 2.46%

From the evaluation of above table, the overall yield provided from the investment

conducted by the investor is evaluated. The number of shares that could be bought from the

particular investment is 599 where the overall dividend that is paid during the half yearly

period is at the levels of 1.03 per share. This directly makes the overall yield at the levels of

2.46%, which is relatively adequate for the current investment criteria. However, the

dividends provided by the company remained stagnant during the half yearly period of 2017,

as compared to the half yearly period of 2016. This directly indicates that the company is able

to provide constant dividends even if the prophets during the half yearly period declined

substantially (Robinson et al. 2015).

4

overall profit will increase in future. On the contrary, the selected companies overall net

profits directly declined during the half yearly period, which directly nullified the

significance of competitive strategy analysis (Wahlen, Baginski and Bradsha 2014).

1.c.i) Identifying the yield based on half-yearly report by using the shares purchased on

28 March:

Particulars Value

Share price on 28 March 2018 41.80

Number of shares 598.09

Investment Amount 25,000.00

Dividends half yearly (31-12-17) 1.03

Dividend received 616.03

Yield 2.46%

From the evaluation of above table, the overall yield provided from the investment

conducted by the investor is evaluated. The number of shares that could be bought from the

particular investment is 599 where the overall dividend that is paid during the half yearly

period is at the levels of 1.03 per share. This directly makes the overall yield at the levels of

2.46%, which is relatively adequate for the current investment criteria. However, the

dividends provided by the company remained stagnant during the half yearly period of 2017,

as compared to the half yearly period of 2016. This directly indicates that the company is able

to provide constant dividends even if the prophets during the half yearly period declined

substantially (Robinson et al. 2015).

FINANCIAL STATEMENT ANALYSIS

5

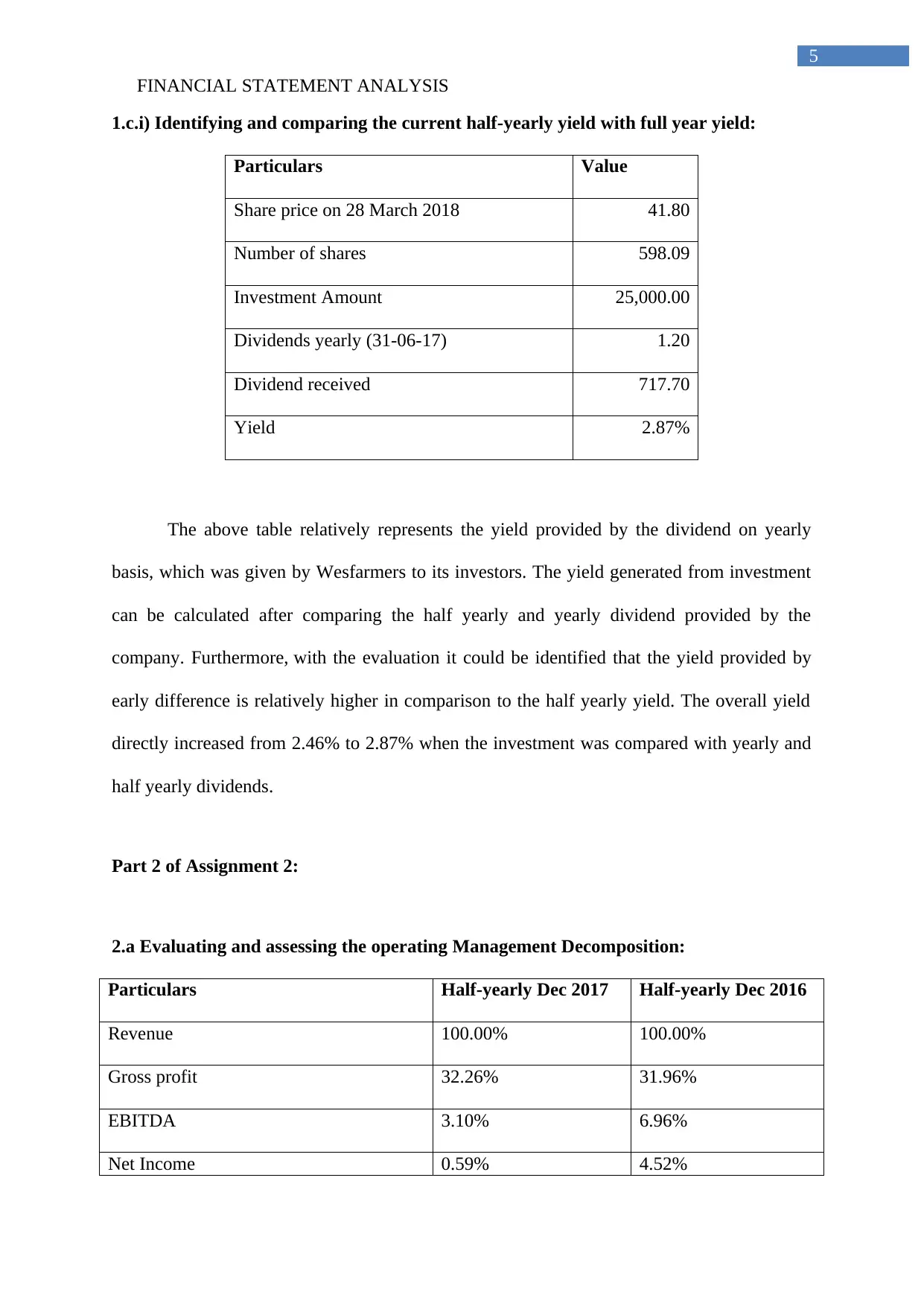

1.c.i) Identifying and comparing the current half-yearly yield with full year yield:

Particulars Value

Share price on 28 March 2018 41.80

Number of shares 598.09

Investment Amount 25,000.00

Dividends yearly (31-06-17) 1.20

Dividend received 717.70

Yield 2.87%

The above table relatively represents the yield provided by the dividend on yearly

basis, which was given by Wesfarmers to its investors. The yield generated from investment

can be calculated after comparing the half yearly and yearly dividend provided by the

company. Furthermore, with the evaluation it could be identified that the yield provided by

early difference is relatively higher in comparison to the half yearly yield. The overall yield

directly increased from 2.46% to 2.87% when the investment was compared with yearly and

half yearly dividends.

Part 2 of Assignment 2:

2.a Evaluating and assessing the operating Management Decomposition:

Particulars Half-yearly Dec 2017 Half-yearly Dec 2016

Revenue 100.00% 100.00%

Gross profit 32.26% 31.96%

EBITDA 3.10% 6.96%

Net Income 0.59% 4.52%

5

1.c.i) Identifying and comparing the current half-yearly yield with full year yield:

Particulars Value

Share price on 28 March 2018 41.80

Number of shares 598.09

Investment Amount 25,000.00

Dividends yearly (31-06-17) 1.20

Dividend received 717.70

Yield 2.87%

The above table relatively represents the yield provided by the dividend on yearly

basis, which was given by Wesfarmers to its investors. The yield generated from investment

can be calculated after comparing the half yearly and yearly dividend provided by the

company. Furthermore, with the evaluation it could be identified that the yield provided by

early difference is relatively higher in comparison to the half yearly yield. The overall yield

directly increased from 2.46% to 2.87% when the investment was compared with yearly and

half yearly dividends.

Part 2 of Assignment 2:

2.a Evaluating and assessing the operating Management Decomposition:

Particulars Half-yearly Dec 2017 Half-yearly Dec 2016

Revenue 100.00% 100.00%

Gross profit 32.26% 31.96%

EBITDA 3.10% 6.96%

Net Income 0.59% 4.52%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL STATEMENT ANALYSIS

6

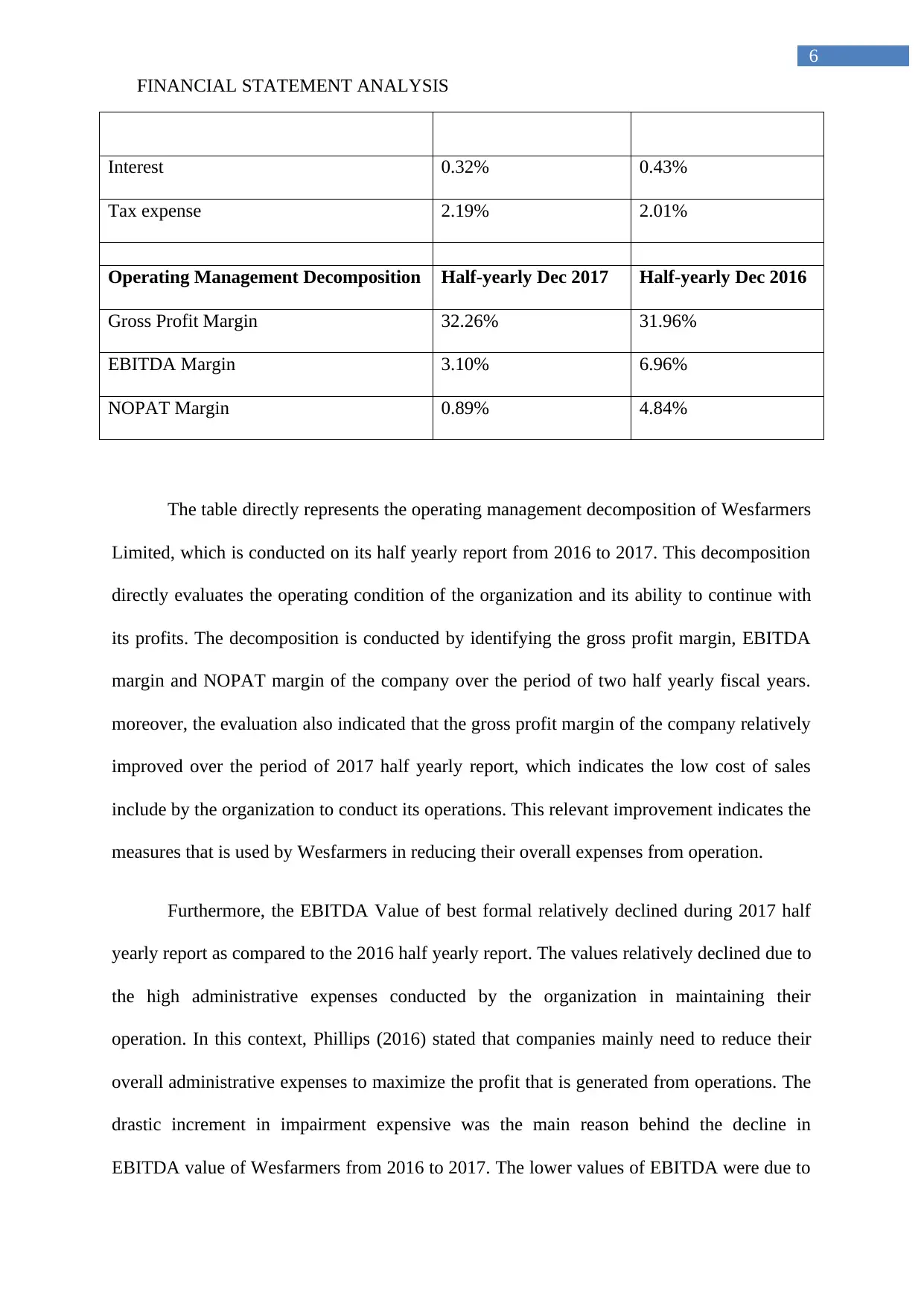

Interest 0.32% 0.43%

Tax expense 2.19% 2.01%

Operating Management Decomposition Half-yearly Dec 2017 Half-yearly Dec 2016

Gross Profit Margin 32.26% 31.96%

EBITDA Margin 3.10% 6.96%

NOPAT Margin 0.89% 4.84%

The table directly represents the operating management decomposition of Wesfarmers

Limited, which is conducted on its half yearly report from 2016 to 2017. This decomposition

directly evaluates the operating condition of the organization and its ability to continue with

its profits. The decomposition is conducted by identifying the gross profit margin, EBITDA

margin and NOPAT margin of the company over the period of two half yearly fiscal years.

moreover, the evaluation also indicated that the gross profit margin of the company relatively

improved over the period of 2017 half yearly report, which indicates the low cost of sales

include by the organization to conduct its operations. This relevant improvement indicates the

measures that is used by Wesfarmers in reducing their overall expenses from operation.

Furthermore, the EBITDA Value of best formal relatively declined during 2017 half

yearly report as compared to the 2016 half yearly report. The values relatively declined due to

the high administrative expenses conducted by the organization in maintaining their

operation. In this context, Phillips (2016) stated that companies mainly need to reduce their

overall administrative expenses to maximize the profit that is generated from operations. The

drastic increment in impairment expensive was the main reason behind the decline in

EBITDA value of Wesfarmers from 2016 to 2017. The lower values of EBITDA were due to

6

Interest 0.32% 0.43%

Tax expense 2.19% 2.01%

Operating Management Decomposition Half-yearly Dec 2017 Half-yearly Dec 2016

Gross Profit Margin 32.26% 31.96%

EBITDA Margin 3.10% 6.96%

NOPAT Margin 0.89% 4.84%

The table directly represents the operating management decomposition of Wesfarmers

Limited, which is conducted on its half yearly report from 2016 to 2017. This decomposition

directly evaluates the operating condition of the organization and its ability to continue with

its profits. The decomposition is conducted by identifying the gross profit margin, EBITDA

margin and NOPAT margin of the company over the period of two half yearly fiscal years.

moreover, the evaluation also indicated that the gross profit margin of the company relatively

improved over the period of 2017 half yearly report, which indicates the low cost of sales

include by the organization to conduct its operations. This relevant improvement indicates the

measures that is used by Wesfarmers in reducing their overall expenses from operation.

Furthermore, the EBITDA Value of best formal relatively declined during 2017 half

yearly report as compared to the 2016 half yearly report. The values relatively declined due to

the high administrative expenses conducted by the organization in maintaining their

operation. In this context, Phillips (2016) stated that companies mainly need to reduce their

overall administrative expenses to maximize the profit that is generated from operations. The

drastic increment in impairment expensive was the main reason behind the decline in

EBITDA value of Wesfarmers from 2016 to 2017. The lower values of EBITDA were due to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMENT ANALYSIS

7

the high Expenses on impairment, which was conducted by Wesfarmers during 2017 half

yearly period. This overall incremental expense of the company directly hampered its

operating revenues and net profit revenues. the other expenses of the organization were

relatively as per the trend, which increased due to the improvements and its operations. The

single transaction of the impairment expenses has relatively depicted the low cash retention

capability of the organization during the fiscal year of 2017.

Furthermore, after evaluating the decomposition value of relevant decline in NOPAT

margin can be identified from 2016 to 2017. The values of NOPAT has declined rapidly from

the levels of 4.48% to 0.89%, which is directly affecting the operational capability of the

organization. From the evaluation of the above calculations it could be identified that net

income of the company has rapidly declined over the period while the interest rate of the

company declined. The increment and tax value and production in industry was the main

reason behind the reducing net income obtained by the organization during the half yearly

period of 2017. According to Lin et al. (2015), the evaluation of net profit margin and gross

profit margin allows the investors to determine the administrative expenses and Finance cost

conducted by the organization to support its operations.

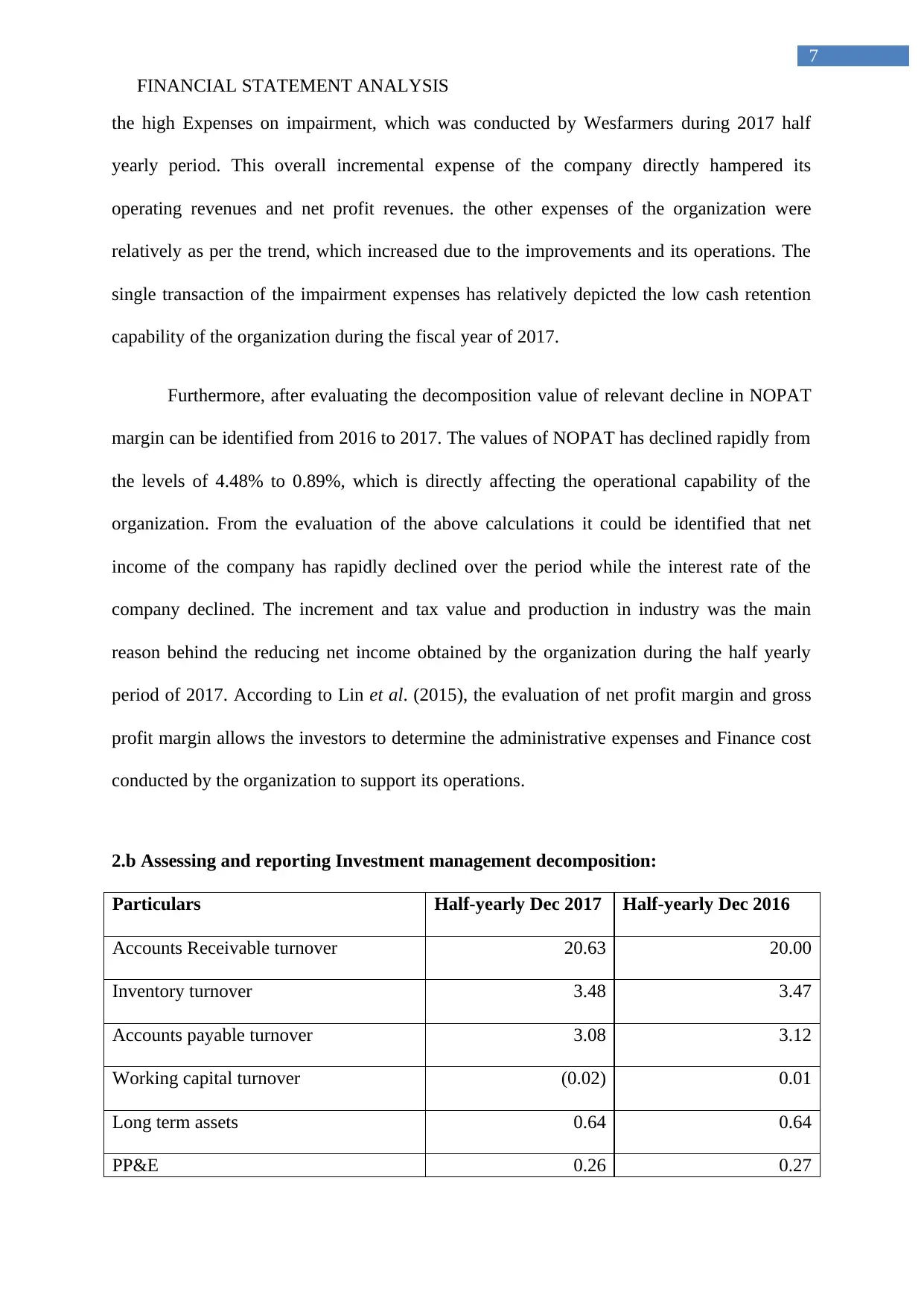

2.b Assessing and reporting Investment management decomposition:

Particulars Half-yearly Dec 2017 Half-yearly Dec 2016

Accounts Receivable turnover 20.63 20.00

Inventory turnover 3.48 3.47

Accounts payable turnover 3.08 3.12

Working capital turnover (0.02) 0.01

Long term assets 0.64 0.64

PP&E 0.26 0.27

7

the high Expenses on impairment, which was conducted by Wesfarmers during 2017 half

yearly period. This overall incremental expense of the company directly hampered its

operating revenues and net profit revenues. the other expenses of the organization were

relatively as per the trend, which increased due to the improvements and its operations. The

single transaction of the impairment expenses has relatively depicted the low cash retention

capability of the organization during the fiscal year of 2017.

Furthermore, after evaluating the decomposition value of relevant decline in NOPAT

margin can be identified from 2016 to 2017. The values of NOPAT has declined rapidly from

the levels of 4.48% to 0.89%, which is directly affecting the operational capability of the

organization. From the evaluation of the above calculations it could be identified that net

income of the company has rapidly declined over the period while the interest rate of the

company declined. The increment and tax value and production in industry was the main

reason behind the reducing net income obtained by the organization during the half yearly

period of 2017. According to Lin et al. (2015), the evaluation of net profit margin and gross

profit margin allows the investors to determine the administrative expenses and Finance cost

conducted by the organization to support its operations.

2.b Assessing and reporting Investment management decomposition:

Particulars Half-yearly Dec 2017 Half-yearly Dec 2016

Accounts Receivable turnover 20.63 20.00

Inventory turnover 3.48 3.47

Accounts payable turnover 3.08 3.12

Working capital turnover (0.02) 0.01

Long term assets 0.64 0.64

PP&E 0.26 0.27

FINANCIAL STATEMENT ANALYSIS

8

Investment Management Decomp Half-yearly Dec 2017 Half-yearly Dec 2016

Days Account receivable 18 18

Days Account inventory 105 105

Days Account payable 118 117

The calculations conducted in the above table relatively represents the overall

investment management decomposition conducted by Wesfarmers during the fiscal years.

The evaluation of investment management decomposition relatively depicts the overall

accounts receivable days, accounts payable days and inventory turnover days of the

organization. The effectiveness of the investments conducted by the organization is evaluated

with the help of investment management decomposition method. On the other hand, the other

investment decomposition components such as long-term assets, have relatively remained

stagnant from 0.64 to 0.64 in 2017 half yearly report. Moreover, the property, plant and

equipment of the organization has reduced from 0.27 to 0.26 in 2017. This relatively

represents that the company is acquiring assets but is not investing in property, plant, and

equipment. On the contrary, the overall working capital turnover ratio of the company

declined to negative value of 0.02, which indicates that the company's overall current

liabilities have exceeded the current assets during 2017 half yearly report. The overall decline

in working capital ratio directly indicated the high levels of short term liabilities that is being

accumulated by the company to conduct its operation. This relatively depicts the overall low

capability of the management to conduct operations of the organization for strengthening its

financial position (Wahlen 2014).

8

Investment Management Decomp Half-yearly Dec 2017 Half-yearly Dec 2016

Days Account receivable 18 18

Days Account inventory 105 105

Days Account payable 118 117

The calculations conducted in the above table relatively represents the overall

investment management decomposition conducted by Wesfarmers during the fiscal years.

The evaluation of investment management decomposition relatively depicts the overall

accounts receivable days, accounts payable days and inventory turnover days of the

organization. The effectiveness of the investments conducted by the organization is evaluated

with the help of investment management decomposition method. On the other hand, the other

investment decomposition components such as long-term assets, have relatively remained

stagnant from 0.64 to 0.64 in 2017 half yearly report. Moreover, the property, plant and

equipment of the organization has reduced from 0.27 to 0.26 in 2017. This relatively

represents that the company is acquiring assets but is not investing in property, plant, and

equipment. On the contrary, the overall working capital turnover ratio of the company

declined to negative value of 0.02, which indicates that the company's overall current

liabilities have exceeded the current assets during 2017 half yearly report. The overall decline

in working capital ratio directly indicated the high levels of short term liabilities that is being

accumulated by the company to conduct its operation. This relatively depicts the overall low

capability of the management to conduct operations of the organization for strengthening its

financial position (Wahlen 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL STATEMENT ANALYSIS

9

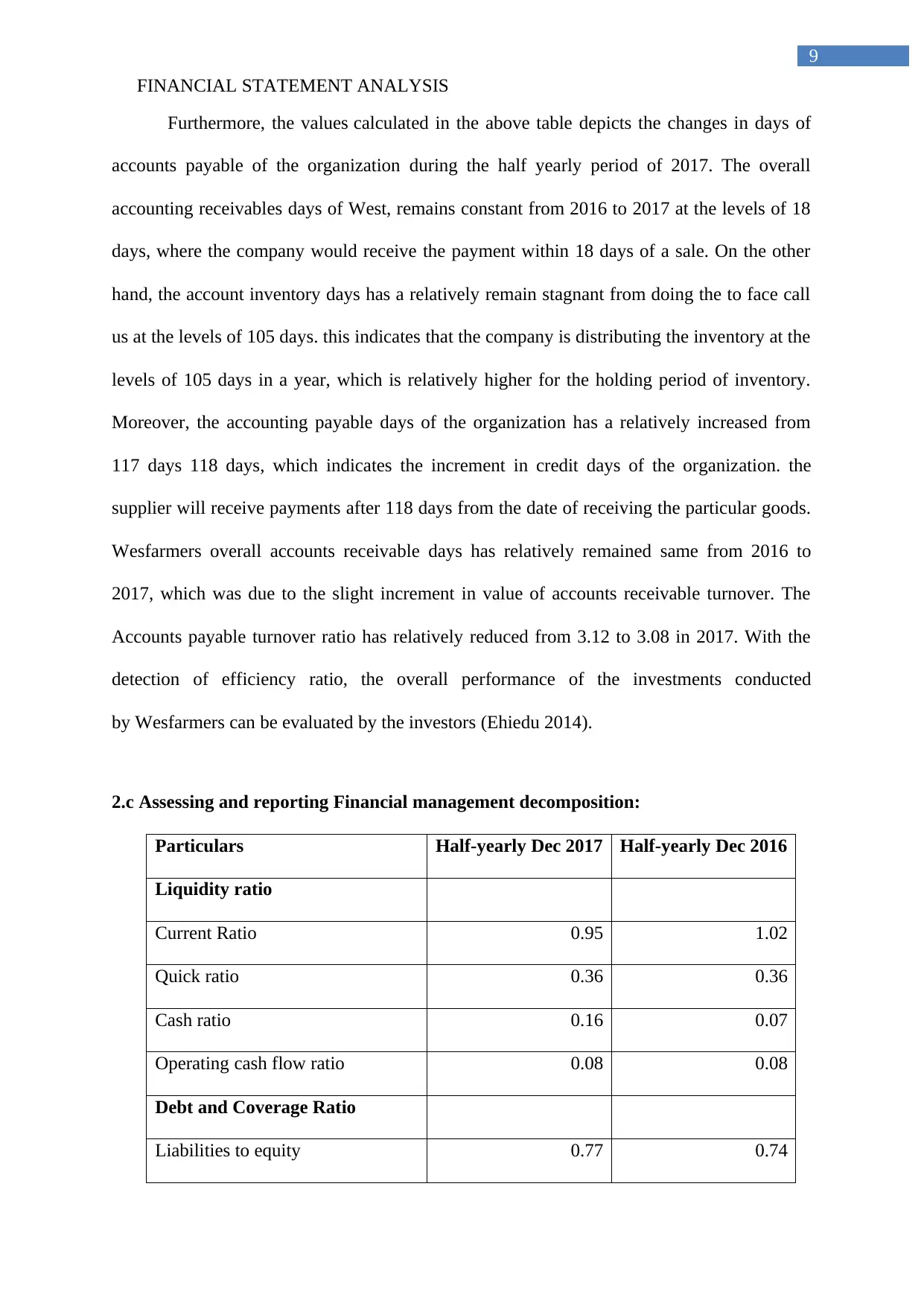

Furthermore, the values calculated in the above table depicts the changes in days of

accounts payable of the organization during the half yearly period of 2017. The overall

accounting receivables days of West, remains constant from 2016 to 2017 at the levels of 18

days, where the company would receive the payment within 18 days of a sale. On the other

hand, the account inventory days has a relatively remain stagnant from doing the to face call

us at the levels of 105 days. this indicates that the company is distributing the inventory at the

levels of 105 days in a year, which is relatively higher for the holding period of inventory.

Moreover, the accounting payable days of the organization has a relatively increased from

117 days 118 days, which indicates the increment in credit days of the organization. the

supplier will receive payments after 118 days from the date of receiving the particular goods.

Wesfarmers overall accounts receivable days has relatively remained same from 2016 to

2017, which was due to the slight increment in value of accounts receivable turnover. The

Accounts payable turnover ratio has relatively reduced from 3.12 to 3.08 in 2017. With the

detection of efficiency ratio, the overall performance of the investments conducted

by Wesfarmers can be evaluated by the investors (Ehiedu 2014).

2.c Assessing and reporting Financial management decomposition:

Particulars Half-yearly Dec 2017 Half-yearly Dec 2016

Liquidity ratio

Current Ratio 0.95 1.02

Quick ratio 0.36 0.36

Cash ratio 0.16 0.07

Operating cash flow ratio 0.08 0.08

Debt and Coverage Ratio

Liabilities to equity 0.77 0.74

9

Furthermore, the values calculated in the above table depicts the changes in days of

accounts payable of the organization during the half yearly period of 2017. The overall

accounting receivables days of West, remains constant from 2016 to 2017 at the levels of 18

days, where the company would receive the payment within 18 days of a sale. On the other

hand, the account inventory days has a relatively remain stagnant from doing the to face call

us at the levels of 105 days. this indicates that the company is distributing the inventory at the

levels of 105 days in a year, which is relatively higher for the holding period of inventory.

Moreover, the accounting payable days of the organization has a relatively increased from

117 days 118 days, which indicates the increment in credit days of the organization. the

supplier will receive payments after 118 days from the date of receiving the particular goods.

Wesfarmers overall accounts receivable days has relatively remained same from 2016 to

2017, which was due to the slight increment in value of accounts receivable turnover. The

Accounts payable turnover ratio has relatively reduced from 3.12 to 3.08 in 2017. With the

detection of efficiency ratio, the overall performance of the investments conducted

by Wesfarmers can be evaluated by the investors (Ehiedu 2014).

2.c Assessing and reporting Financial management decomposition:

Particulars Half-yearly Dec 2017 Half-yearly Dec 2016

Liquidity ratio

Current Ratio 0.95 1.02

Quick ratio 0.36 0.36

Cash ratio 0.16 0.07

Operating cash flow ratio 0.08 0.08

Debt and Coverage Ratio

Liabilities to equity 0.77 0.74

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMENT ANALYSIS

10

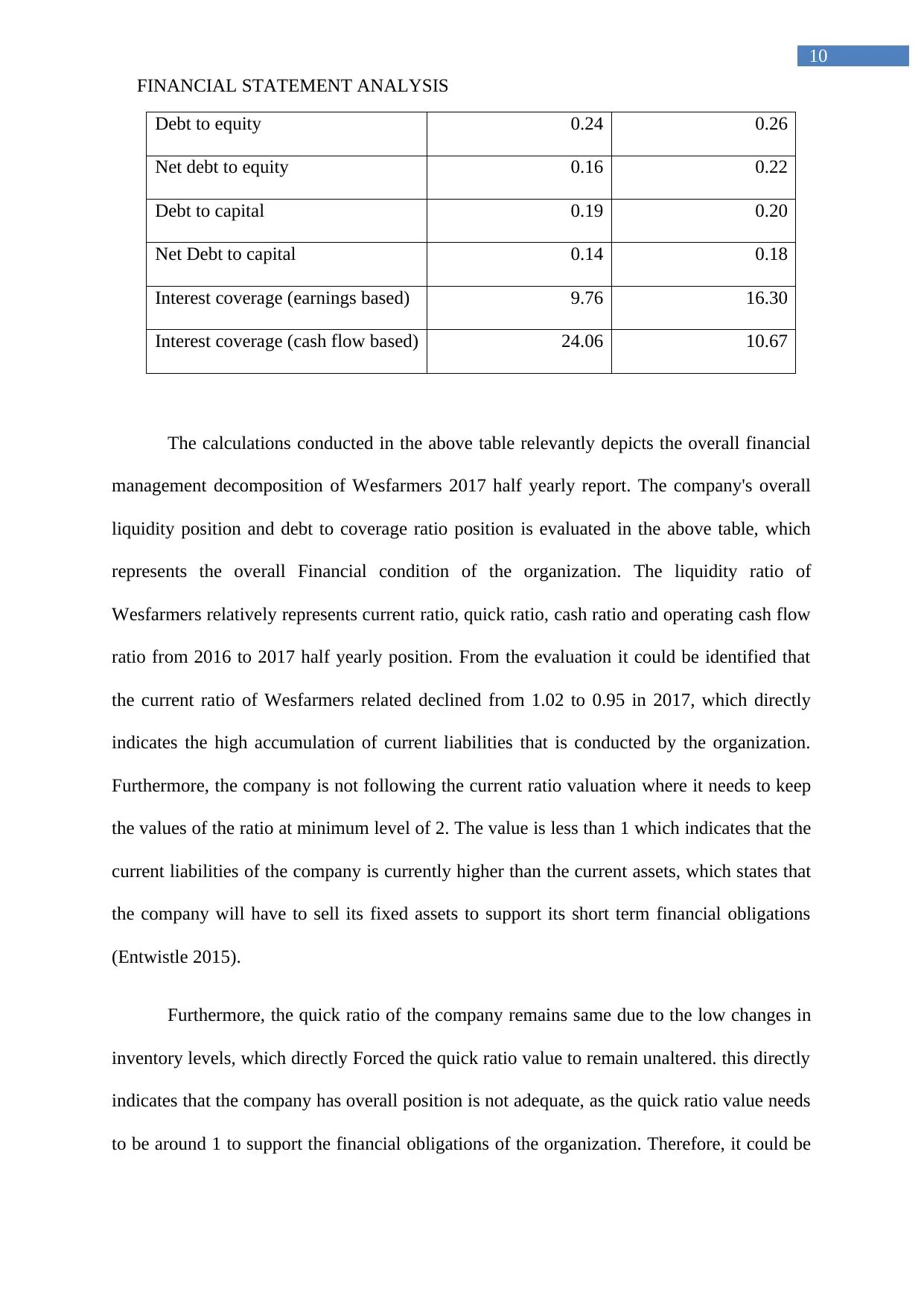

Debt to equity 0.24 0.26

Net debt to equity 0.16 0.22

Debt to capital 0.19 0.20

Net Debt to capital 0.14 0.18

Interest coverage (earnings based) 9.76 16.30

Interest coverage (cash flow based) 24.06 10.67

The calculations conducted in the above table relevantly depicts the overall financial

management decomposition of Wesfarmers 2017 half yearly report. The company's overall

liquidity position and debt to coverage ratio position is evaluated in the above table, which

represents the overall Financial condition of the organization. The liquidity ratio of

Wesfarmers relatively represents current ratio, quick ratio, cash ratio and operating cash flow

ratio from 2016 to 2017 half yearly position. From the evaluation it could be identified that

the current ratio of Wesfarmers related declined from 1.02 to 0.95 in 2017, which directly

indicates the high accumulation of current liabilities that is conducted by the organization.

Furthermore, the company is not following the current ratio valuation where it needs to keep

the values of the ratio at minimum level of 2. The value is less than 1 which indicates that the

current liabilities of the company is currently higher than the current assets, which states that

the company will have to sell its fixed assets to support its short term financial obligations

(Entwistle 2015).

Furthermore, the quick ratio of the company remains same due to the low changes in

inventory levels, which directly Forced the quick ratio value to remain unaltered. this directly

indicates that the company has overall position is not adequate, as the quick ratio value needs

to be around 1 to support the financial obligations of the organization. Therefore, it could be

10

Debt to equity 0.24 0.26

Net debt to equity 0.16 0.22

Debt to capital 0.19 0.20

Net Debt to capital 0.14 0.18

Interest coverage (earnings based) 9.76 16.30

Interest coverage (cash flow based) 24.06 10.67

The calculations conducted in the above table relevantly depicts the overall financial

management decomposition of Wesfarmers 2017 half yearly report. The company's overall

liquidity position and debt to coverage ratio position is evaluated in the above table, which

represents the overall Financial condition of the organization. The liquidity ratio of

Wesfarmers relatively represents current ratio, quick ratio, cash ratio and operating cash flow

ratio from 2016 to 2017 half yearly position. From the evaluation it could be identified that

the current ratio of Wesfarmers related declined from 1.02 to 0.95 in 2017, which directly

indicates the high accumulation of current liabilities that is conducted by the organization.

Furthermore, the company is not following the current ratio valuation where it needs to keep

the values of the ratio at minimum level of 2. The value is less than 1 which indicates that the

current liabilities of the company is currently higher than the current assets, which states that

the company will have to sell its fixed assets to support its short term financial obligations

(Entwistle 2015).

Furthermore, the quick ratio of the company remains same due to the low changes in

inventory levels, which directly Forced the quick ratio value to remain unaltered. this directly

indicates that the company has overall position is not adequate, as the quick ratio value needs

to be around 1 to support the financial obligations of the organization. Therefore, it could be

FINANCIAL STATEMENT ANALYSIS

11

assumed that Wesfarmers current financial position is not adequate to support its short-term

obligations. Moreover, the evaluation of cash ratio indicates an increment in the value from

0.07 in 2016 to 0.16 in 2017, which indicates the relevant Improvement in cash position of

the organization. This is due to the additional credit days that is allowed by the suppliers to

the organization. The operating cash flow position of the company has remained same due to

the stagnant values obtained during 2017 half yearly report. The company's progress has

relatively declined during the period due to the accumulation of high-end current liabilities

and declining profitability (Grant 2016).

From the evaluation of debt and coverage ratio calculated in the above table, the

financial position of Wesfarmers can be identified, which has a relatively deteriorated over

the period half period of 2017. The overall positions of the organization have relatively

declined due to the accumulation of liabilities conducted by the organization during the half

yearly period of 2017. However, the debt position of the company declined during the period

where the reduction in debt to equity ratio is seen from 0.26 to 0.24 in 2017. This relatively

indicates that the company was able to repay some of its debt back to the lender, which

relatively improved its debt to equity ratio. The net debt to equity ratio also improved from

0.22 to 0.16 indicating a positive attribute for the organization and depicting its financial

strength. Supporting values of debt to Capital also indicates a positive attribute of the

organization, as its value declined from 0.20 to 0.19 in 2017. However, the overall interest

coverage ratio based on earnings has a relatively declined due to the low profit that was

generated by the organization during 2017 half yearly position. The company was relatively

not able to generate higher profits from its operations to improve the level of interest

coverage ratio. on the other hand, the interest coverage ratio based on cash flow position has

a relatively improved from 10.67 to 24.06 in 2017. This relatively indicates the positive

cashier position of the organization during the fiscal year. Wesfarmers has been maintaining a

11

assumed that Wesfarmers current financial position is not adequate to support its short-term

obligations. Moreover, the evaluation of cash ratio indicates an increment in the value from

0.07 in 2016 to 0.16 in 2017, which indicates the relevant Improvement in cash position of

the organization. This is due to the additional credit days that is allowed by the suppliers to

the organization. The operating cash flow position of the company has remained same due to

the stagnant values obtained during 2017 half yearly report. The company's progress has

relatively declined during the period due to the accumulation of high-end current liabilities

and declining profitability (Grant 2016).

From the evaluation of debt and coverage ratio calculated in the above table, the

financial position of Wesfarmers can be identified, which has a relatively deteriorated over

the period half period of 2017. The overall positions of the organization have relatively

declined due to the accumulation of liabilities conducted by the organization during the half

yearly period of 2017. However, the debt position of the company declined during the period

where the reduction in debt to equity ratio is seen from 0.26 to 0.24 in 2017. This relatively

indicates that the company was able to repay some of its debt back to the lender, which

relatively improved its debt to equity ratio. The net debt to equity ratio also improved from

0.22 to 0.16 indicating a positive attribute for the organization and depicting its financial

strength. Supporting values of debt to Capital also indicates a positive attribute of the

organization, as its value declined from 0.20 to 0.19 in 2017. However, the overall interest

coverage ratio based on earnings has a relatively declined due to the low profit that was

generated by the organization during 2017 half yearly position. The company was relatively

not able to generate higher profits from its operations to improve the level of interest

coverage ratio. on the other hand, the interest coverage ratio based on cash flow position has

a relatively improved from 10.67 to 24.06 in 2017. This relatively indicates the positive

cashier position of the organization during the fiscal year. Wesfarmers has been maintaining a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.