Management Accounting Report: R.L. Maynard's Financial Strategies

VerifiedAdded on 2020/01/16

|22

|5316

|195

Report

AI Summary

This report delves into the core concepts of management accounting, examining its role in internal decision-making and financial strategy. The analysis begins with an overview of management accounting, differentiating it from financial accounting and highlighting its importance for internal stakeholders, particularly for a company like R.L. Maynard. The report then explores various management accounting systems, including financial accounting, cost accounting, job costing, batch costing, inventory management, price optimization, traditional cost accounting, throughput accounting, transfer pricing, and lean accounting. Furthermore, the report discusses different management accounting reporting methods such as sales reports, cost accounting reports, and budgetary reports. The report also includes a detailed examination of cost analysis techniques, focusing on the preparation of income statements using both marginal and absorption costing methods. Finally, the report investigates the advantages and disadvantages of different planning tools used for budgetary control and compares how organizations adapt their management accounting systems to respond to financial problems, providing a comprehensive overview of management accounting principles and practices.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation on management accounting and give essential requirements of different types

of management accounting.........................................................................................................1

P2 Explain different methods used for management accounting reporting................................4

TASK 2............................................................................................................................................5

P3 Calculate cost using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption cost............................................................................5

TASK 3............................................................................................................................................9

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control........................................................................................................................9

P5 Compare how organisation are adapting management accounting system to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explanation on management accounting and give essential requirements of different types

of management accounting.........................................................................................................1

P2 Explain different methods used for management accounting reporting................................4

TASK 2............................................................................................................................................5

P3 Calculate cost using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption cost............................................................................5

TASK 3............................................................................................................................................9

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control........................................................................................................................9

P5 Compare how organisation are adapting management accounting system to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

ILLUSTRATION INDEX

Illustration 1: Income statement using marginal costing method....................................................6

Illustration 2: Income statement using absorption costing method.................................................7

Illustration 1: Income statement using marginal costing method....................................................6

Illustration 2: Income statement using absorption costing method.................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is differed from financial accounting as it is used by the

management for the purpose of make prediction regard to future. It is used by the internal

stakeholders for which they can easily make their day to day operations so, that business function

run smoothly. The research project in the context of R.L. Maynard it runs their business with 50

employees and earn annual profit that is less than the £500,000. In this project report there is

mainly discussion on the management accounting and its essential that needed in the

management accounting system (Pipan and Czarniawska, 2010). Furthermore, there is an also

study on the different management accounting system such as lean accounting, cost accounting,

traditional cost accounting and throughput accounting that are mainly used in responding

financial problem. Thereafter, in the project there is a discussion on different costing method that

are used at the time of ascertained of income statement. The cost is identified with both costing

techniques are marginal and absorption costing. In ending portion there is also study on the

management accounting reporting techniques are the job costing reporting, sales report, budget

report and also cost accounting etc.

TASK 1

P1 Explanation on management accounting and give essential requirements of different types of

management accounting

Management accounting include information relating to financial as well as statistical to

the business managers that assist them to take day-to-day decision for the organisation. It can be

said that it is a short-term decision regard to managerial. Therefore, it is totally differed from

financial accounting as it is used for internal stakeholder that are really opposed to external

affairs stakeholder. The reports are generated periodically such as weekly, monthly for the each

department managers as well as chief executive officer (Burritt, Schaltegger and Zvezdov,

2011). The detail information include in it are the sale revenues, cash inflow, bills payable and

receivable and sales revenue etc. Thus, it is totally different from financial accounting in which

the information used for the purpose of making future decisions. The R.L. Maynard used

management accounting for internal used only and it gives essential requirement of various types

that are as follows-

1

Management accounting is differed from financial accounting as it is used by the

management for the purpose of make prediction regard to future. It is used by the internal

stakeholders for which they can easily make their day to day operations so, that business function

run smoothly. The research project in the context of R.L. Maynard it runs their business with 50

employees and earn annual profit that is less than the £500,000. In this project report there is

mainly discussion on the management accounting and its essential that needed in the

management accounting system (Pipan and Czarniawska, 2010). Furthermore, there is an also

study on the different management accounting system such as lean accounting, cost accounting,

traditional cost accounting and throughput accounting that are mainly used in responding

financial problem. Thereafter, in the project there is a discussion on different costing method that

are used at the time of ascertained of income statement. The cost is identified with both costing

techniques are marginal and absorption costing. In ending portion there is also study on the

management accounting reporting techniques are the job costing reporting, sales report, budget

report and also cost accounting etc.

TASK 1

P1 Explanation on management accounting and give essential requirements of different types of

management accounting

Management accounting include information relating to financial as well as statistical to

the business managers that assist them to take day-to-day decision for the organisation. It can be

said that it is a short-term decision regard to managerial. Therefore, it is totally differed from

financial accounting as it is used for internal stakeholder that are really opposed to external

affairs stakeholder. The reports are generated periodically such as weekly, monthly for the each

department managers as well as chief executive officer (Burritt, Schaltegger and Zvezdov,

2011). The detail information include in it are the sale revenues, cash inflow, bills payable and

receivable and sales revenue etc. Thus, it is totally different from financial accounting in which

the information used for the purpose of making future decisions. The R.L. Maynard used

management accounting for internal used only and it gives essential requirement of various types

that are as follows-

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting system: Under this management accounting system, all financial

records of the organisation are identified such as profit and loss account, income

statement, cash and fund flow etc. Therefore, actual economic position of R.L. Maynard

is determined on which further decisions are made regarding profitability in the future

time (Shah, Malik and Malik, 2011). Moreover, it is also helpful for optimum allocation

of funds and further business operations more efficiently. Therefore, management of fund

can be done appropriately affect profit earning capability other business operations.

Cost accounting system: It is one of the essential tool for cost effectiveness and

increasing sales revenue of R.L. Maynard. However, different ideas are generated for

reducing expenses and enhancing selling of products. Thus, cost accounting system is

beneficial for effective price determination and adequate expenses on business operations

(Zimmerman and Yahya-Zadeh, 2011).

Job costing system: Under this system, expenses on menufacturing of products is

maintained affect further business operations and decision making on price

determination. In this regard, cost incurred on purchasing raw materials, labour and

additional overhead is set for business operations and proper management of entire

business activities efficiently.

Batch costing system: In costing system, cost incurred on production and distribution of

goods and services is identified for expenses on business operations. It affects

productivity and profitability of R.L. Maynard and its market position (Elbashir, Collier

and Sutton, 2011). Therefore, batch costing system remain efficient for effective pricing

and monetary management of the enterprise systematically.

Inventory management system: Management accountant of R.L. Maynard analyses

inventories and their management position affect liquidity position of entity. Therefore,

optimum utilization of resources and fund is possible by using this tool for further

business operations efficiently (Zimmerman and Yahya-Zadeh, 2011).

Price optimization system: This management accounting system is beneficial at most

for optimization of price and economic management of R.L. Maynard properly.

Therefore, decisions are made regarding cost incurred on different business operations

and planning for further years effectively (Garrison and et.al., 2010).

2

records of the organisation are identified such as profit and loss account, income

statement, cash and fund flow etc. Therefore, actual economic position of R.L. Maynard

is determined on which further decisions are made regarding profitability in the future

time (Shah, Malik and Malik, 2011). Moreover, it is also helpful for optimum allocation

of funds and further business operations more efficiently. Therefore, management of fund

can be done appropriately affect profit earning capability other business operations.

Cost accounting system: It is one of the essential tool for cost effectiveness and

increasing sales revenue of R.L. Maynard. However, different ideas are generated for

reducing expenses and enhancing selling of products. Thus, cost accounting system is

beneficial for effective price determination and adequate expenses on business operations

(Zimmerman and Yahya-Zadeh, 2011).

Job costing system: Under this system, expenses on menufacturing of products is

maintained affect further business operations and decision making on price

determination. In this regard, cost incurred on purchasing raw materials, labour and

additional overhead is set for business operations and proper management of entire

business activities efficiently.

Batch costing system: In costing system, cost incurred on production and distribution of

goods and services is identified for expenses on business operations. It affects

productivity and profitability of R.L. Maynard and its market position (Elbashir, Collier

and Sutton, 2011). Therefore, batch costing system remain efficient for effective pricing

and monetary management of the enterprise systematically.

Inventory management system: Management accountant of R.L. Maynard analyses

inventories and their management position affect liquidity position of entity. Therefore,

optimum utilization of resources and fund is possible by using this tool for further

business operations efficiently (Zimmerman and Yahya-Zadeh, 2011).

Price optimization system: This management accounting system is beneficial at most

for optimization of price and economic management of R.L. Maynard properly.

Therefore, decisions are made regarding cost incurred on different business operations

and planning for further years effectively (Garrison and et.al., 2010).

2

Traditional cost accounting- It can be define as a allocation of manufacturing expenses

which are incur in production process. The another name of this is a conventional method that

are assigning the factory's indirect expensed to the each items manufactured based upon the

production such as direct labour hours, number of units produced and production machine hours

etc. Thus, this method fail to assign the non-manufacturing expensed which are concern with

production items like administration overhead. The traditional cost accounting are used for the

external financial reports as it deliver cost of good sold value. The main advantage of these

accounting for the R.L. Maynard is that it can easily implement which gives one product.

Whereas, due to advancement of computer and machines this system in now outdated.

Throughput accounting- It is just simply accounting that are based upon the principle

on theory of constraints ( TOC). It is the most useful for the management for growth purpose and

decisions making process becomes simpler and its is to understandable for the people within the

organisation. It is totally different from the traditional cost accounting as the main aim is that to

maximize profit instead of minimize unit cost. The main advantage of throughput accounting is

to make managerial decisions that are growth-oriented. It also allows them to make report faster

and assist individuals in operations to know the basic accounting.

Transfer pricing- There is a set of rules of regulation that are formulated when any

organisation transfer any kind of movable and immovable goods or services across another

countries. Therefore, in the management accounting system in which there is a transaction to

another at that time transfer pricing is used to measure the cost. Thus, these prices are slightly

differ from market price as on of the entities like losses' transaction. It can be said in another

words in which they either purchase for higher than prevailing MP or selling at low market price

which directly impact on company performance. The rules that are formulated on transfer pricing

that are ensured business entities' fairness as well as accuracy. Therefore, in the financial

reporting document of an organisation which are closely monitored that useful at for the auditors

as well as regulators. Thus, it has an advantage is that it can be used by company to measure

performance of divisions.

Lean accounting- It is used by company to know the information on timely,

understandable and accurately etc. Therefore, it makes decisions faster that directly leads to

enhance customer value and profitability etc. The lean tools assist them to minimize the wastages

3

which are incur in production process. The another name of this is a conventional method that

are assigning the factory's indirect expensed to the each items manufactured based upon the

production such as direct labour hours, number of units produced and production machine hours

etc. Thus, this method fail to assign the non-manufacturing expensed which are concern with

production items like administration overhead. The traditional cost accounting are used for the

external financial reports as it deliver cost of good sold value. The main advantage of these

accounting for the R.L. Maynard is that it can easily implement which gives one product.

Whereas, due to advancement of computer and machines this system in now outdated.

Throughput accounting- It is just simply accounting that are based upon the principle

on theory of constraints ( TOC). It is the most useful for the management for growth purpose and

decisions making process becomes simpler and its is to understandable for the people within the

organisation. It is totally different from the traditional cost accounting as the main aim is that to

maximize profit instead of minimize unit cost. The main advantage of throughput accounting is

to make managerial decisions that are growth-oriented. It also allows them to make report faster

and assist individuals in operations to know the basic accounting.

Transfer pricing- There is a set of rules of regulation that are formulated when any

organisation transfer any kind of movable and immovable goods or services across another

countries. Therefore, in the management accounting system in which there is a transaction to

another at that time transfer pricing is used to measure the cost. Thus, these prices are slightly

differ from market price as on of the entities like losses' transaction. It can be said in another

words in which they either purchase for higher than prevailing MP or selling at low market price

which directly impact on company performance. The rules that are formulated on transfer pricing

that are ensured business entities' fairness as well as accuracy. Therefore, in the financial

reporting document of an organisation which are closely monitored that useful at for the auditors

as well as regulators. Thus, it has an advantage is that it can be used by company to measure

performance of divisions.

Lean accounting- It is used by company to know the information on timely,

understandable and accurately etc. Therefore, it makes decisions faster that directly leads to

enhance customer value and profitability etc. The lean tools assist them to minimize the wastages

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

through financial control. Thus, the data give the accurate timely information which are used by

sales people. Accountants, operations leader and improvement team etc. It does not needed the

complex system and transaction that are wasteful.

P2 Explain different methods used for management accounting reporting

There are various type of Management accounting reporting that are used by R.L.

Maynard that are discussed below-

Sales report- Company record all this information that are related to sales of products or

services during a particular time period. It includes sales volume and expenses that are

incurred in selling as well as selling products. The sales report is used by company

manager for the purpose of check the salesperson performance in which it shows the time

spending in a sales activity. Apart from this, it also aids organisation for the purpose of

measuring company financial performance by comparing with the previous sales profit.

There is an also data include in sales report are the customer meeting, e-mails,

conversation, outbound calls and product demonstrate that are mainly generating in

daily, weekly and monthly basis. There are many purposes that are used by R.L. Maynard

is for the purpose of determining revenue for the future time period and also know the

growth opportunities to expand business.

Cost accounting- It is that type of accounting in which there is recording, allocating,

collecting, analysing, classifying and evaluating used for the purpose of taking action to

control cost. It is used by management to make a most appropriate action on the

capability and cost efficiency(Burritt, Schaltegger and Zvezdov, 2011). It involve a

detailed information regard to cost through management control it current operations so,

they can easily make a plan for future. The usage of cost accounting is that to determine

the cost of process, products and project etc. for the purpose of reporting the actual and

accurate amount of financial statements. Thus, it also helps the management in decision-

making, planning and controlling the organisation. Furthermore, it is also helpful in

computing the operational and capital budgeting, variance analysis, transfer pricing,

standard costing and activity based costing etc.

Budgetary report- The management used budget report to make comparison the actual

performance number attain over a some timing period. It is a kind of internal report that

4

sales people. Accountants, operations leader and improvement team etc. It does not needed the

complex system and transaction that are wasteful.

P2 Explain different methods used for management accounting reporting

There are various type of Management accounting reporting that are used by R.L.

Maynard that are discussed below-

Sales report- Company record all this information that are related to sales of products or

services during a particular time period. It includes sales volume and expenses that are

incurred in selling as well as selling products. The sales report is used by company

manager for the purpose of check the salesperson performance in which it shows the time

spending in a sales activity. Apart from this, it also aids organisation for the purpose of

measuring company financial performance by comparing with the previous sales profit.

There is an also data include in sales report are the customer meeting, e-mails,

conversation, outbound calls and product demonstrate that are mainly generating in

daily, weekly and monthly basis. There are many purposes that are used by R.L. Maynard

is for the purpose of determining revenue for the future time period and also know the

growth opportunities to expand business.

Cost accounting- It is that type of accounting in which there is recording, allocating,

collecting, analysing, classifying and evaluating used for the purpose of taking action to

control cost. It is used by management to make a most appropriate action on the

capability and cost efficiency(Burritt, Schaltegger and Zvezdov, 2011). It involve a

detailed information regard to cost through management control it current operations so,

they can easily make a plan for future. The usage of cost accounting is that to determine

the cost of process, products and project etc. for the purpose of reporting the actual and

accurate amount of financial statements. Thus, it also helps the management in decision-

making, planning and controlling the organisation. Furthermore, it is also helpful in

computing the operational and capital budgeting, variance analysis, transfer pricing,

standard costing and activity based costing etc.

Budgetary report- The management used budget report to make comparison the actual

performance number attain over a some timing period. It is a kind of internal report that

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

show the close budget performance with the actual performance in a accounting periods.

Usually budget are is designed that are based upon future projection and estimation

which are largely differ form the company actual financial performance of an

organisation. It has two purpose for which the managers used to correct issues that are

occurred within the firm to make performance by matching the financial goals in the

report of budget. Thus, the other purpose is to evaluating bow accurate and realistic its

prediction accordingly they adjust its0 next budget.

TASK 2

P3 Calculate cost using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption cost

Income statements show the company financial position in financial year it has been

categorised into two parts are the revenues on debit side and expenses in credit side. Therefore, it

can be also define as an operating as well as operating activities. It can be used to know the

company financial position in terms of net profit or net loss (Elbashir, Collier and Sutton, 2011).

Most of the organisation made income statements by adopting techniques either marginal costing

and absorption costing. R.L. Maynard adopt absorption costing for its advantages as it shows a

higher net profit as compared to the marginal costing. In the present scenario a cited company

needs to calculate cost for this they have to prepare income statement by adopting both methods

of costing are absorption and marginal.

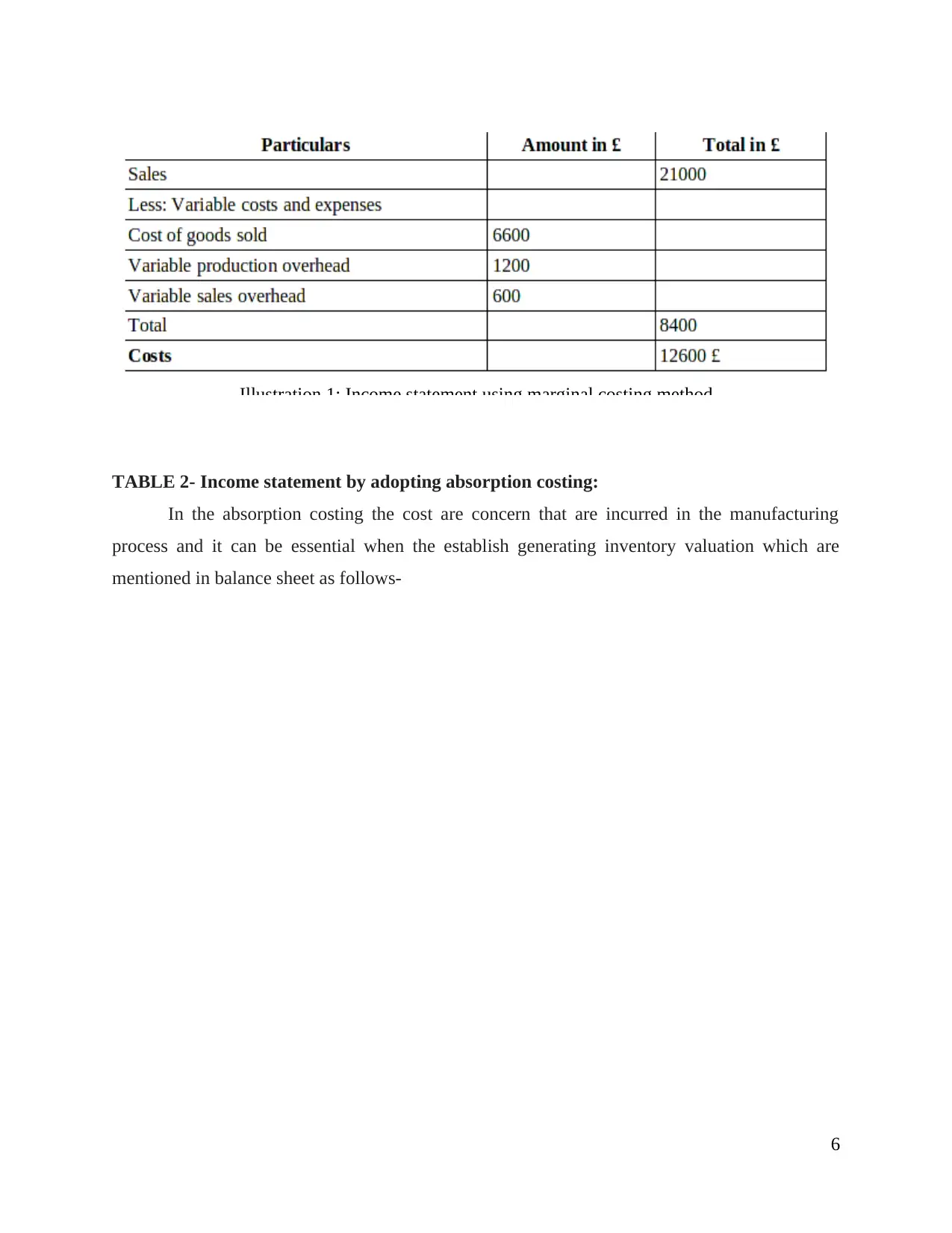

TABLE 1-Income statement by adopting marginal costing:

In the marginal costing which means that total cost of production is either increment or

decrement. It only occurs when there is an addition unit of cost is produced. Thus, the calculation

based upon this method are as follows-

5

Usually budget are is designed that are based upon future projection and estimation

which are largely differ form the company actual financial performance of an

organisation. It has two purpose for which the managers used to correct issues that are

occurred within the firm to make performance by matching the financial goals in the

report of budget. Thus, the other purpose is to evaluating bow accurate and realistic its

prediction accordingly they adjust its0 next budget.

TASK 2

P3 Calculate cost using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption cost

Income statements show the company financial position in financial year it has been

categorised into two parts are the revenues on debit side and expenses in credit side. Therefore, it

can be also define as an operating as well as operating activities. It can be used to know the

company financial position in terms of net profit or net loss (Elbashir, Collier and Sutton, 2011).

Most of the organisation made income statements by adopting techniques either marginal costing

and absorption costing. R.L. Maynard adopt absorption costing for its advantages as it shows a

higher net profit as compared to the marginal costing. In the present scenario a cited company

needs to calculate cost for this they have to prepare income statement by adopting both methods

of costing are absorption and marginal.

TABLE 1-Income statement by adopting marginal costing:

In the marginal costing which means that total cost of production is either increment or

decrement. It only occurs when there is an addition unit of cost is produced. Thus, the calculation

based upon this method are as follows-

5

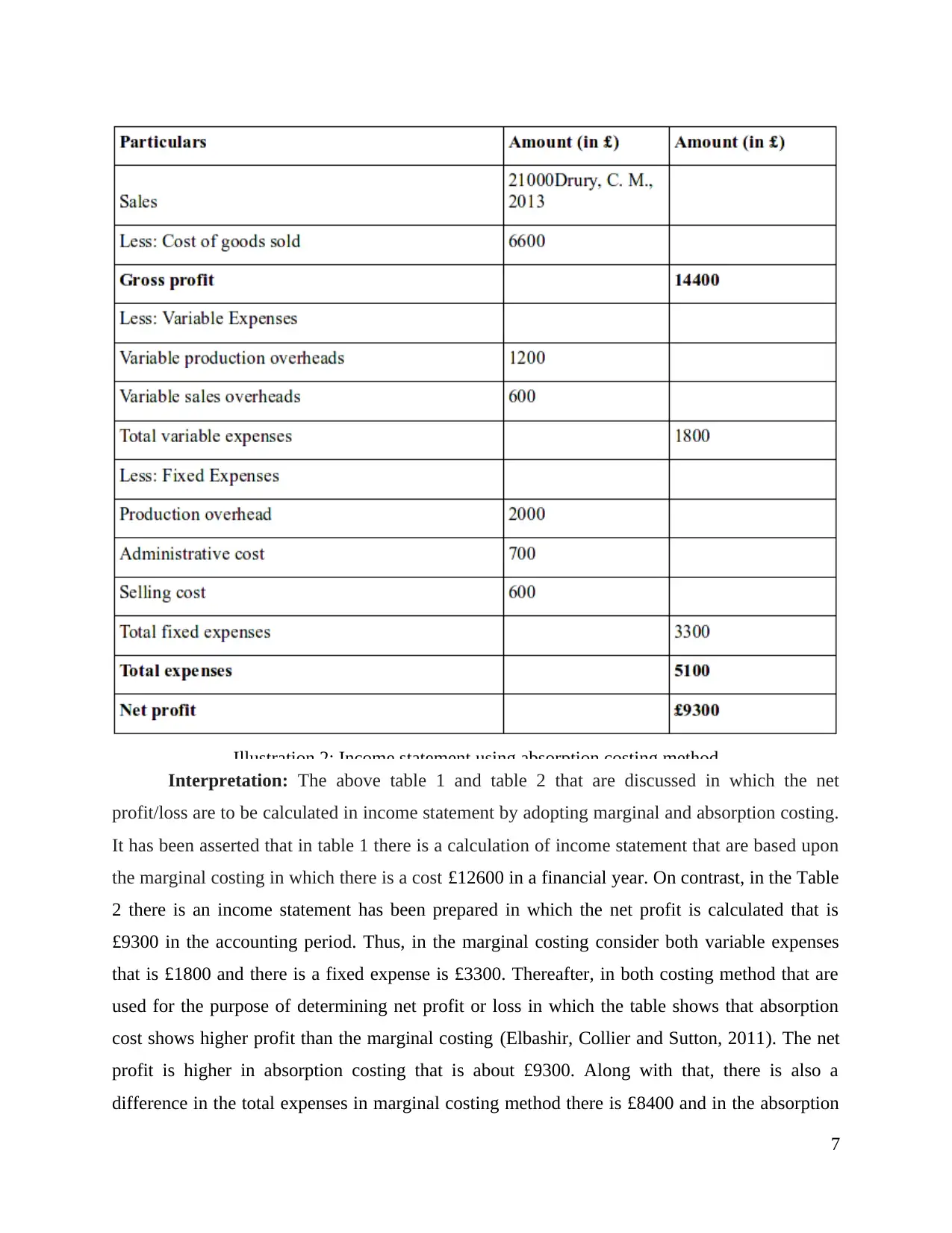

TABLE 2- Income statement by adopting absorption costing:

In the absorption costing the cost are concern that are incurred in the manufacturing

process and it can be essential when the establish generating inventory valuation which are

mentioned in balance sheet as follows-

6

Illustration 1: Income statement using marginal costing method

In the absorption costing the cost are concern that are incurred in the manufacturing

process and it can be essential when the establish generating inventory valuation which are

mentioned in balance sheet as follows-

6

Illustration 1: Income statement using marginal costing method

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration 2: Income statement using absorption costing method

Interpretation: The above table 1 and table 2 that are discussed in which the net

profit/loss are to be calculated in income statement by adopting marginal and absorption costing.

It has been asserted that in table 1 there is a calculation of income statement that are based upon

the marginal costing in which there is a cost £12600 in a financial year. On contrast, in the Table

2 there is an income statement has been prepared in which the net profit is calculated that is

£9300 in the accounting period. Thus, in the marginal costing consider both variable expenses

that is £1800 and there is a fixed expense is £3300. Thereafter, in both costing method that are

used for the purpose of determining net profit or loss in which the table shows that absorption

cost shows higher profit than the marginal costing (Elbashir, Collier and Sutton, 2011). The net

profit is higher in absorption costing that is about £9300. Along with that, there is also a

difference in the total expenses in marginal costing method there is £8400 and in the absorption

7

Interpretation: The above table 1 and table 2 that are discussed in which the net

profit/loss are to be calculated in income statement by adopting marginal and absorption costing.

It has been asserted that in table 1 there is a calculation of income statement that are based upon

the marginal costing in which there is a cost £12600 in a financial year. On contrast, in the Table

2 there is an income statement has been prepared in which the net profit is calculated that is

£9300 in the accounting period. Thus, in the marginal costing consider both variable expenses

that is £1800 and there is a fixed expense is £3300. Thereafter, in both costing method that are

used for the purpose of determining net profit or loss in which the table shows that absorption

cost shows higher profit than the marginal costing (Elbashir, Collier and Sutton, 2011). The net

profit is higher in absorption costing that is about £9300. Along with that, there is also a

difference in the total expenses in marginal costing method there is £8400 and in the absorption

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

costing its is £5100. It has been asserted that in the absorption costing there is a less total

expenses than the marginal costing as it takes both fixed and variable expenses. It has been

occurred at the time of cost of production in these process it has been determines net profit or

loss that are varied from each other.

Several authors said that in the business condition it has been asserted in which the

organisation in which absorption costing technique is more beneficial for the purpose of

calculating net profit. It is due to as in these techniques there is a fixed as well as variable

expenses are to be taken at the time of determine validate and reliable data. Therefore, in the

absorption costing methods it shows a better financial position of an organisation in effective

manner.

Difference among Marginal and Absorption costing

Basis for comparison Marginal costing Absorption Costing

Meaning It is that type of accounting

system in which it does not

take the fixed overhead cost

and it ascertained the overall

cost of production that are

known as marginal costing

(Garrison and et.al., 2010).

Therefore, for the calculation

purpose only variable

overhead take that are arisen

within the firm. Whereas,

fixed cost of production are to

be taken as periodic expenses.

In the absorption costing

methods in which there is a

total cost are to be taken for

the purpose of measuring the

total cost of production are

called as absorption costing. In

the calculation is take both

type of cost are fixed and

variable expenses.

Cost recognition In the product cost only

variable expenses are to be

taken whereas for the periodic

cost it considers a fixed cost.

In the product cost it considers

both fixed and variable

expenses.

8

expenses than the marginal costing as it takes both fixed and variable expenses. It has been

occurred at the time of cost of production in these process it has been determines net profit or

loss that are varied from each other.

Several authors said that in the business condition it has been asserted in which the

organisation in which absorption costing technique is more beneficial for the purpose of

calculating net profit. It is due to as in these techniques there is a fixed as well as variable

expenses are to be taken at the time of determine validate and reliable data. Therefore, in the

absorption costing methods it shows a better financial position of an organisation in effective

manner.

Difference among Marginal and Absorption costing

Basis for comparison Marginal costing Absorption Costing

Meaning It is that type of accounting

system in which it does not

take the fixed overhead cost

and it ascertained the overall

cost of production that are

known as marginal costing

(Garrison and et.al., 2010).

Therefore, for the calculation

purpose only variable

overhead take that are arisen

within the firm. Whereas,

fixed cost of production are to

be taken as periodic expenses.

In the absorption costing

methods in which there is a

total cost are to be taken for

the purpose of measuring the

total cost of production are

called as absorption costing. In

the calculation is take both

type of cost are fixed and

variable expenses.

Cost recognition In the product cost only

variable expenses are to be

taken whereas for the periodic

cost it considers a fixed cost.

In the product cost it considers

both fixed and variable

expenses.

8

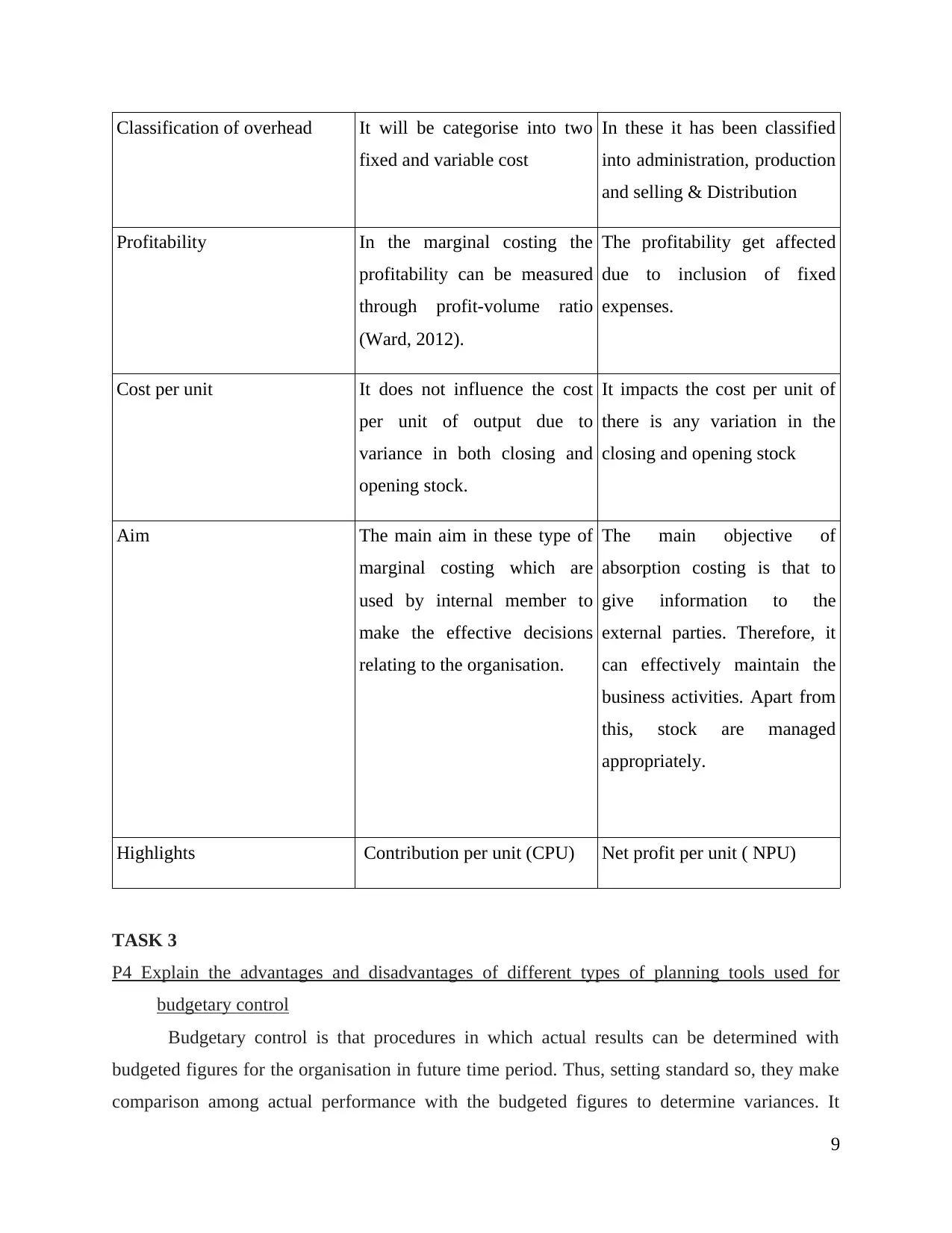

Classification of overhead It will be categorise into two

fixed and variable cost

In these it has been classified

into administration, production

and selling & Distribution

Profitability In the marginal costing the

profitability can be measured

through profit-volume ratio

(Ward, 2012).

The profitability get affected

due to inclusion of fixed

expenses.

Cost per unit It does not influence the cost

per unit of output due to

variance in both closing and

opening stock.

It impacts the cost per unit of

there is any variation in the

closing and opening stock

Aim The main aim in these type of

marginal costing which are

used by internal member to

make the effective decisions

relating to the organisation.

The main objective of

absorption costing is that to

give information to the

external parties. Therefore, it

can effectively maintain the

business activities. Apart from

this, stock are managed

appropriately.

Highlights Contribution per unit (CPU) Net profit per unit ( NPU)

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Budgetary control is that procedures in which actual results can be determined with

budgeted figures for the organisation in future time period. Thus, setting standard so, they make

comparison among actual performance with the budgeted figures to determine variances. It

9

fixed and variable cost

In these it has been classified

into administration, production

and selling & Distribution

Profitability In the marginal costing the

profitability can be measured

through profit-volume ratio

(Ward, 2012).

The profitability get affected

due to inclusion of fixed

expenses.

Cost per unit It does not influence the cost

per unit of output due to

variance in both closing and

opening stock.

It impacts the cost per unit of

there is any variation in the

closing and opening stock

Aim The main aim in these type of

marginal costing which are

used by internal member to

make the effective decisions

relating to the organisation.

The main objective of

absorption costing is that to

give information to the

external parties. Therefore, it

can effectively maintain the

business activities. Apart from

this, stock are managed

appropriately.

Highlights Contribution per unit (CPU) Net profit per unit ( NPU)

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Budgetary control is that procedures in which actual results can be determined with

budgeted figures for the organisation in future time period. Thus, setting standard so, they make

comparison among actual performance with the budgeted figures to determine variances. It

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.