Financial Accounting Report: Stakeholders and Transactions

VerifiedAdded on 2021/02/19

|28

|4582

|33

Report

AI Summary

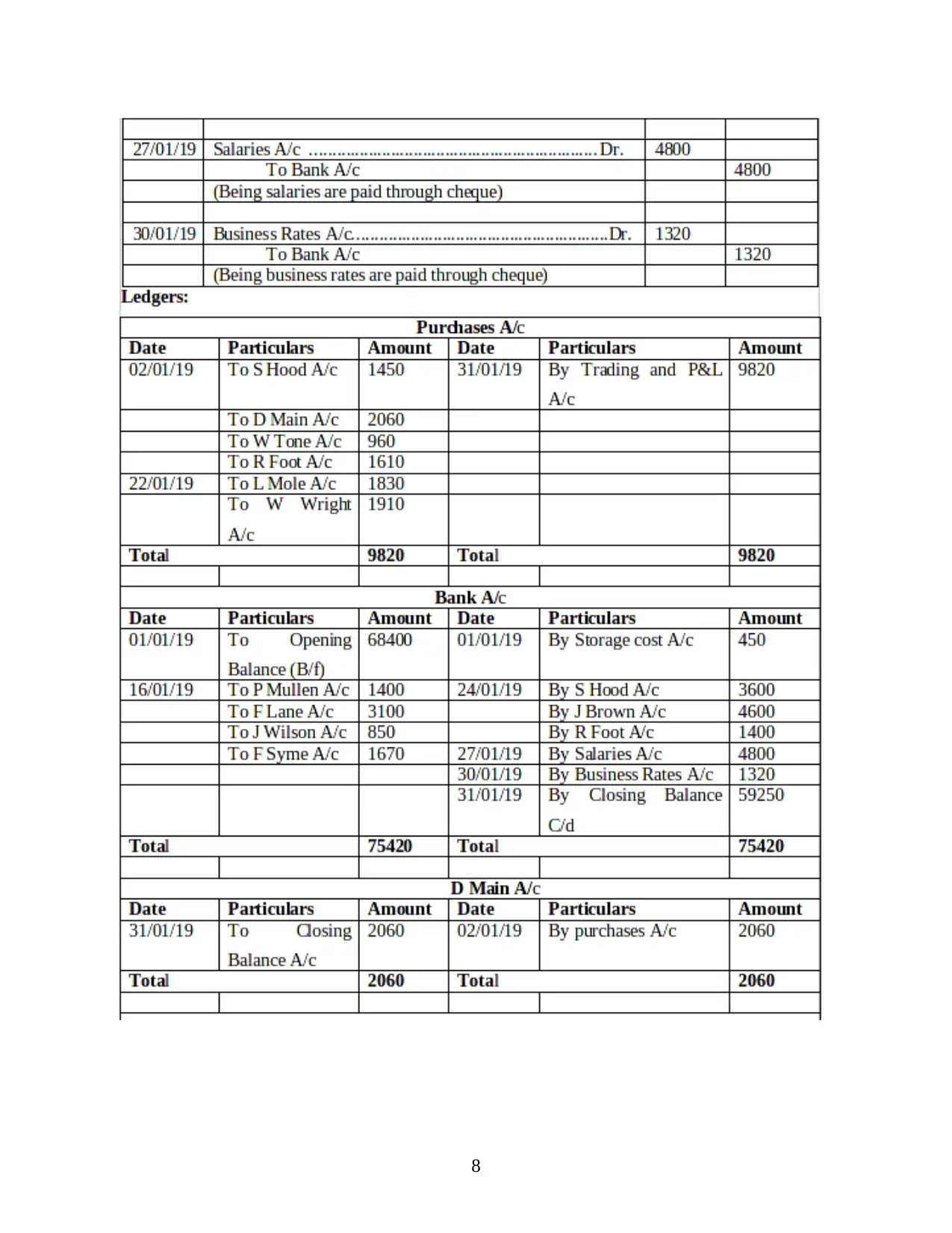

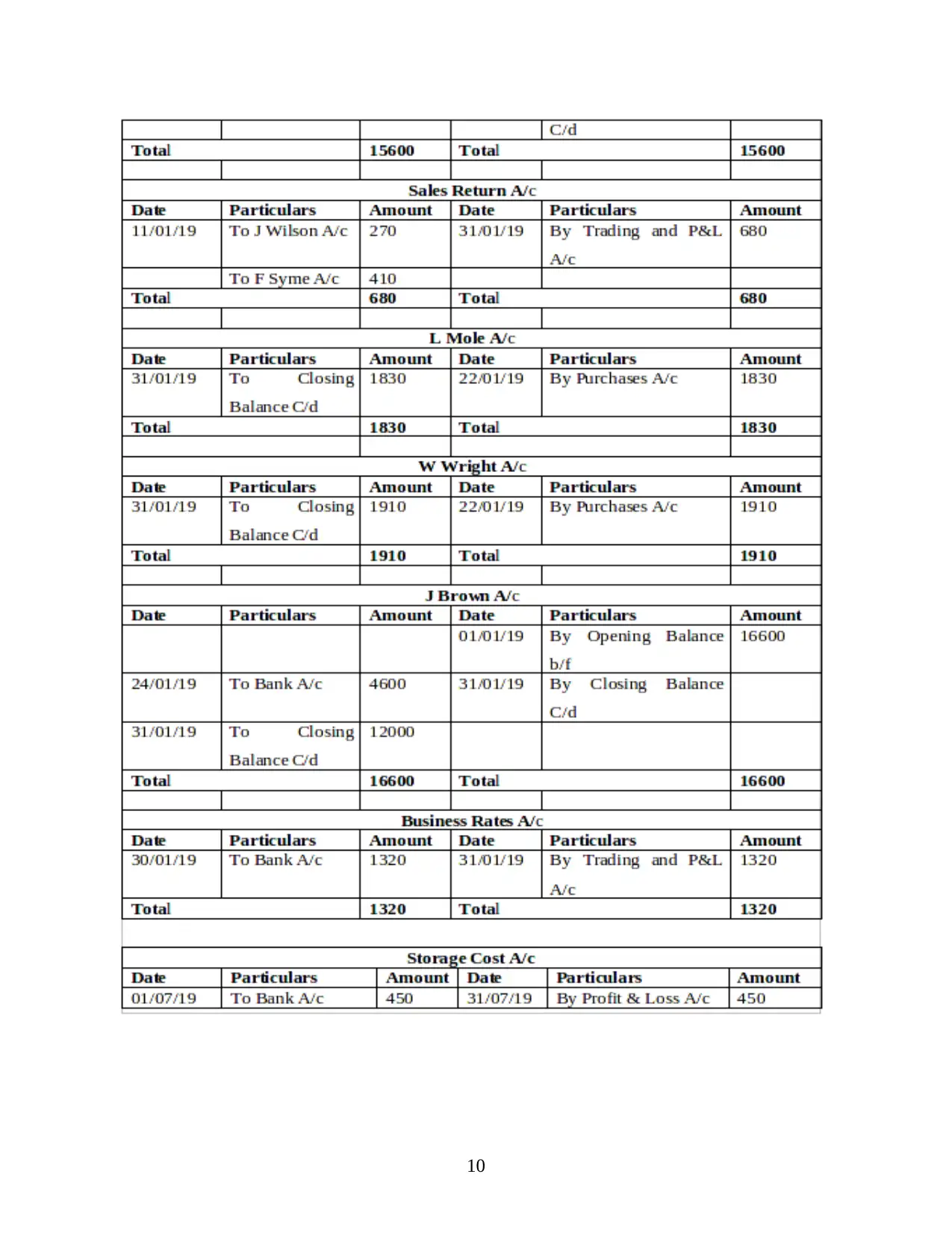

This financial accounting report examines the core concepts of financial accounting, including its purpose, the preparation of financial statements, and the importance of these statements for decision-making. The report identifies and differentiates between internal and external stakeholders, detailing their respective interests and influence on a business. It then delves into business transactions, explaining the double-entry system, manual and electronic accounting methods, and the use of debit and credit in recording transactions. The report also includes a trial balance analysis and a Profit and Loss (P&L) account for Munteanu Limited, providing a practical application of accounting principles. Finally, the report discusses key accounting conventions such as consistency and full disclosure, which are essential for ensuring the reliability and transparency of financial reporting. This report is contributed by a student and is available on Desklib, a platform offering AI-based study tools for students.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.