Financial Sustainability Analysis: Banks and Infant Protection

VerifiedAdded on 2022/08/13

|3

|1059

|14

Homework Assignment

AI Summary

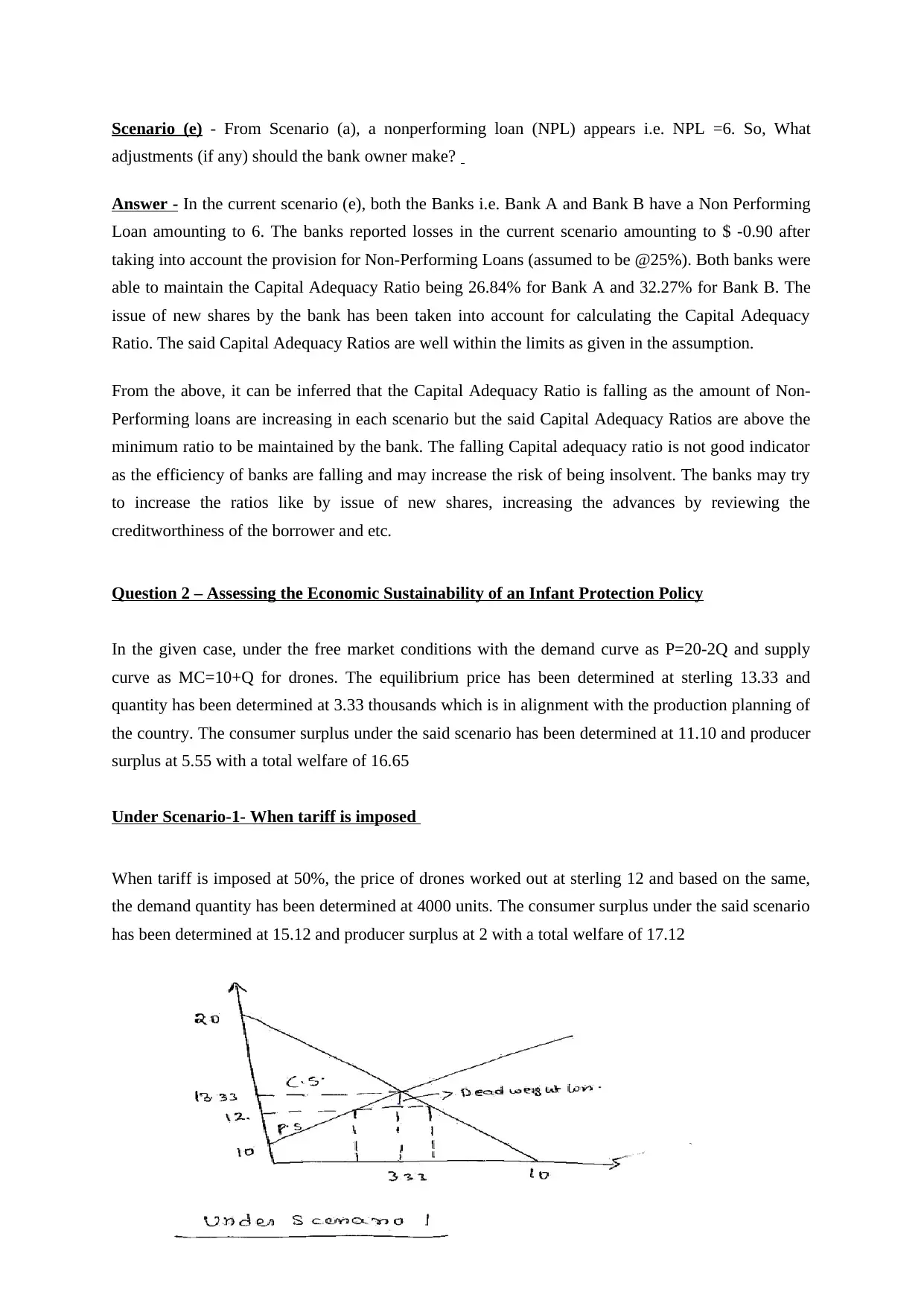

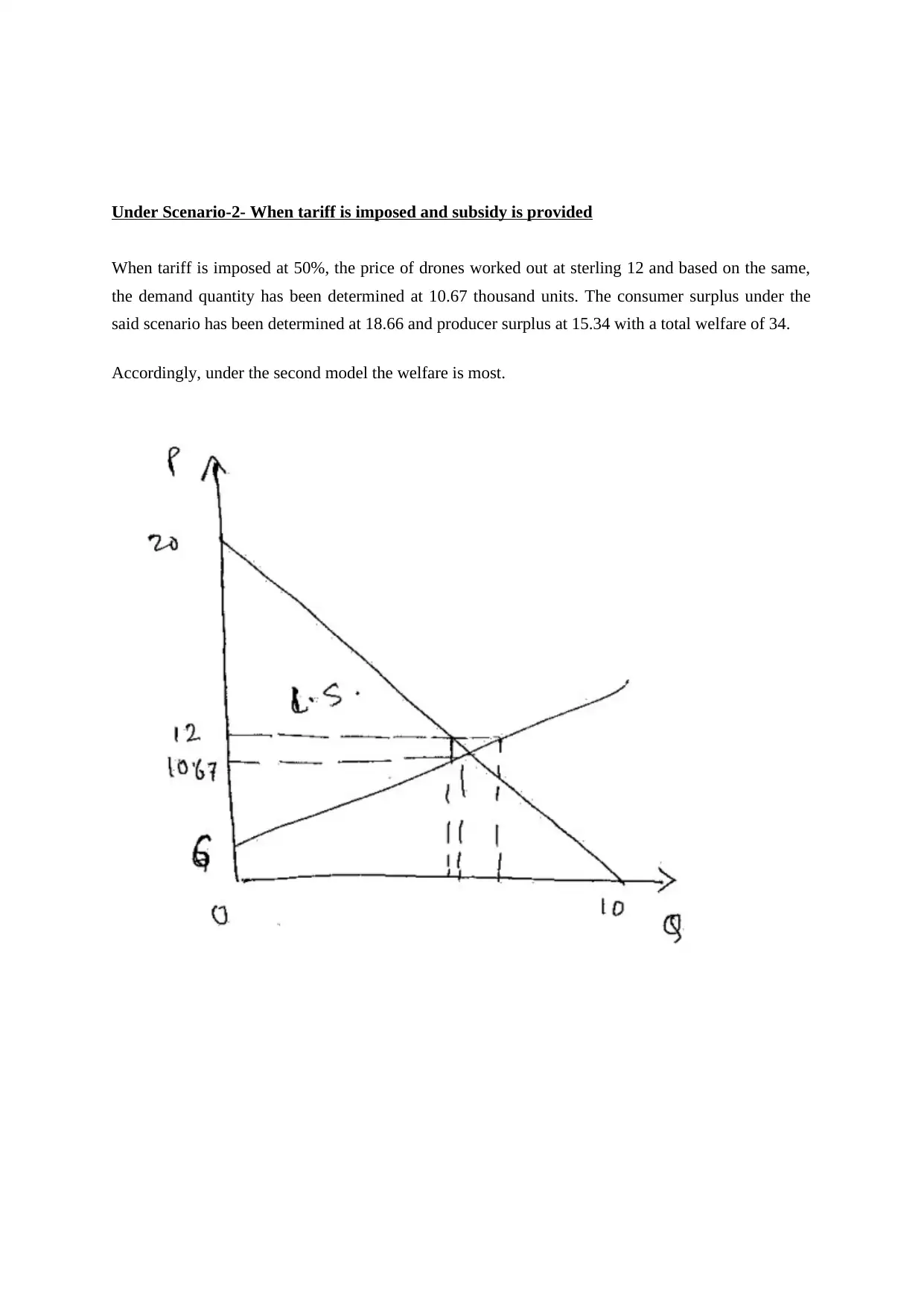

This assignment analyzes the financial sustainability of two banks (Bank A and Bank B) under various scenarios involving non-performing loans (NPLs). It assesses the impact of NPLs on the banks' capital adequacy ratios (CAR) and profitability, considering adjustments like loan loss provisions and new share issues. The assignment also examines the economic sustainability of an infant protection policy, evaluating consumer surplus, producer surplus, and total welfare under free market conditions, with tariffs, and with tariffs and subsidies. The analysis involves calculating equilibrium prices and quantities, and assessing the impact of different policy interventions on market outcomes and overall welfare. The analysis demonstrates the impact of these factors on the banks' financial health and the economic implications of different policy choices.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.