Financial Accounting Project: Trial Balance, Statements, and Ratios

VerifiedAdded on 2022/12/09

|20

|3563

|52

Homework Assignment

AI Summary

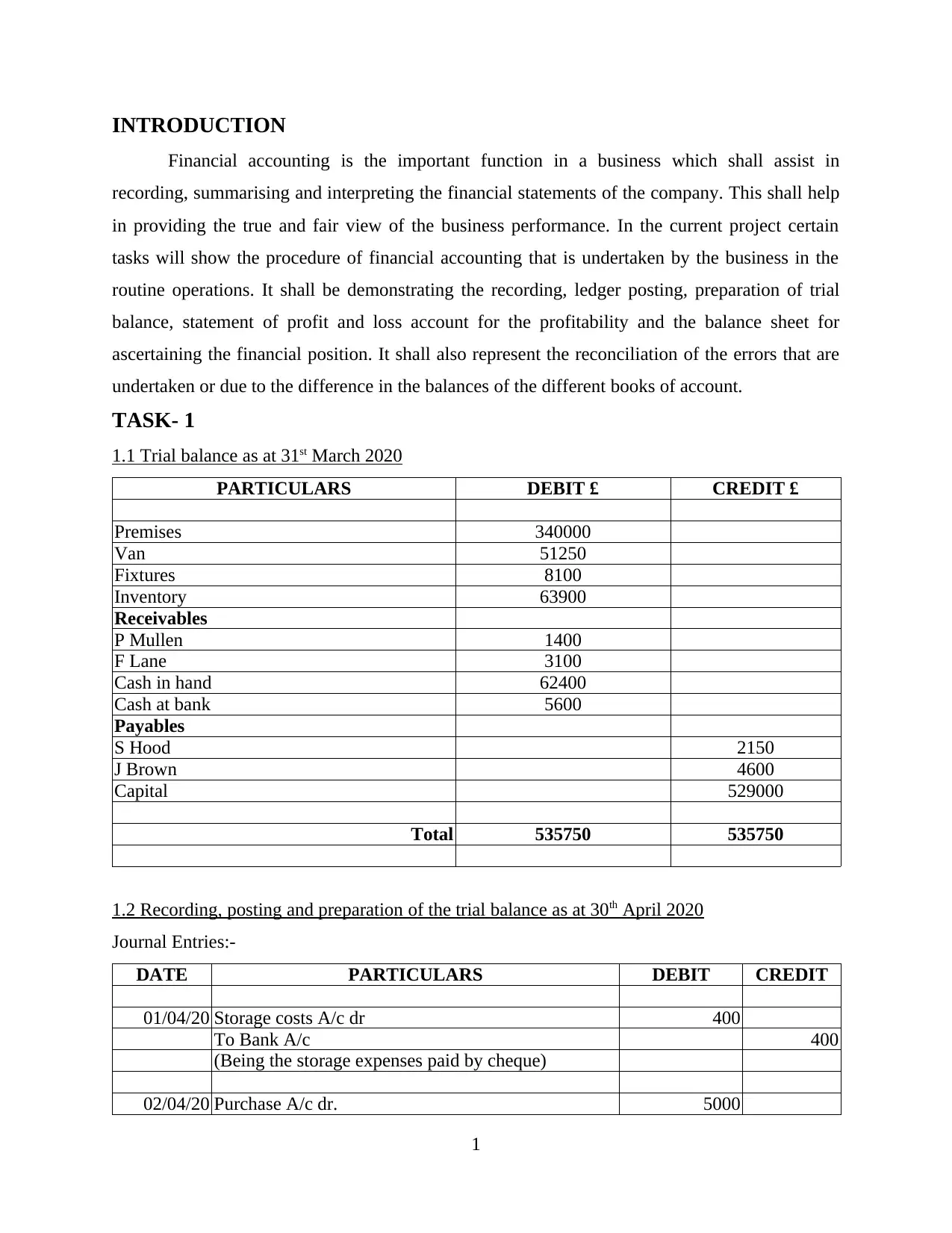

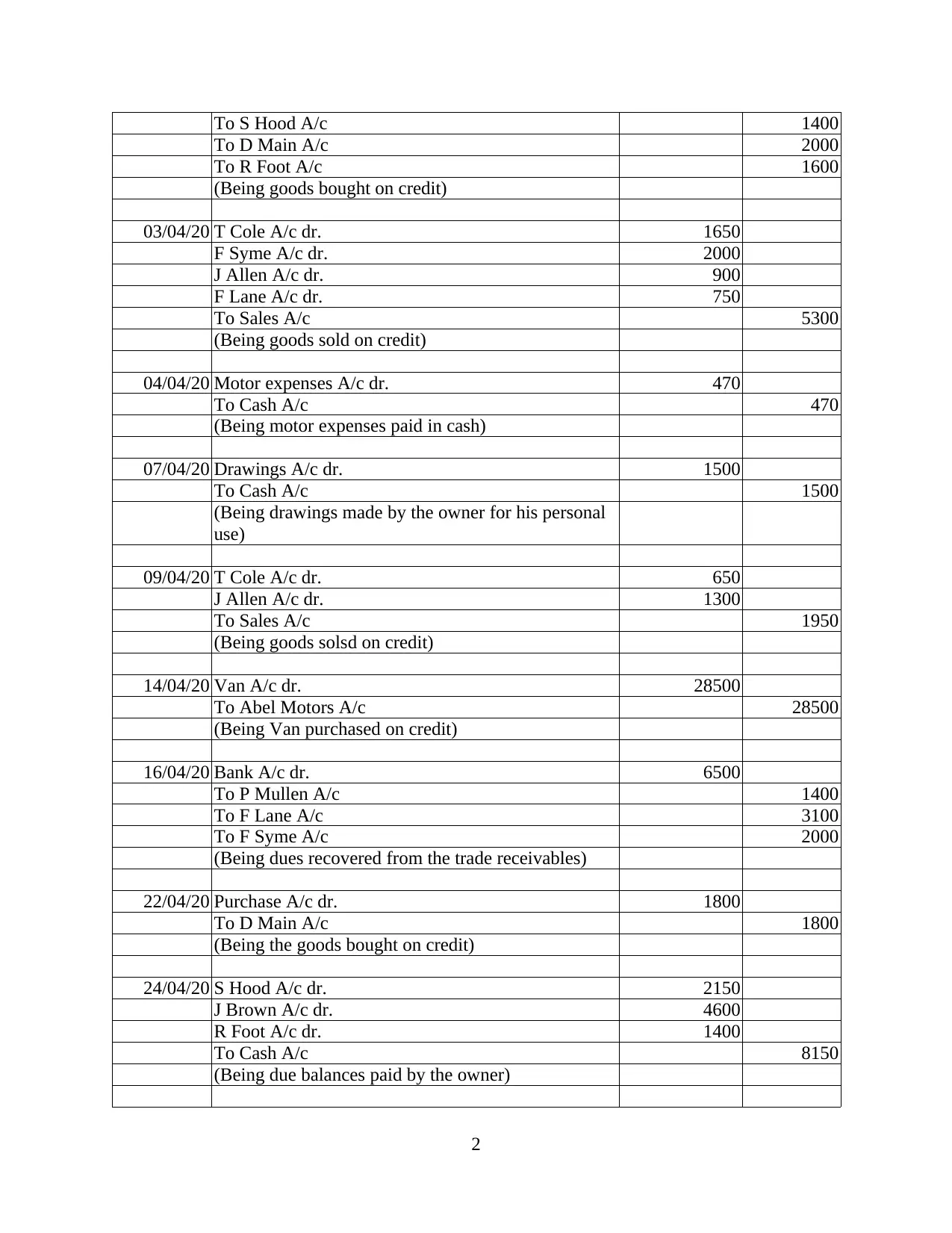

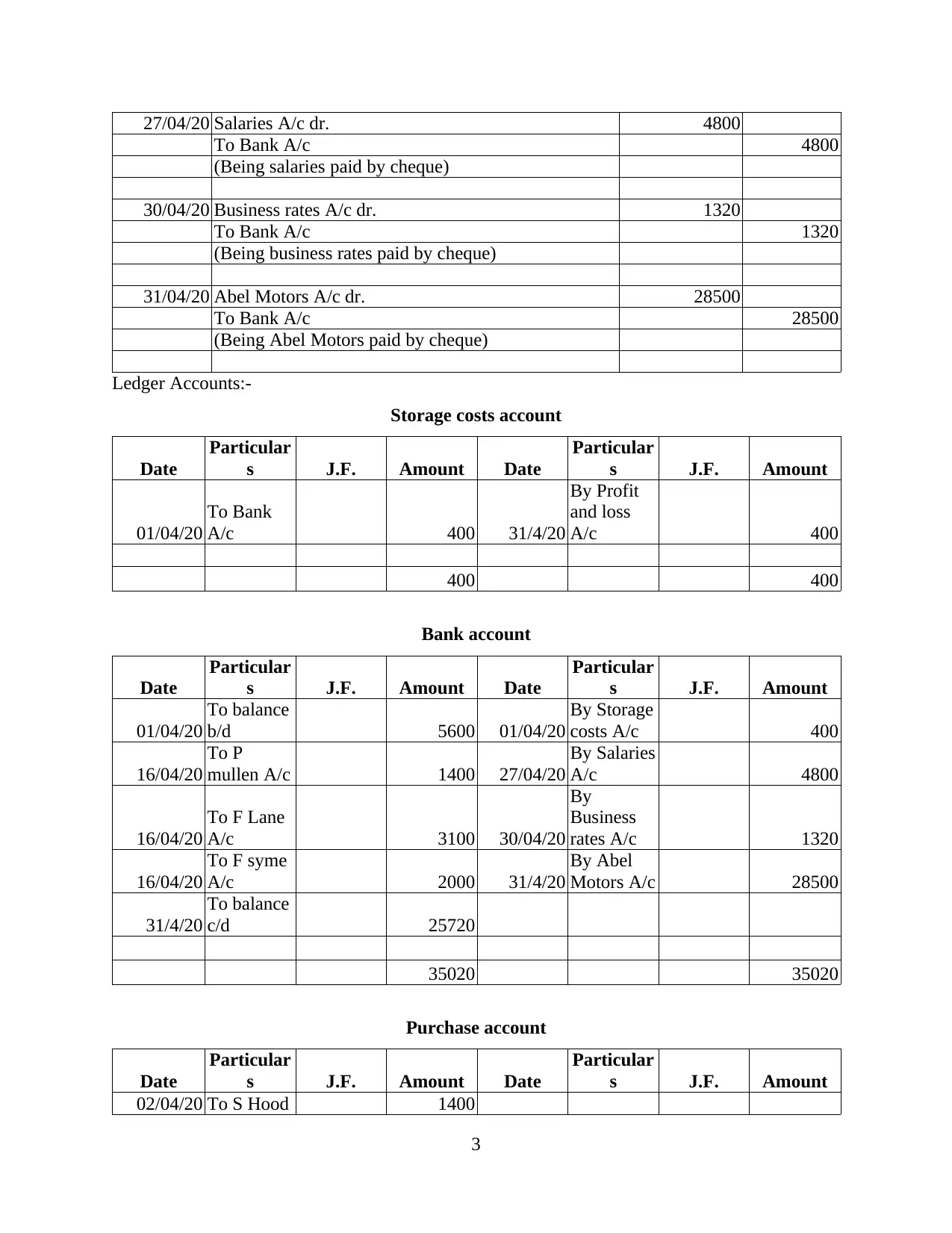

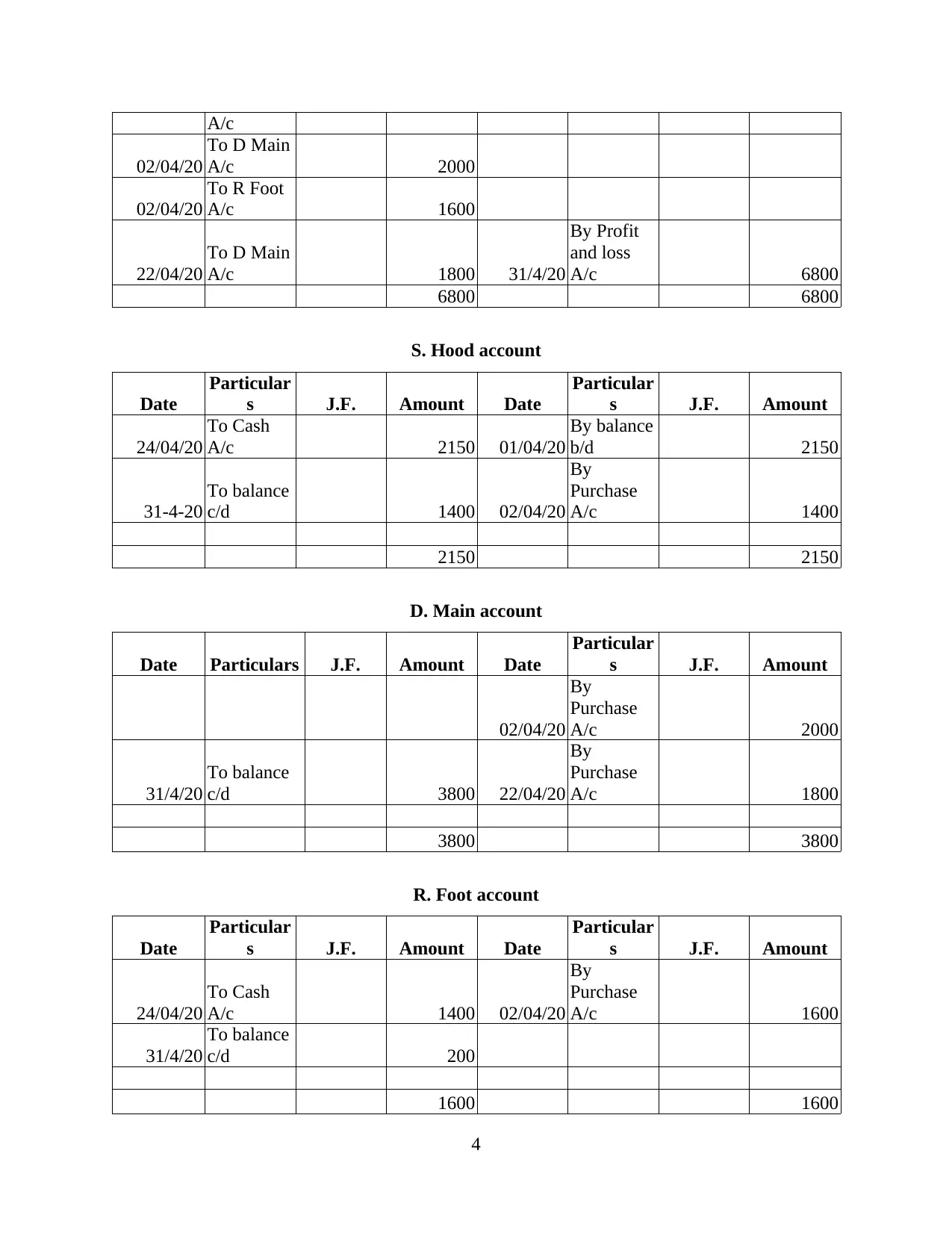

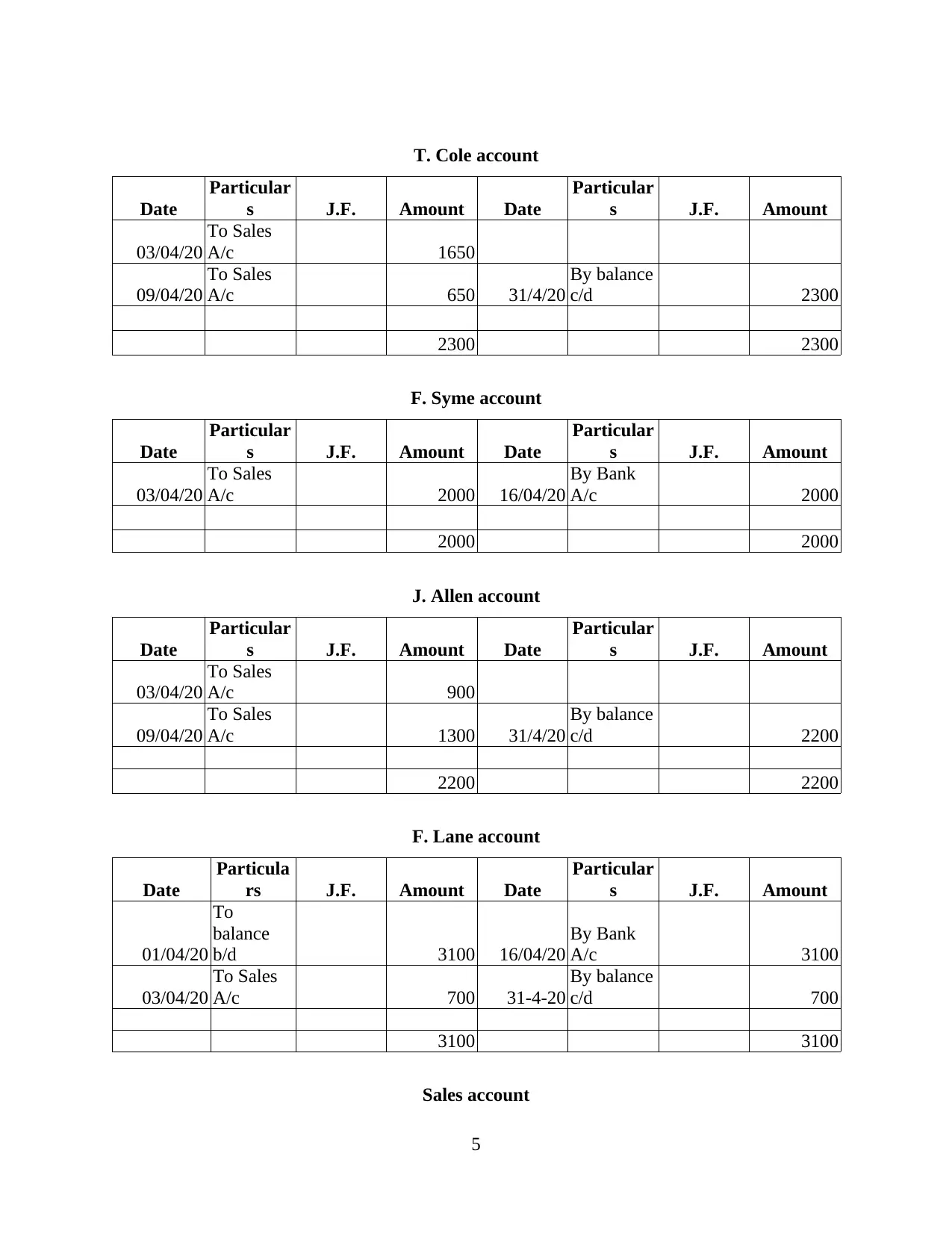

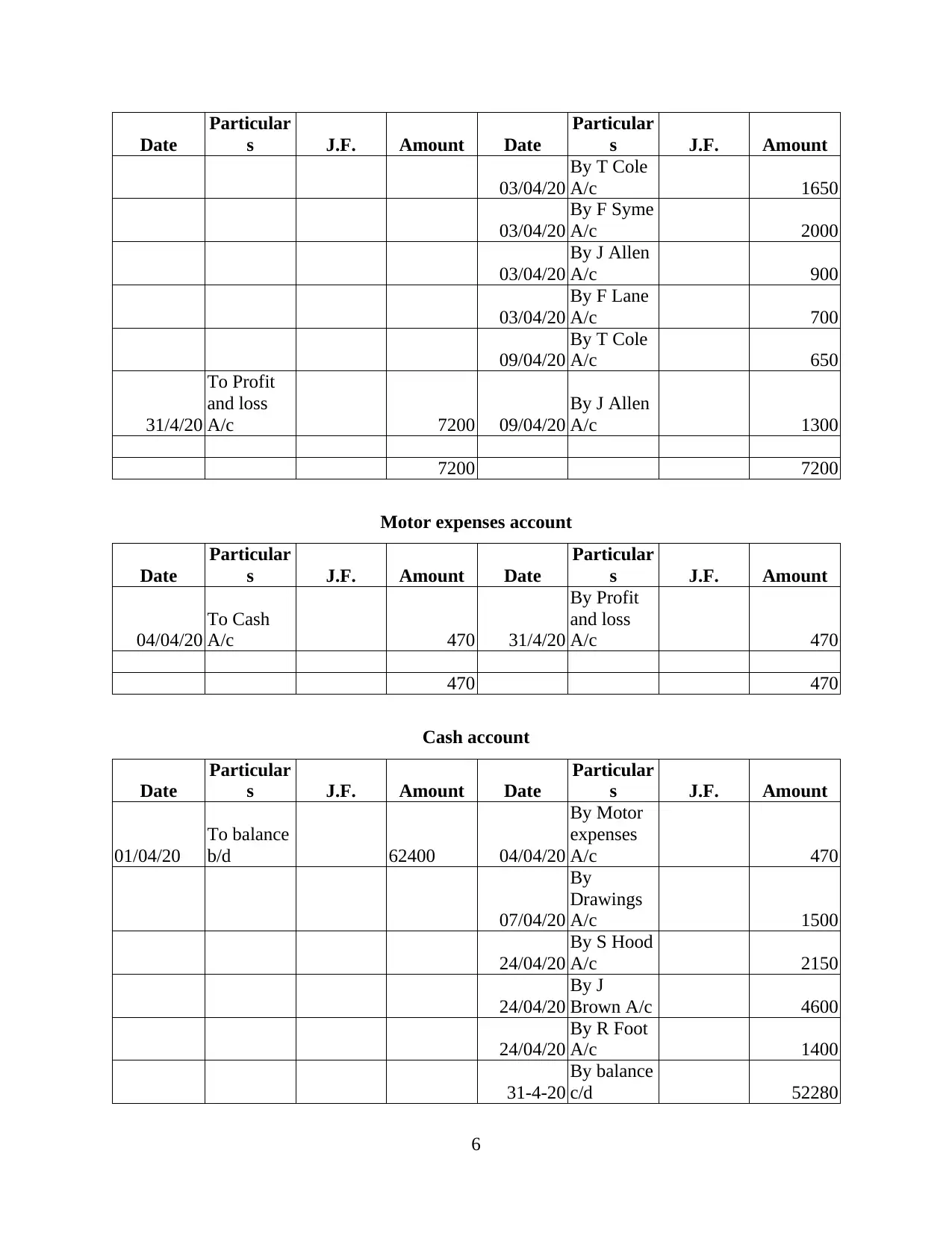

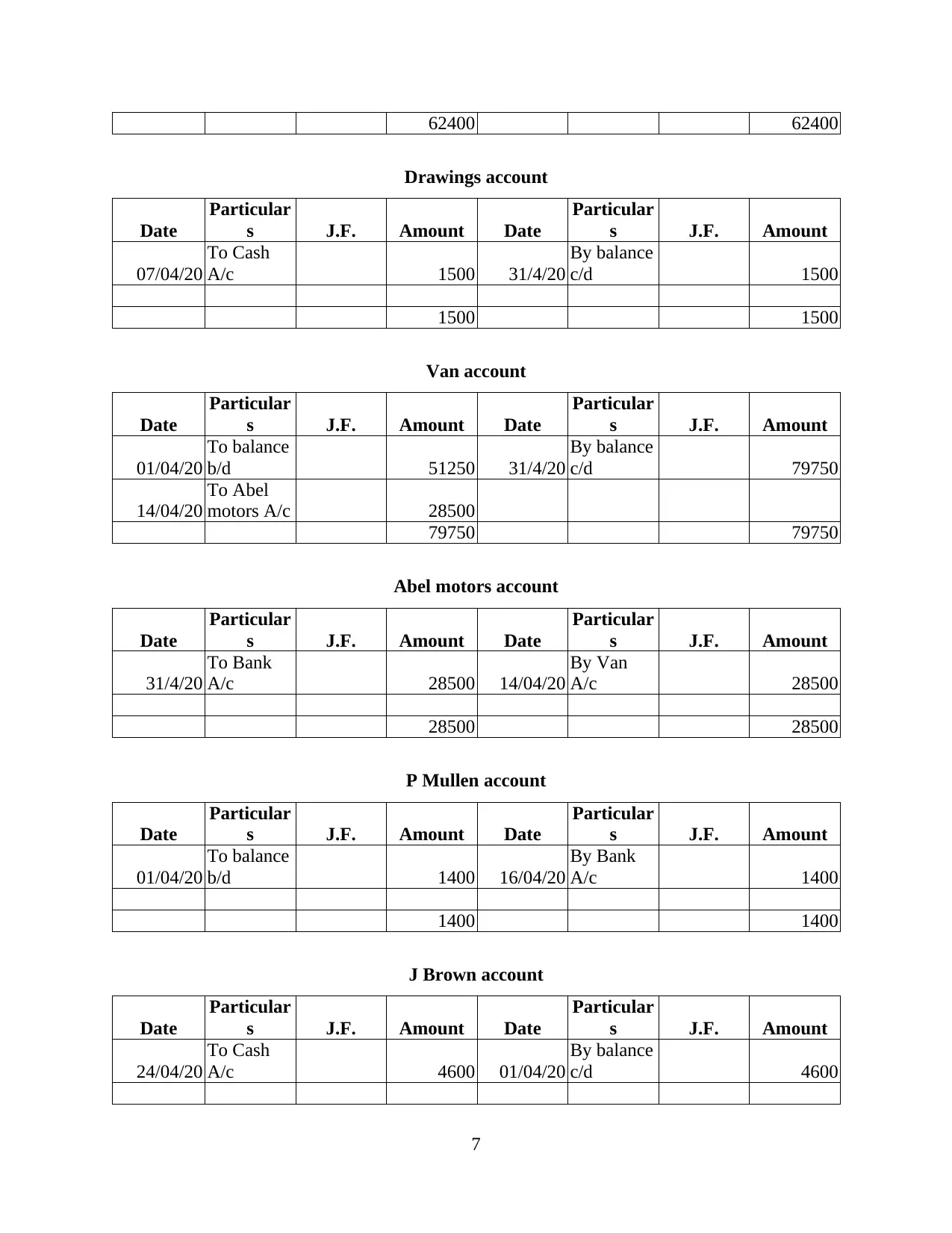

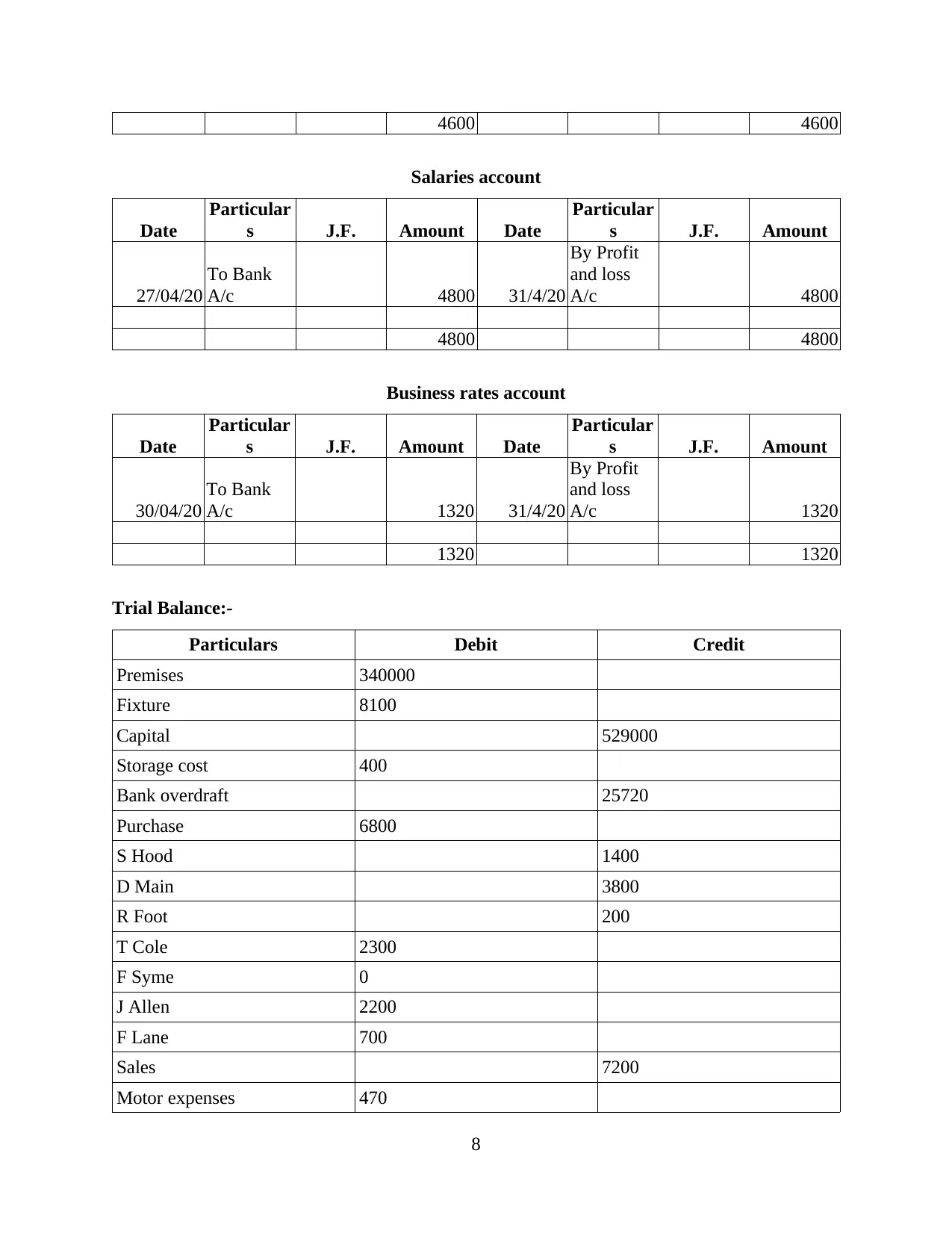

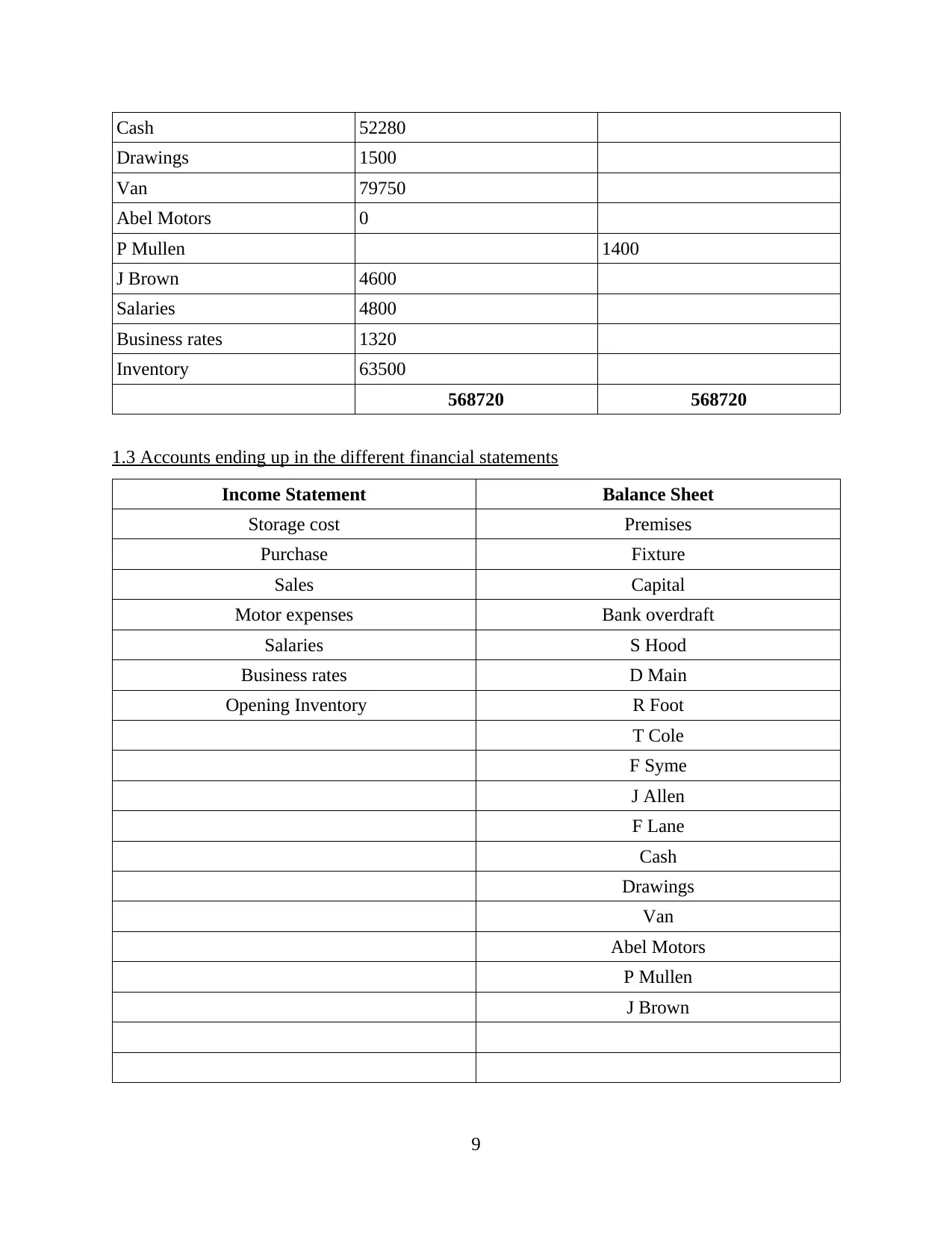

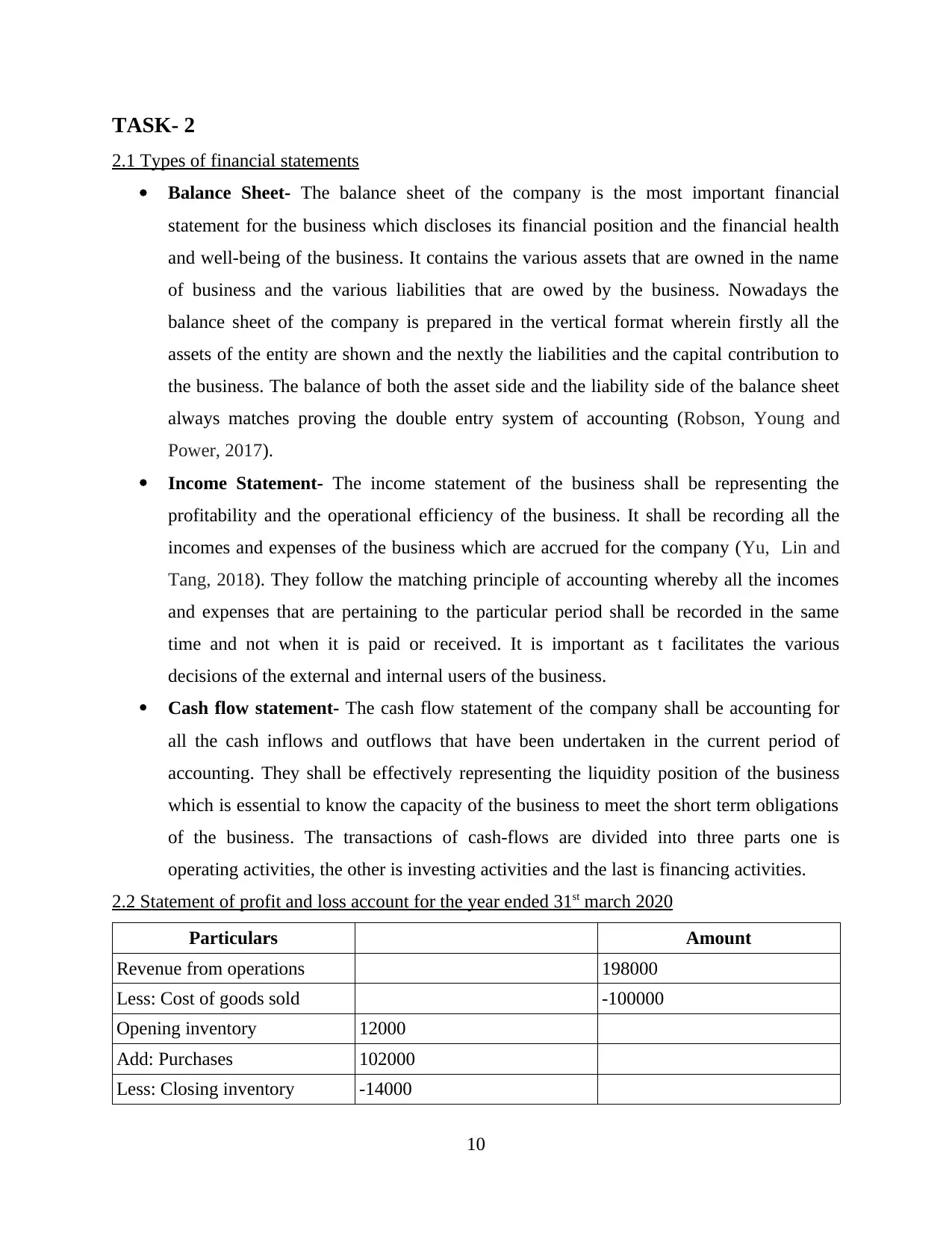

This financial accounting project comprehensively addresses key aspects of financial accounting, starting with the creation of a trial balance as of March 31, 2020, and its subsequent updates for April 30, 2020, including journal entries and ledger postings. The project then delves into the preparation of various financial statements, such as the statement of profit and loss account for the year ending March 31, 2020, and the balance sheet as of the same date, providing a clear depiction of the company's financial performance and position. Furthermore, the project incorporates ratio analysis to evaluate the company's financial health, covering profitability, efficiency, and solvency. A significant portion of the project is dedicated to bank reconciliation, which includes reconciling differences between the company's cash book and bank statements, along with updating the cash book and preparing a bank reconciliation statement. The project concludes with a comprehensive overview of financial accounting principles and practices, offering valuable insights into the recording, summarizing, and interpreting of financial data.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.