Financial Information: Analysis, Users, and Purpose for Businesses

VerifiedAdded on 2020/12/09

|9

|2339

|196

Report

AI Summary

This report provides a comprehensive analysis of financial information, focusing on financial ratios and their application in measuring business performance, particularly using the example of Mercia Trading Ltd. It delves into the legal requirements for financial information across different organizational structures in the UK, including sole traders, partnerships, private limited companies, and public limited companies. The report further evaluates the need for financial information by management, emphasizing the importance of balance sheets, income statements, and cash flow statements in decision-making. It identifies both internal and external users of financial information, outlining their specific interests and how financial statements serve their needs. Finally, the report explains the purpose of financial statements, highlighting their role in providing insights into operational results, cash flow, and financial position for various stakeholders. The report concludes by emphasizing the essential role of financial information in understanding a business's financial health and making informed decisions.

Understanding Financial

Information

Information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

1.1Explaining the financial ratios and measuring the performance of the business...................1

LO2..................................................................................................................................................1

2.1Explaining the legal requirement of the financial information from different types of

organizations in UK....................................................................................................................1

LO3. ................................................................................................................................................2

3.1 Evaluating the need for financial information by the management......................................2

LO4. ................................................................................................................................................3

4.1 Identifying the users of financial information and their interest in this information............3

LO5..................................................................................................................................................4

5.1 Explaining the purpose of the financial statements in the business. ....................................4

CONCLUSION ...............................................................................................................................4

REFERENCES................................................................................................................................5

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

1.1Explaining the financial ratios and measuring the performance of the business...................1

LO2..................................................................................................................................................1

2.1Explaining the legal requirement of the financial information from different types of

organizations in UK....................................................................................................................1

LO3. ................................................................................................................................................2

3.1 Evaluating the need for financial information by the management......................................2

LO4. ................................................................................................................................................3

4.1 Identifying the users of financial information and their interest in this information............3

LO5..................................................................................................................................................4

5.1 Explaining the purpose of the financial statements in the business. ....................................4

CONCLUSION ...............................................................................................................................4

REFERENCES................................................................................................................................5

INTRODUCTION

Financial statements are the systematic record of the financial transactions, activities and

events which contains monetary value. It represents the position of the business and presented in

the structured manner. Such statements are easy to understand and simple to develop. It plays a

crucial role in summarizing, interpreting and communicating the results to the users. The present

study is based on the evaluation of the financial performance of the Mercia Trading Ltd by

analyzing its financial ratios. Furthermore, the report includes the financial information that are

legally needed by various firms in UK. The study also includes the need, users and the purpose

of financial statements for the users and the management.

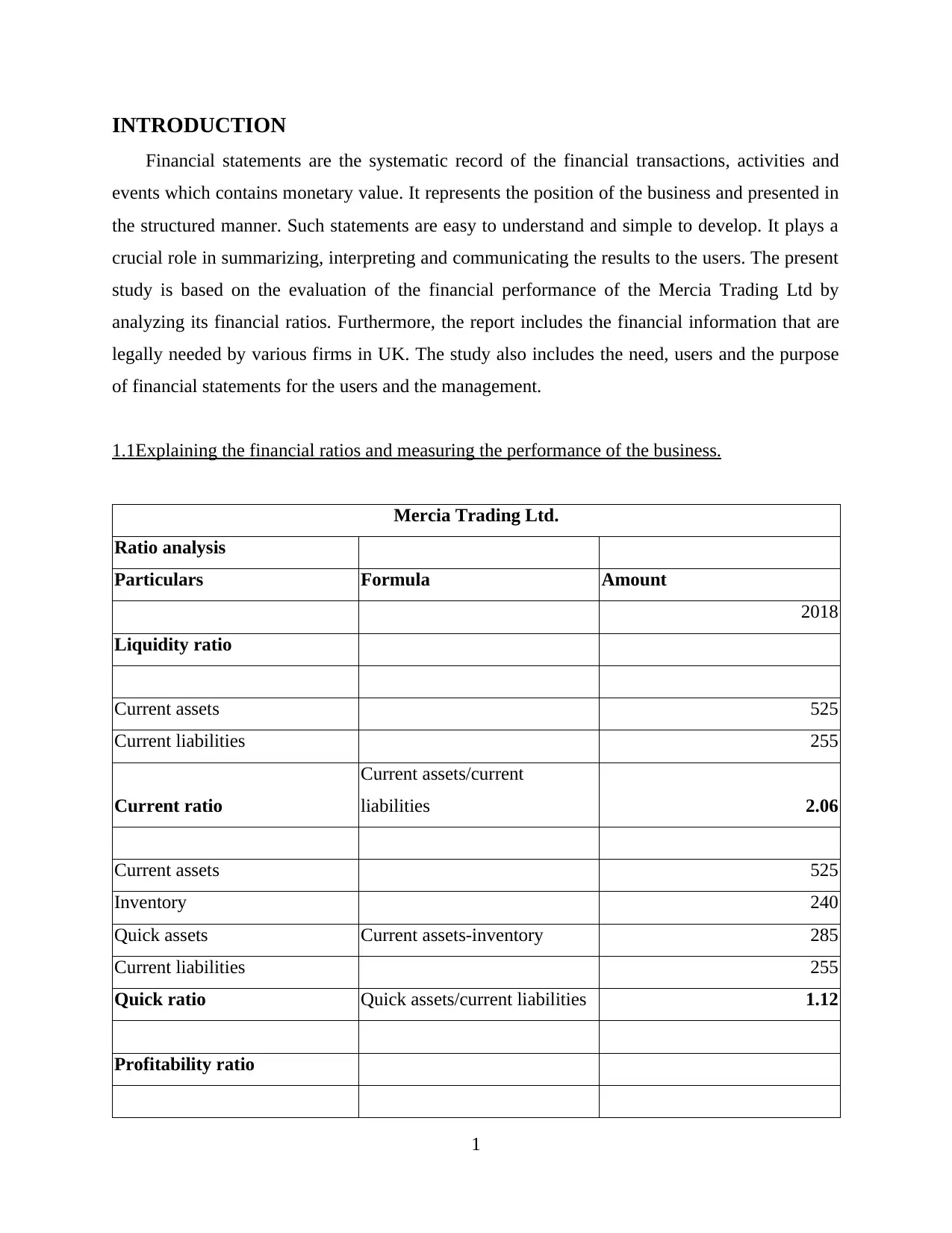

1.1Explaining the financial ratios and measuring the performance of the business.

Mercia Trading Ltd.

Ratio analysis

Particulars Formula Amount

2018

Liquidity ratio

Current assets 525

Current liabilities 255

Current ratio

Current assets/current

liabilities 2.06

Current assets 525

Inventory 240

Quick assets Current assets-inventory 285

Current liabilities 255

Quick ratio Quick assets/current liabilities 1.12

Profitability ratio

1

Financial statements are the systematic record of the financial transactions, activities and

events which contains monetary value. It represents the position of the business and presented in

the structured manner. Such statements are easy to understand and simple to develop. It plays a

crucial role in summarizing, interpreting and communicating the results to the users. The present

study is based on the evaluation of the financial performance of the Mercia Trading Ltd by

analyzing its financial ratios. Furthermore, the report includes the financial information that are

legally needed by various firms in UK. The study also includes the need, users and the purpose

of financial statements for the users and the management.

1.1Explaining the financial ratios and measuring the performance of the business.

Mercia Trading Ltd.

Ratio analysis

Particulars Formula Amount

2018

Liquidity ratio

Current assets 525

Current liabilities 255

Current ratio

Current assets/current

liabilities 2.06

Current assets 525

Inventory 240

Quick assets Current assets-inventory 285

Current liabilities 255

Quick ratio Quick assets/current liabilities 1.12

Profitability ratio

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

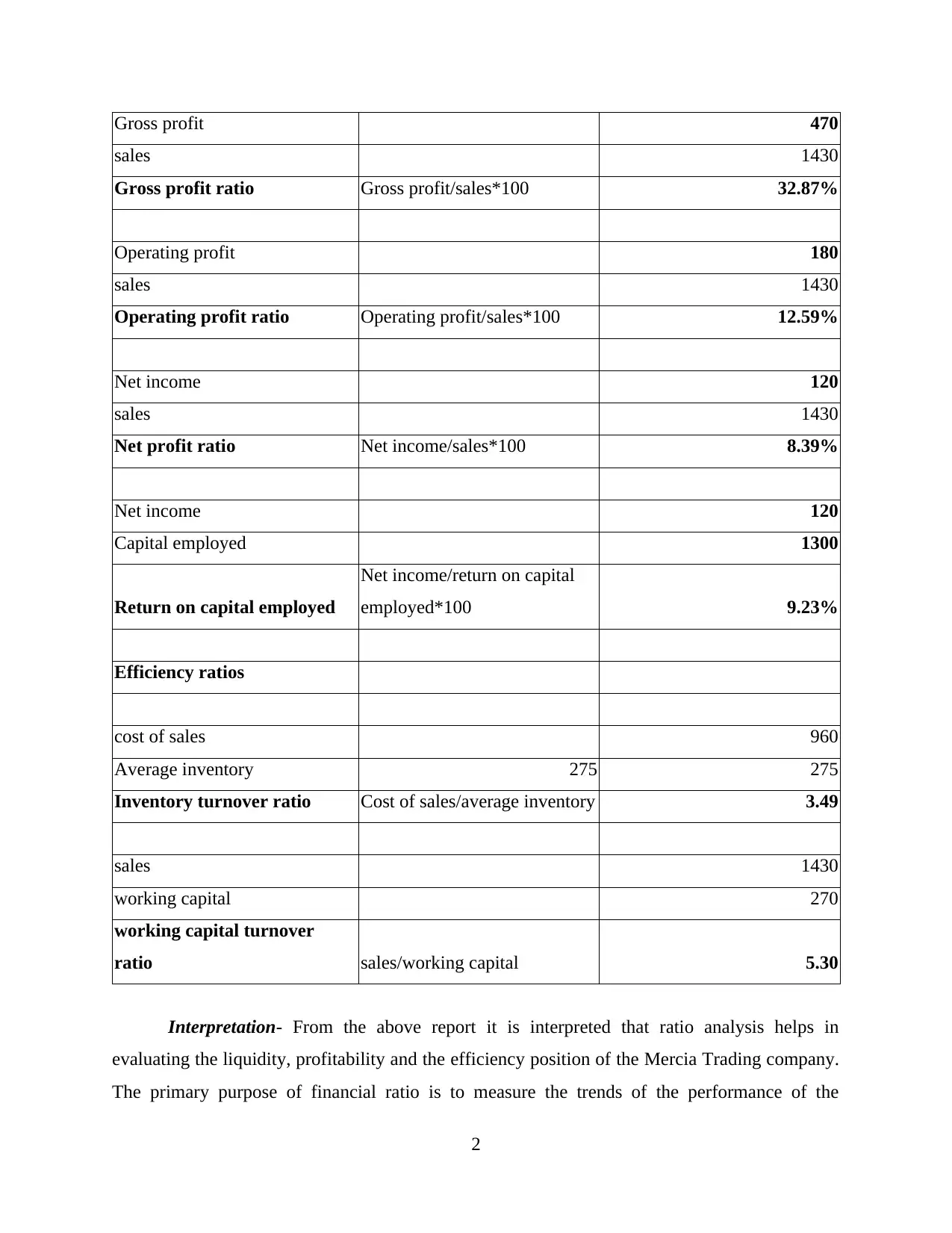

Gross profit 470

sales 1430

Gross profit ratio Gross profit/sales*100 32.87%

Operating profit 180

sales 1430

Operating profit ratio Operating profit/sales*100 12.59%

Net income 120

sales 1430

Net profit ratio Net income/sales*100 8.39%

Net income 120

Capital employed 1300

Return on capital employed

Net income/return on capital

employed*100 9.23%

Efficiency ratios

cost of sales 960

Average inventory 275 275

Inventory turnover ratio Cost of sales/average inventory 3.49

sales 1430

working capital 270

working capital turnover

ratio sales/working capital 5.30

Interpretation- From the above report it is interpreted that ratio analysis helps in

evaluating the liquidity, profitability and the efficiency position of the Mercia Trading company.

The primary purpose of financial ratio is to measure the trends of the performance of the

2

sales 1430

Gross profit ratio Gross profit/sales*100 32.87%

Operating profit 180

sales 1430

Operating profit ratio Operating profit/sales*100 12.59%

Net income 120

sales 1430

Net profit ratio Net income/sales*100 8.39%

Net income 120

Capital employed 1300

Return on capital employed

Net income/return on capital

employed*100 9.23%

Efficiency ratios

cost of sales 960

Average inventory 275 275

Inventory turnover ratio Cost of sales/average inventory 3.49

sales 1430

working capital 270

working capital turnover

ratio sales/working capital 5.30

Interpretation- From the above report it is interpreted that ratio analysis helps in

evaluating the liquidity, profitability and the efficiency position of the Mercia Trading company.

The primary purpose of financial ratio is to measure the trends of the performance of the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business and comparing it with the ideal ratios. However, the limitation of the financial ratio is

they are analyzed on the basis of the accounting figures which are estimated and thus lack

accuracy. Manipulation can be possible in the statements which leads to incorrect valuation of

ratio. Hence, the liquidity position of this company is said to be better as it equates with the ideal

ratio that is 2:1 which indicates efficient management of its assets and has the capability in

meeting the current obligation. The profitability position is also reflects better results which

means company has sufficient profits to meet its expenses and costs. The efficiency ratios

indicated as better ratio as it equates to 3.49 & 5.30 which means inventory and current assets are

managed effectively by the Mercia Trading company.

2.1Explaining the legal requirement of the financial information from different types of

organizations in UK.

Sole trader- It is the organization where an individual run the business on its own and are

called as the self-employed. According to the UK law, Sole trader is one whose earnings are

more than £1000 from its self employment between the one year period that begins with 6th April

2018 to 5th April 2019. They need to have VAT registration if their turnover exceeds £85000. It

is not mandatory for the sole trader to maintain financial statements in the UK.

Partnership firm- In this, each partner has the legal right to take participation in the

management of their business with subject to the terms and conditions in the agreement

(Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros, 2015). Every partner must have to

assess the complete tax returns in proportion of their profits and then must have to submit these

returns annually to the HMRC. They also have to pay the National Insurance Contributions.

Private limited companies- It is compulsory for all the private companies in the UK to file

their accounting information at the companies house. The company need to submit its financial

information within 9 months of the accounting period ended. Companies whose threshold limit

exceeds in relation to the turnover that is £10.2 million, gross assets limits over £5.1 million and

the employees are 50 or more than that must need an audit of their accounts.

Public limited companies- In UK, companies are said to be public limited when it has

minimum two shareholders and have issued the shares to public for a value of at-least £50000.

The financial information or statements of these companies must be submitted at the company

3

they are analyzed on the basis of the accounting figures which are estimated and thus lack

accuracy. Manipulation can be possible in the statements which leads to incorrect valuation of

ratio. Hence, the liquidity position of this company is said to be better as it equates with the ideal

ratio that is 2:1 which indicates efficient management of its assets and has the capability in

meeting the current obligation. The profitability position is also reflects better results which

means company has sufficient profits to meet its expenses and costs. The efficiency ratios

indicated as better ratio as it equates to 3.49 & 5.30 which means inventory and current assets are

managed effectively by the Mercia Trading company.

2.1Explaining the legal requirement of the financial information from different types of

organizations in UK.

Sole trader- It is the organization where an individual run the business on its own and are

called as the self-employed. According to the UK law, Sole trader is one whose earnings are

more than £1000 from its self employment between the one year period that begins with 6th April

2018 to 5th April 2019. They need to have VAT registration if their turnover exceeds £85000. It

is not mandatory for the sole trader to maintain financial statements in the UK.

Partnership firm- In this, each partner has the legal right to take participation in the

management of their business with subject to the terms and conditions in the agreement

(Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros, 2015). Every partner must have to

assess the complete tax returns in proportion of their profits and then must have to submit these

returns annually to the HMRC. They also have to pay the National Insurance Contributions.

Private limited companies- It is compulsory for all the private companies in the UK to file

their accounting information at the companies house. The company need to submit its financial

information within 9 months of the accounting period ended. Companies whose threshold limit

exceeds in relation to the turnover that is £10.2 million, gross assets limits over £5.1 million and

the employees are 50 or more than that must need an audit of their accounts.

Public limited companies- In UK, companies are said to be public limited when it has

minimum two shareholders and have issued the shares to public for a value of at-least £50000.

The financial information or statements of these companies must be submitted at the company

3

house (Du, Yu and Yu, 2017). Registration of such companies is mandatory with the companies

house. It must have minimum two direction of which one must be individual.

3.1 Evaluating the need for financial information by the management.

Financial information act as the powerful tool for the management to bring positive

outcomes within the enterprise. Such information plays a crucial role for the owners of the

business in evaluating the strengths and the weaknesses of its business. Financial information

helps the managers in formulating the budgets and in making effective future projections. The

three major financial statements that presents the financial information are balance sheet, cash

flow and profit or loss accounts.

Balance sheet- It helps the managers in determining the liabilities and the assets of the

corporate through which they can evaluate the position of the company. It directs the

management in meeting its long term obligation and creating the wealth of the shareholder by

increasing the stockholder's equity (Theriou, 2015). It provides the information to the managers

in relation to the exact owing of the business against its debt.

Income statement- Through this statement managers can get the information in terms of

the expenses and the revenues of the organization so that they can prepare the budget with full

accuracy. The managers can make appropriate estimations of the expenses and the revenues for

smooth functioning of the operations. It helps in making the report on the routine expenses of the

business within the management.

Cash flow statement- Such statements provide the financial information in relation to the

cash and cash equivalent of the business. The managers can assess the inflows and the outflows

of cash into and outside the business so that they can prepare the cash budget appropriately

(Cash flow statement, 2019). They could estimate about the coming expenses and the income

opportunities if any for the company.

4.1 Identifying the users of financial information and their interest in this information.

The users of the financial information are categorized into two main segments that are

internal and external users. Internal users are those who are present in the internal working of the

organization such as managers, owners etc. while external users are those who act as the

outsiders for the company but are affected with the performance of the entity like investors,

government authorities etc.

Internal users-

4

house. It must have minimum two direction of which one must be individual.

3.1 Evaluating the need for financial information by the management.

Financial information act as the powerful tool for the management to bring positive

outcomes within the enterprise. Such information plays a crucial role for the owners of the

business in evaluating the strengths and the weaknesses of its business. Financial information

helps the managers in formulating the budgets and in making effective future projections. The

three major financial statements that presents the financial information are balance sheet, cash

flow and profit or loss accounts.

Balance sheet- It helps the managers in determining the liabilities and the assets of the

corporate through which they can evaluate the position of the company. It directs the

management in meeting its long term obligation and creating the wealth of the shareholder by

increasing the stockholder's equity (Theriou, 2015). It provides the information to the managers

in relation to the exact owing of the business against its debt.

Income statement- Through this statement managers can get the information in terms of

the expenses and the revenues of the organization so that they can prepare the budget with full

accuracy. The managers can make appropriate estimations of the expenses and the revenues for

smooth functioning of the operations. It helps in making the report on the routine expenses of the

business within the management.

Cash flow statement- Such statements provide the financial information in relation to the

cash and cash equivalent of the business. The managers can assess the inflows and the outflows

of cash into and outside the business so that they can prepare the cash budget appropriately

(Cash flow statement, 2019). They could estimate about the coming expenses and the income

opportunities if any for the company.

4.1 Identifying the users of financial information and their interest in this information.

The users of the financial information are categorized into two main segments that are

internal and external users. Internal users are those who are present in the internal working of the

organization such as managers, owners etc. while external users are those who act as the

outsiders for the company but are affected with the performance of the entity like investors,

government authorities etc.

Internal users-

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Owners- They assess the performance of their business through the financial statements

of its business. Financial information enables the owners in ascertaining the stability level of

their business and in evaluating several economic factors that affects the functioning of their

business activities (Pucheta‐Martínez, Bel‐Oms and Olcina‐Sempere, 2016). Accounting

information helps them to make decisions regarding the use and procurement of the financial

resources. It also helps them in determining the need of expansion and diversification in their

business.

Managers- They need financial information to monitor, plan and in making business

decisions. They require the information to track the performance of the business by comparing

the current performance against the previous performance and if any deviation resulted then to

take corrective action. For analyzing the competitor and making use of bench-marking or other

tools to resolve the financial problems, such information are of great importance.

External users-

Investors- They use accounting information for identifying the performance of their

investment made in the business of the entity. Primarily they rely on the financial information

represented through the statements in order to assess the valuation, profitability and the risk

involved in their investment (Borio, Disyatat, and Juselius, 2016). Such information helps them

in developing suitable decisions regarding the further investment or to hold the investment made.

Government- Through the financial information government can monitor that the

disclosure made by the company in its statements are as per the rules and regulations. It helps in

protecting the stakeholders interest who uses such information for forming the best decisions. It

enables the government in knowing that the preparation of the statements is in compliance with

the accounting standards and right amount of taxes are paid or not.

5.1 Explaining the purpose of the financial statements in the business.

The basic objective or purpose of the financial statements is to facilitate the information

regarding the operational results, cash flow and financial position of the organization. Such

information is used by several readers in making decisions in terms of the allocation of the

resources. Moreover, different purposes are attached with each statements. Income statement

provides information relating to the ability of the business in generating profits. It reveals about

the sales volume and the expenses of the company (Nobes and Stadler, 2015). Continuous

review of this statement helps in analyzing the resulting trends in the operations of the company.

5

of its business. Financial information enables the owners in ascertaining the stability level of

their business and in evaluating several economic factors that affects the functioning of their

business activities (Pucheta‐Martínez, Bel‐Oms and Olcina‐Sempere, 2016). Accounting

information helps them to make decisions regarding the use and procurement of the financial

resources. It also helps them in determining the need of expansion and diversification in their

business.

Managers- They need financial information to monitor, plan and in making business

decisions. They require the information to track the performance of the business by comparing

the current performance against the previous performance and if any deviation resulted then to

take corrective action. For analyzing the competitor and making use of bench-marking or other

tools to resolve the financial problems, such information are of great importance.

External users-

Investors- They use accounting information for identifying the performance of their

investment made in the business of the entity. Primarily they rely on the financial information

represented through the statements in order to assess the valuation, profitability and the risk

involved in their investment (Borio, Disyatat, and Juselius, 2016). Such information helps them

in developing suitable decisions regarding the further investment or to hold the investment made.

Government- Through the financial information government can monitor that the

disclosure made by the company in its statements are as per the rules and regulations. It helps in

protecting the stakeholders interest who uses such information for forming the best decisions. It

enables the government in knowing that the preparation of the statements is in compliance with

the accounting standards and right amount of taxes are paid or not.

5.1 Explaining the purpose of the financial statements in the business.

The basic objective or purpose of the financial statements is to facilitate the information

regarding the operational results, cash flow and financial position of the organization. Such

information is used by several readers in making decisions in terms of the allocation of the

resources. Moreover, different purposes are attached with each statements. Income statement

provides information relating to the ability of the business in generating profits. It reveals about

the sales volume and the expenses of the company (Nobes and Stadler, 2015). Continuous

review of this statement helps in analyzing the resulting trends in the operations of the company.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The foremost purpose of balance sheet is facilitating the information regarding the present

status of business and measures the financial position of the entity. Such information are used to

anticipate the liquidity, debt position, and funding of an enterprise. It acts as the basis for

evaluating liquidity ratios. The purpose of the cash flow statement is to ascertain the cash

position of the corporate by showing the receipts and the disbursements of the cash. It helps in

maintaining and keeping control over the expenses.

There are some additional purposes of the financial statements that includes the credit

decisions, taxation decisions, investment decisions and the bargaining decisions. Lender make

use of the information for determining the credibility or credit worthiness of the company so that

they can evaluate the extent to which the company can borrow further (Tchamyou, 2019). A

union can make judgments on the probable ability of company to pay so that they could base

their bargaining positions.

CONCLUSION

From the above report it is summarized that financial information is very essential for the

organization in understanding its financial health and to make improved decisions in context of

its business. Financial statements facilitate several financial related matters that the investors,

creditors and other users uses to assess the financial position and performance of the enterprise.

6

status of business and measures the financial position of the entity. Such information are used to

anticipate the liquidity, debt position, and funding of an enterprise. It acts as the basis for

evaluating liquidity ratios. The purpose of the cash flow statement is to ascertain the cash

position of the corporate by showing the receipts and the disbursements of the cash. It helps in

maintaining and keeping control over the expenses.

There are some additional purposes of the financial statements that includes the credit

decisions, taxation decisions, investment decisions and the bargaining decisions. Lender make

use of the information for determining the credibility or credit worthiness of the company so that

they can evaluate the extent to which the company can borrow further (Tchamyou, 2019). A

union can make judgments on the probable ability of company to pay so that they could base

their bargaining positions.

CONCLUSION

From the above report it is summarized that financial information is very essential for the

organization in understanding its financial health and to make improved decisions in context of

its business. Financial statements facilitate several financial related matters that the investors,

creditors and other users uses to assess the financial position and performance of the enterprise.

6

REFERENCES

Books and journals

Borio, C., Disyatat, P. and Juselius, M., 2016. Rethinking potential output: Embedding

information about the financial cycle. Oxford Economic Papers. 69(3). pp.655-677.

Du, Q., Yu, F. and Yu, X., 2017. Cultural proximity and the processing of financial

information. Journal of Financial and Quantitative Analysis. 52(6). pp.2703-2726.

Martínez‐Ferrero, J., Garcia‐Sanchez, I. M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management. 22(1). pp.45-64.

Nobes, C. W. and Stadler, C., 2015. The qualitative characteristics of financial information, and

managers’ accounting decisions: evidence from IFRS policy changes. Accounting and

Business Research. 45(5). pp.572-601.

Pucheta‐Martínez, M. C., Bel‐Oms, I. and Olcina‐Sempere, G., 2016. Corporate governance,

female directors and quality of financial information. Business Ethics: A European

Review. 25(4). pp.363-385.

Tchamyou, V. S., 2019. The role of information sharing in modulating the effect of financial

access on inequality. Journal of African Business. pp.1-22.

Theriou, N. G., 2015. Strategic Management Process and the Importance of Structured

Formality, Financial and Non-Financial Information. European Research Studies. 18(2). p.3.

Online

Cash flow statement. 2019. [Online]. Available through: <

https://www.edupristine.com/blog/cash-flow-statement-in-detail>.

7

Books and journals

Borio, C., Disyatat, P. and Juselius, M., 2016. Rethinking potential output: Embedding

information about the financial cycle. Oxford Economic Papers. 69(3). pp.655-677.

Du, Q., Yu, F. and Yu, X., 2017. Cultural proximity and the processing of financial

information. Journal of Financial and Quantitative Analysis. 52(6). pp.2703-2726.

Martínez‐Ferrero, J., Garcia‐Sanchez, I. M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management. 22(1). pp.45-64.

Nobes, C. W. and Stadler, C., 2015. The qualitative characteristics of financial information, and

managers’ accounting decisions: evidence from IFRS policy changes. Accounting and

Business Research. 45(5). pp.572-601.

Pucheta‐Martínez, M. C., Bel‐Oms, I. and Olcina‐Sempere, G., 2016. Corporate governance,

female directors and quality of financial information. Business Ethics: A European

Review. 25(4). pp.363-385.

Tchamyou, V. S., 2019. The role of information sharing in modulating the effect of financial

access on inequality. Journal of African Business. pp.1-22.

Theriou, N. G., 2015. Strategic Management Process and the Importance of Structured

Formality, Financial and Non-Financial Information. European Research Studies. 18(2). p.3.

Online

Cash flow statement. 2019. [Online]. Available through: <

https://www.edupristine.com/blog/cash-flow-statement-in-detail>.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.