Consolidated Financial Position Analysis: Potter Co. and Sand Co.

VerifiedAdded on 2022/11/29

|2

|406

|50

Report

AI Summary

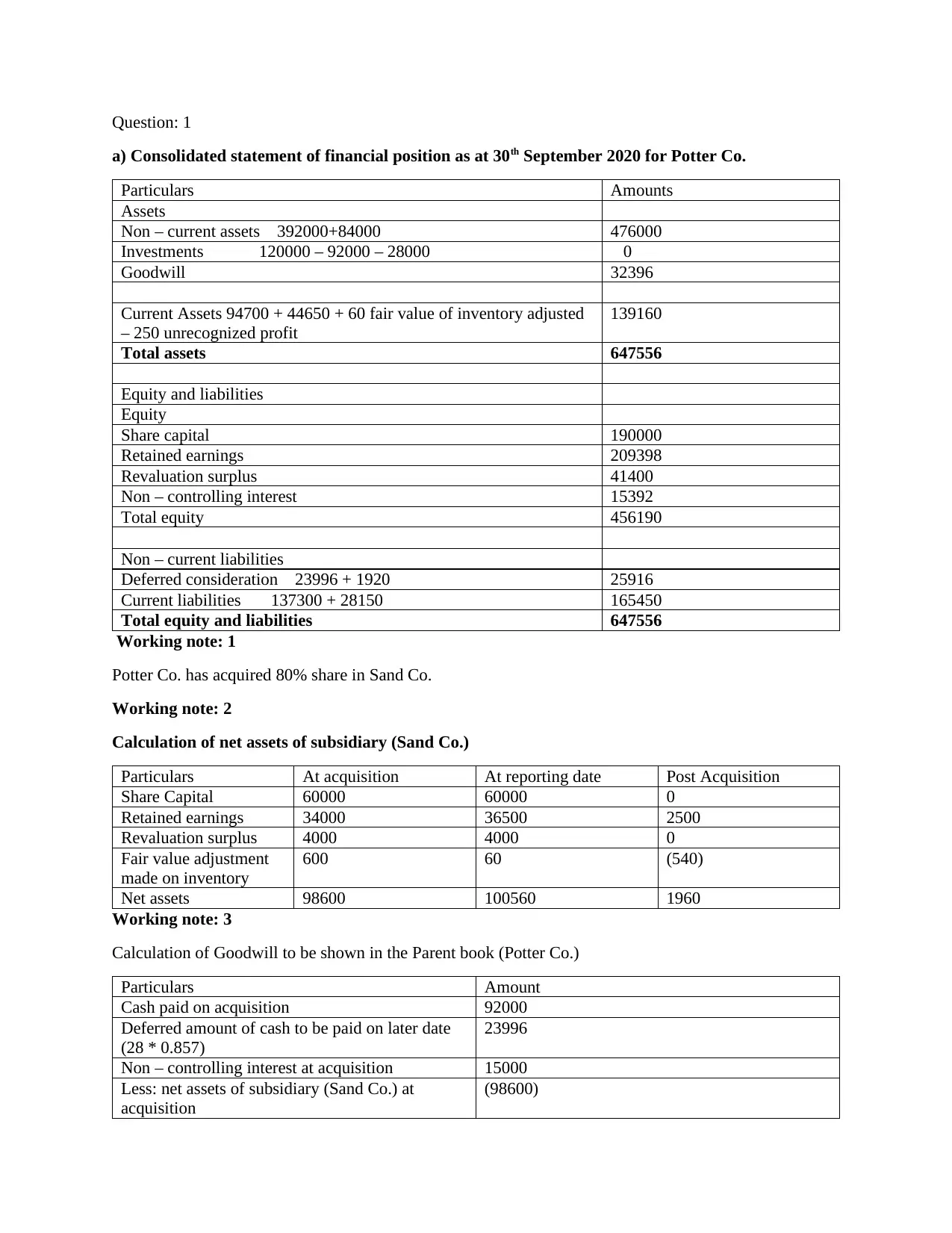

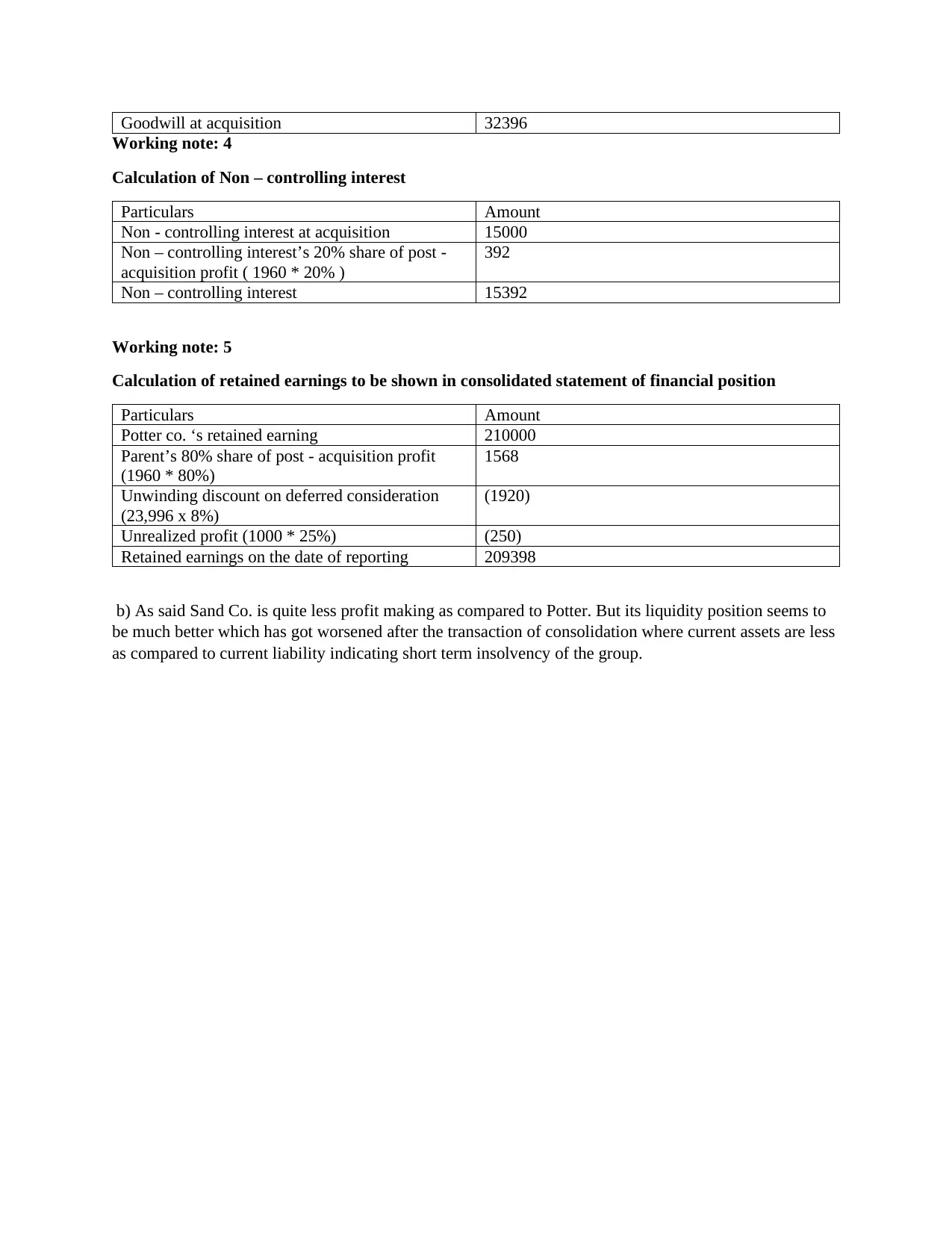

This report presents an analysis of the consolidated financial statements for Potter Co. and its subsidiary, Sand Co. It includes a detailed breakdown of the consolidated statement of financial position, including assets, liabilities, and equity. The report calculates goodwill, non-controlling interest, and retained earnings, providing insights into the financial impact of the acquisition. It also examines the liquidity position of the group, highlighting potential short-term insolvency concerns. The analysis covers key aspects of financial reporting, offering a comprehensive overview of the companies' combined financial performance and position, including working notes for calculations and adjustments. The report shows the acquisition of 80% of Sand Co. by Potter Co., detailing the valuation of assets and liabilities and the impact on equity. The report evaluates the financial health of both companies post-consolidation, addressing profitability and liquidity concerns. The report utilizes the provided data to derive insights into the consolidated financial performance.

1 out of 2

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.