Business and Finance: Statistical Analysis of Boeing, IBM, and S&P 500

VerifiedAdded on 2020/03/28

|14

|1904

|30

Homework Assignment

AI Summary

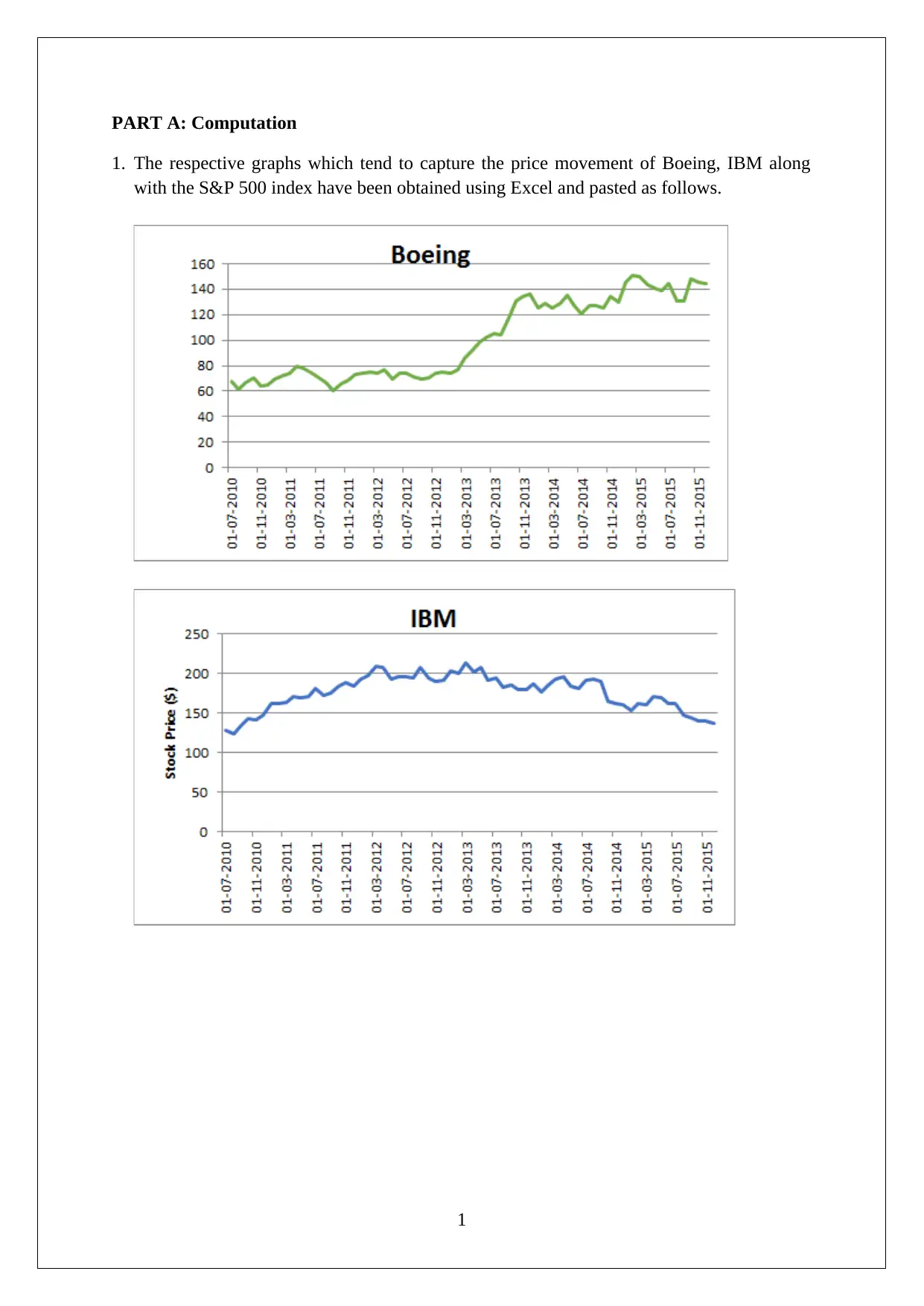

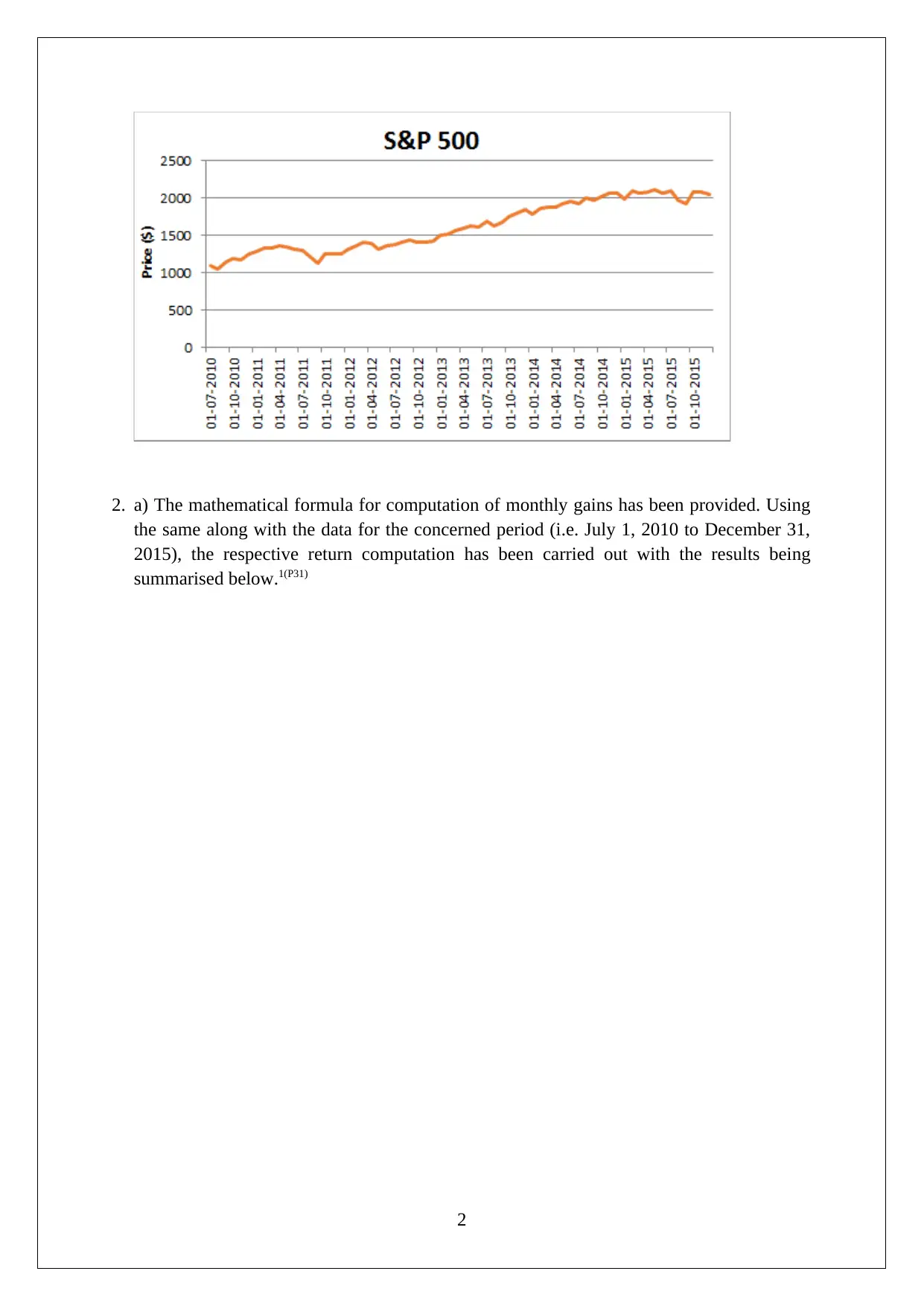

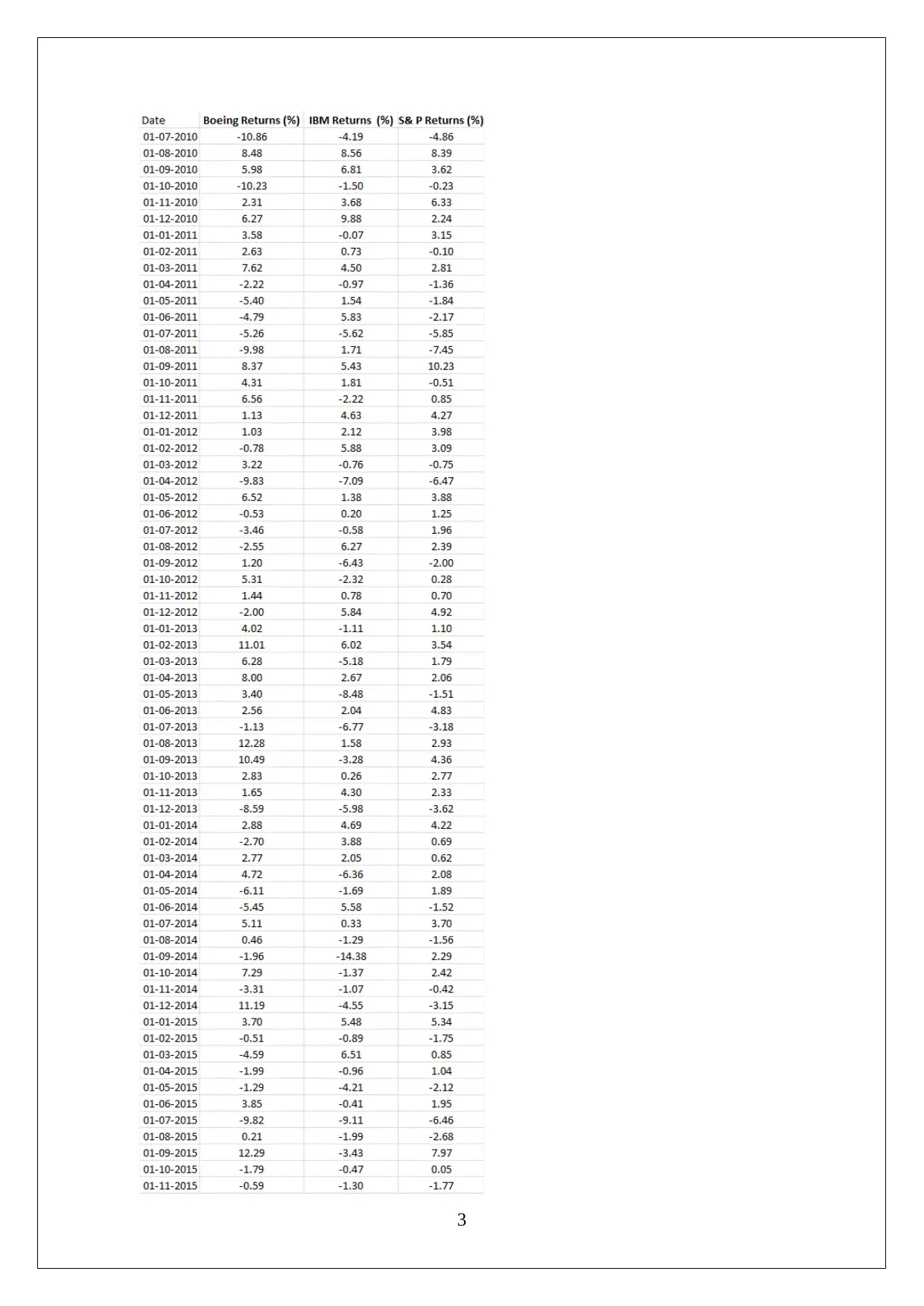

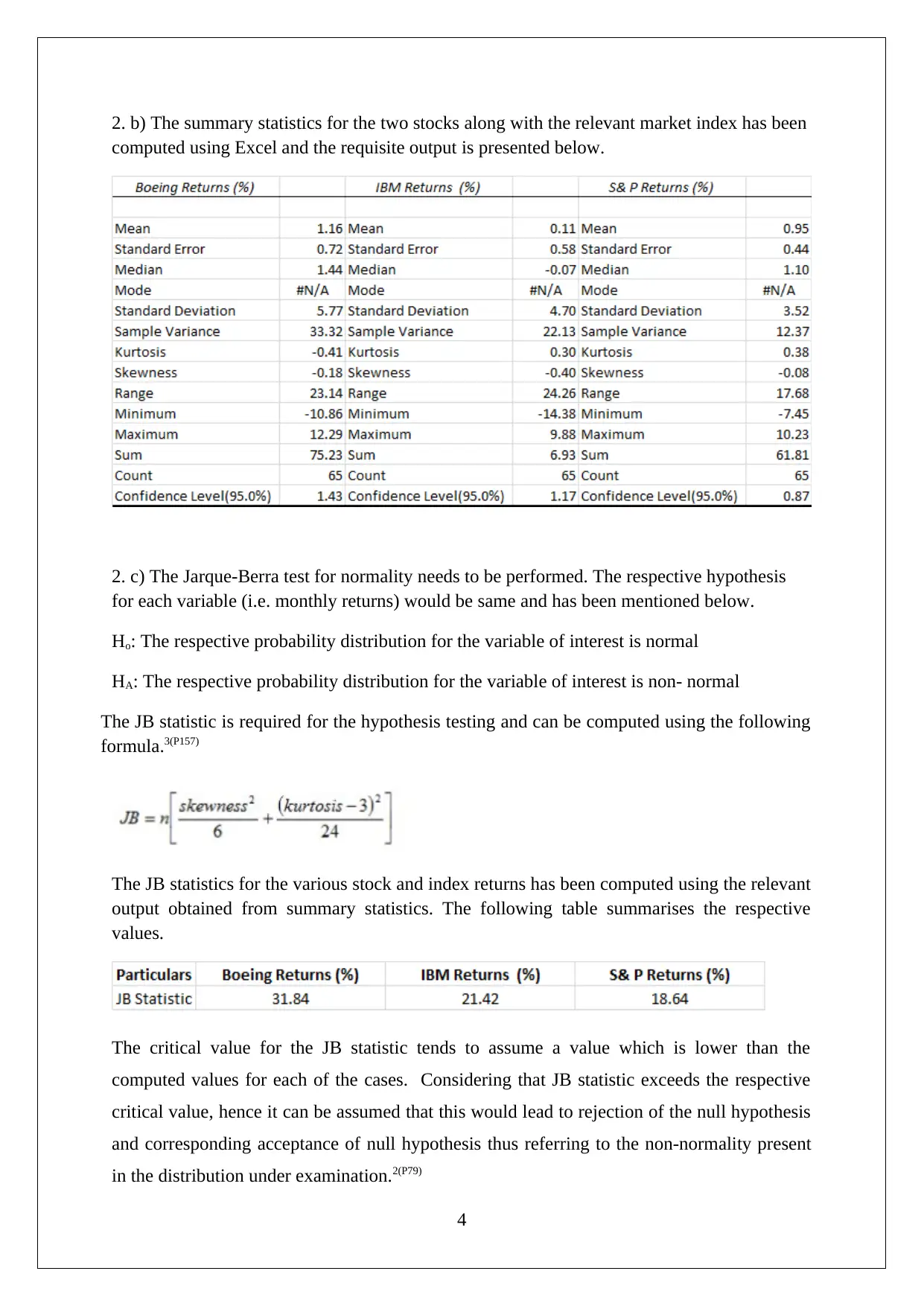

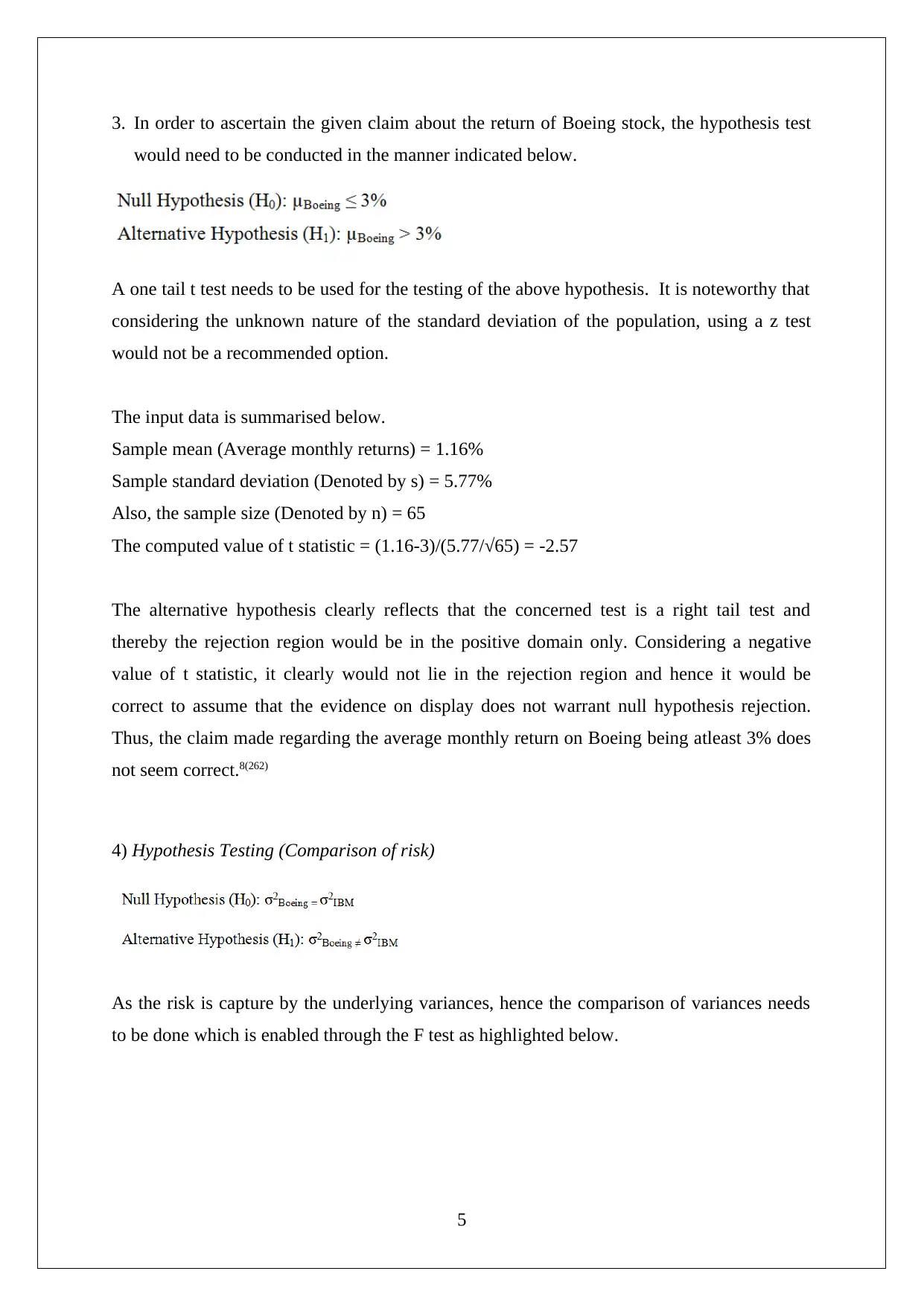

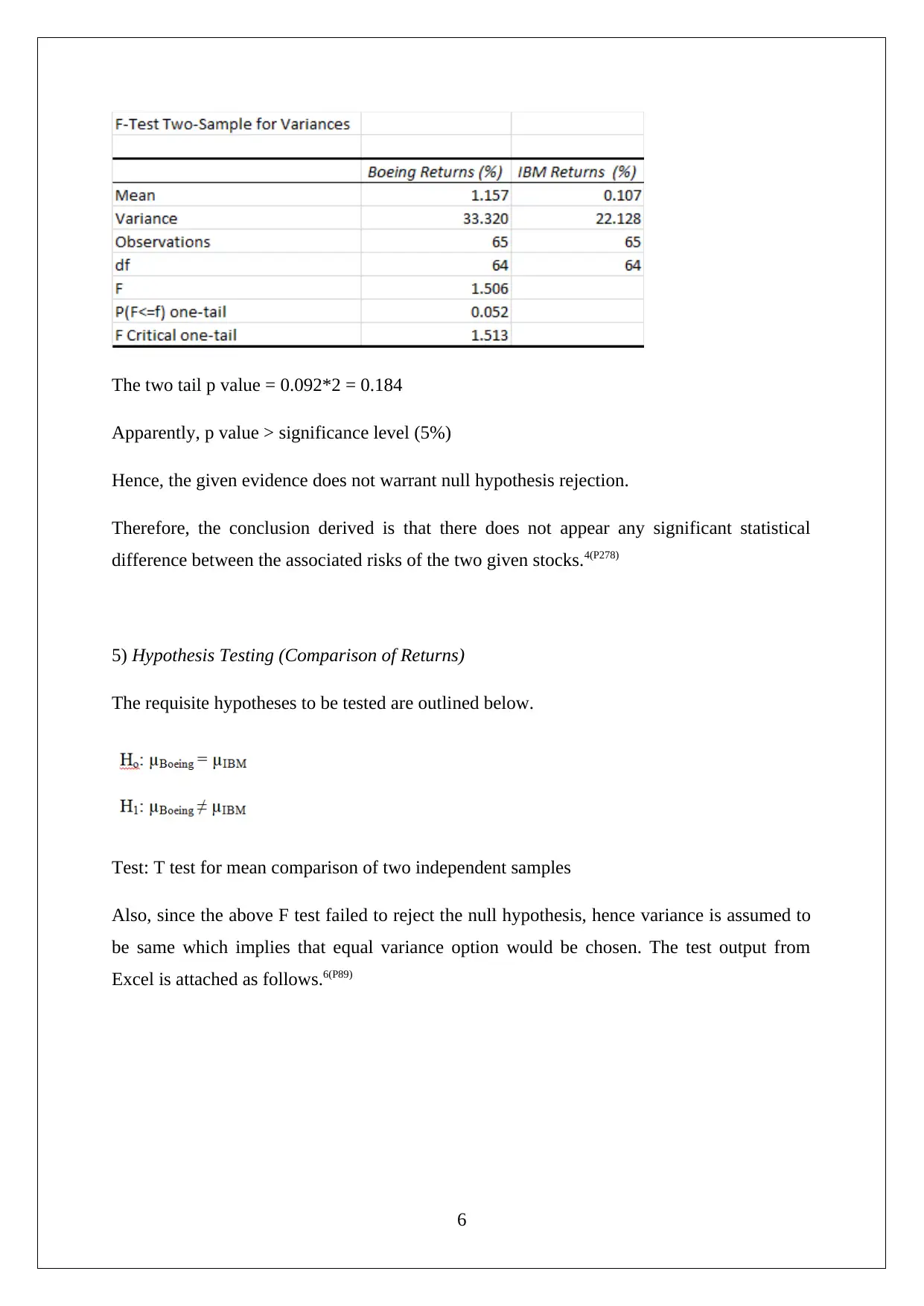

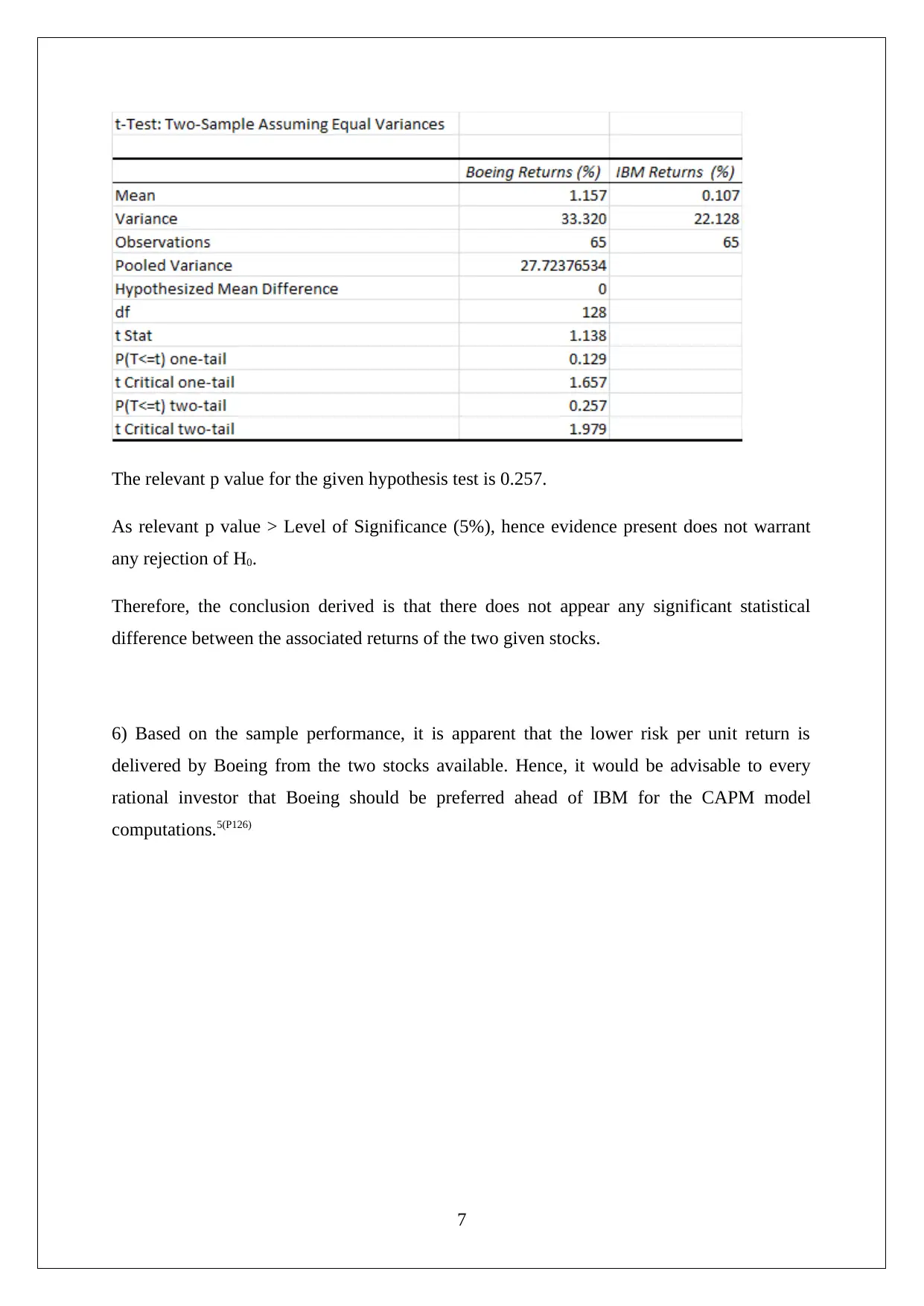

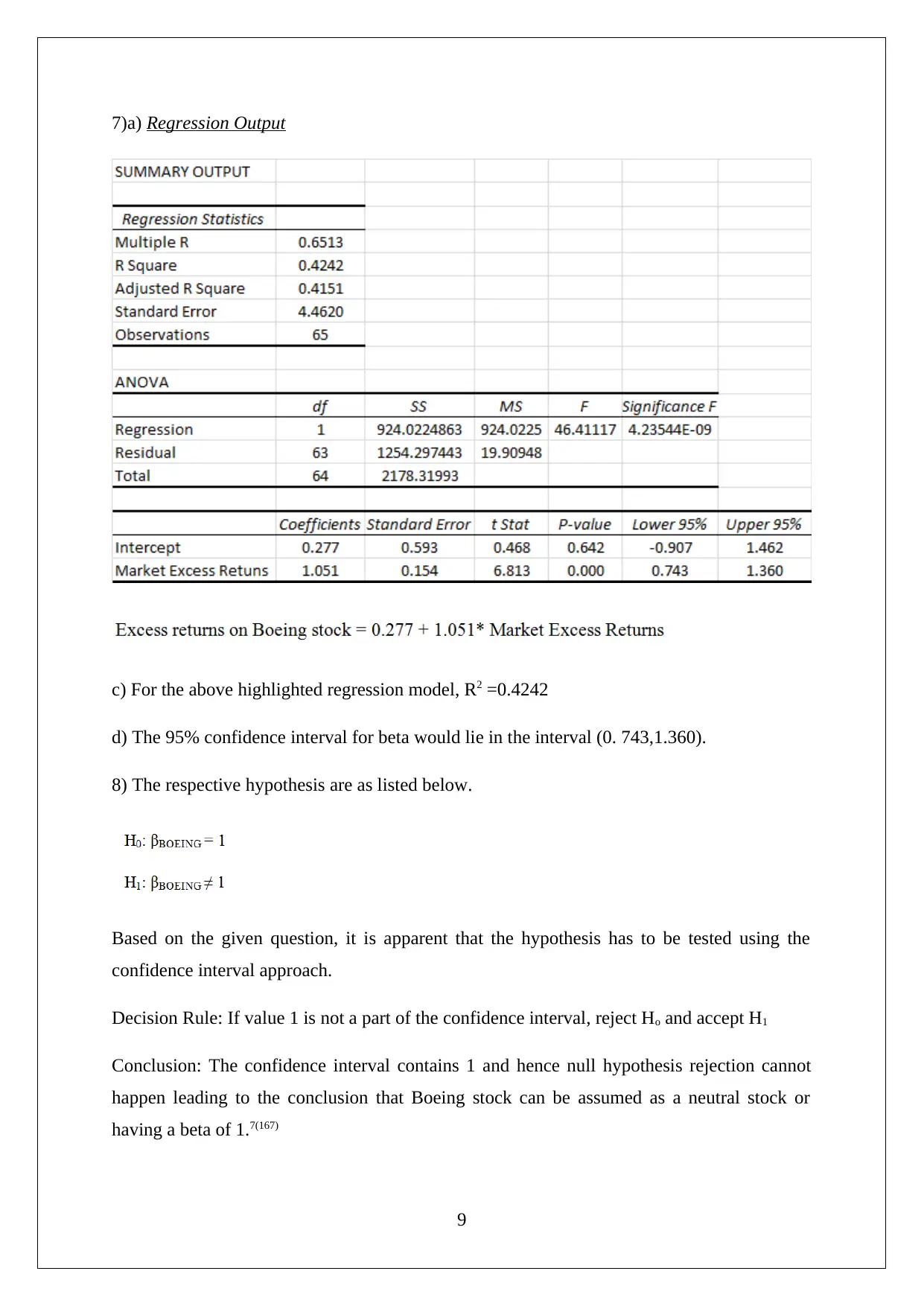

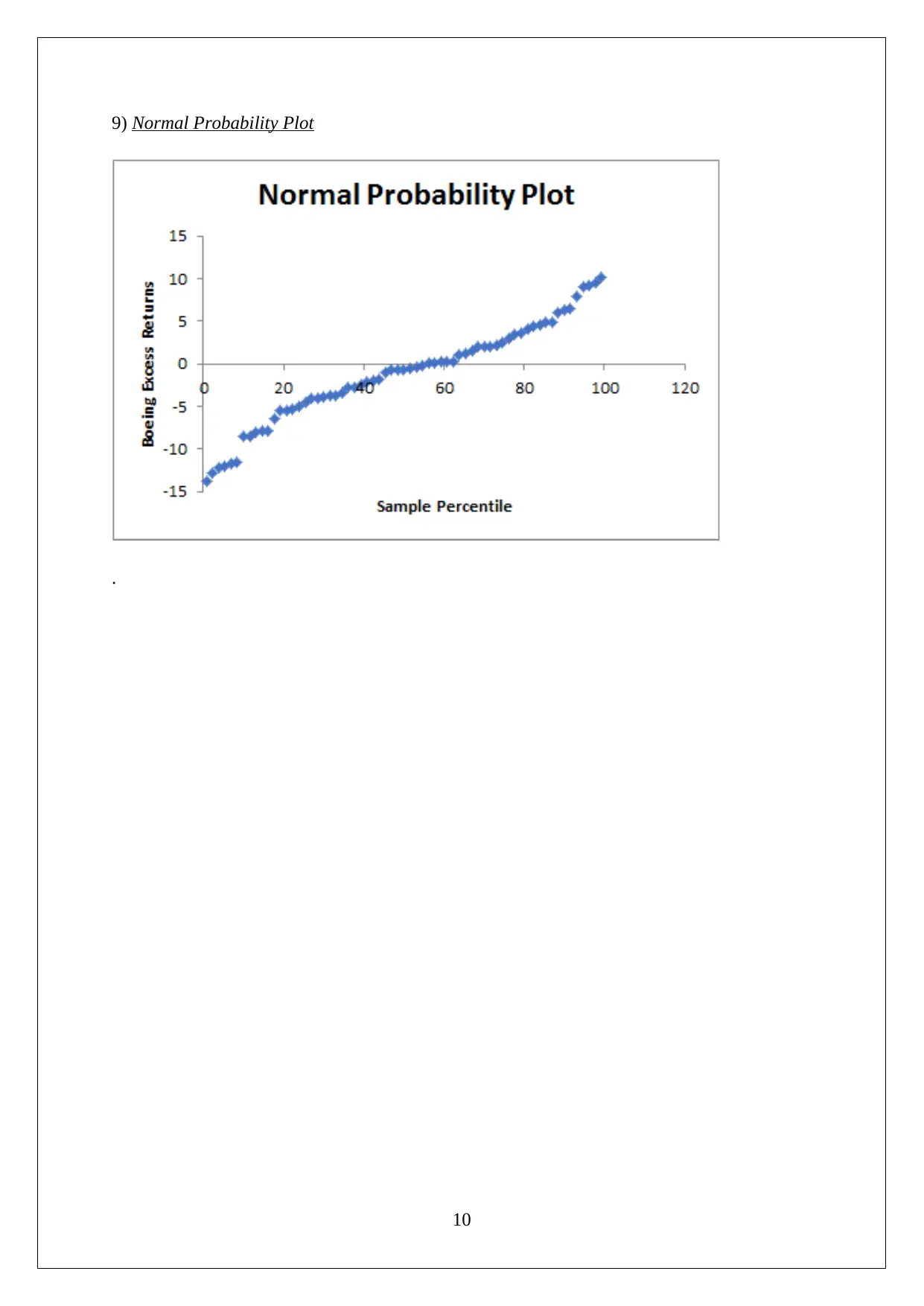

This assignment provides a comprehensive statistical analysis of Boeing and IBM stocks, along with the S&P 500 index, covering the period from July 2010 to December 2015. It includes the computation of monthly gains, summary statistics, and hypothesis testing for normality using the Jarque-Berra test. The assignment conducts t-tests to assess claims about Boeing's returns and F-tests to compare the risks associated with the two stocks. It further compares returns using t-tests, evaluates stock performance for investment decisions, and applies the CAPM model, including beta analysis and regression output interpretation. The document also provides an interpretation of stock movements over time, assesses risk and return characteristics, and analyzes the model's explanatory power through R2. Finally, it examines the normality of error terms via probability plots and draws conclusions on stock performance and investment suitability based on the statistical findings.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.