Financial Accounting Report: Financial Accounting Part 1 Analysis

VerifiedAdded on 2021/01/03

|16

|1395

|327

Report

AI Summary

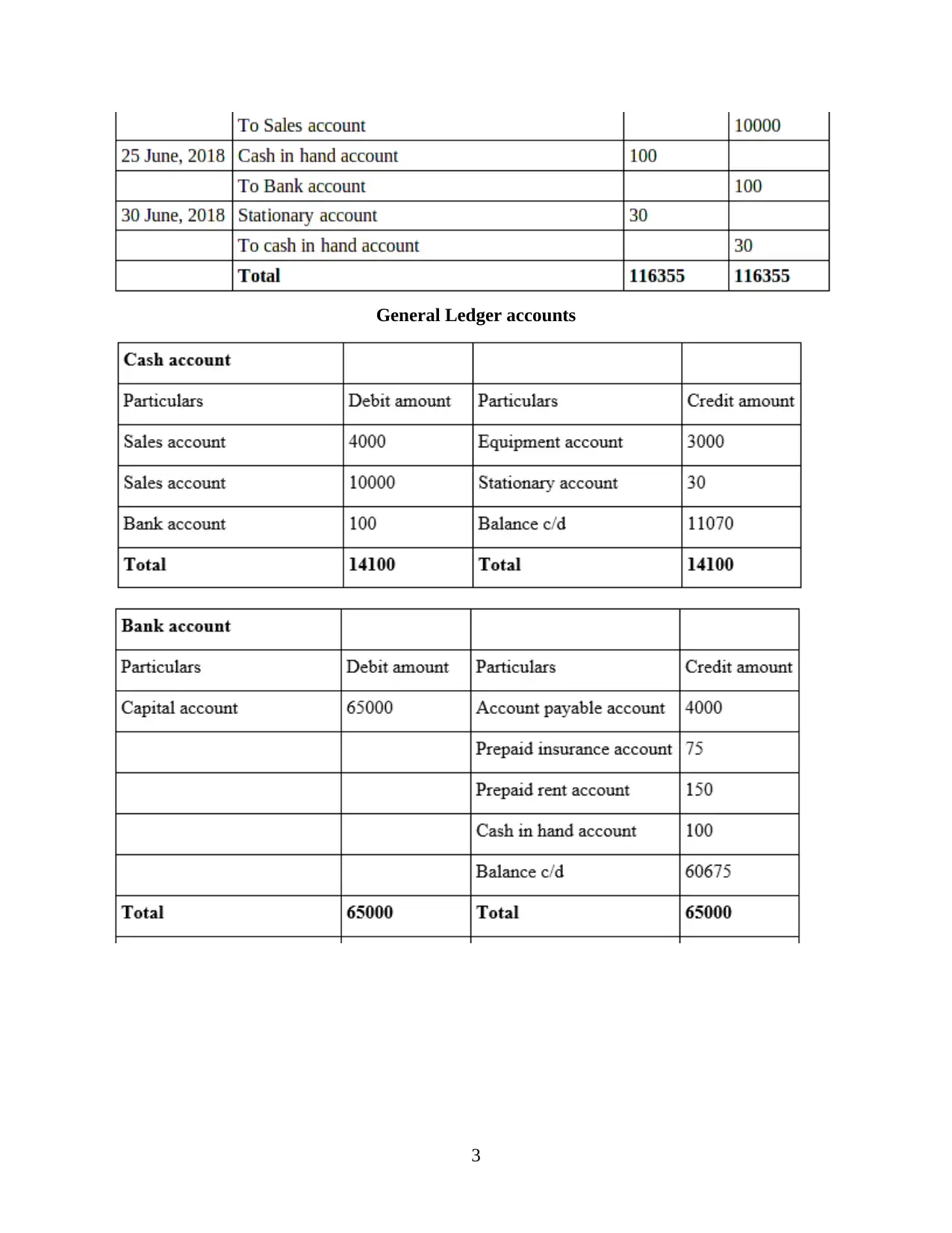

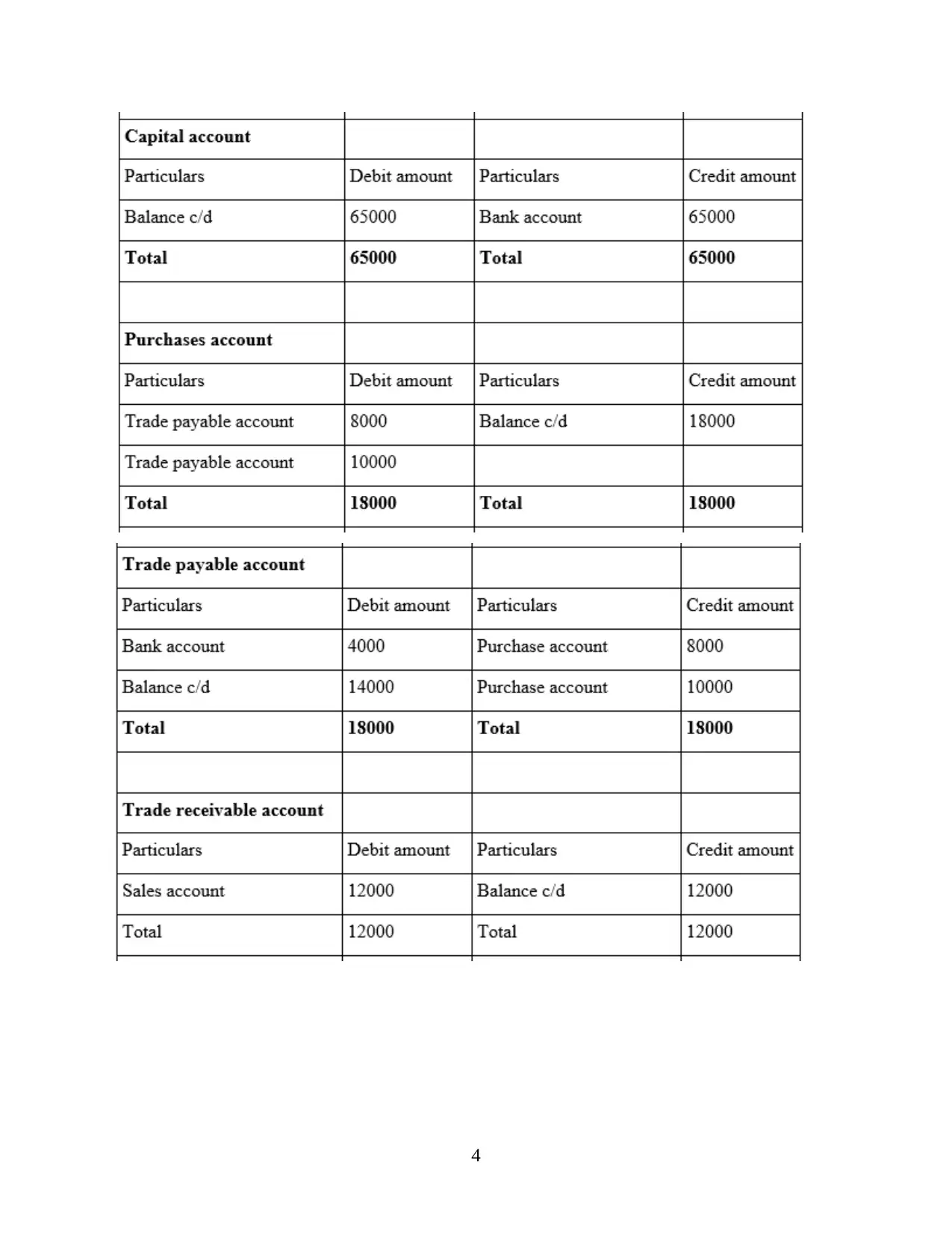

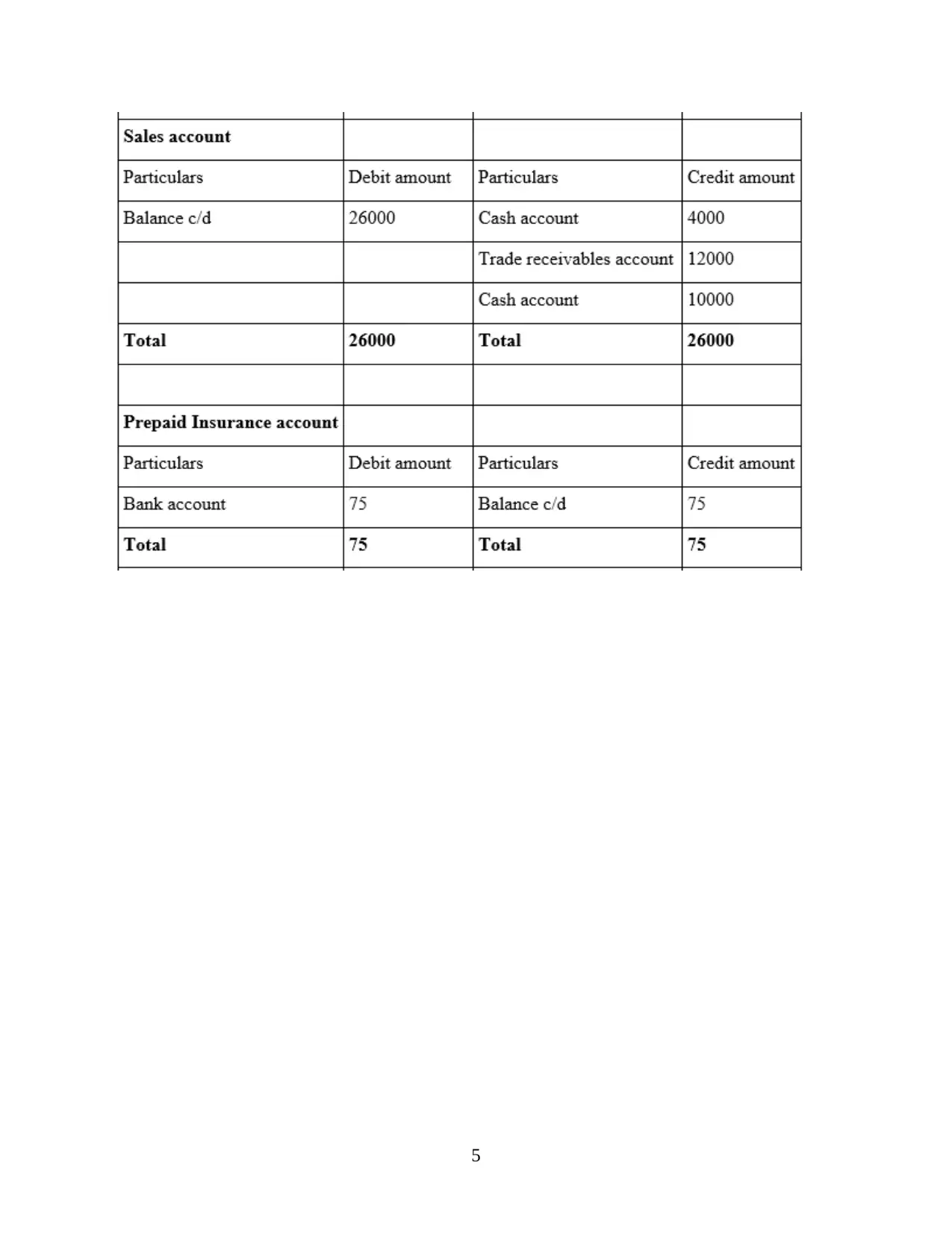

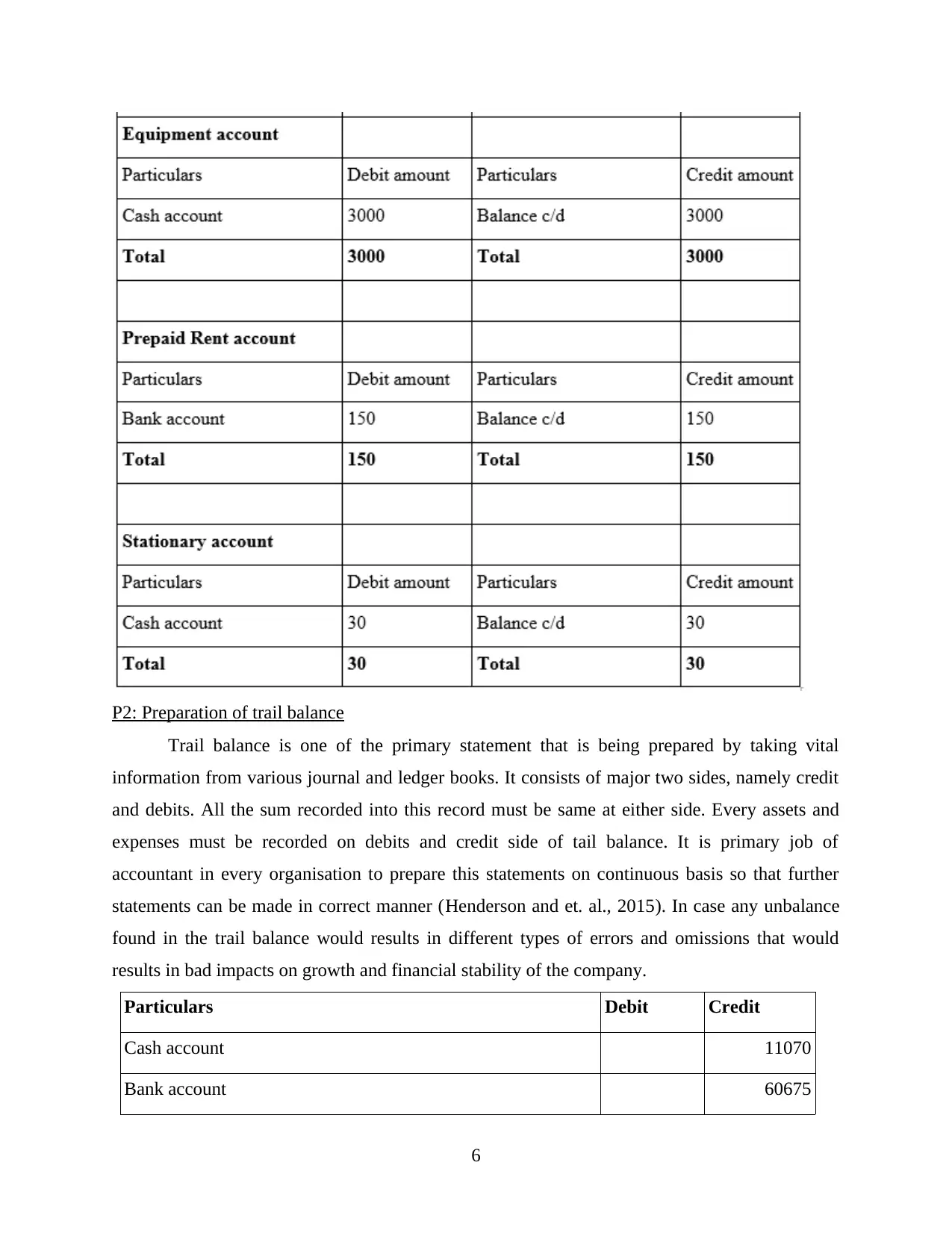

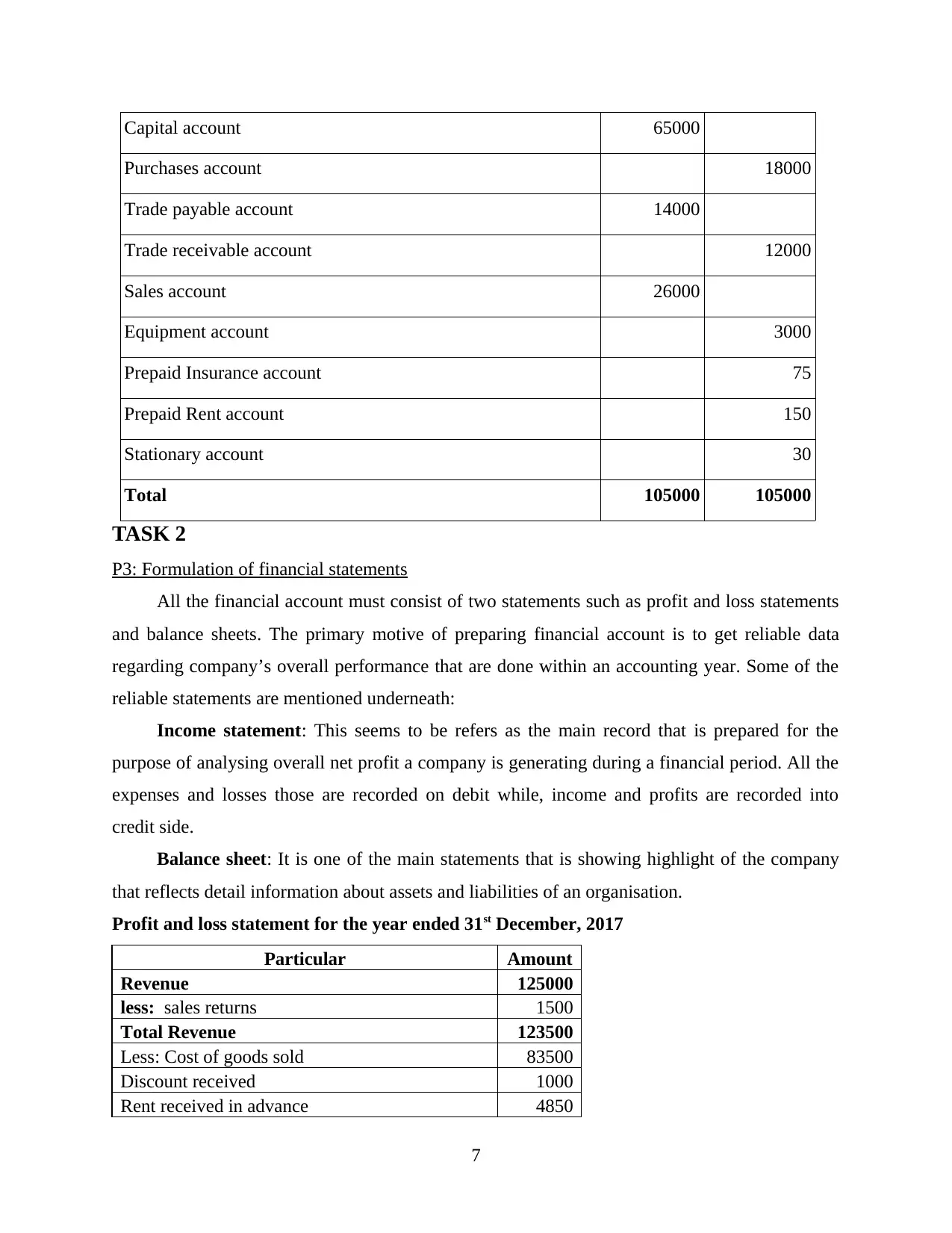

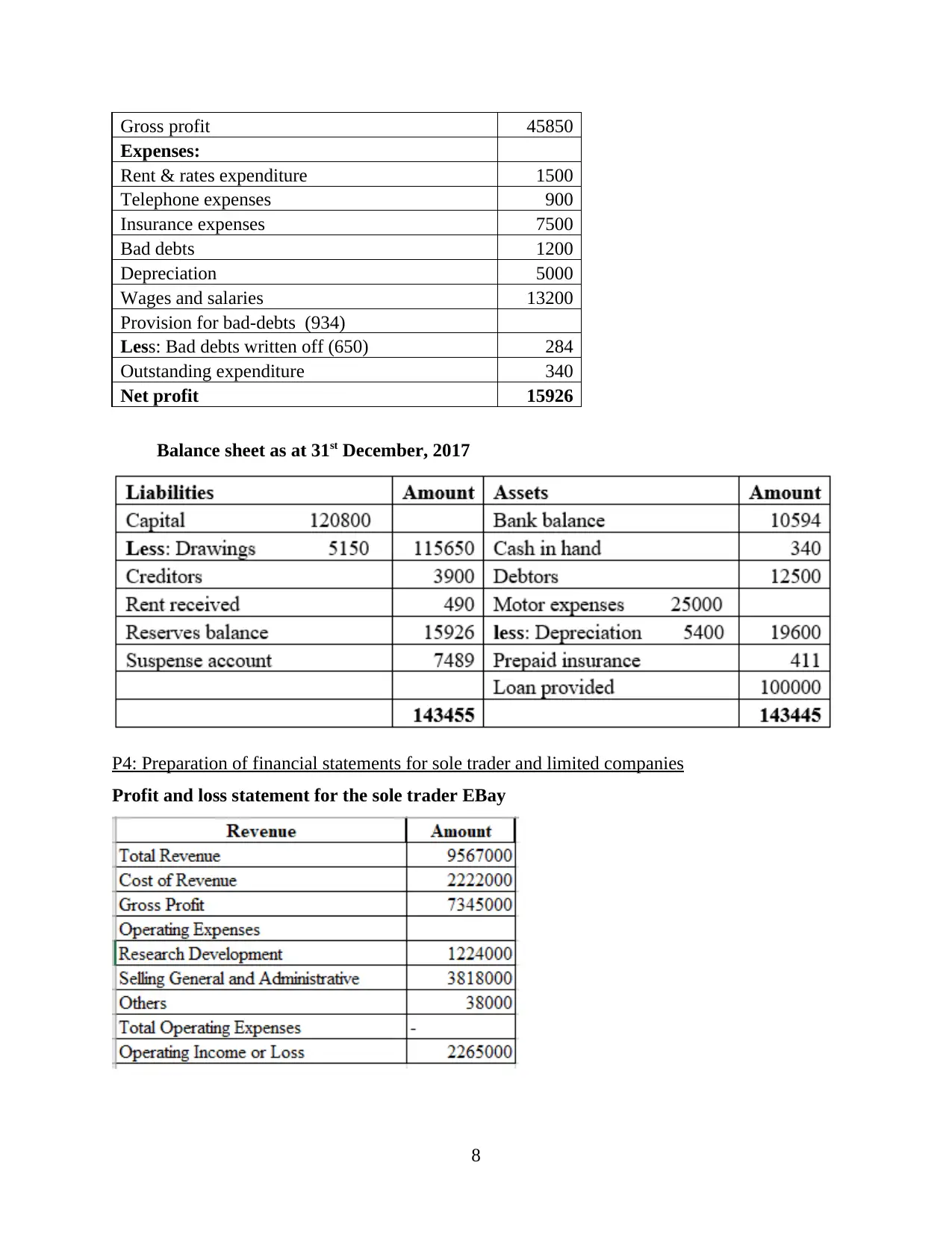

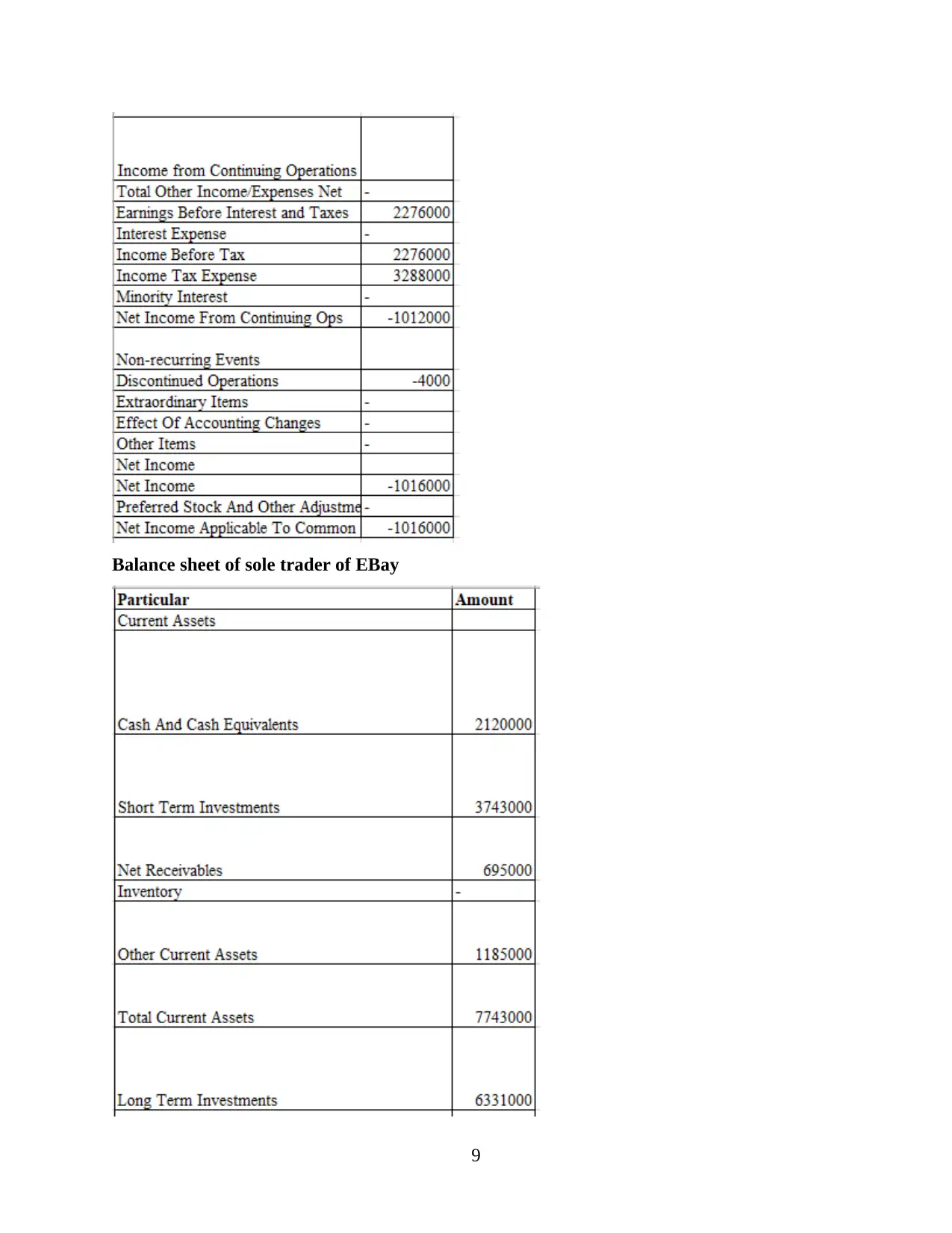

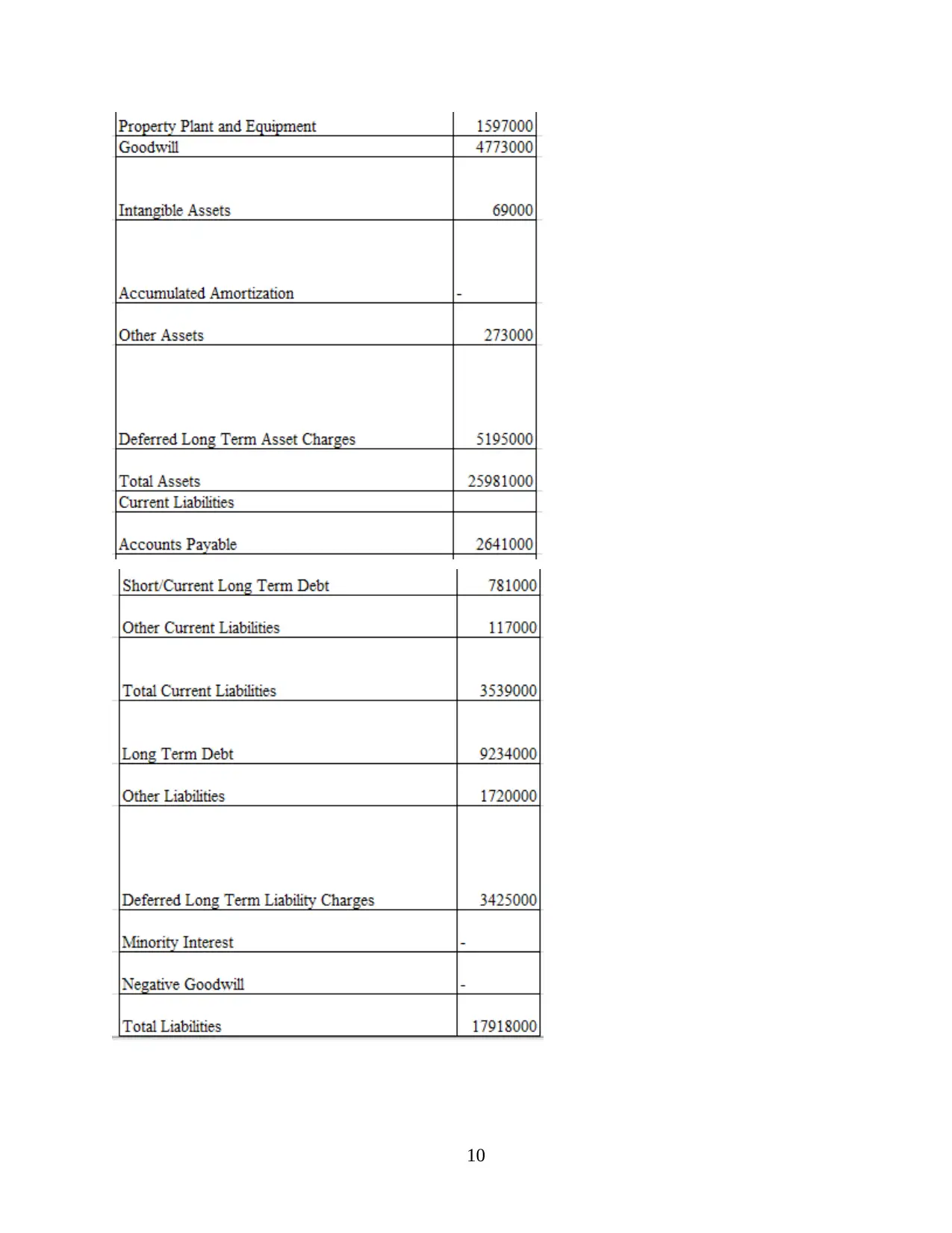

This report provides a detailed analysis of financial accounting principles and practices. It begins with an introduction to the importance of finance and financial accounting, emphasizing the use of double-entry bookkeeping systems. The report explains the process of recording transactions using debits and credits, including journal entries and the preparation of trial balances. It then moves on to the formulation of financial statements, covering both profit and loss statements and balance sheets. Furthermore, the report differentiates between the preparation of financial statements for sole traders and limited companies, offering examples and insights into each. The conclusion summarizes the key takeaways, highlighting the effectiveness of financial accounting in organizational analysis. The report is structured into two main tasks, with each task covering different aspects of financial accounting. The report provides a good understanding of the fundamental concepts of financial accounting and its practical application.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.