Financial Statements and Newsletter Report for Winter Limited Analysis

VerifiedAdded on 2020/03/01

|7

|793

|39

Report

AI Summary

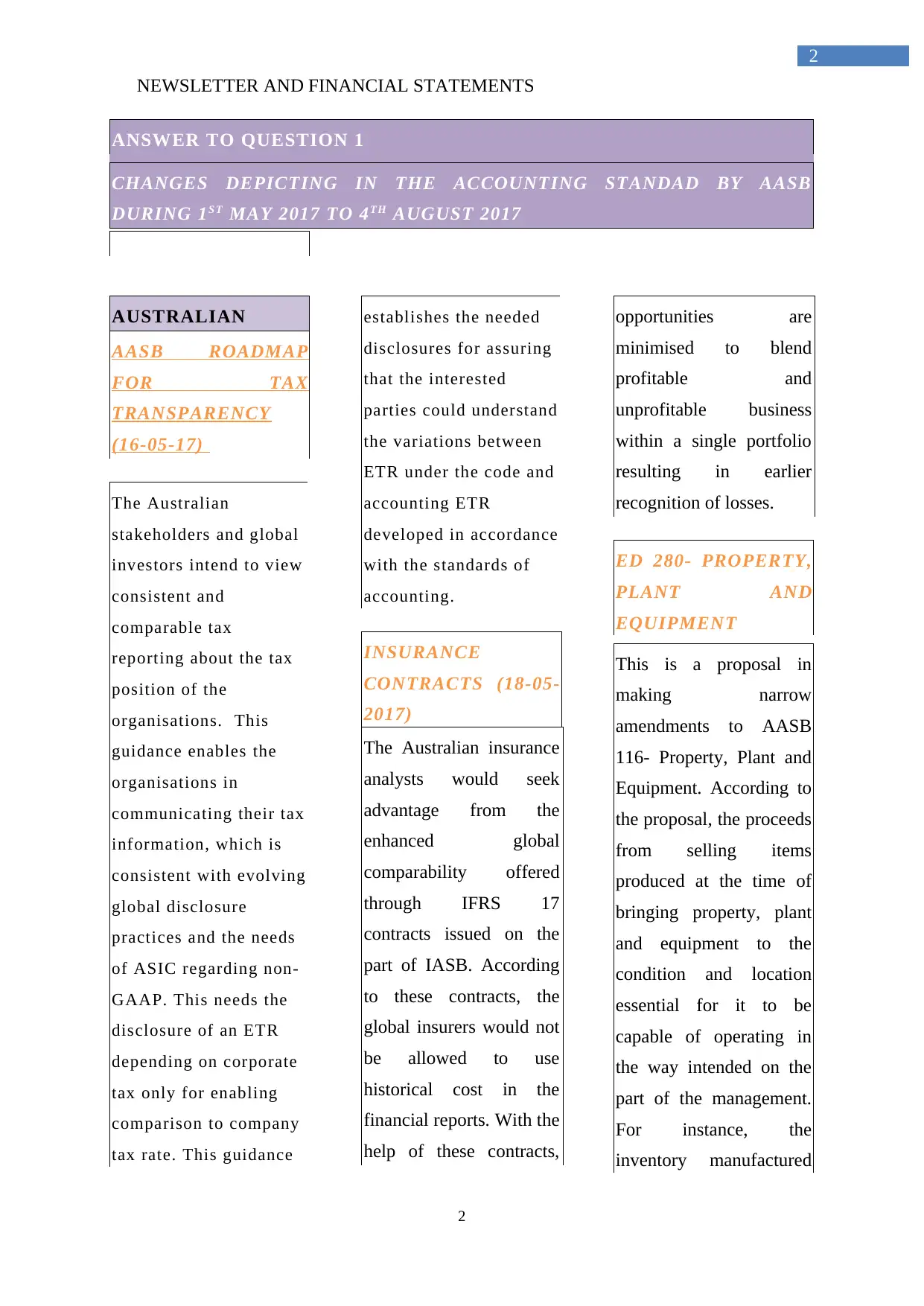

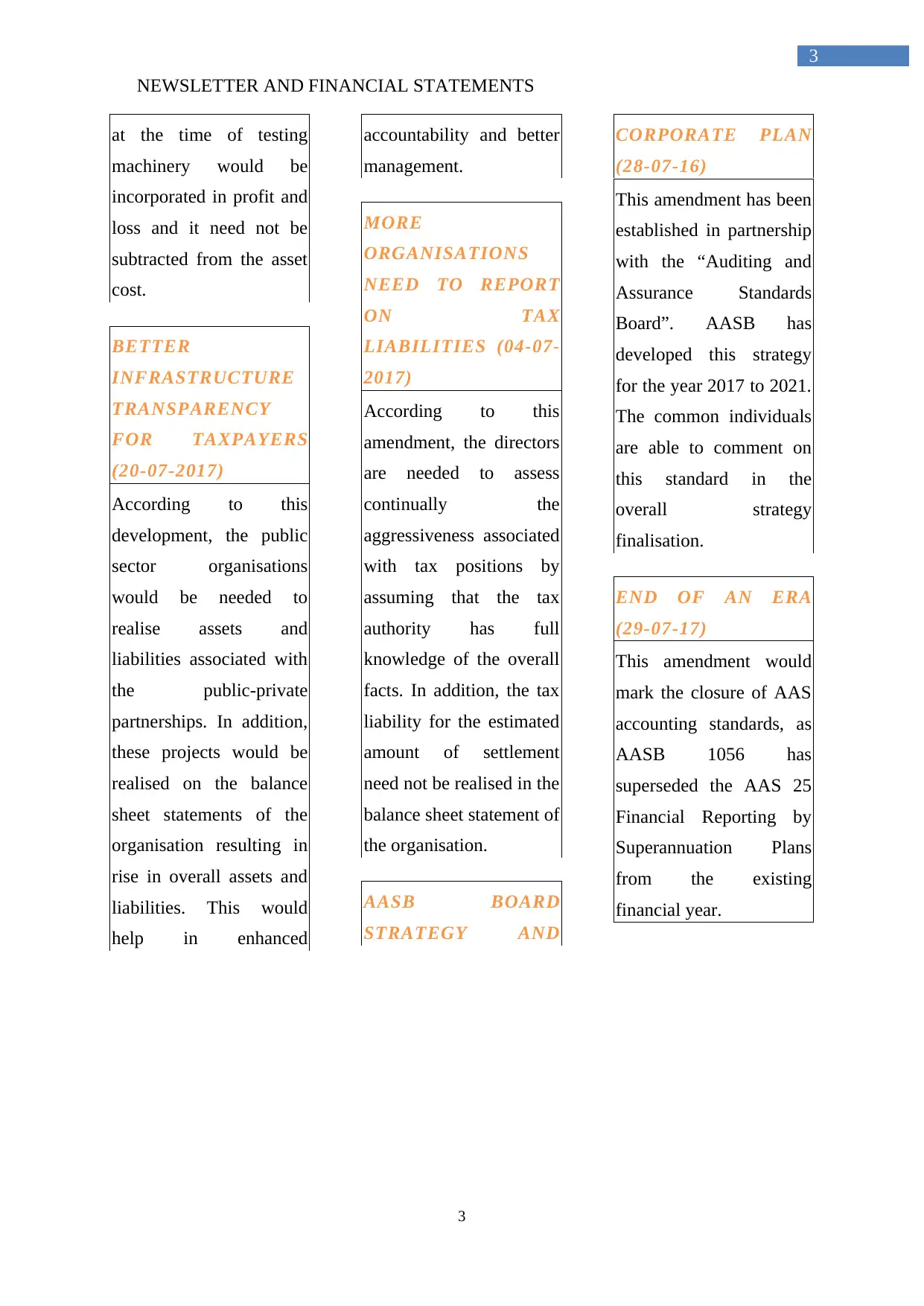

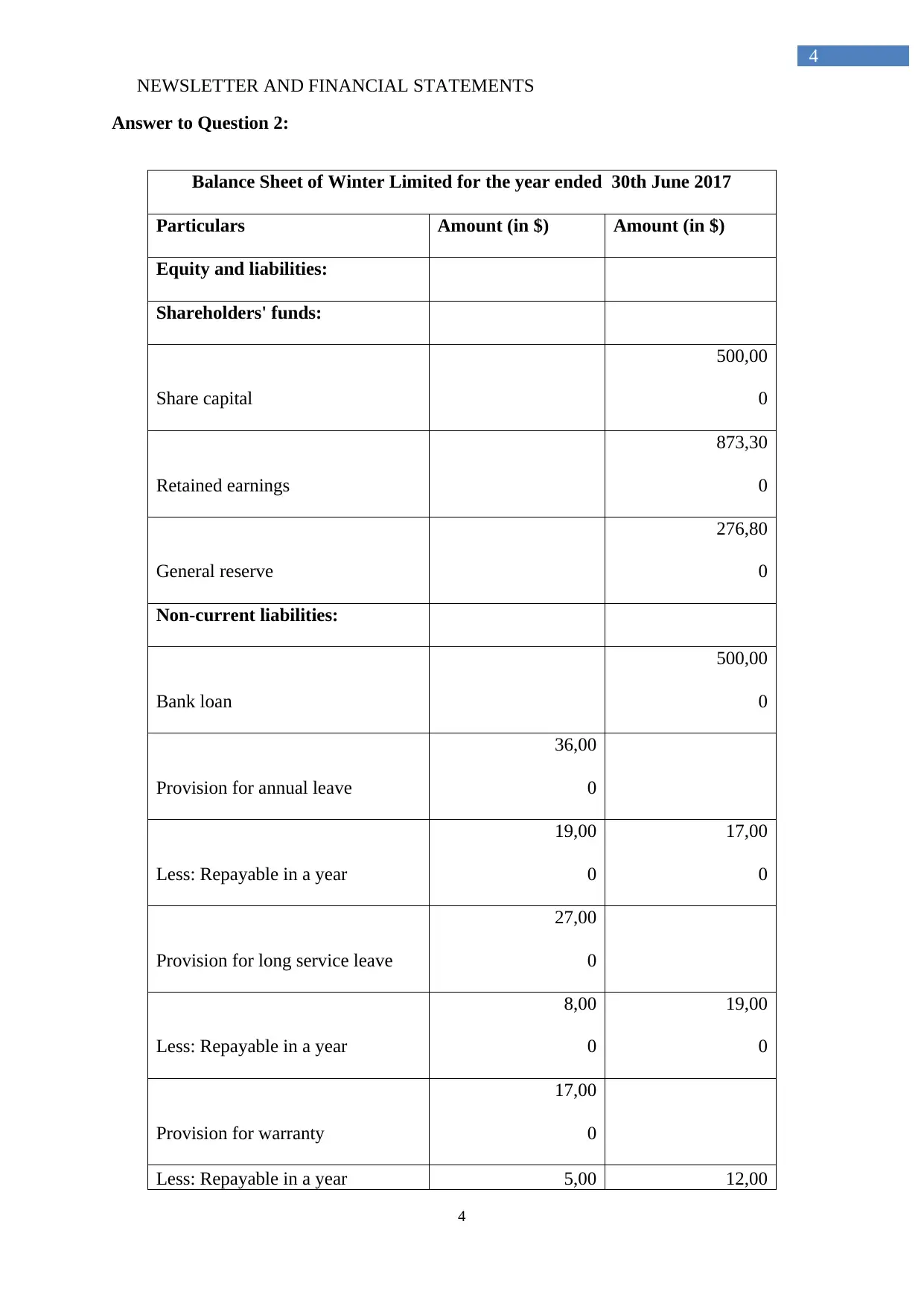

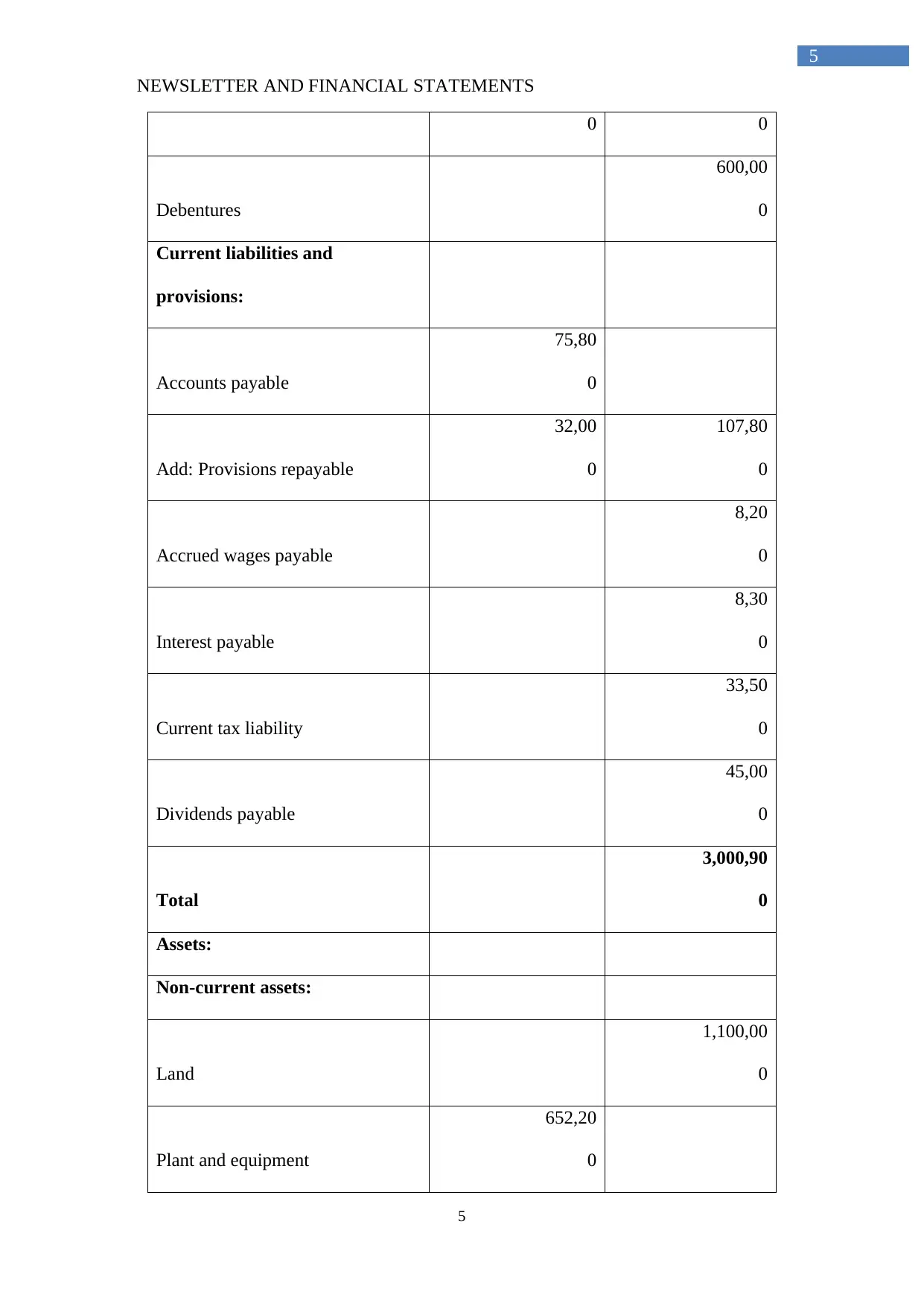

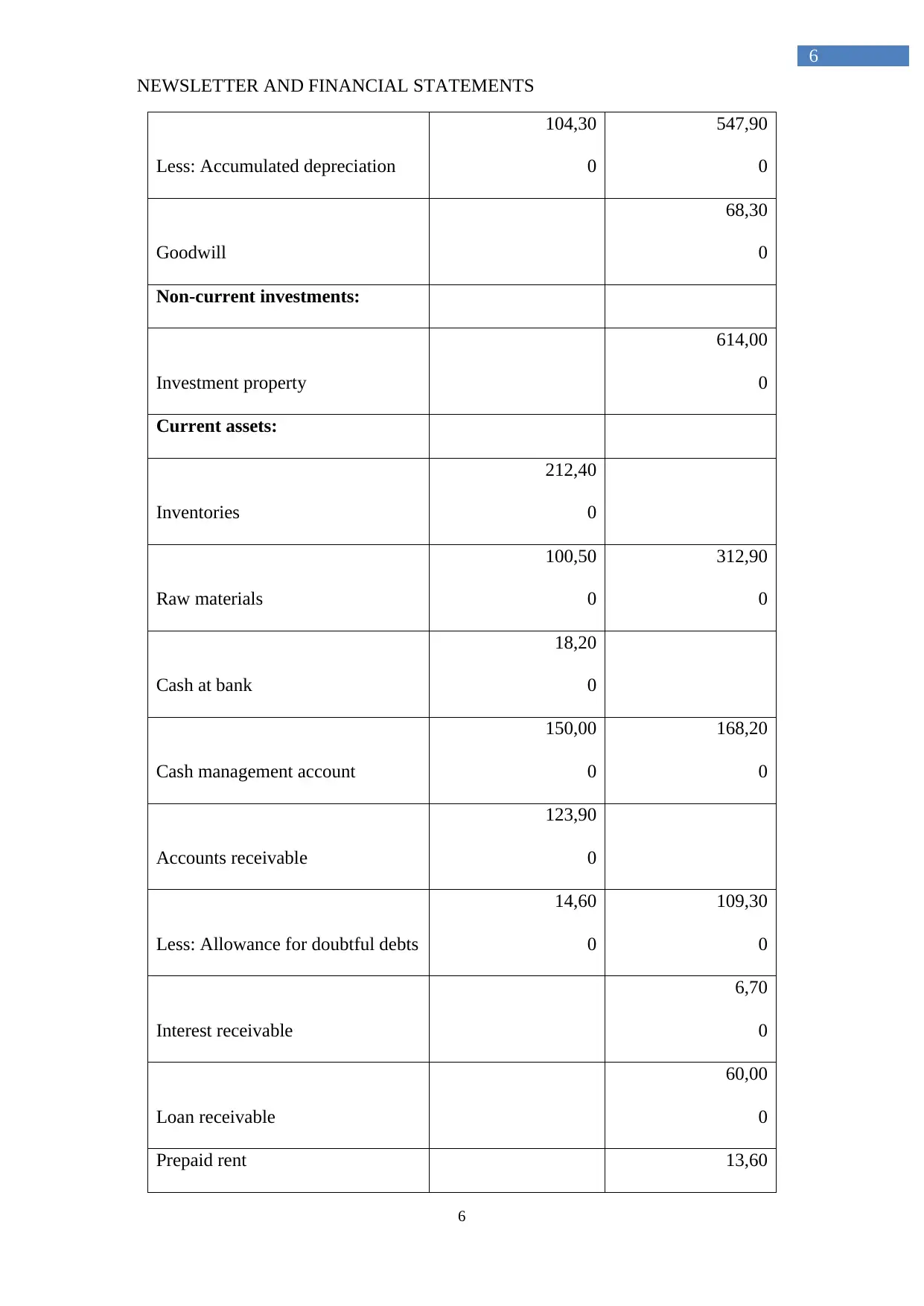

This report analyzes the financial statements and newsletter of Winter Limited, focusing on changes in accounting standards by AASB between May 2017 and August 2017. It provides an overview of the Australian AASB roadmap for tax transparency, insurance contracts, property, plant, and equipment, infrastructure transparency, and tax liability reporting. The report includes Winter Limited's balance sheet as of June 30, 2017, detailing equity, liabilities, and assets. Assets include land, plant and equipment, goodwill, investment property, inventories, cash, and accounts receivable. Liabilities encompass share capital, retained earnings, bank loans, provisions, debentures, accounts payable, accrued wages, interest, tax, and dividends. The document concludes with a bibliography of cited sources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.