ACC104 Accounting for Decisions 2: Financial Statement Analysis

VerifiedAdded on 2023/03/31

|4

|1085

|160

Homework Assignment

AI Summary

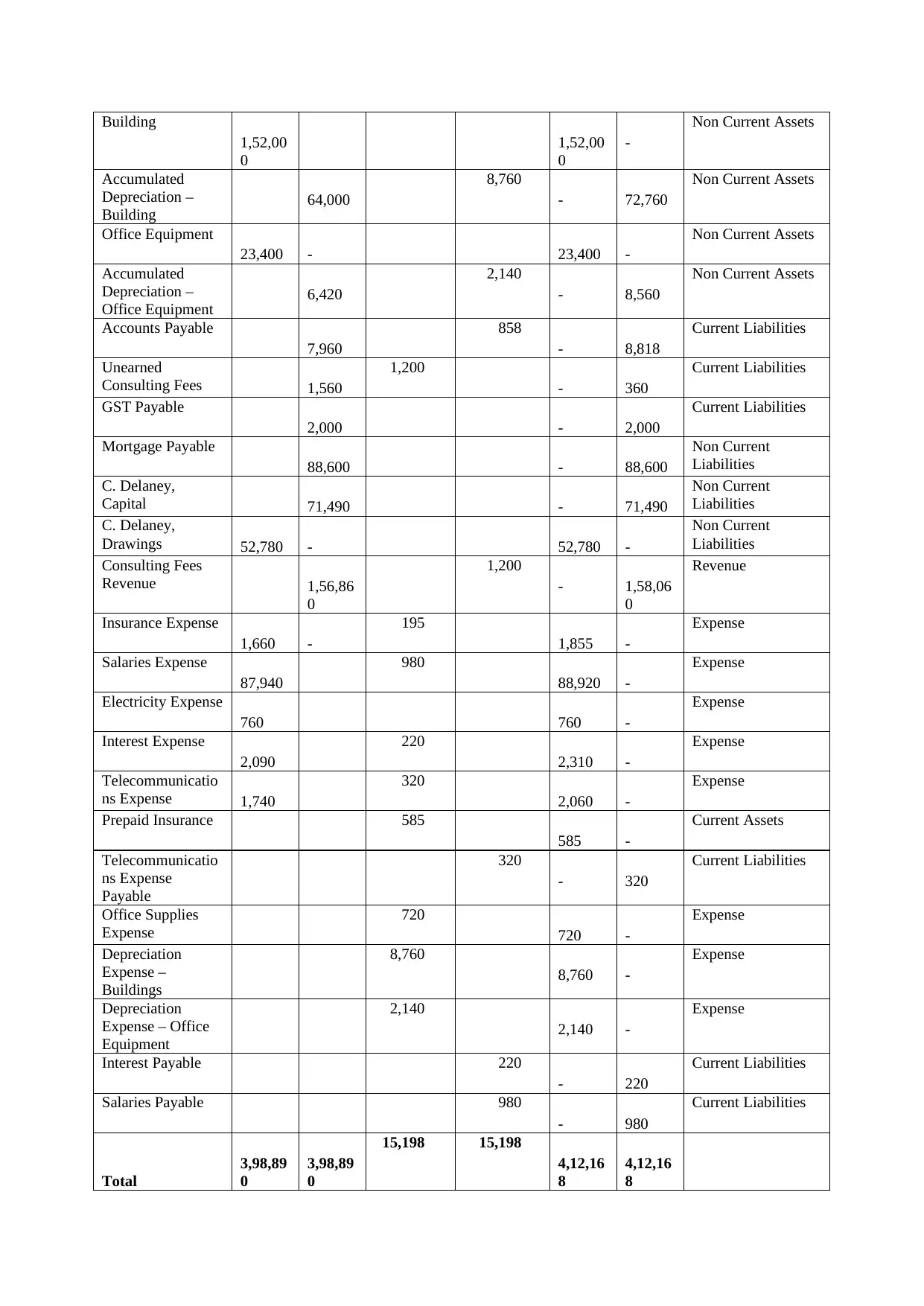

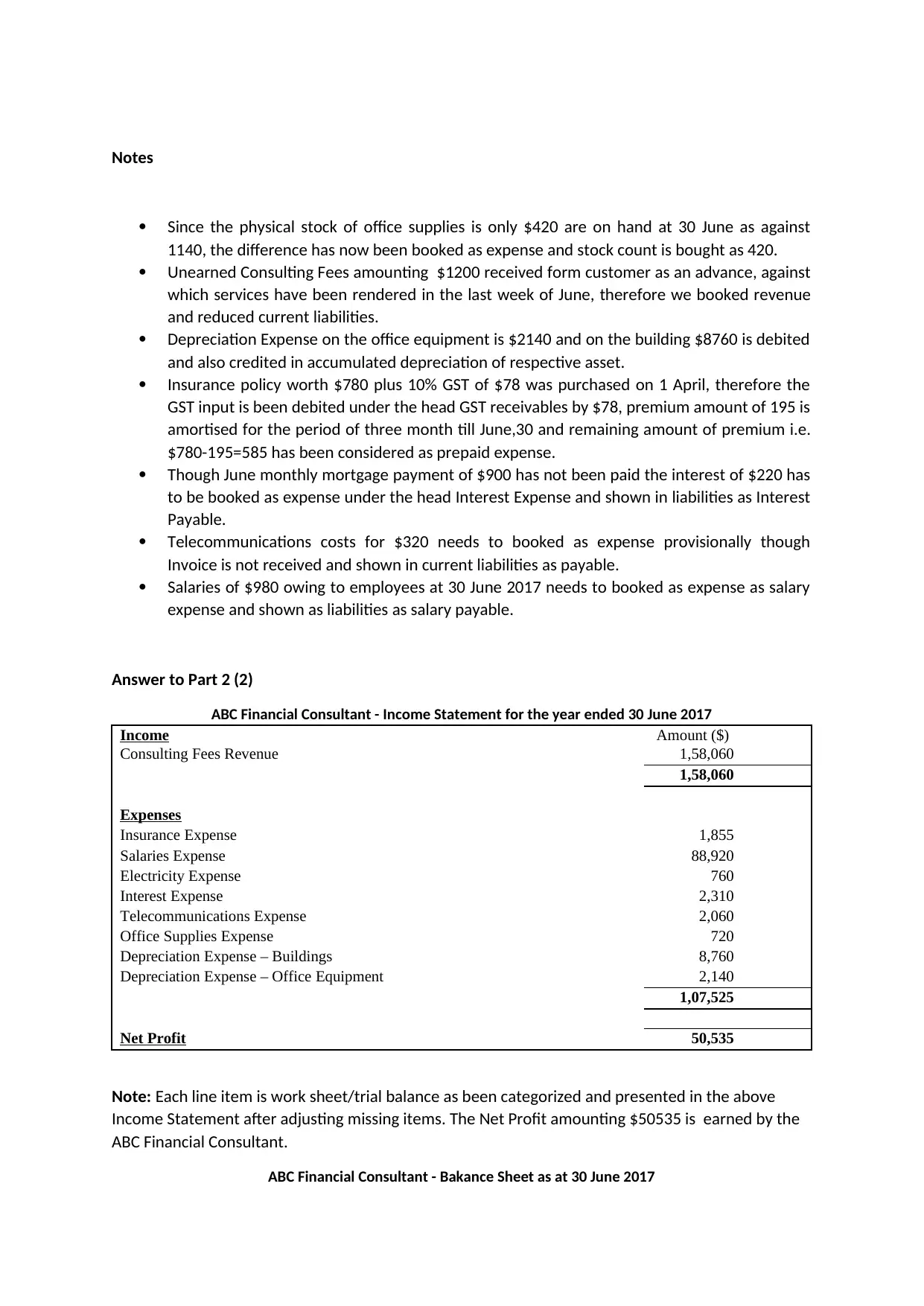

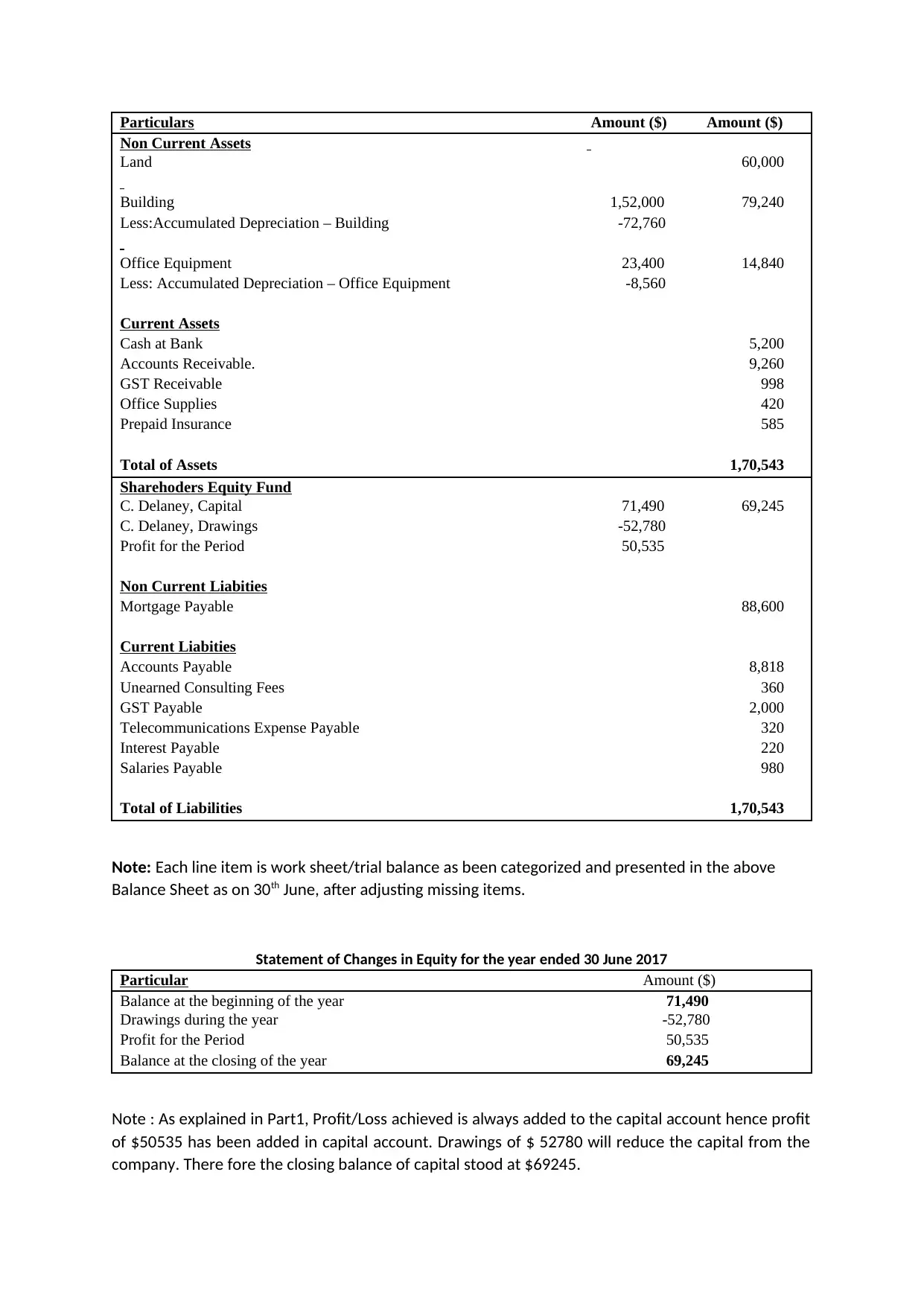

This assignment solution addresses the core concepts of financial statement analysis within the context of ACC104, focusing on the relationship between the balance sheet and income statement, and the process of creating financial statements. The solution begins with a concise explanation of the balance sheet, detailing the structure of assets, liabilities, and equity, and the income statement, highlighting revenue, expenses, and profit. The second part presents a detailed worksheet, income statement, balance sheet, and statement of changes in equity for ABC Financial Consultant. It includes journal entries for adjusting entries, such as depreciation, prepaid insurance, unearned revenue, and accrued expenses. The solution demonstrates the preparation of the financial statements based on the provided trial balance and adjustments, showcasing the net profit, and the final financial position of the company. The assignment provides a complete walkthrough of financial statement preparation, from the unadjusted trial balance to the final statements, illustrating the impact of adjustments on the financial position and performance of a business.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.