Financial Reporting: IFRS, Stakeholders, Financial Statement Analysis

VerifiedAdded on 2020/06/04

|14

|3556

|241

Report

AI Summary

This report provides a comprehensive overview of financial reporting, focusing on the objectives of financial reporting, key principles of the regulatory framework, and the main stakeholders involved. It explores how financial reporting achieves its objectives and includes an analysis of financial statements, such as the income statement, balance sheet, and cash flow statement, alongside their interpretation. The report also highlights the differences between IAS and IFRS, the benefits of IFRS adoption, and factors influencing compliance. The task involves in-depth examination of financial reporting standards, emphasizing the significance of financial statements for decision-making by investors and management. The report also covers the importance of IFRS in providing a standardized approach to financial reporting, ensuring transparency, and facilitating comparisons across different companies and jurisdictions. Moreover, the report examines the impact of financial reporting on business operations, including the use of financial statements for strategic planning and performance evaluation. The report also includes the financial statements of a company for better understanding and interpretation. Finally, the report discusses the role of stakeholders in financial reporting and the benefits they receive, such as reliable information for investment decisions.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Financial reporting objectives............................................................................................1

2. Key principles of regulatory framework............................................................................2

3. Main Stakeholders and benefits received by them.............................................................3

4. Achievement of objectives by using financial reporting....................................................3

5. Financial statements of company.......................................................................................4

6. Interpretation by using financial statements.......................................................................6

7. Difference among IAS and IFRS.......................................................................................8

8. Benefits of IFRS.................................................................................................................9

9. Compliance of IFRS and factors influencing them..........................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1. Financial reporting objectives............................................................................................1

2. Key principles of regulatory framework............................................................................2

3. Main Stakeholders and benefits received by them.............................................................3

4. Achievement of objectives by using financial reporting....................................................3

5. Financial statements of company.......................................................................................4

6. Interpretation by using financial statements.......................................................................6

7. Difference among IAS and IFRS.......................................................................................8

8. Benefits of IFRS.................................................................................................................9

9. Compliance of IFRS and factors influencing them..........................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Finance is the major thing under this business as this makes its operations to run

effectively. Without finance nothing can happen. But, for effective running of business, few

international bodies have made certain financial reporting standards so that the firm can adhere

with them while having financial reporting. Financial reporting includes income statements,

balance sheet and cash flow statements (Agoglia, Doupnik and Tsakumis, 2011). Various

international bodies forms so many laws and regulations regarding under which various

standards are required to be adhere by each company while making financial statements. under

this report, various IFRS standards have been elaboratesd in details in order to make their

business operations effective.

TASK

1. Financial reporting objectives

There are various standards that needs to adhere by each company during framing of

financial statements. This has also been seen that the International financial reporting standards

have formed various regulatory standards for framing financial statements. On the basis of IFRS

guidelines, company made financial statements. Financial statements are the major thing by

which investors and other concerned parties take their investment decisions regarding the firm.

This is the main tool which reflects the genuine picture of firm. However, there are various

issues or conflicts for which these guidelines are not specified. In that case, special guideline

shall be issued to deal with these kinds of issues within a company. Tesco plc. needs to adopt

various reporting standards while making the financial statements. Tesco on the basis of financial

statements can make various strategies and also get to know about its financial positions in an

effective manner. With the help of these standards or policies, company can present their entire

information in a systematic manner along with various concepts like determination, measurement

and definition of whole expenses as well as revenues, assets and liabilities are demonstrated as

per the IFRS framework.

By applying these standards in business, Tesco plc is able to manage its business

activities in the most effective manner, and financial statement can be used by the outside

investor and other management for the decision making. Such financial reporting will also assist

1

Finance is the major thing under this business as this makes its operations to run

effectively. Without finance nothing can happen. But, for effective running of business, few

international bodies have made certain financial reporting standards so that the firm can adhere

with them while having financial reporting. Financial reporting includes income statements,

balance sheet and cash flow statements (Agoglia, Doupnik and Tsakumis, 2011). Various

international bodies forms so many laws and regulations regarding under which various

standards are required to be adhere by each company while making financial statements. under

this report, various IFRS standards have been elaboratesd in details in order to make their

business operations effective.

TASK

1. Financial reporting objectives

There are various standards that needs to adhere by each company during framing of

financial statements. This has also been seen that the International financial reporting standards

have formed various regulatory standards for framing financial statements. On the basis of IFRS

guidelines, company made financial statements. Financial statements are the major thing by

which investors and other concerned parties take their investment decisions regarding the firm.

This is the main tool which reflects the genuine picture of firm. However, there are various

issues or conflicts for which these guidelines are not specified. In that case, special guideline

shall be issued to deal with these kinds of issues within a company. Tesco plc. needs to adopt

various reporting standards while making the financial statements. Tesco on the basis of financial

statements can make various strategies and also get to know about its financial positions in an

effective manner. With the help of these standards or policies, company can present their entire

information in a systematic manner along with various concepts like determination, measurement

and definition of whole expenses as well as revenues, assets and liabilities are demonstrated as

per the IFRS framework.

By applying these standards in business, Tesco plc is able to manage its business

activities in the most effective manner, and financial statement can be used by the outside

investor and other management for the decision making. Such financial reporting will also assist

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in identifying the financial performance and make the firm to run effectually (Altamuron and

Beatty, 2010).

2. Key principles of regulatory framework

To gain stability in an organization regarding financial reporting, the organization should

adopt IFRS rules issued by the IASB and FASB which helps the auditors to ensure that all the

standards which are prescribed by the IASB are followed by the organization in a proper way.

The New Revenue Recognition Standard- Retail & Consumer Product:

IFRS 15 Revenue from Contracts with Customers is the standard which is released by the

IASB that was an outcome of a collective project with the FASB. The new standards, which are

considerably consistent which will replace virtually entire revenue recognition standards in IFRS

and US Generally Accepted Accounting Principles.

IFRS 15 reflects the accounting treatment for entire revenue arising from contracts with

customers. This influence whole entities which makes contracts to render goods or services to

their customers. The standard also furnish a model for the identification and knowing of profits

and losses which arise on the sale of definite non-financial assets, like property and equipment

and intangibles.

Summary of the new standard:

IFRS 15 determines the need under which a firm must use to measure and recognize

revenue and the concerned cash flows. The core principle of the standard is that a firm would

recognize earnings at an amount which shows the consideration under which the firm expect to

be entitled in exchange for transferring promised goods or services to a customer (Ball,

Jayaraman and Shivakumar, 2012). The principles in IFRS 15 are applied using the following

five steps:

1. Identify the contract(s) with a customer

2. Identify the performance obligations in the contract(s)

3. Determine the transaction price

4. Allocate the transaction price to the performance obligations

5. Recognize revenue when (or as) the entity satisfies each performance obligation.

This standard gives proper guidance and benefit to the organization to achieve their goals

and objectives by keeping in mind the requirements of the today’s customer. This standard also

2

Beatty, 2010).

2. Key principles of regulatory framework

To gain stability in an organization regarding financial reporting, the organization should

adopt IFRS rules issued by the IASB and FASB which helps the auditors to ensure that all the

standards which are prescribed by the IASB are followed by the organization in a proper way.

The New Revenue Recognition Standard- Retail & Consumer Product:

IFRS 15 Revenue from Contracts with Customers is the standard which is released by the

IASB that was an outcome of a collective project with the FASB. The new standards, which are

considerably consistent which will replace virtually entire revenue recognition standards in IFRS

and US Generally Accepted Accounting Principles.

IFRS 15 reflects the accounting treatment for entire revenue arising from contracts with

customers. This influence whole entities which makes contracts to render goods or services to

their customers. The standard also furnish a model for the identification and knowing of profits

and losses which arise on the sale of definite non-financial assets, like property and equipment

and intangibles.

Summary of the new standard:

IFRS 15 determines the need under which a firm must use to measure and recognize

revenue and the concerned cash flows. The core principle of the standard is that a firm would

recognize earnings at an amount which shows the consideration under which the firm expect to

be entitled in exchange for transferring promised goods or services to a customer (Ball,

Jayaraman and Shivakumar, 2012). The principles in IFRS 15 are applied using the following

five steps:

1. Identify the contract(s) with a customer

2. Identify the performance obligations in the contract(s)

3. Determine the transaction price

4. Allocate the transaction price to the performance obligations

5. Recognize revenue when (or as) the entity satisfies each performance obligation.

This standard gives proper guidance and benefit to the organization to achieve their goals

and objectives by keeping in mind the requirements of the today’s customer. This standard also

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps the auditor to make sure that the organization follows the accounting standard prescribed

by the IFRS.

3. Main Stakeholders and benefits received by them

Whenever the organization earning more returns in their operations, it is required that all

the information regarding earnings shall be made available to the stakeholders of the

organization. This information helps the investors to take the decision regarding investment.

Organization should also states that their upcoming projects and share each information to their

stakeholders to keep their good reputation in the mind of the stakeholders.

Organization provides proper financial statement of each year through which the

investors can compare current scenario with past scenario of the organization. Financial

statement also helps the investors that the organization meets its liabilities and obligations on

time or not. It’s shows financial soundness of the organization so, that the investors take right

decisions regarding their investment.

Cash flow statement shows the investors that how much cash is available to the

organization and also tells him that the available funds are utilized in appropriate manner (Barth

and Landsman, 2010).

4. Achievement of objectives by using financial reporting

In an organization, there are various objectives which are required to be achieved and this

can be done with the use of financial reporting according with standards. This is because; it helps

in the evaluation of performance by comparing it with the past data which is available to the

organization in a proper manner that is audited by the auditor. By evaluating the performance,

organization can find out mistakes and rectify them so that future performance runs without any

error and omission.

Together with this, investors are attracted and transparency can be attained by using all

the IFRS standards which are mentioned under financial reporting of the organization through

which the investment is increases and the funds are utilizes in the futures operations.

All these rules are framed by the regulatory bodies and organization should follow all the rules in

a prescribed manner because it helps auditors and others stakeholders to find out organization’s

performance in market.

Financial reporting helps the investors and other stakeholders to take decisions regarding

investment and earnings from the organization. With the help of financial reporting, investors

3

by the IFRS.

3. Main Stakeholders and benefits received by them

Whenever the organization earning more returns in their operations, it is required that all

the information regarding earnings shall be made available to the stakeholders of the

organization. This information helps the investors to take the decision regarding investment.

Organization should also states that their upcoming projects and share each information to their

stakeholders to keep their good reputation in the mind of the stakeholders.

Organization provides proper financial statement of each year through which the

investors can compare current scenario with past scenario of the organization. Financial

statement also helps the investors that the organization meets its liabilities and obligations on

time or not. It’s shows financial soundness of the organization so, that the investors take right

decisions regarding their investment.

Cash flow statement shows the investors that how much cash is available to the

organization and also tells him that the available funds are utilized in appropriate manner (Barth

and Landsman, 2010).

4. Achievement of objectives by using financial reporting

In an organization, there are various objectives which are required to be achieved and this

can be done with the use of financial reporting according with standards. This is because; it helps

in the evaluation of performance by comparing it with the past data which is available to the

organization in a proper manner that is audited by the auditor. By evaluating the performance,

organization can find out mistakes and rectify them so that future performance runs without any

error and omission.

Together with this, investors are attracted and transparency can be attained by using all

the IFRS standards which are mentioned under financial reporting of the organization through

which the investment is increases and the funds are utilizes in the futures operations.

All these rules are framed by the regulatory bodies and organization should follow all the rules in

a prescribed manner because it helps auditors and others stakeholders to find out organization’s

performance in market.

Financial reporting helps the investors and other stakeholders to take decisions regarding

investment and earnings from the organization. With the help of financial reporting, investors

3

compare with the other organization in order to take the investment decisions. (Cheng, Dhaliwal

and Zhang, 2013).

Due to this, organization can improve their performance and achieve their objectives in a

time. Organization performance regarding their operations will be improving and this will

enhance profitability of the business.

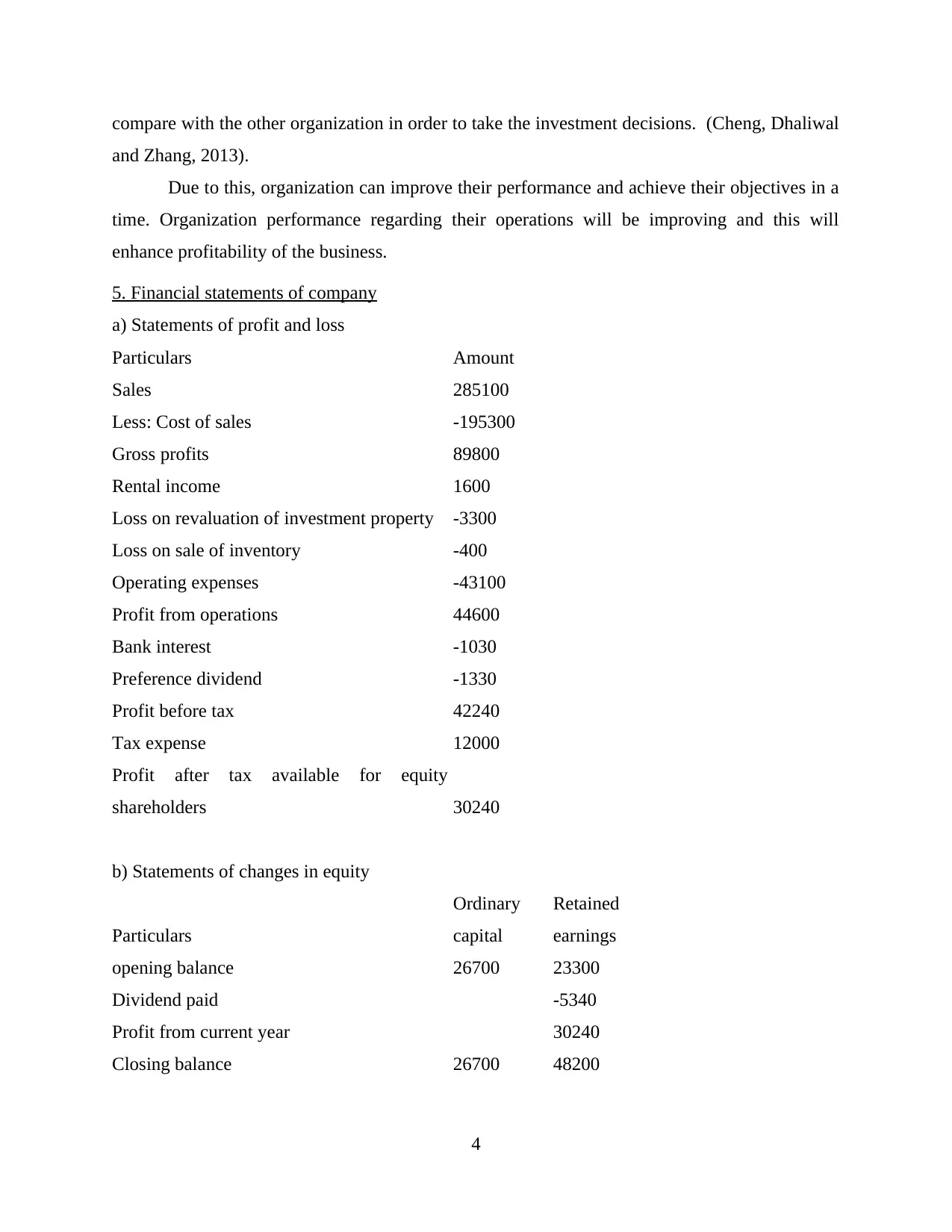

5. Financial statements of company

a) Statements of profit and loss

Particulars Amount

Sales 285100

Less: Cost of sales -195300

Gross profits 89800

Rental income 1600

Loss on revaluation of investment property -3300

Loss on sale of inventory -400

Operating expenses -43100

Profit from operations 44600

Bank interest -1030

Preference dividend -1330

Profit before tax 42240

Tax expense 12000

Profit after tax available for equity

shareholders 30240

b) Statements of changes in equity

Particulars

Ordinary

capital

Retained

earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

4

and Zhang, 2013).

Due to this, organization can improve their performance and achieve their objectives in a

time. Organization performance regarding their operations will be improving and this will

enhance profitability of the business.

5. Financial statements of company

a) Statements of profit and loss

Particulars Amount

Sales 285100

Less: Cost of sales -195300

Gross profits 89800

Rental income 1600

Loss on revaluation of investment property -3300

Loss on sale of inventory -400

Operating expenses -43100

Profit from operations 44600

Bank interest -1030

Preference dividend -1330

Profit before tax 42240

Tax expense 12000

Profit after tax available for equity

shareholders 30240

b) Statements of changes in equity

Particulars

Ordinary

capital

Retained

earnings

opening balance 26700 23300

Dividend paid -5340

Profit from current year 30240

Closing balance 26700 48200

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

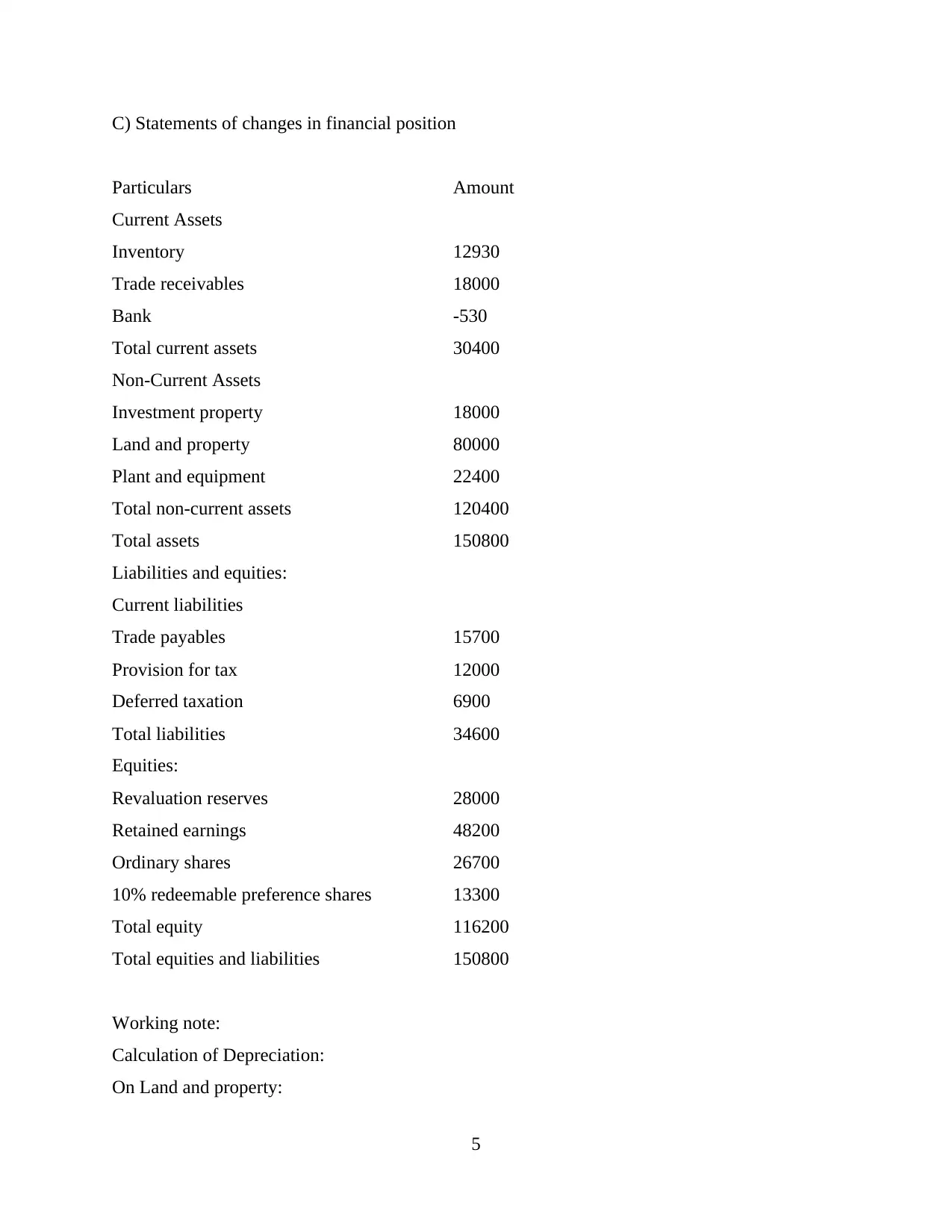

C) Statements of changes in financial position

Particulars Amount

Current Assets

Inventory 12930

Trade receivables 18000

Bank -530

Total current assets 30400

Non-Current Assets

Investment property 18000

Land and property 80000

Plant and equipment 22400

Total non-current assets 120400

Total assets 150800

Liabilities and equities:

Current liabilities

Trade payables 15700

Provision for tax 12000

Deferred taxation 6900

Total liabilities 34600

Equities:

Revaluation reserves 28000

Retained earnings 48200

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

Working note:

Calculation of Depreciation:

On Land and property:

5

Particulars Amount

Current Assets

Inventory 12930

Trade receivables 18000

Bank -530

Total current assets 30400

Non-Current Assets

Investment property 18000

Land and property 80000

Plant and equipment 22400

Total non-current assets 120400

Total assets 150800

Liabilities and equities:

Current liabilities

Trade payables 15700

Provision for tax 12000

Deferred taxation 6900

Total liabilities 34600

Equities:

Revaluation reserves 28000

Retained earnings 48200

Ordinary shares 26700

10% redeemable preference shares 13300

Total equity 116200

Total equities and liabilities 150800

Working note:

Calculation of Depreciation:

On Land and property:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

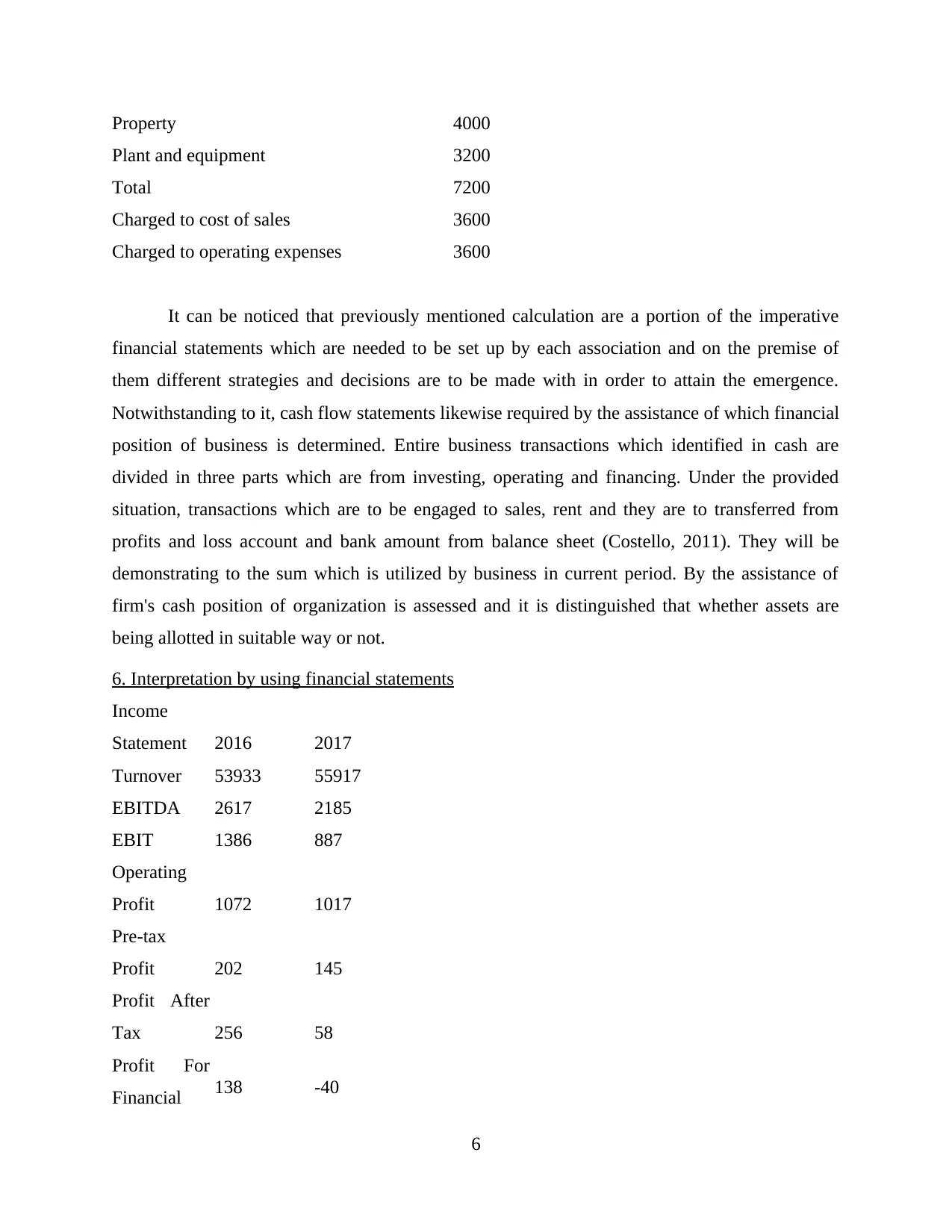

Property 4000

Plant and equipment 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

It can be noticed that previously mentioned calculation are a portion of the imperative

financial statements which are needed to be set up by each association and on the premise of

them different strategies and decisions are to be made with in order to attain the emergence.

Notwithstanding to it, cash flow statements likewise required by the assistance of which financial

position of business is determined. Entire business transactions which identified in cash are

divided in three parts which are from investing, operating and financing. Under the provided

situation, transactions which are to be engaged to sales, rent and they are to transferred from

profits and loss account and bank amount from balance sheet (Costello, 2011). They will be

demonstrating to the sum which is utilized by business in current period. By the assistance of

firm's cash position of organization is assessed and it is distinguished that whether assets are

being allotted in suitable way or not.

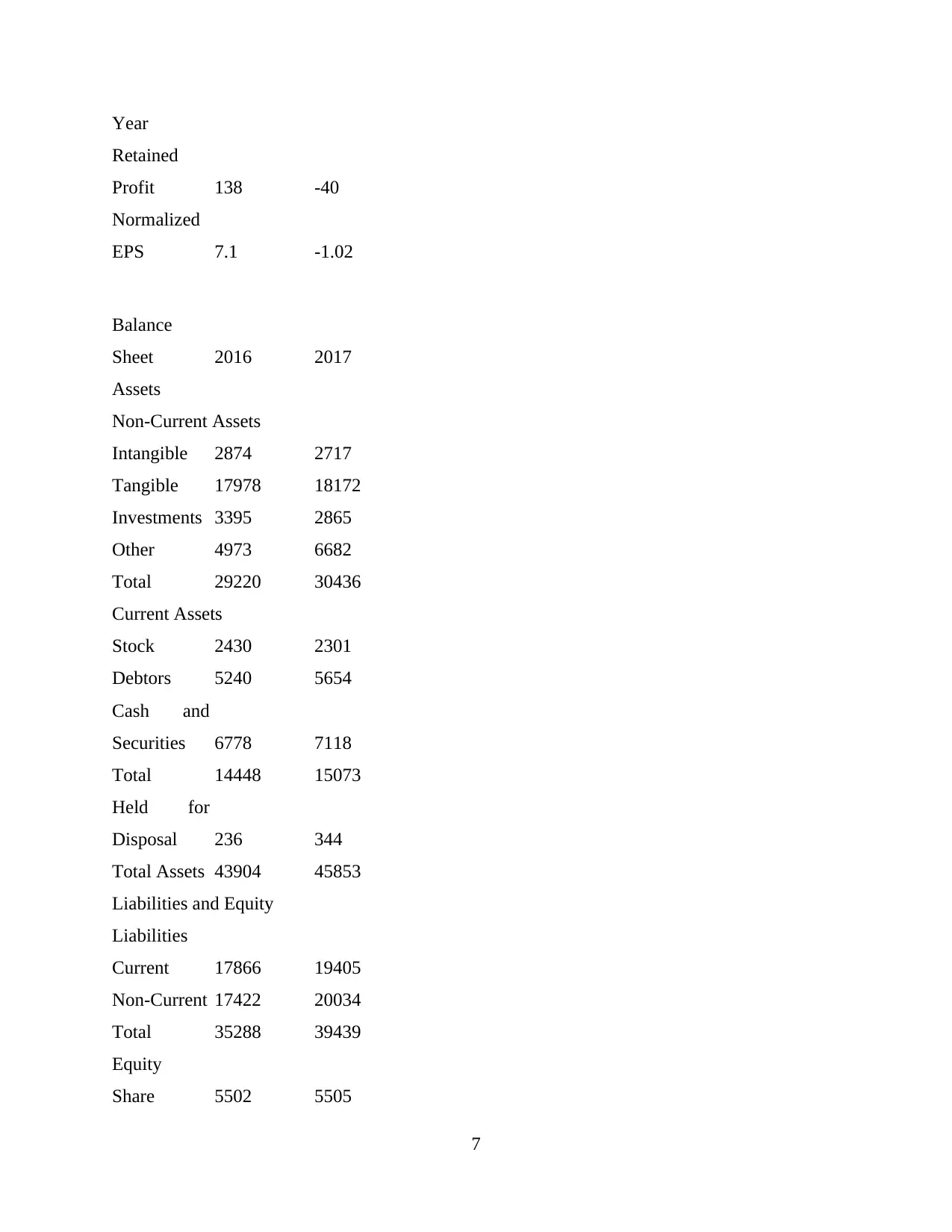

6. Interpretation by using financial statements

Income

Statement 2016 2017

Turnover 53933 55917

EBITDA 2617 2185

EBIT 1386 887

Operating

Profit 1072 1017

Pre-tax

Profit 202 145

Profit After

Tax 256 58

Profit For

Financial 138 -40

6

Plant and equipment 3200

Total 7200

Charged to cost of sales 3600

Charged to operating expenses 3600

It can be noticed that previously mentioned calculation are a portion of the imperative

financial statements which are needed to be set up by each association and on the premise of

them different strategies and decisions are to be made with in order to attain the emergence.

Notwithstanding to it, cash flow statements likewise required by the assistance of which financial

position of business is determined. Entire business transactions which identified in cash are

divided in three parts which are from investing, operating and financing. Under the provided

situation, transactions which are to be engaged to sales, rent and they are to transferred from

profits and loss account and bank amount from balance sheet (Costello, 2011). They will be

demonstrating to the sum which is utilized by business in current period. By the assistance of

firm's cash position of organization is assessed and it is distinguished that whether assets are

being allotted in suitable way or not.

6. Interpretation by using financial statements

Income

Statement 2016 2017

Turnover 53933 55917

EBITDA 2617 2185

EBIT 1386 887

Operating

Profit 1072 1017

Pre-tax

Profit 202 145

Profit After

Tax 256 58

Profit For

Financial 138 -40

6

Year

Retained

Profit 138 -40

Normalized

EPS 7.1 -1.02

Balance

Sheet 2016 2017

Assets

Non-Current Assets

Intangible 2874 2717

Tangible 17978 18172

Investments 3395 2865

Other 4973 6682

Total 29220 30436

Current Assets

Stock 2430 2301

Debtors 5240 5654

Cash and

Securities 6778 7118

Total 14448 15073

Held for

Disposal 236 344

Total Assets 43904 45853

Liabilities and Equity

Liabilities

Current 17866 19405

Non-Current 17422 20034

Total 35288 39439

Equity

Share 5502 5505

7

Retained

Profit 138 -40

Normalized

EPS 7.1 -1.02

Balance

Sheet 2016 2017

Assets

Non-Current Assets

Intangible 2874 2717

Tangible 17978 18172

Investments 3395 2865

Other 4973 6682

Total 29220 30436

Current Assets

Stock 2430 2301

Debtors 5240 5654

Cash and

Securities 6778 7118

Total 14448 15073

Held for

Disposal 236 344

Total Assets 43904 45853

Liabilities and Equity

Liabilities

Current 17866 19405

Non-Current 17422 20034

Total 35288 39439

Equity

Share 5502 5505

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

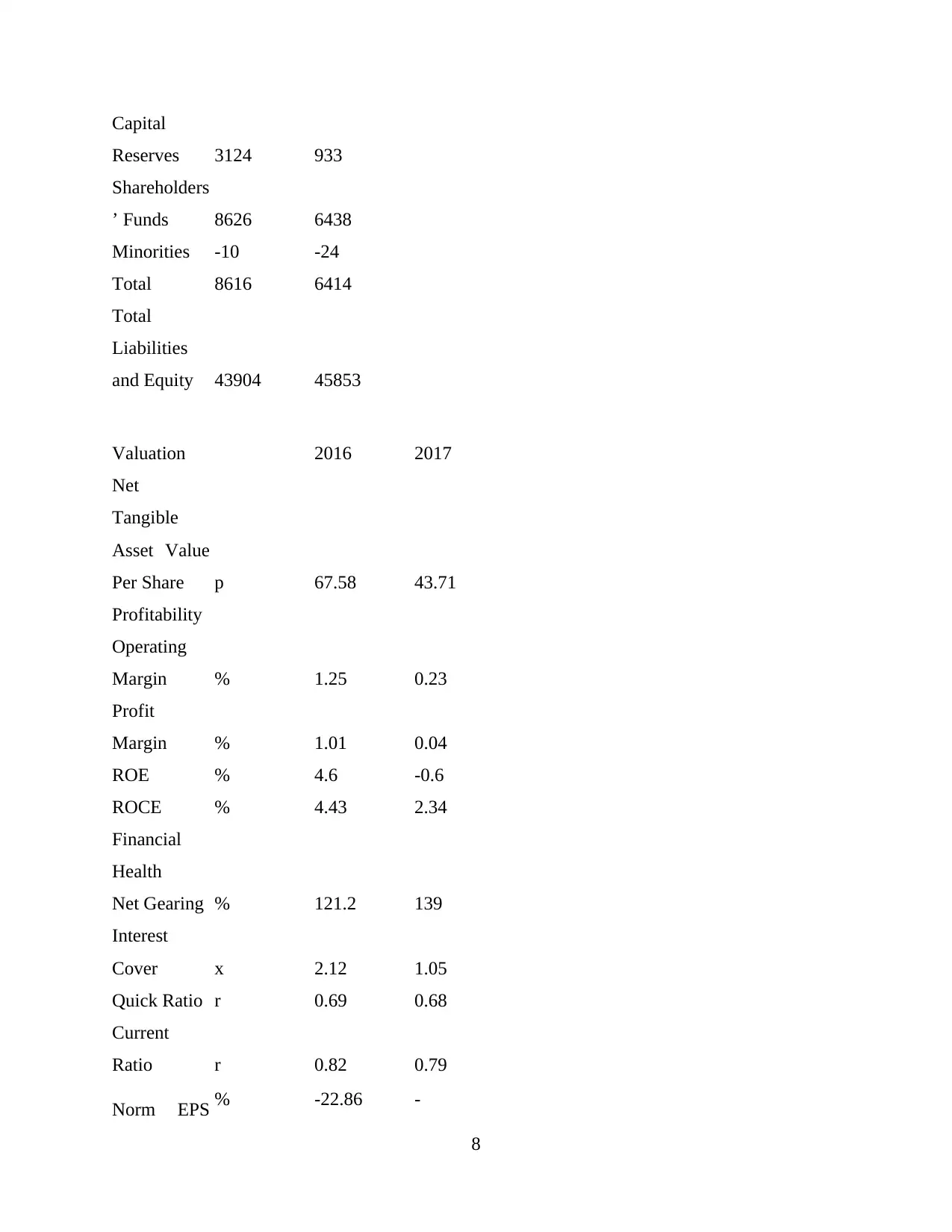

Capital

Reserves 3124 933

Shareholders

’ Funds 8626 6438

Minorities -10 -24

Total 8616 6414

Total

Liabilities

and Equity 43904 45853

Valuation 2016 2017

Net

Tangible

Asset Value

Per Share p 67.58 43.71

Profitability

Operating

Margin % 1.25 0.23

Profit

Margin % 1.01 0.04

ROE % 4.6 -0.6

ROCE % 4.43 2.34

Financial

Health

Net Gearing % 121.2 139

Interest

Cover x 2.12 1.05

Quick Ratio r 0.69 0.68

Current

Ratio r 0.82 0.79

Norm EPS % -22.86 -

8

Reserves 3124 933

Shareholders

’ Funds 8626 6438

Minorities -10 -24

Total 8616 6414

Total

Liabilities

and Equity 43904 45853

Valuation 2016 2017

Net

Tangible

Asset Value

Per Share p 67.58 43.71

Profitability

Operating

Margin % 1.25 0.23

Profit

Margin % 1.01 0.04

ROE % 4.6 -0.6

ROCE % 4.43 2.34

Financial

Health

Net Gearing % 121.2 139

Interest

Cover x 2.12 1.05

Quick Ratio r 0.69 0.68

Current

Ratio r 0.82 0.79

Norm EPS % -22.86 -

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Growth

Cash Flow

Cash Flow

Per Share p 26.7 25.26

CAPEX PS p 8.47 10.58

Previously mentioned calculation are the financial statements of Tesco Plc. and on the

premise of them, evaluation can be done that can be utilized for the aim of decision making in

business. For determination of profitability, this can be said that profit margin is getting lower at

1.01 and 0.04 in years 2016 and 2017 and this demonstrates the are lowering and this isn't a

decent sign for any firm. In addition to this, equity and return on capital employed has also

reduced and this demonstrates negative part of organization.

This can be observed that current ratio is practically similar yet is far substantially less

than standard ratio required. Quick ratio that speaks to liquidity is same in the two years which

implies that organization is meeting its commitments in a comparable way. Organization's

interest cover is decreased which demonstrates that instability is expanding and this isn't useful

for any business (Council, 2010).

7. Difference among IAS and IFRS

There are various international bodies which are authorized to issue several standards that

are known for the International accounting standards and these standards are needed to be

adhered by companies. By using these international standards, company can overcome

misrepresentation which might arise while preparing financial statements. The accounting

standards have be frame out under IAS and all the companies must adhere these standards while

forming financial reporting.

In 2001, a committee was established by the IAS, as per this committee, there were some

modifications which are required to be introduced in the old international accounting standards.

Which emerge the new accounting standard that named as International Financial Reporting

Standards, which comprises all the accounting standards including new.

There are so many differences or variation arises among IAS and IFRS which covers that IFRS is

made after 2001 and names as IFRS and the rest is IAS. Under IAS, there are 39 standards that

have been defined under this, while in IFRS, there are only 9 accounting standards have been

9

Cash Flow

Cash Flow

Per Share p 26.7 25.26

CAPEX PS p 8.47 10.58

Previously mentioned calculation are the financial statements of Tesco Plc. and on the

premise of them, evaluation can be done that can be utilized for the aim of decision making in

business. For determination of profitability, this can be said that profit margin is getting lower at

1.01 and 0.04 in years 2016 and 2017 and this demonstrates the are lowering and this isn't a

decent sign for any firm. In addition to this, equity and return on capital employed has also

reduced and this demonstrates negative part of organization.

This can be observed that current ratio is practically similar yet is far substantially less

than standard ratio required. Quick ratio that speaks to liquidity is same in the two years which

implies that organization is meeting its commitments in a comparable way. Organization's

interest cover is decreased which demonstrates that instability is expanding and this isn't useful

for any business (Council, 2010).

7. Difference among IAS and IFRS

There are various international bodies which are authorized to issue several standards that

are known for the International accounting standards and these standards are needed to be

adhered by companies. By using these international standards, company can overcome

misrepresentation which might arise while preparing financial statements. The accounting

standards have be frame out under IAS and all the companies must adhere these standards while

forming financial reporting.

In 2001, a committee was established by the IAS, as per this committee, there were some

modifications which are required to be introduced in the old international accounting standards.

Which emerge the new accounting standard that named as International Financial Reporting

Standards, which comprises all the accounting standards including new.

There are so many differences or variation arises among IAS and IFRS which covers that IFRS is

made after 2001 and names as IFRS and the rest is IAS. Under IAS, there are 39 standards that

have been defined under this, while in IFRS, there are only 9 accounting standards have been

9

defined. International accounting standard committee and IASB are the main body that were

authorized for making the IAS and IFRS. However, under IAS, nothing is mentioned which are

available in IFRS that covers presentation, identification, measurement and revealing various

amounts which are there under statements. The things that are mentioned under IAS requires to

be follows but which are mentioned in IFRS must have to compulsory adhered along with the

guidelines that assist the manner according to which task is required to be performed (Epstein,

and Jermakowicz, 2010).

8. Benefits of IFRS

International financial reporting standards are the standards that are required to adhere by

each company so that these firms can records and make financial reporting. With the help of

financial statements, company and other outsiders get to know the actual picture of the

organization and then make their decisions in an effective manner. These reporting standards can

lead to provide a great picture about the company in an effective manner.

Various stakeholders will take the benefits of IFRS. Some of them are mentioned hereunder:

For investors: By adopting the IFRS standards by the company, investors would get to

know the accurate picture of the company. So that they could take their investment decisions in a

most effective manner. Now this also been observed that the transparency can be attained by

adhering these standards. Information achieved through financial statements which is prepared as

per the IFRS guidelines are better for investors to take their investment decisions. Company also

limits the international differences under financial reporting standards.

Timely recognition of loss: The main feature of IFRS is to identify the loss of the

company which will assist the investors and the management and other stakeholders. By

implementing IFRS in the company. Company can enhance the efficiency of the contact between

companies and management.

Comparability: By implementing IFRS standards, company can compare its performance

via financial statements in an effective manner. By applying these standards, company is able to

compare its financial performance in an effective manner. Such would be attained by

implementing same reporting standards in an under the same market.

Standardized accounting and financial reporting: This is the key benefits of financial

reporting that enhance the comparability of financial statements. This also able to eliminate the

trade barrier by implementing single reporting standards.

10

authorized for making the IAS and IFRS. However, under IAS, nothing is mentioned which are

available in IFRS that covers presentation, identification, measurement and revealing various

amounts which are there under statements. The things that are mentioned under IAS requires to

be follows but which are mentioned in IFRS must have to compulsory adhered along with the

guidelines that assist the manner according to which task is required to be performed (Epstein,

and Jermakowicz, 2010).

8. Benefits of IFRS

International financial reporting standards are the standards that are required to adhere by

each company so that these firms can records and make financial reporting. With the help of

financial statements, company and other outsiders get to know the actual picture of the

organization and then make their decisions in an effective manner. These reporting standards can

lead to provide a great picture about the company in an effective manner.

Various stakeholders will take the benefits of IFRS. Some of them are mentioned hereunder:

For investors: By adopting the IFRS standards by the company, investors would get to

know the accurate picture of the company. So that they could take their investment decisions in a

most effective manner. Now this also been observed that the transparency can be attained by

adhering these standards. Information achieved through financial statements which is prepared as

per the IFRS guidelines are better for investors to take their investment decisions. Company also

limits the international differences under financial reporting standards.

Timely recognition of loss: The main feature of IFRS is to identify the loss of the

company which will assist the investors and the management and other stakeholders. By

implementing IFRS in the company. Company can enhance the efficiency of the contact between

companies and management.

Comparability: By implementing IFRS standards, company can compare its performance

via financial statements in an effective manner. By applying these standards, company is able to

compare its financial performance in an effective manner. Such would be attained by

implementing same reporting standards in an under the same market.

Standardized accounting and financial reporting: This is the key benefits of financial

reporting that enhance the comparability of financial statements. This also able to eliminate the

trade barrier by implementing single reporting standards.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.