Financial Statement Analysis and Investment Appraisal Report

VerifiedAdded on 2021/02/21

|17

|5128

|72

Report

AI Summary

This report provides an in-depth analysis of financial statements, including income statements and balance sheets, for Yarnshaw Limited. It covers the calculation of key financial metrics and the preparation of these statements. The report further delves into management accounting concepts, models, and techniques, using Reckturk Plc as a case study to illustrate break-even analysis, margin of safety, and profit calculations. It also explores various investment appraisal techniques, their merits, demerits, and the benefits and limitations of budgeting. The report aims to provide a comprehensive understanding of financial accounting, management accounting, and investment decision-making processes. It includes detailed working notes and calculations to support the financial analyses presented.

INTRODUCTION TO

ACCOUNTING AND

FINANCE

ACCOUNTING AND

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

PART A -Yarnshaw Limited...........................................................................................................1

PART B – Reckturk Plc...................................................................................................................5

PART C............................................................................................................................................9

A. Calculation of investment appraisal techniques......................................................................9

B. Merits and demerits of different investment appraisal techniques........................................11

C. Explain the benefits and limitation of Budget.......................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

PART A -Yarnshaw Limited...........................................................................................................1

PART B – Reckturk Plc...................................................................................................................5

PART C............................................................................................................................................9

A. Calculation of investment appraisal techniques......................................................................9

B. Merits and demerits of different investment appraisal techniques........................................11

C. Explain the benefits and limitation of Budget.......................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

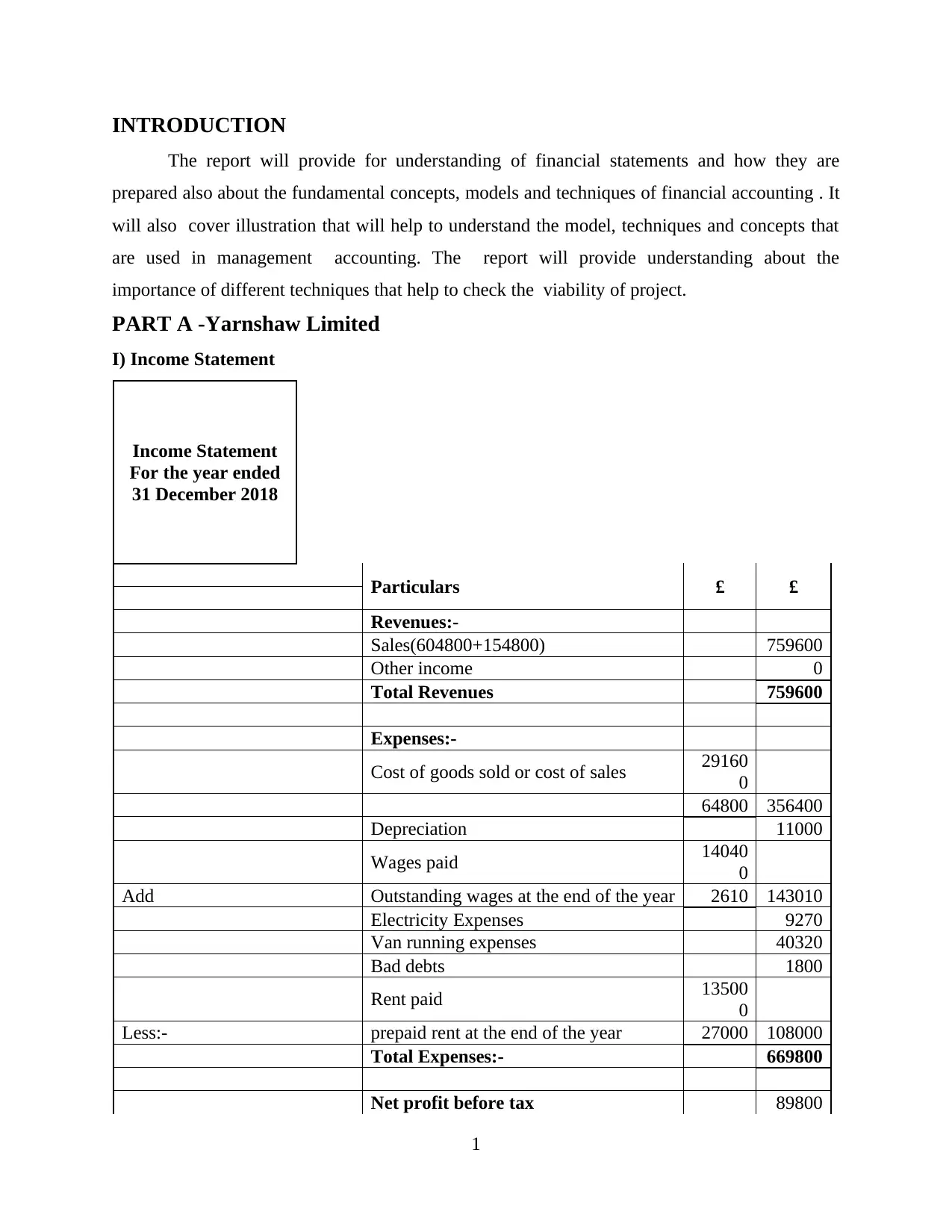

INTRODUCTION

The report will provide for understanding of financial statements and how they are

prepared also about the fundamental concepts, models and techniques of financial accounting . It

will also cover illustration that will help to understand the model, techniques and concepts that

are used in management accounting. The report will provide understanding about the

importance of different techniques that help to check the viability of project.

PART A -Yarnshaw Limited

I) Income Statement

Income Statement

For the year ended

31 December 2018

Particulars £ £

Revenues:-

Sales(604800+154800) 759600

Other income 0

Total Revenues 759600

Expenses:-

Cost of goods sold or cost of sales 29160

0

64800 356400

Depreciation 11000

Wages paid 14040

0

Add Outstanding wages at the end of the year 2610 143010

Electricity Expenses 9270

Van running expenses 40320

Bad debts 1800

Rent paid 13500

0

Less:- prepaid rent at the end of the year 27000 108000

Total Expenses:- 669800

Net profit before tax 89800

1

The report will provide for understanding of financial statements and how they are

prepared also about the fundamental concepts, models and techniques of financial accounting . It

will also cover illustration that will help to understand the model, techniques and concepts that

are used in management accounting. The report will provide understanding about the

importance of different techniques that help to check the viability of project.

PART A -Yarnshaw Limited

I) Income Statement

Income Statement

For the year ended

31 December 2018

Particulars £ £

Revenues:-

Sales(604800+154800) 759600

Other income 0

Total Revenues 759600

Expenses:-

Cost of goods sold or cost of sales 29160

0

64800 356400

Depreciation 11000

Wages paid 14040

0

Add Outstanding wages at the end of the year 2610 143010

Electricity Expenses 9270

Van running expenses 40320

Bad debts 1800

Rent paid 13500

0

Less:- prepaid rent at the end of the year 27000 108000

Total Expenses:- 669800

Net profit before tax 89800

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less:- Tax paid 6930

Net profit after tax 82870

Working Notes

1 Total Sales

credit sales 604800

cash sales 154800

759600

2 Depreciation

Purchase Price of Van 72000

scarp value 6000

life in years 6

Depreciation 11000

3 Tax Computation

Tax upto 31 march 2018 2880

Add:- Tax from 1 april 2018 to 31 march 2019 5400

Less:- prepaid tax of 3 months

(from 1january 2019 to 31 march 2019) 1350

6930

4 Electricity Expenses:-

Expenses paid 6840

Add:- Outstanding expenses at the end of the year 2430

9270

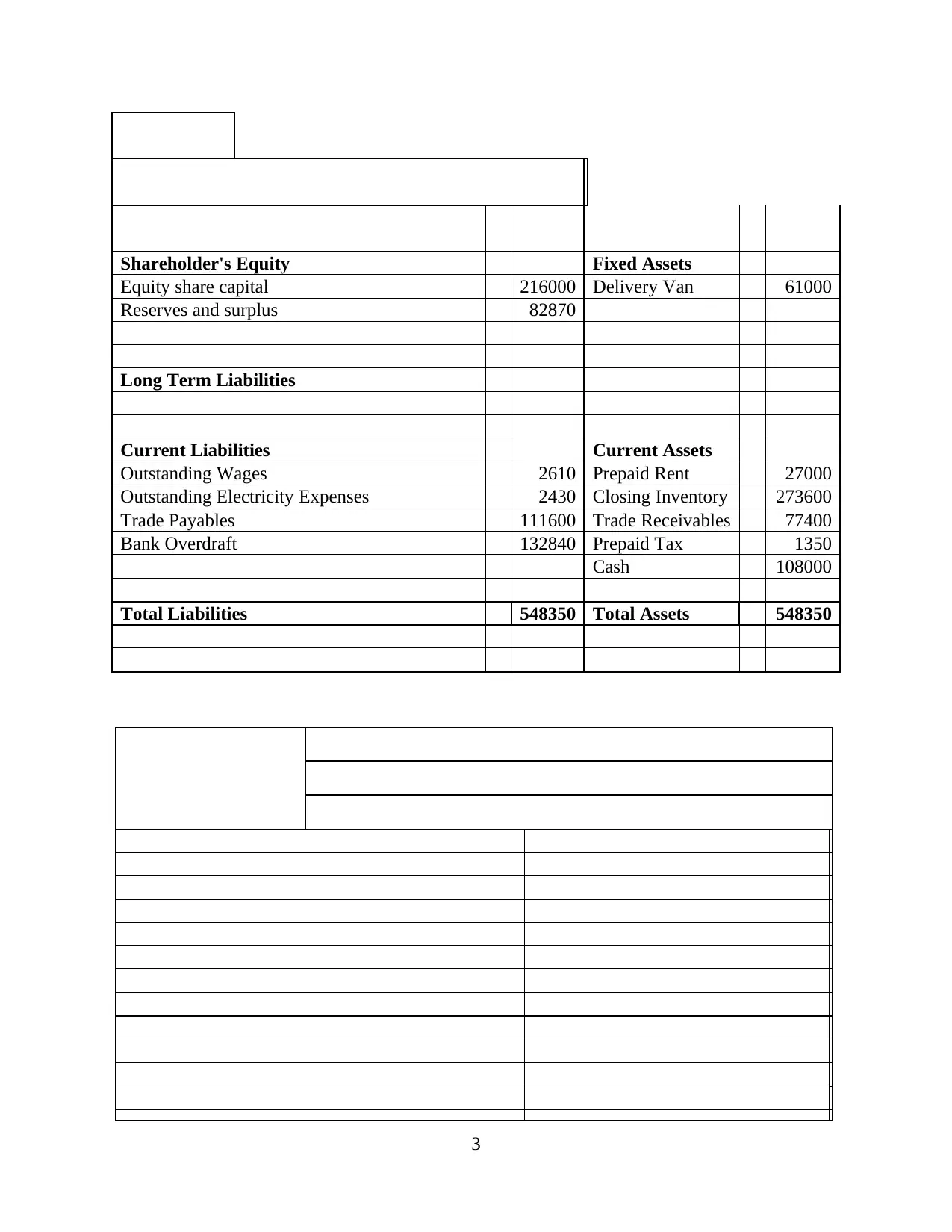

II) Balance Sheet

Balance

Sheet

For the year

ended 31

December

2018

2

Net profit after tax 82870

Working Notes

1 Total Sales

credit sales 604800

cash sales 154800

759600

2 Depreciation

Purchase Price of Van 72000

scarp value 6000

life in years 6

Depreciation 11000

3 Tax Computation

Tax upto 31 march 2018 2880

Add:- Tax from 1 april 2018 to 31 march 2019 5400

Less:- prepaid tax of 3 months

(from 1january 2019 to 31 march 2019) 1350

6930

4 Electricity Expenses:-

Expenses paid 6840

Add:- Outstanding expenses at the end of the year 2430

9270

II) Balance Sheet

Balance

Sheet

For the year

ended 31

December

2018

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shareholder's Equity Fixed Assets

Equity share capital 216000 Delivery Van 61000

Reserves and surplus 82870

Long Term Liabilities

Current Liabilities Current Assets

Outstanding Wages 2610 Prepaid Rent 27000

Outstanding Electricity Expenses 2430 Closing Inventory 273600

Trade Payables 111600 Trade Receivables 77400

Bank Overdraft 132840 Prepaid Tax 1350

Cash 108000

Total Liabilities 548350 Total Assets 548350

3

Equity share capital 216000 Delivery Van 61000

Reserves and surplus 82870

Long Term Liabilities

Current Liabilities Current Assets

Outstanding Wages 2610 Prepaid Rent 27000

Outstanding Electricity Expenses 2430 Closing Inventory 273600

Trade Payables 111600 Trade Receivables 77400

Bank Overdraft 132840 Prepaid Tax 1350

Cash 108000

Total Liabilities 548350 Total Assets 548350

3

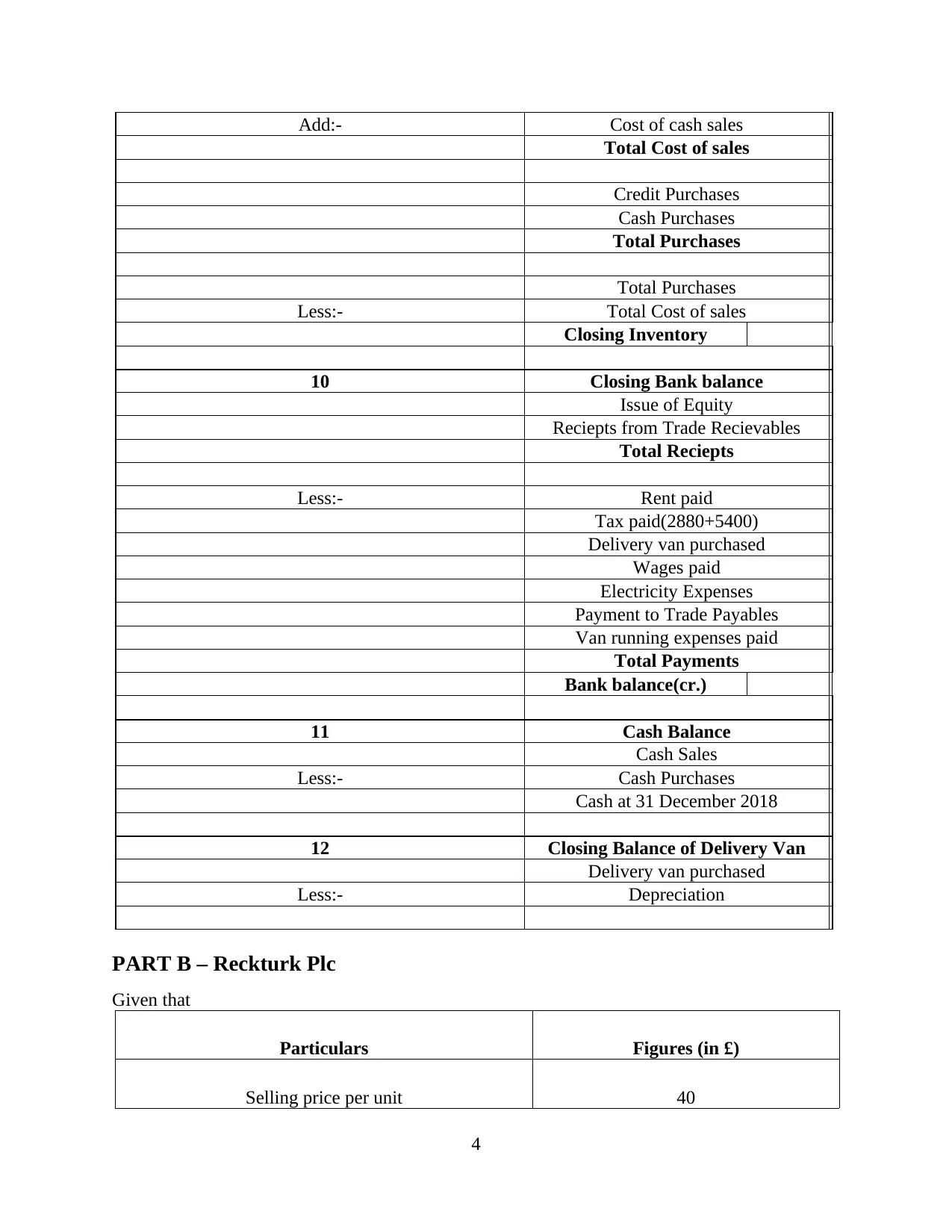

Add:- Cost of cash sales

Total Cost of sales

Credit Purchases

Cash Purchases

Total Purchases

Total Purchases

Less:- Total Cost of sales

Closing Inventory

10 Closing Bank balance

Issue of Equity

Reciepts from Trade Recievables

Total Reciepts

Less:- Rent paid

Tax paid(2880+5400)

Delivery van purchased

Wages paid

Electricity Expenses

Payment to Trade Payables

Van running expenses paid

Total Payments

Bank balance(cr.)

11 Cash Balance

Cash Sales

Less:- Cash Purchases

Cash at 31 December 2018

12 Closing Balance of Delivery Van

Delivery van purchased

Less:- Depreciation

PART B – Reckturk Plc

Given that

Particulars Figures (in £)

Selling price per unit 40

4

Total Cost of sales

Credit Purchases

Cash Purchases

Total Purchases

Total Purchases

Less:- Total Cost of sales

Closing Inventory

10 Closing Bank balance

Issue of Equity

Reciepts from Trade Recievables

Total Reciepts

Less:- Rent paid

Tax paid(2880+5400)

Delivery van purchased

Wages paid

Electricity Expenses

Payment to Trade Payables

Van running expenses paid

Total Payments

Bank balance(cr.)

11 Cash Balance

Cash Sales

Less:- Cash Purchases

Cash at 31 December 2018

12 Closing Balance of Delivery Van

Delivery van purchased

Less:- Depreciation

PART B – Reckturk Plc

Given that

Particulars Figures (in £)

Selling price per unit 40

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

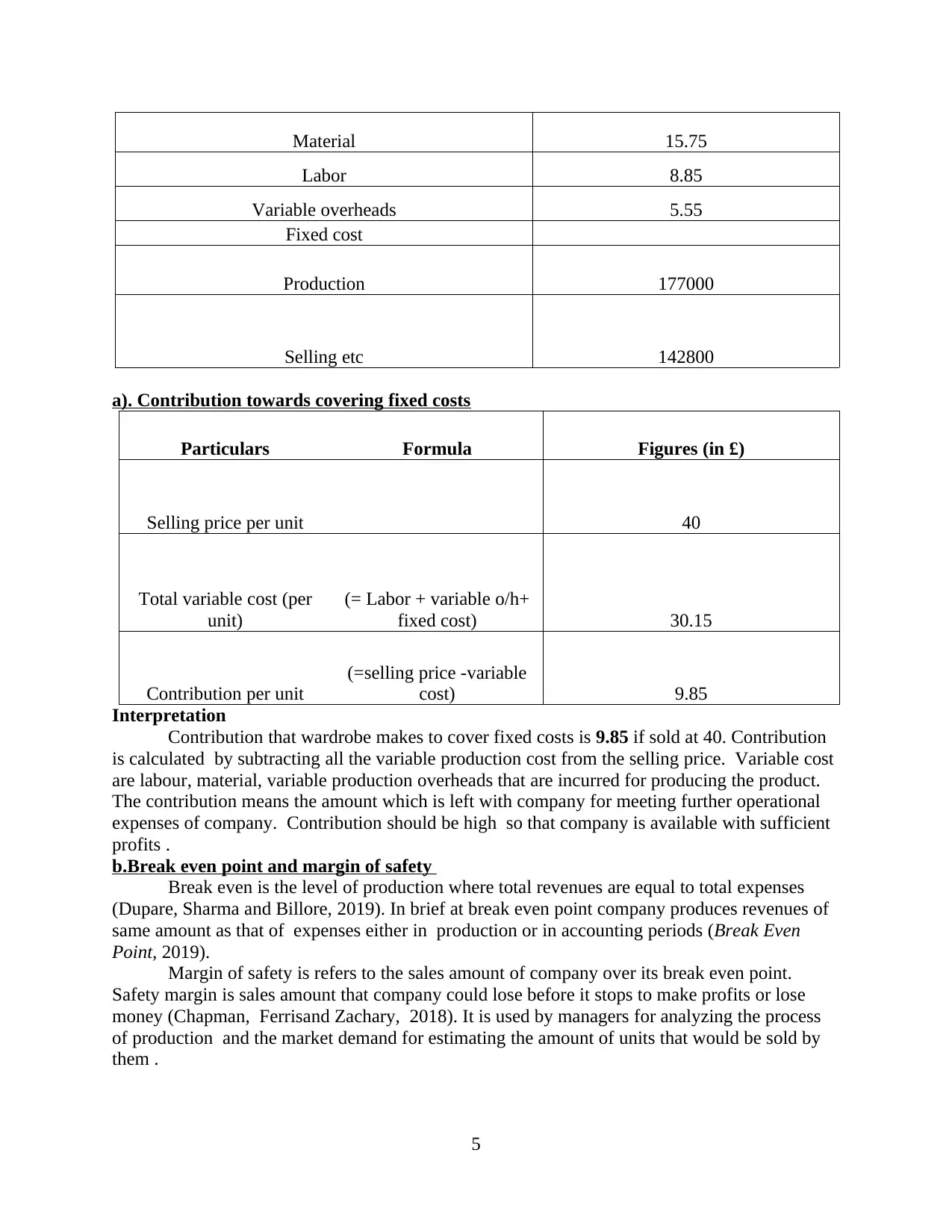

Material 15.75

Labor 8.85

Variable overheads 5.55

Fixed cost

Production 177000

Selling etc 142800

a). Contribution towards covering fixed costs

Particulars Formula Figures (in £)

Selling price per unit 40

Total variable cost (per

unit)

(= Labor + variable o/h+

fixed cost) 30.15

Contribution per unit

(=selling price -variable

cost) 9.85

Interpretation

Contribution that wardrobe makes to cover fixed costs is 9.85 if sold at 40. Contribution

is calculated by subtracting all the variable production cost from the selling price. Variable cost

are labour, material, variable production overheads that are incurred for producing the product.

The contribution means the amount which is left with company for meeting further operational

expenses of company. Contribution should be high so that company is available with sufficient

profits .

b.Break even point and margin of safety

Break even is the level of production where total revenues are equal to total expenses

(Dupare, Sharma and Billore, 2019). In brief at break even point company produces revenues of

same amount as that of expenses either in production or in accounting periods (Break Even

Point, 2019).

Margin of safety is refers to the sales amount of company over its break even point.

Safety margin is sales amount that company could lose before it stops to make profits or lose

money (Chapman, Ferrisand Zachary, 2018). It is used by managers for analyzing the process

of production and the market demand for estimating the amount of units that would be sold by

them .

5

Labor 8.85

Variable overheads 5.55

Fixed cost

Production 177000

Selling etc 142800

a). Contribution towards covering fixed costs

Particulars Formula Figures (in £)

Selling price per unit 40

Total variable cost (per

unit)

(= Labor + variable o/h+

fixed cost) 30.15

Contribution per unit

(=selling price -variable

cost) 9.85

Interpretation

Contribution that wardrobe makes to cover fixed costs is 9.85 if sold at 40. Contribution

is calculated by subtracting all the variable production cost from the selling price. Variable cost

are labour, material, variable production overheads that are incurred for producing the product.

The contribution means the amount which is left with company for meeting further operational

expenses of company. Contribution should be high so that company is available with sufficient

profits .

b.Break even point and margin of safety

Break even is the level of production where total revenues are equal to total expenses

(Dupare, Sharma and Billore, 2019). In brief at break even point company produces revenues of

same amount as that of expenses either in production or in accounting periods (Break Even

Point, 2019).

Margin of safety is refers to the sales amount of company over its break even point.

Safety margin is sales amount that company could lose before it stops to make profits or lose

money (Chapman, Ferrisand Zachary, 2018). It is used by managers for analyzing the process

of production and the market demand for estimating the amount of units that would be sold by

them .

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

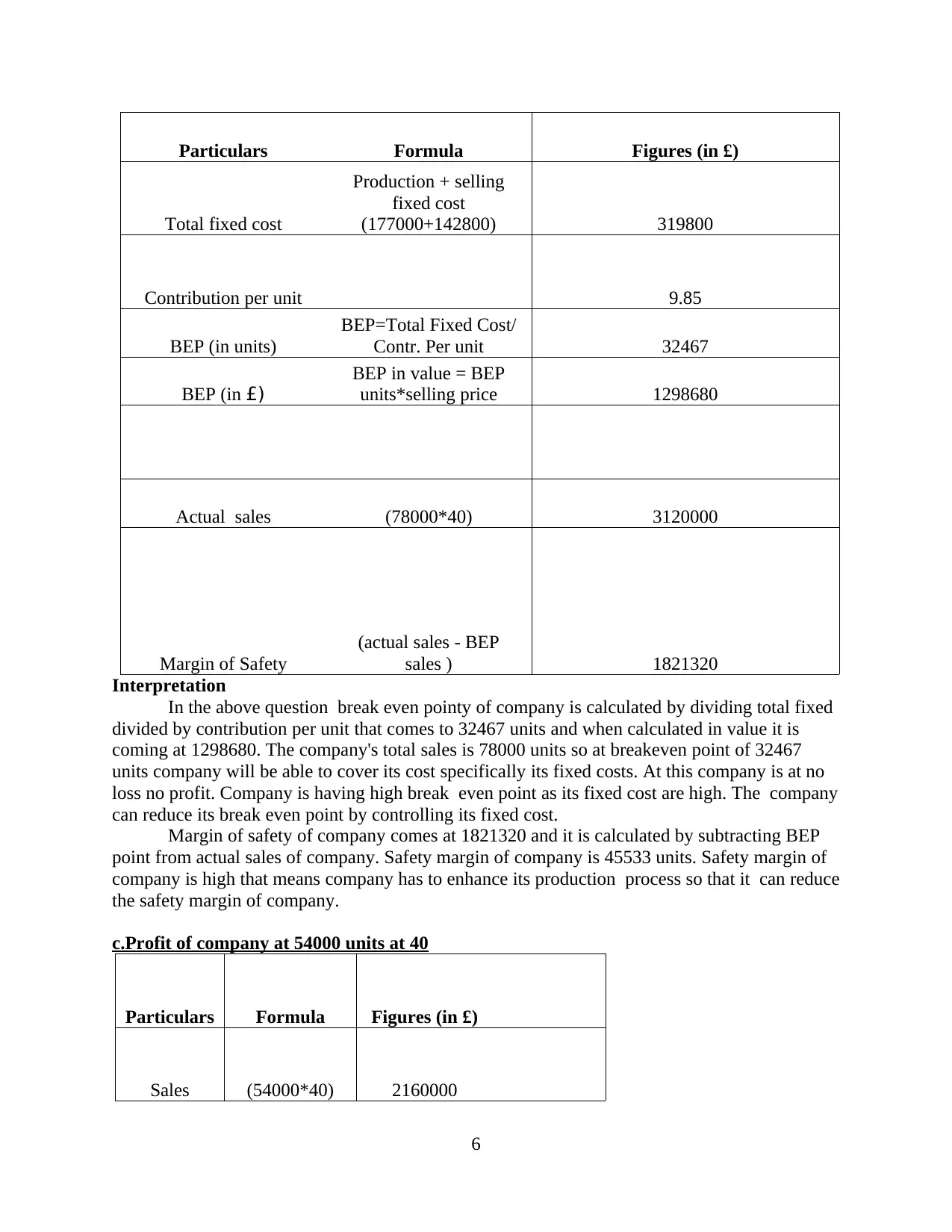

Particulars Formula Figures (in £)

Total fixed cost

Production + selling

fixed cost

(177000+142800) 319800

Contribution per unit 9.85

BEP (in units)

BEP=Total Fixed Cost/

Contr. Per unit 32467

BEP (in £)

BEP in value = BEP

units*selling price 1298680

Actual sales (78000*40) 3120000

Margin of Safety

(actual sales - BEP

sales ) 1821320

Interpretation

In the above question break even pointy of company is calculated by dividing total fixed

divided by contribution per unit that comes to 32467 units and when calculated in value it is

coming at 1298680. The company's total sales is 78000 units so at breakeven point of 32467

units company will be able to cover its cost specifically its fixed costs. At this company is at no

loss no profit. Company is having high break even point as its fixed cost are high. The company

can reduce its break even point by controlling its fixed cost.

Margin of safety of company comes at 1821320 and it is calculated by subtracting BEP

point from actual sales of company. Safety margin of company is 45533 units. Safety margin of

company is high that means company has to enhance its production process so that it can reduce

the safety margin of company.

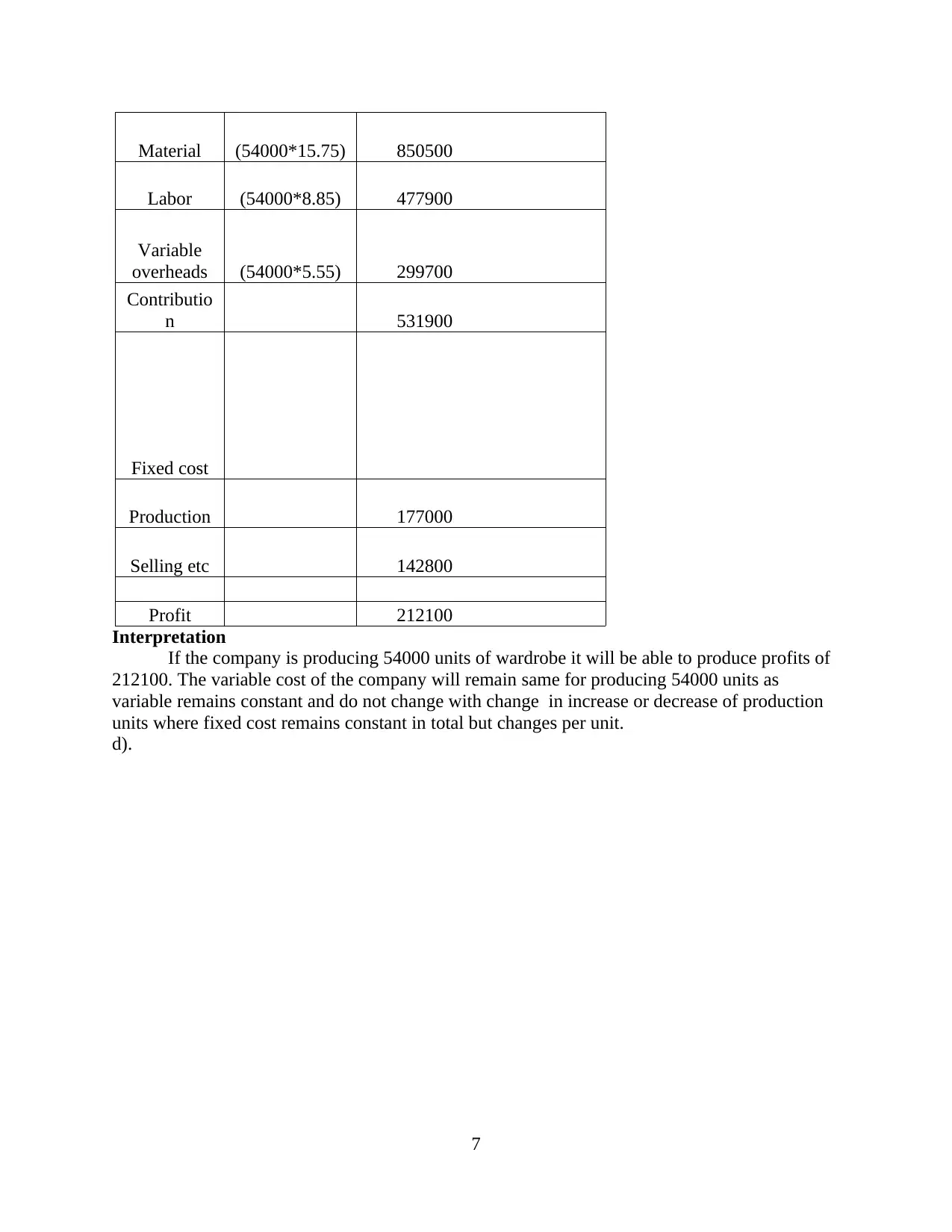

c.Profit of company at 54000 units at 40

Particulars Formula Figures (in £)

Sales (54000*40) 2160000

6

Total fixed cost

Production + selling

fixed cost

(177000+142800) 319800

Contribution per unit 9.85

BEP (in units)

BEP=Total Fixed Cost/

Contr. Per unit 32467

BEP (in £)

BEP in value = BEP

units*selling price 1298680

Actual sales (78000*40) 3120000

Margin of Safety

(actual sales - BEP

sales ) 1821320

Interpretation

In the above question break even pointy of company is calculated by dividing total fixed

divided by contribution per unit that comes to 32467 units and when calculated in value it is

coming at 1298680. The company's total sales is 78000 units so at breakeven point of 32467

units company will be able to cover its cost specifically its fixed costs. At this company is at no

loss no profit. Company is having high break even point as its fixed cost are high. The company

can reduce its break even point by controlling its fixed cost.

Margin of safety of company comes at 1821320 and it is calculated by subtracting BEP

point from actual sales of company. Safety margin of company is 45533 units. Safety margin of

company is high that means company has to enhance its production process so that it can reduce

the safety margin of company.

c.Profit of company at 54000 units at 40

Particulars Formula Figures (in £)

Sales (54000*40) 2160000

6

Material (54000*15.75) 850500

Labor (54000*8.85) 477900

Variable

overheads (54000*5.55) 299700

Contributio

n 531900

Fixed cost

Production 177000

Selling etc 142800

Profit 212100

Interpretation

If the company is producing 54000 units of wardrobe it will be able to produce profits of

212100. The variable cost of the company will remain same for producing 54000 units as

variable remains constant and do not change with change in increase or decrease of production

units where fixed cost remains constant in total but changes per unit.

d).

7

Labor (54000*8.85) 477900

Variable

overheads (54000*5.55) 299700

Contributio

n 531900

Fixed cost

Production 177000

Selling etc 142800

Profit 212100

Interpretation

If the company is producing 54000 units of wardrobe it will be able to produce profits of

212100. The variable cost of the company will remain same for producing 54000 units as

variable remains constant and do not change with change in increase or decrease of production

units where fixed cost remains constant in total but changes per unit.

d).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

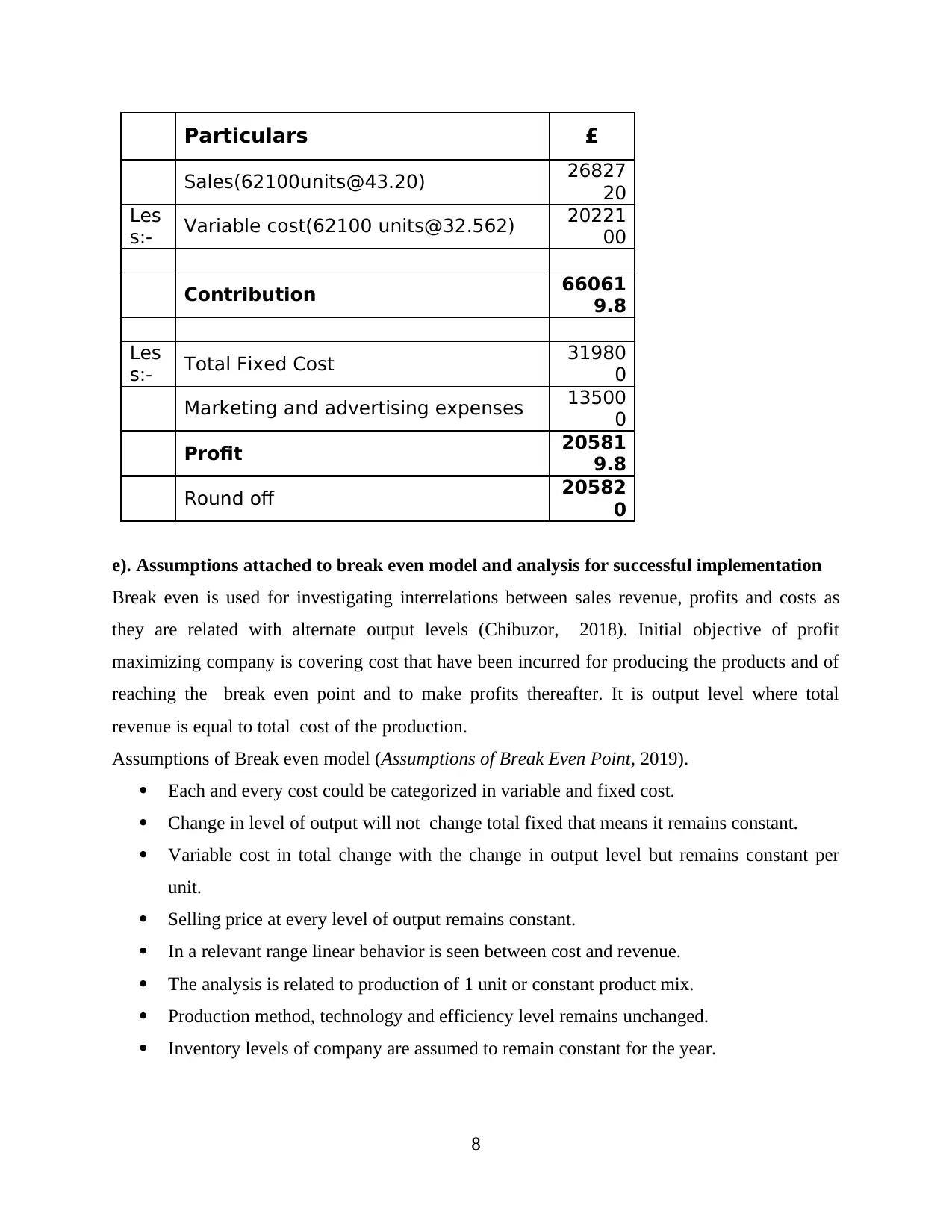

Particulars £

Sales(62100units@43.20) 26827

20

Les

s:- Variable cost(62100 units@32.562) 20221

00

Contribution 66061

9.8

Les

s:- Total Fixed Cost 31980

0

Marketing and advertising expenses 13500

0

Profit 20581

9.8

Round off 20582

0

e). Assumptions attached to break even model and analysis for successful implementation

Break even is used for investigating interrelations between sales revenue, profits and costs as

they are related with alternate output levels (Chibuzor, 2018). Initial objective of profit

maximizing company is covering cost that have been incurred for producing the products and of

reaching the break even point and to make profits thereafter. It is output level where total

revenue is equal to total cost of the production.

Assumptions of Break even model (Assumptions of Break Even Point, 2019).

Each and every cost could be categorized in variable and fixed cost.

Change in level of output will not change total fixed that means it remains constant.

Variable cost in total change with the change in output level but remains constant per

unit.

Selling price at every level of output remains constant.

In a relevant range linear behavior is seen between cost and revenue.

The analysis is related to production of 1 unit or constant product mix.

Production method, technology and efficiency level remains unchanged.

Inventory levels of company are assumed to remain constant for the year.

8

Sales(62100units@43.20) 26827

20

Les

s:- Variable cost(62100 units@32.562) 20221

00

Contribution 66061

9.8

Les

s:- Total Fixed Cost 31980

0

Marketing and advertising expenses 13500

0

Profit 20581

9.8

Round off 20582

0

e). Assumptions attached to break even model and analysis for successful implementation

Break even is used for investigating interrelations between sales revenue, profits and costs as

they are related with alternate output levels (Chibuzor, 2018). Initial objective of profit

maximizing company is covering cost that have been incurred for producing the products and of

reaching the break even point and to make profits thereafter. It is output level where total

revenue is equal to total cost of the production.

Assumptions of Break even model (Assumptions of Break Even Point, 2019).

Each and every cost could be categorized in variable and fixed cost.

Change in level of output will not change total fixed that means it remains constant.

Variable cost in total change with the change in output level but remains constant per

unit.

Selling price at every level of output remains constant.

In a relevant range linear behavior is seen between cost and revenue.

The analysis is related to production of 1 unit or constant product mix.

Production method, technology and efficiency level remains unchanged.

Inventory levels of company are assumed to remain constant for the year.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

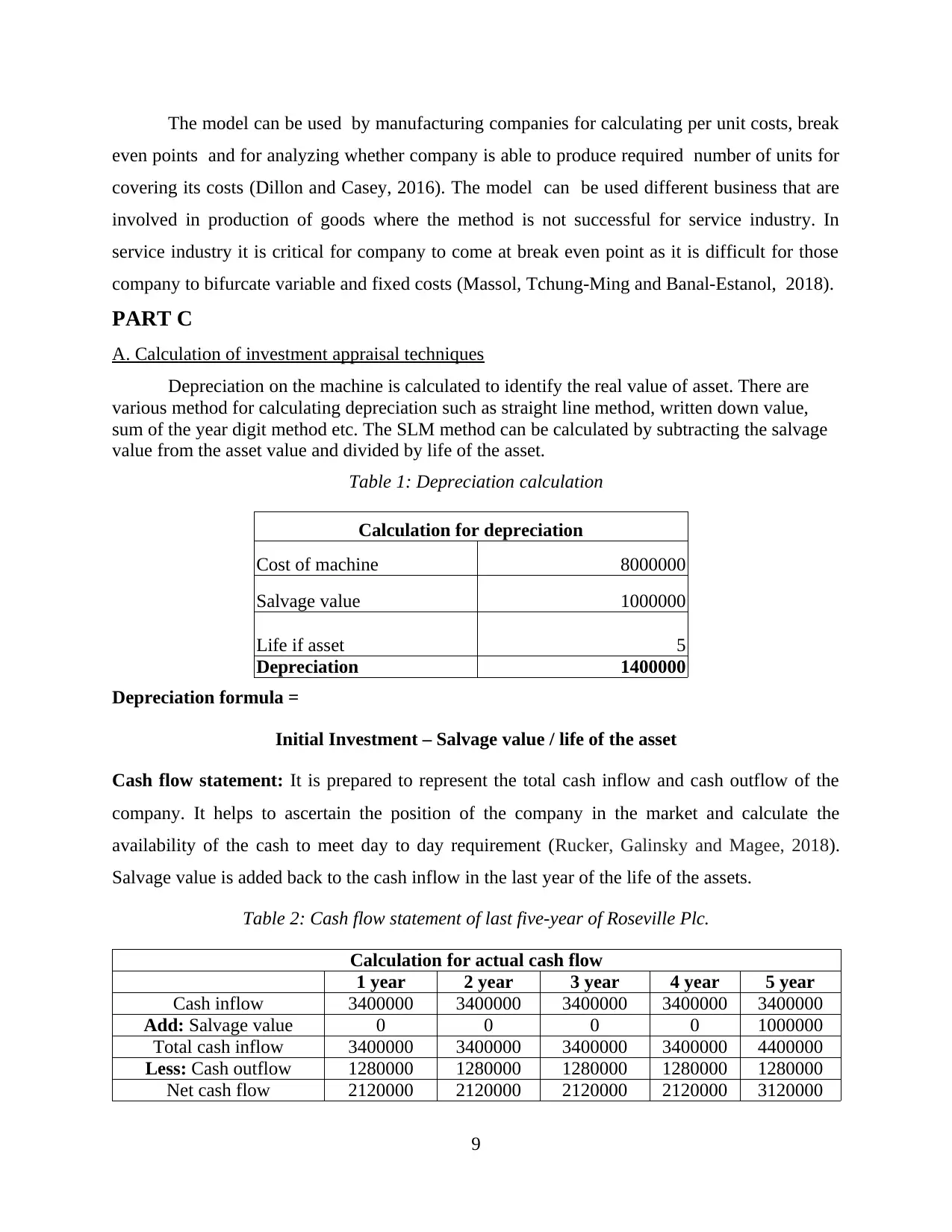

The model can be used by manufacturing companies for calculating per unit costs, break

even points and for analyzing whether company is able to produce required number of units for

covering its costs (Dillon and Casey, 2016). The model can be used different business that are

involved in production of goods where the method is not successful for service industry. In

service industry it is critical for company to come at break even point as it is difficult for those

company to bifurcate variable and fixed costs (Massol, Tchung-Ming and Banal-Estanol, 2018).

PART C

A. Calculation of investment appraisal techniques

Depreciation on the machine is calculated to identify the real value of asset. There are

various method for calculating depreciation such as straight line method, written down value,

sum of the year digit method etc. The SLM method can be calculated by subtracting the salvage

value from the asset value and divided by life of the asset.

Table 1: Depreciation calculation

Calculation for depreciation

Cost of machine 8000000

Salvage value 1000000

Life if asset 5

Depreciation 1400000

Depreciation formula =

Initial Investment – Salvage value / life of the asset

Cash flow statement: It is prepared to represent the total cash inflow and cash outflow of the

company. It helps to ascertain the position of the company in the market and calculate the

availability of the cash to meet day to day requirement (Rucker, Galinsky and Magee, 2018).

Salvage value is added back to the cash inflow in the last year of the life of the assets.

Table 2: Cash flow statement of last five-year of Roseville Plc.

Calculation for actual cash flow

1 year 2 year 3 year 4 year 5 year

Cash inflow 3400000 3400000 3400000 3400000 3400000

Add: Salvage value 0 0 0 0 1000000

Total cash inflow 3400000 3400000 3400000 3400000 4400000

Less: Cash outflow 1280000 1280000 1280000 1280000 1280000

Net cash flow 2120000 2120000 2120000 2120000 3120000

9

even points and for analyzing whether company is able to produce required number of units for

covering its costs (Dillon and Casey, 2016). The model can be used different business that are

involved in production of goods where the method is not successful for service industry. In

service industry it is critical for company to come at break even point as it is difficult for those

company to bifurcate variable and fixed costs (Massol, Tchung-Ming and Banal-Estanol, 2018).

PART C

A. Calculation of investment appraisal techniques

Depreciation on the machine is calculated to identify the real value of asset. There are

various method for calculating depreciation such as straight line method, written down value,

sum of the year digit method etc. The SLM method can be calculated by subtracting the salvage

value from the asset value and divided by life of the asset.

Table 1: Depreciation calculation

Calculation for depreciation

Cost of machine 8000000

Salvage value 1000000

Life if asset 5

Depreciation 1400000

Depreciation formula =

Initial Investment – Salvage value / life of the asset

Cash flow statement: It is prepared to represent the total cash inflow and cash outflow of the

company. It helps to ascertain the position of the company in the market and calculate the

availability of the cash to meet day to day requirement (Rucker, Galinsky and Magee, 2018).

Salvage value is added back to the cash inflow in the last year of the life of the assets.

Table 2: Cash flow statement of last five-year of Roseville Plc.

Calculation for actual cash flow

1 year 2 year 3 year 4 year 5 year

Cash inflow 3400000 3400000 3400000 3400000 3400000

Add: Salvage value 0 0 0 0 1000000

Total cash inflow 3400000 3400000 3400000 3400000 4400000

Less: Cash outflow 1280000 1280000 1280000 1280000 1280000

Net cash flow 2120000 2120000 2120000 2120000 3120000

9

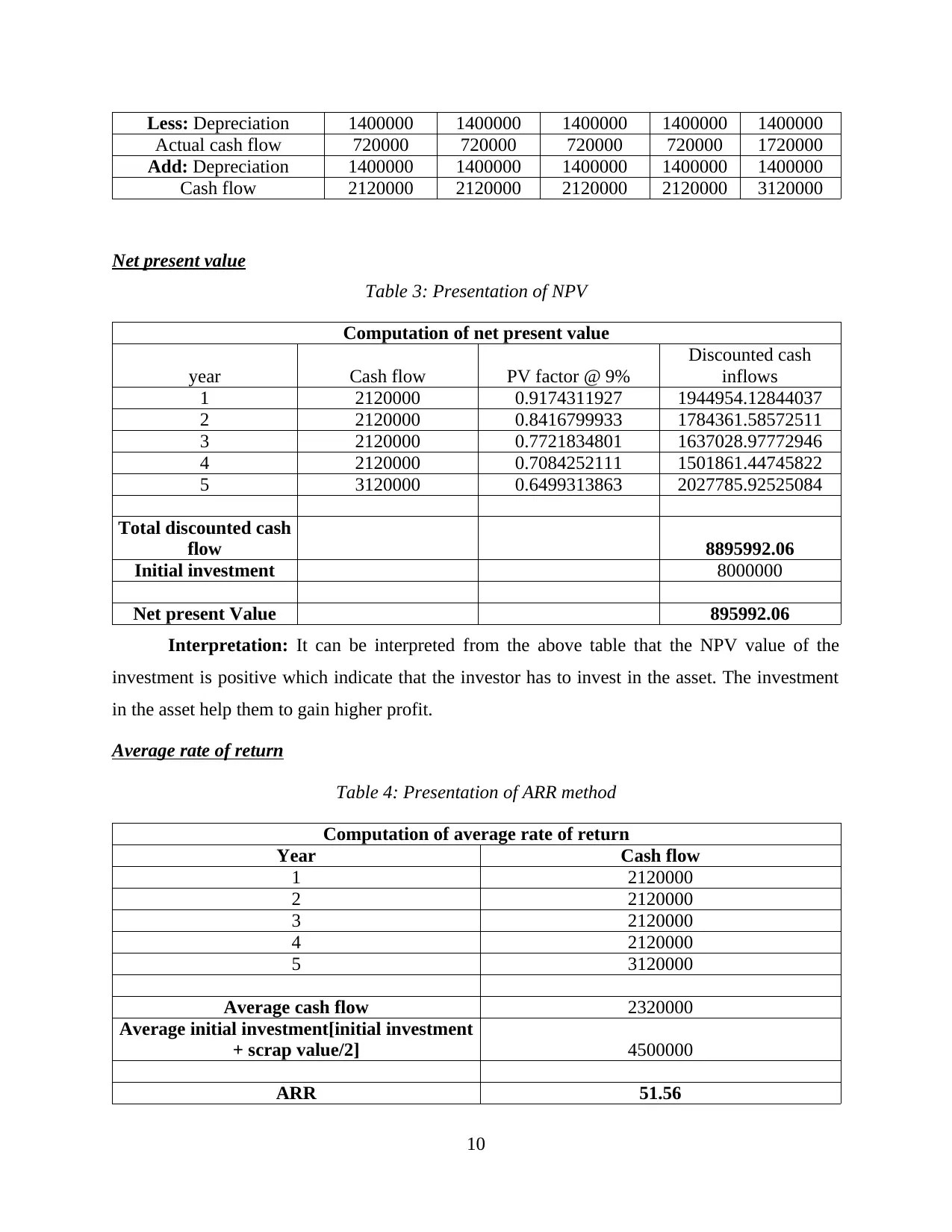

Less: Depreciation 1400000 1400000 1400000 1400000 1400000

Actual cash flow 720000 720000 720000 720000 1720000

Add: Depreciation 1400000 1400000 1400000 1400000 1400000

Cash flow 2120000 2120000 2120000 2120000 3120000

Net present value

Table 3: Presentation of NPV

Computation of net present value

year Cash flow PV factor @ 9%

Discounted cash

inflows

1 2120000 0.9174311927 1944954.12844037

2 2120000 0.8416799933 1784361.58572511

3 2120000 0.7721834801 1637028.97772946

4 2120000 0.7084252111 1501861.44745822

5 3120000 0.6499313863 2027785.92525084

Total discounted cash

flow 8895992.06

Initial investment 8000000

Net present Value 895992.06

Interpretation: It can be interpreted from the above table that the NPV value of the

investment is positive which indicate that the investor has to invest in the asset. The investment

in the asset help them to gain higher profit.

Average rate of return

Table 4: Presentation of ARR method

Computation of average rate of return

Year Cash flow

1 2120000

2 2120000

3 2120000

4 2120000

5 3120000

Average cash flow 2320000

Average initial investment[initial investment

+ scrap value/2] 4500000

ARR 51.56

10

Actual cash flow 720000 720000 720000 720000 1720000

Add: Depreciation 1400000 1400000 1400000 1400000 1400000

Cash flow 2120000 2120000 2120000 2120000 3120000

Net present value

Table 3: Presentation of NPV

Computation of net present value

year Cash flow PV factor @ 9%

Discounted cash

inflows

1 2120000 0.9174311927 1944954.12844037

2 2120000 0.8416799933 1784361.58572511

3 2120000 0.7721834801 1637028.97772946

4 2120000 0.7084252111 1501861.44745822

5 3120000 0.6499313863 2027785.92525084

Total discounted cash

flow 8895992.06

Initial investment 8000000

Net present Value 895992.06

Interpretation: It can be interpreted from the above table that the NPV value of the

investment is positive which indicate that the investor has to invest in the asset. The investment

in the asset help them to gain higher profit.

Average rate of return

Table 4: Presentation of ARR method

Computation of average rate of return

Year Cash flow

1 2120000

2 2120000

3 2120000

4 2120000

5 3120000

Average cash flow 2320000

Average initial investment[initial investment

+ scrap value/2] 4500000

ARR 51.56

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.