Financial Consolidation and Analysis: Ghostbusters Ltd. Assignment

VerifiedAdded on 2023/06/04

|5

|1448

|201

Practical Assignment

AI Summary

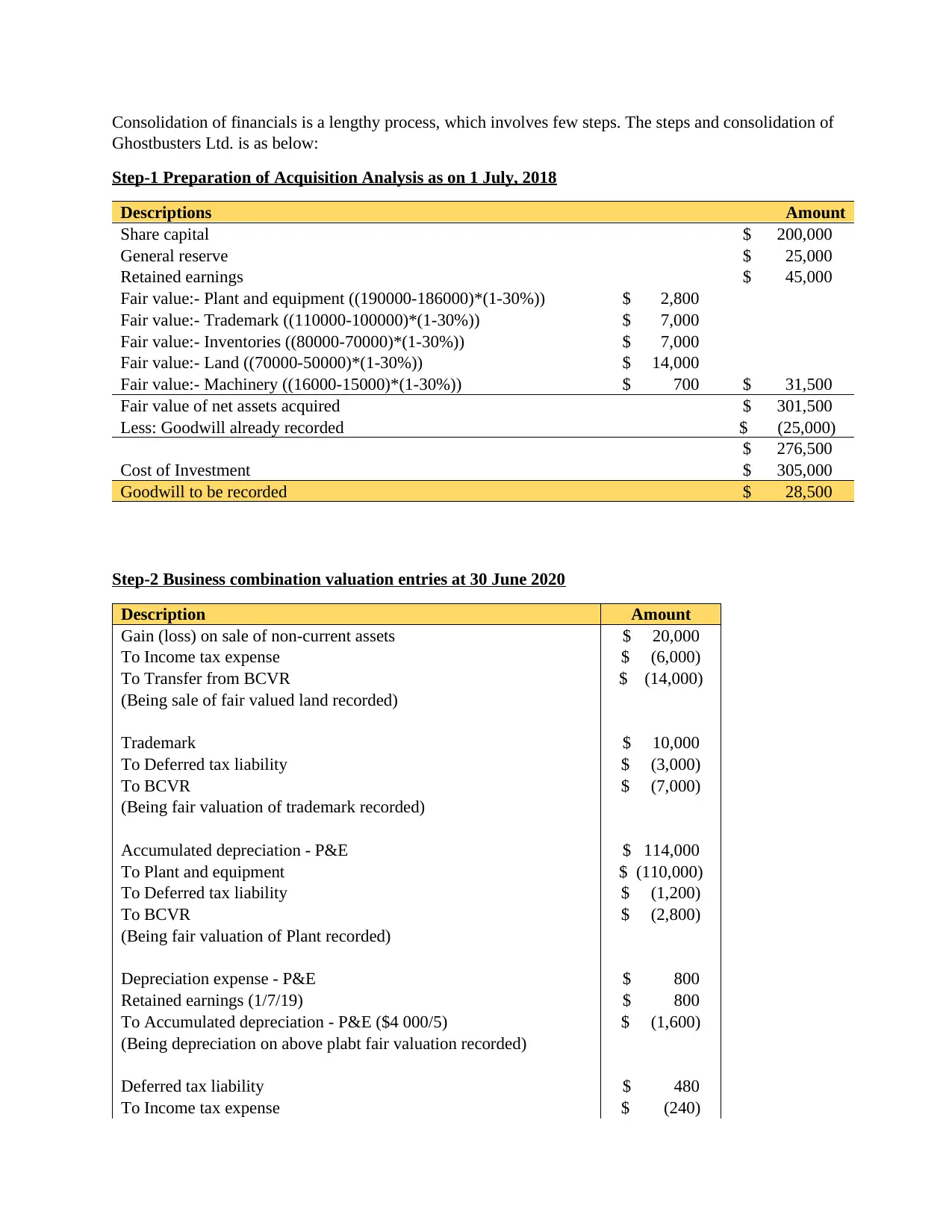

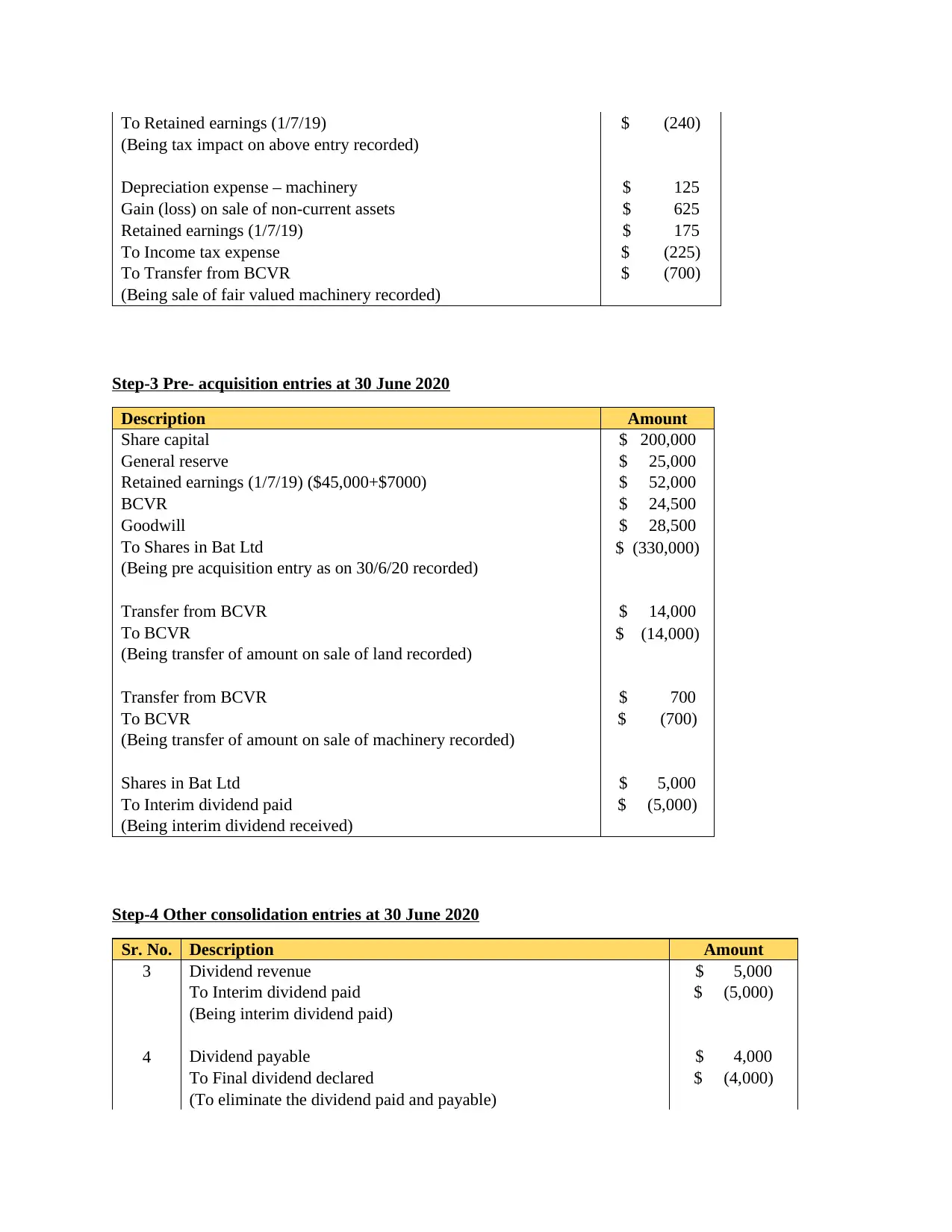

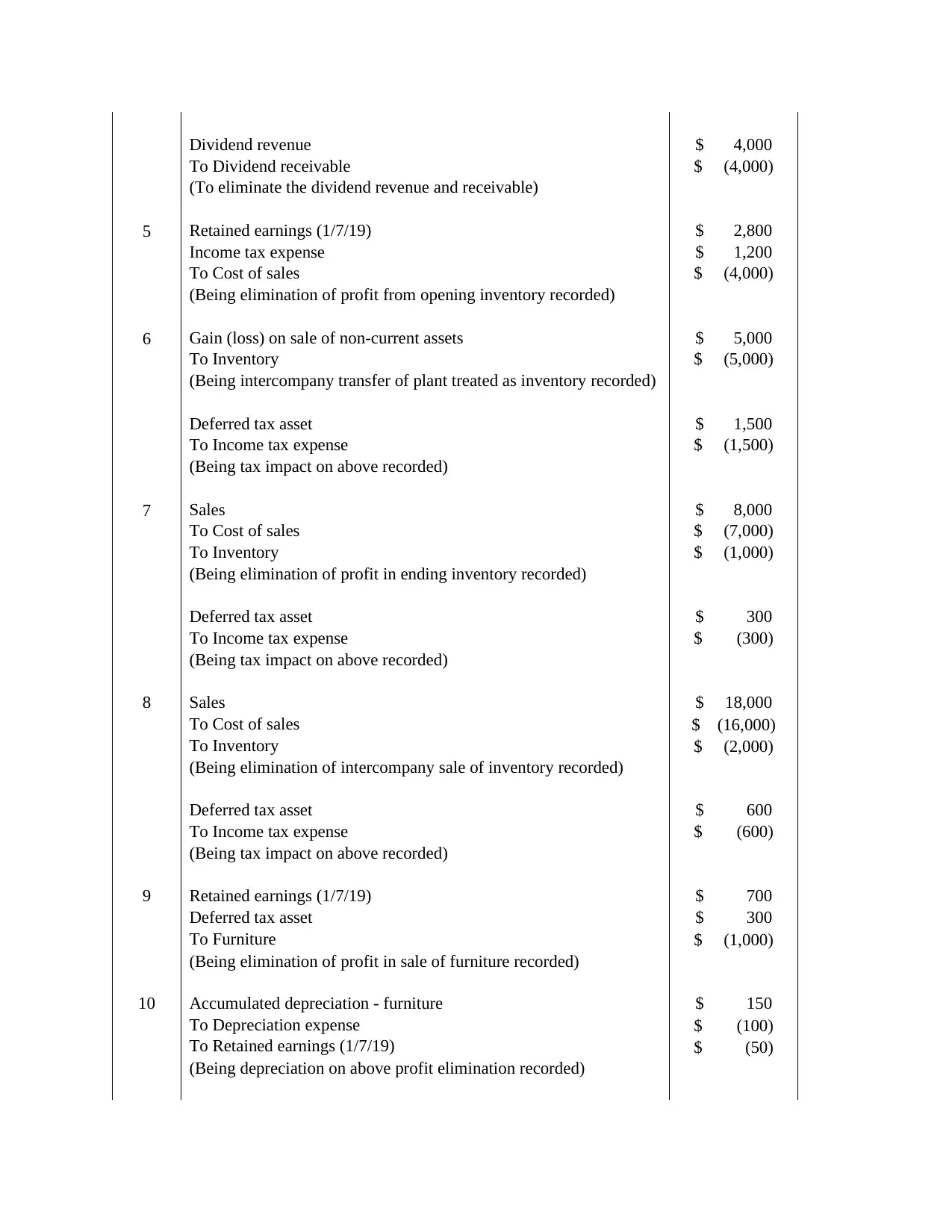

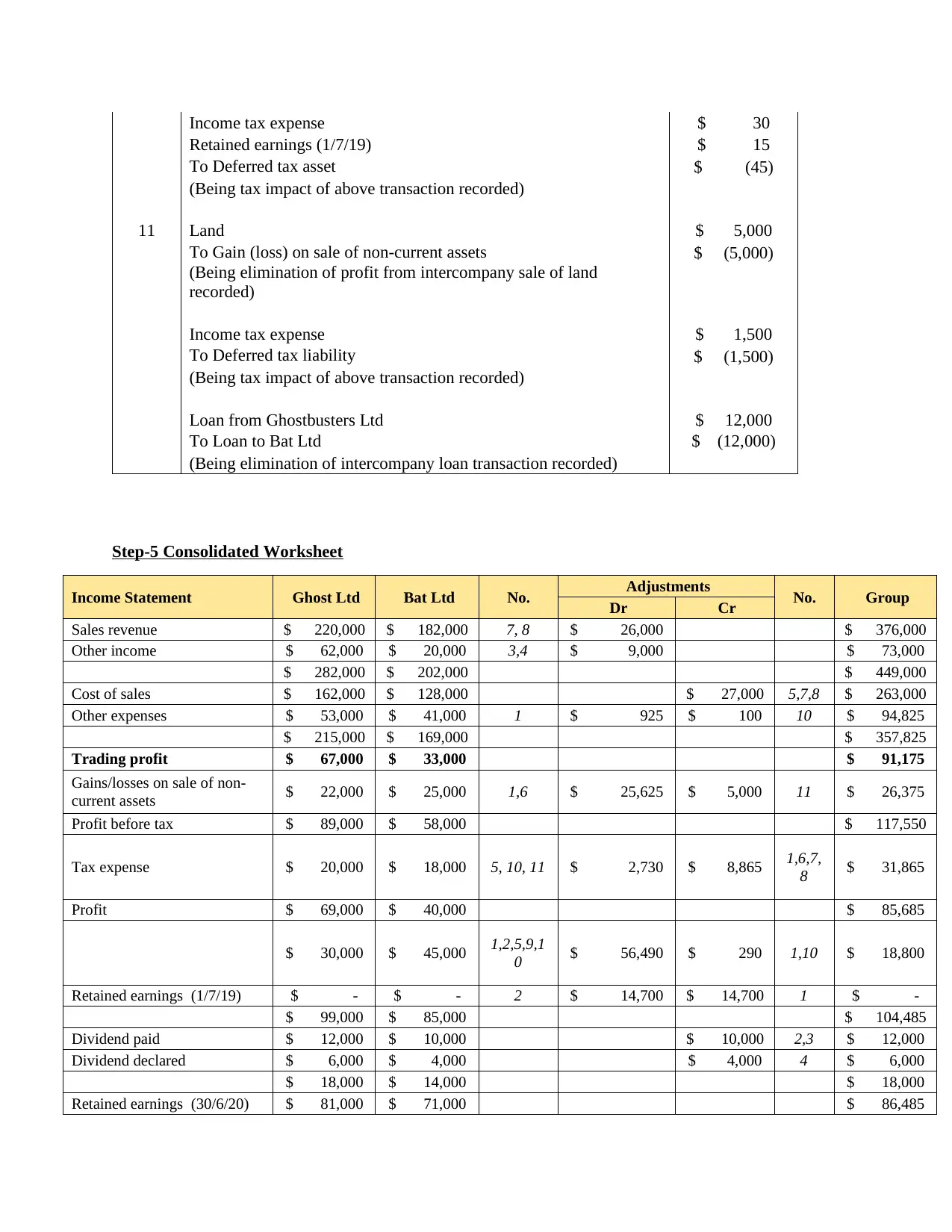

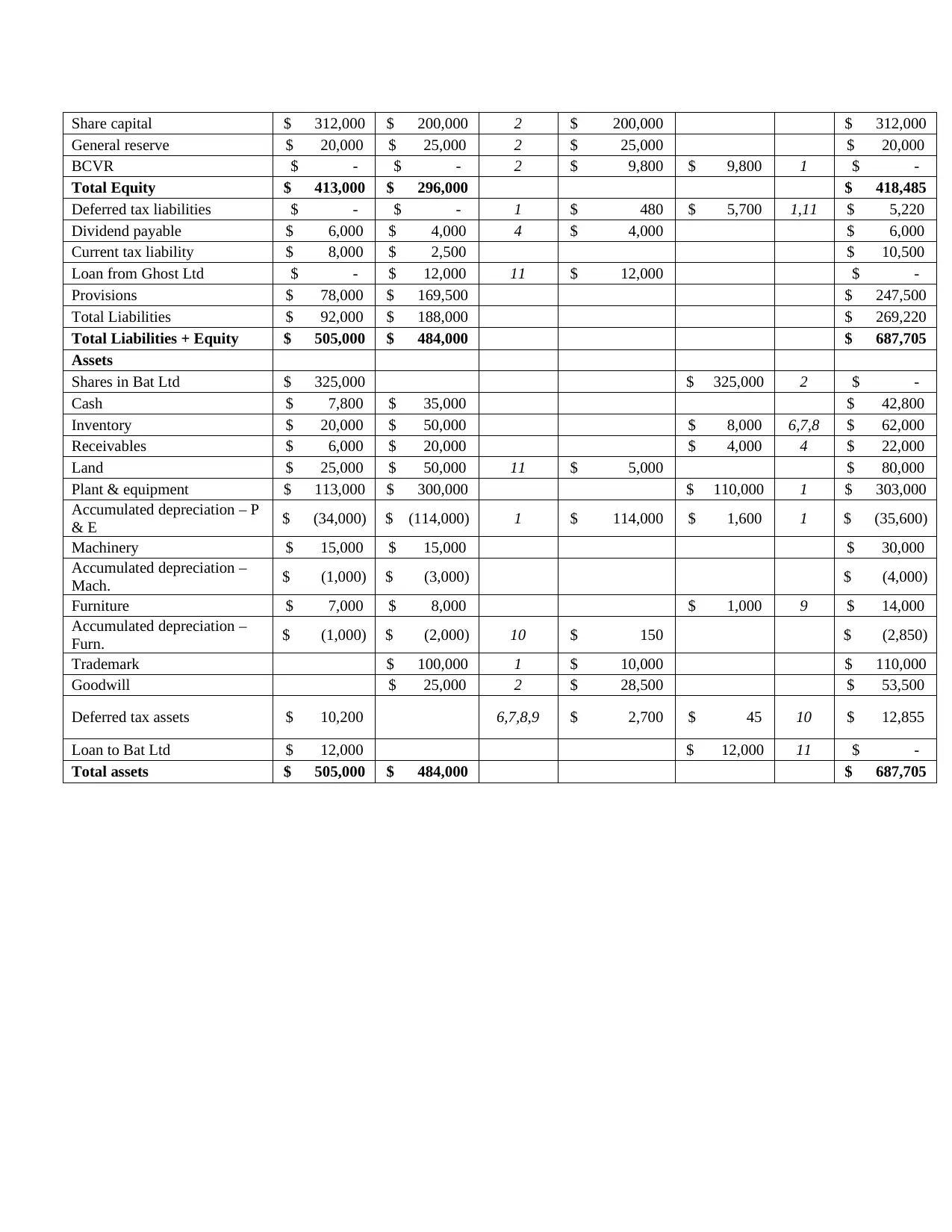

This assignment provides a comprehensive solution to a financial consolidation problem involving Ghostbusters Ltd. and its acquisition of Bat Ltd. It begins with an acquisition analysis, detailing the fair value adjustments for various assets and liabilities. The solution then presents business combination valuation entries, pre-acquisition entries, and other necessary consolidation entries to eliminate intercompany transactions and adjust for fair value differences. A consolidated worksheet is provided, summarizing the financial data for both companies and showing the adjustments needed to prepare the consolidated financial statements. The assignment covers key aspects such as goodwill calculations, depreciation adjustments, intercompany profit eliminations, and tax implications. The final section presents the consolidated financial statements, including the income statement and balance sheet, demonstrating the combined financial performance and position of Ghostbusters Ltd. and its subsidiary.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.