Financial Accounting Report: Analysis of Financial Statements 2020

VerifiedAdded on 2023/06/15

|10

|2084

|307

Report

AI Summary

This financial accounting report analyzes the financial performance of ASOS plc using financial ratios from 2018 to 2021, along with their limitations. It includes the preparation of an income statement and balance sheet for the year ended December 31, 2020, and identifies five accounting concepts applied in the preparation of financial statements. The report also features Harma Limited’s statement of cash flows for the year ended December 31, 2021, with a memo explaining the findings. Key financial ratios such as return on shareholder funds, gross profit, and operational profit are interpreted, and concepts like money measurement, historical cost, and going concern are discussed. The analysis concludes with insights into profitability, liquidity, and solvency.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

SECTION A...................................................................................................................................................3

Introduction.............................................................................................................................................3

Interpretation of ratios............................................................................................................................3

Highlight limitations in the use of accounting ratios...............................................................................4

Conclusion...............................................................................................................................................5

SECTION B....................................................................................................................................................5

QUESTION 1.................................................................................................................................................5

Prepare Income statement for the year ended 31st December 2020.....................................................5

Prepare Balance Sheet as at 31st December 2020..................................................................................6

Identify FIVE accounting concepts that have been applied in the preparation of financial Statements

and explain their meaning.......................................................................................................................7

QUESTION 2.................................................................................................................................................8

Prepare Harma Limited’s statement of cash flows for the year ended 31st December 2021.................8

Write a short memo to Mrs Harma explaining the findings of your statement of cash flow...................9

INTRODUCTION...........................................................................................................................................3

SECTION A...................................................................................................................................................3

Introduction.............................................................................................................................................3

Interpretation of ratios............................................................................................................................3

Highlight limitations in the use of accounting ratios...............................................................................4

Conclusion...............................................................................................................................................5

SECTION B....................................................................................................................................................5

QUESTION 1.................................................................................................................................................5

Prepare Income statement for the year ended 31st December 2020.....................................................5

Prepare Balance Sheet as at 31st December 2020..................................................................................6

Identify FIVE accounting concepts that have been applied in the preparation of financial Statements

and explain their meaning.......................................................................................................................7

QUESTION 2.................................................................................................................................................8

Prepare Harma Limited’s statement of cash flows for the year ended 31st December 2021.................8

Write a short memo to Mrs Harma explaining the findings of your statement of cash flow...................9

INTRODUCTION

Financial accounting is essentially the recording and evaluation of activities. It is conducted

out to assess company sales and effectiveness. To standardize the procedure, government

regulators have outlined several fundamental values. Companies in the United States use GAAP

principles. All money transfers centre on five necessary elements: assets, liabilities, revenue,

expenditures, and ownership (Zhang and Zhang, 2017). In addition, each business deal comprises

two equal halves. For instance, when money is taken from a bank and recorded in the income

statement using the dual procedure. These report categories into two sections in fist section

analysis the financial performance of ASOS plc in three years by financial ration with

limitations. In second section prepare financial statements and explain their meetings.

SECTION A

Introduction

ASOS plc is a Leading digital retailer of clothing and cosmetics. The firm was started in London

in 2000, with a primary focus on young people. The website sells over 850 brands or its own

fashion accessories, and delivers to all 196 nations through distribution center in the United

Kingdom, the United States, and Europe.

Interpretation of ratios

There are analyzing the different financial ratios in order to know actual financial performance

and identify the changes in compare of last year. There are analyzing from 2018 to 2021 such as:

Profitability ratios: Profit offers a "return" on capital for shareholders, as well as a critical supply

of money (i.e. retained earnings) to support the firm's continued prospects. Profitable is used to

assess company's financial success. In this category consist of different types of ratios that help

to investors to analysis profitability of ASOS in different year. From the return on shareholder

funds analysis that

Return on shareholder fund: It is mainly used to compare different originations in different sector

and between 15 to 20% consider as good ratio. In the year 2018 was 23.25 which was good but it

was declining in 2019 reach on 7.3 which is not good for investors after that in the year of 2020

Financial accounting is essentially the recording and evaluation of activities. It is conducted

out to assess company sales and effectiveness. To standardize the procedure, government

regulators have outlined several fundamental values. Companies in the United States use GAAP

principles. All money transfers centre on five necessary elements: assets, liabilities, revenue,

expenditures, and ownership (Zhang and Zhang, 2017). In addition, each business deal comprises

two equal halves. For instance, when money is taken from a bank and recorded in the income

statement using the dual procedure. These report categories into two sections in fist section

analysis the financial performance of ASOS plc in three years by financial ration with

limitations. In second section prepare financial statements and explain their meetings.

SECTION A

Introduction

ASOS plc is a Leading digital retailer of clothing and cosmetics. The firm was started in London

in 2000, with a primary focus on young people. The website sells over 850 brands or its own

fashion accessories, and delivers to all 196 nations through distribution center in the United

Kingdom, the United States, and Europe.

Interpretation of ratios

There are analyzing the different financial ratios in order to know actual financial performance

and identify the changes in compare of last year. There are analyzing from 2018 to 2021 such as:

Profitability ratios: Profit offers a "return" on capital for shareholders, as well as a critical supply

of money (i.e. retained earnings) to support the firm's continued prospects. Profitable is used to

assess company's financial success. In this category consist of different types of ratios that help

to investors to analysis profitability of ASOS in different year. From the return on shareholder

funds analysis that

Return on shareholder fund: It is mainly used to compare different originations in different sector

and between 15 to 20% consider as good ratio. In the year 2018 was 23.25 which was good but it

was declining in 2019 reach on 7.3 which is not good for investors after that in the year of 2020

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

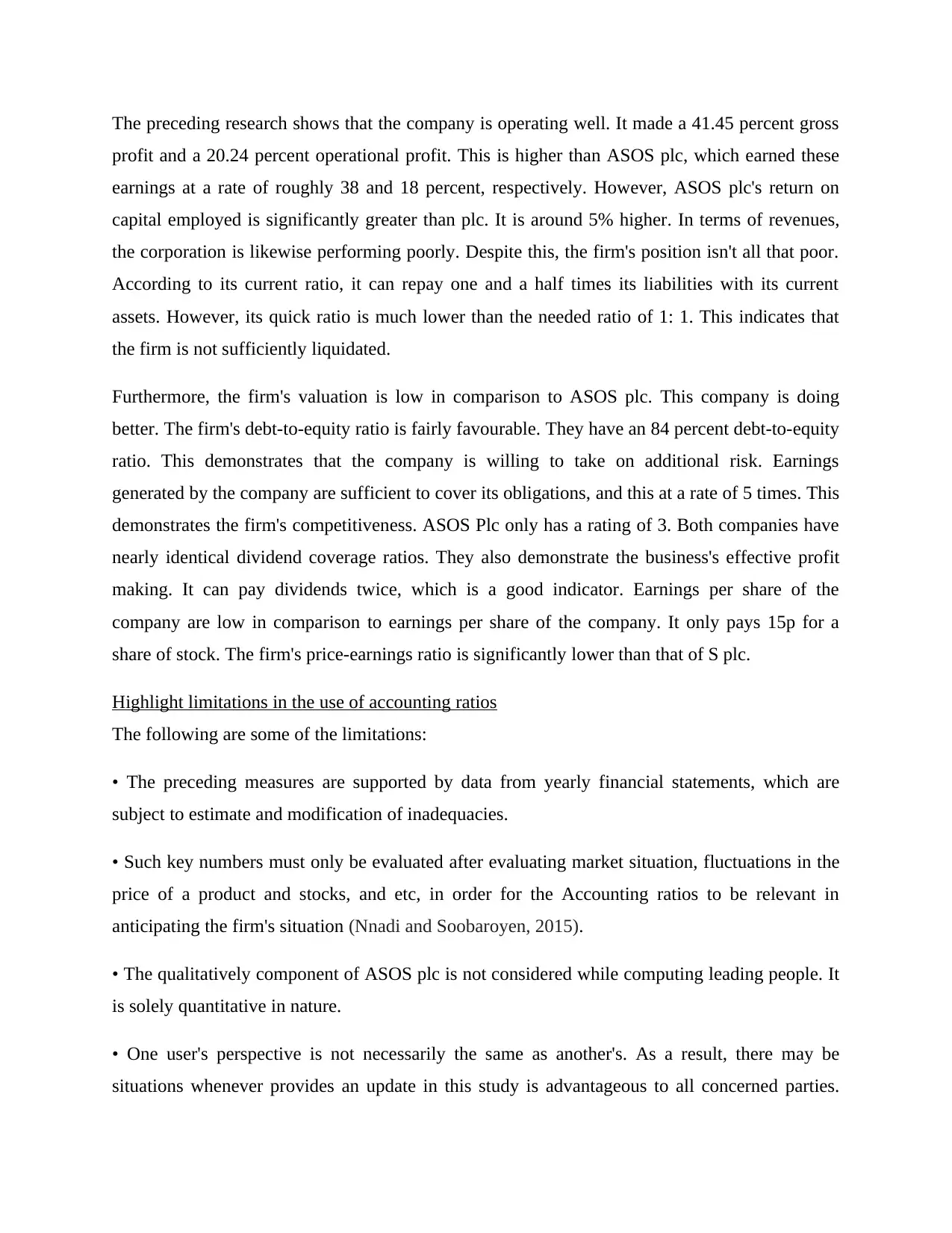

The preceding research shows that the company is operating well. It made a 41.45 percent gross

profit and a 20.24 percent operational profit. This is higher than ASOS plc, which earned these

earnings at a rate of roughly 38 and 18 percent, respectively. However, ASOS plc's return on

capital employed is significantly greater than plc. It is around 5% higher. In terms of revenues,

the corporation is likewise performing poorly. Despite this, the firm's position isn't all that poor.

According to its current ratio, it can repay one and a half times its liabilities with its current

assets. However, its quick ratio is much lower than the needed ratio of 1: 1. This indicates that

the firm is not sufficiently liquidated.

Furthermore, the firm's valuation is low in comparison to ASOS plc. This company is doing

better. The firm's debt-to-equity ratio is fairly favourable. They have an 84 percent debt-to-equity

ratio. This demonstrates that the company is willing to take on additional risk. Earnings

generated by the company are sufficient to cover its obligations, and this at a rate of 5 times. This

demonstrates the firm's competitiveness. ASOS Plc only has a rating of 3. Both companies have

nearly identical dividend coverage ratios. They also demonstrate the business's effective profit

making. It can pay dividends twice, which is a good indicator. Earnings per share of the

company are low in comparison to earnings per share of the company. It only pays 15p for a

share of stock. The firm's price-earnings ratio is significantly lower than that of S plc.

Highlight limitations in the use of accounting ratios

The following are some of the limitations:

• The preceding measures are supported by data from yearly financial statements, which are

subject to estimate and modification of inadequacies.

• Such key numbers must only be evaluated after evaluating market situation, fluctuations in the

price of a product and stocks, and etc, in order for the Accounting ratios to be relevant in

anticipating the firm's situation (Nnadi and Soobaroyen, 2015).

• The qualitatively component of ASOS plc is not considered while computing leading people. It

is solely quantitative in nature.

• One user's perspective is not necessarily the same as another's. As a result, there may be

situations whenever provides an update in this study is advantageous to all concerned parties.

profit and a 20.24 percent operational profit. This is higher than ASOS plc, which earned these

earnings at a rate of roughly 38 and 18 percent, respectively. However, ASOS plc's return on

capital employed is significantly greater than plc. It is around 5% higher. In terms of revenues,

the corporation is likewise performing poorly. Despite this, the firm's position isn't all that poor.

According to its current ratio, it can repay one and a half times its liabilities with its current

assets. However, its quick ratio is much lower than the needed ratio of 1: 1. This indicates that

the firm is not sufficiently liquidated.

Furthermore, the firm's valuation is low in comparison to ASOS plc. This company is doing

better. The firm's debt-to-equity ratio is fairly favourable. They have an 84 percent debt-to-equity

ratio. This demonstrates that the company is willing to take on additional risk. Earnings

generated by the company are sufficient to cover its obligations, and this at a rate of 5 times. This

demonstrates the firm's competitiveness. ASOS Plc only has a rating of 3. Both companies have

nearly identical dividend coverage ratios. They also demonstrate the business's effective profit

making. It can pay dividends twice, which is a good indicator. Earnings per share of the

company are low in comparison to earnings per share of the company. It only pays 15p for a

share of stock. The firm's price-earnings ratio is significantly lower than that of S plc.

Highlight limitations in the use of accounting ratios

The following are some of the limitations:

• The preceding measures are supported by data from yearly financial statements, which are

subject to estimate and modification of inadequacies.

• Such key numbers must only be evaluated after evaluating market situation, fluctuations in the

price of a product and stocks, and etc, in order for the Accounting ratios to be relevant in

anticipating the firm's situation (Nnadi and Soobaroyen, 2015).

• The qualitatively component of ASOS plc is not considered while computing leading people. It

is solely quantitative in nature.

• One user's perspective is not necessarily the same as another's. As a result, there may be

situations whenever provides an update in this study is advantageous to all concerned parties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lenders, for instance, desire the firm to have a large voltage quota, but shareholders might like a

smaller present quota so that they may spend capital in development operations.

• The influence of fluctuations in ASOS plc Company’s stock or rate of inflation has been

neglected throughout study, reducing the competence of such ratios (Al-Sartawi, Alrawahi and

Sanad, 2016).

Conclusion

As per the above report it has been concluded that Ratio analysis examines paragraph

information from a business’s operations to elicit information about profitability, liquidity,

operational efficiency, and solvency. Ratio analysis may show how a firm has changed over the

years, as well as compare one business to the next in the similar industry sector.

SECTION B

QUESTION 1

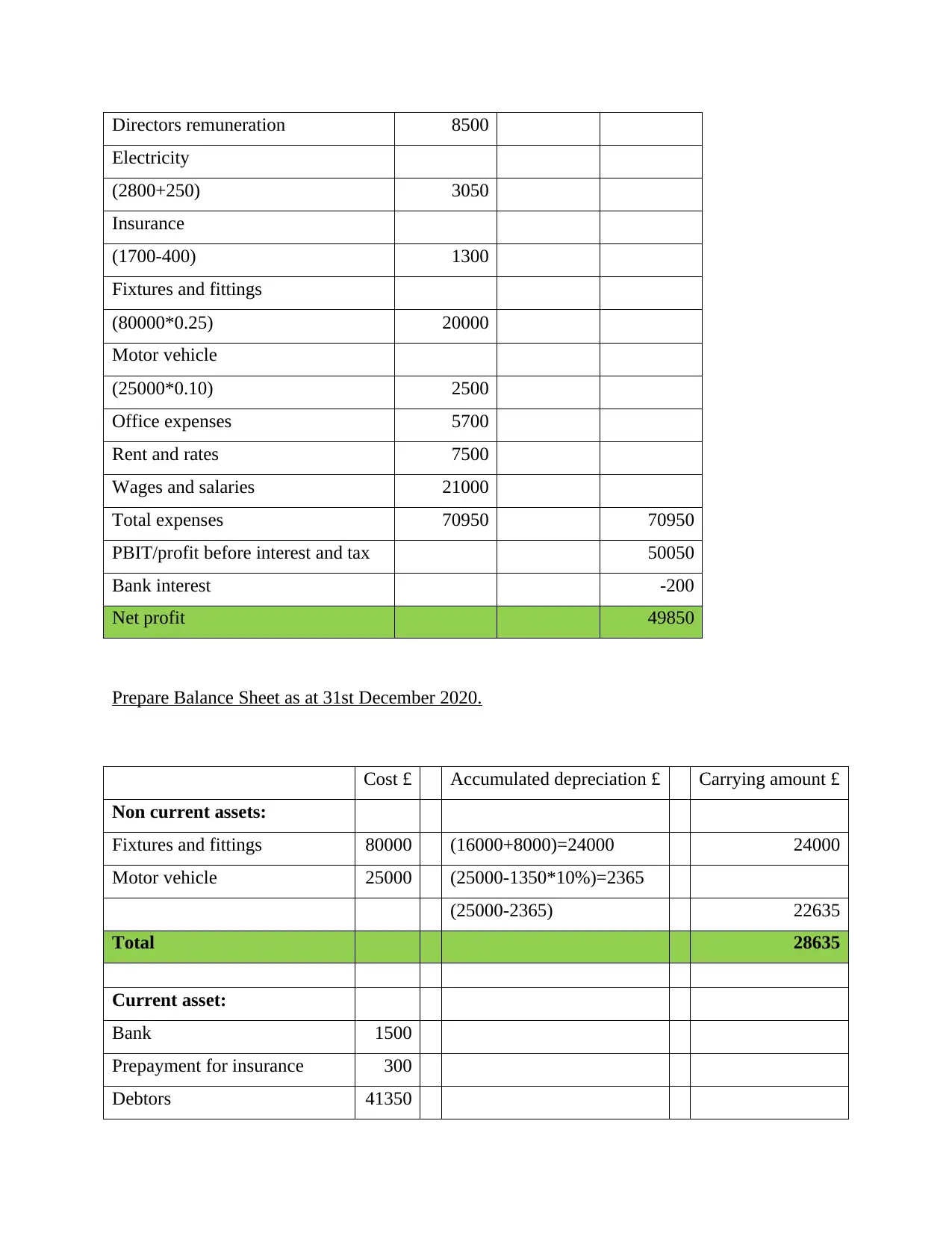

Prepare Income statement for the year ended 31st December 2020

£ £

Sales 285000

Cost of sales:

Purchases 160000

Opening stock 18000

Less: Closing stock -14000

Cost of sales: 164000 -164000

Gross profit 121000

Expenses

Audit and accountancy 500

Advertising 900

smaller present quota so that they may spend capital in development operations.

• The influence of fluctuations in ASOS plc Company’s stock or rate of inflation has been

neglected throughout study, reducing the competence of such ratios (Al-Sartawi, Alrawahi and

Sanad, 2016).

Conclusion

As per the above report it has been concluded that Ratio analysis examines paragraph

information from a business’s operations to elicit information about profitability, liquidity,

operational efficiency, and solvency. Ratio analysis may show how a firm has changed over the

years, as well as compare one business to the next in the similar industry sector.

SECTION B

QUESTION 1

Prepare Income statement for the year ended 31st December 2020

£ £

Sales 285000

Cost of sales:

Purchases 160000

Opening stock 18000

Less: Closing stock -14000

Cost of sales: 164000 -164000

Gross profit 121000

Expenses

Audit and accountancy 500

Advertising 900

Directors remuneration 8500

Electricity

(2800+250) 3050

Insurance

(1700-400) 1300

Fixtures and fittings

(80000*0.25) 20000

Motor vehicle

(25000*0.10) 2500

Office expenses 5700

Rent and rates 7500

Wages and salaries 21000

Total expenses 70950 70950

PBIT/profit before interest and tax 50050

Bank interest -200

Net profit 49850

Prepare Balance Sheet as at 31st December 2020.

Cost £ Accumulated depreciation £ Carrying amount £

Non current assets:

Fixtures and fittings 80000 (16000+8000)=24000 24000

Motor vehicle 25000 (25000-1350*10%)=2365

(25000-2365) 22635

Total 28635

Current asset:

Bank 1500

Prepayment for insurance 300

Debtors 41350

Electricity

(2800+250) 3050

Insurance

(1700-400) 1300

Fixtures and fittings

(80000*0.25) 20000

Motor vehicle

(25000*0.10) 2500

Office expenses 5700

Rent and rates 7500

Wages and salaries 21000

Total expenses 70950 70950

PBIT/profit before interest and tax 50050

Bank interest -200

Net profit 49850

Prepare Balance Sheet as at 31st December 2020.

Cost £ Accumulated depreciation £ Carrying amount £

Non current assets:

Fixtures and fittings 80000 (16000+8000)=24000 24000

Motor vehicle 25000 (25000-1350*10%)=2365

(25000-2365) 22635

Total 28635

Current asset:

Bank 1500

Prepayment for insurance 300

Debtors 41350

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

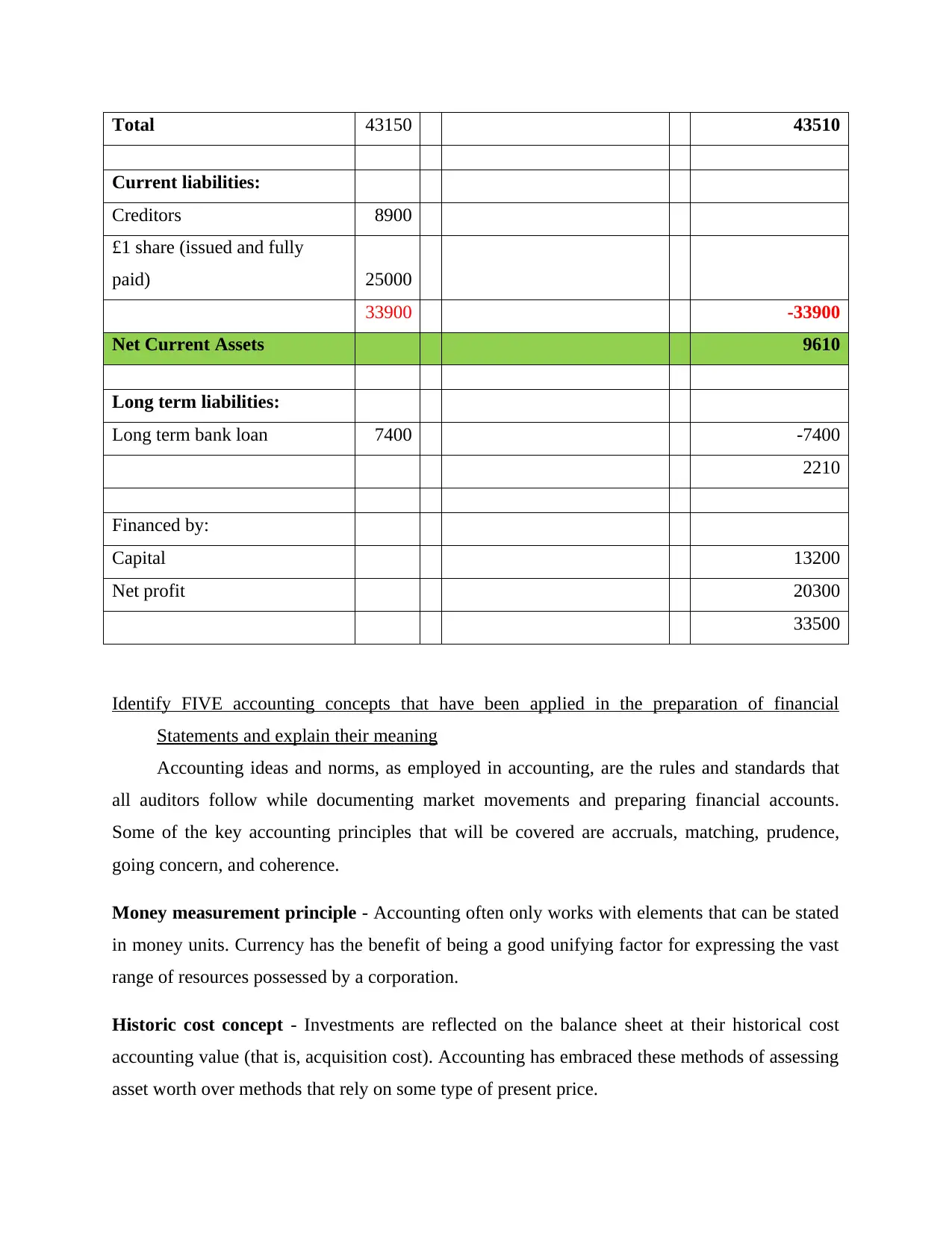

Total 43150 43510

Current liabilities:

Creditors 8900

£1 share (issued and fully

paid) 25000

33900 -33900

Net Current Assets 9610

Long term liabilities:

Long term bank loan 7400 -7400

2210

Financed by:

Capital 13200

Net profit 20300

33500

Identify FIVE accounting concepts that have been applied in the preparation of financial

Statements and explain their meaning

Accounting ideas and norms, as employed in accounting, are the rules and standards that

all auditors follow while documenting market movements and preparing financial accounts.

Some of the key accounting principles that will be covered are accruals, matching, prudence,

going concern, and coherence.

Money measurement principle - Accounting often only works with elements that can be stated

in money units. Currency has the benefit of being a good unifying factor for expressing the vast

range of resources possessed by a corporation.

Historic cost concept - Investments are reflected on the balance sheet at their historical cost

accounting value (that is, acquisition cost). Accounting has embraced these methods of assessing

asset worth over methods that rely on some type of present price.

Current liabilities:

Creditors 8900

£1 share (issued and fully

paid) 25000

33900 -33900

Net Current Assets 9610

Long term liabilities:

Long term bank loan 7400 -7400

2210

Financed by:

Capital 13200

Net profit 20300

33500

Identify FIVE accounting concepts that have been applied in the preparation of financial

Statements and explain their meaning

Accounting ideas and norms, as employed in accounting, are the rules and standards that

all auditors follow while documenting market movements and preparing financial accounts.

Some of the key accounting principles that will be covered are accruals, matching, prudence,

going concern, and coherence.

Money measurement principle - Accounting often only works with elements that can be stated

in money units. Currency has the benefit of being a good unifying factor for expressing the vast

range of resources possessed by a corporation.

Historic cost concept - Investments are reflected on the balance sheet at their historical cost

accounting value (that is, acquisition cost). Accounting has embraced these methods of assessing

asset worth over methods that rely on some type of present price.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The going concern notion states that a company will keep operating for the near future. In other

respects, there is no plan or necessity to transfer the company's assets. Whenever a company is in

financial distress and needs to pay its debts, this type of transaction may occur (Cleary and

Quinn, 2016).

The notion of a business entity: For accrual basis, the company and its owner(s) are recognized

as independent and separate entities. As a result, owners are recognized as creditors towards their

own businesses for their invested capital.

The notion of dual aspects: Every operation has two sides, both of which affect the balance

sheet. Therefore, the cash purchase of a car results in a rise in one asset and a drop in the other

(cash). The payback of a loan reduces the obligation (debt) and increases the asset (cash/bank).

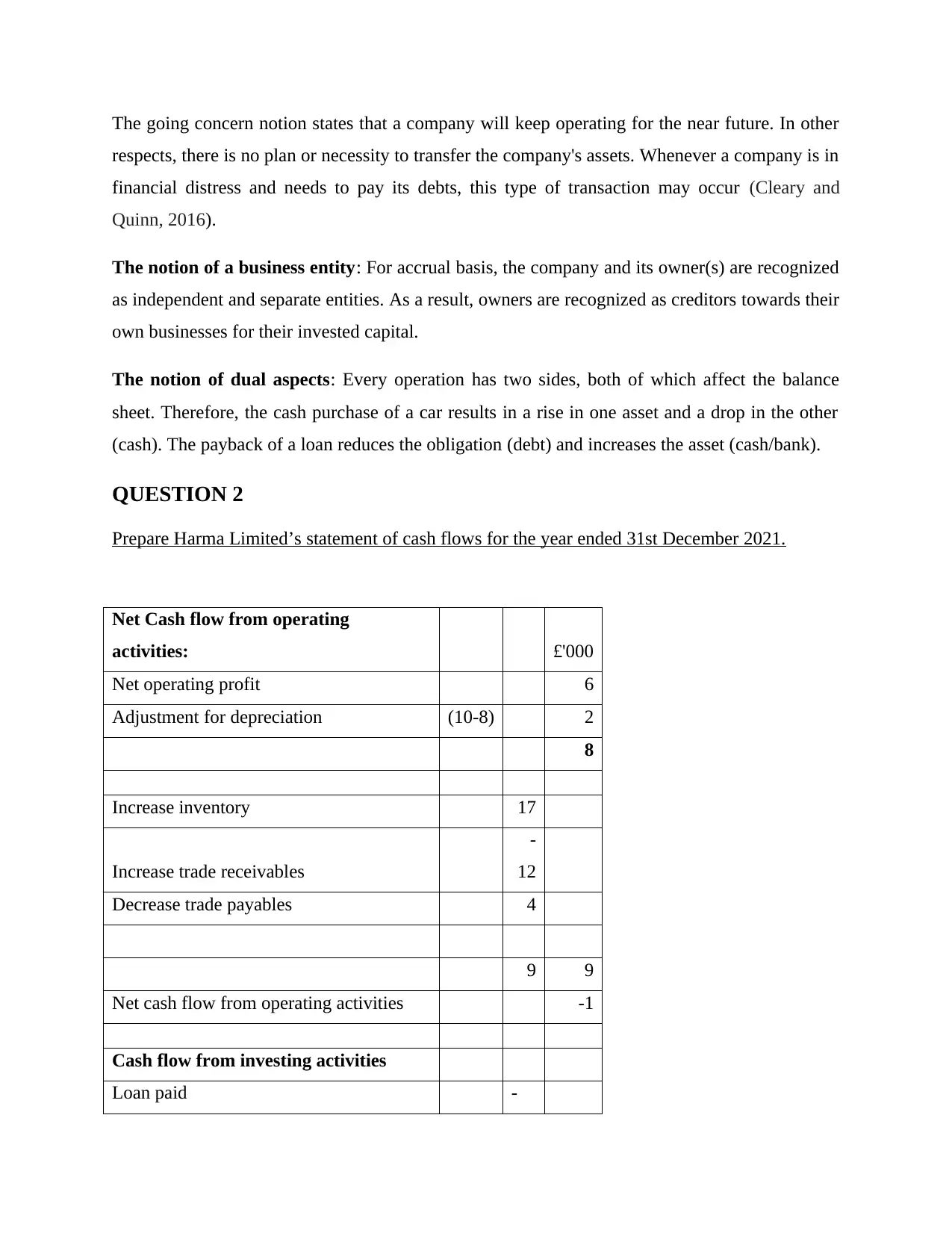

QUESTION 2

Prepare Harma Limited’s statement of cash flows for the year ended 31st December 2021.

Net Cash flow from operating

activities: £'000

Net operating profit 6

Adjustment for depreciation (10-8) 2

8

Increase inventory 17

Increase trade receivables

-

12

Decrease trade payables 4

9 9

Net cash flow from operating activities -1

Cash flow from investing activities

Loan paid -

respects, there is no plan or necessity to transfer the company's assets. Whenever a company is in

financial distress and needs to pay its debts, this type of transaction may occur (Cleary and

Quinn, 2016).

The notion of a business entity: For accrual basis, the company and its owner(s) are recognized

as independent and separate entities. As a result, owners are recognized as creditors towards their

own businesses for their invested capital.

The notion of dual aspects: Every operation has two sides, both of which affect the balance

sheet. Therefore, the cash purchase of a car results in a rise in one asset and a drop in the other

(cash). The payback of a loan reduces the obligation (debt) and increases the asset (cash/bank).

QUESTION 2

Prepare Harma Limited’s statement of cash flows for the year ended 31st December 2021.

Net Cash flow from operating

activities: £'000

Net operating profit 6

Adjustment for depreciation (10-8) 2

8

Increase inventory 17

Increase trade receivables

-

12

Decrease trade payables 4

9 9

Net cash flow from operating activities -1

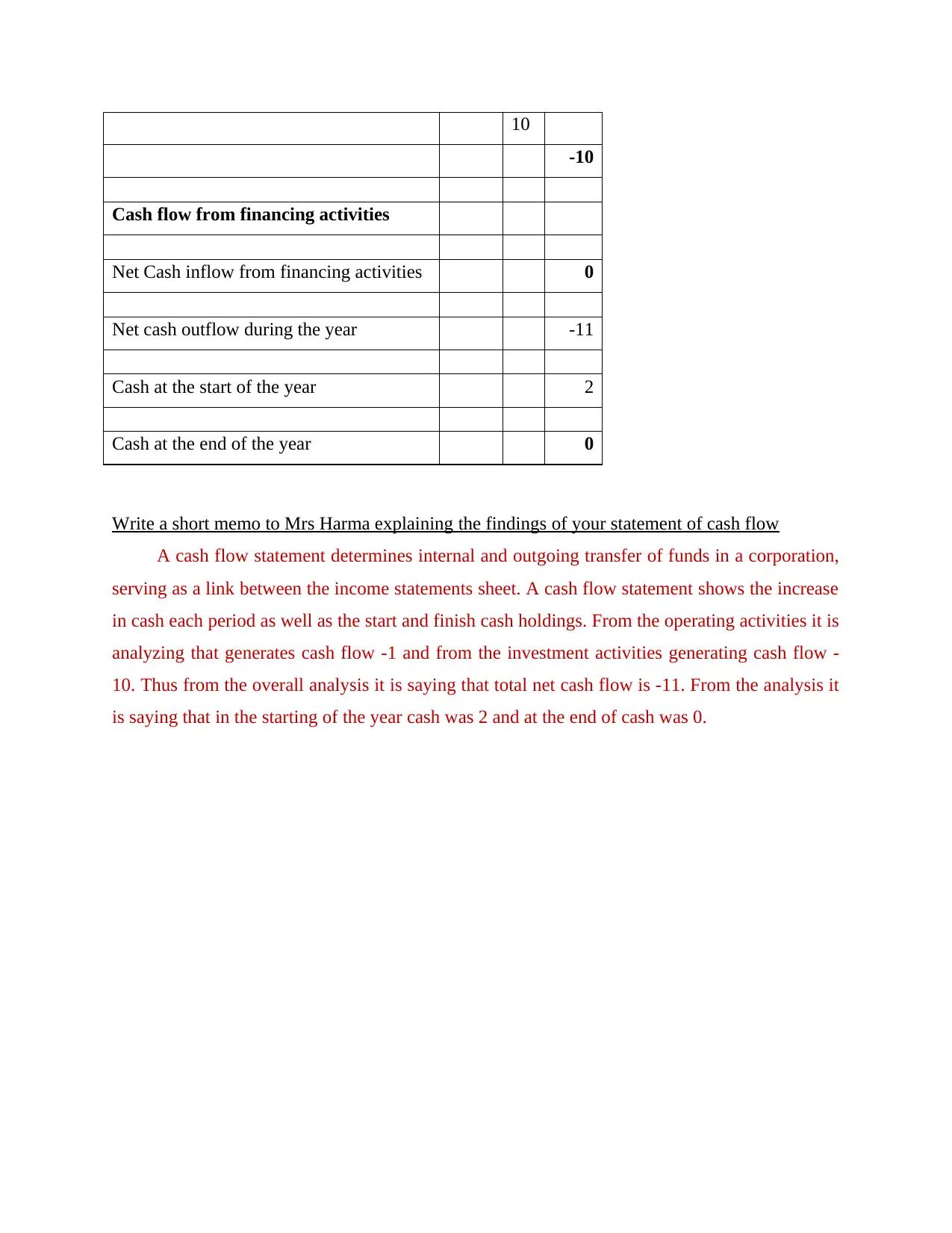

Cash flow from investing activities

Loan paid -

10

-10

Cash flow from financing activities

Net Cash inflow from financing activities 0

Net cash outflow during the year -11

Cash at the start of the year 2

Cash at the end of the year 0

Write a short memo to Mrs Harma explaining the findings of your statement of cash flow

A cash flow statement determines internal and outgoing transfer of funds in a corporation,

serving as a link between the income statements sheet. A cash flow statement shows the increase

in cash each period as well as the start and finish cash holdings. From the operating activities it is

analyzing that generates cash flow -1 and from the investment activities generating cash flow -

10. Thus from the overall analysis it is saying that total net cash flow is -11. From the analysis it

is saying that in the starting of the year cash was 2 and at the end of cash was 0.

-10

Cash flow from financing activities

Net Cash inflow from financing activities 0

Net cash outflow during the year -11

Cash at the start of the year 2

Cash at the end of the year 0

Write a short memo to Mrs Harma explaining the findings of your statement of cash flow

A cash flow statement determines internal and outgoing transfer of funds in a corporation,

serving as a link between the income statements sheet. A cash flow statement shows the increase

in cash each period as well as the start and finish cash holdings. From the operating activities it is

analyzing that generates cash flow -1 and from the investment activities generating cash flow -

10. Thus from the overall analysis it is saying that total net cash flow is -11. From the analysis it

is saying that in the starting of the year cash was 2 and at the end of cash was 0.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journal

Zhang, I .X. and Zhang, Y., 2017. Accounting discretion and purchase price allocation after

acquisitions. Journal of Accounting, Auditing & Finance. 32(2). pp.241-270.

Nnadi, M. and Soobaroyen, T., 2015. International financial reporting standards and foreign

direct investment: The case of Africa. Advances in accounting. 31(2). pp.228-238.

Gomes, P .S., Fernandes, M .J. and Carvalho, J. B. D. C., 2015. The international harmonization

process of public sector accounting in Portugal: the perspective of different

stakeholders. International Journal of Public Administration. 38(4). pp.268-281.

Ionescu, L., 2017. Productivity accounting and business financial performance: a review of

current evidence. Economics, Management, and Financial Markets. 12(2). pp.67-73.

Al-Sartawi, A., Alrawahi, F. and Sanad, Z., 2016. Corporate governance and the level of

compliance with international accounting standards (IAS-1): Evidence from Bahrain

Bourse. International Research Journal of Finance and Economics. 157. pp.110-122.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance: An exploratory

study of the impact of cloud-based accounting and finance infrastructure. Journal of

Intellectual Capital. 17(2). pp.255-278.

Books and Journal

Zhang, I .X. and Zhang, Y., 2017. Accounting discretion and purchase price allocation after

acquisitions. Journal of Accounting, Auditing & Finance. 32(2). pp.241-270.

Nnadi, M. and Soobaroyen, T., 2015. International financial reporting standards and foreign

direct investment: The case of Africa. Advances in accounting. 31(2). pp.228-238.

Gomes, P .S., Fernandes, M .J. and Carvalho, J. B. D. C., 2015. The international harmonization

process of public sector accounting in Portugal: the perspective of different

stakeholders. International Journal of Public Administration. 38(4). pp.268-281.

Ionescu, L., 2017. Productivity accounting and business financial performance: a review of

current evidence. Economics, Management, and Financial Markets. 12(2). pp.67-73.

Al-Sartawi, A., Alrawahi, F. and Sanad, Z., 2016. Corporate governance and the level of

compliance with international accounting standards (IAS-1): Evidence from Bahrain

Bourse. International Research Journal of Finance and Economics. 157. pp.110-122.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance: An exploratory

study of the impact of cloud-based accounting and finance infrastructure. Journal of

Intellectual Capital. 17(2). pp.255-278.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.