MPA702 Assignment 1: Financial Statements and Analysis of Park Health

VerifiedAdded on 2023/06/10

|8

|1352

|322

Homework Assignment

AI Summary

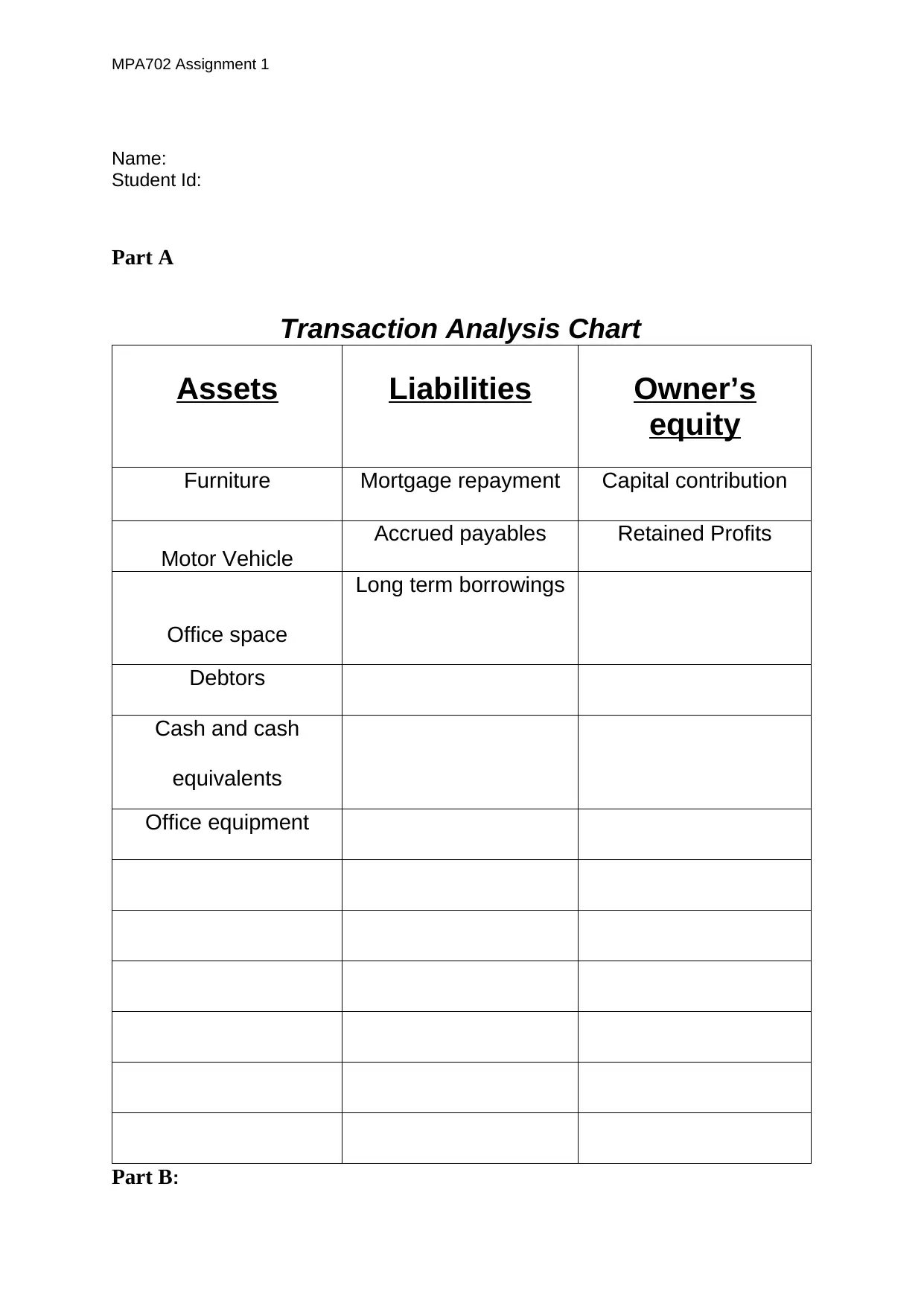

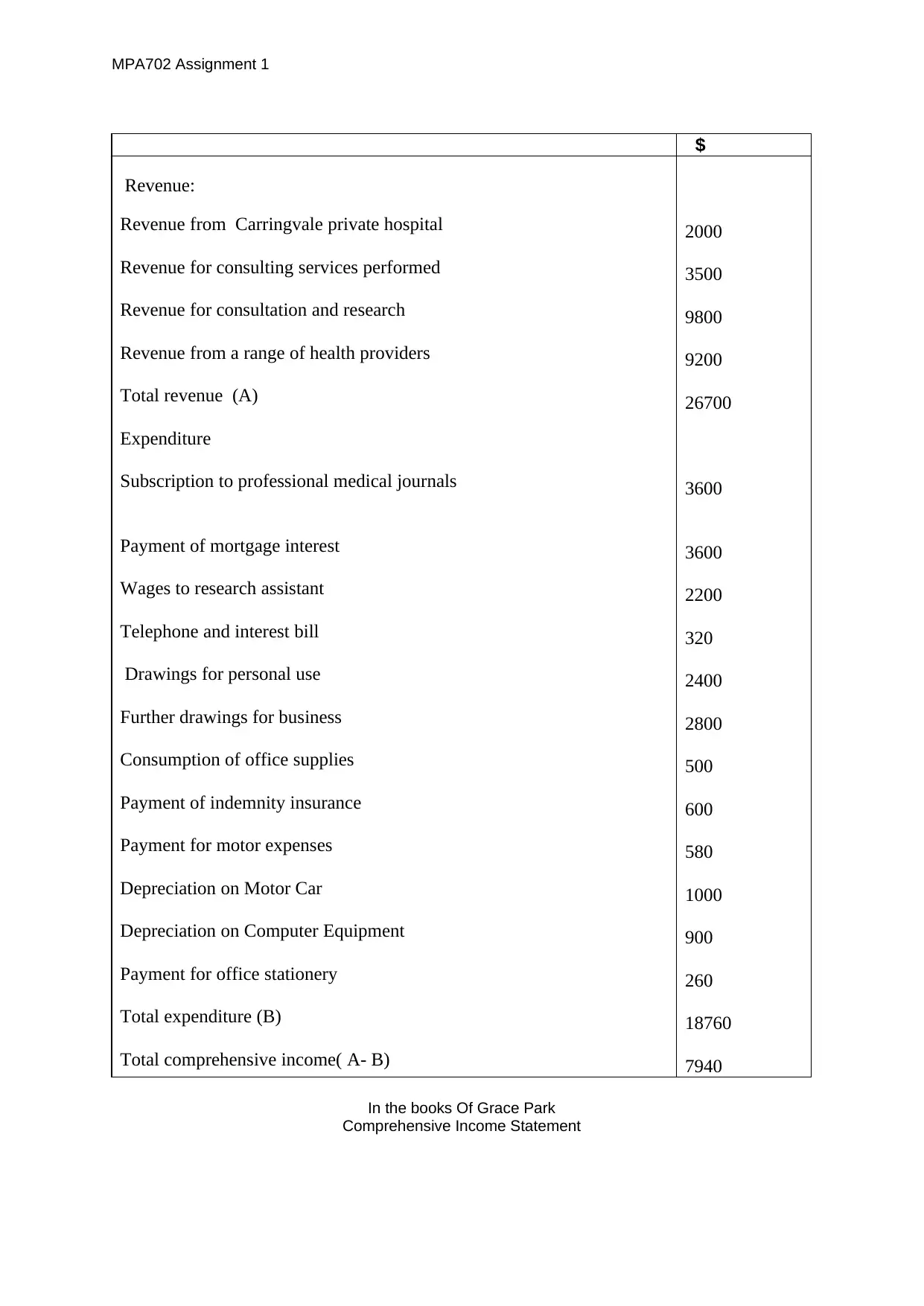

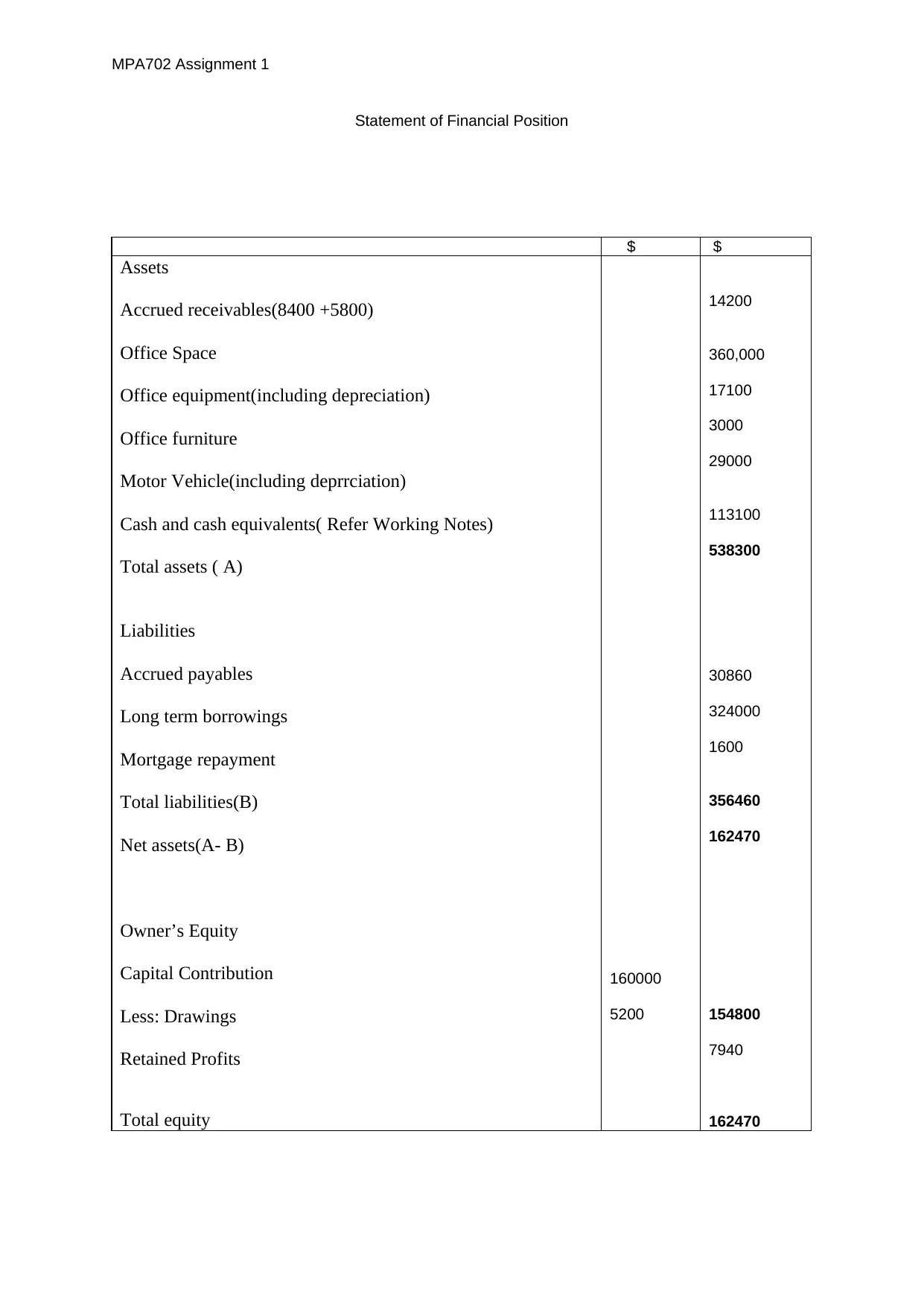

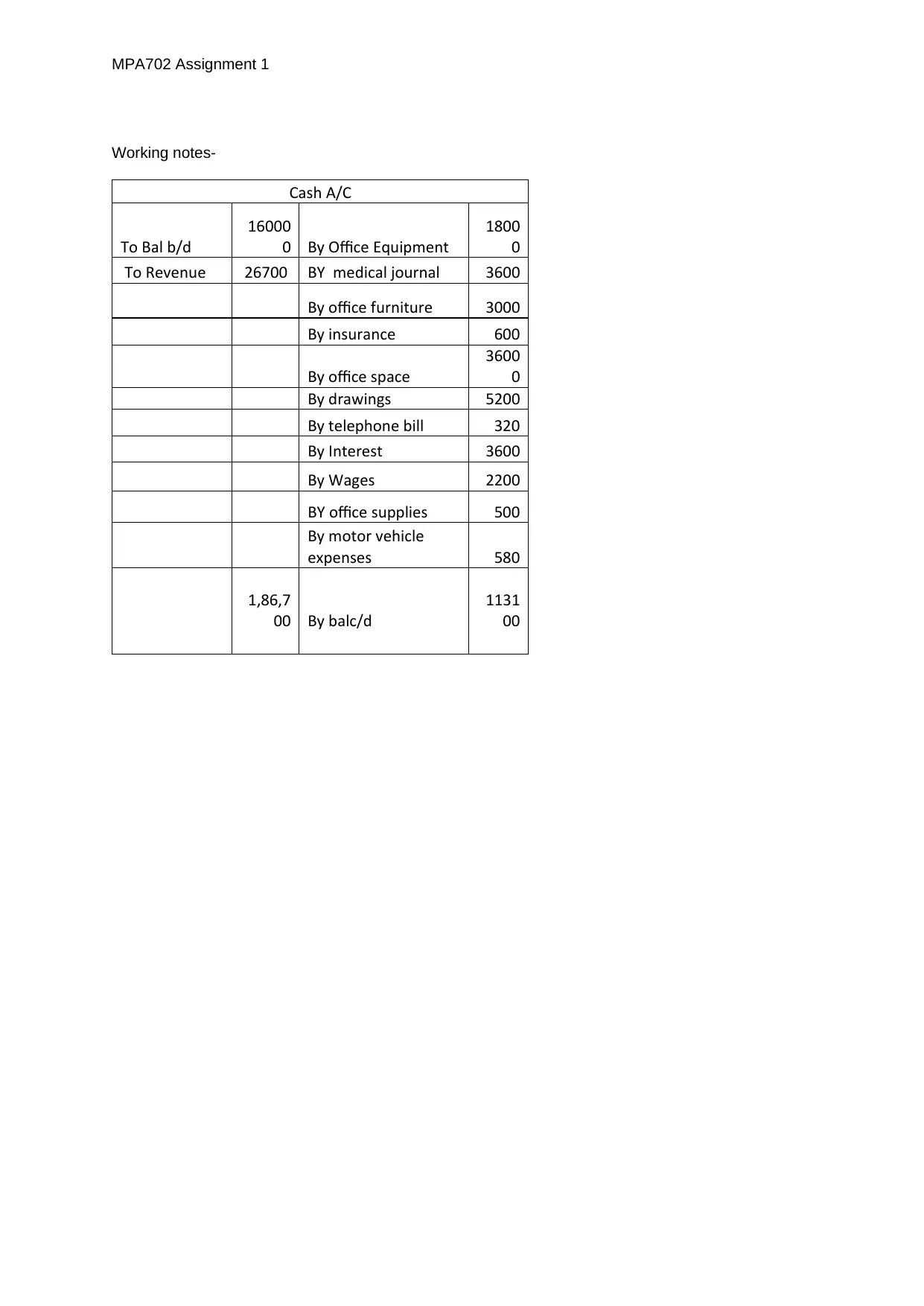

This assignment solution for MPA702, focuses on the financial analysis of a health policy and research consultant business, Park Health, owned by Grace Park. The assignment requires students to analyze transactions, create a transaction analysis chart, prepare an income statement and a statement of financial position. It includes recording transactions such as investment of funds, purchase of assets, and revenue generation. Part C of the assignment addresses the business structure, discussing the implications of unlimited liability for a sole proprietorship and recommending the formation of a Limited Liability Company (LLC) to minimize risk. The solution highlights the tax benefits and potential liabilities associated with an LLC, including instances where the corporate veil can be lifted. The document includes references to relevant academic sources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.