Financial Accounting 1: Financial Reporting and Accounting Principles

VerifiedAdded on 2023/01/10

|22

|4501

|43

Report

AI Summary

This financial accounting report delves into key concepts such as business transactions, encompassing sales, purchases, receipts, and payments, and their recording using single and double-entry bookkeeping methods. It explores the significance of the trial balance in verifying arithmetic accuracy and preparing financial statements. The report further distinguishes between financial reports and financial statements, outlining their differences in content, scope, and users. It also explains fundamental accounting principles, including monetary unit accounting, the going concern principle, and conservatism. The report examines journal entries, ledger accounts, and trial balance. Additionally, the report touches on bank reconciliation and control accounts, providing a complete analysis of financial accounting principles and practices.

Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

SCENARIO 1..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................5

Question 3. Difference between financial report and statement................................................11

Question 4. Description of the fundamental principles of accounting......................................13

Question 5..................................................................................................................................14

SCENARIO 2................................................................................................................................16

Question 1. Description about bank reconciliation....................................................................16

Question 2. Description about control accounts........................................................................17

Question 4..................................................................................................................................17

Question 5..................................................................................................................................18

REFERENCES..............................................................................................................................20

2

INTRODUCTION...........................................................................................................................3

SCENARIO 1..................................................................................................................................3

Question 1....................................................................................................................................3

Question 2....................................................................................................................................5

Question 3. Difference between financial report and statement................................................11

Question 4. Description of the fundamental principles of accounting......................................13

Question 5..................................................................................................................................14

SCENARIO 2................................................................................................................................16

Question 1. Description about bank reconciliation....................................................................16

Question 2. Description about control accounts........................................................................17

Question 4..................................................................................................................................17

Question 5..................................................................................................................................18

REFERENCES..............................................................................................................................20

2

INTRODUCTION

Financial accounting is a unique part of accounting that monitors a person's budget swaps.

Using standard rules, exchanges are recorded, resumed and included in a cash report or a balance

sheet report, such as a paycheck or cash register.

Organizations publish tax summaries on a standard calendar. Notifications are considered

external because they are issued to people outside the organization, with the essential

beneficiaries being the owners / investors, just like specialized loan experts. In the event that the

company's shares are not traded on an open market, at least its balance sheet reports (and other

balance sheet reports) will be widely disseminated and the data could become optional

beneficiaries, such as, for example, contenders, messengers, employees, work associations and

business analysts.

It is essential to note that the purpose of financial accounting is not to report an agency

estimate. Or perhaps, his motivation is to provide others with enough data to justify a group

estimate for themselves. (Suryanto and Ridwansyah, 2016).

This study is divided into two categories, each of which has specific problems. To complete

the main partition, some questions should be asked, similar to the type of exchanges, including a

one-section framework, as well as the double configuration of accounting corridor, first -justice

just as widely. The second part of this section aims to create the diary extract sections as for each

exchange, the tables and a trial balance. The difference between the tax summary and the balance

sheet report, the required accounting standards and the salary call are also key elements of this

dimension. Area 2 focuses on designing banking negotiation relationships, diary sections, several

control accounts, debit charts and a number of different dimensions.

SCENARIO 1

Question 1

Business transction: In the accounting sector, a business transaction implies a sort of trend that

modifies the estimate of the benefits, liabilities or value of an association owner. These types of

exchanges are two-category exchanges that involve a buyer and a seller and usually involve

money here and there. Currency exchanges in the accounts are recorded in the accounting journal

in sequence.

Types of business transaction

3

Financial accounting is a unique part of accounting that monitors a person's budget swaps.

Using standard rules, exchanges are recorded, resumed and included in a cash report or a balance

sheet report, such as a paycheck or cash register.

Organizations publish tax summaries on a standard calendar. Notifications are considered

external because they are issued to people outside the organization, with the essential

beneficiaries being the owners / investors, just like specialized loan experts. In the event that the

company's shares are not traded on an open market, at least its balance sheet reports (and other

balance sheet reports) will be widely disseminated and the data could become optional

beneficiaries, such as, for example, contenders, messengers, employees, work associations and

business analysts.

It is essential to note that the purpose of financial accounting is not to report an agency

estimate. Or perhaps, his motivation is to provide others with enough data to justify a group

estimate for themselves. (Suryanto and Ridwansyah, 2016).

This study is divided into two categories, each of which has specific problems. To complete

the main partition, some questions should be asked, similar to the type of exchanges, including a

one-section framework, as well as the double configuration of accounting corridor, first -justice

just as widely. The second part of this section aims to create the diary extract sections as for each

exchange, the tables and a trial balance. The difference between the tax summary and the balance

sheet report, the required accounting standards and the salary call are also key elements of this

dimension. Area 2 focuses on designing banking negotiation relationships, diary sections, several

control accounts, debit charts and a number of different dimensions.

SCENARIO 1

Question 1

Business transction: In the accounting sector, a business transaction implies a sort of trend that

modifies the estimate of the benefits, liabilities or value of an association owner. These types of

exchanges are two-category exchanges that involve a buyer and a seller and usually involve

money here and there. Currency exchanges in the accounts are recorded in the accounting journal

in sequence.

Types of business transaction

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are four main types of currency exchange that take place in a company. These four types

of budget exchanges are business, purchasing, revenue and allowances. How about pausing for a

moment to find out all:

Sales are transactions in which ownership is transferred from the buyer to the seller for

cash or credit. Market exchanges are recorded in the accounting diary for the seller as an

expense of cash or available documents and as a strong representative for the business

account.

Purchases are the transactions which are needed by a company to obtain the products or

administrations that are expected to fulfil the goals of the society. Purchases made with

real money include a charge on the stock register and a good cash rep. If the purchase is

made with a credit account, the debit department would now be in the share register and

the credit transfer would be to the debt register.

Receipts are trade related to the transportation of products or administrations to another

company. The exchange of receipts is recorded in the seller's diary as cash expenditure

and as a strong representative for creditors.

Payments are transactions that relate to a company that receives cash for a reasonable

amount of money or administration. They are recorded in the company's accounting diary

giving a deserving representative and an allowance for the debtor's liabilities.

Single entry and double entry book keeping

In single entry accounting, revenues and expenses for exchanges are recorded in a sales

schedule, but the structure of the two-pointed corridor begins with a diary, followed by records,

initial actions, last tax reports.

Date Description Transaction value Balance

XX-XX-XXXX £ 0000.00 £ 0000.00

Most organizations, even most private companies, use a two-pronged division to describe their

accounting requirements. Two features of double entry accounting are that each record has two

sections and each exchange has two records. Two corridors are created for each exchange: cost

in one table and credit in another. Double-entry accounting method works on basis of the

4

of budget exchanges are business, purchasing, revenue and allowances. How about pausing for a

moment to find out all:

Sales are transactions in which ownership is transferred from the buyer to the seller for

cash or credit. Market exchanges are recorded in the accounting diary for the seller as an

expense of cash or available documents and as a strong representative for the business

account.

Purchases are the transactions which are needed by a company to obtain the products or

administrations that are expected to fulfil the goals of the society. Purchases made with

real money include a charge on the stock register and a good cash rep. If the purchase is

made with a credit account, the debit department would now be in the share register and

the credit transfer would be to the debt register.

Receipts are trade related to the transportation of products or administrations to another

company. The exchange of receipts is recorded in the seller's diary as cash expenditure

and as a strong representative for creditors.

Payments are transactions that relate to a company that receives cash for a reasonable

amount of money or administration. They are recorded in the company's accounting diary

giving a deserving representative and an allowance for the debtor's liabilities.

Single entry and double entry book keeping

In single entry accounting, revenues and expenses for exchanges are recorded in a sales

schedule, but the structure of the two-pointed corridor begins with a diary, followed by records,

initial actions, last tax reports.

Date Description Transaction value Balance

XX-XX-XXXX £ 0000.00 £ 0000.00

Most organizations, even most private companies, use a two-pronged division to describe their

accounting requirements. Two features of double entry accounting are that each record has two

sections and each exchange has two records. Two corridors are created for each exchange: cost

in one table and credit in another. Double-entry accounting method works on basis of the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting formula, for eg, Assets = Liabilities + Owner's capital (Robson,, Young and Power,

2017). Framework of the Double Entry keeping records is seen as follows:

Date Description L.F Debit Credit

XX-XX-XXXX £ 0000.00

£ 0000.00

Trial balance and its importance

The trial balance of a company is a summary of the closing balance of the accounting

statements on a given date and is the first step towards preparing tax reports. It is usually

prepared near the end of an accounting period to facilitate the preparation of the financial

statements. Changes in the setting of margin records are in debit and credit adjustments. The

utility and business records are presented on the debit balance side of the test, while the liability,

capital and revenue accounts are presented on the credit side. If all accounting shares are

effectively recorded and all postage changes are extracted with accuracy, the totality of the debit

changes occurring in the original balance sheet must be equal to the total of the credit changes.

Importance of trial balance:

Verification of arithmetic precision: It means that the test balance is used to determine the

actual quantity recorded in the right half of the current record while transferring the

figures from various registers such as books to buy, trade books, cash books and so on.

The starting balance sheet along with the standard ledger accounts is also useful for

examining the accuracy of the books for special purposes.

Assistance in preparing the balance sheets: Profit and loss account, balance sheet and

cash flow statement towards the end of each year should help accounting. The

equivalents of all the record accounts used to obtain ready-made tax summaries are now

available in the first parity and subsequently simplify the planning and analysis of the

balance sheet reports.

Assistance with correction errors: The total start-up equity cost must be equal to the

equity credit accumulation. This examines the accuracy of the record numbers. In the

event that this does not happen, the accounting officer will recover it and correct it.

Accountants therefore feel relieved when coordinating start-up cost balances and

collections (Narayanaswamy, 2017).

5

2017). Framework of the Double Entry keeping records is seen as follows:

Date Description L.F Debit Credit

XX-XX-XXXX £ 0000.00

£ 0000.00

Trial balance and its importance

The trial balance of a company is a summary of the closing balance of the accounting

statements on a given date and is the first step towards preparing tax reports. It is usually

prepared near the end of an accounting period to facilitate the preparation of the financial

statements. Changes in the setting of margin records are in debit and credit adjustments. The

utility and business records are presented on the debit balance side of the test, while the liability,

capital and revenue accounts are presented on the credit side. If all accounting shares are

effectively recorded and all postage changes are extracted with accuracy, the totality of the debit

changes occurring in the original balance sheet must be equal to the total of the credit changes.

Importance of trial balance:

Verification of arithmetic precision: It means that the test balance is used to determine the

actual quantity recorded in the right half of the current record while transferring the

figures from various registers such as books to buy, trade books, cash books and so on.

The starting balance sheet along with the standard ledger accounts is also useful for

examining the accuracy of the books for special purposes.

Assistance in preparing the balance sheets: Profit and loss account, balance sheet and

cash flow statement towards the end of each year should help accounting. The

equivalents of all the record accounts used to obtain ready-made tax summaries are now

available in the first parity and subsequently simplify the planning and analysis of the

balance sheet reports.

Assistance with correction errors: The total start-up equity cost must be equal to the

equity credit accumulation. This examines the accuracy of the record numbers. In the

event that this does not happen, the accounting officer will recover it and correct it.

Accountants therefore feel relieved when coordinating start-up cost balances and

collections (Narayanaswamy, 2017).

5

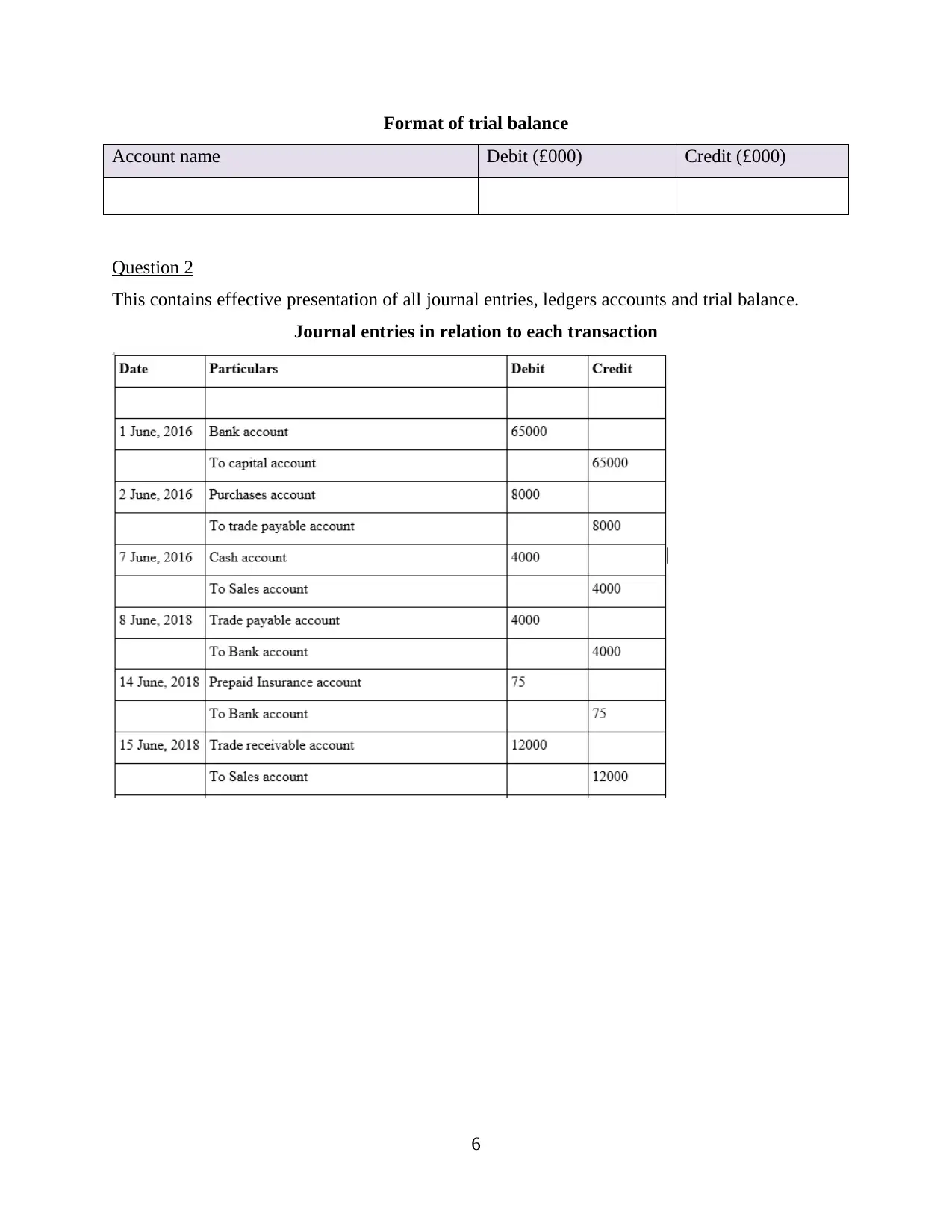

Format of trial balance

Account name Debit (£000) Credit (£000)

Question 2

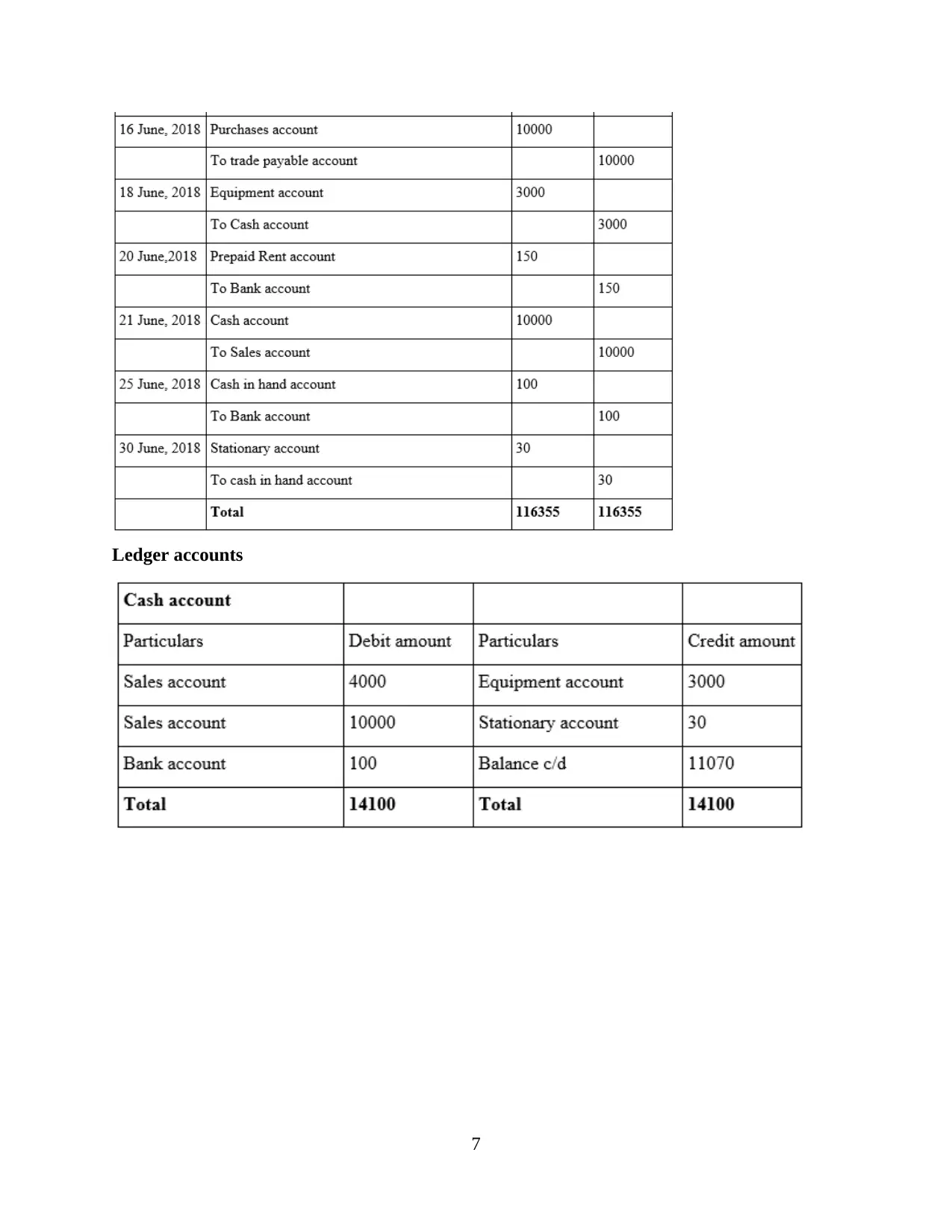

This contains effective presentation of all journal entries, ledgers accounts and trial balance.

Journal entries in relation to each transaction

6

Account name Debit (£000) Credit (£000)

Question 2

This contains effective presentation of all journal entries, ledgers accounts and trial balance.

Journal entries in relation to each transaction

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

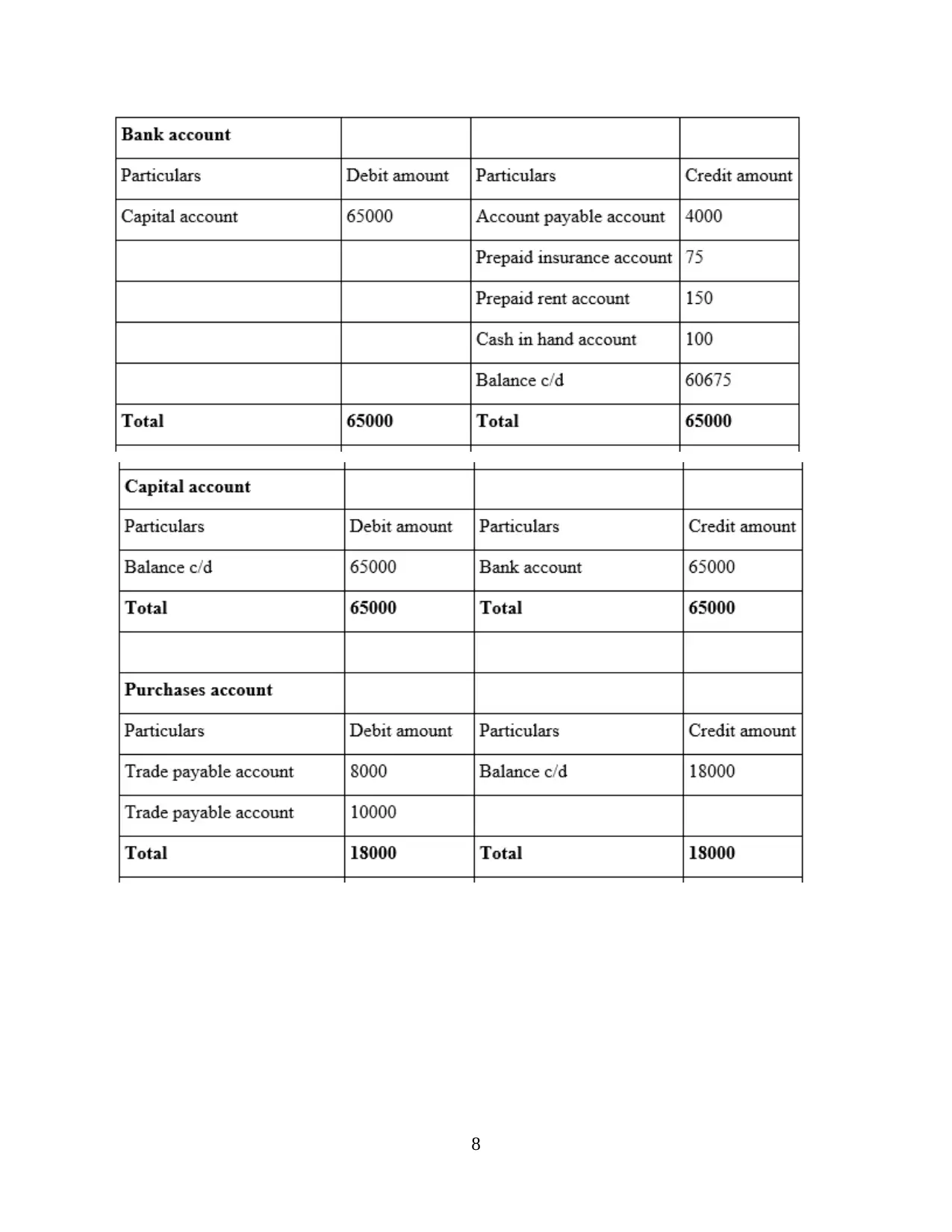

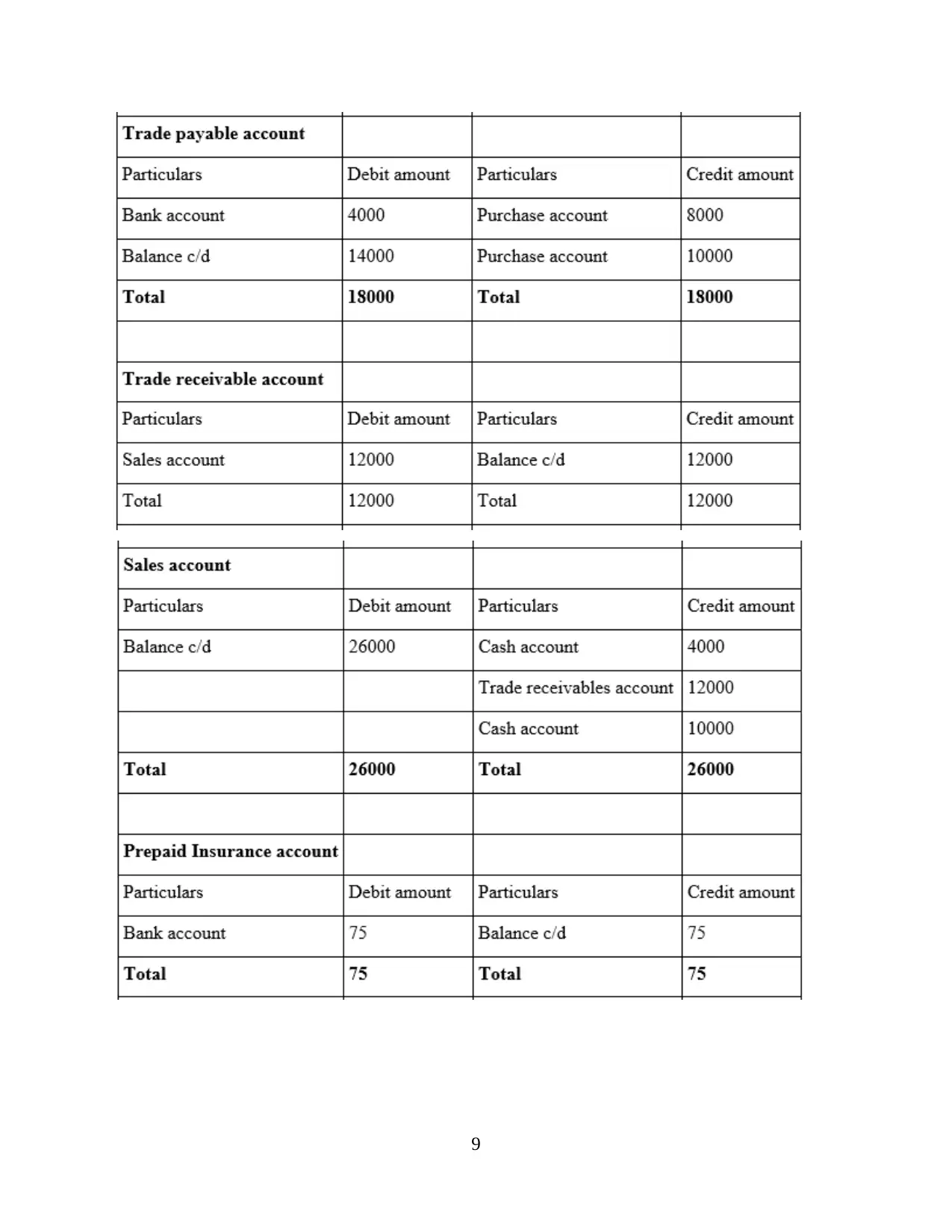

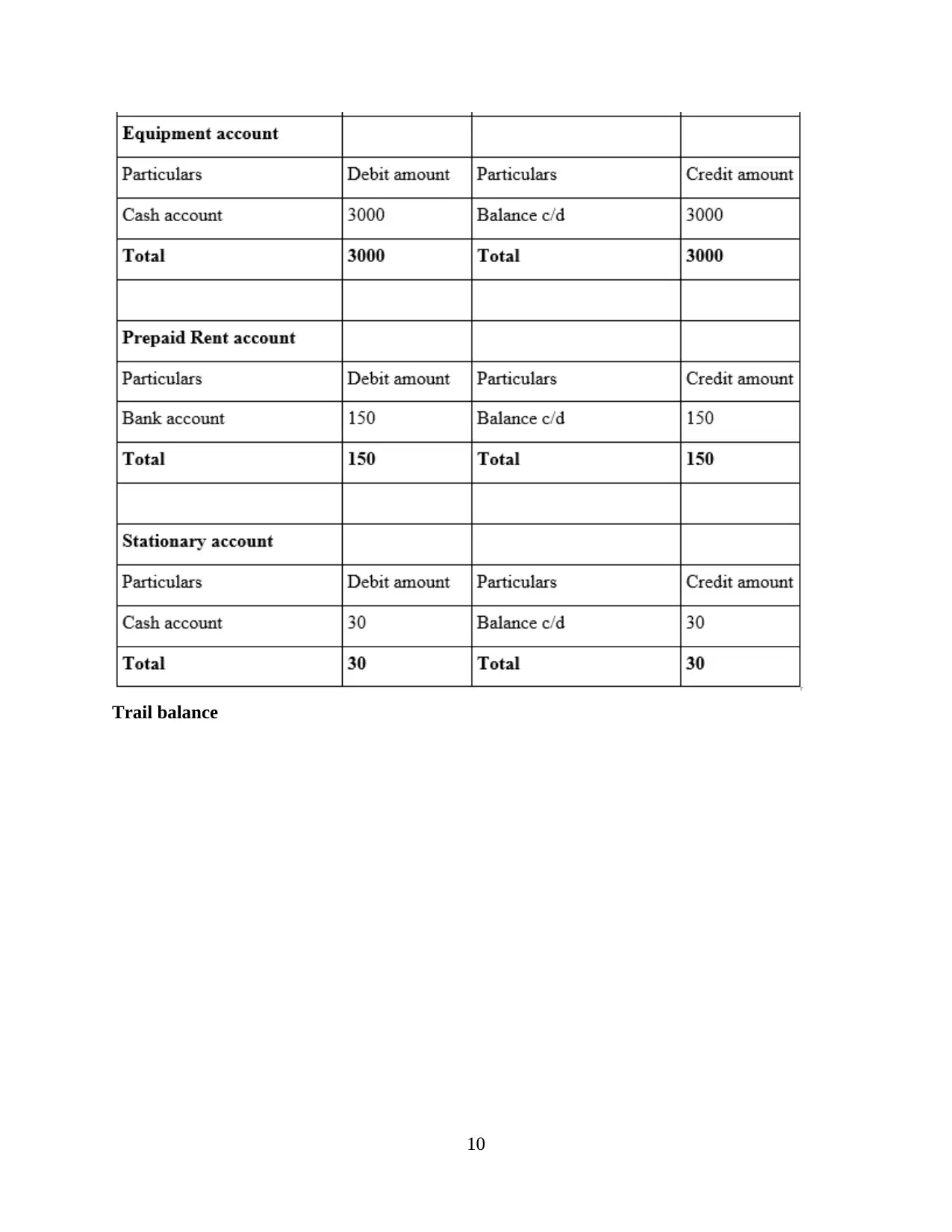

Ledger accounts

7

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

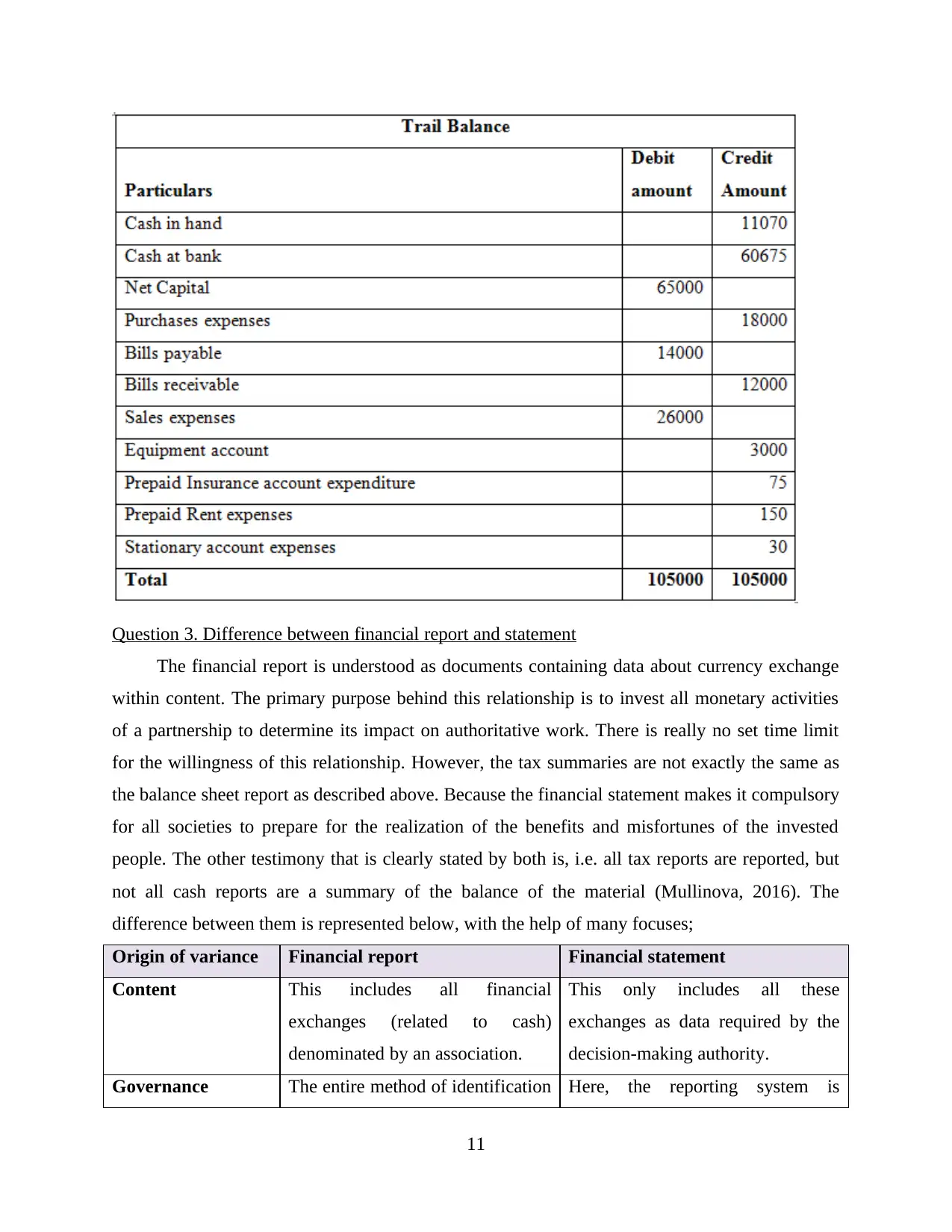

Trail balance

10

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3. Difference between financial report and statement

The financial report is understood as documents containing data about currency exchange

within content. The primary purpose behind this relationship is to invest all monetary activities

of a partnership to determine its impact on authoritative work. There is really no set time limit

for the willingness of this relationship. However, the tax summaries are not exactly the same as

the balance sheet report as described above. Because the financial statement makes it compulsory

for all societies to prepare for the realization of the benefits and misfortunes of the invested

people. The other testimony that is clearly stated by both is, i.e. all tax reports are reported, but

not all cash reports are a summary of the balance of the material (Mullinova, 2016). The

difference between them is represented below, with the help of many focuses;

Origin of variance Financial report Financial statement

Content This includes all financial

exchanges (related to cash)

denominated by an association.

This only includes all these

exchanges as data required by the

decision-making authority.

Governance The entire method of identification Here, the reporting system is

11

The financial report is understood as documents containing data about currency exchange

within content. The primary purpose behind this relationship is to invest all monetary activities

of a partnership to determine its impact on authoritative work. There is really no set time limit

for the willingness of this relationship. However, the tax summaries are not exactly the same as

the balance sheet report as described above. Because the financial statement makes it compulsory

for all societies to prepare for the realization of the benefits and misfortunes of the invested

people. The other testimony that is clearly stated by both is, i.e. all tax reports are reported, but

not all cash reports are a summary of the balance of the material (Mullinova, 2016). The

difference between them is represented below, with the help of many focuses;

Origin of variance Financial report Financial statement

Content This includes all financial

exchanges (related to cash)

denominated by an association.

This only includes all these

exchanges as data required by the

decision-making authority.

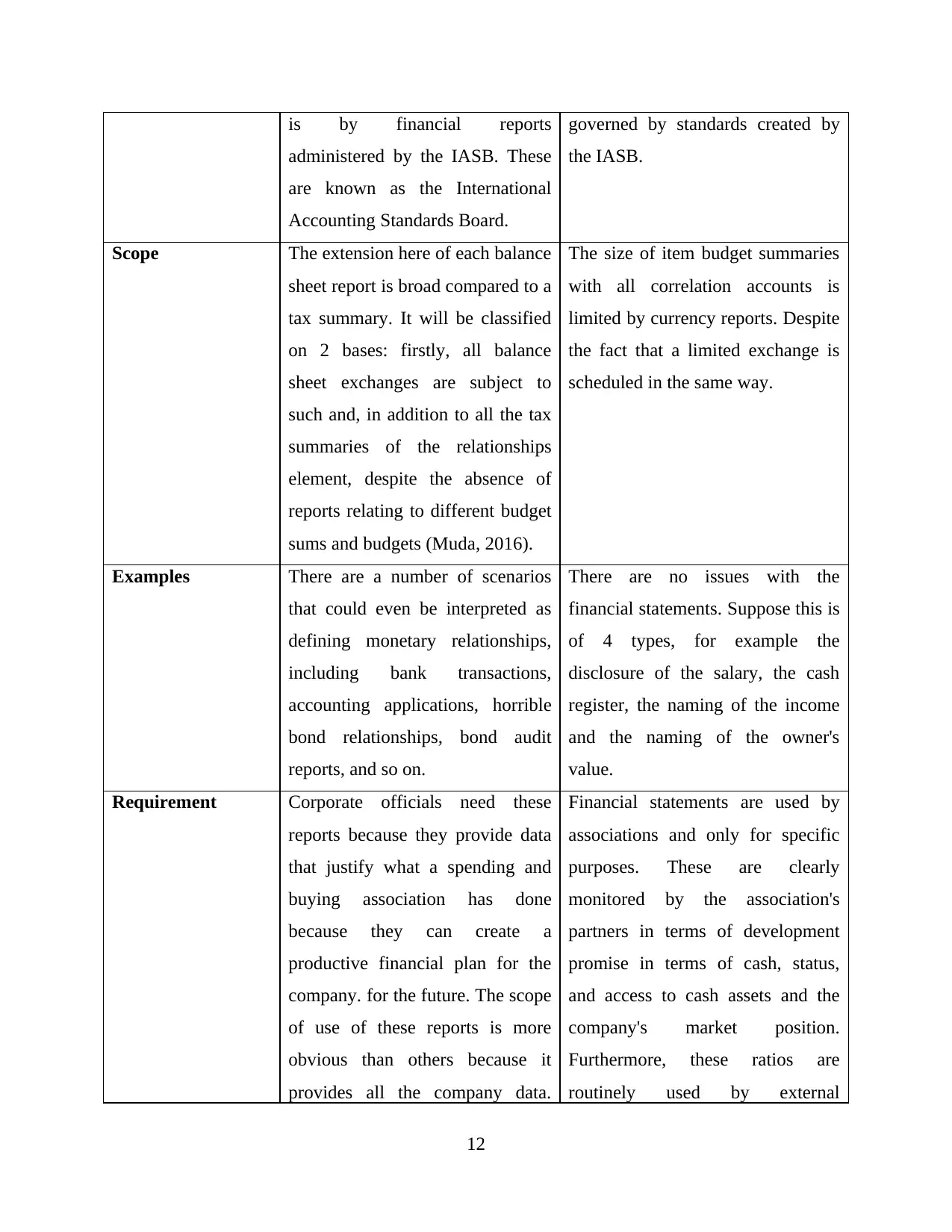

Governance The entire method of identification Here, the reporting system is

11

is by financial reports

administered by the IASB. These

are known as the International

Accounting Standards Board.

governed by standards created by

the IASB.

Scope The extension here of each balance

sheet report is broad compared to a

tax summary. It will be classified

on 2 bases: firstly, all balance

sheet exchanges are subject to

such and, in addition to all the tax

summaries of the relationships

element, despite the absence of

reports relating to different budget

sums and budgets (Muda, 2016).

The size of item budget summaries

with all correlation accounts is

limited by currency reports. Despite

the fact that a limited exchange is

scheduled in the same way.

Examples There are a number of scenarios

that could even be interpreted as

defining monetary relationships,

including bank transactions,

accounting applications, horrible

bond relationships, bond audit

reports, and so on.

There are no issues with the

financial statements. Suppose this is

of 4 types, for example the

disclosure of the salary, the cash

register, the naming of the income

and the naming of the owner's

value.

Requirement Corporate officials need these

reports because they provide data

that justify what a spending and

buying association has done

because they can create a

productive financial plan for the

company. for the future. The scope

of use of these reports is more

obvious than others because it

provides all the company data.

Financial statements are used by

associations and only for specific

purposes. These are clearly

monitored by the association's

partners in terms of development

promise in terms of cash, status,

and access to cash assets and the

company's market position.

Furthermore, these ratios are

routinely used by external

12

administered by the IASB. These

are known as the International

Accounting Standards Board.

governed by standards created by

the IASB.

Scope The extension here of each balance

sheet report is broad compared to a

tax summary. It will be classified

on 2 bases: firstly, all balance

sheet exchanges are subject to

such and, in addition to all the tax

summaries of the relationships

element, despite the absence of

reports relating to different budget

sums and budgets (Muda, 2016).

The size of item budget summaries

with all correlation accounts is

limited by currency reports. Despite

the fact that a limited exchange is

scheduled in the same way.

Examples There are a number of scenarios

that could even be interpreted as

defining monetary relationships,

including bank transactions,

accounting applications, horrible

bond relationships, bond audit

reports, and so on.

There are no issues with the

financial statements. Suppose this is

of 4 types, for example the

disclosure of the salary, the cash

register, the naming of the income

and the naming of the owner's

value.

Requirement Corporate officials need these

reports because they provide data

that justify what a spending and

buying association has done

because they can create a

productive financial plan for the

company. for the future. The scope

of use of these reports is more

obvious than others because it

provides all the company data.

Financial statements are used by

associations and only for specific

purposes. These are clearly

monitored by the association's

partners in terms of development

promise in terms of cash, status,

and access to cash assets and the

company's market position.

Furthermore, these ratios are

routinely used by external

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.