STAT6003: Financial Statistics Analysis of Market Prices

VerifiedAdded on 2023/03/20

|11

|1785

|97

Report

AI Summary

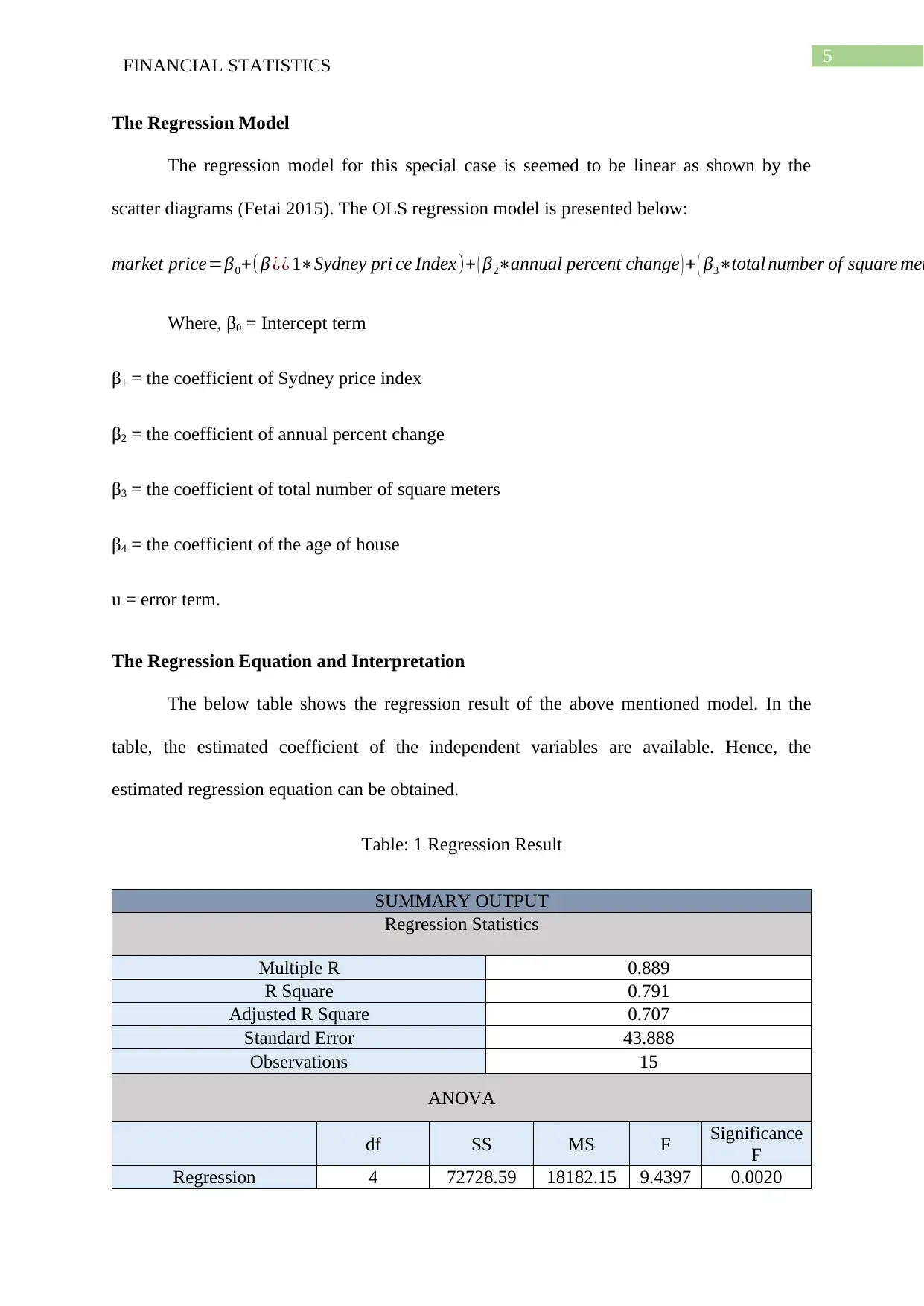

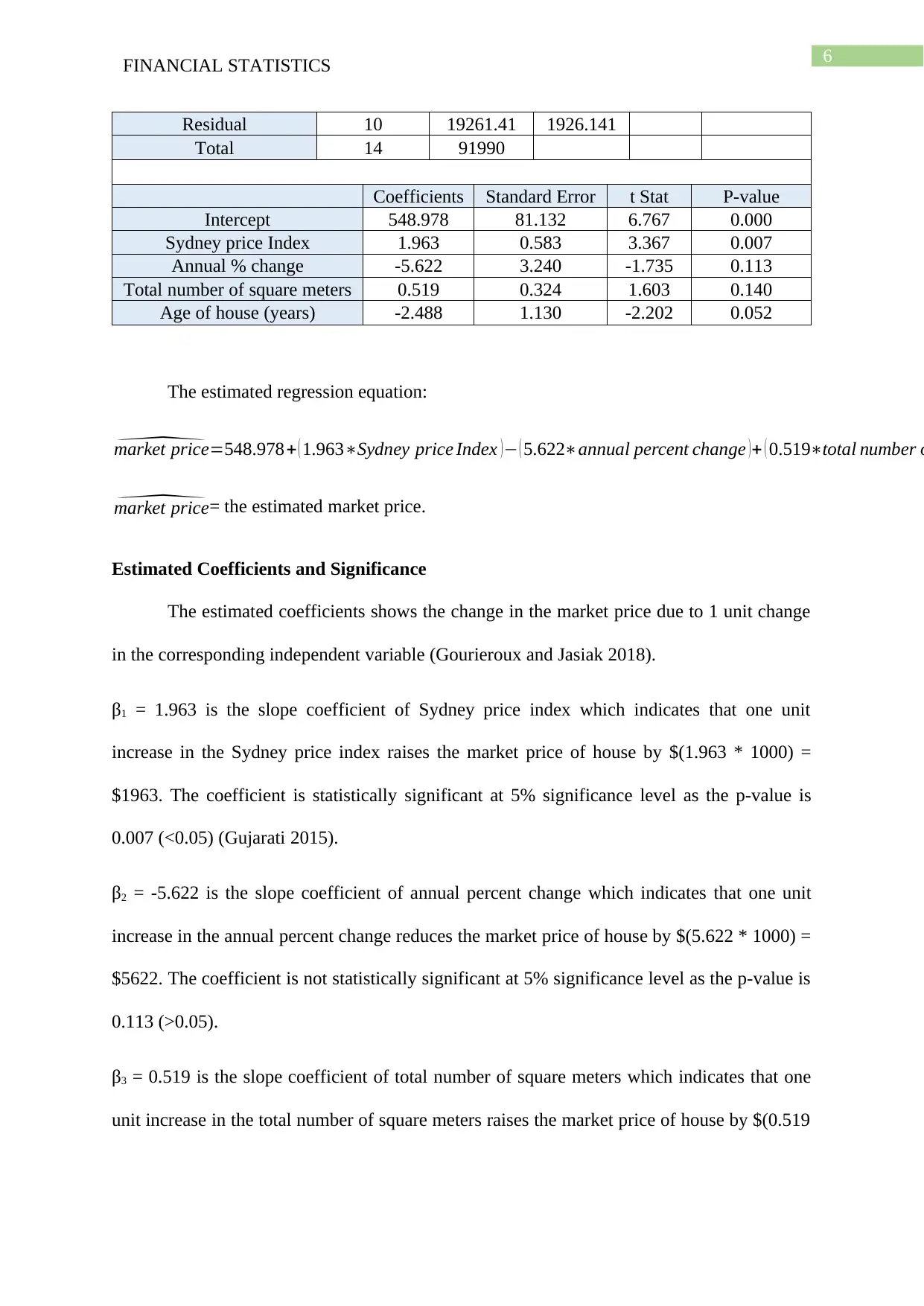

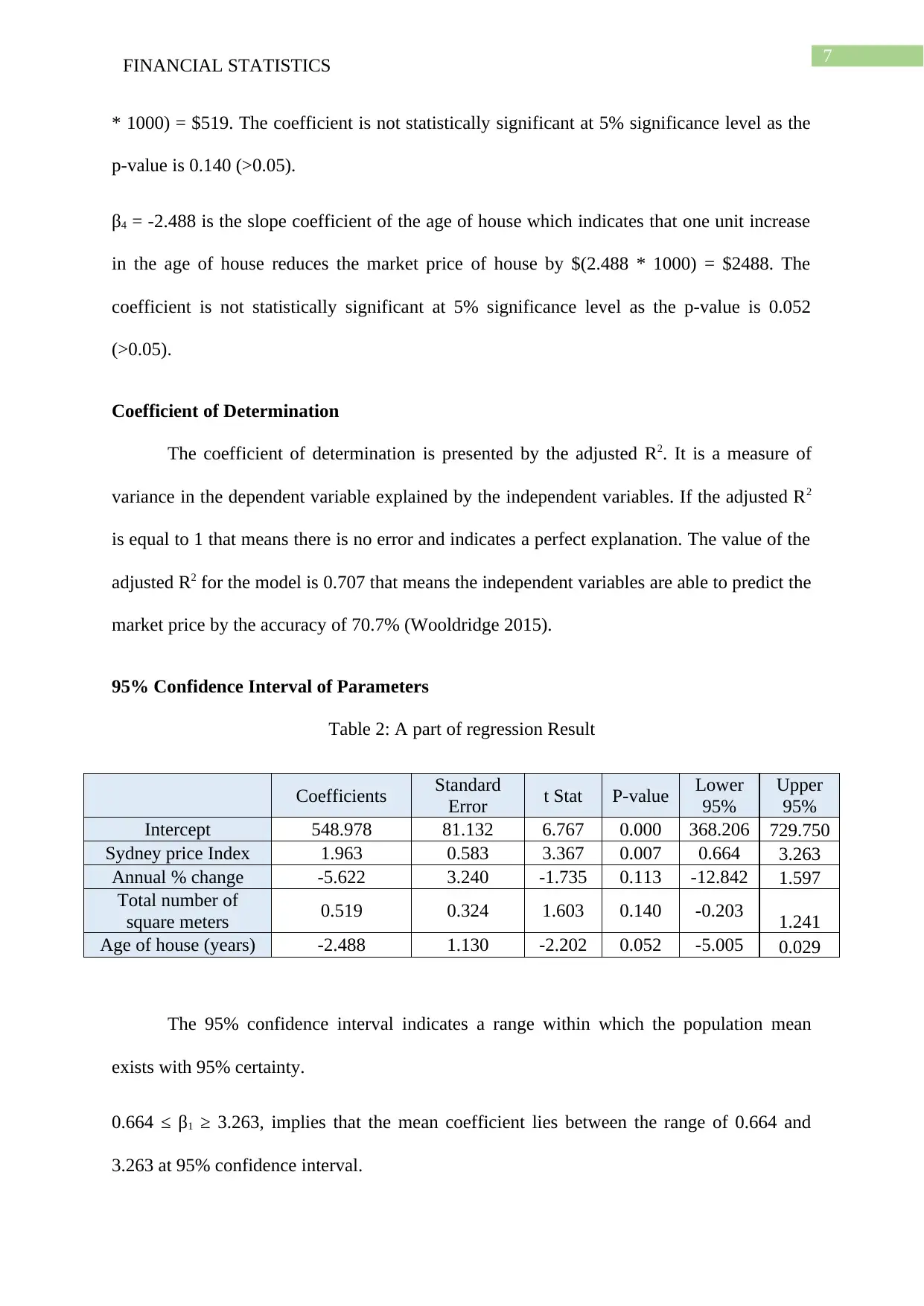

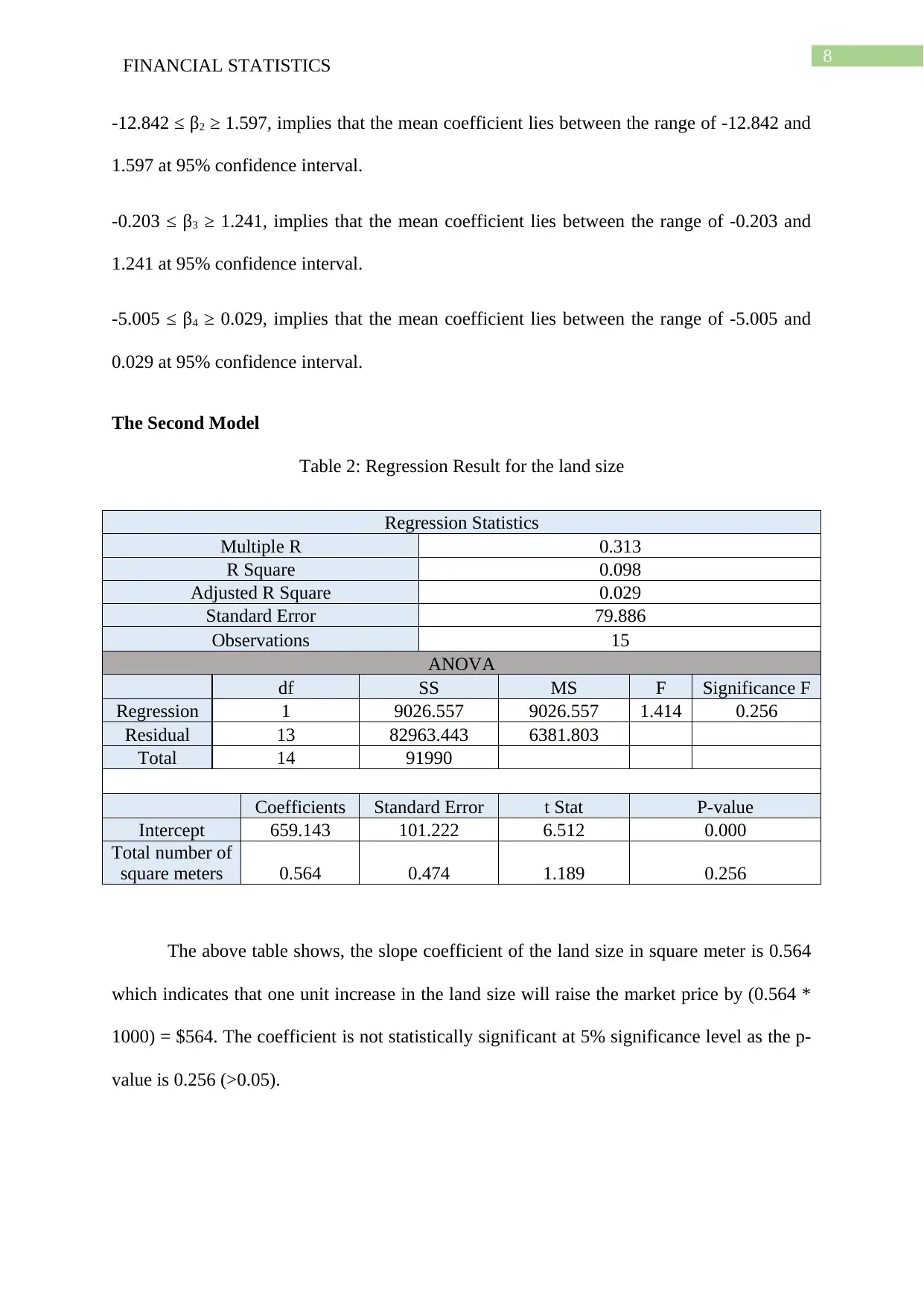

This report presents a financial statistics analysis, focusing on the relationship between market price and various economic indicators using data from 2002-2017. The analysis employs Ordinary Least Squares (OLS) regression and scatter plots to examine the influence of the Sydney Price Index, annual percentage change, total number of square meters, and age of the house on market price. The report includes the development of regression models, interpretation of coefficients, and assessment of statistical significance. The findings reveal positive correlations between market price and both the Sydney Price Index and the total number of square meters, while a negative correlation is observed with the age of the house. The report also provides a comparison between a multivariate regression model and a linear regression model, offering insights into their predictive capabilities. The report concludes with an estimated market price for a specific land size and includes relevant references.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.