Accounting Report: Financial Statements, Costing Methods, and Analysis

VerifiedAdded on 2023/01/18

|23

|3349

|99

Report

AI Summary

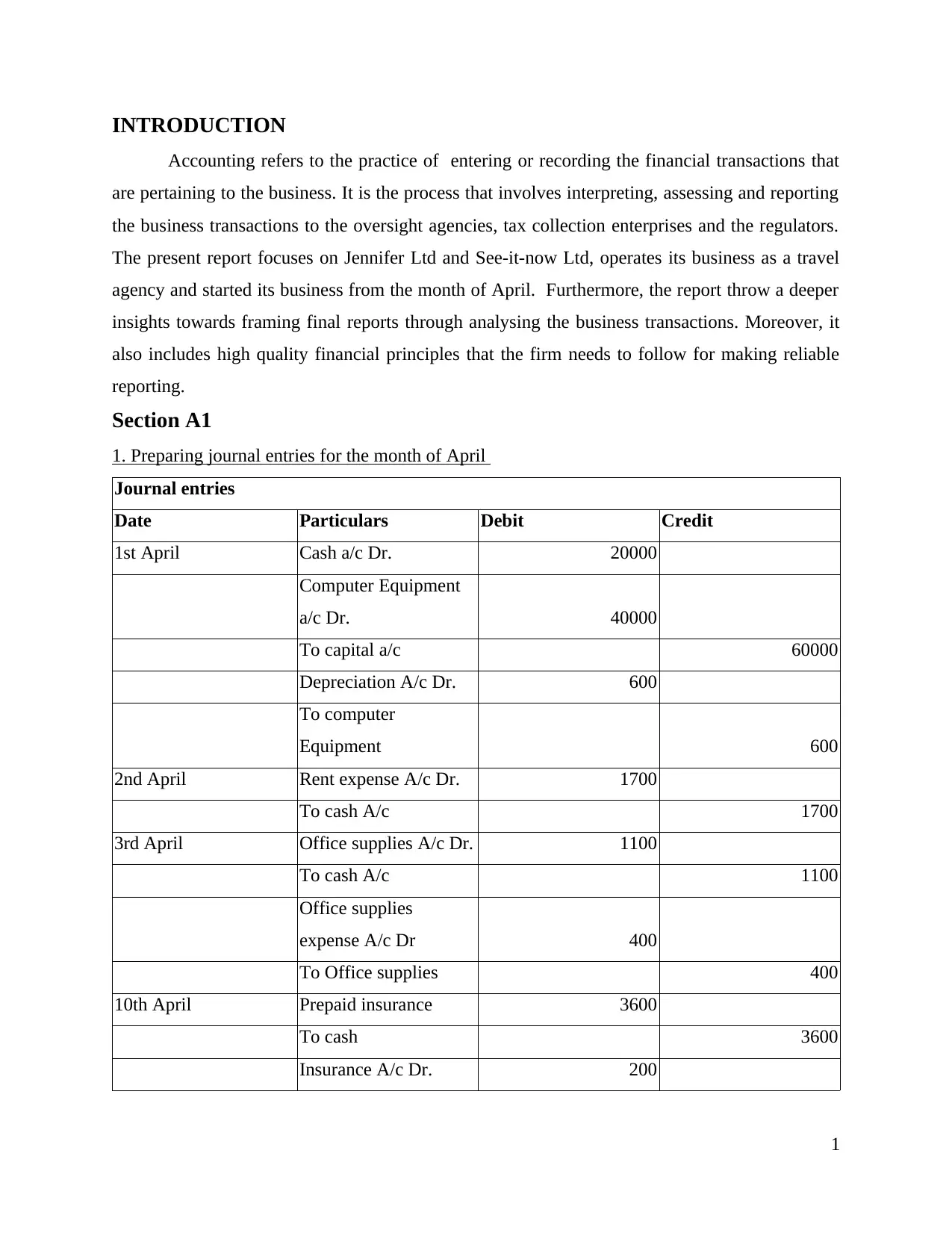

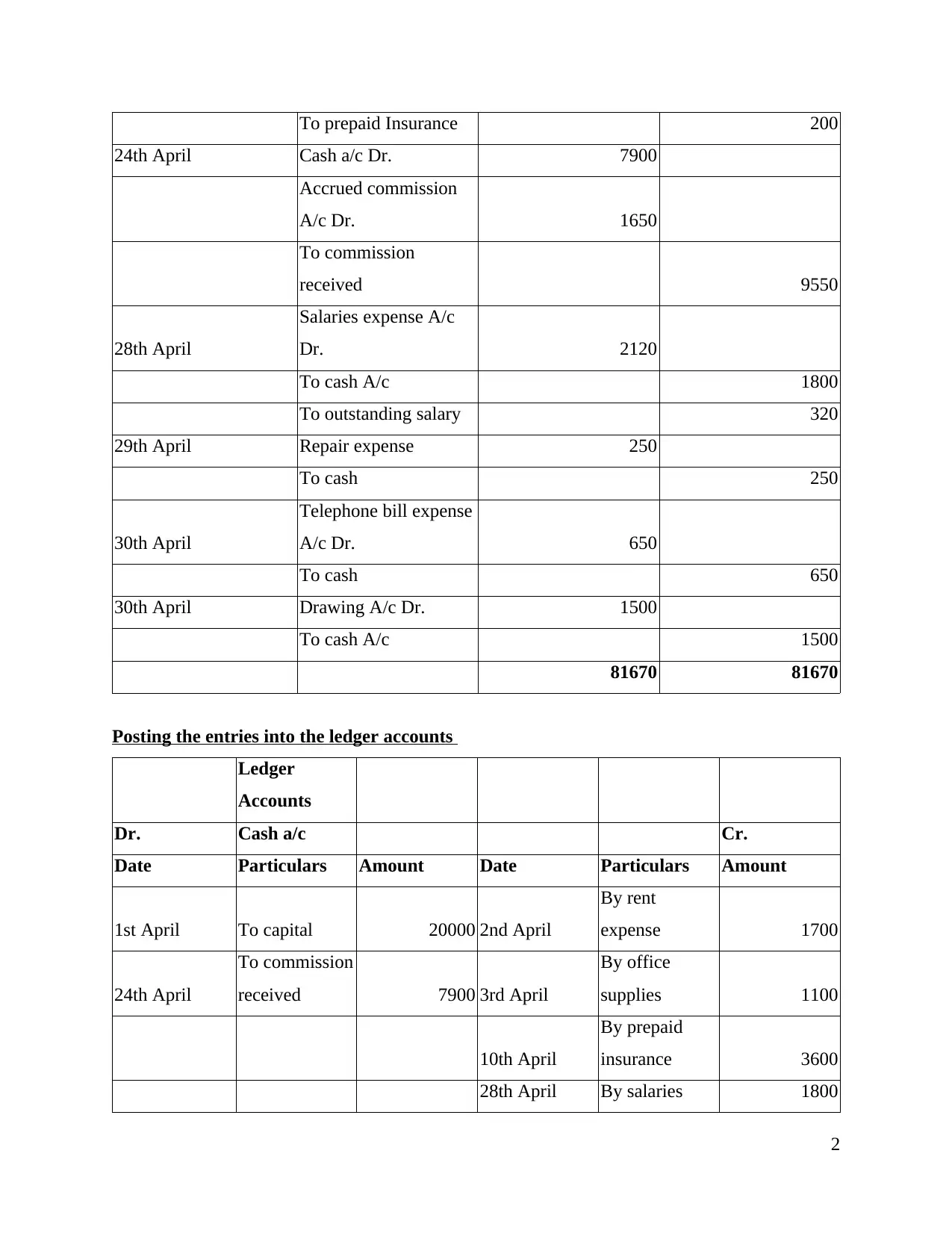

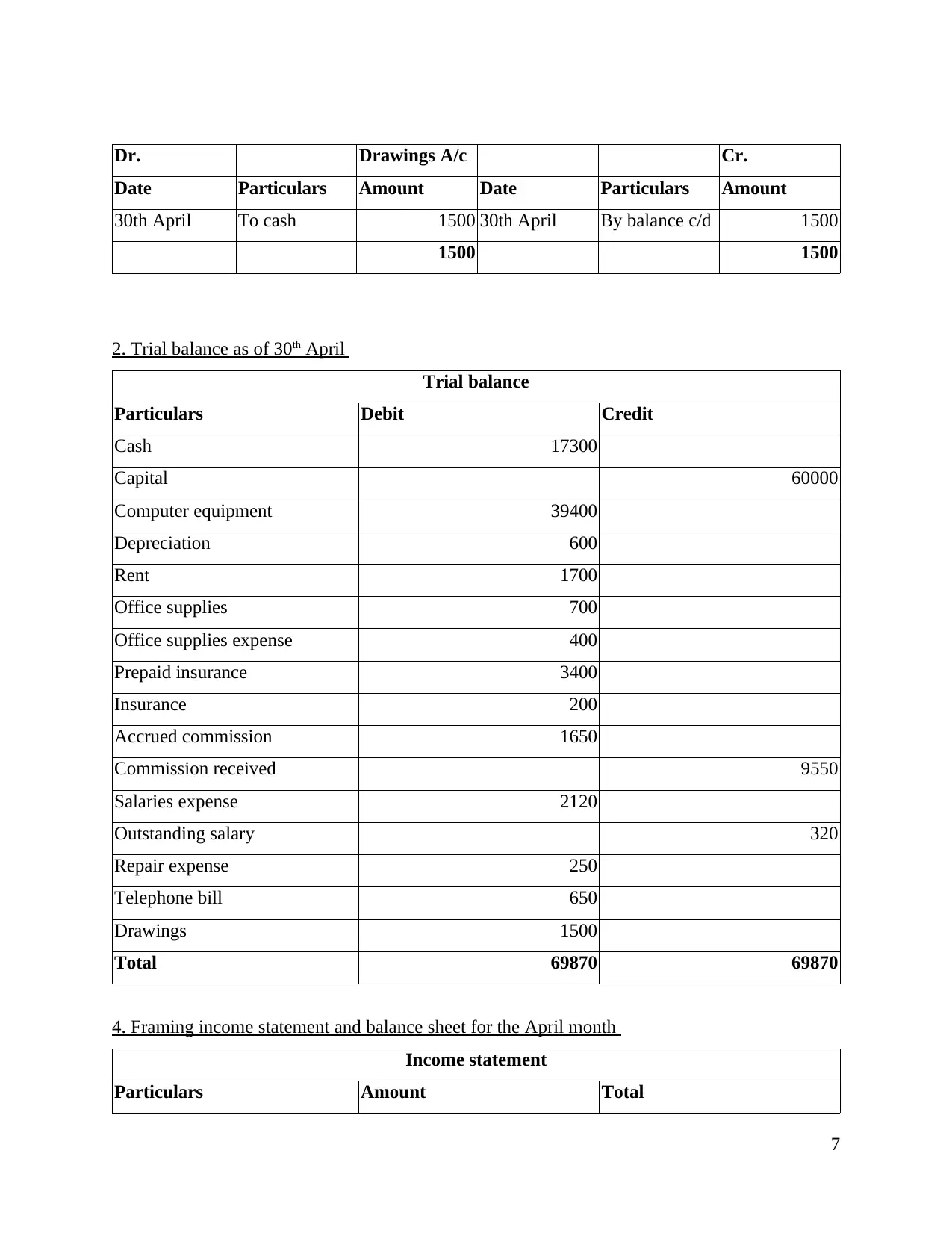

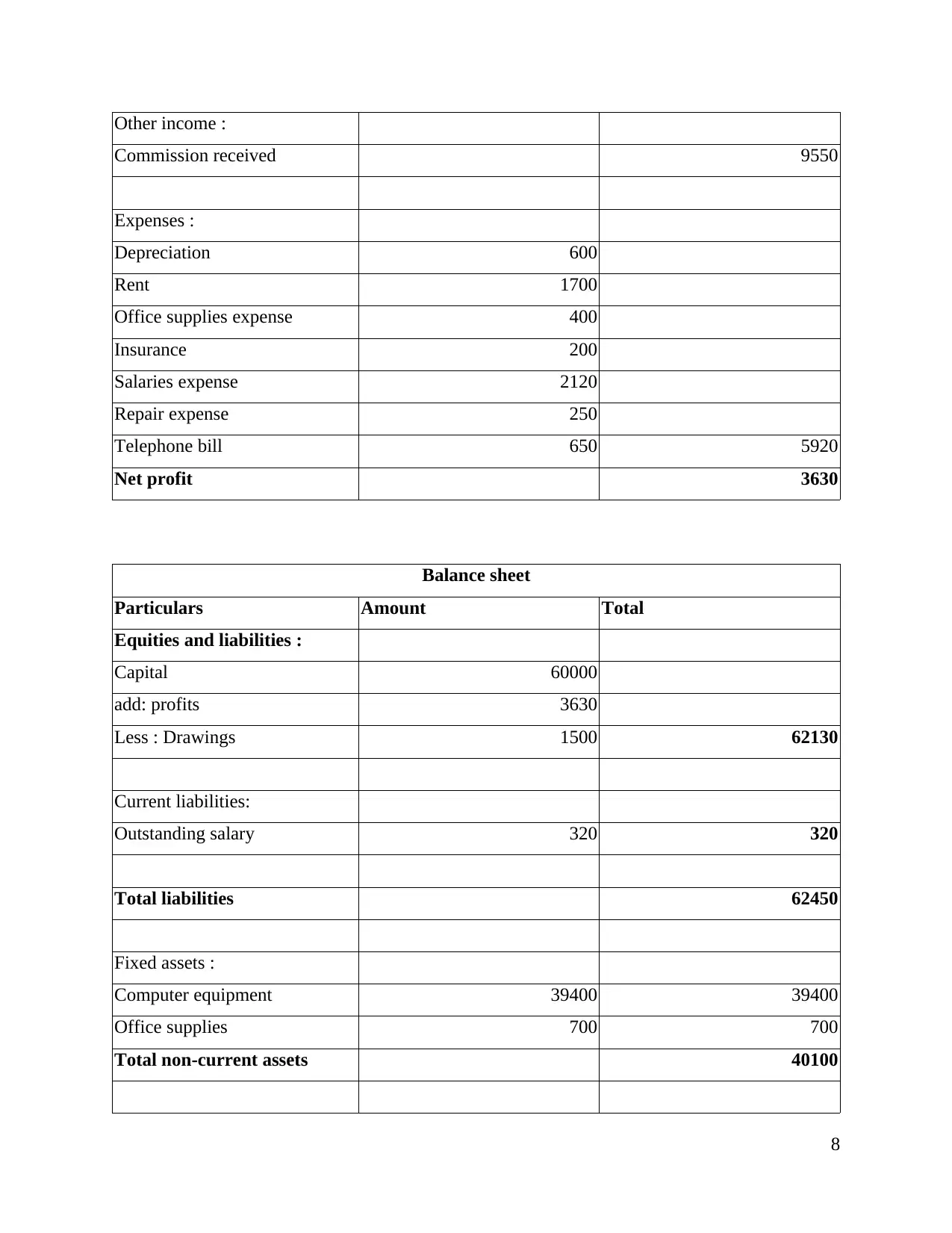

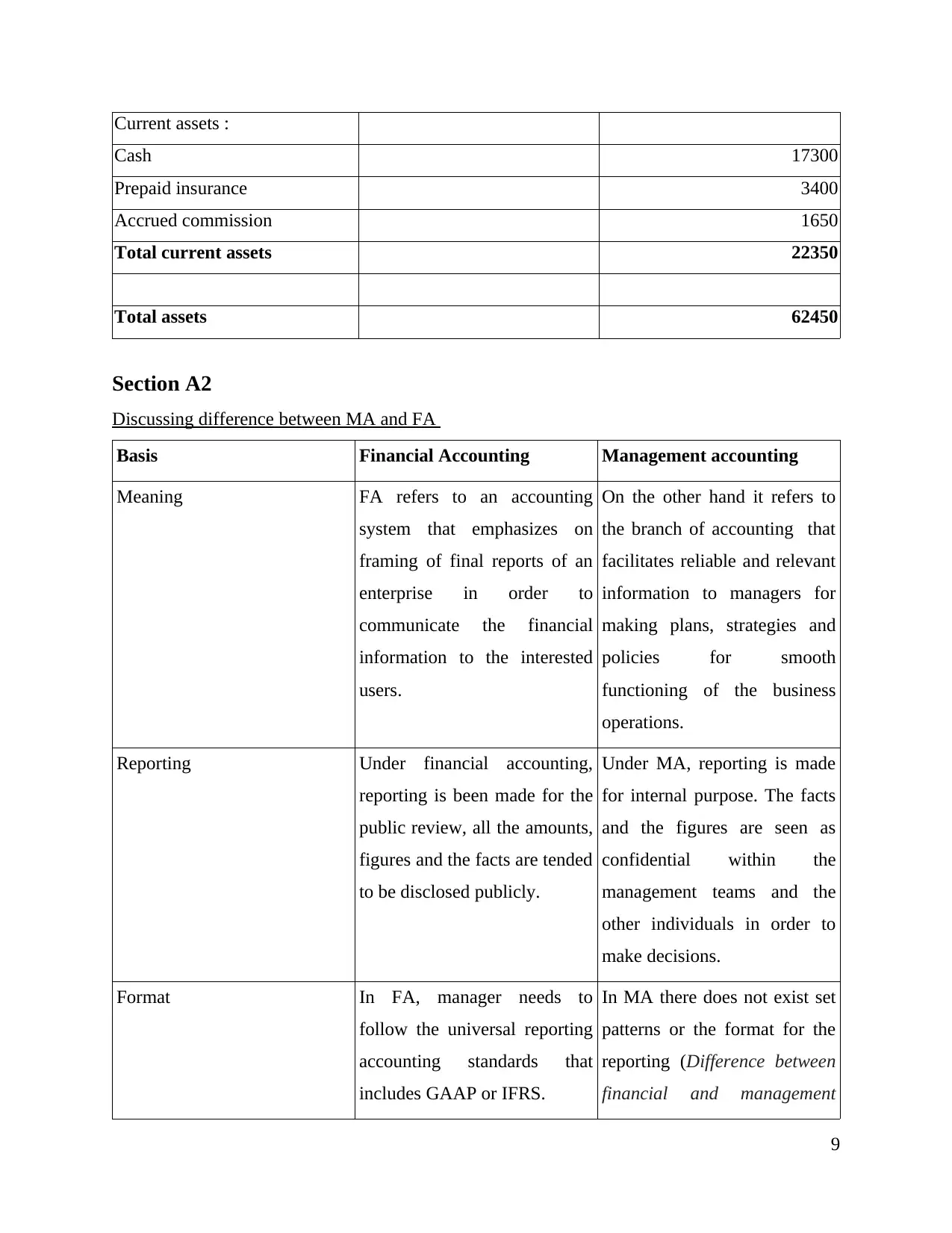

This accounting report offers a detailed examination of business transactions, including the preparation of financial statements for Jennifer Ltd and See-it-now Ltd, a travel agency. It contrasts financial and management accounting, covering journal entries, ledger accounts, trial balances, income statements, and balance sheets. The report computes product costs and net profits using marginal and absorption costing methods, analyzing their differences. Furthermore, it explores high-quality financial information principles, emphasizing relevance, reliability, understandability, comparability, consistency, neutrality, and materiality to ensure accurate and reliable financial reporting. The report also discusses the features of high-quality financial information to both the company's management.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.