Financial Accounting: Bank Reconciliation and Control Accounts

VerifiedAdded on 2020/11/09

|19

|2547

|48

Homework Assignment

AI Summary

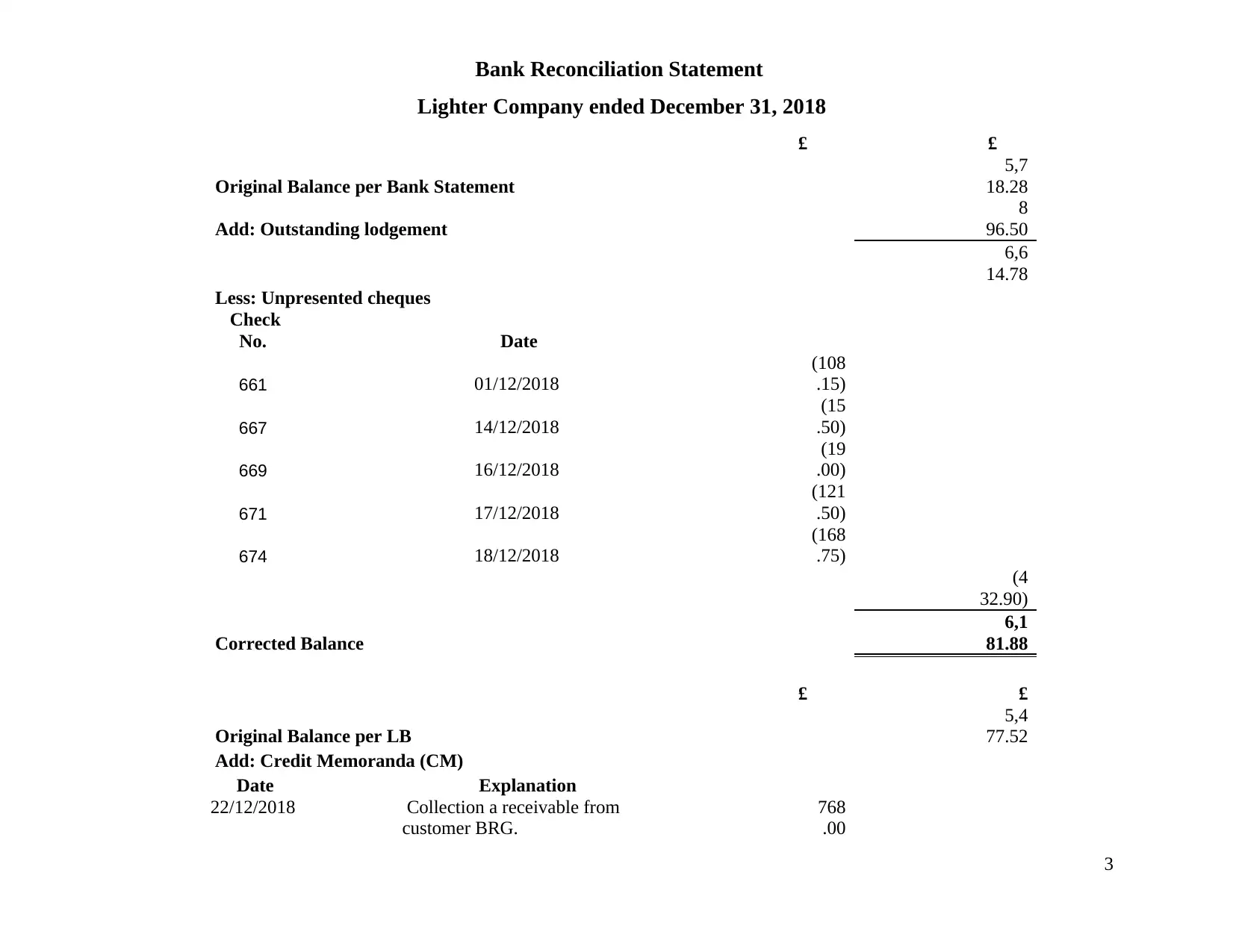

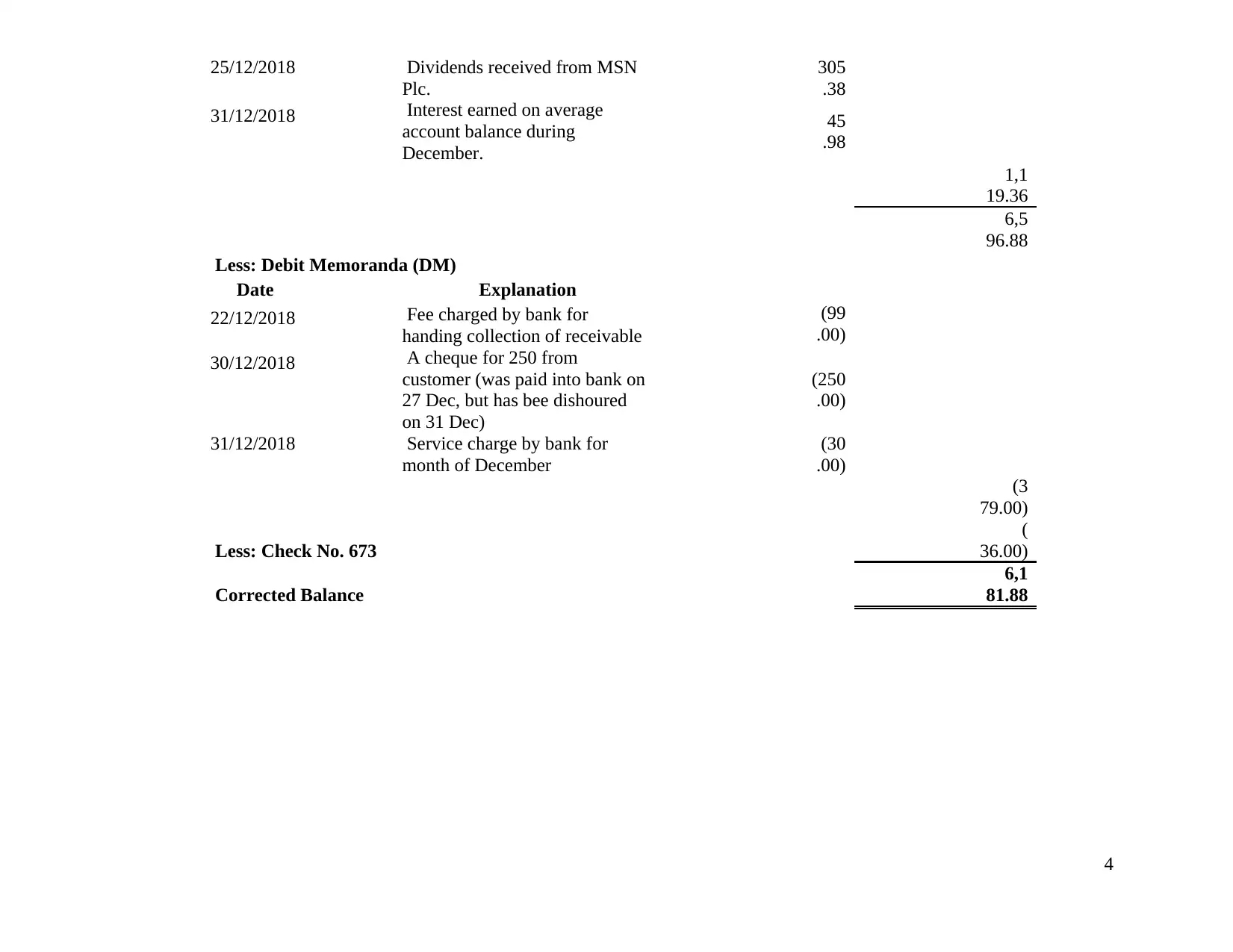

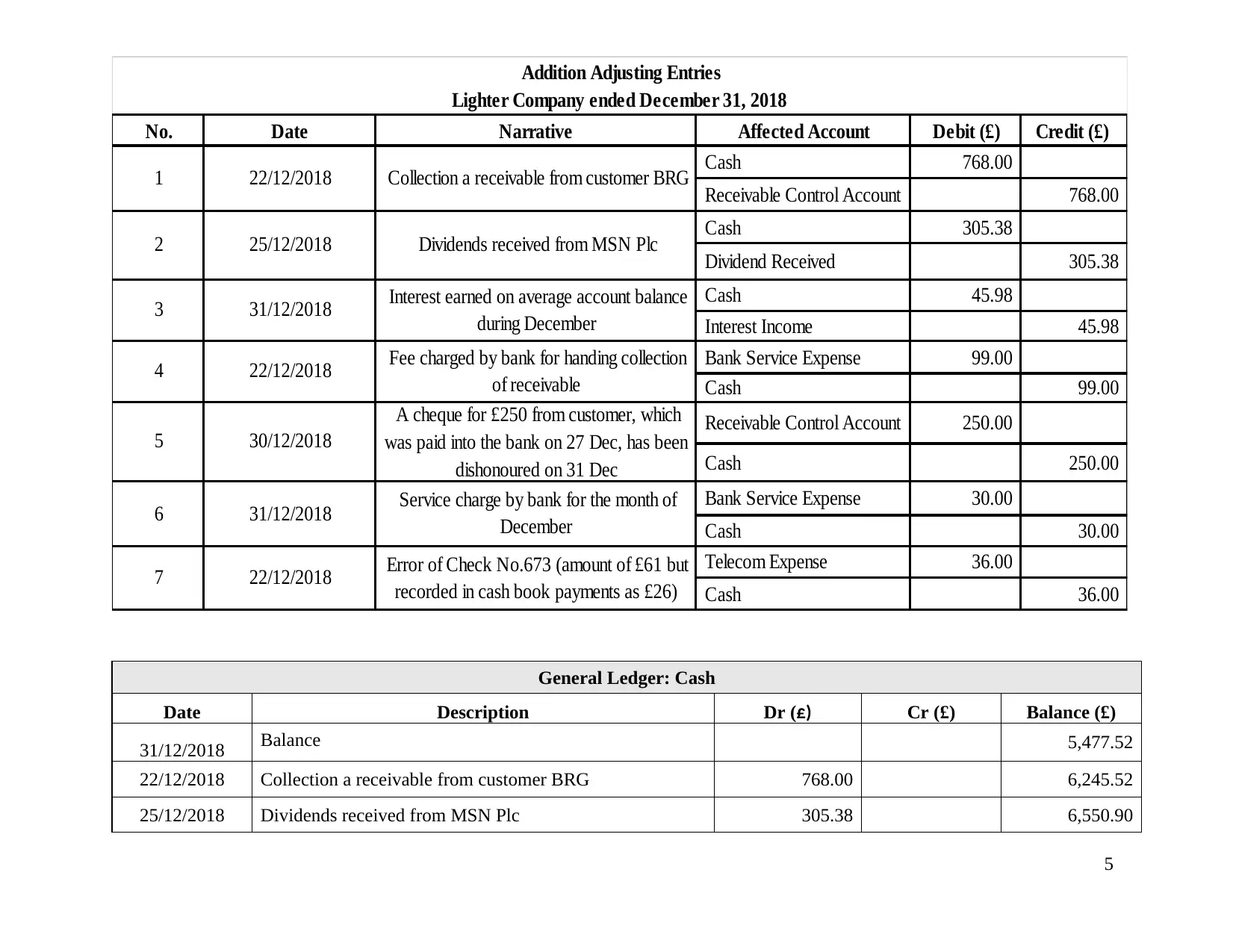

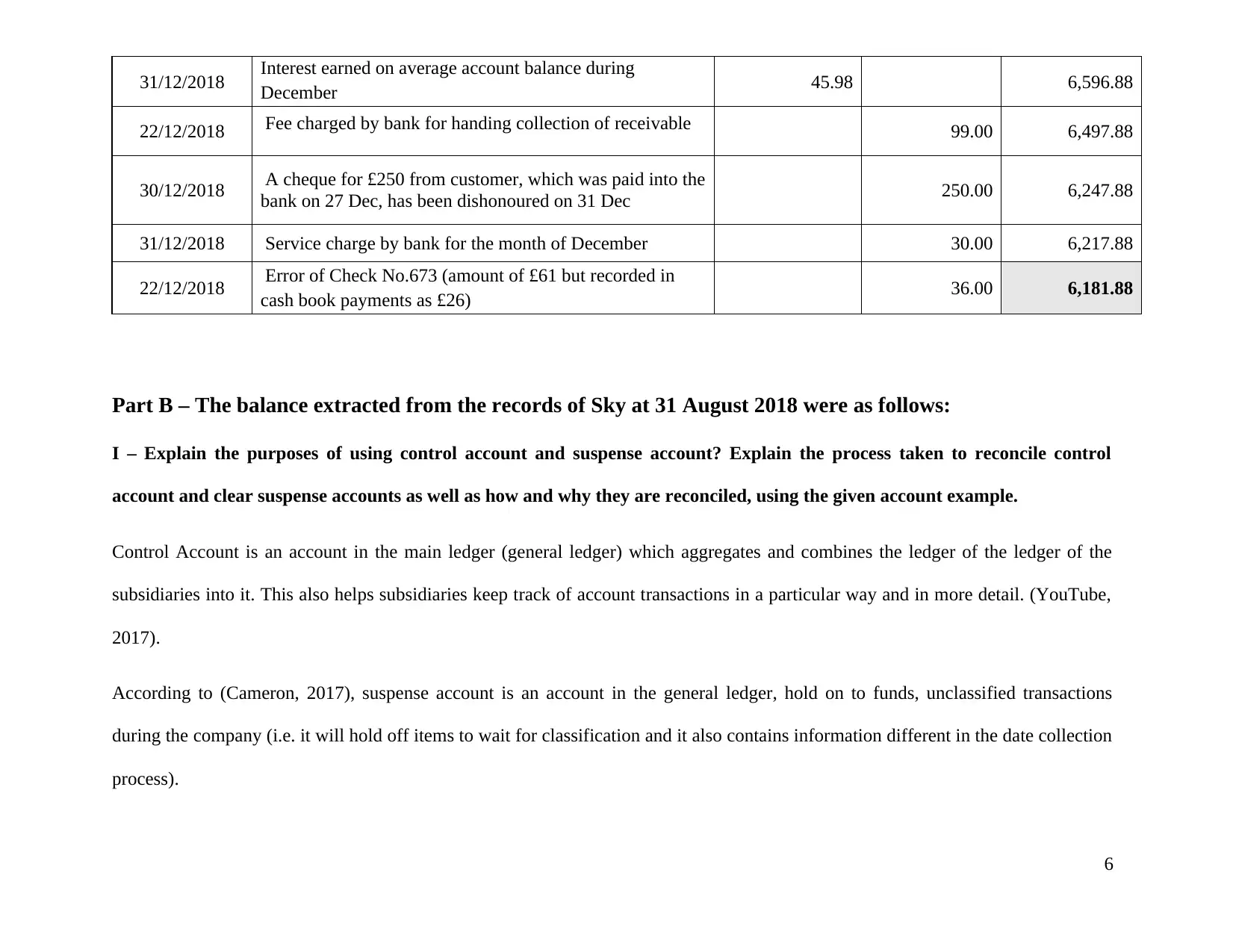

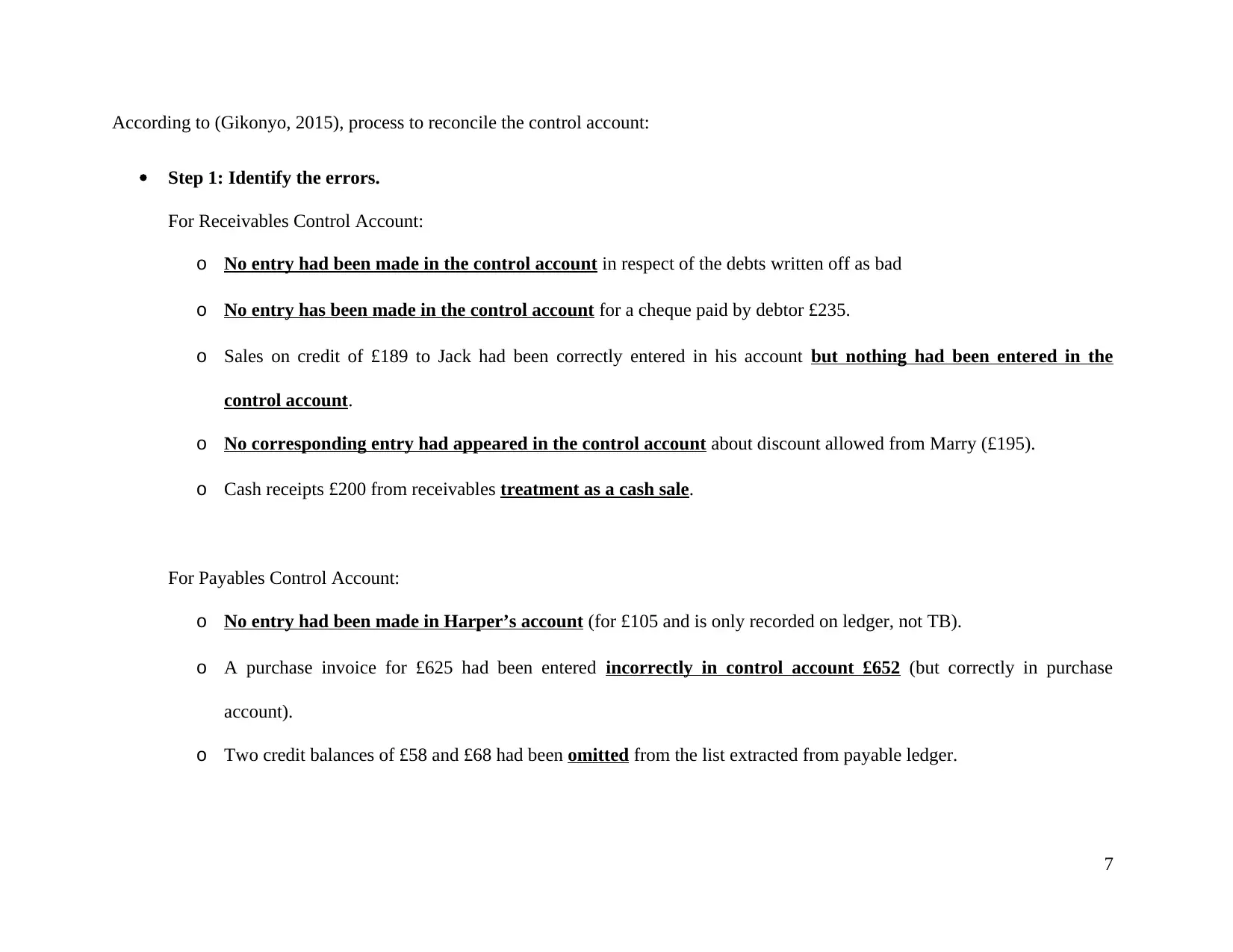

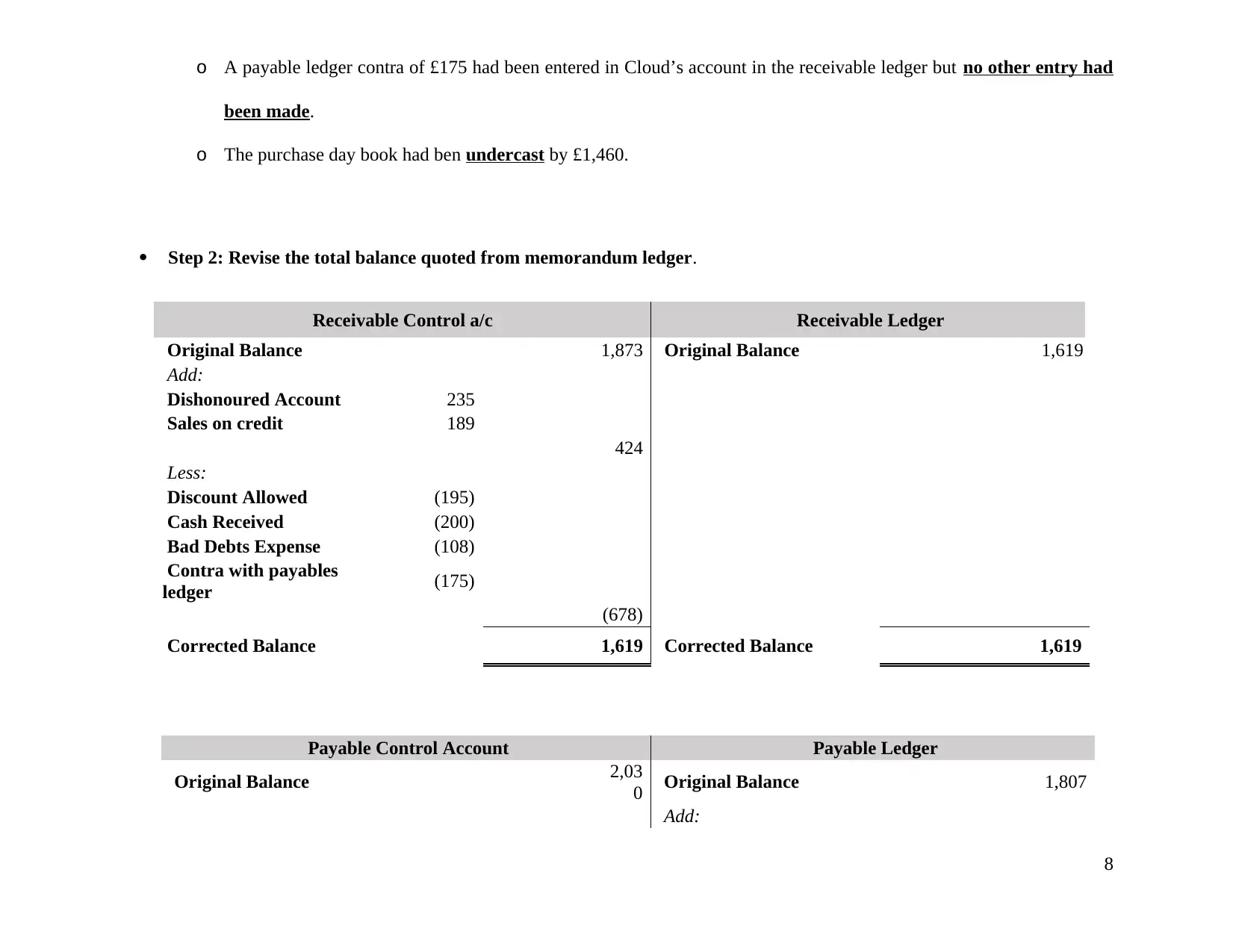

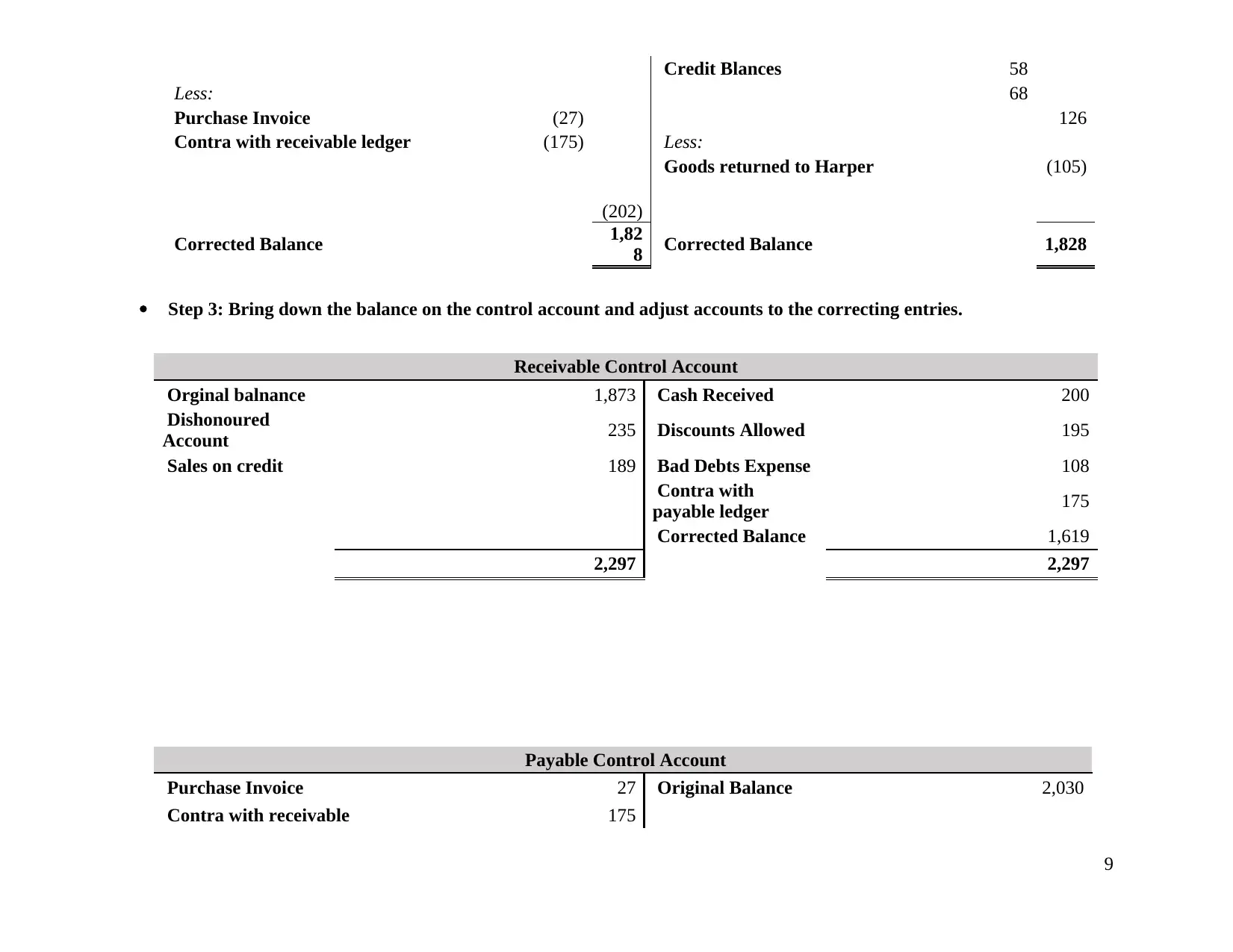

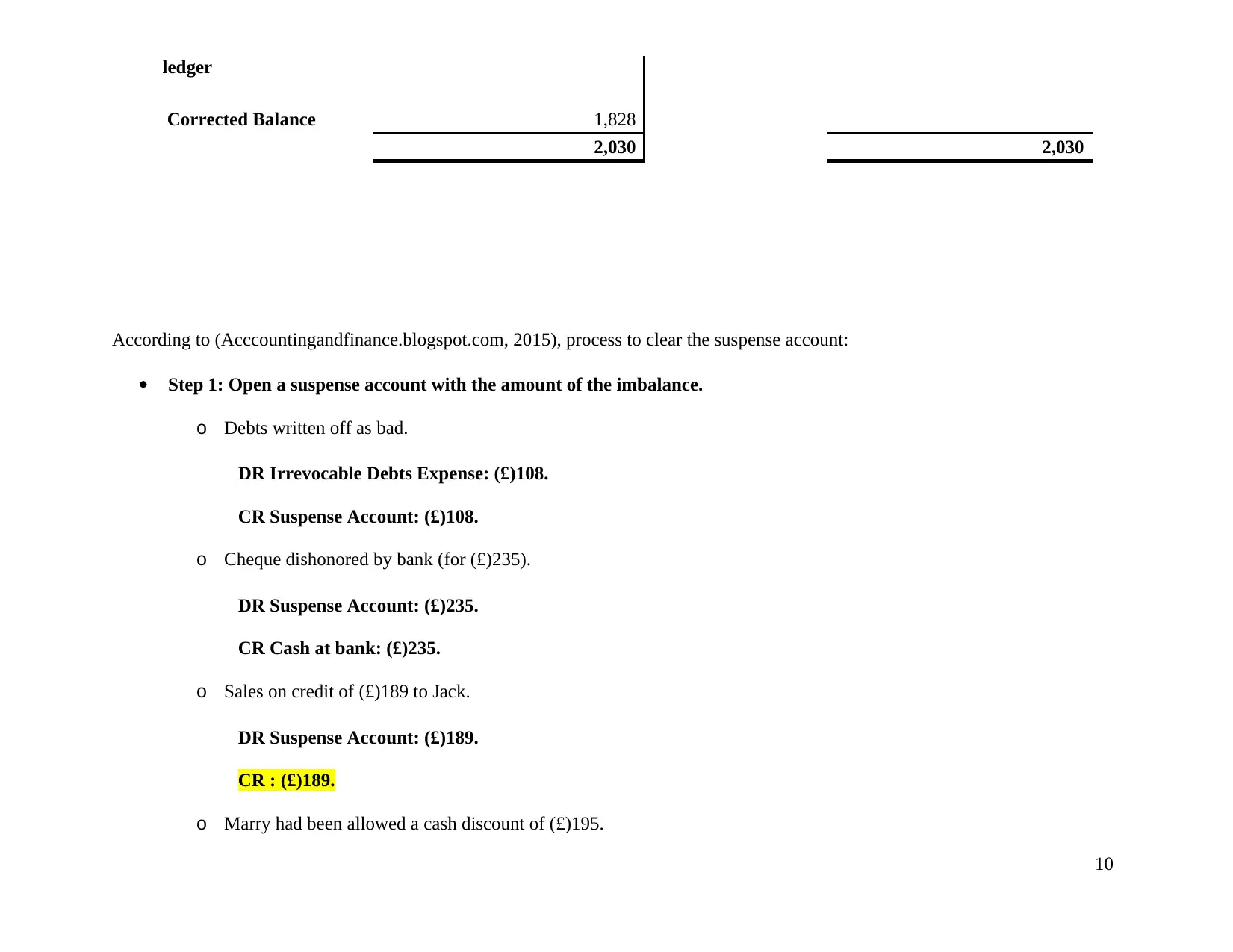

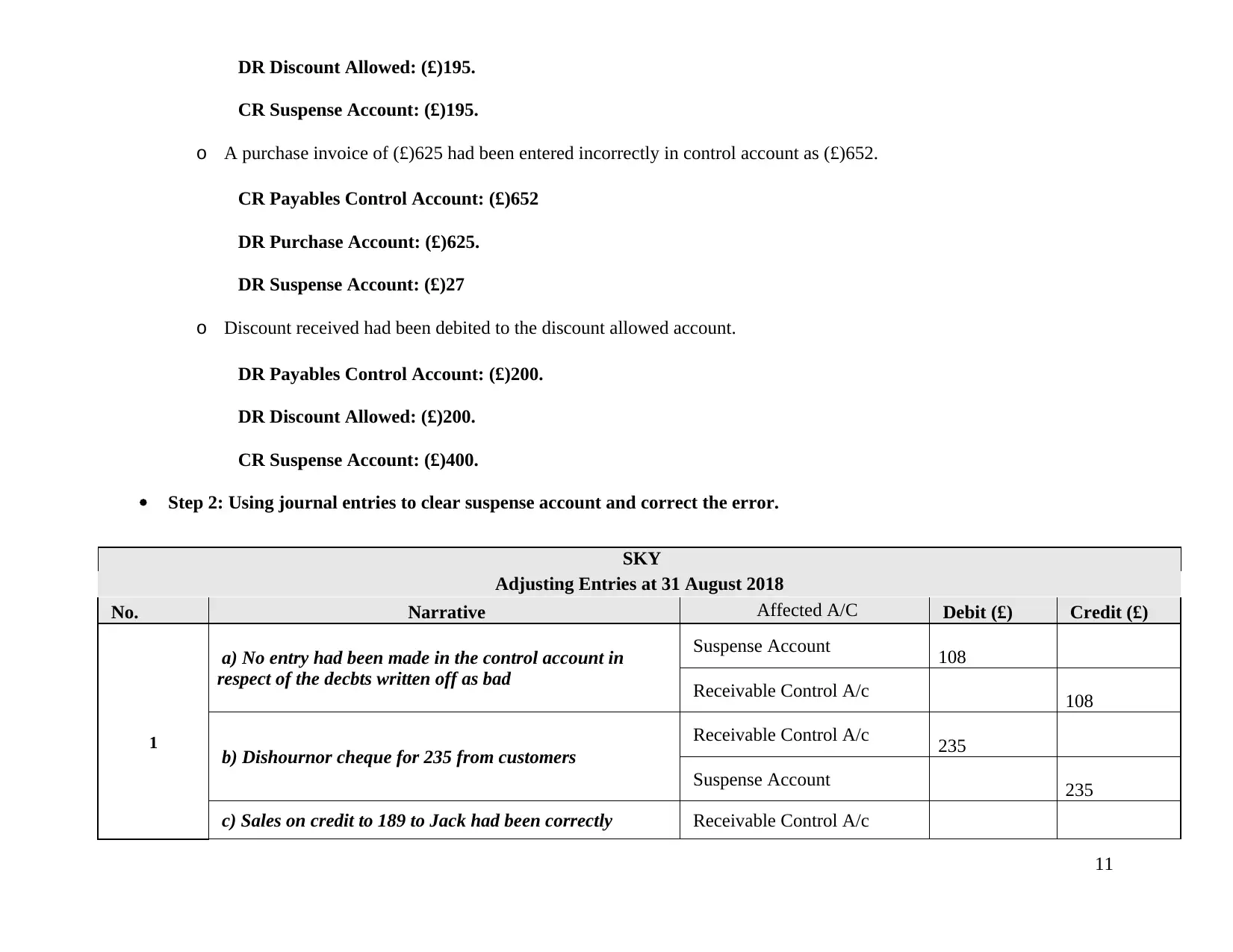

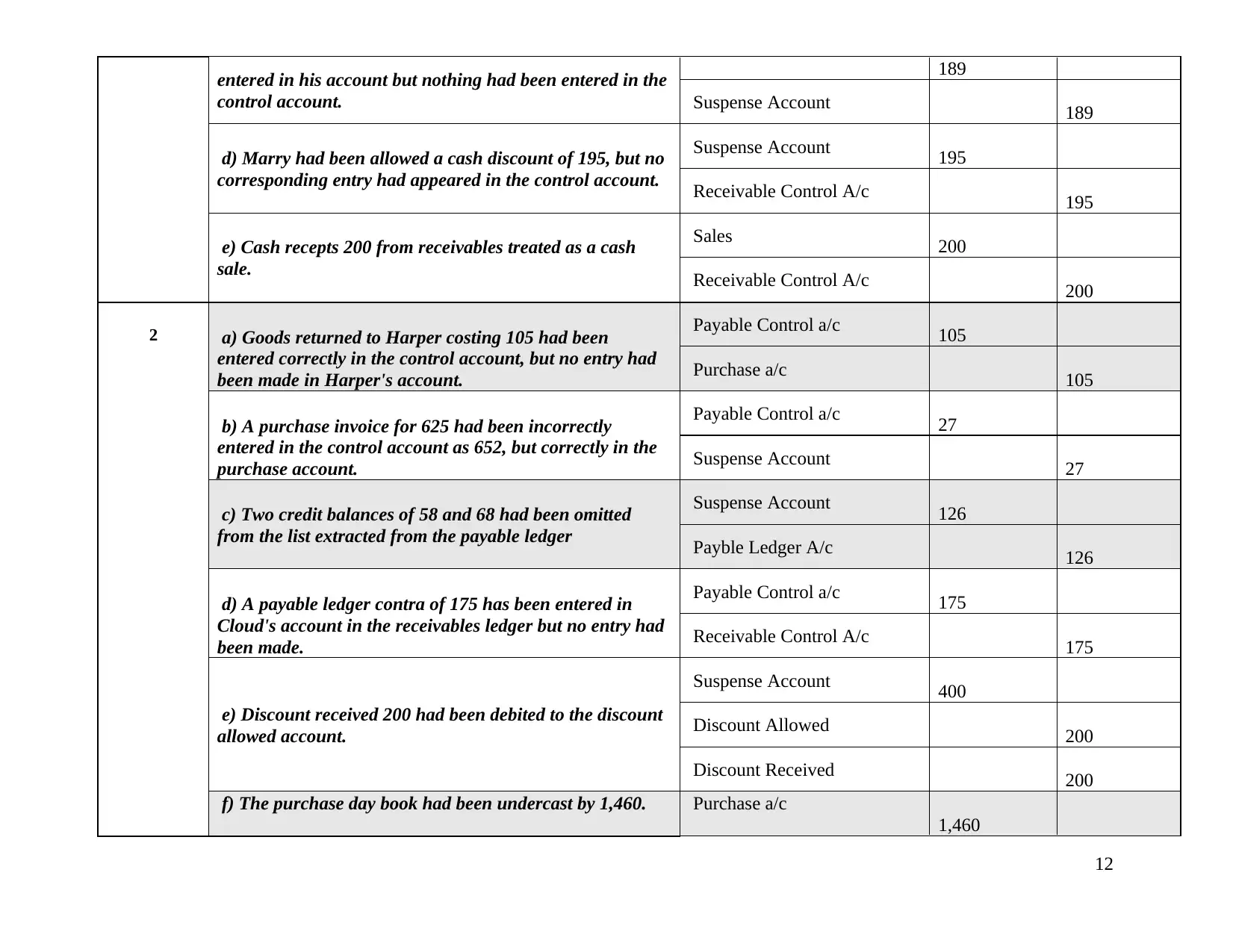

This financial accounting assignment solution, submitted by a student, is divided into two parts. Part A focuses on preparing a bank reconciliation statement and adjusting entries for Lighter Company, based on provided bank transaction information. The solution includes the bank reconciliation statement, along with the necessary debit and credit memoranda, and the corrected balance. Part B delves into control accounts and suspense accounts, explaining their purposes and the process of reconciliation. The solution details the steps to reconcile control accounts and clear suspense accounts, using the example of Sky's financial records. It provides a detailed analysis of the adjustments required, including journal entries, and presents the unadjusted and adjusted trial balances, along with the statement of profit or loss, statement of retained earnings, and statement of financial position. This comprehensive solution provides a clear understanding of the financial accounting principles and practices involved.

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.