Financial Accounting Assignment: Ray Finance Limited Analysis

VerifiedAdded on 2023/01/10

|21

|4113

|31

Homework Assignment

AI Summary

This financial accounting assignment, prepared for Ray Finance Limited, delves into various aspects of financial bookkeeping. It begins with an introduction to financial accounting, followed by an analysis of business transactions, including cash and credit transactions, and the application of single and double-entry bookkeeping systems. The assignment includes journal entries, ledgers, and the preparation of a trial balance. Furthermore, it identifies the major differences between financial reports and financial statements, emphasizing their importance for stakeholders. It also explains fundamental accounting principles. The assignment then proceeds to Task 2, which covers bank reconciliations, control accounts, and suspense accounts, along with the preparation of a cash book and a bank reconciliation statement. The document includes journal entries, ledgers, and the preparation of a trial balance. Finally, the assignment concludes with a comprehensive set of references.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK1.............................................................................................................................................3

Question 1. Identification of business transaction and their type also discussion about the

single entry and double entry system of bookkeeping buy land in term of trial balance.......3

Question 3: Identify major differences in financial reports and statements and why these are

important for various stakeholders?.......................................................................................8

Question 4: explain different fundamental principles of accounting...................................10

Question 5:Prepare a profit and loss account for the year ended 31 December 2017 and

balance sheet at that date......................................................................................................10

TASK2...........................................................................................................................................12

Question1: What is meant by bank reconciliation and why is it required? How is this

achieved? Why is this necessary?.........................................................................................12

Question 2: what are control accounts? Explain the role of control accounts in financial

management..........................................................................................................................13

Question 3: what is suspense account? What are the reasons for drafting suspense accounts?

..............................................................................................................................................13

Question 3 prepare cash book...............................................................................................14

Question 4 Prepare a bank reconciliation statement.............................................................14

REFRENCES.................................................................................................................................16

Books and journal..........................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK1.............................................................................................................................................3

Question 1. Identification of business transaction and their type also discussion about the

single entry and double entry system of bookkeeping buy land in term of trial balance.......3

Question 3: Identify major differences in financial reports and statements and why these are

important for various stakeholders?.......................................................................................8

Question 4: explain different fundamental principles of accounting...................................10

Question 5:Prepare a profit and loss account for the year ended 31 December 2017 and

balance sheet at that date......................................................................................................10

TASK2...........................................................................................................................................12

Question1: What is meant by bank reconciliation and why is it required? How is this

achieved? Why is this necessary?.........................................................................................12

Question 2: what are control accounts? Explain the role of control accounts in financial

management..........................................................................................................................13

Question 3: what is suspense account? What are the reasons for drafting suspense accounts?

..............................................................................................................................................13

Question 3 prepare cash book...............................................................................................14

Question 4 Prepare a bank reconciliation statement.............................................................14

REFRENCES.................................................................................................................................16

Books and journal..........................................................................................................................16

INTRODUCTION

Financial bookkeeping can be defined as a combination of different account and financial

information which are related to development of a proper system by the organisation with the

help of tools and techniques related to accounting and business records for analysing and

interpreting information and using it for the further benefit. In this report which is an

organisation is Ray finance limited. Present report have been considered, the sense and concept

of journal entries, how they apply in the organization their use in formulating trial balance and

financial statements. This reports their discussion about the importance and maintenance of trial

balance and various accounts which are required to the organisation for controlling its cash flow

and bank reconciliation statement. is also discussion about how the bank reconciliation statement

are prepared by the organisation and how it can be used in day to day operations and activities of

the firm.

TASK1

Question 1. Identification of business transaction and their type also discussion about the single

entry and double entry system of bookkeeping buy land in term of trial balance.

Commercial transaction: It includes those activities or deals which measure in monetary

term and indirectly affect processes of business. There dealings direct affect on assets, liabilities,

expense and income of the business organization. Business transactions are the activity which is

related with business and record in periodicals of the organization. The transactions rare divided

into 2 parts which are Cash transactions and credit business transaction(Nicholls and Mastrolia,

2015).

Cash transaction: Activities which are related to flow of cash inward and outward. It

includes sales, purchase, purchase of investment etc.

Credit deal: It considered that kind of activities in which there is no need of cash at the

time when transaction incurred. Examples, goods purchase on credit, stock sold on credit,.

These transaction directly as credit purchase increase obligation of organization and affect on

asset and liability and decent sold on praise enhance the possessions of the organization

Internal and External deals: Theses deal has separate part. .

External deal: It is related with activities which are related with external parties. Business

dealings, purchase of assets, issuing shares, purchase raw material etc.

Financial bookkeeping can be defined as a combination of different account and financial

information which are related to development of a proper system by the organisation with the

help of tools and techniques related to accounting and business records for analysing and

interpreting information and using it for the further benefit. In this report which is an

organisation is Ray finance limited. Present report have been considered, the sense and concept

of journal entries, how they apply in the organization their use in formulating trial balance and

financial statements. This reports their discussion about the importance and maintenance of trial

balance and various accounts which are required to the organisation for controlling its cash flow

and bank reconciliation statement. is also discussion about how the bank reconciliation statement

are prepared by the organisation and how it can be used in day to day operations and activities of

the firm.

TASK1

Question 1. Identification of business transaction and their type also discussion about the single

entry and double entry system of bookkeeping buy land in term of trial balance.

Commercial transaction: It includes those activities or deals which measure in monetary

term and indirectly affect processes of business. There dealings direct affect on assets, liabilities,

expense and income of the business organization. Business transactions are the activity which is

related with business and record in periodicals of the organization. The transactions rare divided

into 2 parts which are Cash transactions and credit business transaction(Nicholls and Mastrolia,

2015).

Cash transaction: Activities which are related to flow of cash inward and outward. It

includes sales, purchase, purchase of investment etc.

Credit deal: It considered that kind of activities in which there is no need of cash at the

time when transaction incurred. Examples, goods purchase on credit, stock sold on credit,.

These transaction directly as credit purchase increase obligation of organization and affect on

asset and liability and decent sold on praise enhance the possessions of the organization

Internal and External deals: Theses deal has separate part. .

External deal: It is related with activities which are related with external parties. Business

dealings, purchase of assets, issuing shares, purchase raw material etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal transaction: Theses are non enhance transactions . In internal transactions only internal

parties of business are involved. It does not considered transactions which are related with

exchange of good. There are different Internal transaction considered, devaluation charge on

secure asset, repayment loss of asset as due to on fire.

Single entry book keeping: Under single entry accounting system organisation has to

record each and every transaction on the basis of proper record with the financial information.

this is the transaction is recorded from the one side which also generate the incomplete

transactions. System of accounting is used by sole proprietor firm where the organisation has no

legal authority apply this system. is completely different from double entry system where the

ride it of the transactions are recorded for each and every transaction. (Elefterie and Badea, ,

2016).

Double entry accounting system: In this system of accounting transaction or business

activities are record on 2 sided thus it is known as double entry book keeping system. According

to the rules, every business transaction have 2 sided effects, it affect asset and liabilities also.

Every transaction is recorded in debit or credit side. This is the official and authorise format of

recording entry which is applicable in the entire world as it precedes base for formulating

financial statement and the whole accounting system is based on book keeping it is the source of

staring of recording all the transaction of business (Mangala, and Kumari, 2017).

Trail balance: It is statement which show list of all account related wit business transactions

which contains in the books of ledger statements. In this all accounts with their balance have

been show in debit or credit side of the statement. In other words trial balance is the format

which is formulated at the end of the account years to identify the debit and credit balance of the

accounts with the help of leader Import in context of trial balance.

Manager of organization use trial balance to identify the debit and credit balance of accounts.

It is useful to organtional in finding out error during journal entry.

It is help in providing basic for formation of financial statement.

Auditors use it as base of recordings.

Trail balance help in deifying the end balance.

It is provides various mathematical impartialities which are associated with debit and credit side

of accounts.

parties of business are involved. It does not considered transactions which are related with

exchange of good. There are different Internal transaction considered, devaluation charge on

secure asset, repayment loss of asset as due to on fire.

Single entry book keeping: Under single entry accounting system organisation has to

record each and every transaction on the basis of proper record with the financial information.

this is the transaction is recorded from the one side which also generate the incomplete

transactions. System of accounting is used by sole proprietor firm where the organisation has no

legal authority apply this system. is completely different from double entry system where the

ride it of the transactions are recorded for each and every transaction. (Elefterie and Badea, ,

2016).

Double entry accounting system: In this system of accounting transaction or business

activities are record on 2 sided thus it is known as double entry book keeping system. According

to the rules, every business transaction have 2 sided effects, it affect asset and liabilities also.

Every transaction is recorded in debit or credit side. This is the official and authorise format of

recording entry which is applicable in the entire world as it precedes base for formulating

financial statement and the whole accounting system is based on book keeping it is the source of

staring of recording all the transaction of business (Mangala, and Kumari, 2017).

Trail balance: It is statement which show list of all account related wit business transactions

which contains in the books of ledger statements. In this all accounts with their balance have

been show in debit or credit side of the statement. In other words trial balance is the format

which is formulated at the end of the account years to identify the debit and credit balance of the

accounts with the help of leader Import in context of trial balance.

Manager of organization use trial balance to identify the debit and credit balance of accounts.

It is useful to organtional in finding out error during journal entry.

It is help in providing basic for formation of financial statement.

Auditors use it as base of recordings.

Trail balance help in deifying the end balance.

It is provides various mathematical impartialities which are associated with debit and credit side

of accounts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

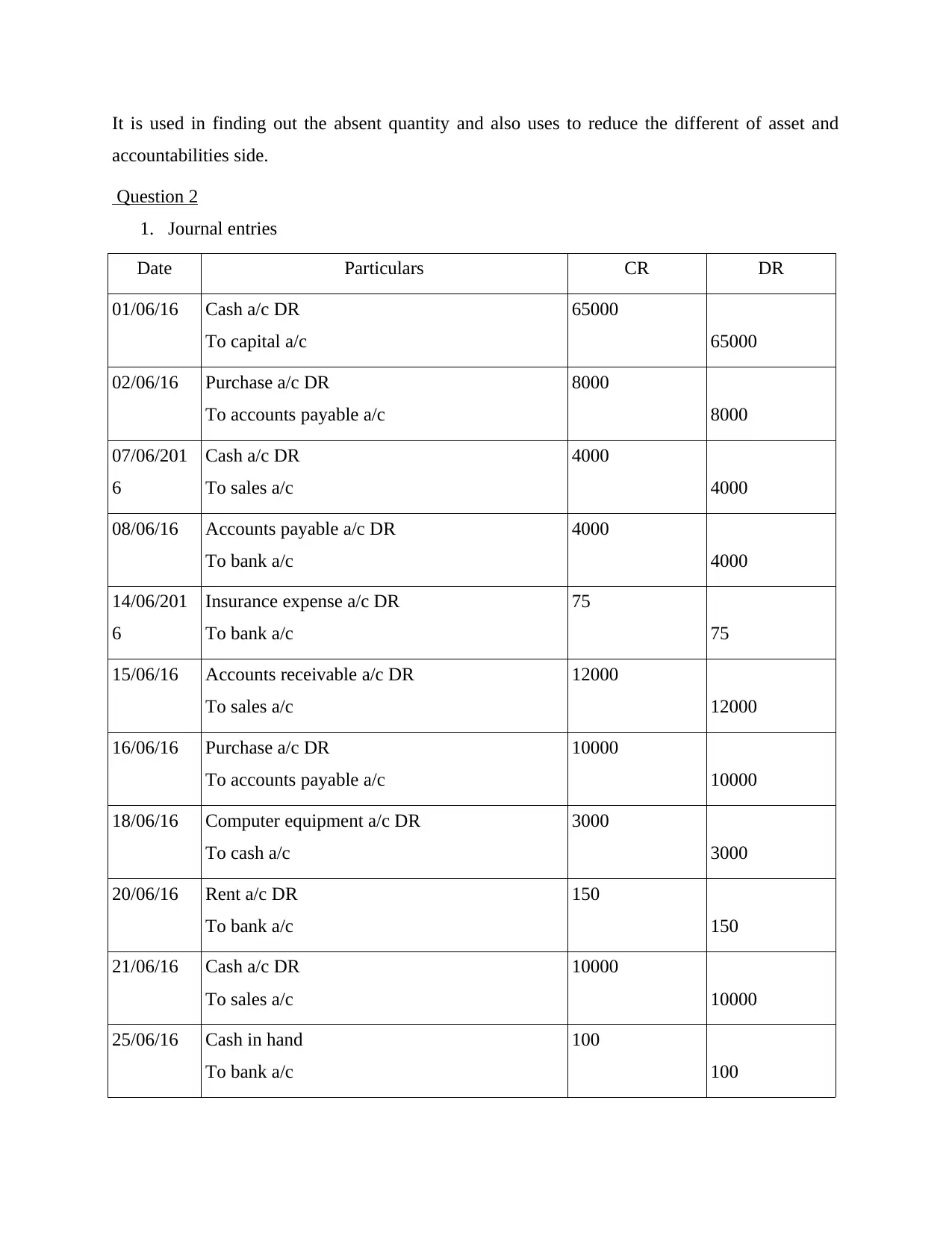

It is used in finding out the absent quantity and also uses to reduce the different of asset and

accountabilities side.

Question 2

1. Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/201

6

Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/201

6

Insurance expense a/c DR

To bank a/c

75

75

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

accountabilities side.

Question 2

1. Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/201

6

Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/201

6

Insurance expense a/c DR

To bank a/c

75

75

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

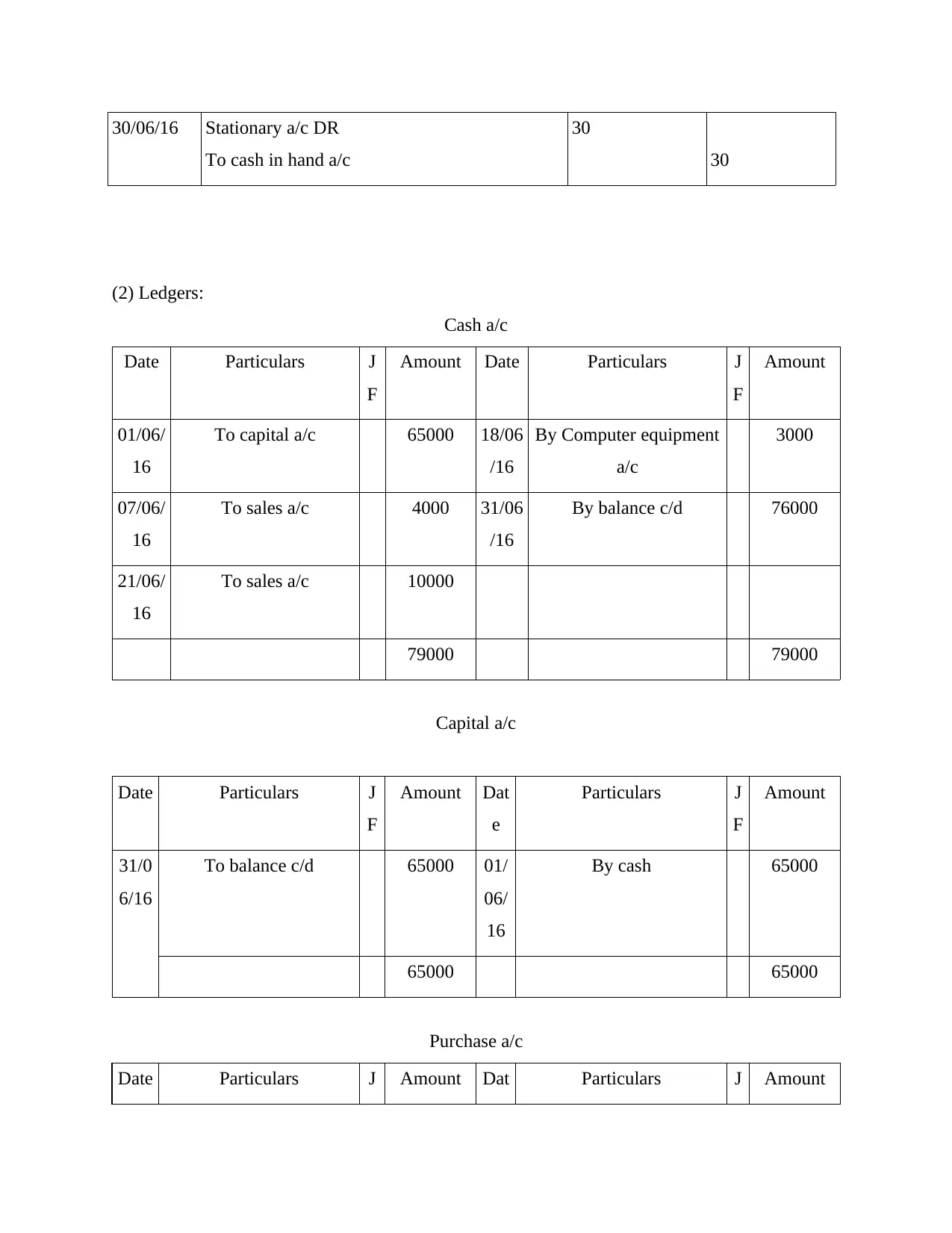

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

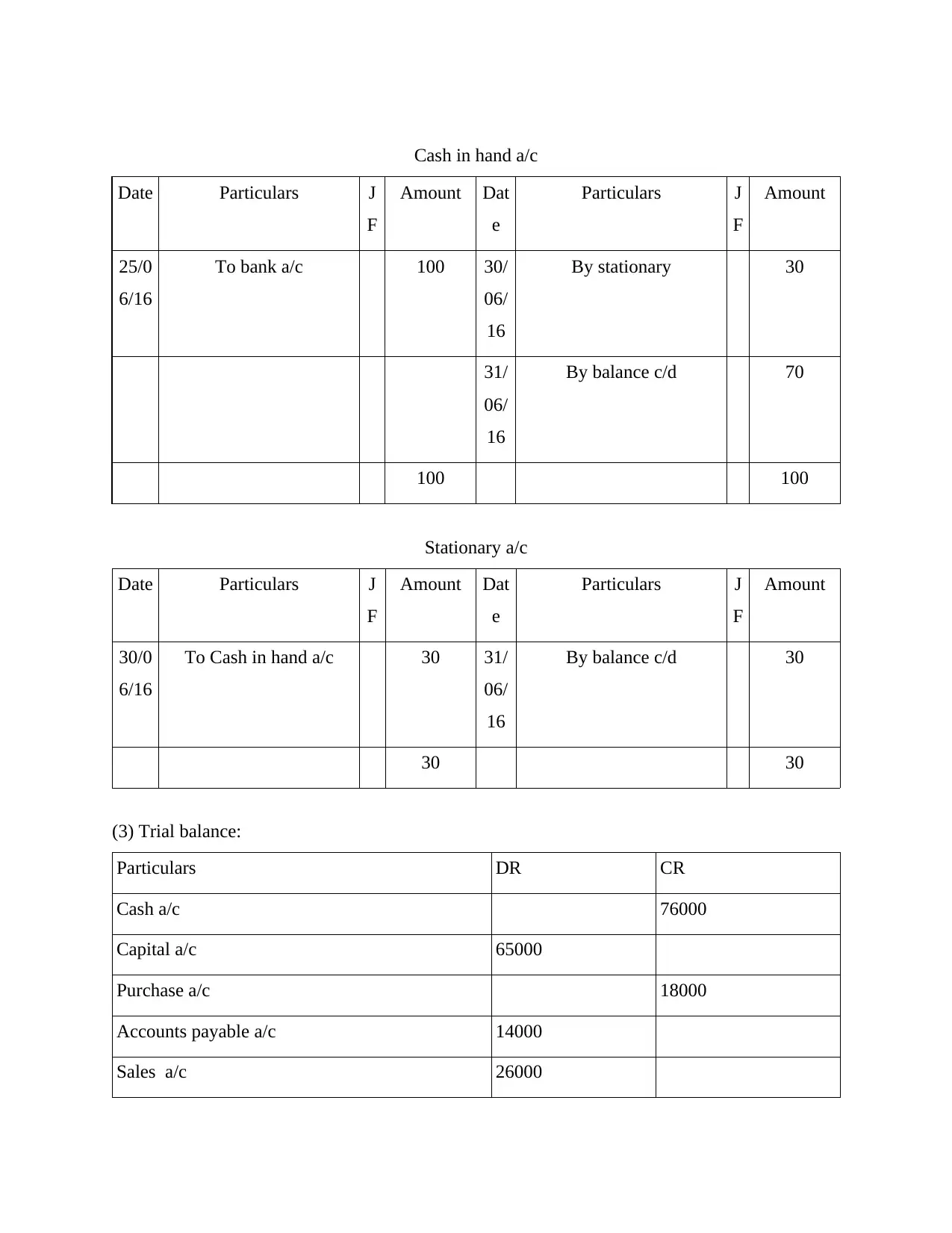

(2) Ledgers:

Cash a/c

Date Particulars J

F

Amount Date Particulars J

F

Amount

01/06/

16

To capital a/c 65000 18/06

/16

By Computer equipment

a/c

3000

07/06/

16

To sales a/c 4000 31/06

/16

By balance c/d 76000

21/06/

16

To sales a/c 10000

79000 79000

Capital a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

31/0

6/16

To balance c/d 65000 01/

06/

16

By cash 65000

65000 65000

Purchase a/c

Date Particulars J Amount Dat Particulars J Amount

To cash in hand a/c

30

30

(2) Ledgers:

Cash a/c

Date Particulars J

F

Amount Date Particulars J

F

Amount

01/06/

16

To capital a/c 65000 18/06

/16

By Computer equipment

a/c

3000

07/06/

16

To sales a/c 4000 31/06

/16

By balance c/d 76000

21/06/

16

To sales a/c 10000

79000 79000

Capital a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

31/0

6/16

To balance c/d 65000 01/

06/

16

By cash 65000

65000 65000

Purchase a/c

Date Particulars J Amount Dat Particulars J Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

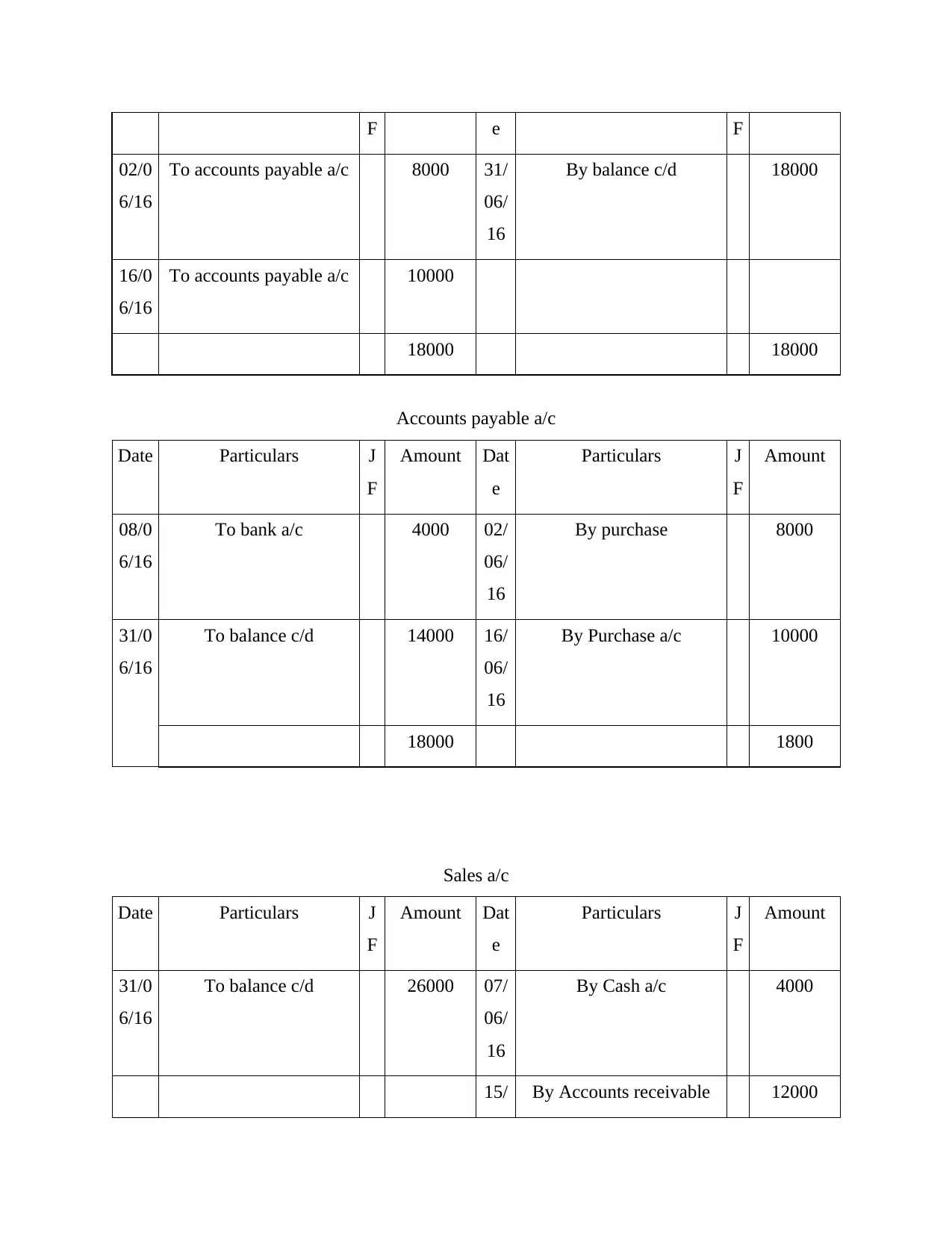

F e F

02/0

6/16

To accounts payable a/c 8000 31/

06/

16

By balance c/d 18000

16/0

6/16

To accounts payable a/c 10000

18000 18000

Accounts payable a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

08/0

6/16

To bank a/c 4000 02/

06/

16

By purchase 8000

31/0

6/16

To balance c/d 14000 16/

06/

16

By Purchase a/c 10000

18000 1800

Sales a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

31/0

6/16

To balance c/d 26000 07/

06/

16

By Cash a/c 4000

15/ By Accounts receivable 12000

02/0

6/16

To accounts payable a/c 8000 31/

06/

16

By balance c/d 18000

16/0

6/16

To accounts payable a/c 10000

18000 18000

Accounts payable a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

08/0

6/16

To bank a/c 4000 02/

06/

16

By purchase 8000

31/0

6/16

To balance c/d 14000 16/

06/

16

By Purchase a/c 10000

18000 1800

Sales a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

31/0

6/16

To balance c/d 26000 07/

06/

16

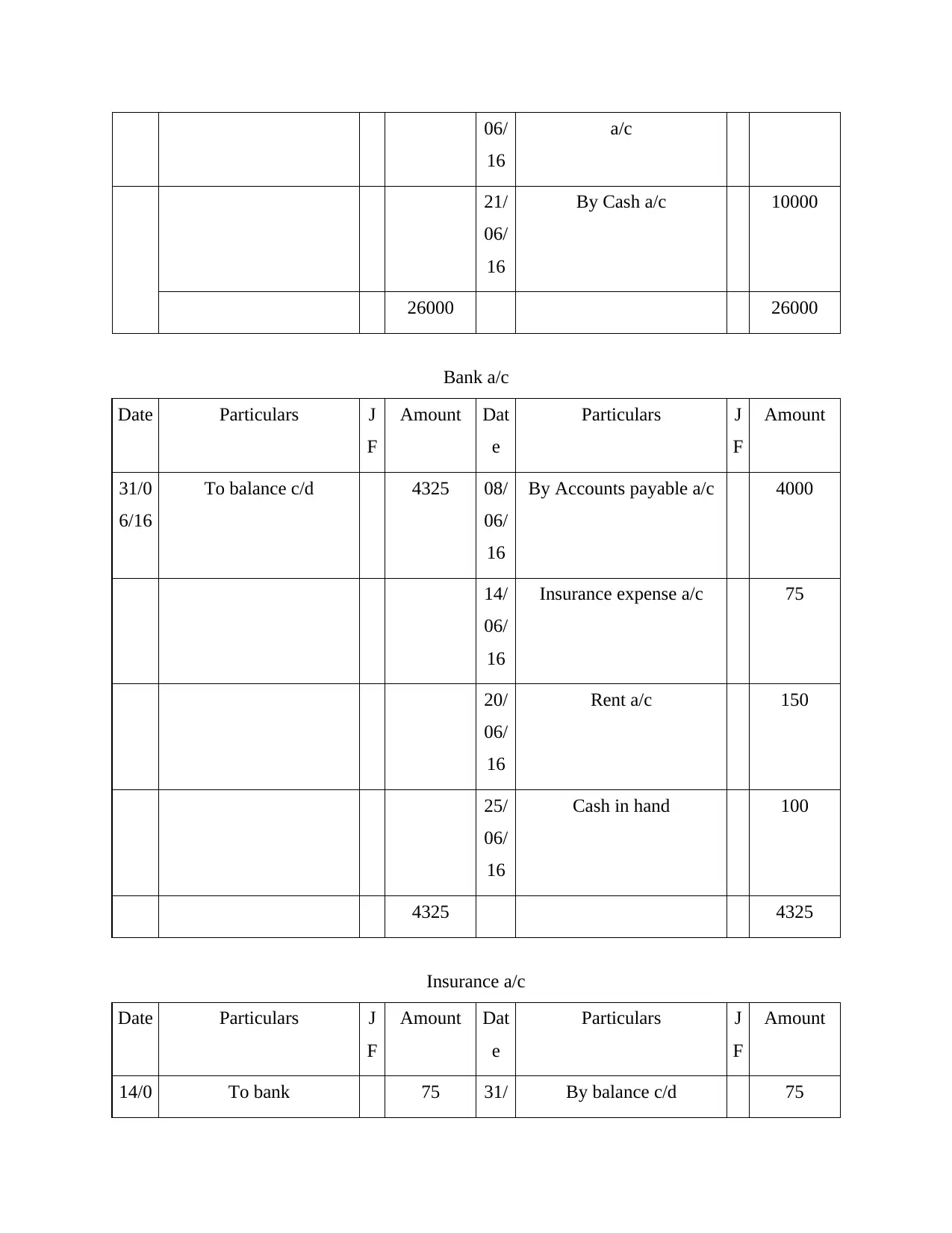

By Cash a/c 4000

15/ By Accounts receivable 12000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

06/

16

a/c

21/

06/

16

By Cash a/c 10000

26000 26000

Bank a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

31/0

6/16

To balance c/d 4325 08/

06/

16

By Accounts payable a/c 4000

14/

06/

16

Insurance expense a/c 75

20/

06/

16

Rent a/c 150

25/

06/

16

Cash in hand 100

4325 4325

Insurance a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

14/0 To bank 75 31/ By balance c/d 75

16

a/c

21/

06/

16

By Cash a/c 10000

26000 26000

Bank a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

31/0

6/16

To balance c/d 4325 08/

06/

16

By Accounts payable a/c 4000

14/

06/

16

Insurance expense a/c 75

20/

06/

16

Rent a/c 150

25/

06/

16

Cash in hand 100

4325 4325

Insurance a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

14/0 To bank 75 31/ By balance c/d 75

6/16 06/

16

75 75

Account receivable a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

15/0

6/16

To sales a/c 12000 31/

06/

16

By balance c/d 12000

12000 12000

Computer a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

18/0

6/16

To cash a/c 3000 31/

06/

16

By balance c/d 3000

3000 3000

Rent a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

20/0

6/16

To bank a/c 150 31/

06/

16

By balance c/d 150

150 150

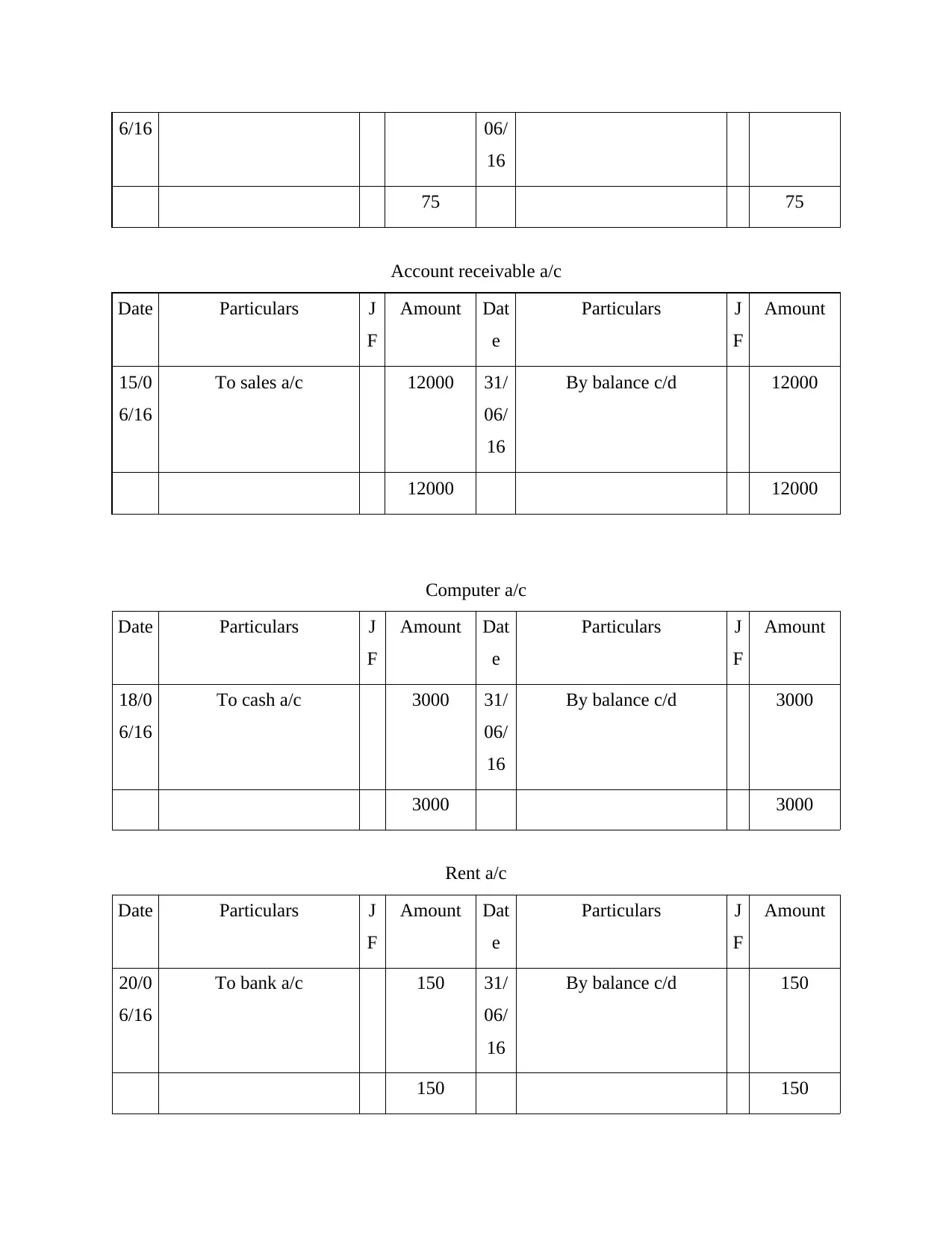

16

75 75

Account receivable a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

15/0

6/16

To sales a/c 12000 31/

06/

16

By balance c/d 12000

12000 12000

Computer a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

18/0

6/16

To cash a/c 3000 31/

06/

16

By balance c/d 3000

3000 3000

Rent a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

20/0

6/16

To bank a/c 150 31/

06/

16

By balance c/d 150

150 150

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash in hand a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

25/0

6/16

To bank a/c 100 30/

06/

16

By stationary 30

31/

06/

16

By balance c/d 70

100 100

Stationary a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

30/0

6/16

To Cash in hand a/c 30 31/

06/

16

By balance c/d 30

30 30

(3) Trial balance:

Particulars DR CR

Cash a/c 76000

Capital a/c 65000

Purchase a/c 18000

Accounts payable a/c 14000

Sales a/c 26000

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

25/0

6/16

To bank a/c 100 30/

06/

16

By stationary 30

31/

06/

16

By balance c/d 70

100 100

Stationary a/c

Date Particulars J

F

Amount Dat

e

Particulars J

F

Amount

30/0

6/16

To Cash in hand a/c 30 31/

06/

16

By balance c/d 30

30 30

(3) Trial balance:

Particulars DR CR

Cash a/c 76000

Capital a/c 65000

Purchase a/c 18000

Accounts payable a/c 14000

Sales a/c 26000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

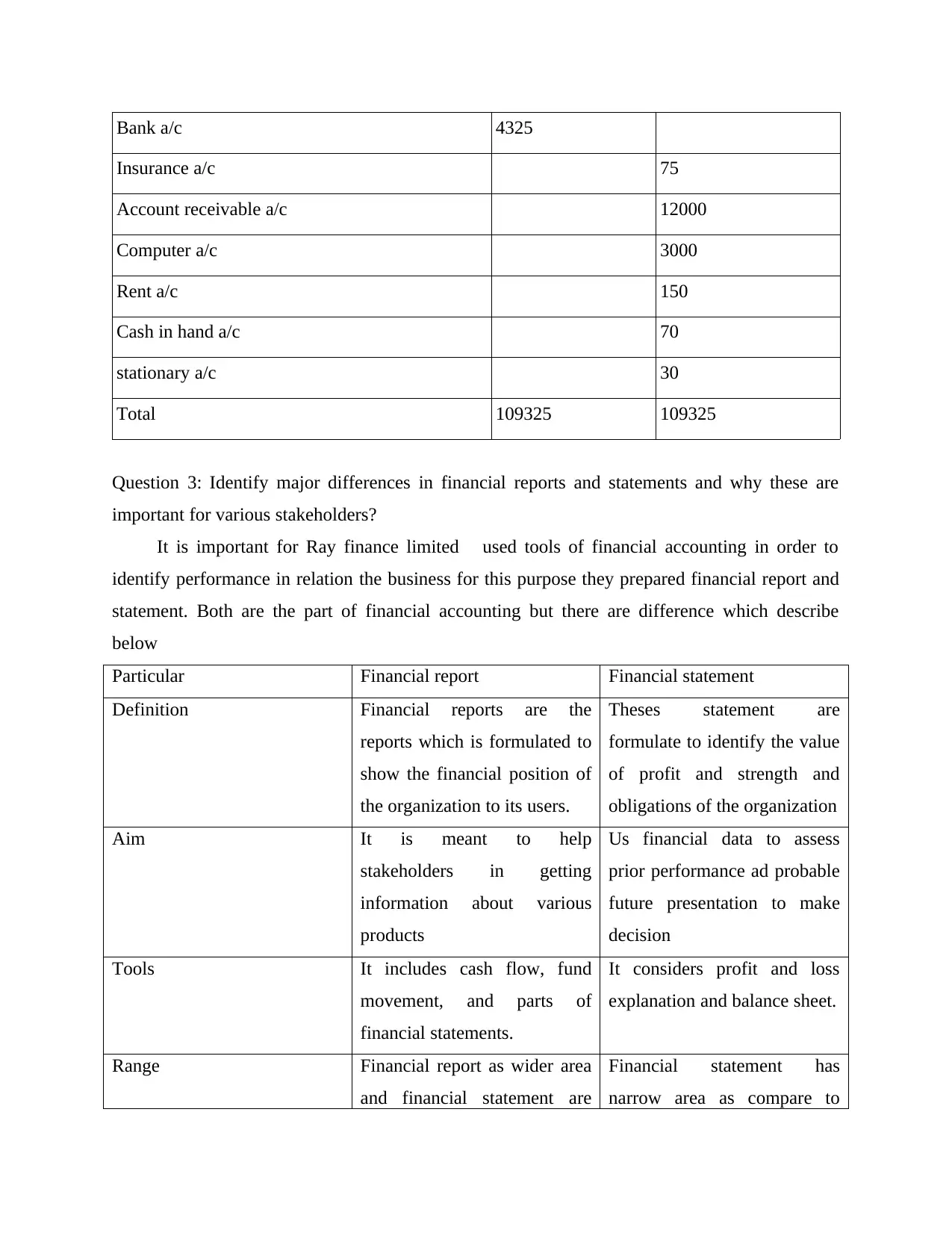

Bank a/c 4325

Insurance a/c 75

Account receivable a/c 12000

Computer a/c 3000

Rent a/c 150

Cash in hand a/c 70

stationary a/c 30

Total 109325 109325

Question 3: Identify major differences in financial reports and statements and why these are

important for various stakeholders?

It is important for Ray finance limited used tools of financial accounting in order to

identify performance in relation the business for this purpose they prepared financial report and

statement. Both are the part of financial accounting but there are difference which describe

below

Particular Financial report Financial statement

Definition Financial reports are the

reports which is formulated to

show the financial position of

the organization to its users.

Theses statement are

formulate to identify the value

of profit and strength and

obligations of the organization

Aim It is meant to help

stakeholders in getting

information about various

products

Us financial data to assess

prior performance ad probable

future presentation to make

decision

Tools It includes cash flow, fund

movement, and parts of

financial statements.

It considers profit and loss

explanation and balance sheet.

Range Financial report as wider area

and financial statement are

Financial statement has

narrow area as compare to

Insurance a/c 75

Account receivable a/c 12000

Computer a/c 3000

Rent a/c 150

Cash in hand a/c 70

stationary a/c 30

Total 109325 109325

Question 3: Identify major differences in financial reports and statements and why these are

important for various stakeholders?

It is important for Ray finance limited used tools of financial accounting in order to

identify performance in relation the business for this purpose they prepared financial report and

statement. Both are the part of financial accounting but there are difference which describe

below

Particular Financial report Financial statement

Definition Financial reports are the

reports which is formulated to

show the financial position of

the organization to its users.

Theses statement are

formulate to identify the value

of profit and strength and

obligations of the organization

Aim It is meant to help

stakeholders in getting

information about various

products

Us financial data to assess

prior performance ad probable

future presentation to make

decision

Tools It includes cash flow, fund

movement, and parts of

financial statements.

It considers profit and loss

explanation and balance sheet.

Range Financial report as wider area

and financial statement are

Financial statement has

narrow area as compare to

part of it financial reports.

Requirement of financial report: it can be define as that standard practices which organization

proved accurate information to the users of company . Following are the requirement of finance

report(Chhabra, and Pattanayak, 2014).

Financial reports are use to provide article as proof.

It is useful in analysing financial performance of the business organization.

It helps in tracking period ad managements of obligation

With use of financial report manager take decision regarding future business policies

Back and other financial institution give loan to organization on the basis of checking financial

reports of the organization

It is useful in identify real cash inflow and out flow activities.

With the use of financial report Ray finance limited will be able to compare their performance

with rival companies.

It helps in taking division regarding given incentive future business project.

There are two types of users of financial reports

Internal users: These includes member which are belongs with part of business

organization, which help in running business activities

Management department: They are help in formulating policies and taking decision

regarding business activities. They use financial reports for caging strategies and take decision

regarding expansion of business

Employees: They are parson which engaged in performing business activities. They are

directly interest in financial report as by analysis the report they make sure regarding their job

security, profit and incentive organization given to them.

External users: Those users which are not part of organization but indirectly internal to

the business are external users (Klein, 2015).

Investors: Define as those persons were directly related to the organisation and help firm

in fulfilling the financial requirement because these individuals invest in the different policies of

the organisation so that form can perform its various activities.

Requirement of financial report: it can be define as that standard practices which organization

proved accurate information to the users of company . Following are the requirement of finance

report(Chhabra, and Pattanayak, 2014).

Financial reports are use to provide article as proof.

It is useful in analysing financial performance of the business organization.

It helps in tracking period ad managements of obligation

With use of financial report manager take decision regarding future business policies

Back and other financial institution give loan to organization on the basis of checking financial

reports of the organization

It is useful in identify real cash inflow and out flow activities.

With the use of financial report Ray finance limited will be able to compare their performance

with rival companies.

It helps in taking division regarding given incentive future business project.

There are two types of users of financial reports

Internal users: These includes member which are belongs with part of business

organization, which help in running business activities

Management department: They are help in formulating policies and taking decision

regarding business activities. They use financial reports for caging strategies and take decision

regarding expansion of business

Employees: They are parson which engaged in performing business activities. They are

directly interest in financial report as by analysis the report they make sure regarding their job

security, profit and incentive organization given to them.

External users: Those users which are not part of organization but indirectly internal to

the business are external users (Klein, 2015).

Investors: Define as those persons were directly related to the organisation and help firm

in fulfilling the financial requirement because these individuals invest in the different policies of

the organisation so that form can perform its various activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.