Financial Statement Analysis Exam Questions and Answers

VerifiedAdded on 2022/12/30

|5

|603

|54

Quiz and Exam

AI Summary

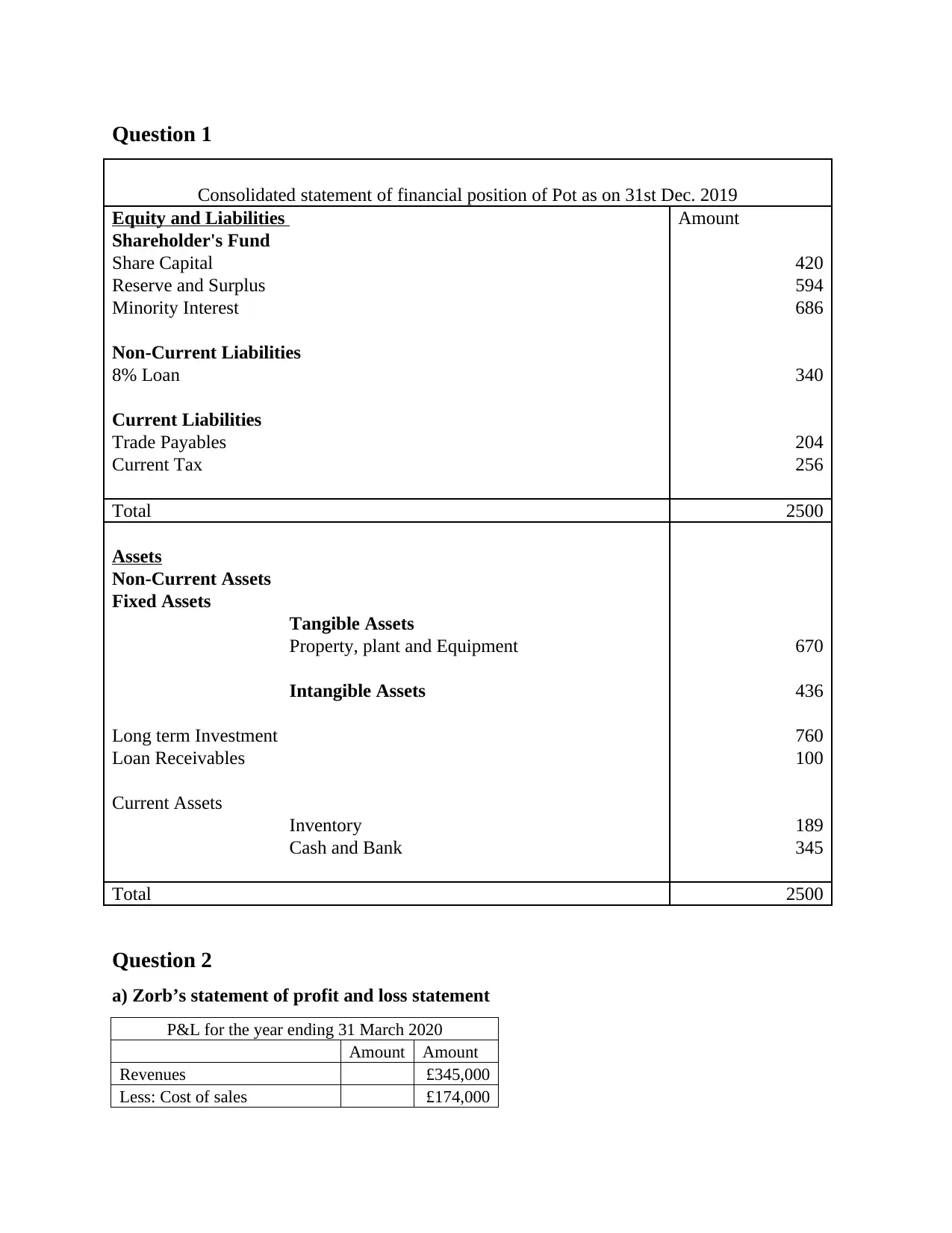

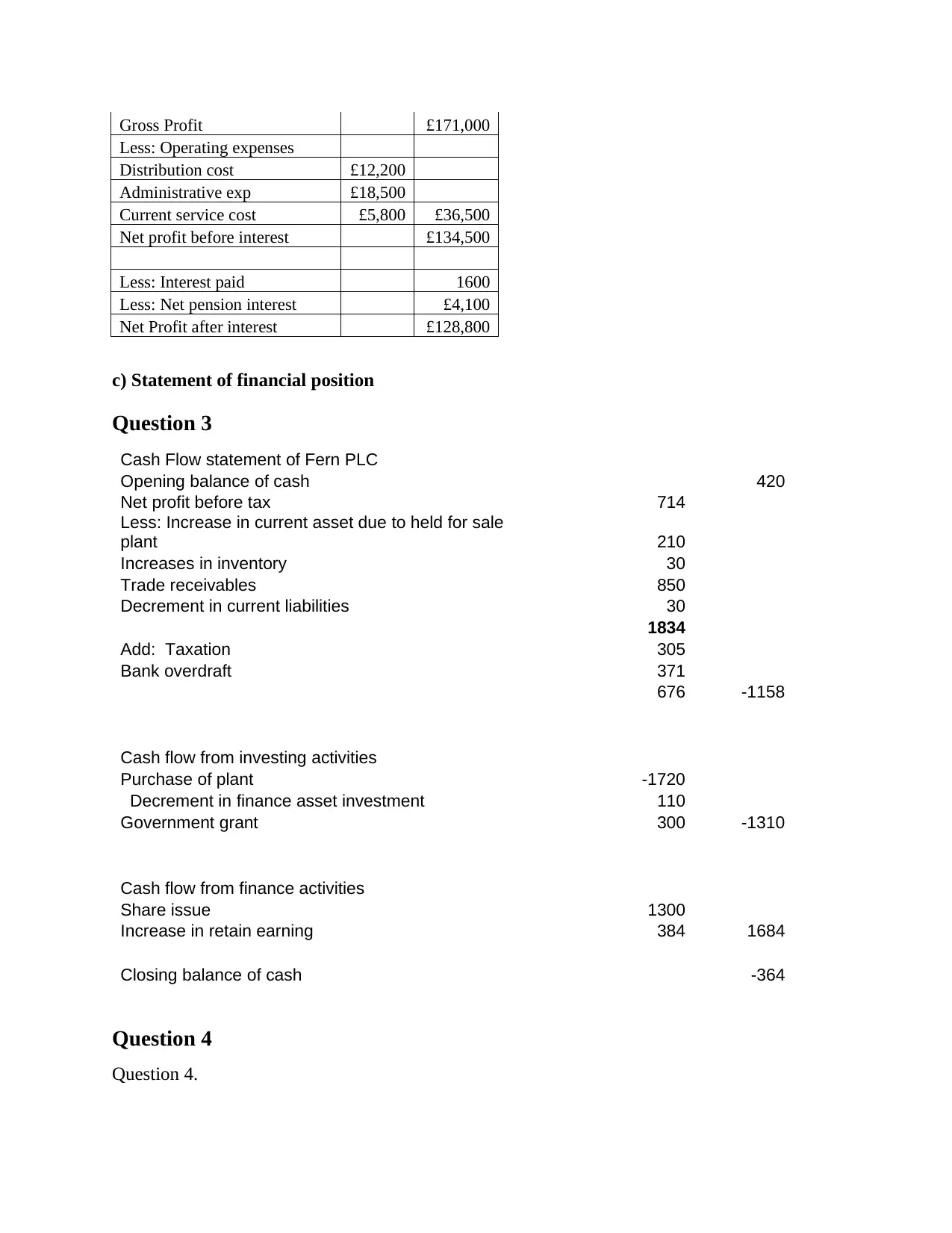

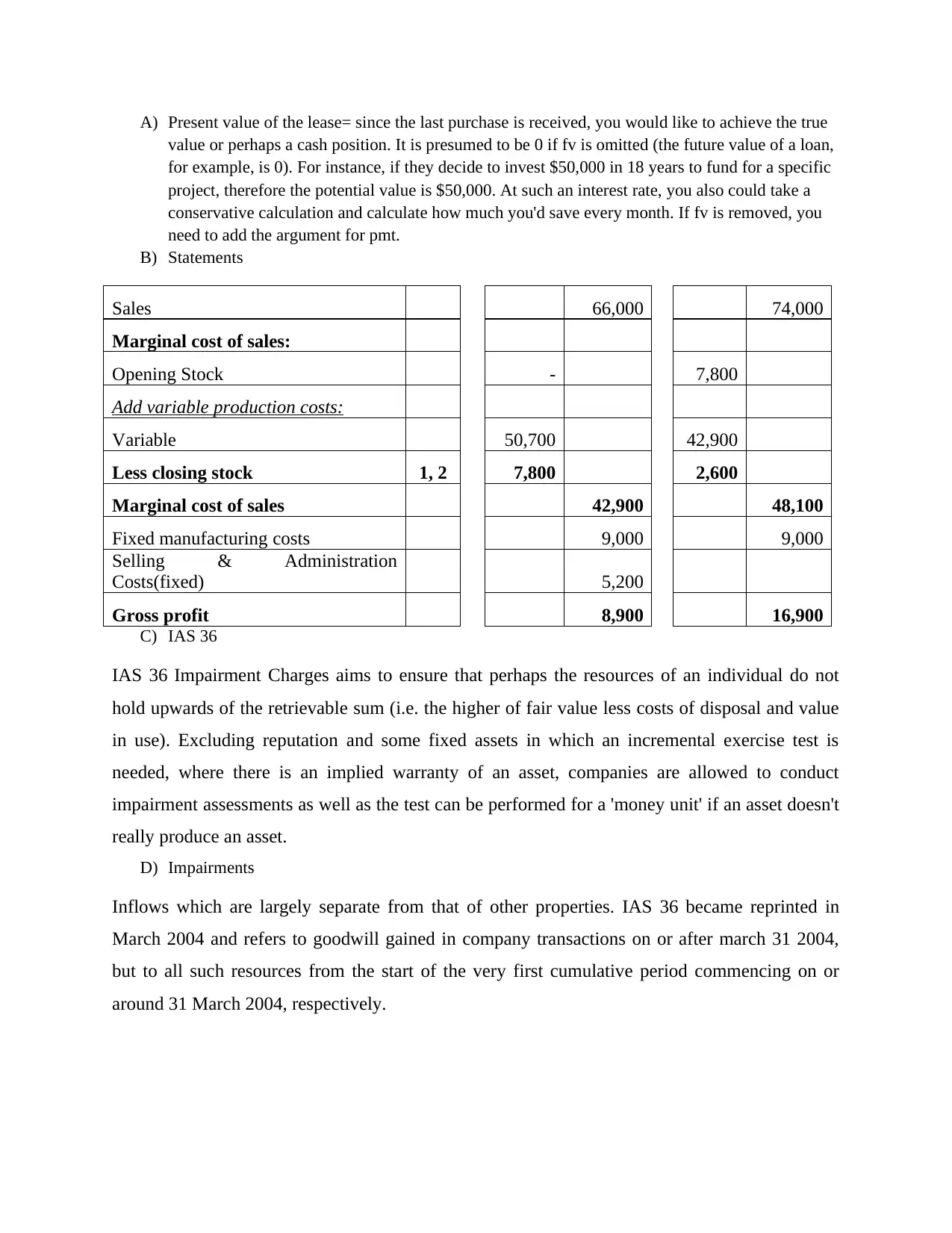

This document presents a comprehensive set of solutions to finance exam questions, encompassing various aspects of financial accounting and reporting. The content includes detailed answers to questions on consolidated statements of financial position, profit and loss statements, and cash flow statements. It explores topics such as the calculation of net profit, the impact of operating expenses, and the analysis of financial ratios. Furthermore, the document provides insights into the present value of leases, marginal cost of sales, and the application of accounting standards like IAS 36 concerning impairment charges. The solutions are designed to assist students in understanding key financial concepts and preparing for their examinations.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.