Management Accounting Report: Financial Statement Analysis, Costing

VerifiedAdded on 2023/01/06

|19

|3881

|37

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on cost calculation, financial statement preparation, and interpretation, using Prime Furniture Limited as a case study. It covers marginal and absorption costing methods, exploring their application in financial reporting and analysis. The report further examines budgetary control, including operational, cash, and capital budgets, along with their benefits and limitations. It also delves into pricing strategies, supply-demand dynamics, and strategic planning using SWOT analysis. Furthermore, the report analyzes how management accounting methods help organizations respond to financial problems and achieve sustainable success, emphasizing the importance of financial planning and management accounting systems in overcoming financial challenges. The report concludes with a discussion of the key findings and their implications for effective financial management.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

MAIN BODY..................................................................................................................................................3

TASK 2......................................................................................................................................................3

P3. Calculation of costs and preparation of financial statements under marginal and absorption

costing method........................................................................................................................................3

M2. Accounting techniques to produce financial statements.................................................................5

D2. Interpretation of prepared financial statements...............................................................................6

TASK 3......................................................................................................................................................6

P4. Limitations and benefits of planning tools of budgetary control.......................................................6

M3. Use of different planning tools and their application for preparing and forecasting budgets........10

TASK 4....................................................................................................................................................10

P5. Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success...........................................................................10

M4. MAS to solve financial issue...........................................................................................................12

D3. Importance of financial plans for planning and managing monetary sources which can contribute

in overcoming problems regards to finance..........................................................................................13

CONCLUSION.............................................................................................................................................13

REFERENCES..............................................................................................................................................14

INTRODUCTION...........................................................................................................................................3

MAIN BODY..................................................................................................................................................3

TASK 2......................................................................................................................................................3

P3. Calculation of costs and preparation of financial statements under marginal and absorption

costing method........................................................................................................................................3

M2. Accounting techniques to produce financial statements.................................................................5

D2. Interpretation of prepared financial statements...............................................................................6

TASK 3......................................................................................................................................................6

P4. Limitations and benefits of planning tools of budgetary control.......................................................6

M3. Use of different planning tools and their application for preparing and forecasting budgets........10

TASK 4....................................................................................................................................................10

P5. Analysis of ways in which management accounting methods help organisation to respond to

financial problems that will have sustainable success...........................................................................10

M4. MAS to solve financial issue...........................................................................................................12

D3. Importance of financial plans for planning and managing monetary sources which can contribute

in overcoming problems regards to finance..........................................................................................13

CONCLUSION.............................................................................................................................................13

REFERENCES..............................................................................................................................................14

INTRODUCTION

The word MA is described as a means of establishing internal reporting with aid of monetary and

non - monetary details (Alsharari, 2019). There are a broad variety of strategies such as

absorption, marginal in which to render financial reports. This form of accounting is too crucial

for each type of business sectors because under it detailed information about internal reports is

offered and each of them contains financial & non financial information. Such information acts

as a key tool for making decisions in an effective manner. This is so because such accounting

information acts as a framework for taking judgments. Prime furniture limited is the firm chosen

for this project. It involves in manufacturing of different types of furniture items. The document

provides detailed information on different accounting methods, corporate accounting preparation

tools and management processes to address financial problems.

MAIN BODY

TASK 2

P3. Calculation of costs and preparation of financial statements under marginal and absorption

costing method.

Micro economic techniques:

Cost- This can be described as the overall cost of undertaking various forms of development and

operations. Various categories of costs occur, including fixed costs, contingent costs, actual

expenses, indirect costs, and many others.

Cost volume analysis- The cost-benefit planning is a significant method to the weakening

framework and attributes of options that are used to assess the optimal way to achieve gains

while preserving costs (Cescon, and Grassetti,

Taschner and Charifzadeh, 2020).

Cost variance- This can be described as the estimation method for the disparity between real and

expected costs. It is viewed in unfavorable and positive ways.

The word MA is described as a means of establishing internal reporting with aid of monetary and

non - monetary details (Alsharari, 2019). There are a broad variety of strategies such as

absorption, marginal in which to render financial reports. This form of accounting is too crucial

for each type of business sectors because under it detailed information about internal reports is

offered and each of them contains financial & non financial information. Such information acts

as a key tool for making decisions in an effective manner. This is so because such accounting

information acts as a framework for taking judgments. Prime furniture limited is the firm chosen

for this project. It involves in manufacturing of different types of furniture items. The document

provides detailed information on different accounting methods, corporate accounting preparation

tools and management processes to address financial problems.

MAIN BODY

TASK 2

P3. Calculation of costs and preparation of financial statements under marginal and absorption

costing method.

Micro economic techniques:

Cost- This can be described as the overall cost of undertaking various forms of development and

operations. Various categories of costs occur, including fixed costs, contingent costs, actual

expenses, indirect costs, and many others.

Cost volume analysis- The cost-benefit planning is a significant method to the weakening

framework and attributes of options that are used to assess the optimal way to achieve gains

while preserving costs (Cescon, and Grassetti,

Taschner and Charifzadeh, 2020).

Cost variance- This can be described as the estimation method for the disparity between real and

expected costs. It is viewed in unfavorable and positive ways.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the context of planning financial accounts, there are a variety of important techniques such as

absorption and marginal strategies. They can be used for writing business financial reports. In the

following description, these are defined as follows:

Absorption costing method- This is a method of costing methodology which specifies and

generally allocates the costs of different activities. Under it item's costs shall be done as

fixed and unfixed costs.

Marginal costing method- The costs involved in multiple operations can be interpreted as

a way to classify them. The fixed costs are called the cost of time and the cost of the

products varies.

Product costing:

Fixed cost- It is a kind of expense not influenced or adjusted by the change in the volume

of output.

Variable cost- It is a form of expense which can be modified or influenced by changes in

the amount of output.

Standard costing- Standard costing incorporates planned expenses with real costs in

financial reports. The adjustments between the expected costs and the real costs are then

reported as shown.

Activity based costing- The activity costing approach determines the operating functions

of each process and measures the cost relative to the practical usage of the product and

the facility for each process (Aureli, Cardoni and Lombardi, 2019). This method

attributes indirect costs more direct than conventional costs. In the context of prime

limited company, such costing technique is used in order to assess day to day activities

and cost related to each. By this method, it becomes easier for managers to know which

kind of activity is leading to higher amount of cost.

Role of costing in setting prices- Costing plays a significant role in price regulation when

firms adjust rates on the basis of it. That's because if the costs are greater than anticipated

than the values fixed by businesses, vice versa.

absorption and marginal strategies. They can be used for writing business financial reports. In the

following description, these are defined as follows:

Absorption costing method- This is a method of costing methodology which specifies and

generally allocates the costs of different activities. Under it item's costs shall be done as

fixed and unfixed costs.

Marginal costing method- The costs involved in multiple operations can be interpreted as

a way to classify them. The fixed costs are called the cost of time and the cost of the

products varies.

Product costing:

Fixed cost- It is a kind of expense not influenced or adjusted by the change in the volume

of output.

Variable cost- It is a form of expense which can be modified or influenced by changes in

the amount of output.

Standard costing- Standard costing incorporates planned expenses with real costs in

financial reports. The adjustments between the expected costs and the real costs are then

reported as shown.

Activity based costing- The activity costing approach determines the operating functions

of each process and measures the cost relative to the practical usage of the product and

the facility for each process (Aureli, Cardoni and Lombardi, 2019). This method

attributes indirect costs more direct than conventional costs. In the context of prime

limited company, such costing technique is used in order to assess day to day activities

and cost related to each. By this method, it becomes easier for managers to know which

kind of activity is leading to higher amount of cost.

Role of costing in setting prices- Costing plays a significant role in price regulation when

firms adjust rates on the basis of it. That's because if the costs are greater than anticipated

than the values fixed by businesses, vice versa.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of inventory:

Inventory cost- Costs in inventory are purchase costs, distribution costs and increased

cost control. Various forms of manufacturing expenses are defined as follows:

Ordering cost

Carrying cost

Purchasing cost

Hiring cost

Valuation methods:

First in first out method- This approach is correlated with the inventory in the factories

for manufacturing first of goods that comes first. In relation to Prime limited company,

they use such method to manage their available amount of stock in an effective manner.

They deal with those stock which comes first in the store.

Last in first out method- This is a process which is related to the last stock in factories for

output. In the context of above Prime furniture limited, they use such accounting system

to manage those stock which comes last in warehouses and used on a priority basis.

Weighted average costing method- The weighted average accounting value methodology

is one of three approaches to measure the business inventory that measures the overall

expenditure of a commodity component based on the output of-item, relative to their

number. To evaluate the amount and value of the products being made, businesses use the

weighted average.

Calculations:

Inventory cost- Costs in inventory are purchase costs, distribution costs and increased

cost control. Various forms of manufacturing expenses are defined as follows:

Ordering cost

Carrying cost

Purchasing cost

Hiring cost

Valuation methods:

First in first out method- This approach is correlated with the inventory in the factories

for manufacturing first of goods that comes first. In relation to Prime limited company,

they use such method to manage their available amount of stock in an effective manner.

They deal with those stock which comes first in the store.

Last in first out method- This is a process which is related to the last stock in factories for

output. In the context of above Prime furniture limited, they use such accounting system

to manage those stock which comes last in warehouses and used on a priority basis.

Weighted average costing method- The weighted average accounting value methodology

is one of three approaches to measure the business inventory that measures the overall

expenditure of a commodity component based on the output of-item, relative to their

number. To evaluate the amount and value of the products being made, businesses use the

weighted average.

Calculations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal costing method:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2. Accounting techniques to produce financial statements.

In the corporate finance sector, most revenue reports are organized through absorption and

marginal costing structures. As with Prime furniture, income is reported by absorption and

incremental costing approaches (Ferdous, Adams and Boyce, 2019). The pluralities of

approaches, with the exception of these, include planning of financial reports such as a

traditional cost scheme, costing events, etc. In relation to standard costing, the calculation of

potential costs used for comparison will be seen as being related. Operational expense is

dispersed and assessed for different types of operation by growing activity.

D2. Interpretation of prepared financial statements.

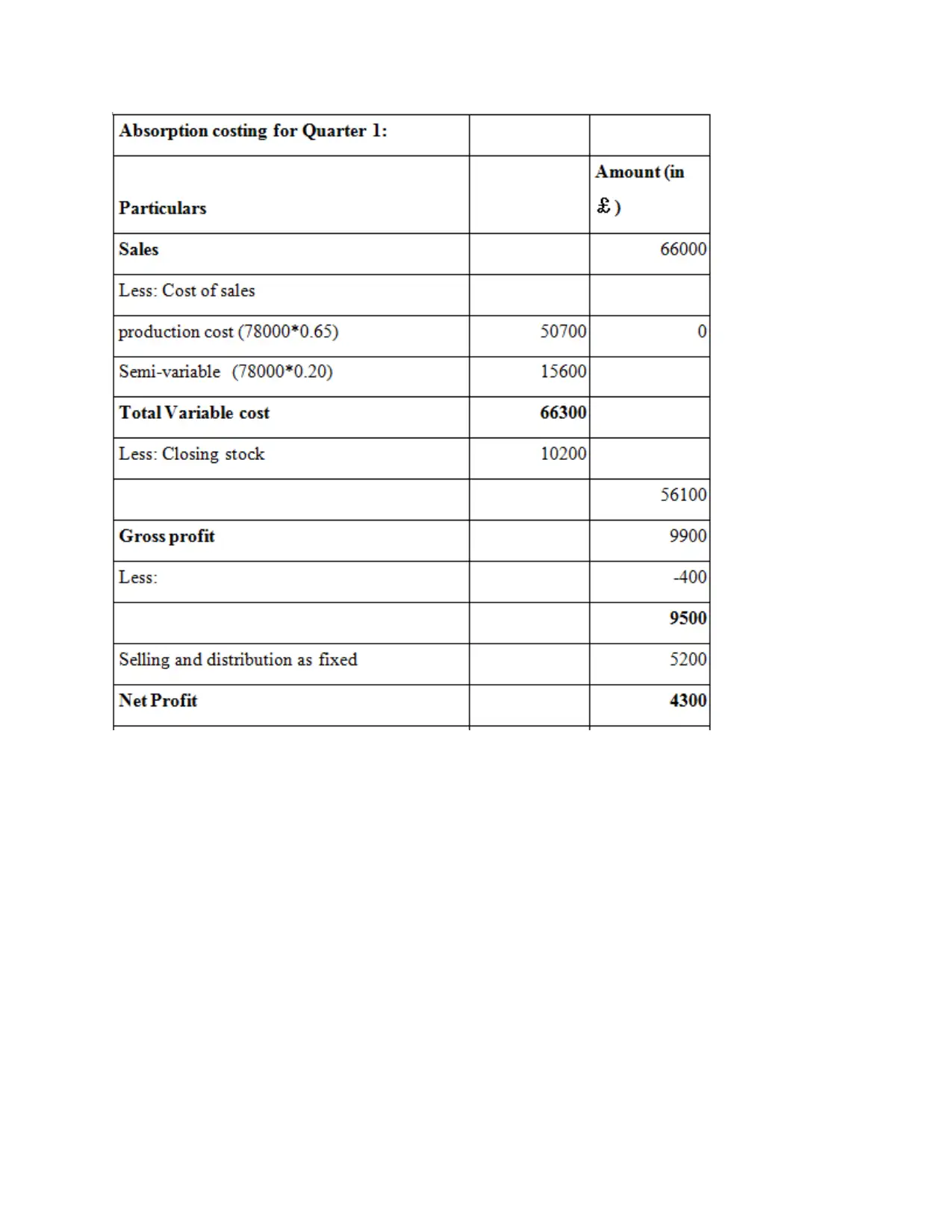

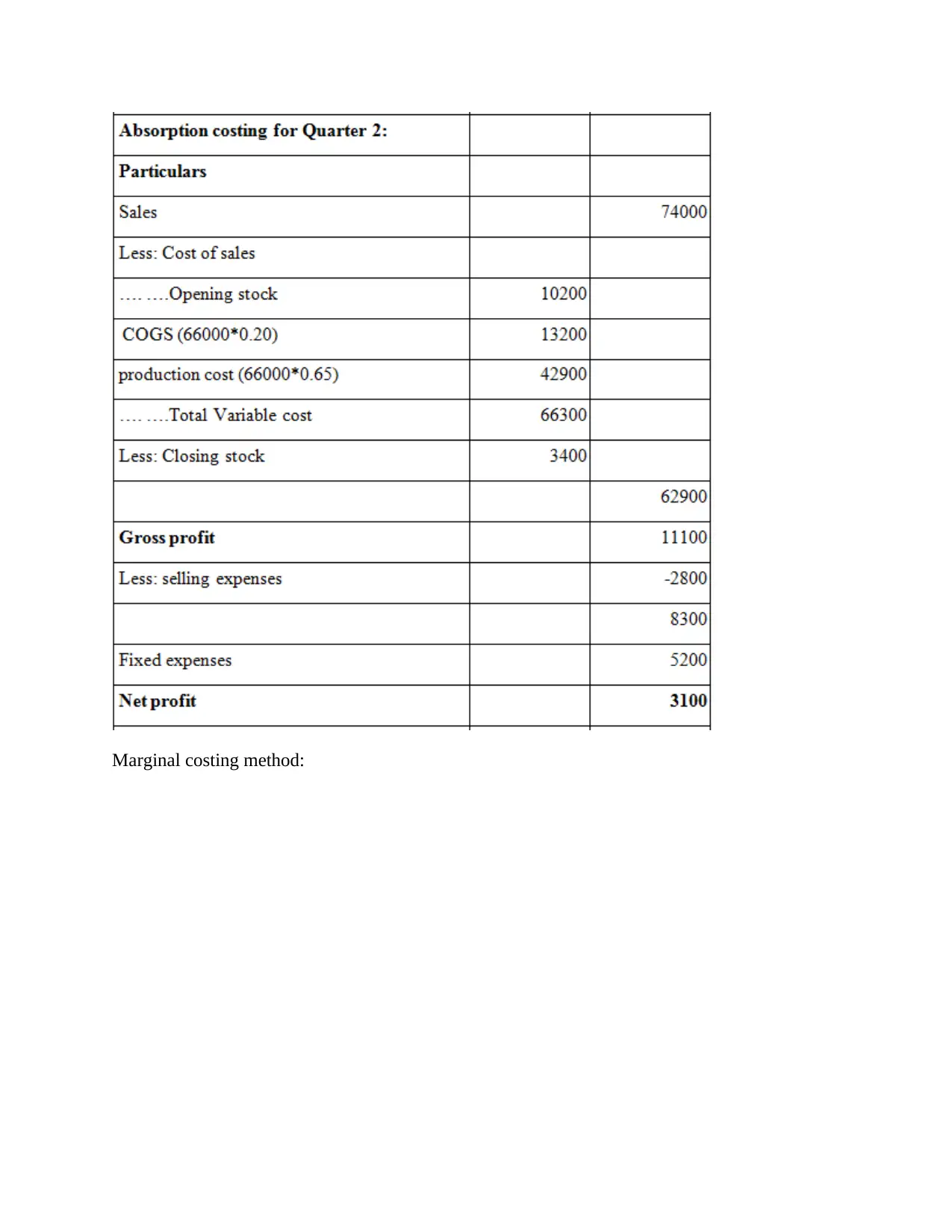

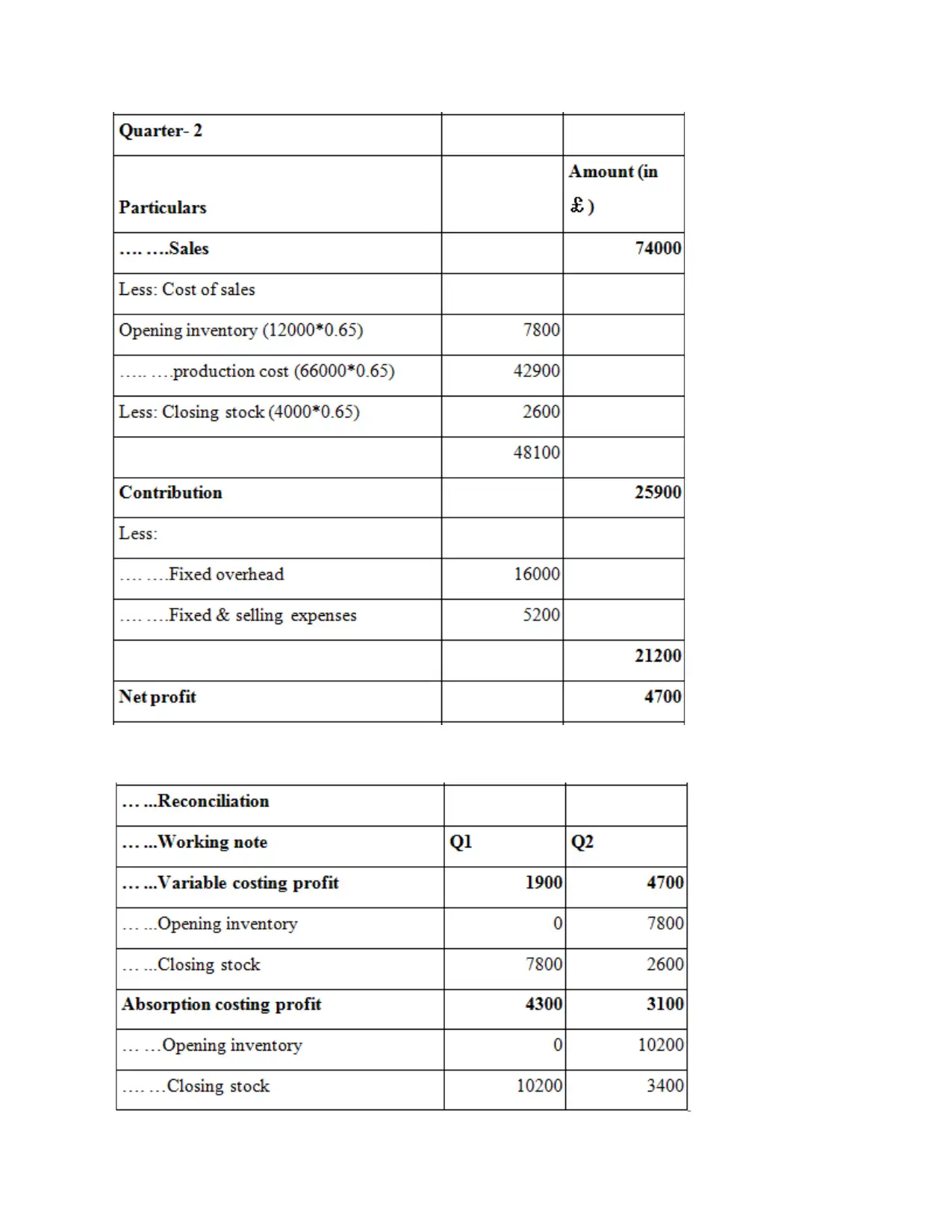

From above, it could be seen that net income for quarters 1 is £ 4300 under absorption costs and

this is £ 3100 for quarters 2. Owing to the increased amount of sales, net profit was higher in Q2.

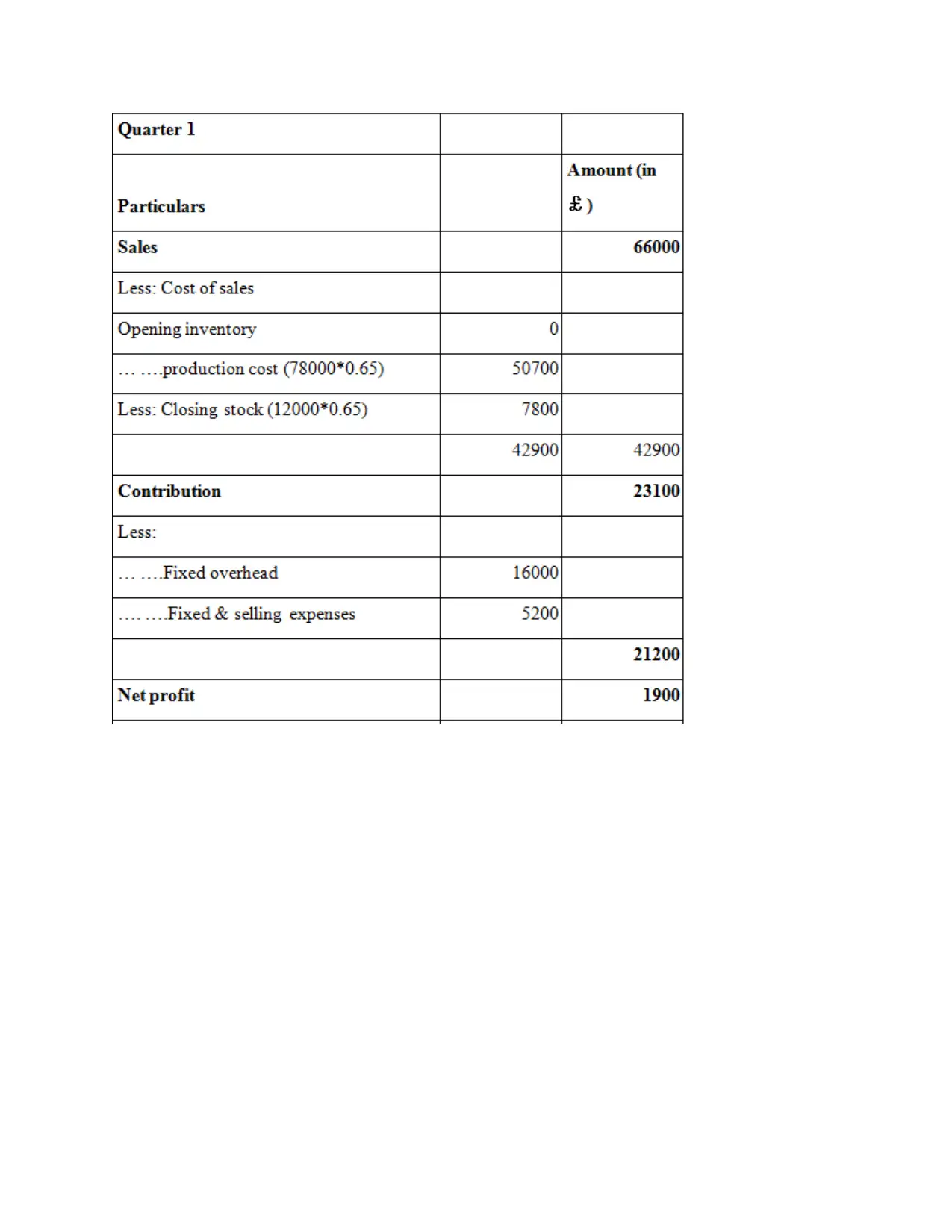

Under marginal costs, the profits are reported by both quarters. Net profit of £ 1900 for portion 1,

whereas it is £ 4700 for quarter 2, in quarter 2, high net margin were due to increased marginal

sales prices. Different methods of taking expenses can be due to the disparity in profit/loss

between both the two strategies-fixed and variable through 2 methods when planning the income

statement. The rationale behind change in net margin and loss under both techniques is due to

consideration of cost in different manner as in marginal costing only variable cost is taken as cost

of production. While in absorption costing fixed and variable both are taken as cost of

production.

TASK 3.

P4. Limitations and benefits of planning tools of budgetary control.

Budgetary control- This can be understood as a kind of method and efforts by several various

expenditure plan to control monetary and anti-financial performance. In this aspect of budget

position, the management of organizations takes corrective measures to produce more results

through these strategic planning. There are a variety of budgets expected so these are:

Operational budget- It is a budget type that allows the management to determine over a certain

time the volume of product needed to complete multiple activities. For the management in the

sense which prime furniture is limited, the accountants plan this estimation. The managers take

In the corporate finance sector, most revenue reports are organized through absorption and

marginal costing structures. As with Prime furniture, income is reported by absorption and

incremental costing approaches (Ferdous, Adams and Boyce, 2019). The pluralities of

approaches, with the exception of these, include planning of financial reports such as a

traditional cost scheme, costing events, etc. In relation to standard costing, the calculation of

potential costs used for comparison will be seen as being related. Operational expense is

dispersed and assessed for different types of operation by growing activity.

D2. Interpretation of prepared financial statements.

From above, it could be seen that net income for quarters 1 is £ 4300 under absorption costs and

this is £ 3100 for quarters 2. Owing to the increased amount of sales, net profit was higher in Q2.

Under marginal costs, the profits are reported by both quarters. Net profit of £ 1900 for portion 1,

whereas it is £ 4700 for quarter 2, in quarter 2, high net margin were due to increased marginal

sales prices. Different methods of taking expenses can be due to the disparity in profit/loss

between both the two strategies-fixed and variable through 2 methods when planning the income

statement. The rationale behind change in net margin and loss under both techniques is due to

consideration of cost in different manner as in marginal costing only variable cost is taken as cost

of production. While in absorption costing fixed and variable both are taken as cost of

production.

TASK 3.

P4. Limitations and benefits of planning tools of budgetary control.

Budgetary control- This can be understood as a kind of method and efforts by several various

expenditure plan to control monetary and anti-financial performance. In this aspect of budget

position, the management of organizations takes corrective measures to produce more results

through these strategic planning. There are a variety of budgets expected so these are:

Operational budget- It is a budget type that allows the management to determine over a certain

time the volume of product needed to complete multiple activities. For the management in the

sense which prime furniture is limited, the accountants plan this estimation. The managers take

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

corrective decisions with regard to the control of multiple activities in this budget. In the aspect

of above Prime furniture limited, they adopt such budget in order to manage different kinds of

operations like how much amount of wood is needed to produce furniture and many more.

Benefits-

This budget is useful for businesses to track the use of various types of resources in an

organization.

In addition to this, above budget contributes in managing different kind of operations which are

performed in prime furniture limited to produce various kinds of items.

Drawbacks-

It takes too much time and resources for allocating expenditures, which is the key issues under

this budget.

This budget is not suitable for companies which are operated at small level or have small size.

Cash budget- It is a report that describes both cash revenue and expenditures and concentrates on

projections for a given accounting cycle (Modell, 2019). After all budgets such as income,

master budget, capital budget and buying budget, the final budget is produced. Expenditures and

changes of financial items are marked. It is primarily for external actors and cannot be

conveniently modified after release. In relation to above Prime furniture limited they apply such

budget in order to manage all those activities which are related to cash receipts and expenses

during a particular time period. This budget has many advantages and disadvantages in the

above-mentioned company aspect, such as:

Benefits-

This is useful for businesses to manage cash and profits on a daily basis.

By help of such budget, it becomes easier for companies to track usage of allocated cash items

and different kinds of items which lead to cash incomes.

of above Prime furniture limited, they adopt such budget in order to manage different kinds of

operations like how much amount of wood is needed to produce furniture and many more.

Benefits-

This budget is useful for businesses to track the use of various types of resources in an

organization.

In addition to this, above budget contributes in managing different kind of operations which are

performed in prime furniture limited to produce various kinds of items.

Drawbacks-

It takes too much time and resources for allocating expenditures, which is the key issues under

this budget.

This budget is not suitable for companies which are operated at small level or have small size.

Cash budget- It is a report that describes both cash revenue and expenditures and concentrates on

projections for a given accounting cycle (Modell, 2019). After all budgets such as income,

master budget, capital budget and buying budget, the final budget is produced. Expenditures and

changes of financial items are marked. It is primarily for external actors and cannot be

conveniently modified after release. In relation to above Prime furniture limited they apply such

budget in order to manage all those activities which are related to cash receipts and expenses

during a particular time period. This budget has many advantages and disadvantages in the

above-mentioned company aspect, such as:

Benefits-

This is useful for businesses to manage cash and profits on a daily basis.

By help of such budget, it becomes easier for companies to track usage of allocated cash items

and different kinds of items which lead to cash incomes.

Drawbacks-

This budget is focused on assumptions such that corporations cannot rely solely on it for other

financial arrangements.

This budget does not produce any accurate outcome for companies and due to which it becomes

risk for companies to take better decisions.

Capital budget- The process for assessing potentially huge project or investment is the working

capital process undertaken by a company. Building of a new facility or large investments in an

external undertaking is project reports requiring the budgeting of wealth before approval or

rejection. In order to decide whether expected rewards that are produced follow a appropriate

goal benchmark, a business could evaluate cash inflows and outflows in a future project for life.

Investment assessment is sometimes considered the capital budgeting process.

Benefits-

The financial situation of primary furniture is evaluated with a thorough budget analysis.

Another benefit of this budget is that it is helpful for assessing company’s long term investments

and guiding about investments.

Drawback-

The major challenge in this budget is that changes are difficult to create.

It does not produce accurate projections each time and companies cannot rely on this because

investment error may lead to huge loss of company.

Pricing:

Pricing strategies:

This budget is focused on assumptions such that corporations cannot rely solely on it for other

financial arrangements.

This budget does not produce any accurate outcome for companies and due to which it becomes

risk for companies to take better decisions.

Capital budget- The process for assessing potentially huge project or investment is the working

capital process undertaken by a company. Building of a new facility or large investments in an

external undertaking is project reports requiring the budgeting of wealth before approval or

rejection. In order to decide whether expected rewards that are produced follow a appropriate

goal benchmark, a business could evaluate cash inflows and outflows in a future project for life.

Investment assessment is sometimes considered the capital budgeting process.

Benefits-

The financial situation of primary furniture is evaluated with a thorough budget analysis.

Another benefit of this budget is that it is helpful for assessing company’s long term investments

and guiding about investments.

Drawback-

The major challenge in this budget is that changes are difficult to create.

It does not produce accurate projections each time and companies cannot rely on this because

investment error may lead to huge loss of company.

Pricing:

Pricing strategies:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.