Financial Reporting and Consolidated Financial Statements Analysis

VerifiedAdded on 2021/06/18

|12

|2899

|176

Report

AI Summary

This comprehensive report delves into the realm of financial reporting and consolidated financial statements, offering a detailed analysis of accounting practices. The report begins with an executive summary outlining the key objectives, which include assessing the qualitative characteristics of financial reporting, evaluating compliance with environmental regulations, and understanding the preparation of consolidated financial statements, with a specific focus on the role of subsidiaries. Part A of the report examines the financial reporting of Woolworths Limited, evaluating the relevance and comparability of its financial statements, as well as its environmental reporting practices and the adequacy of information disclosed. The report then provides recommendations to strengthen these areas. Part B focuses on the accounting for pre-acquisition entries, explaining their purpose, as well as discussing dividend treatment and the effects of goodwill in consolidated financial statements. The analysis provides a clear understanding of the accounting treatments for pre and post acquisition dividends.

FINANCIAL REPORTING AND CONSOLIDATED FINANCIAL STATEMENTS

Student Name: Student Number:

5/25/2018

Student Name: Student Number:

5/25/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

PART A.........................................................................................................................................................2

DETAILS OF COMPANY SELECTED............................................................................................................2

RELEVANCE AND COMPARABILITY..........................................................................................................2

ENVIRONMENTAL REPORTING PRACTICES..............................................................................................2

ADEQUACY OF INFORMATION AND DISCLOSURES..................................................................................2

RECOMMENDATION TO STRENGHTEN....................................................................................................2

PART B.........................................................................................................................................................2

PURPOSE OF PREACQUISTION ENTRIES...................................................................................................2

DIVIDEND IN PREACQUISITON ENTRIES...................................................................................................2

DIVIDED – PRE AND POST........................................................................................................................2

EFFECT OF GOODWILL.............................................................................................................................2

ADJUSTMENTS IN THE CONSOLIDATED FINANCIAL STATEMENTS...........................................................2

CONCLUSION...............................................................................................................................................2

LIST OF REFERENCES....................................................................................................................................2

EXECUTIVE SUMMARY

The financial reporting shall be made in the manner as defined by the various statutes and laws

and regulations contained therein so as to provide the maximum available information to the

stakeholders of the company so that the efficient and the effective decision can be taken. This

study has been conducted with the view to have the understanding of the financial reporting

practices being adopted by the companies across the globe. The report has been framed with the

four main purposes. The first purpose has been to analyze whether the financial reporting made

by the companies is as per the conceptual framework of accounting and represents the qualitative

characteristics of the financial reporting. The second purpose has been to have analyzed the

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

PART A.........................................................................................................................................................2

DETAILS OF COMPANY SELECTED............................................................................................................2

RELEVANCE AND COMPARABILITY..........................................................................................................2

ENVIRONMENTAL REPORTING PRACTICES..............................................................................................2

ADEQUACY OF INFORMATION AND DISCLOSURES..................................................................................2

RECOMMENDATION TO STRENGHTEN....................................................................................................2

PART B.........................................................................................................................................................2

PURPOSE OF PREACQUISTION ENTRIES...................................................................................................2

DIVIDEND IN PREACQUISITON ENTRIES...................................................................................................2

DIVIDED – PRE AND POST........................................................................................................................2

EFFECT OF GOODWILL.............................................................................................................................2

ADJUSTMENTS IN THE CONSOLIDATED FINANCIAL STATEMENTS...........................................................2

CONCLUSION...............................................................................................................................................2

LIST OF REFERENCES....................................................................................................................................2

EXECUTIVE SUMMARY

The financial reporting shall be made in the manner as defined by the various statutes and laws

and regulations contained therein so as to provide the maximum available information to the

stakeholders of the company so that the efficient and the effective decision can be taken. This

study has been conducted with the view to have the understanding of the financial reporting

practices being adopted by the companies across the globe. The report has been framed with the

four main purposes. The first purpose has been to analyze whether the financial reporting made

by the companies is as per the conceptual framework of accounting and represents the qualitative

characteristics of the financial reporting. The second purpose has been to have analyzed the

compliance with the environmental laws and regulations. The third purpose has been to

understand how the consolidation financial statements are likely to be prepared and how the each

of the accounting shall be done in the books of accounts. The last major purpose is to consider

the role of the subsidiary in the preparation of the financial statements of the company. With

these considerations and the purposes the report has been prepared.

INTRODUCTION

The financial reporting made by the company shall have and exhibits the qualitative features.

These qualitative features have been prescribed by the conceptual framework of financial

reporting. These features shall not be neglected in any manner while preparing and presenting

not only the annual financial statements but also shall be considered in providing interim

reporting. For the purpose of verifying the qualitative features of the financial reporting, the

financial statements have been analysed with reference to the disclosure made and the necessary

information provided in the said financial statements. For the furtherance of this report, the

company – Woolworths Limited has been selected. The company has been one of the top

hundred of the ASX listed companies. The report has started with the verification of the presence

of the qualitative features of the financial reporting with the help of the financial statements.

Along with the financial Statements of the company, the environment reporting has also been

verified and analyzed as to whether the company has been disclosing the information which will

be relevant for the investors. Then the adequacy of the disclosures made or information provided

have been checked in detail and thereon the recommendation has been provided to the

management in order to further increase the disclosure requirements. Then the detailed analysis

of the accounting of the pre acquisition transaction has been made with respect to clarification on

every part with respect to its accounting treatment and reasons for its differences. The report has

then ended with the appropriate conclusion.

understand how the consolidation financial statements are likely to be prepared and how the each

of the accounting shall be done in the books of accounts. The last major purpose is to consider

the role of the subsidiary in the preparation of the financial statements of the company. With

these considerations and the purposes the report has been prepared.

INTRODUCTION

The financial reporting made by the company shall have and exhibits the qualitative features.

These qualitative features have been prescribed by the conceptual framework of financial

reporting. These features shall not be neglected in any manner while preparing and presenting

not only the annual financial statements but also shall be considered in providing interim

reporting. For the purpose of verifying the qualitative features of the financial reporting, the

financial statements have been analysed with reference to the disclosure made and the necessary

information provided in the said financial statements. For the furtherance of this report, the

company – Woolworths Limited has been selected. The company has been one of the top

hundred of the ASX listed companies. The report has started with the verification of the presence

of the qualitative features of the financial reporting with the help of the financial statements.

Along with the financial Statements of the company, the environment reporting has also been

verified and analyzed as to whether the company has been disclosing the information which will

be relevant for the investors. Then the adequacy of the disclosures made or information provided

have been checked in detail and thereon the recommendation has been provided to the

management in order to further increase the disclosure requirements. Then the detailed analysis

of the accounting of the pre acquisition transaction has been made with respect to clarification on

every part with respect to its accounting treatment and reasons for its differences. The report has

then ended with the appropriate conclusion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART A

DETAILS OF COMPANY SELECTED

For the purpose of making the study, the group has chosen the Woolworths Limited. The

company is registered in stock exchange of Australia and is one of the top hundred listed

companies. It has been founded in the year of 1920 and has its headquarters based in New South

Wales Australia. The company has been into the retail sector since its inception. The areas of the

business of the company has been into the chain of the departmental stores where every product

of the house can be purchase the items which are required for the running of the household, then

the company also have the liquor chains and the stores which supplies the fresh food and dairy

products. With the focus on the customer’s satisfaction, the company has been into the business

for the last so many years. For the purpose of analysis, the annual report for the year ending 2017

and 2016 has been selected (Woolworths Limited, 2017).

RELEVANCE AND COMPARABILITY

Although there are four features which enhance the quality of the financial reporting, but under

this section, two features will be discussed in relation to the annual report of the company. These

are as follows:

Relevance – It states that the information so disclosed in the annual report shall be relevant to the

stakeholders so that the accordingly decision can be made (Beyer, 2012). Thus, the information,

the omission of which will affect the decision of the users of the financial statements will be

referred as the relevant. As per the annual report of the company, the relevant information has

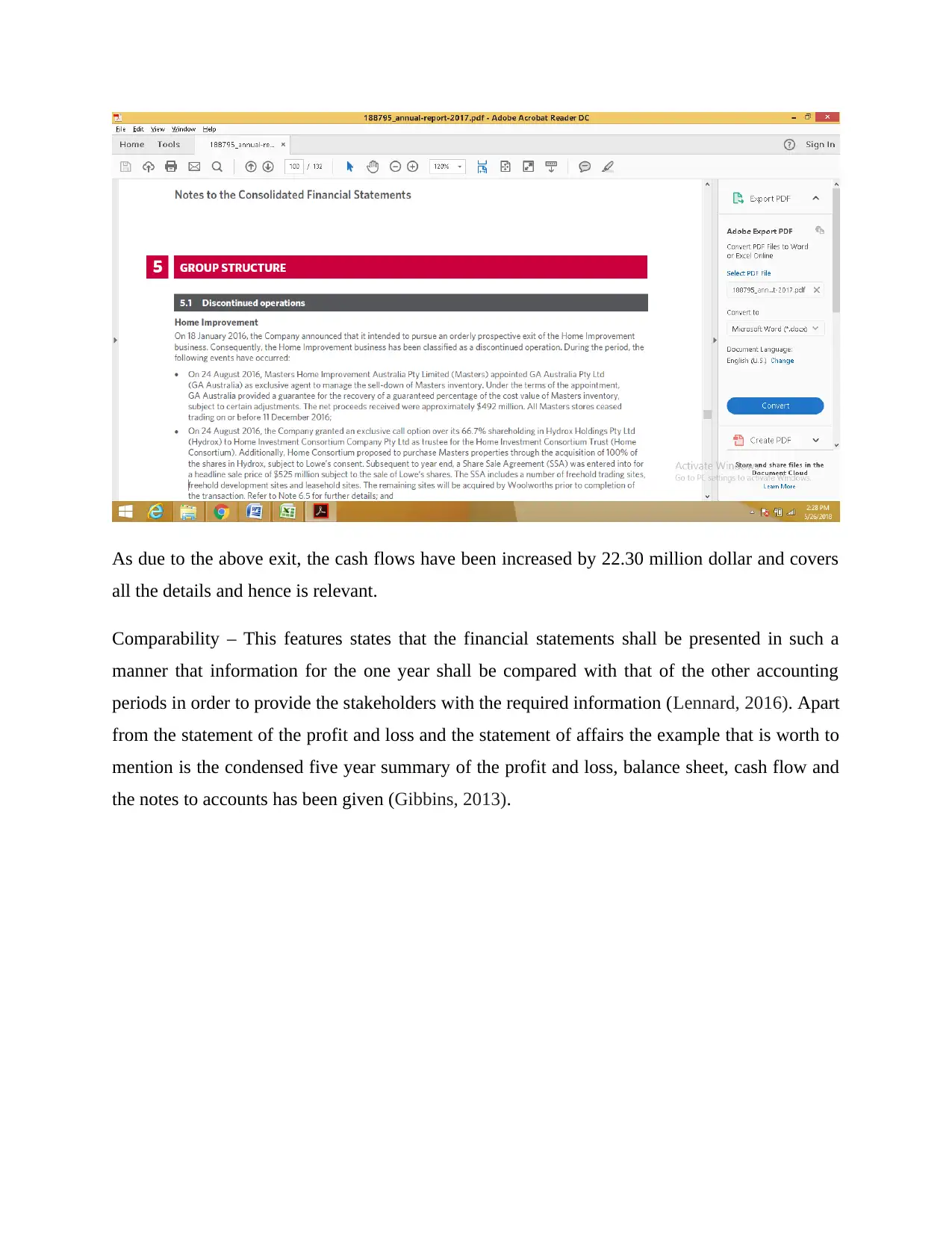

been the exit of Home Improvement business of the company (Schroeder, 2011). The company

has declared on the 18th of January 2016 that business of the home improvement shall be

discontinued in the future year and therefore, the same has been classified as the operation which

has been discontinued during the year. All the events that have happened in the series have been

detailed in the annual report as:

- Home Timber and the hardware group has been soled

- Then the inventory of the masters has been sold

- Payment of the amounts to the employees and settling the obligations

- The accounting treatment and the presentation of the transaction relating to the home

consortium.

DETAILS OF COMPANY SELECTED

For the purpose of making the study, the group has chosen the Woolworths Limited. The

company is registered in stock exchange of Australia and is one of the top hundred listed

companies. It has been founded in the year of 1920 and has its headquarters based in New South

Wales Australia. The company has been into the retail sector since its inception. The areas of the

business of the company has been into the chain of the departmental stores where every product

of the house can be purchase the items which are required for the running of the household, then

the company also have the liquor chains and the stores which supplies the fresh food and dairy

products. With the focus on the customer’s satisfaction, the company has been into the business

for the last so many years. For the purpose of analysis, the annual report for the year ending 2017

and 2016 has been selected (Woolworths Limited, 2017).

RELEVANCE AND COMPARABILITY

Although there are four features which enhance the quality of the financial reporting, but under

this section, two features will be discussed in relation to the annual report of the company. These

are as follows:

Relevance – It states that the information so disclosed in the annual report shall be relevant to the

stakeholders so that the accordingly decision can be made (Beyer, 2012). Thus, the information,

the omission of which will affect the decision of the users of the financial statements will be

referred as the relevant. As per the annual report of the company, the relevant information has

been the exit of Home Improvement business of the company (Schroeder, 2011). The company

has declared on the 18th of January 2016 that business of the home improvement shall be

discontinued in the future year and therefore, the same has been classified as the operation which

has been discontinued during the year. All the events that have happened in the series have been

detailed in the annual report as:

- Home Timber and the hardware group has been soled

- Then the inventory of the masters has been sold

- Payment of the amounts to the employees and settling the obligations

- The accounting treatment and the presentation of the transaction relating to the home

consortium.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As due to the above exit, the cash flows have been increased by 22.30 million dollar and covers

all the details and hence is relevant.

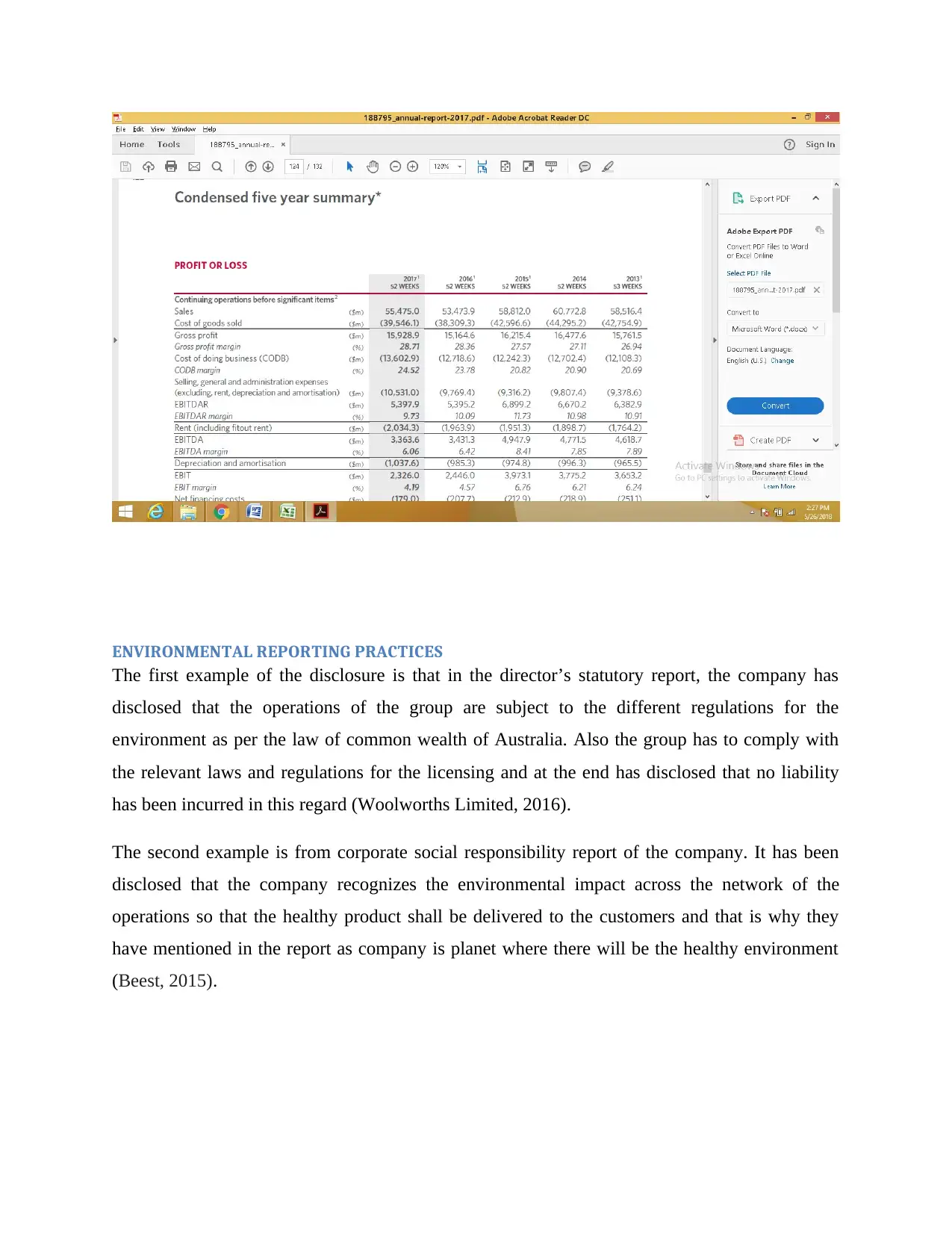

Comparability – This features states that the financial statements shall be presented in such a

manner that information for the one year shall be compared with that of the other accounting

periods in order to provide the stakeholders with the required information (Lennard, 2016). Apart

from the statement of the profit and loss and the statement of affairs the example that is worth to

mention is the condensed five year summary of the profit and loss, balance sheet, cash flow and

the notes to accounts has been given (Gibbins, 2013).

all the details and hence is relevant.

Comparability – This features states that the financial statements shall be presented in such a

manner that information for the one year shall be compared with that of the other accounting

periods in order to provide the stakeholders with the required information (Lennard, 2016). Apart

from the statement of the profit and loss and the statement of affairs the example that is worth to

mention is the condensed five year summary of the profit and loss, balance sheet, cash flow and

the notes to accounts has been given (Gibbins, 2013).

ENVIRONMENTAL REPORTING PRACTICES

The first example of the disclosure is that in the director’s statutory report, the company has

disclosed that the operations of the group are subject to the different regulations for the

environment as per the law of common wealth of Australia. Also the group has to comply with

the relevant laws and regulations for the licensing and at the end has disclosed that no liability

has been incurred in this regard (Woolworths Limited, 2016).

The second example is from corporate social responsibility report of the company. It has been

disclosed that the company recognizes the environmental impact across the network of the

operations so that the healthy product shall be delivered to the customers and that is why they

have mentioned in the report as company is planet where there will be the healthy environment

(Beest, 2015).

The first example of the disclosure is that in the director’s statutory report, the company has

disclosed that the operations of the group are subject to the different regulations for the

environment as per the law of common wealth of Australia. Also the group has to comply with

the relevant laws and regulations for the licensing and at the end has disclosed that no liability

has been incurred in this regard (Woolworths Limited, 2016).

The second example is from corporate social responsibility report of the company. It has been

disclosed that the company recognizes the environmental impact across the network of the

operations so that the healthy product shall be delivered to the customers and that is why they

have mentioned in the report as company is planet where there will be the healthy environment

(Beest, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADEQUACY OF INFORMATION AND DISCLOSURES

Yes, in our opinion, the information and the disclosures that the company has made is adequate

in accordance with the nature and size of the business of the company. The adequacy comes

from the end of the readers and the users of the financial statements of the company. If they are

satisfied then it will be said that the adequate information and disclosures have been made.

In the annual report following justifies that the disclosure is adequate:

- The major information regarding the exit of the Home improvement business and the

impairment charged on the Big W business has been disclosed in detail.

- The key audit matter has been disclosed in accordance with the ASA 701 which requires

the attention of the management as well as the users.

- Corporate social responsibility along with the disclosure of the corporate governance

principles and practices.

Impairment has been the area which in our opinion is not adequate as the future cash flows

estimation have not been detailed.

Yes, in our opinion, the information and the disclosures that the company has made is adequate

in accordance with the nature and size of the business of the company. The adequacy comes

from the end of the readers and the users of the financial statements of the company. If they are

satisfied then it will be said that the adequate information and disclosures have been made.

In the annual report following justifies that the disclosure is adequate:

- The major information regarding the exit of the Home improvement business and the

impairment charged on the Big W business has been disclosed in detail.

- The key audit matter has been disclosed in accordance with the ASA 701 which requires

the attention of the management as well as the users.

- Corporate social responsibility along with the disclosure of the corporate governance

principles and practices.

Impairment has been the area which in our opinion is not adequate as the future cash flows

estimation have not been detailed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RECOMMENDATION TO STRENGHTEN

It is recommended for the top management of the company to estimate the future cash flows in

the better manner with the proper and due care. Second recommendation is to provide the

disclosure of the reasons for the transaction like exit of the Home Improvement business.

PART B

No company is required to be selected for this part and hence it has been presented

independently. Under this part accounting discussion has been made with regard to the

consolidated financial statement as to how the same has been dealt with the following concepts.

PURPOSE OF PREACQUISTION ENTRIES

There are major four purposes for which the pre acquisition entries are made for the preparation

of the consolidated financial statements. These are:

- It helps in the prevention of the situation where the asset is required to be counted and it

has been read as twice wrongly. In other words, it avoids the counting of the same asset

twice.

- It helps in the prevention of the situation where the equity is required to be derived and it

has been read as twice wrongly. In other words, it avoids the counting of the equity twice.

- It helps the entity in accounting for the gain if any received on the bargain purchase

(Shizhong, 2014).

- It helps in the recognition of those assets and liabilities which has been acquired by the

entity in the course of the business combination and which has not been recognized by

the entities in the whole group separately.

DIVIDEND IN PREACQUISITON ENTRIES

If on the acquisition date, in the books of accounts of the subsidiary company, the dividend

payable has been existing then the same shall be considered in the preparation of the

consolidated financial statements only in the case where the share purchased are cum dividend.

It is recommended for the top management of the company to estimate the future cash flows in

the better manner with the proper and due care. Second recommendation is to provide the

disclosure of the reasons for the transaction like exit of the Home Improvement business.

PART B

No company is required to be selected for this part and hence it has been presented

independently. Under this part accounting discussion has been made with regard to the

consolidated financial statement as to how the same has been dealt with the following concepts.

PURPOSE OF PREACQUISTION ENTRIES

There are major four purposes for which the pre acquisition entries are made for the preparation

of the consolidated financial statements. These are:

- It helps in the prevention of the situation where the asset is required to be counted and it

has been read as twice wrongly. In other words, it avoids the counting of the same asset

twice.

- It helps in the prevention of the situation where the equity is required to be derived and it

has been read as twice wrongly. In other words, it avoids the counting of the equity twice.

- It helps the entity in accounting for the gain if any received on the bargain purchase

(Shizhong, 2014).

- It helps in the recognition of those assets and liabilities which has been acquired by the

entity in the course of the business combination and which has not been recognized by

the entities in the whole group separately.

DIVIDEND IN PREACQUISITON ENTRIES

If on the acquisition date, in the books of accounts of the subsidiary company, the dividend

payable has been existing then the same shall be considered in the preparation of the

consolidated financial statements only in the case where the share purchased are cum dividend.

Shares cum divided extends the right to receive the dividend immediately on the purchase of the

share that is in this the shares carries the dividend with him (Shalev, 2011). Thus, the acquirer

will receive the dividend on its purchase and the necessary treatment has been explained with the

example.

X Limited acquires all the shares of Z Limited for the amount of $100000. On the date of the

acquisition Z Limited has the following balances:

Cash Balance - $100000

Dividend payable - $5000

Share Capital - $95000

Now, the consideration amount of $100000 will be separated into two parts. First one will deal

with the amount of the dividend which will be received separately which is equal to $5000 and

the second one deal with the amount of consideration amounting to $95000. Therefore the pre

acquisition entry will be:

Share Capital Debit $95000

To Investment in Z Ltd $95000

As X Ltd has the asset of dividend receivable and the Z Ltd has the corresponding liability and

the balances are removed by passing the elimination entry by debiting the dividend payable and

crediting the dividend receivable by $5000.

DIVIDED – PRE AND POST

The acquisition date has been defined as the date on which the acquirer entity gains the control

over the other entity. It occurs when the acquiring entity transfers the amount of consideration to

other entity in lieu of the acquisition of the assets and liabilities (Holthausen, 2016)

Pre acquisition dividend is the amount of the dividend which will be received from the pre

acquisition of the profits and post acquisition dividend is the amount of the dividend which will

be received from the pre acquisition profits.

share that is in this the shares carries the dividend with him (Shalev, 2011). Thus, the acquirer

will receive the dividend on its purchase and the necessary treatment has been explained with the

example.

X Limited acquires all the shares of Z Limited for the amount of $100000. On the date of the

acquisition Z Limited has the following balances:

Cash Balance - $100000

Dividend payable - $5000

Share Capital - $95000

Now, the consideration amount of $100000 will be separated into two parts. First one will deal

with the amount of the dividend which will be received separately which is equal to $5000 and

the second one deal with the amount of consideration amounting to $95000. Therefore the pre

acquisition entry will be:

Share Capital Debit $95000

To Investment in Z Ltd $95000

As X Ltd has the asset of dividend receivable and the Z Ltd has the corresponding liability and

the balances are removed by passing the elimination entry by debiting the dividend payable and

crediting the dividend receivable by $5000.

DIVIDED – PRE AND POST

The acquisition date has been defined as the date on which the acquirer entity gains the control

over the other entity. It occurs when the acquiring entity transfers the amount of consideration to

other entity in lieu of the acquisition of the assets and liabilities (Holthausen, 2016)

Pre acquisition dividend is the amount of the dividend which will be received from the pre

acquisition of the profits and post acquisition dividend is the amount of the dividend which will

be received from the pre acquisition profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is necessary to differentiate between the two dividends because of the fact that the pre

acquisition dividend is deducted from the amount of the investment that the acquirer made and

the post acquisition dividend is credited as income in the statement of the profit and loss account.

EFFECT OF GOODWILL

Goodwill as recorded by the subsidiary in its record is very essential in pre acquisition entries

because of the following reasons:

- While arriving at the figure of the fair value of the assets and liabilities, some adjustment

come for unidentifiable assets known as goodwill which is required to calculate the

goodwill of the whole company group. In this case the pre acquisition entries will nullify

the effect of Business Combination Valuation Reserve which will treated as the equity of

pre acquisition.

- Secondly the recorded goodwill help the group to recognized that in the consolidated

financial statements and hence will be the part of the pre acquisition entries.

ADJUSTMENTS IN THE CONSOLIDATED FINANCIAL STATEMENTS

In accordance with the provision of the Australian Accounting Standard number three, all the

assets and the liabilities which are identifiable shall be measured at the fair value as it is

considered as the most relevant and valuable for the stakeholders of the company (Schipper,

2013). Although it also states that the cost shall be allocated of business combination but it does

not require in any manner the valuation of identifiable assets and liabilities at cost. The

consolidation consists of the assets which only recorded at fair value is the amount of the

goodwill. Fair values are kept as constant and the gain is recognized. In this manner, the

adjustments are required (Davis, 2012).

CONCLUSION

Every company is required to follow the qualitative features of the financial reporting and shall

be reflected from the financial report of the company. For the first section of the report dealing

acquisition dividend is deducted from the amount of the investment that the acquirer made and

the post acquisition dividend is credited as income in the statement of the profit and loss account.

EFFECT OF GOODWILL

Goodwill as recorded by the subsidiary in its record is very essential in pre acquisition entries

because of the following reasons:

- While arriving at the figure of the fair value of the assets and liabilities, some adjustment

come for unidentifiable assets known as goodwill which is required to calculate the

goodwill of the whole company group. In this case the pre acquisition entries will nullify

the effect of Business Combination Valuation Reserve which will treated as the equity of

pre acquisition.

- Secondly the recorded goodwill help the group to recognized that in the consolidated

financial statements and hence will be the part of the pre acquisition entries.

ADJUSTMENTS IN THE CONSOLIDATED FINANCIAL STATEMENTS

In accordance with the provision of the Australian Accounting Standard number three, all the

assets and the liabilities which are identifiable shall be measured at the fair value as it is

considered as the most relevant and valuable for the stakeholders of the company (Schipper,

2013). Although it also states that the cost shall be allocated of business combination but it does

not require in any manner the valuation of identifiable assets and liabilities at cost. The

consolidation consists of the assets which only recorded at fair value is the amount of the

goodwill. Fair values are kept as constant and the gain is recognized. In this manner, the

adjustments are required (Davis, 2012).

CONCLUSION

Every company is required to follow the qualitative features of the financial reporting and shall

be reflected from the financial report of the company. For the first section of the report dealing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with these features, the company – Woolworths Limited has been selected and it has been

identified that the company has been following the qualitative features of the financial reporting

and as well as in the environmental reporting. In the second section the consolidated financial

statements have been discussed with regard to the pre acquisition and how the same have been

done as per the mentioned five heads. In order to conclude the report, it has detailed the

importance of each and every item of the financial reporting and has been identified as useful for

the management and the stakeholders of the company.

LIST OF REFERENCES

Beyer, A., (2012), “The financial reporting environment: Review of the recent literature” Journal

of accounting and economics, 50(2), pp.296-343.

Beest, F.V, (2015), “Quality of Financial Reporting: measuring qualitative characteristics”,

Journal of Accounting Review”, 40 (2), pp 378-401.

Bushman, R.M., (2016), “Financial reporting incentives for conservative accounting: The

influence of legal and political institutions” Journal of Accounting and Economics, 42(1-2),

pp.107-148.

Davis, M., (2012), “Consolidated financial statements” The CPA journal, 78(2), p.26.

Gibbins, M., (2013), “Evidence about auditor–client management negotiation concerning client’s

financial reporting” Journal of Accounting Research, 39(3), pp.535-563.

Holthausen, R.W., (2013) “Testing the relative power of accounting standards versus incentives

and other institutional features to influence the outcome of financial reporting in an international

setting” Journal of Accounting and Economics, 36(1), pp.271-283.

Lennard, A., (2016), “Stewardship and the objectives of financial statements: a comment on

IASB's preliminary views on an improved conceptual framework for financial reporting: the

identified that the company has been following the qualitative features of the financial reporting

and as well as in the environmental reporting. In the second section the consolidated financial

statements have been discussed with regard to the pre acquisition and how the same have been

done as per the mentioned five heads. In order to conclude the report, it has detailed the

importance of each and every item of the financial reporting and has been identified as useful for

the management and the stakeholders of the company.

LIST OF REFERENCES

Beyer, A., (2012), “The financial reporting environment: Review of the recent literature” Journal

of accounting and economics, 50(2), pp.296-343.

Beest, F.V, (2015), “Quality of Financial Reporting: measuring qualitative characteristics”,

Journal of Accounting Review”, 40 (2), pp 378-401.

Bushman, R.M., (2016), “Financial reporting incentives for conservative accounting: The

influence of legal and political institutions” Journal of Accounting and Economics, 42(1-2),

pp.107-148.

Davis, M., (2012), “Consolidated financial statements” The CPA journal, 78(2), p.26.

Gibbins, M., (2013), “Evidence about auditor–client management negotiation concerning client’s

financial reporting” Journal of Accounting Research, 39(3), pp.535-563.

Holthausen, R.W., (2013) “Testing the relative power of accounting standards versus incentives

and other institutional features to influence the outcome of financial reporting in an international

setting” Journal of Accounting and Economics, 36(1), pp.271-283.

Lennard, A., (2016), “Stewardship and the objectives of financial statements: a comment on

IASB's preliminary views on an improved conceptual framework for financial reporting: the

objective of financial reporting and qualitative characteristics of decision-useful financial

reporting information” Accounting in Europe, 4(1), pp.51-66.

Schroeder, R.G., (2011), “Accounting: Theory and Analysi”. John Wiley & Sons.

Schipper, K., (2013), “Principles-based accounting standards. Accounting horizons, 17(1), pp.61-

72.

Shalev, R., (2011), “The information content of business combination disclosure level” The

Accounting Review, 84(1), pp.239-270.

Shizhong, H., (2014), “An Analysis of Economic Consequences of Accounting for Business

Combination”. Accounting Research, 8, p.006.

Woolworths Limited, (2017), “Annual Report 2017” available on

https://www.woolworths.com.au/ accessed on 25-05-2018.

Woolworths Limited, (2016), “Annual Report 2016” available on

https://www.woolworths.com.au/ accessed on 25-05-2018.

reporting information” Accounting in Europe, 4(1), pp.51-66.

Schroeder, R.G., (2011), “Accounting: Theory and Analysi”. John Wiley & Sons.

Schipper, K., (2013), “Principles-based accounting standards. Accounting horizons, 17(1), pp.61-

72.

Shalev, R., (2011), “The information content of business combination disclosure level” The

Accounting Review, 84(1), pp.239-270.

Shizhong, H., (2014), “An Analysis of Economic Consequences of Accounting for Business

Combination”. Accounting Research, 8, p.006.

Woolworths Limited, (2017), “Annual Report 2017” available on

https://www.woolworths.com.au/ accessed on 25-05-2018.

Woolworths Limited, (2016), “Annual Report 2016” available on

https://www.woolworths.com.au/ accessed on 25-05-2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.