Financial Management: Effective Decision Making and Stakeholder Value

VerifiedAdded on 2023/01/11

|19

|5691

|87

Report

AI Summary

This report delves into financial management principles, exploring effective decision-making approaches, stakeholder management, and the value of management accounting in cost control and maximizing shareholder value. It examines techniques for fraud detection and prevention, alongside a ratio analysis of J Sainsbury Plc from 2018 to 2020, assessing data for operational and strategic decisions. The report further discusses investment appraisal techniques, financial decision-making's impact on long-term sustainability, and provides recommendations for improving financial sustainability. It highlights the importance of management accounting practices in making informed business decisions and managing stakeholder conflicts.

Financial

Management

TABLE OF CONTENTS

Management

TABLE OF CONTENTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

Scenario A........................................................................................................................................3

Range of approaches, factors and techniques of effective decision making................................3

Stakeholder management and conflicting objective.....................................................................4

Value of management accounting cost control and maximizing the shareholder’s value...........5

Techniques of fraud detection and prevention.............................................................................6

Reflection.....................................................................................................................................7

Scenario B........................................................................................................................................8

Ratio analysis of J Sainsbury Plc for the year 2018, 2019 and 2020...........................................8

Data obtained useful in operational and strategic decisions making.........................................14

Investment appraisal techniques that will help in maximizing the return on investment..........15

Techniques useful in informed decision making........................................................................15

Analyzing financial decision making supports long-term sustainability...................................16

Recommendation how management can improve financial sustainability................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

Scenario A........................................................................................................................................3

Range of approaches, factors and techniques of effective decision making................................3

Stakeholder management and conflicting objective.....................................................................4

Value of management accounting cost control and maximizing the shareholder’s value...........5

Techniques of fraud detection and prevention.............................................................................6

Reflection.....................................................................................................................................7

Scenario B........................................................................................................................................8

Ratio analysis of J Sainsbury Plc for the year 2018, 2019 and 2020...........................................8

Data obtained useful in operational and strategic decisions making.........................................14

Investment appraisal techniques that will help in maximizing the return on investment..........15

Techniques useful in informed decision making........................................................................15

Analyzing financial decision making supports long-term sustainability...................................16

Recommendation how management can improve financial sustainability................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Financial management is essential part of every business organization organization or it

can be considered as a function of management with the main role is to effectively manage the

financial resources with respect to the procurement, allocation and application of it. This report

provides an insight about the value of management accounting techniques and approaches which

can be beneficial for the organization in terms of cost control and the increasing the shareholder

value. It also covers the ratio analysis of Sainsbury with the aim of evaluating its performance

and effectiveness of financial decision making in achieving long term sustainability.

Scenario A

Range of approaches, factors and techniques of effective decision making

For the business to be successful the most essential thing for the business is the proper

and effective decision making (Kadoić, Divjak and Ređep, 2019). This is essential because of the

reason that if the decision will not be taken in proper manner then the working of the company

will not be good. For taking effective decision there are different approaches, techniques and

factors affecting it which are as follows-

Approaches to decision making- the major approaches which can assist company in

managing the decision in effective manner are as follows-

Autocratic approach- under this approach the top management of the company only has

the power to take the decision. This is due to the fact that the role of top management is to work

for the betterment of the company and for this they will take more effective decision.

Democratic approach- under this type of approach the top management and the decision

making team also takes the suggestion and reviews of the other employees as well (Snow, 2018).

This is majorly because of the reason that the when the top management takes the ideas of the

subordinates then this will have much better decision making. This is majorly because of the

reason that the subordinates are the one which actually works and they know what is good for the

working and what is not.

Techniques of decision making- the techniques are the one which includes the methods

through which effective decision can be taken. These techniques are as follows-

Financial management is essential part of every business organization organization or it

can be considered as a function of management with the main role is to effectively manage the

financial resources with respect to the procurement, allocation and application of it. This report

provides an insight about the value of management accounting techniques and approaches which

can be beneficial for the organization in terms of cost control and the increasing the shareholder

value. It also covers the ratio analysis of Sainsbury with the aim of evaluating its performance

and effectiveness of financial decision making in achieving long term sustainability.

Scenario A

Range of approaches, factors and techniques of effective decision making

For the business to be successful the most essential thing for the business is the proper

and effective decision making (Kadoić, Divjak and Ređep, 2019). This is essential because of the

reason that if the decision will not be taken in proper manner then the working of the company

will not be good. For taking effective decision there are different approaches, techniques and

factors affecting it which are as follows-

Approaches to decision making- the major approaches which can assist company in

managing the decision in effective manner are as follows-

Autocratic approach- under this approach the top management of the company only has

the power to take the decision. This is due to the fact that the role of top management is to work

for the betterment of the company and for this they will take more effective decision.

Democratic approach- under this type of approach the top management and the decision

making team also takes the suggestion and reviews of the other employees as well (Snow, 2018).

This is majorly because of the reason that the when the top management takes the ideas of the

subordinates then this will have much better decision making. This is majorly because of the

reason that the subordinates are the one which actually works and they know what is good for the

working and what is not.

Techniques of decision making- the techniques are the one which includes the methods

through which effective decision can be taken. These techniques are as follows-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Brainstorming- this is the most common and important technique for taking the decision

(Cristofaro, 2017). Under this technique all the people involved in the decision making process

sits together and then they discuss over the issue for which the decision need to be taken.

Simulation- this is another major important tool or technique of decision making as

under this method the people try to create the same situation for which the decision is to be taken

(Sandhu and Sood, 2017). This role play helps the company in managing all the activities which

will take place and will assist the management in analyzing the situation in advance and then

take decision for managing that situation.

Factors affecting decision making- in addition to all these approaches and techniques

there are also some of the factors which affects the decision making process of the company.

These factors are as follows-

Working environment- this is a major factor which may affect the decision making

process of the company (Khan, Akhtar and Merali, 2018). This is majorly because of the reason

that when the working environment of the company is not coordinated then the company is not

able to take the effective decision. The major reason underlying this fact is that if there will not

be proper coordination then the proper information will not be available and decision will not be

made in effective manner.

Perception of employees- this is another major factor which affects the working of the

company and the process of effective decision making. This is certainly due to the fact that every

person has their own perception and way of thinking (Shahzad and et.al, 2018). Thus, it is very

essential for the people who takes the decision to make sure that all the people who are

responsible for the decision are same or similar in the way of thinking so that identical decision

can be taken.

Stakeholder management and conflicting objective

Stakeholder management is the process or series of steps through which the company

plan and manages to build good relation with the stakeholders. The stakeholders are the people

who are interested in the working and operations of the company. These stakeholders can be

either internal or external to the company and it is the responsibility of the company to manage

their needs and requirements. Every stakeholder has different types of need and interest and for

(Cristofaro, 2017). Under this technique all the people involved in the decision making process

sits together and then they discuss over the issue for which the decision need to be taken.

Simulation- this is another major important tool or technique of decision making as

under this method the people try to create the same situation for which the decision is to be taken

(Sandhu and Sood, 2017). This role play helps the company in managing all the activities which

will take place and will assist the management in analyzing the situation in advance and then

take decision for managing that situation.

Factors affecting decision making- in addition to all these approaches and techniques

there are also some of the factors which affects the decision making process of the company.

These factors are as follows-

Working environment- this is a major factor which may affect the decision making

process of the company (Khan, Akhtar and Merali, 2018). This is majorly because of the reason

that when the working environment of the company is not coordinated then the company is not

able to take the effective decision. The major reason underlying this fact is that if there will not

be proper coordination then the proper information will not be available and decision will not be

made in effective manner.

Perception of employees- this is another major factor which affects the working of the

company and the process of effective decision making. This is certainly due to the fact that every

person has their own perception and way of thinking (Shahzad and et.al, 2018). Thus, it is very

essential for the people who takes the decision to make sure that all the people who are

responsible for the decision are same or similar in the way of thinking so that identical decision

can be taken.

Stakeholder management and conflicting objective

Stakeholder management is the process or series of steps through which the company

plan and manages to build good relation with the stakeholders. The stakeholders are the people

who are interested in the working and operations of the company. These stakeholders can be

either internal or external to the company and it is the responsibility of the company to manage

their needs and requirements. Every stakeholder has different types of need and interest and for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

managing this it is essential for the company to first understand the requirement of the

stakeholders.

There are different stakeholders like consumer, employees, suppliers, owners,

shareholders, government, creditors and many other type of stakeholder. All the different

stakeholder has different types of need and requirement and interest within the company. For

instance, the consumers are interested that company provides for good quality products at

reasonable price. On the other hand, government thinks that the company earns good amount of

profits so that they can charge high taxes over the income earned by the company (van Niekerk

and Getz, 2019).

There are always the conflicts among the objectives of the various stakeholders as the

need and interest and requirement of all the stakeholder is different. Thus, there is many a times

conflict between the objectives of the company and the stakeholders. For instance, the major

objective of the shareholder is to cut the cost and focus on the bulk production of the goods and

services wherein some compromise with the quality is done. But on the other side another

stakeholder that is consumer is the one whose major objective is good quality product and that to

with a reasonable price. Thus, in this case both the stakeholders are having conflicting objective

as one states that the cost must be reduced event at the cost of quality and other states that quality

need to be superior (Oppong, Chan and Dansoh, 2017).

On the flip side the government which is another external stakeholder states that the profit of the

company must be high so that they can charge high taxes from the company. But in against of

this the shareholders want that they pay less taxes as this will reduce the amount of dividend for

the shareholder and the profits of the company as well. Hence, in the end it can be said that the

management of the stakeholder and their need and requirement is very essential for the success

of the company. This is majorly because of the reason that if the stakeholder will not be happy

and satisfied then the company will not be able to get success. Thus, it is very necessary and

crucial for the company to manage the working and efficiency of the company.

For example, the major interest of the employees within the company and its working is related

to getting high bonus and extra payment. But in against of this the owner of the company aims at

reducing the cost of the company by deducting the extra payment of the employees.

stakeholders.

There are different stakeholders like consumer, employees, suppliers, owners,

shareholders, government, creditors and many other type of stakeholder. All the different

stakeholder has different types of need and requirement and interest within the company. For

instance, the consumers are interested that company provides for good quality products at

reasonable price. On the other hand, government thinks that the company earns good amount of

profits so that they can charge high taxes over the income earned by the company (van Niekerk

and Getz, 2019).

There are always the conflicts among the objectives of the various stakeholders as the

need and interest and requirement of all the stakeholder is different. Thus, there is many a times

conflict between the objectives of the company and the stakeholders. For instance, the major

objective of the shareholder is to cut the cost and focus on the bulk production of the goods and

services wherein some compromise with the quality is done. But on the other side another

stakeholder that is consumer is the one whose major objective is good quality product and that to

with a reasonable price. Thus, in this case both the stakeholders are having conflicting objective

as one states that the cost must be reduced event at the cost of quality and other states that quality

need to be superior (Oppong, Chan and Dansoh, 2017).

On the flip side the government which is another external stakeholder states that the profit of the

company must be high so that they can charge high taxes from the company. But in against of

this the shareholders want that they pay less taxes as this will reduce the amount of dividend for

the shareholder and the profits of the company as well. Hence, in the end it can be said that the

management of the stakeholder and their need and requirement is very essential for the success

of the company. This is majorly because of the reason that if the stakeholder will not be happy

and satisfied then the company will not be able to get success. Thus, it is very necessary and

crucial for the company to manage the working and efficiency of the company.

For example, the major interest of the employees within the company and its working is related

to getting high bonus and extra payment. But in against of this the owner of the company aims at

reducing the cost of the company by deducting the extra payment of the employees.

Value of management accounting cost control and maximizing the shareholder’s value

There are different types of management accounting techniques which add significant

value to the organization. But in terms of cost control and increasing the shareholder’s value,

there are mainly two main techniques or standards which are internal and external standards

(Pradhan, Swain and Dash, 2018). A detailed description is given below.

External standards are used for comparing the performance of the organization with its

competitors within the industry. This comparison is manly in respect to the cost and cost related

ratios which helps in determining the areas of improvement in the organization.

Internal standards, in contract to the above, is used in infra firm evaluation of the cost

which includes material, labor, processing cost and so forth (Garcia Osma and et.al, 2020). There

are two types of internal standards which are used for budgetary control and standard costing are

stated below.

Budgetary control

This technique is derived from the concept of budget. It is mainly the budgeted plan

which is formulated for the specific period and is used as the planning and controlling tool for

effective management of the organizational activities (Ameen and et.al, 2018). It provides pre-

determined objectives along with the basis which is used in measuring the performance in

respect to the objectives set. It assists in integrating the business activities all together and also

provides a standard based on which the actual outcome is compared to the budgeted ones. Also

helps in avoiding unnecessary expenses which leads to reduction in cost and consequently leads

to increase in shareholders’ value.

Standard costing

It is mostly used for the purpose of cost control. It establishes the standards and targets

which are required to be achieved under the given set of working conditions. It helps in

evaluation the cost and benefit associated with each of the product and services of the

organization (Paul, 2020). It is the yardstick with which efficiency is measured and controlled. It

assists in optimum utilization of resources which leads to cost management and reduction as

well. The variance analysis and reporting will also help in taking corrective actions.

There are different types of management accounting techniques which add significant

value to the organization. But in terms of cost control and increasing the shareholder’s value,

there are mainly two main techniques or standards which are internal and external standards

(Pradhan, Swain and Dash, 2018). A detailed description is given below.

External standards are used for comparing the performance of the organization with its

competitors within the industry. This comparison is manly in respect to the cost and cost related

ratios which helps in determining the areas of improvement in the organization.

Internal standards, in contract to the above, is used in infra firm evaluation of the cost

which includes material, labor, processing cost and so forth (Garcia Osma and et.al, 2020). There

are two types of internal standards which are used for budgetary control and standard costing are

stated below.

Budgetary control

This technique is derived from the concept of budget. It is mainly the budgeted plan

which is formulated for the specific period and is used as the planning and controlling tool for

effective management of the organizational activities (Ameen and et.al, 2018). It provides pre-

determined objectives along with the basis which is used in measuring the performance in

respect to the objectives set. It assists in integrating the business activities all together and also

provides a standard based on which the actual outcome is compared to the budgeted ones. Also

helps in avoiding unnecessary expenses which leads to reduction in cost and consequently leads

to increase in shareholders’ value.

Standard costing

It is mostly used for the purpose of cost control. It establishes the standards and targets

which are required to be achieved under the given set of working conditions. It helps in

evaluation the cost and benefit associated with each of the product and services of the

organization (Paul, 2020). It is the yardstick with which efficiency is measured and controlled. It

assists in optimum utilization of resources which leads to cost management and reduction as

well. The variance analysis and reporting will also help in taking corrective actions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Techniques of fraud detection and prevention

There are various techniques and approaches that can be used by the organization with

the objective of preventing and detecting the fraud at the right time. Few of the important steps

that can be taken by the organization are given below.

Identifying the potential frauds

The company should work on identifying the major areas where there is a major chances

of detecting fraud. The complete list should be prepared based on the priorities (Fadilah and et.al,

2019). After which the type of risk and exposure is identified. The company should also aim at

areas and risks that has an influence over the shareholder’s value.

Implement continuous auditing and monitoring system

Exercising control over the transactions and introducing the continuous auditing in order

to test and validate the effectiveness of the data (White, 2018). Regular audit can be done by

setting up the scripts which runs across all the data which are large in volume as it helps in

identifying the anomalies that might occur over a period. This will help in improving the

efficiency, consistency and the quality of fraud detection processes.

Communicating the monitoring activity in the organization

The most important technique is communicating the systems and the activities introduced

in the organization to its employees (Simeon, 2018). If everyone in the organization is aware of

the fraud detection systems putted in place will help in reducing the chances of the occurrence of

fraud. This will stop the person from carrying out any activity which will breach the control

system and get identified. This is the great preventive measure that can be taken by the

organization. For example, if an employee is thinking to conduct something wrong but after

communicating about the monitoring system, he /she will not be doing it.

Reflection

After evaluating the above questions, I can say that the management accounting practices

has an immense importance in an organization. The techniques and approaches associated with it

helps in taking better and improved business decisions which is very crucial for the effective

business decision making processes. The conflicts which arises because of the existence of the

There are various techniques and approaches that can be used by the organization with

the objective of preventing and detecting the fraud at the right time. Few of the important steps

that can be taken by the organization are given below.

Identifying the potential frauds

The company should work on identifying the major areas where there is a major chances

of detecting fraud. The complete list should be prepared based on the priorities (Fadilah and et.al,

2019). After which the type of risk and exposure is identified. The company should also aim at

areas and risks that has an influence over the shareholder’s value.

Implement continuous auditing and monitoring system

Exercising control over the transactions and introducing the continuous auditing in order

to test and validate the effectiveness of the data (White, 2018). Regular audit can be done by

setting up the scripts which runs across all the data which are large in volume as it helps in

identifying the anomalies that might occur over a period. This will help in improving the

efficiency, consistency and the quality of fraud detection processes.

Communicating the monitoring activity in the organization

The most important technique is communicating the systems and the activities introduced

in the organization to its employees (Simeon, 2018). If everyone in the organization is aware of

the fraud detection systems putted in place will help in reducing the chances of the occurrence of

fraud. This will stop the person from carrying out any activity which will breach the control

system and get identified. This is the great preventive measure that can be taken by the

organization. For example, if an employee is thinking to conduct something wrong but after

communicating about the monitoring system, he /she will not be doing it.

Reflection

After evaluating the above questions, I can say that the management accounting practices

has an immense importance in an organization. The techniques and approaches associated with it

helps in taking better and improved business decisions which is very crucial for the effective

business decision making processes. The conflicts which arises because of the existence of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

different interest groups in the organization which has a huge impact over the decision making

process. The businesses are required to consider the welfare of the each and every person having

interest in the organization. The proper evaluation of each aspect is carried out which helps in

taking informed decisions which results into meeting the goals and objectives of every

stakeholder in the organization. The implementation of various management accounting

techniques such as budgetary standards and standard costing provides assistance to the

organization in respect to meeting the set targets and objectives. This will result into effective

management of the business operations and the processes which helps the business organization

in identifying the areas where actions can be taken in order to reduce the unnecessary cost. The

reduction in cost will lead to increase in the profitability of the organization and will

consequently lead to increase in the shareholder’s value. Also, various steps can be taken by the

organization in order to prevent and detect fraud on time.

These steps will help the business entity in working in an ethical manner which will

result into ethical decision making. All these together will work on ensuring that the company

achieves its goal of long term sustainability. Thus, management accounting along with its

various approaches and techniques is very useful for a business organization in taking crucial

business decisions.

Scenario B

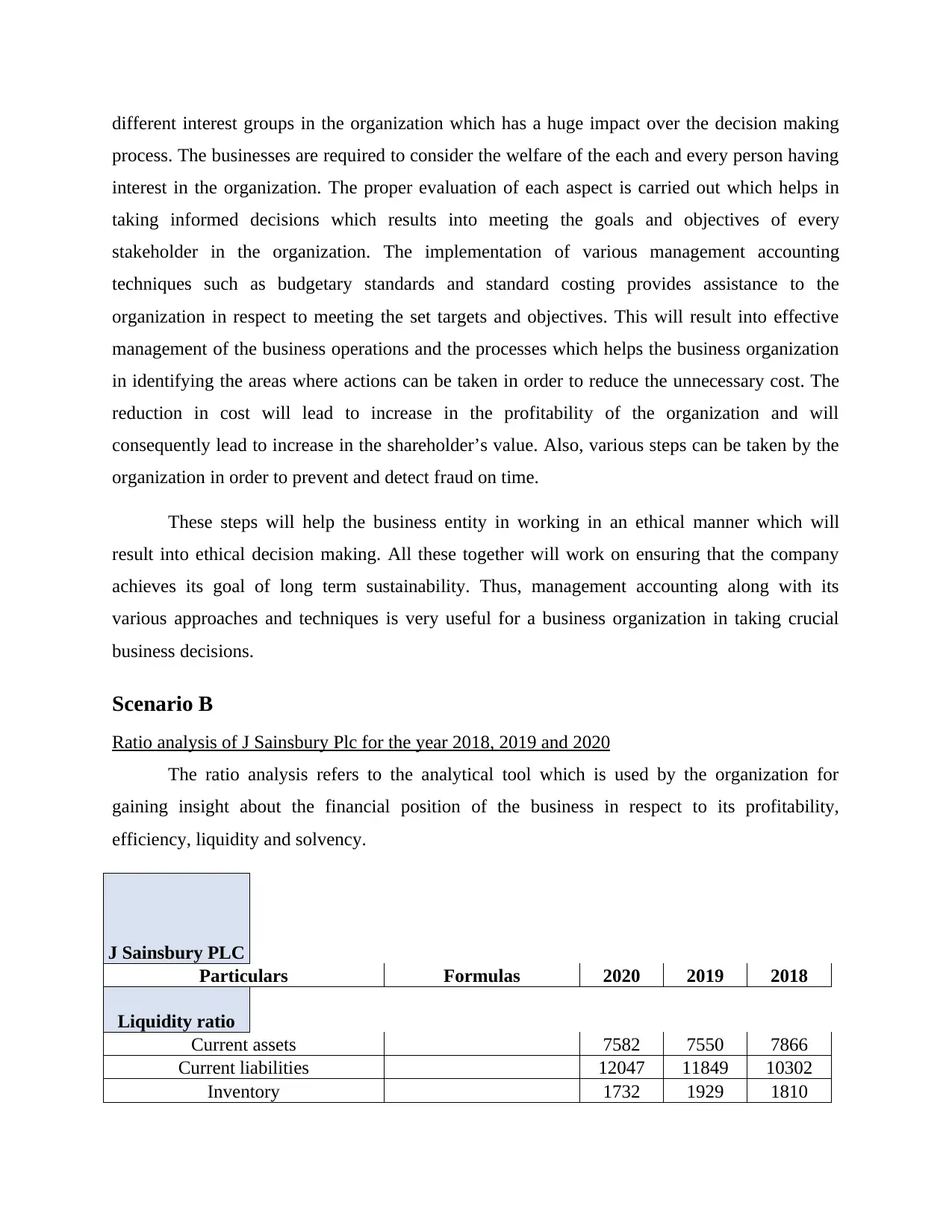

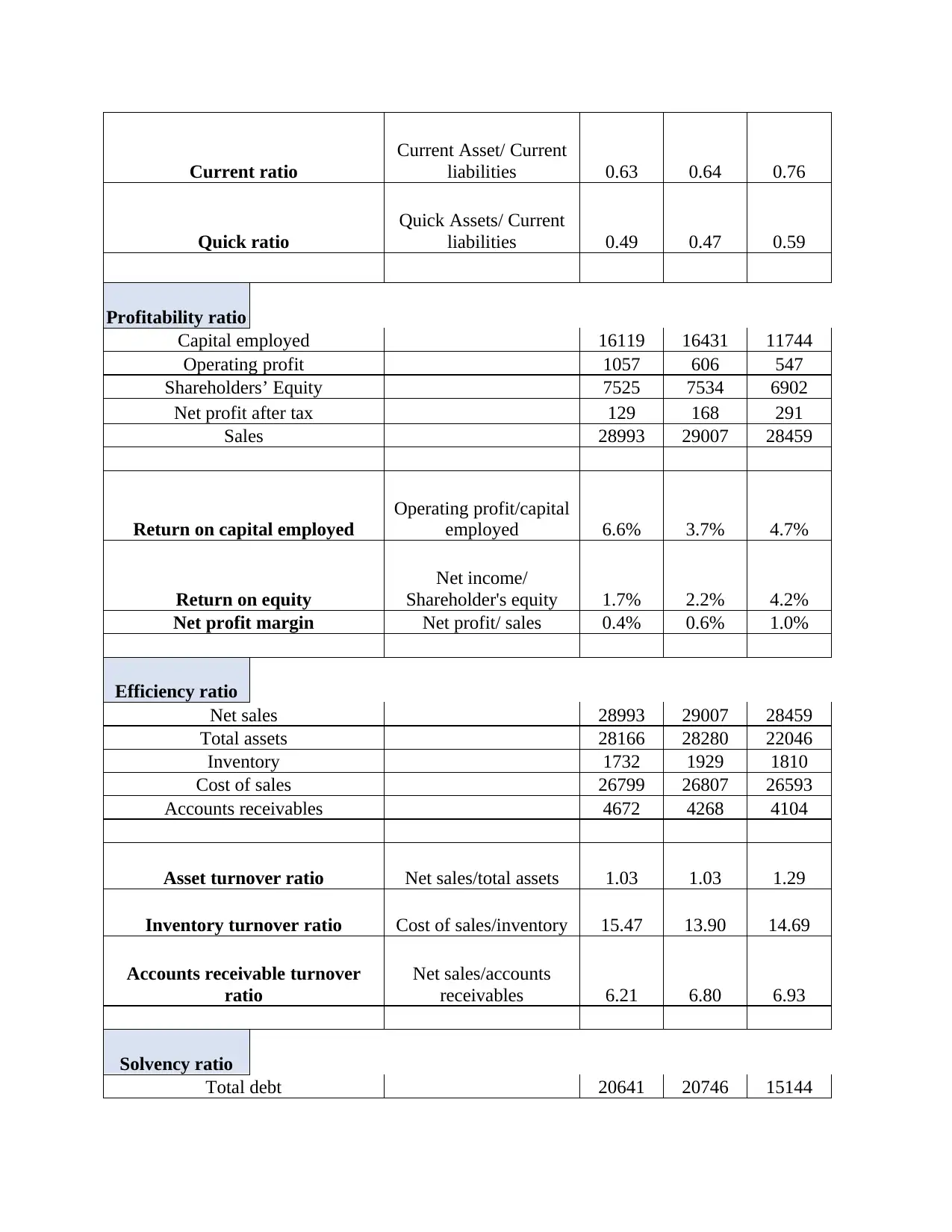

Ratio analysis of J Sainsbury Plc for the year 2018, 2019 and 2020

The ratio analysis refers to the analytical tool which is used by the organization for

gaining insight about the financial position of the business in respect to its profitability,

efficiency, liquidity and solvency.

J Sainsbury PLC

Particulars Formulas 2020 2019 2018

Liquidity ratio

Current assets 7582 7550 7866

Current liabilities 12047 11849 10302

Inventory 1732 1929 1810

process. The businesses are required to consider the welfare of the each and every person having

interest in the organization. The proper evaluation of each aspect is carried out which helps in

taking informed decisions which results into meeting the goals and objectives of every

stakeholder in the organization. The implementation of various management accounting

techniques such as budgetary standards and standard costing provides assistance to the

organization in respect to meeting the set targets and objectives. This will result into effective

management of the business operations and the processes which helps the business organization

in identifying the areas where actions can be taken in order to reduce the unnecessary cost. The

reduction in cost will lead to increase in the profitability of the organization and will

consequently lead to increase in the shareholder’s value. Also, various steps can be taken by the

organization in order to prevent and detect fraud on time.

These steps will help the business entity in working in an ethical manner which will

result into ethical decision making. All these together will work on ensuring that the company

achieves its goal of long term sustainability. Thus, management accounting along with its

various approaches and techniques is very useful for a business organization in taking crucial

business decisions.

Scenario B

Ratio analysis of J Sainsbury Plc for the year 2018, 2019 and 2020

The ratio analysis refers to the analytical tool which is used by the organization for

gaining insight about the financial position of the business in respect to its profitability,

efficiency, liquidity and solvency.

J Sainsbury PLC

Particulars Formulas 2020 2019 2018

Liquidity ratio

Current assets 7582 7550 7866

Current liabilities 12047 11849 10302

Inventory 1732 1929 1810

Current ratio

Current Asset/ Current

liabilities 0.63 0.64 0.76

Quick ratio

Quick Assets/ Current

liabilities 0.49 0.47 0.59

Profitability ratio

Capital employed 16119 16431 11744

Operating profit 1057 606 547

Shareholders’ Equity 7525 7534 6902

Net profit after tax 129 168 291

Sales 28993 29007 28459

Return on capital employed

Operating profit/capital

employed 6.6% 3.7% 4.7%

Return on equity

Net income/

Shareholder's equity 1.7% 2.2% 4.2%

Net profit margin Net profit/ sales 0.4% 0.6% 1.0%

Efficiency ratio

Net sales 28993 29007 28459

Total assets 28166 28280 22046

Inventory 1732 1929 1810

Cost of sales 26799 26807 26593

Accounts receivables 4672 4268 4104

Asset turnover ratio Net sales/total assets 1.03 1.03 1.29

Inventory turnover ratio Cost of sales/inventory 15.47 13.90 14.69

Accounts receivable turnover

ratio

Net sales/accounts

receivables 6.21 6.80 6.93

Solvency ratio

Total debt 20641 20746 15144

Current Asset/ Current

liabilities 0.63 0.64 0.76

Quick ratio

Quick Assets/ Current

liabilities 0.49 0.47 0.59

Profitability ratio

Capital employed 16119 16431 11744

Operating profit 1057 606 547

Shareholders’ Equity 7525 7534 6902

Net profit after tax 129 168 291

Sales 28993 29007 28459

Return on capital employed

Operating profit/capital

employed 6.6% 3.7% 4.7%

Return on equity

Net income/

Shareholder's equity 1.7% 2.2% 4.2%

Net profit margin Net profit/ sales 0.4% 0.6% 1.0%

Efficiency ratio

Net sales 28993 29007 28459

Total assets 28166 28280 22046

Inventory 1732 1929 1810

Cost of sales 26799 26807 26593

Accounts receivables 4672 4268 4104

Asset turnover ratio Net sales/total assets 1.03 1.03 1.29

Inventory turnover ratio Cost of sales/inventory 15.47 13.90 14.69

Accounts receivable turnover

ratio

Net sales/accounts

receivables 6.21 6.80 6.93

Solvency ratio

Total debt 20641 20746 15144

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

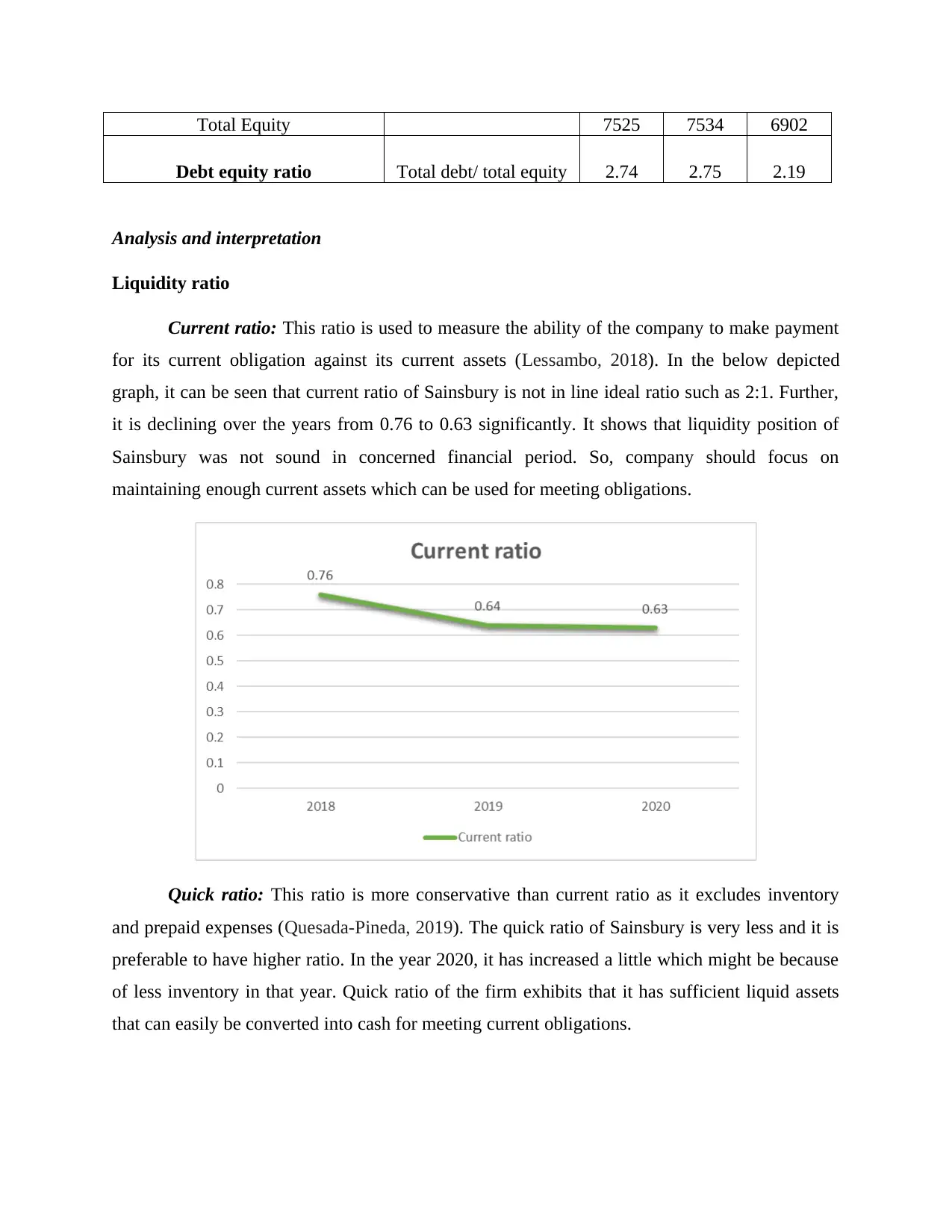

Total Equity 7525 7534 6902

Debt equity ratio Total debt/ total equity 2.74 2.75 2.19

Analysis and interpretation

Liquidity ratio

Current ratio: This ratio is used to measure the ability of the company to make payment

for its current obligation against its current assets (Lessambo, 2018). In the below depicted

graph, it can be seen that current ratio of Sainsbury is not in line ideal ratio such as 2:1. Further,

it is declining over the years from 0.76 to 0.63 significantly. It shows that liquidity position of

Sainsbury was not sound in concerned financial period. So, company should focus on

maintaining enough current assets which can be used for meeting obligations.

Quick ratio: This ratio is more conservative than current ratio as it excludes inventory

and prepaid expenses (Quesada-Pineda, 2019). The quick ratio of Sainsbury is very less and it is

preferable to have higher ratio. In the year 2020, it has increased a little which might be because

of less inventory in that year. Quick ratio of the firm exhibits that it has sufficient liquid assets

that can easily be converted into cash for meeting current obligations.

Debt equity ratio Total debt/ total equity 2.74 2.75 2.19

Analysis and interpretation

Liquidity ratio

Current ratio: This ratio is used to measure the ability of the company to make payment

for its current obligation against its current assets (Lessambo, 2018). In the below depicted

graph, it can be seen that current ratio of Sainsbury is not in line ideal ratio such as 2:1. Further,

it is declining over the years from 0.76 to 0.63 significantly. It shows that liquidity position of

Sainsbury was not sound in concerned financial period. So, company should focus on

maintaining enough current assets which can be used for meeting obligations.

Quick ratio: This ratio is more conservative than current ratio as it excludes inventory

and prepaid expenses (Quesada-Pineda, 2019). The quick ratio of Sainsbury is very less and it is

preferable to have higher ratio. In the year 2020, it has increased a little which might be because

of less inventory in that year. Quick ratio of the firm exhibits that it has sufficient liquid assets

that can easily be converted into cash for meeting current obligations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

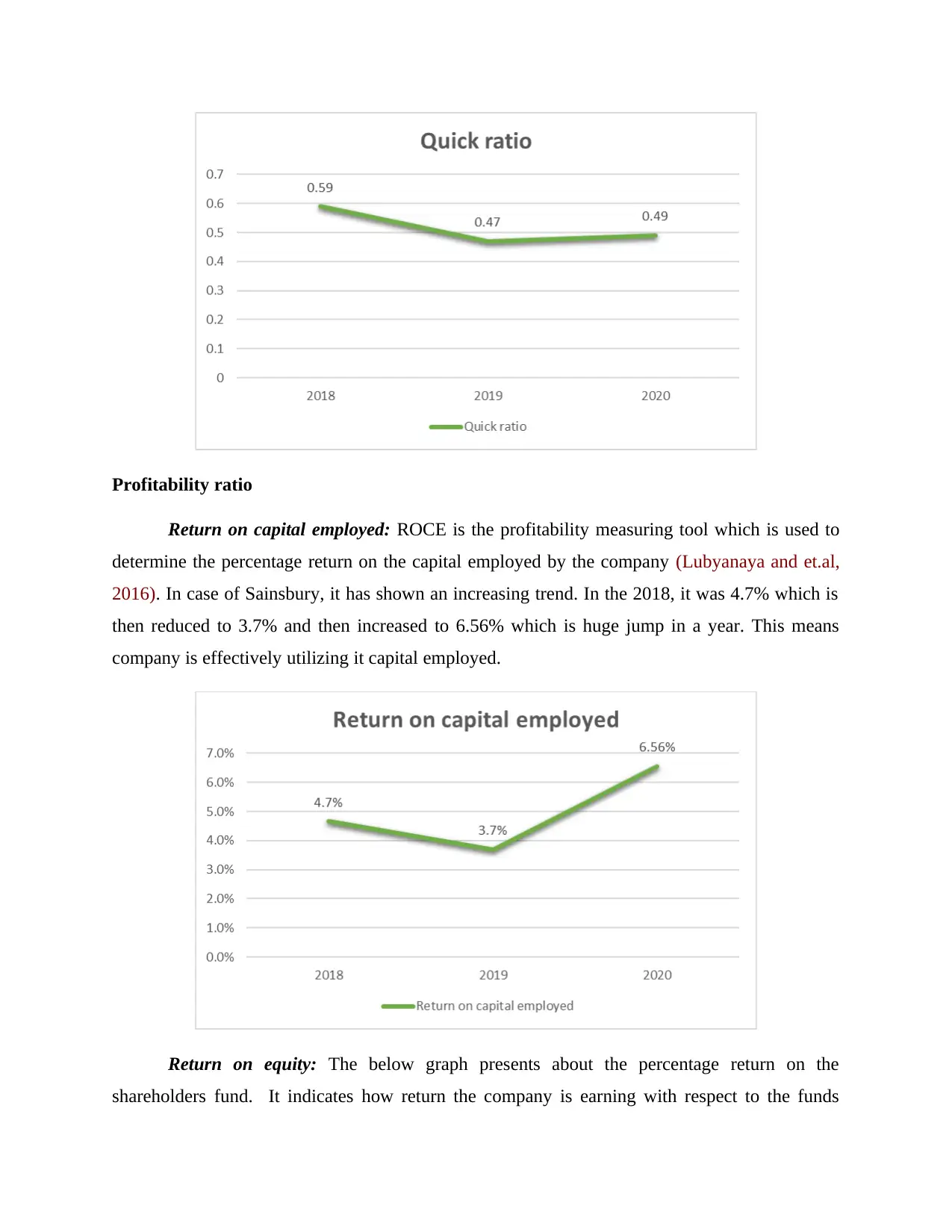

Profitability ratio

Return on capital employed: ROCE is the profitability measuring tool which is used to

determine the percentage return on the capital employed by the company (Lubyanaya and et.al,

2016). In case of Sainsbury, it has shown an increasing trend. In the 2018, it was 4.7% which is

then reduced to 3.7% and then increased to 6.56% which is huge jump in a year. This means

company is effectively utilizing it capital employed.

Return on equity: The below graph presents about the percentage return on the

shareholders fund. It indicates how return the company is earning with respect to the funds

Return on capital employed: ROCE is the profitability measuring tool which is used to

determine the percentage return on the capital employed by the company (Lubyanaya and et.al,

2016). In case of Sainsbury, it has shown an increasing trend. In the 2018, it was 4.7% which is

then reduced to 3.7% and then increased to 6.56% which is huge jump in a year. This means

company is effectively utilizing it capital employed.

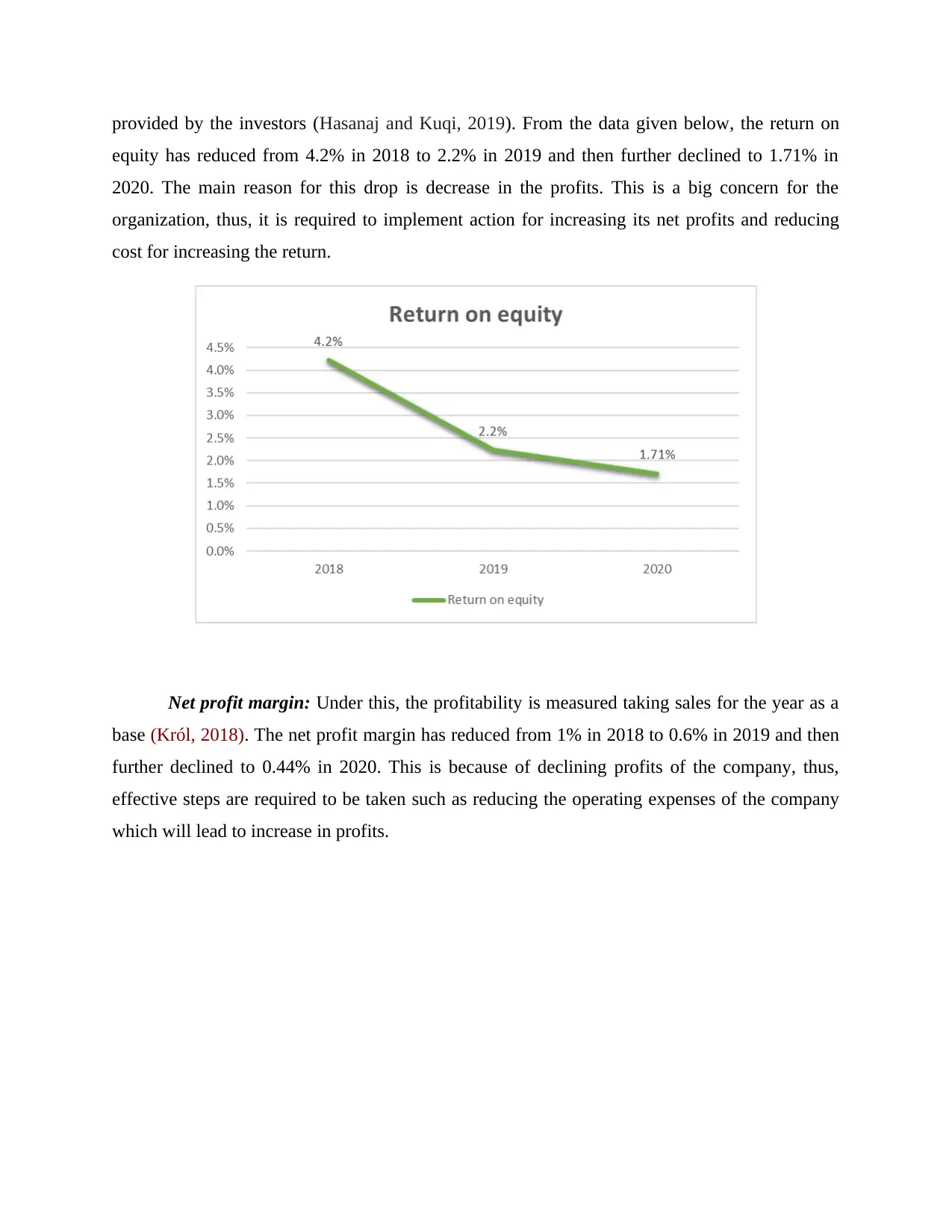

Return on equity: The below graph presents about the percentage return on the

shareholders fund. It indicates how return the company is earning with respect to the funds

provided by the investors (Hasanaj and Kuqi, 2019). From the data given below, the return on

equity has reduced from 4.2% in 2018 to 2.2% in 2019 and then further declined to 1.71% in

2020. The main reason for this drop is decrease in the profits. This is a big concern for the

organization, thus, it is required to implement action for increasing its net profits and reducing

cost for increasing the return.

Net profit margin: Under this, the profitability is measured taking sales for the year as a

base (Król, 2018). The net profit margin has reduced from 1% in 2018 to 0.6% in 2019 and then

further declined to 0.44% in 2020. This is because of declining profits of the company, thus,

effective steps are required to be taken such as reducing the operating expenses of the company

which will lead to increase in profits.

equity has reduced from 4.2% in 2018 to 2.2% in 2019 and then further declined to 1.71% in

2020. The main reason for this drop is decrease in the profits. This is a big concern for the

organization, thus, it is required to implement action for increasing its net profits and reducing

cost for increasing the return.

Net profit margin: Under this, the profitability is measured taking sales for the year as a

base (Król, 2018). The net profit margin has reduced from 1% in 2018 to 0.6% in 2019 and then

further declined to 0.44% in 2020. This is because of declining profits of the company, thus,

effective steps are required to be taken such as reducing the operating expenses of the company

which will lead to increase in profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.