Accounting for Government and Non-Profit: Journal Entries

VerifiedAdded on 2020/05/16

|6

|939

|53

Homework Assignment

AI Summary

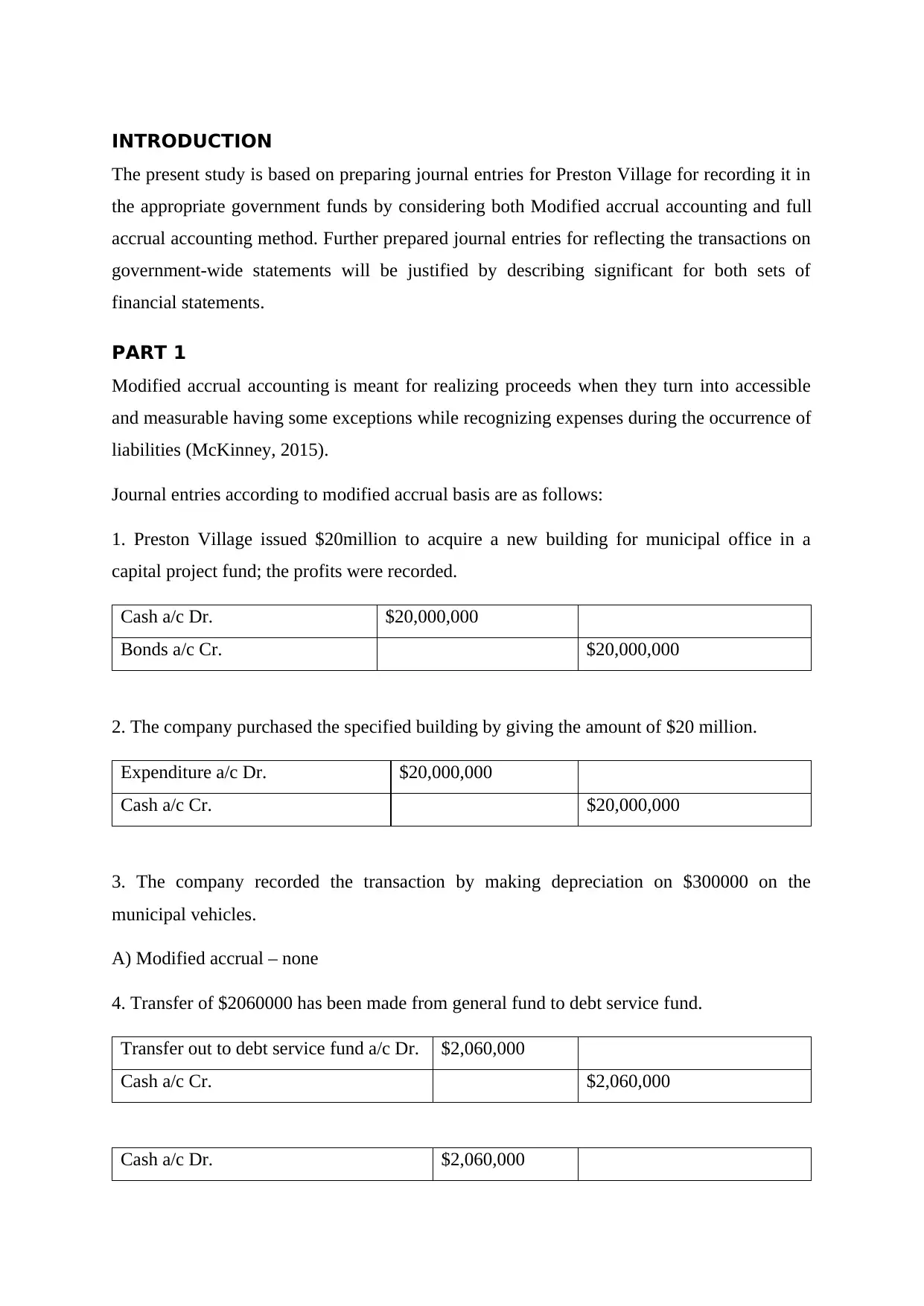

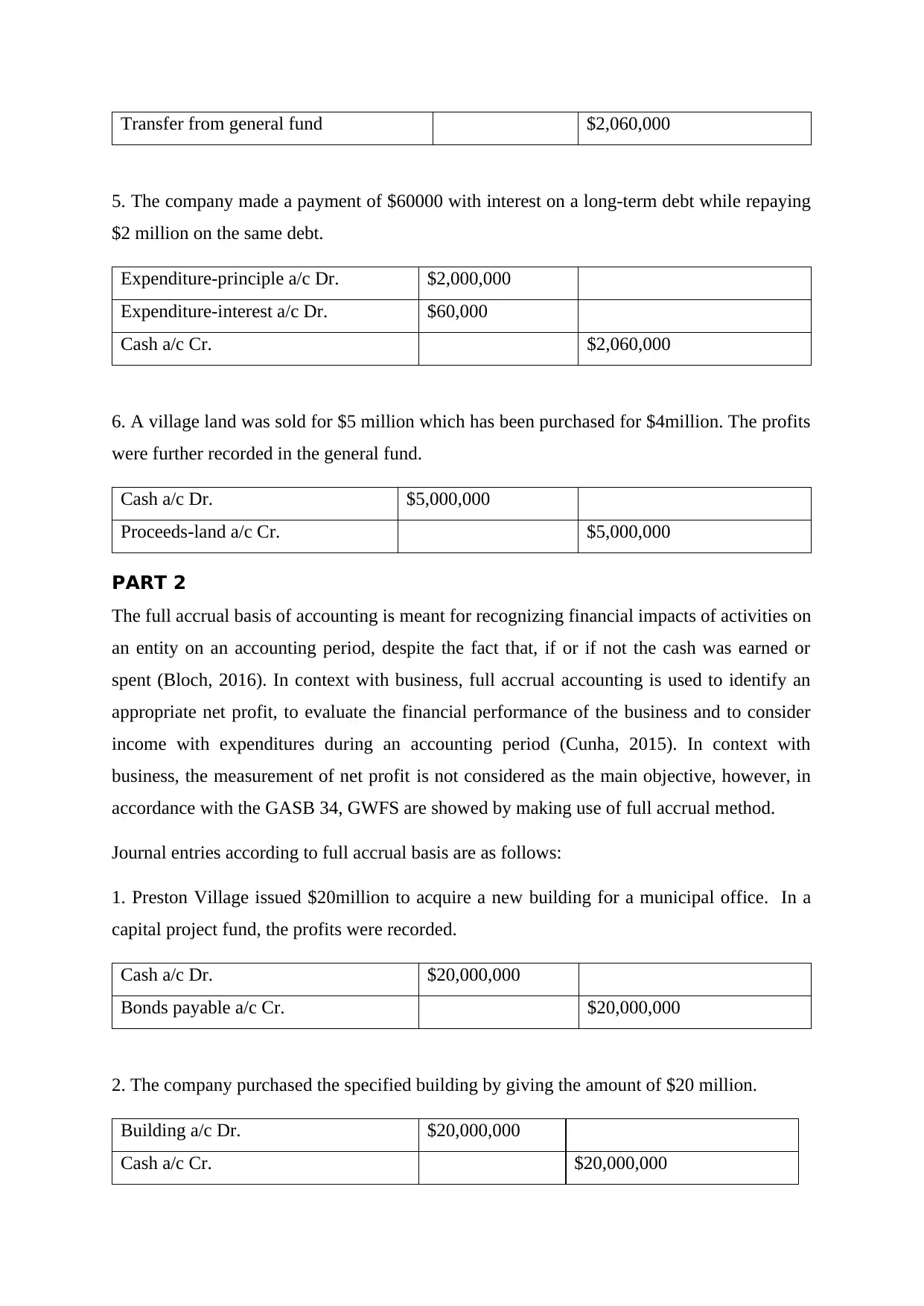

This assignment solution focuses on government and non-profit accounting, specifically addressing the preparation of journal entries for Preston Village using both modified accrual and full accrual accounting methods. The solution details journal entries for various transactions, including bond issuance, building purchases, depreciation, fund transfers, debt payments, and land sales. Part 1 presents journal entries under the modified accrual basis, while Part 2 demonstrates the same transactions using the full accrual method. The assignment also justifies the preparation of two sets of financial statements, one reflecting budgetary requirements and the other presenting the entity as a whole, emphasizing inter-period equity. The conclusion highlights the importance of accurate accounting practices for government entities, similar to corporate entities, and references relevant accounting principles and standards, including GASB 34.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.