Introduction to Accounting and Finance Assessment Report Analysis

VerifiedAdded on 2021/02/19

|17

|4544

|22

Report

AI Summary

This comprehensive report delves into key aspects of accounting and finance, beginning with an introduction that highlights the interrelation between accounting and financial management. The report then presents financial statements for Yarnshaw Limited, including the statement of income and financial position. Part B focuses on Reckturk Plc, performing a break-even analysis, calculating the margin of safety, and computing profit based on varying production and sales volumes, and also presents a new marketing proposal. Finally, Part C evaluates investment appraisal techniques for Roseville Plc, including payback period, net present value, and accounting rate of return, and discusses the benefits and limitations of budgeting as a strategic planning tool. The report provides detailed calculations and analyses throughout, offering insights into financial statement preparation, break-even analysis, and investment appraisal.

Introduction

to Accounting and

Finance Assessment

to Accounting and

Finance Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Part A – Yarnshaw Limited:.......................................................................................................3

Statement of Income of Yarnshaw Limited:...............................................................................3

Statement of Financial Position of Yarnshaw Limited:..............................................................4

Part B – Reckturk Plc:.................................................................................................................6

A. Calculation of contribution per wardrobe makes towards covering fixed costs if selling

price is £40:.................................................................................................................................6

B. Computation of break-even point and margin of safety in terms of both units of wardrobe

and revenue if selling price is £40:.............................................................................................7

C. Computation of the profit of company if production and selling units are 54,000 wardrobe

and selling price is £40 per wardrobe:........................................................................................8

D..................................................................................................................................................8

E. Break-even Model:.................................................................................................................9

Part C – Roseville Plc:..............................................................................................................10

A. Calculation of Payback Period, Net Present Value and Accounting Rate of Return of the

machine and recommendation:.................................................................................................10

B. Explanation and analyses of differing investment appraisal technique's major merits and

limitations:.................................................................................................................................12

C. Key benefits and limitations of using budgets as a tool for strategic planning:...................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Part A – Yarnshaw Limited:.......................................................................................................3

Statement of Income of Yarnshaw Limited:...............................................................................3

Statement of Financial Position of Yarnshaw Limited:..............................................................4

Part B – Reckturk Plc:.................................................................................................................6

A. Calculation of contribution per wardrobe makes towards covering fixed costs if selling

price is £40:.................................................................................................................................6

B. Computation of break-even point and margin of safety in terms of both units of wardrobe

and revenue if selling price is £40:.............................................................................................7

C. Computation of the profit of company if production and selling units are 54,000 wardrobe

and selling price is £40 per wardrobe:........................................................................................8

D..................................................................................................................................................8

E. Break-even Model:.................................................................................................................9

Part C – Roseville Plc:..............................................................................................................10

A. Calculation of Payback Period, Net Present Value and Accounting Rate of Return of the

machine and recommendation:.................................................................................................10

B. Explanation and analyses of differing investment appraisal technique's major merits and

limitations:.................................................................................................................................12

C. Key benefits and limitations of using budgets as a tool for strategic planning:...................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

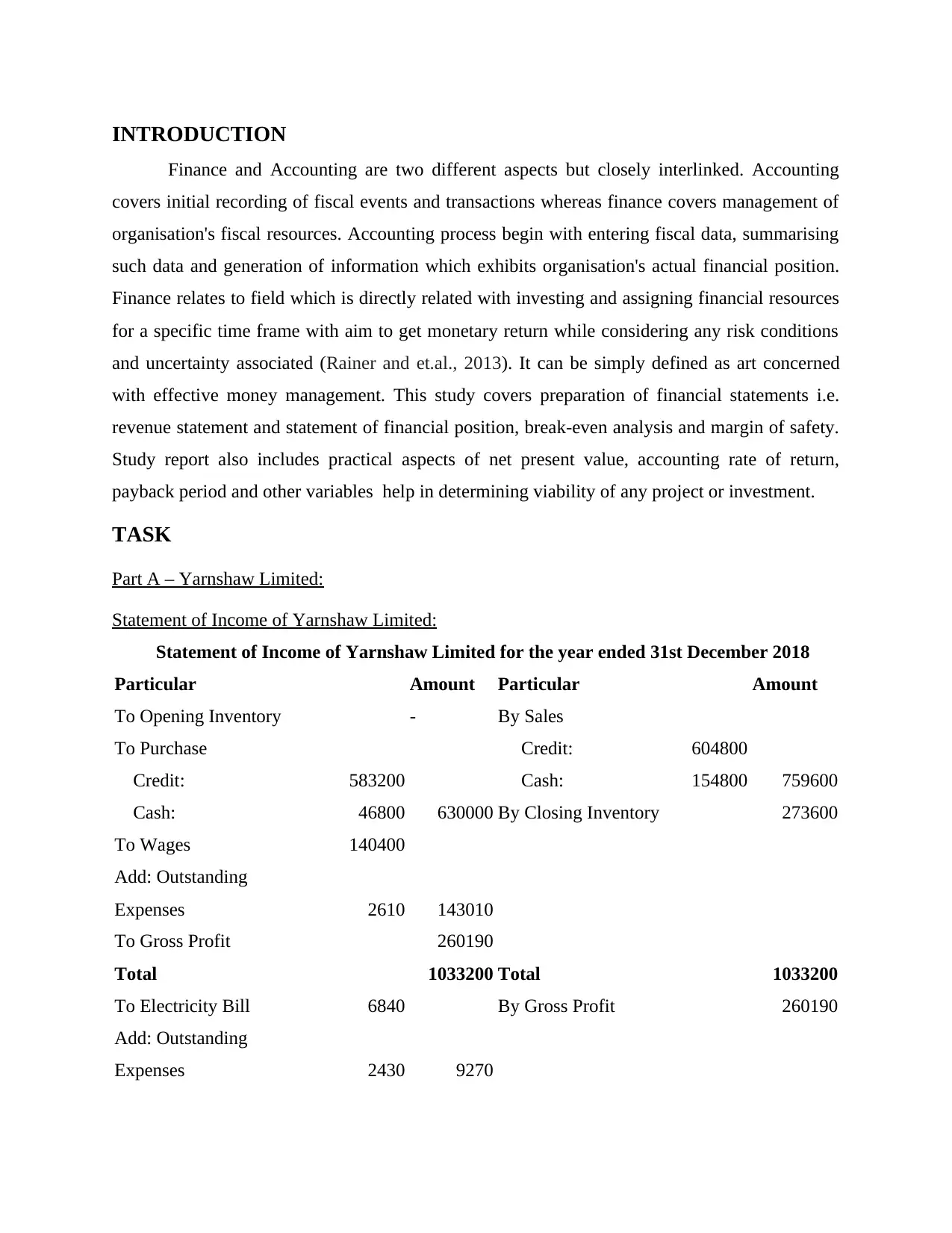

INTRODUCTION

Finance and Accounting are two different aspects but closely interlinked. Accounting

covers initial recording of fiscal events and transactions whereas finance covers management of

organisation's fiscal resources. Accounting process begin with entering fiscal data, summarising

such data and generation of information which exhibits organisation's actual financial position.

Finance relates to field which is directly related with investing and assigning financial resources

for a specific time frame with aim to get monetary return while considering any risk conditions

and uncertainty associated (Rainer and et.al., 2013). It can be simply defined as art concerned

with effective money management. This study covers preparation of financial statements i.e.

revenue statement and statement of financial position, break-even analysis and margin of safety.

Study report also includes practical aspects of net present value, accounting rate of return,

payback period and other variables help in determining viability of any project or investment.

TASK

Part A – Yarnshaw Limited:

Statement of Income of Yarnshaw Limited:

Statement of Income of Yarnshaw Limited for the year ended 31st December 2018

Particular Amount Particular Amount

To Opening Inventory - By Sales

To Purchase Credit: 604800

Credit: 583200 Cash: 154800 759600

Cash: 46800 630000 By Closing Inventory 273600

To Wages 140400

Add: Outstanding

Expenses 2610 143010

To Gross Profit 260190

Total 1033200 Total 1033200

To Electricity Bill 6840 By Gross Profit 260190

Add: Outstanding

Expenses 2430 9270

Finance and Accounting are two different aspects but closely interlinked. Accounting

covers initial recording of fiscal events and transactions whereas finance covers management of

organisation's fiscal resources. Accounting process begin with entering fiscal data, summarising

such data and generation of information which exhibits organisation's actual financial position.

Finance relates to field which is directly related with investing and assigning financial resources

for a specific time frame with aim to get monetary return while considering any risk conditions

and uncertainty associated (Rainer and et.al., 2013). It can be simply defined as art concerned

with effective money management. This study covers preparation of financial statements i.e.

revenue statement and statement of financial position, break-even analysis and margin of safety.

Study report also includes practical aspects of net present value, accounting rate of return,

payback period and other variables help in determining viability of any project or investment.

TASK

Part A – Yarnshaw Limited:

Statement of Income of Yarnshaw Limited:

Statement of Income of Yarnshaw Limited for the year ended 31st December 2018

Particular Amount Particular Amount

To Opening Inventory - By Sales

To Purchase Credit: 604800

Credit: 583200 Cash: 154800 759600

Cash: 46800 630000 By Closing Inventory 273600

To Wages 140400

Add: Outstanding

Expenses 2610 143010

To Gross Profit 260190

Total 1033200 Total 1033200

To Electricity Bill 6840 By Gross Profit 260190

Add: Outstanding

Expenses 2430 9270

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To Van Running

Expenses 40320

To Bad-debts 1800

To Rent Expenses 135000

Less: Prepaid Rent 27000 108000

To Rates 8280

Less: Prepaid Rent 1350 6930

To Depreciation on Van 11000

To Net Profit 82870

Total 260190 Total 260190

Statement of Financial Position of Yarnshaw Limited:

Statement of Financial Position of Yarnshaw Limited as on 31th December 2018

Amount

Assets

Current Assets

Prepaid Rent 27000

Prepaid Rates 1350

Debtors 77400

Inventories 273600

Total Current Assets 379350

Non Current Assets

Van 72000

Less: Depreciation 11000 61000

Total Assets 440350

Less: Liabilities

Current Liabilities

Outstanding Wages 2610

Outstanding Electricity Expenses 2430

Expenses 40320

To Bad-debts 1800

To Rent Expenses 135000

Less: Prepaid Rent 27000 108000

To Rates 8280

Less: Prepaid Rent 1350 6930

To Depreciation on Van 11000

To Net Profit 82870

Total 260190 Total 260190

Statement of Financial Position of Yarnshaw Limited:

Statement of Financial Position of Yarnshaw Limited as on 31th December 2018

Amount

Assets

Current Assets

Prepaid Rent 27000

Prepaid Rates 1350

Debtors 77400

Inventories 273600

Total Current Assets 379350

Non Current Assets

Van 72000

Less: Depreciation 11000 61000

Total Assets 440350

Less: Liabilities

Current Liabilities

Outstanding Wages 2610

Outstanding Electricity Expenses 2430

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

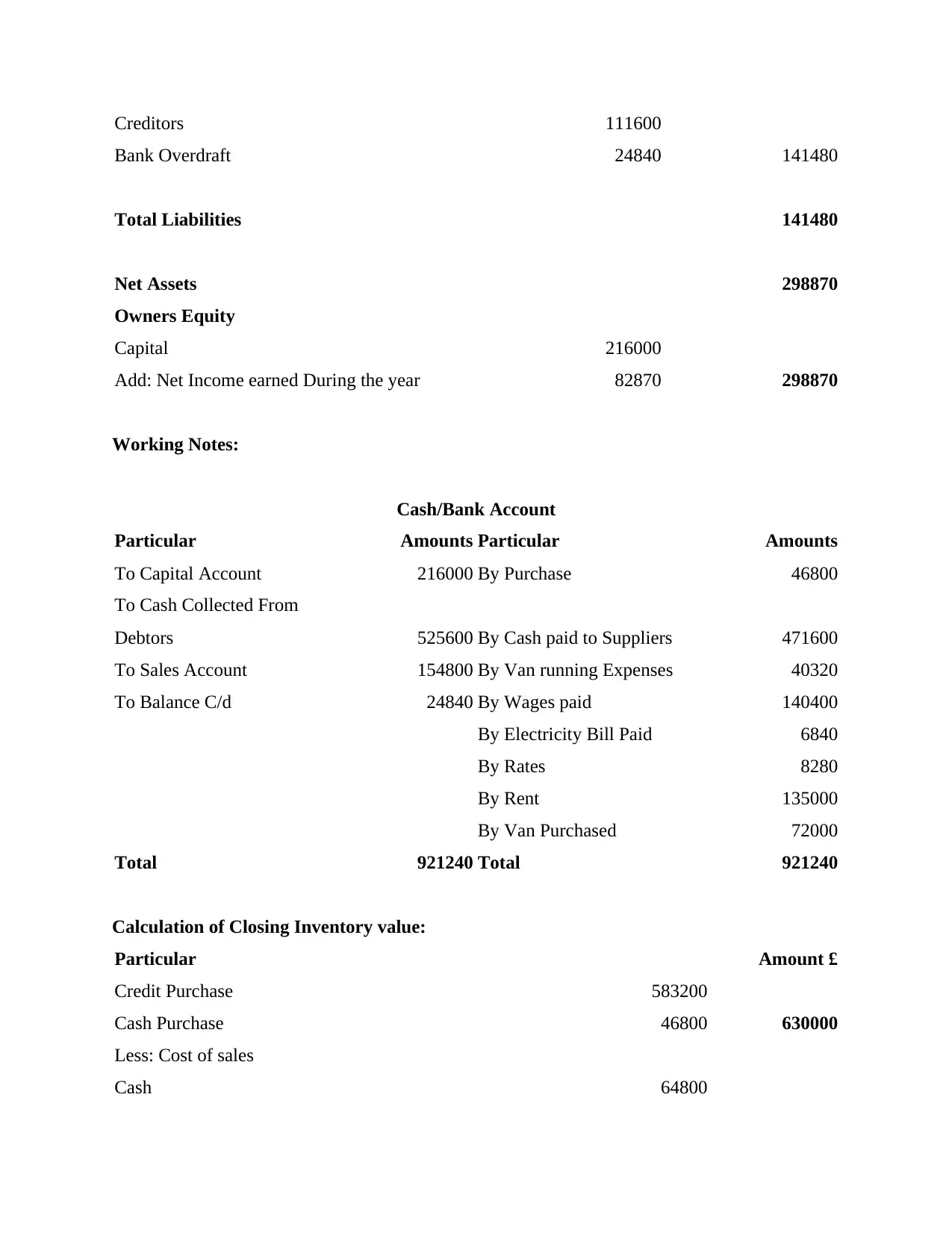

Creditors 111600

Bank Overdraft 24840 141480

Total Liabilities 141480

Net Assets 298870

Owners Equity

Capital 216000

Add: Net Income earned During the year 82870 298870

Working Notes:

Cash/Bank Account

Particular Amounts Particular Amounts

To Capital Account 216000 By Purchase 46800

To Cash Collected From

Debtors 525600 By Cash paid to Suppliers 471600

To Sales Account 154800 By Van running Expenses 40320

To Balance C/d 24840 By Wages paid 140400

By Electricity Bill Paid 6840

By Rates 8280

By Rent 135000

By Van Purchased 72000

Total 921240 Total 921240

Calculation of Closing Inventory value:

Particular Amount £

Credit Purchase 583200

Cash Purchase 46800 630000

Less: Cost of sales

Cash 64800

Bank Overdraft 24840 141480

Total Liabilities 141480

Net Assets 298870

Owners Equity

Capital 216000

Add: Net Income earned During the year 82870 298870

Working Notes:

Cash/Bank Account

Particular Amounts Particular Amounts

To Capital Account 216000 By Purchase 46800

To Cash Collected From

Debtors 525600 By Cash paid to Suppliers 471600

To Sales Account 154800 By Van running Expenses 40320

To Balance C/d 24840 By Wages paid 140400

By Electricity Bill Paid 6840

By Rates 8280

By Rent 135000

By Van Purchased 72000

Total 921240 Total 921240

Calculation of Closing Inventory value:

Particular Amount £

Credit Purchase 583200

Cash Purchase 46800 630000

Less: Cost of sales

Cash 64800

Credit 291600 356400

Closing Inventory 273600

Calculation of Debtors balance at year end:

Particular Amount £

Credit Sales 604800 604800

Less:

Cash collected from Debtors 525600

Bad debt 1800 527400

Debtors Balance at year end 77400

Calculation of Creditors balance at year end:

Particular Amount £

Credit Purchase 583200

Less:

Cash paid from Suppliers 471600

Closing Creditors 111600

Calculation of Depreciation:

SLM Method: (Value of Assets – Salvage Value)/Number of years

Computation of depreciation on Van purchased on 1 January 2018:

= £(72000 – 6000)/6

= £11000

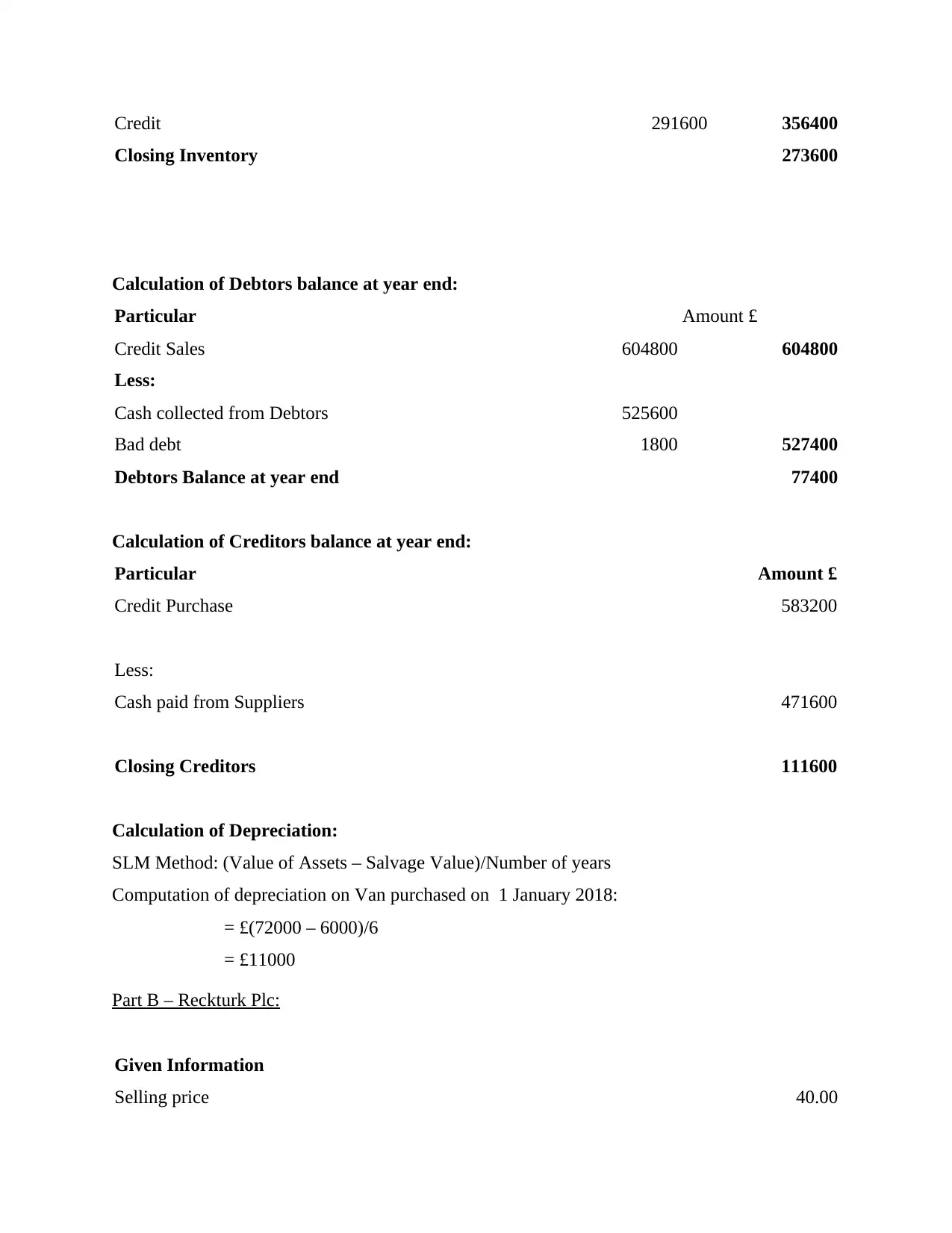

Part B – Reckturk Plc:

Given Information

Selling price 40.00

Closing Inventory 273600

Calculation of Debtors balance at year end:

Particular Amount £

Credit Sales 604800 604800

Less:

Cash collected from Debtors 525600

Bad debt 1800 527400

Debtors Balance at year end 77400

Calculation of Creditors balance at year end:

Particular Amount £

Credit Purchase 583200

Less:

Cash paid from Suppliers 471600

Closing Creditors 111600

Calculation of Depreciation:

SLM Method: (Value of Assets – Salvage Value)/Number of years

Computation of depreciation on Van purchased on 1 January 2018:

= £(72000 – 6000)/6

= £11000

Part B – Reckturk Plc:

Given Information

Selling price 40.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current Production (Units) 78000.00

Budgeted production for next year 60000.00

Costs

Variable Costs (per unit) 15.75

Labour 8.85

Variable Overheads 5.55

Fixed Costs

Production 177000.00

Selling etc. 142800.00

A. Calculation of contribution per wardrobe makes towards covering fixed costs if selling price

is £40:

Rate per Unit Actual Budgeted

Units 78000 60000

Total Revenues 40.00 3120000.00 2400000.00

Material 15.75 1228500.00 945000.00

Labour 8.85 690300.00 531000.00

Variable Overhead 5.55 432900.00 333000.00

Total Variable Costs 2351700.00 1809000.00

Contribution 768300.00 591000.00

Contribution per unit 9.85 9.85

Budgeted production for next year 60000.00

Costs

Variable Costs (per unit) 15.75

Labour 8.85

Variable Overheads 5.55

Fixed Costs

Production 177000.00

Selling etc. 142800.00

A. Calculation of contribution per wardrobe makes towards covering fixed costs if selling price

is £40:

Rate per Unit Actual Budgeted

Units 78000 60000

Total Revenues 40.00 3120000.00 2400000.00

Material 15.75 1228500.00 945000.00

Labour 8.85 690300.00 531000.00

Variable Overhead 5.55 432900.00 333000.00

Total Variable Costs 2351700.00 1809000.00

Contribution 768300.00 591000.00

Contribution per unit 9.85 9.85

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

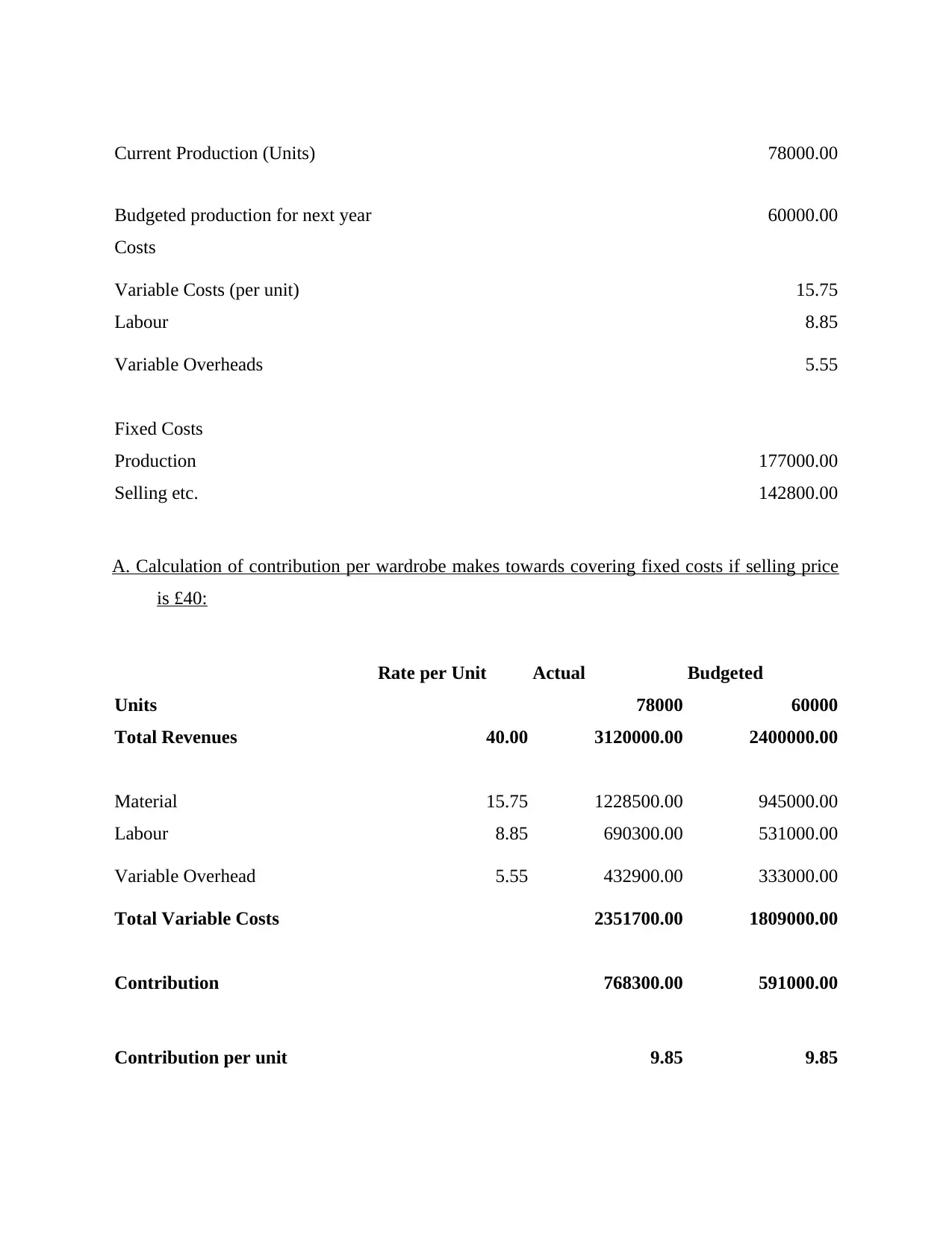

B. Computation of break-even point and margin of safety in terms of both units of wardrobe and

revenue if selling price is £40:

Break-even point (Units of Wardrobe):

Fixed Costs: Amount Amount

Production 177000.00 177000.00

Selling 142800.00 142800.00

Total Fixed Costs 319800.00 319800.00

Contribution per unit 9.85 9.85

Break Even Point

= Fixed Cost / Contribution

per unit 32467.01 32467.01

Break-even point (Revenue):

Sales per Unit 40.00 40.00

Contribution per unit 9.85 9.85

Contribution Margin

(Contribution per unit/ Sales

per unit)*100 24.63% 24.63%

Total Fixed Costs 319800.00 319800.00

Break Even Point

Total Fixed

Costs/Contribution Margin 1298680.20 1298680.20

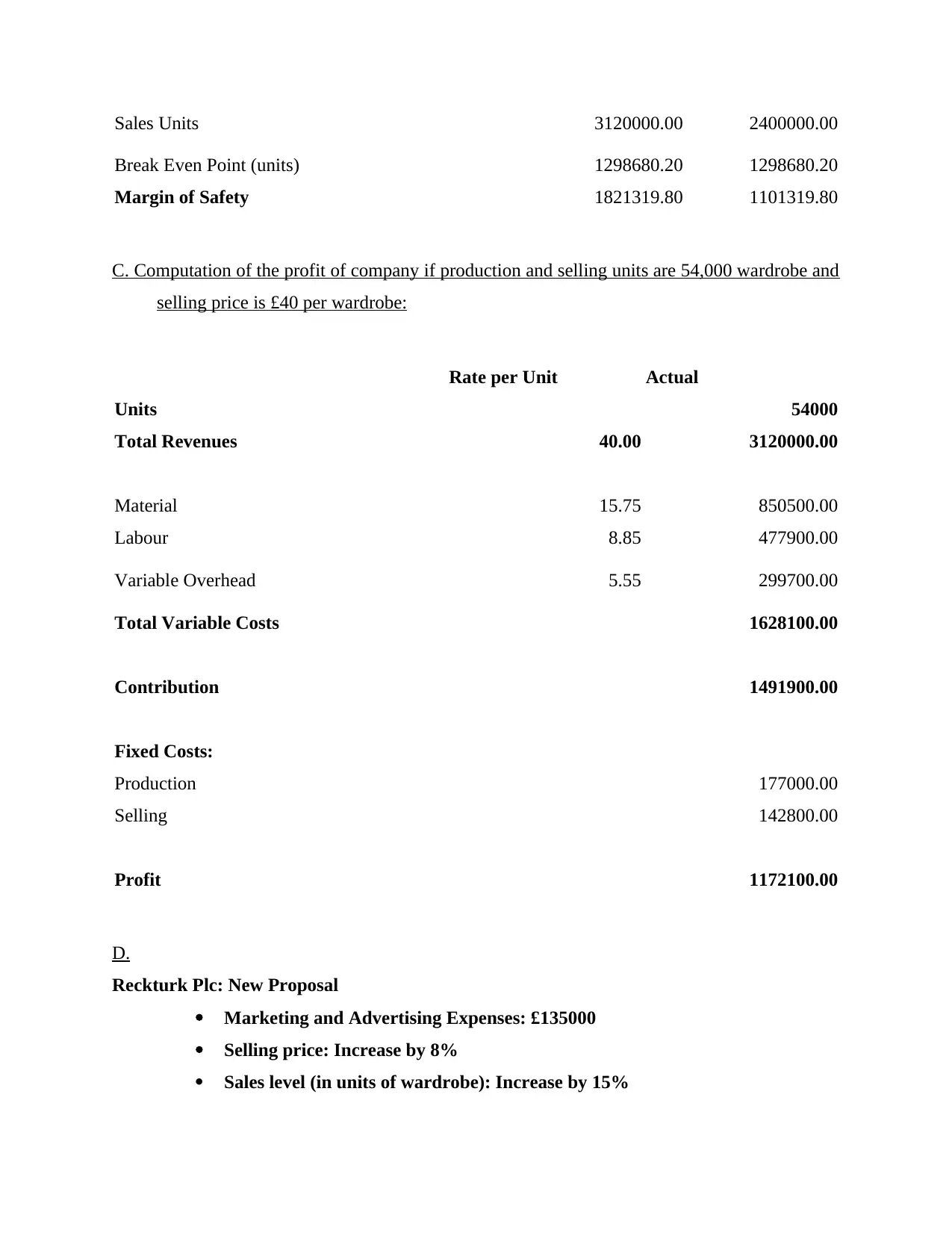

Margin of Safety (Units of Wardrobe):

Actual Budgeted

Sales Units 78000.00 60000.00

Break Even Point (units) 32467.01 32467.01

Margin of Safety 45532.99 27532.99

Margin of Safety (Revenue):

Actual Budgeted

revenue if selling price is £40:

Break-even point (Units of Wardrobe):

Fixed Costs: Amount Amount

Production 177000.00 177000.00

Selling 142800.00 142800.00

Total Fixed Costs 319800.00 319800.00

Contribution per unit 9.85 9.85

Break Even Point

= Fixed Cost / Contribution

per unit 32467.01 32467.01

Break-even point (Revenue):

Sales per Unit 40.00 40.00

Contribution per unit 9.85 9.85

Contribution Margin

(Contribution per unit/ Sales

per unit)*100 24.63% 24.63%

Total Fixed Costs 319800.00 319800.00

Break Even Point

Total Fixed

Costs/Contribution Margin 1298680.20 1298680.20

Margin of Safety (Units of Wardrobe):

Actual Budgeted

Sales Units 78000.00 60000.00

Break Even Point (units) 32467.01 32467.01

Margin of Safety 45532.99 27532.99

Margin of Safety (Revenue):

Actual Budgeted

Sales Units 3120000.00 2400000.00

Break Even Point (units) 1298680.20 1298680.20

Margin of Safety 1821319.80 1101319.80

C. Computation of the profit of company if production and selling units are 54,000 wardrobe and

selling price is £40 per wardrobe:

Rate per Unit Actual

Units 54000

Total Revenues 40.00 3120000.00

Material 15.75 850500.00

Labour 8.85 477900.00

Variable Overhead 5.55 299700.00

Total Variable Costs 1628100.00

Contribution 1491900.00

Fixed Costs:

Production 177000.00

Selling 142800.00

Profit 1172100.00

D.

Reckturk Plc: New Proposal

Marketing and Advertising Expenses: £135000

Selling price: Increase by 8%

Sales level (in units of wardrobe): Increase by 15%

Break Even Point (units) 1298680.20 1298680.20

Margin of Safety 1821319.80 1101319.80

C. Computation of the profit of company if production and selling units are 54,000 wardrobe and

selling price is £40 per wardrobe:

Rate per Unit Actual

Units 54000

Total Revenues 40.00 3120000.00

Material 15.75 850500.00

Labour 8.85 477900.00

Variable Overhead 5.55 299700.00

Total Variable Costs 1628100.00

Contribution 1491900.00

Fixed Costs:

Production 177000.00

Selling 142800.00

Profit 1172100.00

D.

Reckturk Plc: New Proposal

Marketing and Advertising Expenses: £135000

Selling price: Increase by 8%

Sales level (in units of wardrobe): Increase by 15%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

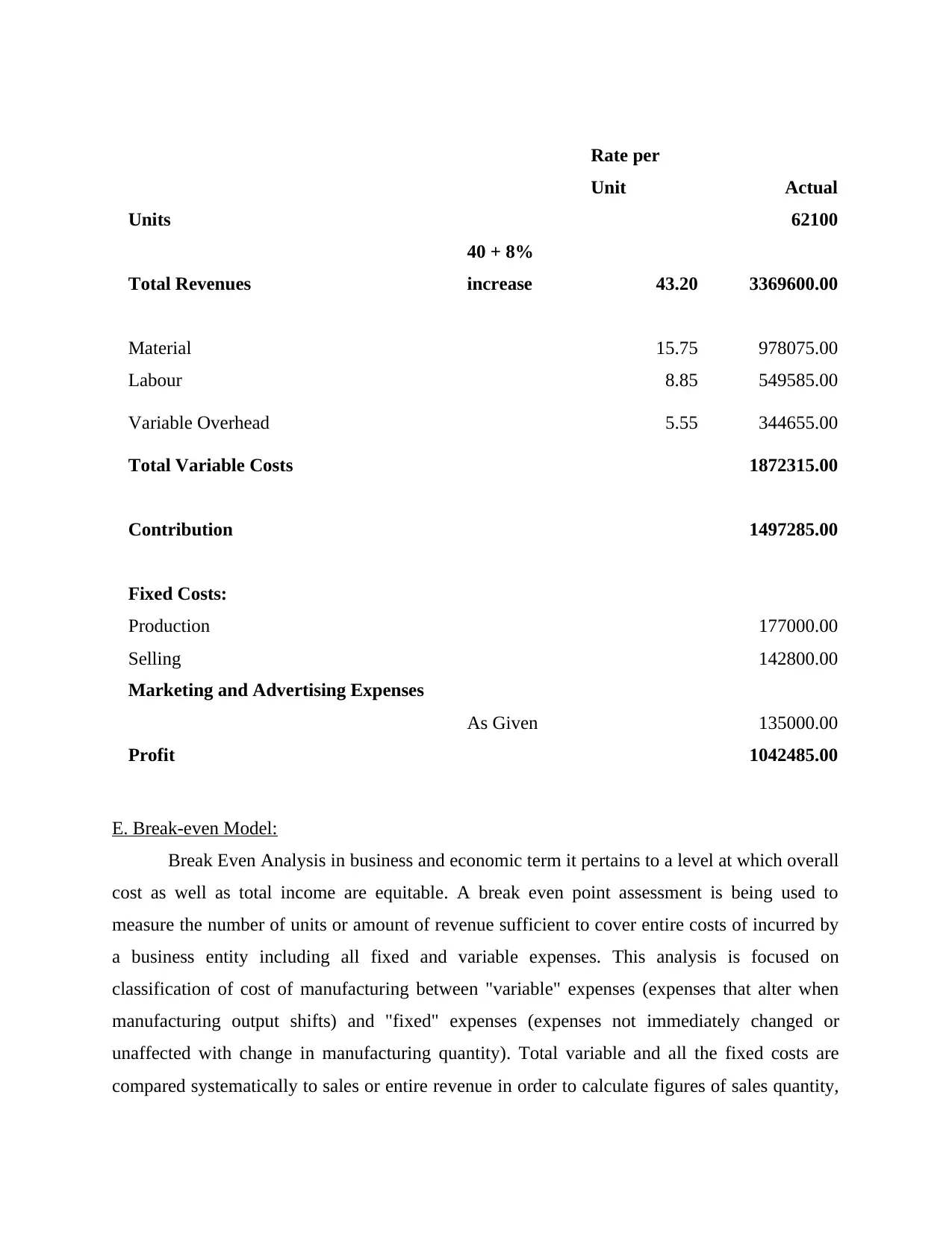

Rate per

Unit Actual

Units 62100

Total Revenues

40 + 8%

increase 43.20 3369600.00

Material 15.75 978075.00

Labour 8.85 549585.00

Variable Overhead 5.55 344655.00

Total Variable Costs 1872315.00

Contribution 1497285.00

Fixed Costs:

Production 177000.00

Selling 142800.00

Marketing and Advertising Expenses

As Given 135000.00

Profit 1042485.00

E. Break-even Model:

Break Even Analysis in business and economic term it pertains to a level at which overall

cost as well as total income are equitable. A break even point assessment is being used to

measure the number of units or amount of revenue sufficient to cover entire costs of incurred by

a business entity including all fixed and variable expenses. This analysis is focused on

classification of cost of manufacturing between "variable" expenses (expenses that alter when

manufacturing output shifts) and "fixed" expenses (expenses not immediately changed or

unaffected with change in manufacturing quantity). Total variable and all the fixed costs are

compared systematically to sales or entire revenue in order to calculate figures of sales quantity,

Unit Actual

Units 62100

Total Revenues

40 + 8%

increase 43.20 3369600.00

Material 15.75 978075.00

Labour 8.85 549585.00

Variable Overhead 5.55 344655.00

Total Variable Costs 1872315.00

Contribution 1497285.00

Fixed Costs:

Production 177000.00

Selling 142800.00

Marketing and Advertising Expenses

As Given 135000.00

Profit 1042485.00

E. Break-even Model:

Break Even Analysis in business and economic term it pertains to a level at which overall

cost as well as total income are equitable. A break even point assessment is being used to

measure the number of units or amount of revenue sufficient to cover entire costs of incurred by

a business entity including all fixed and variable expenses. This analysis is focused on

classification of cost of manufacturing between "variable" expenses (expenses that alter when

manufacturing output shifts) and "fixed" expenses (expenses not immediately changed or

unaffected with change in manufacturing quantity). Total variable and all the fixed costs are

compared systematically to sales or entire revenue in order to calculate figures of sales quantity,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales price or outputs level at which enterprise does not make any profit or any loss (Maskell,

Baggaley and Grasso, 2012). It also facilitates determining what quantity is required to sold,

annually or monthly, to recover cost incurred in making such sales. Break even point can be

presented in number of units and amount of revenue. Formulas which help in assessing a break

even point is discussed as follows:

Break even units = Fixed costs / (Sales price per unit – Variable cost per unit)

Break-even point ( Revenue) = Fixed costs / Contribution Margin

Where:

Fixed costs are expenses which do not fluctuate with changes in output.

Sales price p.u. Implies to selling price of each single unit.

Variable cost p.u. is variable expenses associated with manufacturing of single unit.

Contribution Margin = Contribution per unit x 100

Sales per unit

Contribution per unit = Sales price per unit less Variable cost per unit

Break even model can be applied by all form of business entities. It is simple method

which provides appropriate result irrespective of nature of business. Further it act as base for

calculating margin of safety. Because executives understand that fixed and variable costs

influence company profit margins, with the aid of break-even analysis, they could see the impact

of cost adjustments. It enables them to determine the level to which change in costs or cost

adjustments influence profit margins and break-even (Di Pietra, McLeay and Ronen, 2013). The

break-even point could be affected by any shift in sales price. For illustration, the number of

units required to be sold to break-even will be decreased if the sale price is expanded. Similarly,

a company requires to buy more to break-even if the sale price is decreased.

As in given case of Reckturk Plc, from calculation of break even point it has been

analysed that at production and sales level of 78000 units company's break-even sales in units is

32467.01 or 32467 units approx and break-even sales is pound 1298680.20. Which implies that

company is required to maintain their sales and production level at 32467 at least to avoid any

loss. Also revenue benchmark of 1298680.20 is necessary to avoid net loss figures.

Baggaley and Grasso, 2012). It also facilitates determining what quantity is required to sold,

annually or monthly, to recover cost incurred in making such sales. Break even point can be

presented in number of units and amount of revenue. Formulas which help in assessing a break

even point is discussed as follows:

Break even units = Fixed costs / (Sales price per unit – Variable cost per unit)

Break-even point ( Revenue) = Fixed costs / Contribution Margin

Where:

Fixed costs are expenses which do not fluctuate with changes in output.

Sales price p.u. Implies to selling price of each single unit.

Variable cost p.u. is variable expenses associated with manufacturing of single unit.

Contribution Margin = Contribution per unit x 100

Sales per unit

Contribution per unit = Sales price per unit less Variable cost per unit

Break even model can be applied by all form of business entities. It is simple method

which provides appropriate result irrespective of nature of business. Further it act as base for

calculating margin of safety. Because executives understand that fixed and variable costs

influence company profit margins, with the aid of break-even analysis, they could see the impact

of cost adjustments. It enables them to determine the level to which change in costs or cost

adjustments influence profit margins and break-even (Di Pietra, McLeay and Ronen, 2013). The

break-even point could be affected by any shift in sales price. For illustration, the number of

units required to be sold to break-even will be decreased if the sale price is expanded. Similarly,

a company requires to buy more to break-even if the sale price is decreased.

As in given case of Reckturk Plc, from calculation of break even point it has been

analysed that at production and sales level of 78000 units company's break-even sales in units is

32467.01 or 32467 units approx and break-even sales is pound 1298680.20. Which implies that

company is required to maintain their sales and production level at 32467 at least to avoid any

loss. Also revenue benchmark of 1298680.20 is necessary to avoid net loss figures.

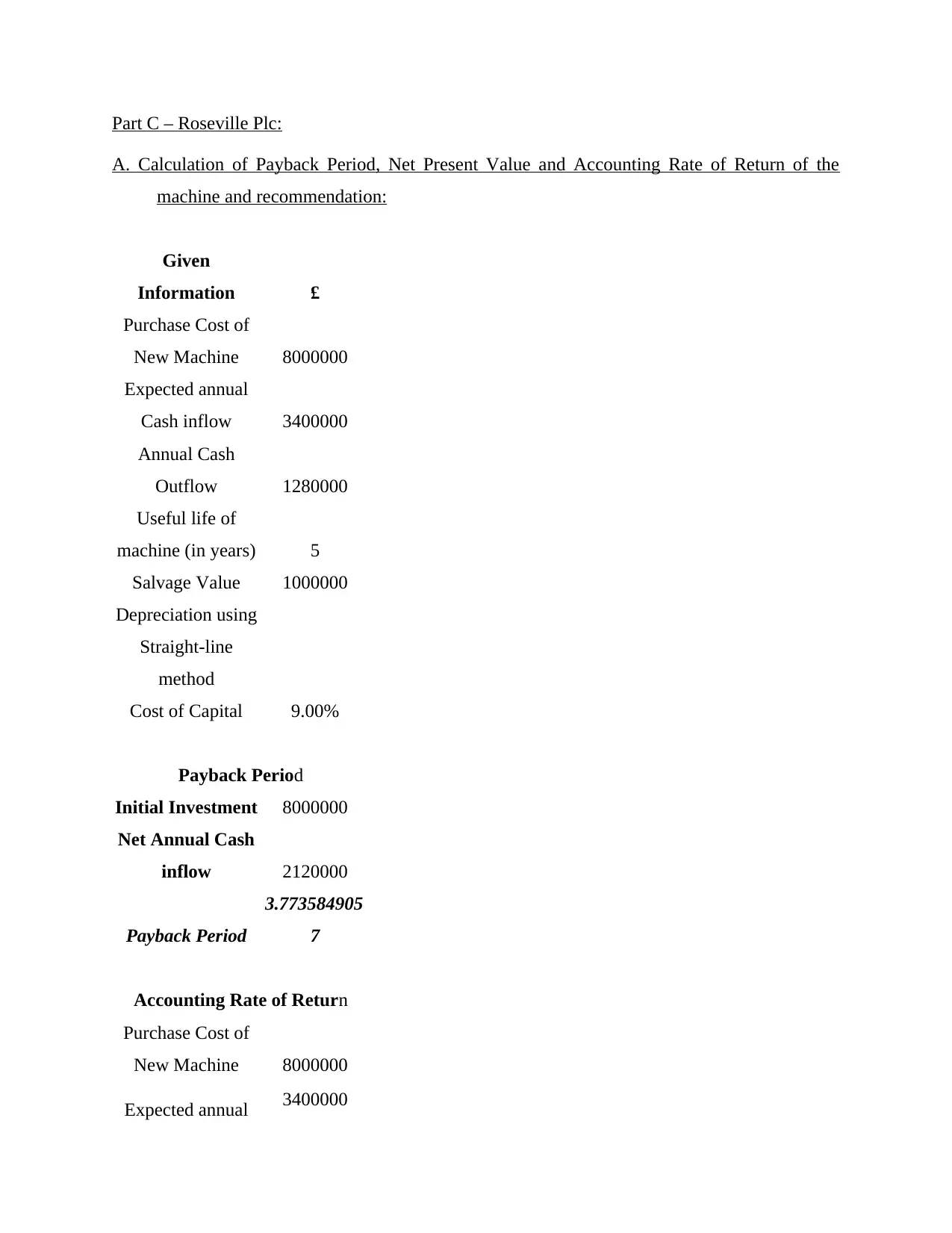

Part C – Roseville Plc:

A. Calculation of Payback Period, Net Present Value and Accounting Rate of Return of the

machine and recommendation:

Given

Information £

Purchase Cost of

New Machine 8000000

Expected annual

Cash inflow 3400000

Annual Cash

Outflow 1280000

Useful life of

machine (in years) 5

Salvage Value 1000000

Depreciation using

Straight-line

method

Cost of Capital 9.00%

Payback Period

Initial Investment 8000000

Net Annual Cash

inflow 2120000

Payback Period

3.773584905

7

Accounting Rate of Return

Purchase Cost of

New Machine 8000000

Expected annual 3400000

A. Calculation of Payback Period, Net Present Value and Accounting Rate of Return of the

machine and recommendation:

Given

Information £

Purchase Cost of

New Machine 8000000

Expected annual

Cash inflow 3400000

Annual Cash

Outflow 1280000

Useful life of

machine (in years) 5

Salvage Value 1000000

Depreciation using

Straight-line

method

Cost of Capital 9.00%

Payback Period

Initial Investment 8000000

Net Annual Cash

inflow 2120000

Payback Period

3.773584905

7

Accounting Rate of Return

Purchase Cost of

New Machine 8000000

Expected annual 3400000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.