HPS121/HPY713: Financial Wellbeing and Subjective Wellbeing Report

VerifiedAdded on 2022/09/12

|16

|4056

|19

Report

AI Summary

This laboratory report investigates the relationship between financial wellbeing and subjective wellbeing among university students. The study utilized a web-based questionnaire to collect data from 20 participants, including undergraduate and postgraduate students, as well as parents of students. The research assessed financial wellbeing using the CBA-Melbourne Institute Reported Financial Wellbeing Scale and subjective wellbeing via the Personal Wellbeing Index. The results revealed a significant number of negative responses regarding financial wellbeing, indicating that a majority of the participants faced difficulties in meeting living expenses. The report found a direct association between financial wellbeing and subjective wellbeing, influenced by academic performance and social wellbeing. The study also highlights the potential impact of financial stress on overall wellbeing and satisfaction with life, emphasizing the need for a balance between healthy saving and spending habits. The study's findings suggest a correlation between positive financial behaviors and positive subjective wellbeing, which can be used to improve the lives of students.

Running head: Laboratory Report

“RELATIONSHIP BETWEEN FINANCIAL WELLBEING AND SUBJECTIVE

WELLBEING”

LABORATORY REPORT

Student Name:

Student ID:

Word Count:

“RELATIONSHIP BETWEEN FINANCIAL WELLBEING AND SUBJECTIVE

WELLBEING”

LABORATORY REPORT

Student Name:

Student ID:

Word Count:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Laboratory Report 2

Abstract

The satisfaction from financial domain influences the outcomes of various other domains. This

study aims to explore the association between financial wellness to the subjective wellness

index. The study uses web based questionnaire as research method with random sampling. Data

is collected from 20 participants at the university which involve under graduate students, post

graduate students and the parents of students. Web based questionnaire was used to collect data

where the link was sent to individual participants and the filled forms were retrieved. The results

show significant number of negative responses when compared to positive. The study involved

students as major participant groups. Hence, there is direct association of financial well being

with the subjective well being of the participants which is also influenced by academic

performance and social well being.

Abstract

The satisfaction from financial domain influences the outcomes of various other domains. This

study aims to explore the association between financial wellness to the subjective wellness

index. The study uses web based questionnaire as research method with random sampling. Data

is collected from 20 participants at the university which involve under graduate students, post

graduate students and the parents of students. Web based questionnaire was used to collect data

where the link was sent to individual participants and the filled forms were retrieved. The results

show significant number of negative responses when compared to positive. The study involved

students as major participant groups. Hence, there is direct association of financial well being

with the subjective well being of the participants which is also influenced by academic

performance and social well being.

Laboratory Report 3

Introduction

Financial Well Being may be termed as one’s perception to sustain his current and expected

living standards along with financial freedom (Bruggen, Hogreve, Holmlund, Kabadayi &

Lofgren, 2017). The individuals can only assess their own financial well being and cannot be

estimated by others. It is a personal attribute and depends on multiple factors like age, gender,

family structure, education and marital status. The people may perceive high or low financial

well being and it does not depend on their objective financial position.

The Subjective Well being may be termed as one’s cognitive and affective evaluation of his life

(Cummins, 2016). It involves extensive factors related to quality of life (QOL) such as inborn

temperament, cognitive judgments, social interactions, ability to meet basic needs, society in

which they live and emotional reactions. These factors reflect the overall satisfaction from his

life. For the students, the subjective well being also involves the academic satisfaction and life

satisfaction.

College graduates aged 20-35 years of age spend 18% of their income in loan payments in US

which reduces their consumption and retirement savings (Bruggen et al., 2017). Average savings

of people in US are just 4% of current salaries. However, they need to save 15-20% annually to

sustain similar living standards after retirement. For 85% of the working people, retirement is not

one of the main priority for savings. Consequently, 69% of the working people are worried about

getting out of money during retirement while 66% are worried about maintain adequate money

for the everyday expenses at old age (Bruggen et al., 2017). This condition reflects that the

financial well being is most important aspect for everyone throughout the world. A balance of

healthy saving and spending is necessary to maintain long term personal and financial well

being. The people who remain indebted most of the age, are at highest risk of depression. Lack

of financial well being leads to personal stress which adversely affects the people, families and

society.

In wake of extensive need of research on this topic, this study provides evidence based research

on association between financial well being and subjective well being in youth of Australia.

Introduction

Financial Well Being may be termed as one’s perception to sustain his current and expected

living standards along with financial freedom (Bruggen, Hogreve, Holmlund, Kabadayi &

Lofgren, 2017). The individuals can only assess their own financial well being and cannot be

estimated by others. It is a personal attribute and depends on multiple factors like age, gender,

family structure, education and marital status. The people may perceive high or low financial

well being and it does not depend on their objective financial position.

The Subjective Well being may be termed as one’s cognitive and affective evaluation of his life

(Cummins, 2016). It involves extensive factors related to quality of life (QOL) such as inborn

temperament, cognitive judgments, social interactions, ability to meet basic needs, society in

which they live and emotional reactions. These factors reflect the overall satisfaction from his

life. For the students, the subjective well being also involves the academic satisfaction and life

satisfaction.

College graduates aged 20-35 years of age spend 18% of their income in loan payments in US

which reduces their consumption and retirement savings (Bruggen et al., 2017). Average savings

of people in US are just 4% of current salaries. However, they need to save 15-20% annually to

sustain similar living standards after retirement. For 85% of the working people, retirement is not

one of the main priority for savings. Consequently, 69% of the working people are worried about

getting out of money during retirement while 66% are worried about maintain adequate money

for the everyday expenses at old age (Bruggen et al., 2017). This condition reflects that the

financial well being is most important aspect for everyone throughout the world. A balance of

healthy saving and spending is necessary to maintain long term personal and financial well

being. The people who remain indebted most of the age, are at highest risk of depression. Lack

of financial well being leads to personal stress which adversely affects the people, families and

society.

In wake of extensive need of research on this topic, this study provides evidence based research

on association between financial well being and subjective well being in youth of Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Laboratory Report 4

Financial Issues are one of the biggest stressors in the lives of Australian adults (Australian

Psychological Society, 2015). The financial stress gives rise to broad range of adverse outcomes

like reduced QOL (Bruggens et al., 2017). Having adequate resources to satisfy the needs may

act as buffer to the activities which threaten the subjective well being. Financial well being is

associated to happiness through mediating variables. For example, if someone is effectively

handling the financial resources, it may influence his satisfaction and quality of life. The

subjective well being may be assessed in terms of whether my life is close to my ideal in most

ways, the conditions of life are very favorable, high level of satisfaction with life, achievement of

important goals in life and the need to change the condition.

Experiences of financial imbalances (due to foreclosure) are associated with poor behavioral and

psychological indicators like declining health, violent behavior and anxiety. The research

highlights the different factors responsible for financial well being such as contextual factors,

personal factors, traits, skills, attitude and socio demographic factors as identified in the analysis

of collected data.

Research Question & Hypotheses

What is the relationship between financial wellbeing and subjective wellbeing?

The study proposes the following hypothesis: “Positive financial behaviors/ well being is

associated with positive subjective well being”. For testing the hypothesis, co relational analysis

was conducted to identify the available relationship between the two variables.

Rationale

The study aims to identify and interpret the real time experiences of students, friends and their

parents about their perception of financial wellness and its association with subjective wellness.

Financial Issues are one of the biggest stressors in the lives of Australian adults (Australian

Psychological Society, 2015). The financial stress gives rise to broad range of adverse outcomes

like reduced QOL (Bruggens et al., 2017). Having adequate resources to satisfy the needs may

act as buffer to the activities which threaten the subjective well being. Financial well being is

associated to happiness through mediating variables. For example, if someone is effectively

handling the financial resources, it may influence his satisfaction and quality of life. The

subjective well being may be assessed in terms of whether my life is close to my ideal in most

ways, the conditions of life are very favorable, high level of satisfaction with life, achievement of

important goals in life and the need to change the condition.

Experiences of financial imbalances (due to foreclosure) are associated with poor behavioral and

psychological indicators like declining health, violent behavior and anxiety. The research

highlights the different factors responsible for financial well being such as contextual factors,

personal factors, traits, skills, attitude and socio demographic factors as identified in the analysis

of collected data.

Research Question & Hypotheses

What is the relationship between financial wellbeing and subjective wellbeing?

The study proposes the following hypothesis: “Positive financial behaviors/ well being is

associated with positive subjective well being”. For testing the hypothesis, co relational analysis

was conducted to identify the available relationship between the two variables.

Rationale

The study aims to identify and interpret the real time experiences of students, friends and their

parents about their perception of financial wellness and its association with subjective wellness.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Laboratory Report 5

METHOD

Web based questionnaire was employed as a method of data collection. Financial wellbeing was

assessed via the Commonwealth Bank of Australia (CBA)-Melbourne Institute Reported

Financial Wellbeing Scale (version 1) while the Subjective wellbeing was assessed via the

Personal Wellbeing Index. The pretest of the questionnaire was made on the basis of literature

review and data collected from the respondents.

Participants

Data was collected from 25 participants in the University campus. However, the completely

filled forms were retrieved from 20 participants only.

The data was collected from the students, friends and the family members of students through

online questionnaire. The participants were young people aged 20-26 years. The link to

questionnaire was provided to the participants through email and they were asked to complete

the questions about their financial well being, general demographic and subjective well being.

For random sampling, the follow up reminder was sent after one week. Overall 20 students

responded to the survey with 80% response rate. Of these, 10 were undergraduate students, 5

were post graduate students and 5 were the relatives or parents of the students. 15 participants

were males while 5 were females.

Materials

The questionnaire was prepared keeping in mind the demographic characteristics of the

participants. The responses were obtained through webpage links. The responses were collected

in form of Likert scale for financial and personal index. The responses obtained were assessed

for their validity in terms of available research material by the earlier researchers. The data

analysis software like MS Excel and SPSS were also used to interpret the findings for the

validation of the results.

METHOD

Web based questionnaire was employed as a method of data collection. Financial wellbeing was

assessed via the Commonwealth Bank of Australia (CBA)-Melbourne Institute Reported

Financial Wellbeing Scale (version 1) while the Subjective wellbeing was assessed via the

Personal Wellbeing Index. The pretest of the questionnaire was made on the basis of literature

review and data collected from the respondents.

Participants

Data was collected from 25 participants in the University campus. However, the completely

filled forms were retrieved from 20 participants only.

The data was collected from the students, friends and the family members of students through

online questionnaire. The participants were young people aged 20-26 years. The link to

questionnaire was provided to the participants through email and they were asked to complete

the questions about their financial well being, general demographic and subjective well being.

For random sampling, the follow up reminder was sent after one week. Overall 20 students

responded to the survey with 80% response rate. Of these, 10 were undergraduate students, 5

were post graduate students and 5 were the relatives or parents of the students. 15 participants

were males while 5 were females.

Materials

The questionnaire was prepared keeping in mind the demographic characteristics of the

participants. The responses were obtained through webpage links. The responses were collected

in form of Likert scale for financial and personal index. The responses obtained were assessed

for their validity in terms of available research material by the earlier researchers. The data

analysis software like MS Excel and SPSS were also used to interpret the findings for the

validation of the results.

Laboratory Report 6

Procedure

Informed consent forms were signed by the participants after informing them about the objective

and structure of the study. Extensive literature review was also consulted for the theories and

evidence based literature on this topic.

The participants were selected through random sampling through known links of the friends and

classmates and their parents. None of the participants was contacted personally by meeting him

at any physical location. The participants were given 7 days time to complete the survey and

send it back to us. After two days, they were reminded for filling up the questionnaire. The study

gave 80% response rate.

Financial Measures were assessed using 7 themes ranging from standard of living, health,

achievements, personal relationship, personal safety, community connectedness and future

security.

Demographic Features of the Participants

Age 20-26 years

Gender 75% males, 25% females

Education 10 Undergraduates, 5 Post graduates, 5 parents (Adults)

Profession 10 UG Not working, 10 PG and parents working

Income $500-750 (10 UG students)

$2000-$3000 (5 PG students)

$25000-$50000 (5 Adults)

Education

Loan

$10,000 or more (5 Students)

Procedure

Informed consent forms were signed by the participants after informing them about the objective

and structure of the study. Extensive literature review was also consulted for the theories and

evidence based literature on this topic.

The participants were selected through random sampling through known links of the friends and

classmates and their parents. None of the participants was contacted personally by meeting him

at any physical location. The participants were given 7 days time to complete the survey and

send it back to us. After two days, they were reminded for filling up the questionnaire. The study

gave 80% response rate.

Financial Measures were assessed using 7 themes ranging from standard of living, health,

achievements, personal relationship, personal safety, community connectedness and future

security.

Demographic Features of the Participants

Age 20-26 years

Gender 75% males, 25% females

Education 10 Undergraduates, 5 Post graduates, 5 parents (Adults)

Profession 10 UG Not working, 10 PG and parents working

Income $500-750 (10 UG students)

$2000-$3000 (5 PG students)

$25000-$50000 (5 Adults)

Education

Loan

$10,000 or more (5 Students)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

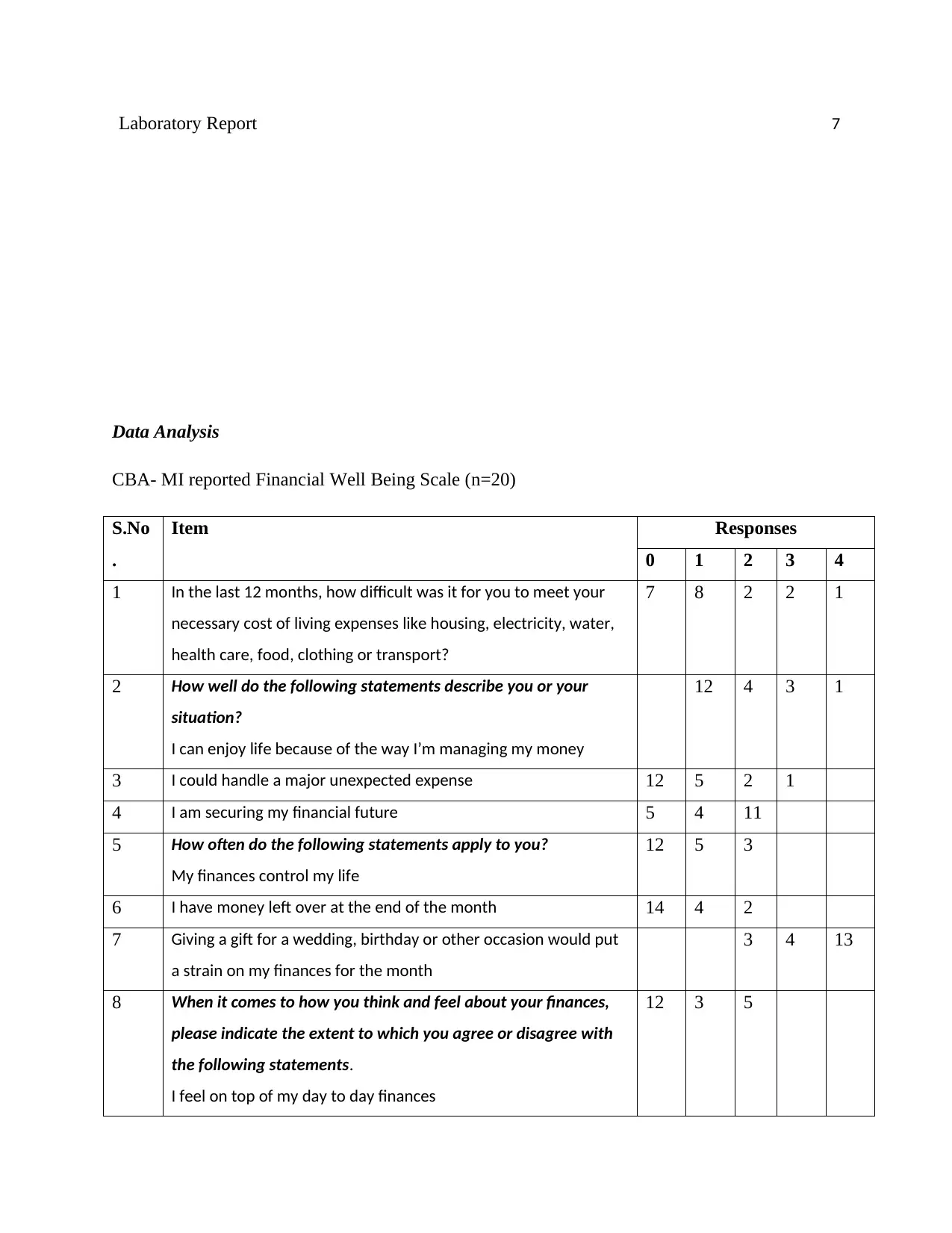

Laboratory Report 7

Data Analysis

CBA- MI reported Financial Well Being Scale (n=20)

S.No

.

Item Responses

0 1 2 3 4

1 In the last 12 months, how difficult was it for you to meet your

necessary cost of living expenses like housing, electricity, water,

health care, food, clothing or transport?

7 8 2 2 1

2 How well do the following statements describe you or your

situation?

I can enjoy life because of the way I’m managing my money

12 4 3 1

3 I could handle a major unexpected expense 12 5 2 1

4 I am securing my financial future 5 4 11

5 How often do the following statements apply to you?

My finances control my life

12 5 3

6 I have money left over at the end of the month 14 4 2

7 Giving a gift for a wedding, birthday or other occasion would put

a strain on my finances for the month

3 4 13

8 When it comes to how you think and feel about your finances,

please indicate the extent to which you agree or disagree with

the following statements.

I feel on top of my day to day finances

12 3 5

Data Analysis

CBA- MI reported Financial Well Being Scale (n=20)

S.No

.

Item Responses

0 1 2 3 4

1 In the last 12 months, how difficult was it for you to meet your

necessary cost of living expenses like housing, electricity, water,

health care, food, clothing or transport?

7 8 2 2 1

2 How well do the following statements describe you or your

situation?

I can enjoy life because of the way I’m managing my money

12 4 3 1

3 I could handle a major unexpected expense 12 5 2 1

4 I am securing my financial future 5 4 11

5 How often do the following statements apply to you?

My finances control my life

12 5 3

6 I have money left over at the end of the month 14 4 2

7 Giving a gift for a wedding, birthday or other occasion would put

a strain on my finances for the month

3 4 13

8 When it comes to how you think and feel about your finances,

please indicate the extent to which you agree or disagree with

the following statements.

I feel on top of my day to day finances

12 3 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

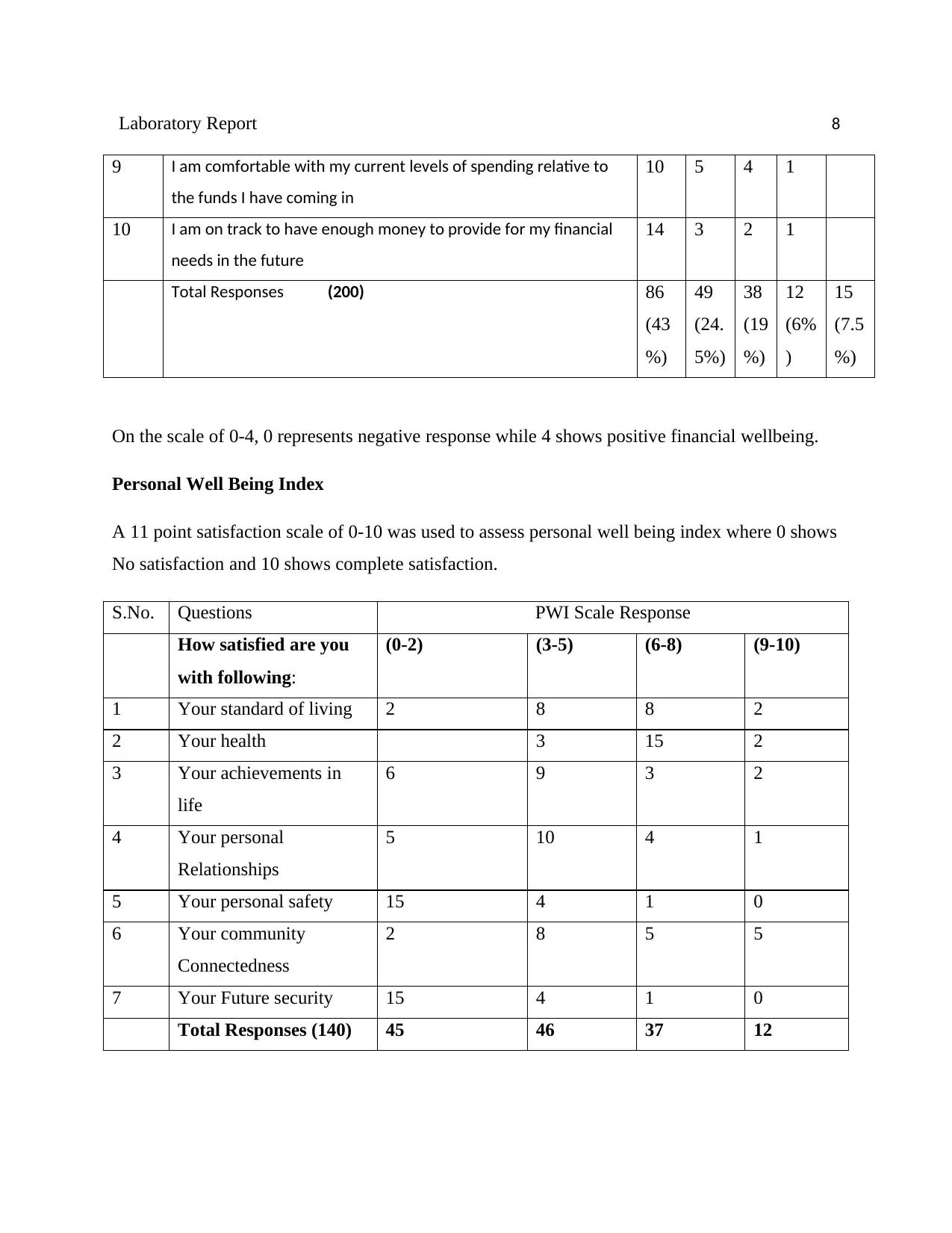

Laboratory Report 8

9 I am comfortable with my current levels of spending relative to

the funds I have coming in

10 5 4 1

10 I am on track to have enough money to provide for my financial

needs in the future

14 3 2 1

Total Responses (200) 86

(43

%)

49

(24.

5%)

38

(19

%)

12

(6%

)

15

(7.5

%)

On the scale of 0-4, 0 represents negative response while 4 shows positive financial wellbeing.

Personal Well Being Index

A 11 point satisfaction scale of 0-10 was used to assess personal well being index where 0 shows

No satisfaction and 10 shows complete satisfaction.

S.No. Questions PWI Scale Response

How satisfied are you

with following:

(0-2) (3-5) (6-8) (9-10)

1 Your standard of living 2 8 8 2

2 Your health 3 15 2

3 Your achievements in

life

6 9 3 2

4 Your personal

Relationships

5 10 4 1

5 Your personal safety 15 4 1 0

6 Your community

Connectedness

2 8 5 5

7 Your Future security 15 4 1 0

Total Responses (140) 45 46 37 12

9 I am comfortable with my current levels of spending relative to

the funds I have coming in

10 5 4 1

10 I am on track to have enough money to provide for my financial

needs in the future

14 3 2 1

Total Responses (200) 86

(43

%)

49

(24.

5%)

38

(19

%)

12

(6%

)

15

(7.5

%)

On the scale of 0-4, 0 represents negative response while 4 shows positive financial wellbeing.

Personal Well Being Index

A 11 point satisfaction scale of 0-10 was used to assess personal well being index where 0 shows

No satisfaction and 10 shows complete satisfaction.

S.No. Questions PWI Scale Response

How satisfied are you

with following:

(0-2) (3-5) (6-8) (9-10)

1 Your standard of living 2 8 8 2

2 Your health 3 15 2

3 Your achievements in

life

6 9 3 2

4 Your personal

Relationships

5 10 4 1

5 Your personal safety 15 4 1 0

6 Your community

Connectedness

2 8 5 5

7 Your Future security 15 4 1 0

Total Responses (140) 45 46 37 12

Laboratory Report 9

Results

To analyze whether any relationship exists between subjective wellbeing and financial

wellbeing, we completed a bivariate correlational analysis. The financial well being entities

taken were 86,49,38,12 and 15 while the personal Well Being Identities involved 45,46,37,and

12.

A significant positive and strong relationship between openness to financial wellbeing and

subjective wellbeing was found, r = 0.80, p <0.05, representing …% shared variance between the

two variables.

In Financial Well being Index, the responses from 20 participants reflected 86 negative responses

(43%) and 15 positive responses (7.5%). It shows, most of the respondents have problems with

their financial well being. Majority of them find it difficult to meet their necessary cost of living

expenses like housing, electricity, water, health care, food, clothing or transport. A high

proportion of students do not enjoy their life due to stressful financial management. 80% of them

cannot handle a major unexpected expenditure. 11% of the respondents try to save for their

future. 80% of the people think theta their finances control their life. They refrain from doing

things they like, just to save money. There is an increased dissatisfaction in terms of high level of

current expenses, with 70% of the people unable to save for future expenses.

In Personal Well being Index, out of total 140 responses collected, 91 responses (65%) were

below 5 Index value. 49 responses (35%) were above average satisfaction level having index

value 6 to 10.

The responses collected showed that the student debt did not impact significantly to their

satisfaction level in presence of positive financial behaviors. It may be due to their coping skills,

the students who are in debt do not exhibit depression in their behavior. The financial behaviors

like spending the limited money within budget, tracking the monthly expenditure does not

improve the overall satisfaction of students with their life. The financial expenses also do not

affect the academic performance of student.

Results

To analyze whether any relationship exists between subjective wellbeing and financial

wellbeing, we completed a bivariate correlational analysis. The financial well being entities

taken were 86,49,38,12 and 15 while the personal Well Being Identities involved 45,46,37,and

12.

A significant positive and strong relationship between openness to financial wellbeing and

subjective wellbeing was found, r = 0.80, p <0.05, representing …% shared variance between the

two variables.

In Financial Well being Index, the responses from 20 participants reflected 86 negative responses

(43%) and 15 positive responses (7.5%). It shows, most of the respondents have problems with

their financial well being. Majority of them find it difficult to meet their necessary cost of living

expenses like housing, electricity, water, health care, food, clothing or transport. A high

proportion of students do not enjoy their life due to stressful financial management. 80% of them

cannot handle a major unexpected expenditure. 11% of the respondents try to save for their

future. 80% of the people think theta their finances control their life. They refrain from doing

things they like, just to save money. There is an increased dissatisfaction in terms of high level of

current expenses, with 70% of the people unable to save for future expenses.

In Personal Well being Index, out of total 140 responses collected, 91 responses (65%) were

below 5 Index value. 49 responses (35%) were above average satisfaction level having index

value 6 to 10.

The responses collected showed that the student debt did not impact significantly to their

satisfaction level in presence of positive financial behaviors. It may be due to their coping skills,

the students who are in debt do not exhibit depression in their behavior. The financial behaviors

like spending the limited money within budget, tracking the monthly expenditure does not

improve the overall satisfaction of students with their life. The financial expenses also do not

affect the academic performance of student.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Laboratory Report

10

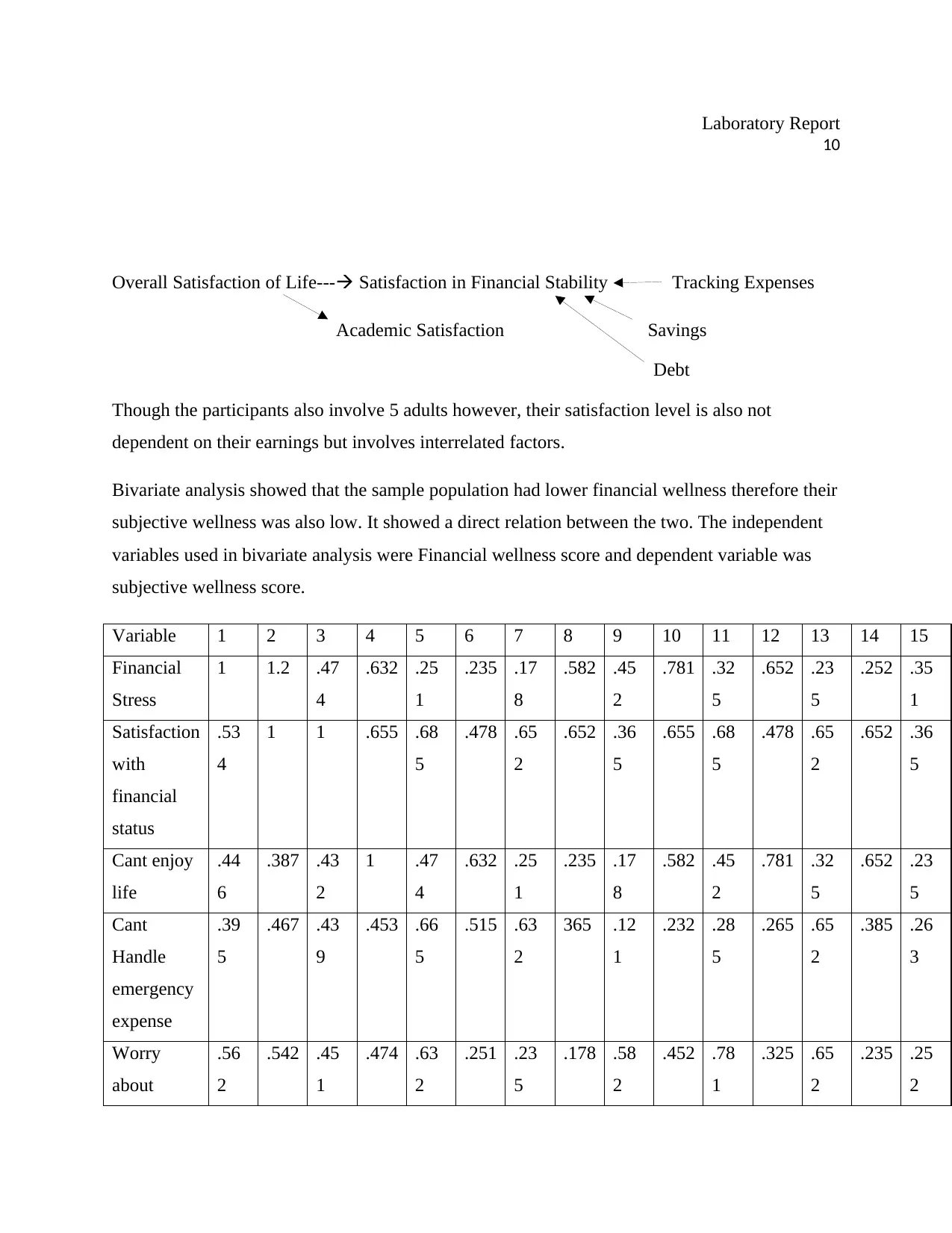

Overall Satisfaction of Life--- Satisfaction in Financial Stability Tracking Expenses

Academic Satisfaction Savings

Debt

Though the participants also involve 5 adults however, their satisfaction level is also not

dependent on their earnings but involves interrelated factors.

Bivariate analysis showed that the sample population had lower financial wellness therefore their

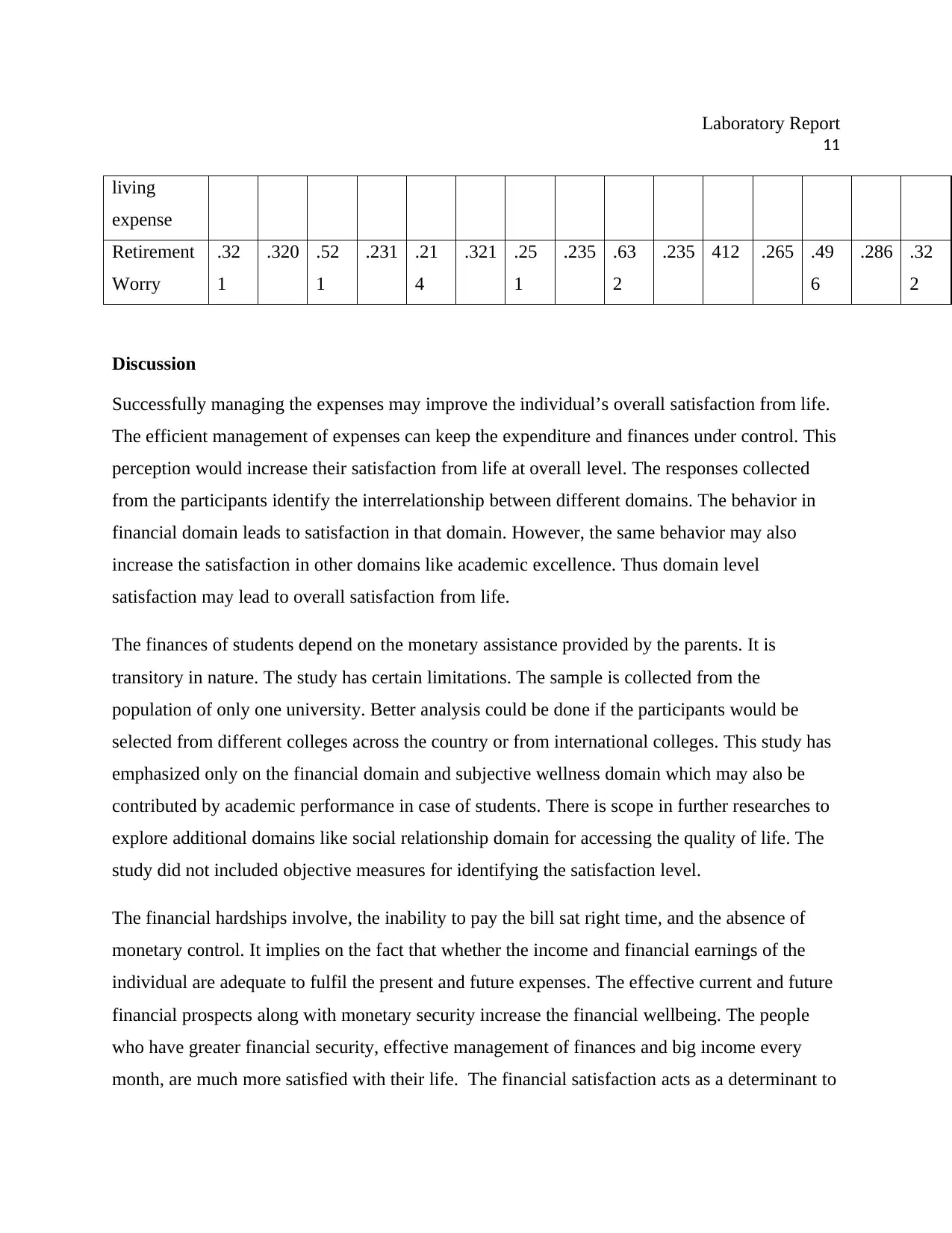

subjective wellness was also low. It showed a direct relation between the two. The independent

variables used in bivariate analysis were Financial wellness score and dependent variable was

subjective wellness score.

Variable 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Financial

Stress

1 1.2 .47

4

.632 .25

1

.235 .17

8

.582 .45

2

.781 .32

5

.652 .23

5

.252 .35

1

Satisfaction

with

financial

status

.53

4

1 1 .655 .68

5

.478 .65

2

.652 .36

5

.655 .68

5

.478 .65

2

.652 .36

5

Cant enjoy

life

.44

6

.387 .43

2

1 .47

4

.632 .25

1

.235 .17

8

.582 .45

2

.781 .32

5

.652 .23

5

Cant

Handle

emergency

expense

.39

5

.467 .43

9

.453 .66

5

.515 .63

2

365 .12

1

.232 .28

5

.265 .65

2

.385 .26

3

Worry

about

.56

2

.542 .45

1

.474 .63

2

.251 .23

5

.178 .58

2

.452 .78

1

.325 .65

2

.235 .25

2

10

Overall Satisfaction of Life--- Satisfaction in Financial Stability Tracking Expenses

Academic Satisfaction Savings

Debt

Though the participants also involve 5 adults however, their satisfaction level is also not

dependent on their earnings but involves interrelated factors.

Bivariate analysis showed that the sample population had lower financial wellness therefore their

subjective wellness was also low. It showed a direct relation between the two. The independent

variables used in bivariate analysis were Financial wellness score and dependent variable was

subjective wellness score.

Variable 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Financial

Stress

1 1.2 .47

4

.632 .25

1

.235 .17

8

.582 .45

2

.781 .32

5

.652 .23

5

.252 .35

1

Satisfaction

with

financial

status

.53

4

1 1 .655 .68

5

.478 .65

2

.652 .36

5

.655 .68

5

.478 .65

2

.652 .36

5

Cant enjoy

life

.44

6

.387 .43

2

1 .47

4

.632 .25

1

.235 .17

8

.582 .45

2

.781 .32

5

.652 .23

5

Cant

Handle

emergency

expense

.39

5

.467 .43

9

.453 .66

5

.515 .63

2

365 .12

1

.232 .28

5

.265 .65

2

.385 .26

3

Worry

about

.56

2

.542 .45

1

.474 .63

2

.251 .23

5

.178 .58

2

.452 .78

1

.325 .65

2

.235 .25

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Laboratory Report

11

living

expense

Retirement

Worry

.32

1

.320 .52

1

.231 .21

4

.321 .25

1

.235 .63

2

.235 412 .265 .49

6

.286 .32

2

Discussion

Successfully managing the expenses may improve the individual’s overall satisfaction from life.

The efficient management of expenses can keep the expenditure and finances under control. This

perception would increase their satisfaction from life at overall level. The responses collected

from the participants identify the interrelationship between different domains. The behavior in

financial domain leads to satisfaction in that domain. However, the same behavior may also

increase the satisfaction in other domains like academic excellence. Thus domain level

satisfaction may lead to overall satisfaction from life.

The finances of students depend on the monetary assistance provided by the parents. It is

transitory in nature. The study has certain limitations. The sample is collected from the

population of only one university. Better analysis could be done if the participants would be

selected from different colleges across the country or from international colleges. This study has

emphasized only on the financial domain and subjective wellness domain which may also be

contributed by academic performance in case of students. There is scope in further researches to

explore additional domains like social relationship domain for accessing the quality of life. The

study did not included objective measures for identifying the satisfaction level.

The financial hardships involve, the inability to pay the bill sat right time, and the absence of

monetary control. It implies on the fact that whether the income and financial earnings of the

individual are adequate to fulfil the present and future expenses. The effective current and future

financial prospects along with monetary security increase the financial wellbeing. The people

who have greater financial security, effective management of finances and big income every

month, are much more satisfied with their life. The financial satisfaction acts as a determinant to

11

living

expense

Retirement

Worry

.32

1

.320 .52

1

.231 .21

4

.321 .25

1

.235 .63

2

.235 412 .265 .49

6

.286 .32

2

Discussion

Successfully managing the expenses may improve the individual’s overall satisfaction from life.

The efficient management of expenses can keep the expenditure and finances under control. This

perception would increase their satisfaction from life at overall level. The responses collected

from the participants identify the interrelationship between different domains. The behavior in

financial domain leads to satisfaction in that domain. However, the same behavior may also

increase the satisfaction in other domains like academic excellence. Thus domain level

satisfaction may lead to overall satisfaction from life.

The finances of students depend on the monetary assistance provided by the parents. It is

transitory in nature. The study has certain limitations. The sample is collected from the

population of only one university. Better analysis could be done if the participants would be

selected from different colleges across the country or from international colleges. This study has

emphasized only on the financial domain and subjective wellness domain which may also be

contributed by academic performance in case of students. There is scope in further researches to

explore additional domains like social relationship domain for accessing the quality of life. The

study did not included objective measures for identifying the satisfaction level.

The financial hardships involve, the inability to pay the bill sat right time, and the absence of

monetary control. It implies on the fact that whether the income and financial earnings of the

individual are adequate to fulfil the present and future expenses. The effective current and future

financial prospects along with monetary security increase the financial wellbeing. The people

who have greater financial security, effective management of finances and big income every

month, are much more satisfied with their life. The financial satisfaction acts as a determinant to

Laboratory Report

12

improve the satisfaction from life. The average or low income groups have insufficient financial

resources to invest in the planning for better future wellness. However, in certain cases, a high

income does not result into greater level of personal satisfaction. The relationship between these

two variable sis also dependent on the complex array of factors like good social connectedness,

good reputation, family, marital status, children, and time to leisure and relax.

In terms of collected responses, the sample showed greater positive perception about inabilities

or lack of handling financial control. The sample being the students mainly had monetary

restrictions. This sample showed greater responses in lower satisfaction in both the domains

(financial and personal). Though few subjects have good income levels, they did not exhibit

financial satisfaction. Similar results are shown in a Brazilian Study by Campara, Viera &

Potrich (2016).

In addition to financial well being, main drivers of subjective wellness also includes the impact

of demographic factors like gender, status in labor market, urbanization level, household type

and age. Negative perception is associated with the single parent houses, the adults living

without the children is also a factor. The young people are more satisfied with their life in

comparison to old age people. The bivariate analysis showed no significant impact of gender.

However the women are more satisfied than the men in overall personal well being. Being

unemployed adversely affects the satisfaction from life. The health is very closely associated

with the life satisfaction. The education level shows a mixed response towards the subjective

wellness. It is not necessary that the people who are highly educated will be more satisfied with

their life. Several studies assert that the higher education level increase the satisfaction level in

people in comparison to those who are not educated. The factors like Inability to meet

emergency expenses show negative impact on life satisfaction.

The low or negative responses submitted by most of the participants in our study may be due to

the student age. This age involves uncertainty about the future and potential career options which

may affect the perception of financial and personal satisfaction level. The students are not

financially independent and their financial effectiveness depend so n their parents and care

providers.

12

improve the satisfaction from life. The average or low income groups have insufficient financial

resources to invest in the planning for better future wellness. However, in certain cases, a high

income does not result into greater level of personal satisfaction. The relationship between these

two variable sis also dependent on the complex array of factors like good social connectedness,

good reputation, family, marital status, children, and time to leisure and relax.

In terms of collected responses, the sample showed greater positive perception about inabilities

or lack of handling financial control. The sample being the students mainly had monetary

restrictions. This sample showed greater responses in lower satisfaction in both the domains

(financial and personal). Though few subjects have good income levels, they did not exhibit

financial satisfaction. Similar results are shown in a Brazilian Study by Campara, Viera &

Potrich (2016).

In addition to financial well being, main drivers of subjective wellness also includes the impact

of demographic factors like gender, status in labor market, urbanization level, household type

and age. Negative perception is associated with the single parent houses, the adults living

without the children is also a factor. The young people are more satisfied with their life in

comparison to old age people. The bivariate analysis showed no significant impact of gender.

However the women are more satisfied than the men in overall personal well being. Being

unemployed adversely affects the satisfaction from life. The health is very closely associated

with the life satisfaction. The education level shows a mixed response towards the subjective

wellness. It is not necessary that the people who are highly educated will be more satisfied with

their life. Several studies assert that the higher education level increase the satisfaction level in

people in comparison to those who are not educated. The factors like Inability to meet

emergency expenses show negative impact on life satisfaction.

The low or negative responses submitted by most of the participants in our study may be due to

the student age. This age involves uncertainty about the future and potential career options which

may affect the perception of financial and personal satisfaction level. The students are not

financially independent and their financial effectiveness depend so n their parents and care

providers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.