Financial System and Auditing Report: Accounting and Audit Processes

VerifiedAdded on 2020/01/15

|16

|5917

|460

Report

AI Summary

This report provides a comprehensive overview of financial systems and auditing. It begins by defining accounting records and their purpose within an organization, including journals, ledgers, trial balances, and financial statements. The report then delves into fundamental accounting concepts such as dual aspect, accounting period, accounting cost, and accrual concepts, explaining their significance. It further evaluates the factors influencing the nature and structure of accounting systems, like business size, personnel skills, and process complexity. The report identifies the components of business risk, including strategic, financial, and operational risks, and explores ways to detect and prevent fraud. Additionally, it outlines the stages of the audit process, from planning with regard to scope, materiality, and risk to identifying and applying audit tests. The report concludes with the preparation of a draft audit report and management letters.

Financial System and Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Stating the purpose and use of different accounting records within an organization...........1

1.2 Assessing the meaning and importance of fundamental accounting concepts......................3

1.3 Evaluating the factors which influence the nature and structure of accounting systems .....4

TASK 2............................................................................................................................................5

2.1 Identifying the different components of business risk..........................................................5

2.2 Analyzing the control system which take place within the business organization to assess

the fraudulent activities...............................................................................................................6

2.3 Evaluating the risk of fraud within the enterprise and ways to detect such fraudulent.........6

TASK 3............................................................................................................................................8

3.1 Planning an audit with reference to scope, materiality and risk...........................................8

3.2 Identifying and use appropriate audit tests............................................................................8

3.3 Analysis of the stages of the audit process............................................................................9

TASK 4..........................................................................................................................................11

4.1 Preparation of the draft audit report....................................................................................11

4.2 Drafting the suitable management letters in relation to the statutory audit report..............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Stating the purpose and use of different accounting records within an organization...........1

1.2 Assessing the meaning and importance of fundamental accounting concepts......................3

1.3 Evaluating the factors which influence the nature and structure of accounting systems .....4

TASK 2............................................................................................................................................5

2.1 Identifying the different components of business risk..........................................................5

2.2 Analyzing the control system which take place within the business organization to assess

the fraudulent activities...............................................................................................................6

2.3 Evaluating the risk of fraud within the enterprise and ways to detect such fraudulent.........6

TASK 3............................................................................................................................................8

3.1 Planning an audit with reference to scope, materiality and risk...........................................8

3.2 Identifying and use appropriate audit tests............................................................................8

3.3 Analysis of the stages of the audit process............................................................................9

TASK 4..........................................................................................................................................11

4.1 Preparation of the draft audit report....................................................................................11

4.2 Drafting the suitable management letters in relation to the statutory audit report..............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial system consists of the method which facilitates national as well as global

monetary transaction between money lenders, investors and borrowers. Financial system plays a

vital role in mobilizing the saving of household and individual investors by offering attractive

surplus to them (Sikka, 2015). In addition to this, it also encourages entrepreneurship within the

nation by offering financial assistance to business entities at very cost effective rates. Along with

it, auditing is the most essential part of each and every business organization. Auditing refers to

systematic evaluation of the financial records on the basis of vouchers, account books etc.

Through this, business entity is able to represent fair or realistic view of the financial records in

front of the different stakeholders.

The present report will discuss the purposes due to which organization prefers to

maintain accounting records. Further, it will also shed light on the fundamental concepts of

accounting which help company in recording their financial transactions in an effective manner.

This report will also examine the factors which influence the structure of accounting system.

Besides this, it depicts about the different components of business risk as well as various ways

through which firm can detect fraud from the financial records. In addition to this, present

project report will develop understanding about the stages of audit which helps company in

finding fraud.

TASK 1

1.1 Stating the purpose and use of different accounting records within an organization

Accounting records may be defined as a documentation of all the financial transactions

which are made by an organization during the financial year. It includes journal, ledger, trial

balance and financial statements of an organization. Accounting records provide assistance to the

finance manager in representing the fair view of financial statements of an organization.

Purpose and use of different accounting records within CAMIC Associates Ltd. are

enumerated below: Journals or prime entry book: It refers to book which records all the monetary

transactions along with their dates which are made by an organization. It involves sales

book, purchase book, cash book etc. which separately provide information about the

organizational transactions. Each and every organization prepares journal in order to get

1

Financial system consists of the method which facilitates national as well as global

monetary transaction between money lenders, investors and borrowers. Financial system plays a

vital role in mobilizing the saving of household and individual investors by offering attractive

surplus to them (Sikka, 2015). In addition to this, it also encourages entrepreneurship within the

nation by offering financial assistance to business entities at very cost effective rates. Along with

it, auditing is the most essential part of each and every business organization. Auditing refers to

systematic evaluation of the financial records on the basis of vouchers, account books etc.

Through this, business entity is able to represent fair or realistic view of the financial records in

front of the different stakeholders.

The present report will discuss the purposes due to which organization prefers to

maintain accounting records. Further, it will also shed light on the fundamental concepts of

accounting which help company in recording their financial transactions in an effective manner.

This report will also examine the factors which influence the structure of accounting system.

Besides this, it depicts about the different components of business risk as well as various ways

through which firm can detect fraud from the financial records. In addition to this, present

project report will develop understanding about the stages of audit which helps company in

finding fraud.

TASK 1

1.1 Stating the purpose and use of different accounting records within an organization

Accounting records may be defined as a documentation of all the financial transactions

which are made by an organization during the financial year. It includes journal, ledger, trial

balance and financial statements of an organization. Accounting records provide assistance to the

finance manager in representing the fair view of financial statements of an organization.

Purpose and use of different accounting records within CAMIC Associates Ltd. are

enumerated below: Journals or prime entry book: It refers to book which records all the monetary

transactions along with their dates which are made by an organization. It involves sales

book, purchase book, cash book etc. which separately provide information about the

organizational transactions. Each and every organization prepares journal in order to get

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information about their daily financial activities. In addition to this, Journal provides

assistance to the accountant in preparing ledger of all the financial transactions. Ledgers: It represents individual account of each transaction of the business unit in

relation to sales, purchase, assets, liabilities etc. Firm prepares ledger account in order to

assess the accuracy of journal entries which are recorded in the books of accounts (Ho

and Mallick, 2015). It is one of the main purposes of the enterprise due to which they

prepare ledger accounts. It is used to prepare trial balance of the organization.

Trial balance: It is the summary statement of all the financial transactions which

company has made in the accounting year. Trial balance contains closing balance of all

the ledger accounts. Main purpose behind the preparation of trial balance is to assess

deficiencies of journals as well as ledgers account. Finance manager makes the use of

trial balance in preparing financial statements such as income statement, balance sheet

and cash flow statement.

Financial statements

a. Income statement: It contains information about the revenue or income which is

generated by an organization. In addition to this, it also provides detail about the expenditures

which are incurred by the firm during the accounting period. By preparing income statement,

firm is able to assess their profitability aspects (Fedele, 2015). Company uses income statement

in framing competent strategies or policies which enable them to increase their profit aspect by

making control upon the expenses.

b. Balance sheet: It includes detail about the assets and liabilities of business unit. Main

purpose of the preparation of balance sheet is to provide information to different stakeholders

about the financial position and aspects of the enterprise. Balance sheet helps organization in

making financial plan as well as managing and evaluating the operations of firm.

c. Cash flow statement: It may be defined as a statement which provides information

about operating, investing and financing activities of the enterprise. Each organization prepares

cash flow statement to get information about the cash inflow and outflow (Carnero, 2015). It is

used by an organization in preparing strategies through which they are able to make optimum

utilization of financial resources.

2

assistance to the accountant in preparing ledger of all the financial transactions. Ledgers: It represents individual account of each transaction of the business unit in

relation to sales, purchase, assets, liabilities etc. Firm prepares ledger account in order to

assess the accuracy of journal entries which are recorded in the books of accounts (Ho

and Mallick, 2015). It is one of the main purposes of the enterprise due to which they

prepare ledger accounts. It is used to prepare trial balance of the organization.

Trial balance: It is the summary statement of all the financial transactions which

company has made in the accounting year. Trial balance contains closing balance of all

the ledger accounts. Main purpose behind the preparation of trial balance is to assess

deficiencies of journals as well as ledgers account. Finance manager makes the use of

trial balance in preparing financial statements such as income statement, balance sheet

and cash flow statement.

Financial statements

a. Income statement: It contains information about the revenue or income which is

generated by an organization. In addition to this, it also provides detail about the expenditures

which are incurred by the firm during the accounting period. By preparing income statement,

firm is able to assess their profitability aspects (Fedele, 2015). Company uses income statement

in framing competent strategies or policies which enable them to increase their profit aspect by

making control upon the expenses.

b. Balance sheet: It includes detail about the assets and liabilities of business unit. Main

purpose of the preparation of balance sheet is to provide information to different stakeholders

about the financial position and aspects of the enterprise. Balance sheet helps organization in

making financial plan as well as managing and evaluating the operations of firm.

c. Cash flow statement: It may be defined as a statement which provides information

about operating, investing and financing activities of the enterprise. Each organization prepares

cash flow statement to get information about the cash inflow and outflow (Carnero, 2015). It is

used by an organization in preparing strategies through which they are able to make optimum

utilization of financial resources.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

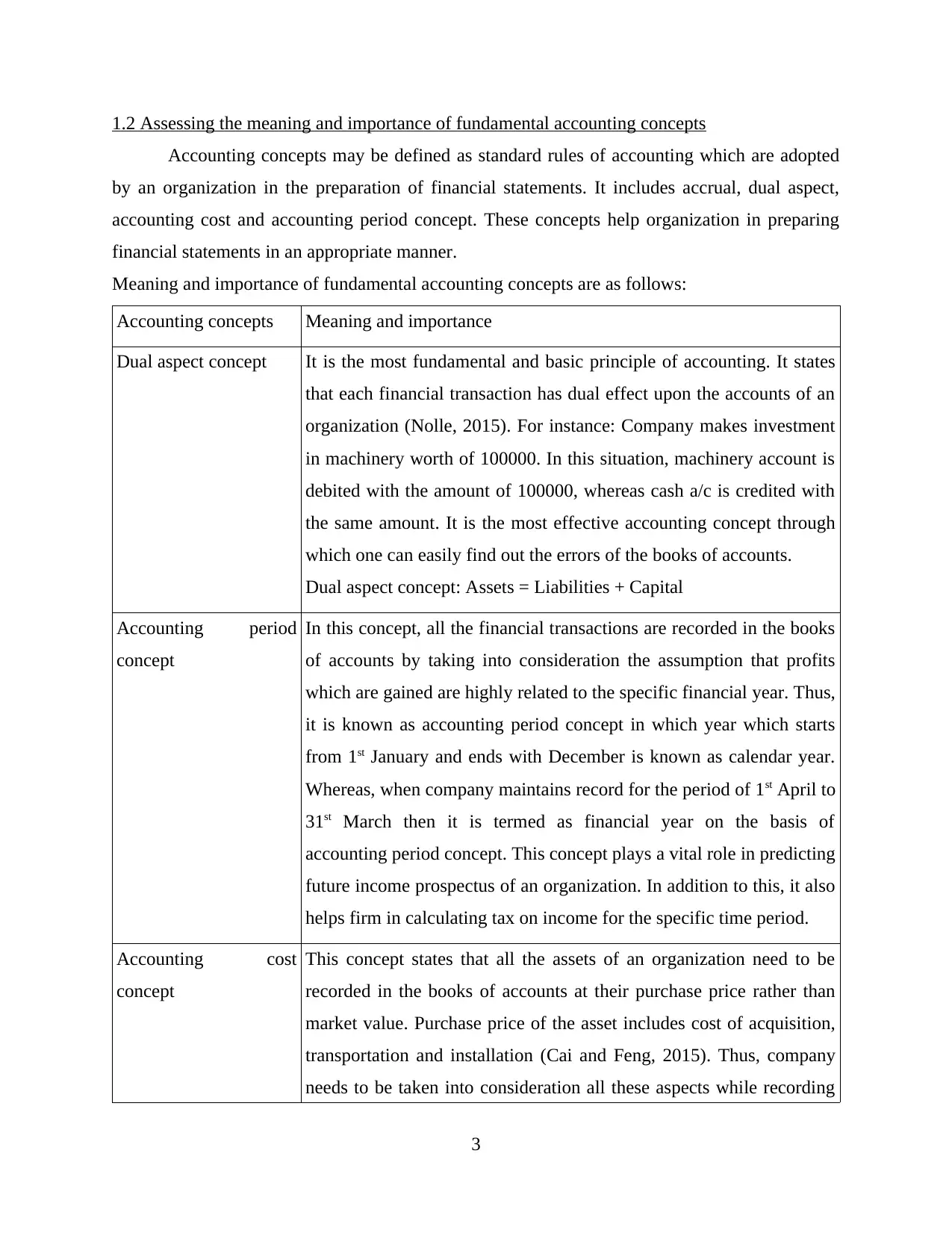

1.2 Assessing the meaning and importance of fundamental accounting concepts

Accounting concepts may be defined as standard rules of accounting which are adopted

by an organization in the preparation of financial statements. It includes accrual, dual aspect,

accounting cost and accounting period concept. These concepts help organization in preparing

financial statements in an appropriate manner.

Meaning and importance of fundamental accounting concepts are as follows:

Accounting concepts Meaning and importance

Dual aspect concept It is the most fundamental and basic principle of accounting. It states

that each financial transaction has dual effect upon the accounts of an

organization (Nolle, 2015). For instance: Company makes investment

in machinery worth of 100000. In this situation, machinery account is

debited with the amount of 100000, whereas cash a/c is credited with

the same amount. It is the most effective accounting concept through

which one can easily find out the errors of the books of accounts.

Dual aspect concept: Assets = Liabilities + Capital

Accounting period

concept

In this concept, all the financial transactions are recorded in the books

of accounts by taking into consideration the assumption that profits

which are gained are highly related to the specific financial year. Thus,

it is known as accounting period concept in which year which starts

from 1st January and ends with December is known as calendar year.

Whereas, when company maintains record for the period of 1st April to

31st March then it is termed as financial year on the basis of

accounting period concept. This concept plays a vital role in predicting

future income prospectus of an organization. In addition to this, it also

helps firm in calculating tax on income for the specific time period.

Accounting cost

concept

This concept states that all the assets of an organization need to be

recorded in the books of accounts at their purchase price rather than

market value. Purchase price of the asset includes cost of acquisition,

transportation and installation (Cai and Feng, 2015). Thus, company

needs to be taken into consideration all these aspects while recording

3

Accounting concepts may be defined as standard rules of accounting which are adopted

by an organization in the preparation of financial statements. It includes accrual, dual aspect,

accounting cost and accounting period concept. These concepts help organization in preparing

financial statements in an appropriate manner.

Meaning and importance of fundamental accounting concepts are as follows:

Accounting concepts Meaning and importance

Dual aspect concept It is the most fundamental and basic principle of accounting. It states

that each financial transaction has dual effect upon the accounts of an

organization (Nolle, 2015). For instance: Company makes investment

in machinery worth of 100000. In this situation, machinery account is

debited with the amount of 100000, whereas cash a/c is credited with

the same amount. It is the most effective accounting concept through

which one can easily find out the errors of the books of accounts.

Dual aspect concept: Assets = Liabilities + Capital

Accounting period

concept

In this concept, all the financial transactions are recorded in the books

of accounts by taking into consideration the assumption that profits

which are gained are highly related to the specific financial year. Thus,

it is known as accounting period concept in which year which starts

from 1st January and ends with December is known as calendar year.

Whereas, when company maintains record for the period of 1st April to

31st March then it is termed as financial year on the basis of

accounting period concept. This concept plays a vital role in predicting

future income prospectus of an organization. In addition to this, it also

helps firm in calculating tax on income for the specific time period.

Accounting cost

concept

This concept states that all the assets of an organization need to be

recorded in the books of accounts at their purchase price rather than

market value. Purchase price of the asset includes cost of acquisition,

transportation and installation (Cai and Feng, 2015). Thus, company

needs to be taken into consideration all these aspects while recording

3

the value of asset. Accounting cost concept is highly significant

because it helps in calculating appropriate depreciation on fixed assets.

In addition to this, following concept also provides assistance in

verifying the value of asset with the help of supporting document at

the time of auditing.

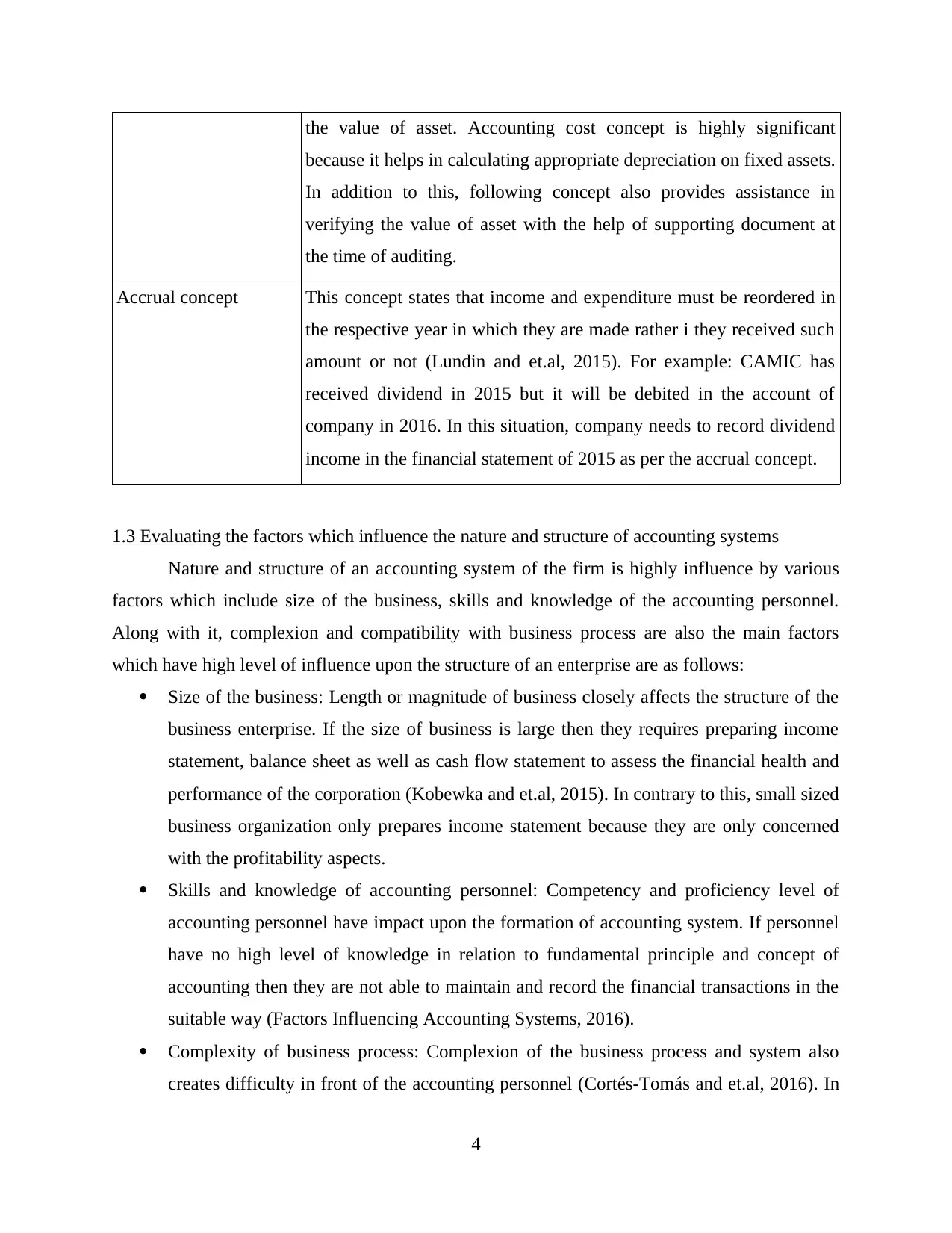

Accrual concept This concept states that income and expenditure must be reordered in

the respective year in which they are made rather i they received such

amount or not (Lundin and et.al, 2015). For example: CAMIC has

received dividend in 2015 but it will be debited in the account of

company in 2016. In this situation, company needs to record dividend

income in the financial statement of 2015 as per the accrual concept.

1.3 Evaluating the factors which influence the nature and structure of accounting systems

Nature and structure of an accounting system of the firm is highly influence by various

factors which include size of the business, skills and knowledge of the accounting personnel.

Along with it, complexion and compatibility with business process are also the main factors

which have high level of influence upon the structure of an enterprise are as follows:

Size of the business: Length or magnitude of business closely affects the structure of the

business enterprise. If the size of business is large then they requires preparing income

statement, balance sheet as well as cash flow statement to assess the financial health and

performance of the corporation (Kobewka and et.al, 2015). In contrary to this, small sized

business organization only prepares income statement because they are only concerned

with the profitability aspects.

Skills and knowledge of accounting personnel: Competency and proficiency level of

accounting personnel have impact upon the formation of accounting system. If personnel

have no high level of knowledge in relation to fundamental principle and concept of

accounting then they are not able to maintain and record the financial transactions in the

suitable way (Factors Influencing Accounting Systems, 2016).

Complexity of business process: Complexion of the business process and system also

creates difficulty in front of the accounting personnel (Cortés-Tomás and et.al, 2016). In

4

because it helps in calculating appropriate depreciation on fixed assets.

In addition to this, following concept also provides assistance in

verifying the value of asset with the help of supporting document at

the time of auditing.

Accrual concept This concept states that income and expenditure must be reordered in

the respective year in which they are made rather i they received such

amount or not (Lundin and et.al, 2015). For example: CAMIC has

received dividend in 2015 but it will be debited in the account of

company in 2016. In this situation, company needs to record dividend

income in the financial statement of 2015 as per the accrual concept.

1.3 Evaluating the factors which influence the nature and structure of accounting systems

Nature and structure of an accounting system of the firm is highly influence by various

factors which include size of the business, skills and knowledge of the accounting personnel.

Along with it, complexion and compatibility with business process are also the main factors

which have high level of influence upon the structure of an enterprise are as follows:

Size of the business: Length or magnitude of business closely affects the structure of the

business enterprise. If the size of business is large then they requires preparing income

statement, balance sheet as well as cash flow statement to assess the financial health and

performance of the corporation (Kobewka and et.al, 2015). In contrary to this, small sized

business organization only prepares income statement because they are only concerned

with the profitability aspects.

Skills and knowledge of accounting personnel: Competency and proficiency level of

accounting personnel have impact upon the formation of accounting system. If personnel

have no high level of knowledge in relation to fundamental principle and concept of

accounting then they are not able to maintain and record the financial transactions in the

suitable way (Factors Influencing Accounting Systems, 2016).

Complexity of business process: Complexion of the business process and system also

creates difficulty in front of the accounting personnel (Cortés-Tomás and et.al, 2016). In

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

complex business accounting personnel faces difficulty in the adoption of suitable

accounting practices.

On the basis of all the above mentioned aspects it can be stated that there are several

factors which impacts the structure of an accounting system.

TASK 2

2.1 Identifying the different components of business risk

Business risk may be defined as a situation inadequate profit and high loss due which

occurs due to uncertainties. There are several causes due to which risk occur within the business

enterprise includes irregular supply of raw material, machinery breakdown, changes in customer

preferences, strike or lockouts etc. All these risk place negative impact upon the profitability

aspect of an organization. There is several type of risk which affects the smooth functioning and

operations of business organization are as follows:

Strategic risk: It consists of the risk which occurs due to changes which take place in the

customer behavior as well in the activities of competitors. Customers’ needs and wants

are changes with the time passes. In addition to this, strategic and policies framed by the

competitors also have significant impact upon the enterprise (Verver, 2015). Thus, all

theses aspect closely affects the operation as well as objective of an organization.

Moreover, company also needs to make changes in their strategies and objectives in

accordance with the competitors’ movement to survive in the competitive business arena.

Financial or monetary risk: It entails the risk which occurs when finance manager fails to

make appropriate financing and investing decisions. For instance: manger of the company

has taken decision to invest money in the new project. In this, if project fails to give

desirable return to the company due to their wrong estimation then such decision closely

impacts the financial aspects of an organization.

Operational risk: This type of risk places adverse impact upon the financial position and

performance of an organization (Kaplan and Atkinson, 2015). For instance: Corporation

fails to make proper estimation of raw material which is required to produce the budgeted

amount of finished goods. In this situation, employees are not able to work more

efficiently due to the unavailability of raw material. Due to the operational risk business

unit has to bear high level of financial loss.

5

accounting practices.

On the basis of all the above mentioned aspects it can be stated that there are several

factors which impacts the structure of an accounting system.

TASK 2

2.1 Identifying the different components of business risk

Business risk may be defined as a situation inadequate profit and high loss due which

occurs due to uncertainties. There are several causes due to which risk occur within the business

enterprise includes irregular supply of raw material, machinery breakdown, changes in customer

preferences, strike or lockouts etc. All these risk place negative impact upon the profitability

aspect of an organization. There is several type of risk which affects the smooth functioning and

operations of business organization are as follows:

Strategic risk: It consists of the risk which occurs due to changes which take place in the

customer behavior as well in the activities of competitors. Customers’ needs and wants

are changes with the time passes. In addition to this, strategic and policies framed by the

competitors also have significant impact upon the enterprise (Verver, 2015). Thus, all

theses aspect closely affects the operation as well as objective of an organization.

Moreover, company also needs to make changes in their strategies and objectives in

accordance with the competitors’ movement to survive in the competitive business arena.

Financial or monetary risk: It entails the risk which occurs when finance manager fails to

make appropriate financing and investing decisions. For instance: manger of the company

has taken decision to invest money in the new project. In this, if project fails to give

desirable return to the company due to their wrong estimation then such decision closely

impacts the financial aspects of an organization.

Operational risk: This type of risk places adverse impact upon the financial position and

performance of an organization (Kaplan and Atkinson, 2015). For instance: Corporation

fails to make proper estimation of raw material which is required to produce the budgeted

amount of finished goods. In this situation, employees are not able to work more

efficiently due to the unavailability of raw material. Due to the operational risk business

unit has to bear high level of financial loss.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

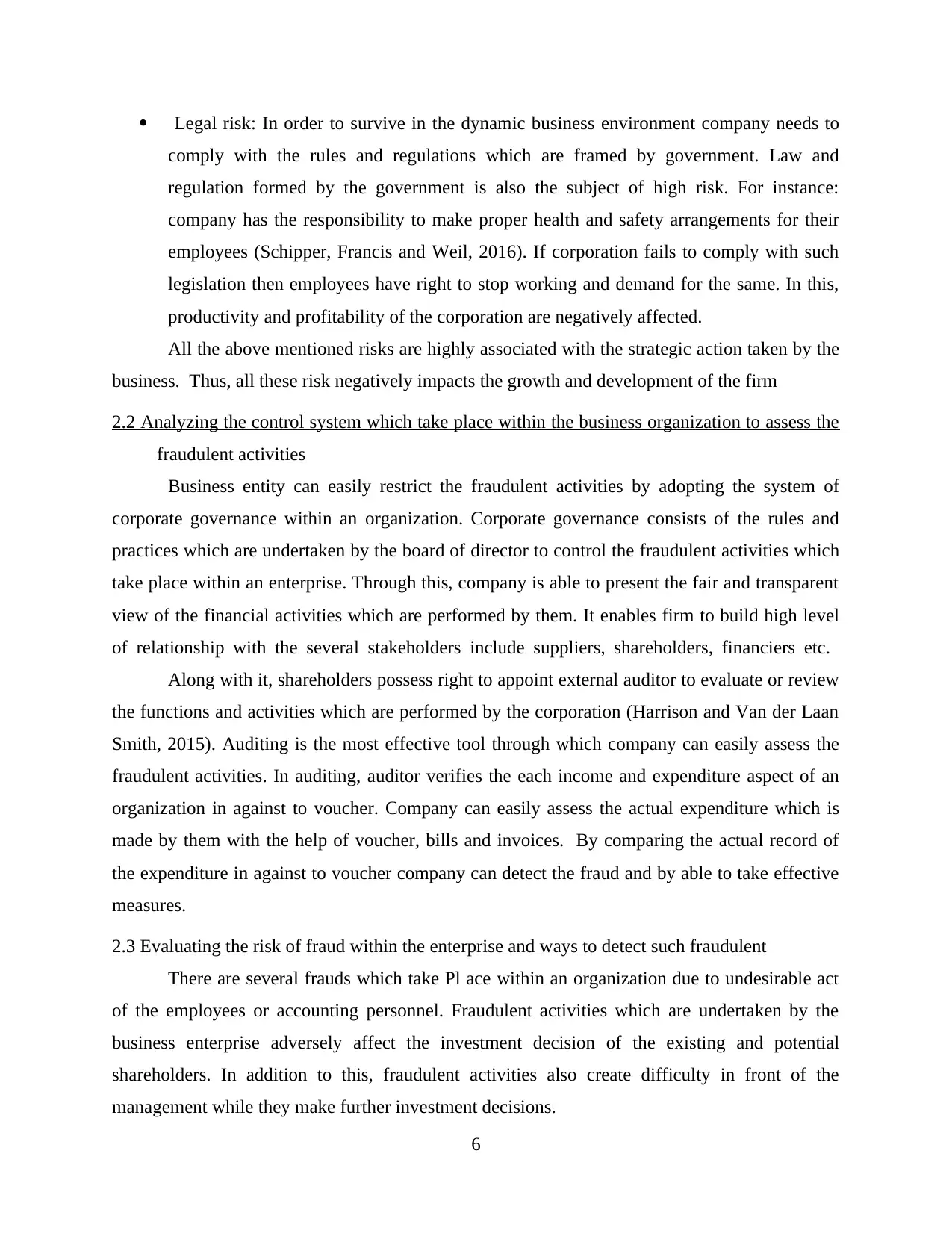

Legal risk: In order to survive in the dynamic business environment company needs to

comply with the rules and regulations which are framed by government. Law and

regulation formed by the government is also the subject of high risk. For instance:

company has the responsibility to make proper health and safety arrangements for their

employees (Schipper, Francis and Weil, 2016). If corporation fails to comply with such

legislation then employees have right to stop working and demand for the same. In this,

productivity and profitability of the corporation are negatively affected.

All the above mentioned risks are highly associated with the strategic action taken by the

business. Thus, all these risk negatively impacts the growth and development of the firm

2.2 Analyzing the control system which take place within the business organization to assess the

fraudulent activities

Business entity can easily restrict the fraudulent activities by adopting the system of

corporate governance within an organization. Corporate governance consists of the rules and

practices which are undertaken by the board of director to control the fraudulent activities which

take place within an enterprise. Through this, company is able to present the fair and transparent

view of the financial activities which are performed by them. It enables firm to build high level

of relationship with the several stakeholders include suppliers, shareholders, financiers etc.

Along with it, shareholders possess right to appoint external auditor to evaluate or review

the functions and activities which are performed by the corporation (Harrison and Van der Laan

Smith, 2015). Auditing is the most effective tool through which company can easily assess the

fraudulent activities. In auditing, auditor verifies the each income and expenditure aspect of an

organization in against to voucher. Company can easily assess the actual expenditure which is

made by them with the help of voucher, bills and invoices. By comparing the actual record of

the expenditure in against to voucher company can detect the fraud and by able to take effective

measures.

2.3 Evaluating the risk of fraud within the enterprise and ways to detect such fraudulent

There are several frauds which take Pl ace within an organization due to undesirable act

of the employees or accounting personnel. Fraudulent activities which are undertaken by the

business enterprise adversely affect the investment decision of the existing and potential

shareholders. In addition to this, fraudulent activities also create difficulty in front of the

management while they make further investment decisions.

6

comply with the rules and regulations which are framed by government. Law and

regulation formed by the government is also the subject of high risk. For instance:

company has the responsibility to make proper health and safety arrangements for their

employees (Schipper, Francis and Weil, 2016). If corporation fails to comply with such

legislation then employees have right to stop working and demand for the same. In this,

productivity and profitability of the corporation are negatively affected.

All the above mentioned risks are highly associated with the strategic action taken by the

business. Thus, all these risk negatively impacts the growth and development of the firm

2.2 Analyzing the control system which take place within the business organization to assess the

fraudulent activities

Business entity can easily restrict the fraudulent activities by adopting the system of

corporate governance within an organization. Corporate governance consists of the rules and

practices which are undertaken by the board of director to control the fraudulent activities which

take place within an enterprise. Through this, company is able to present the fair and transparent

view of the financial activities which are performed by them. It enables firm to build high level

of relationship with the several stakeholders include suppliers, shareholders, financiers etc.

Along with it, shareholders possess right to appoint external auditor to evaluate or review

the functions and activities which are performed by the corporation (Harrison and Van der Laan

Smith, 2015). Auditing is the most effective tool through which company can easily assess the

fraudulent activities. In auditing, auditor verifies the each income and expenditure aspect of an

organization in against to voucher. Company can easily assess the actual expenditure which is

made by them with the help of voucher, bills and invoices. By comparing the actual record of

the expenditure in against to voucher company can detect the fraud and by able to take effective

measures.

2.3 Evaluating the risk of fraud within the enterprise and ways to detect such fraudulent

There are several frauds which take Pl ace within an organization due to undesirable act

of the employees or accounting personnel. Fraudulent activities which are undertaken by the

business enterprise adversely affect the investment decision of the existing and potential

shareholders. In addition to this, fraudulent activities also create difficulty in front of the

management while they make further investment decisions.

6

Risk of fraud: Company faces several risks or problems when fraudulent activities take place

within the business enterprise. Usually, employees of an organization give false record to the

accountant in relation to the expenses which are incurred by them. In this situation, accountant

personnel fail to represent the fair view of the profitability aspects of an organization (Vogel,

2014). In addition to this, business enterprise prefers to represent the high income aspect in

comparison to their expenditure. This aspect is considered as a fraud which is undertaken by an

organization with the aim to attract large number of investors. Such fraudulent activities

negatively affect the brand value or image of an organization in front of the several stakeholders.

Along with it, firm also make modification in their financial statement to save the tax

amount which they require to pay the government on the basis of laws and legislation. It is the

main cause due to which organization show high level of expenditure as compared to the actual

expenses incurred by them. Such kind of activity also affects the national income of an

organization (Weirich and Reinstein, 2014). Moreover, growth and productivity aspects are

highly associated with the national income. Tax is the one of the main source which helps

government in generating the income. Thus, fraudulent activities impose high level of risk and

there affects the growth and development aspect of the corporation.

Methods for the detection of fraud: Several ways are available to an organization through which

they can easily detect the fraud. Business entity can prevent the fraud by observing the activities

and functions of the employees. In addition to this, by communicating the fraud risk policies to

their employees’ owner can also restricts the undesirable activities of their employees.

Organization needs to include the type of frauds along with their consequences in fraud risk

policy. When employees are aware from such policies then they are hesitate to make fraud within

the business organization.

Furthermore, by creating the positive working environment business unit can prevent

employee fraud and theft. Thus, management needs to introduce open door policy within an

organization. It provides opportunity to share their ideas, views and suggestion with the

management of the firm. It is also the most effective of fraud prevention (Philippon, 2014).

Besides this, auditing is the best tool which helps organization in detecting the errors which are

present in the financial statements of an organization. Through this, company is able to present

the fair picture of their financial health and performance in front of the stakeholders. All the

7

within the business enterprise. Usually, employees of an organization give false record to the

accountant in relation to the expenses which are incurred by them. In this situation, accountant

personnel fail to represent the fair view of the profitability aspects of an organization (Vogel,

2014). In addition to this, business enterprise prefers to represent the high income aspect in

comparison to their expenditure. This aspect is considered as a fraud which is undertaken by an

organization with the aim to attract large number of investors. Such fraudulent activities

negatively affect the brand value or image of an organization in front of the several stakeholders.

Along with it, firm also make modification in their financial statement to save the tax

amount which they require to pay the government on the basis of laws and legislation. It is the

main cause due to which organization show high level of expenditure as compared to the actual

expenses incurred by them. Such kind of activity also affects the national income of an

organization (Weirich and Reinstein, 2014). Moreover, growth and productivity aspects are

highly associated with the national income. Tax is the one of the main source which helps

government in generating the income. Thus, fraudulent activities impose high level of risk and

there affects the growth and development aspect of the corporation.

Methods for the detection of fraud: Several ways are available to an organization through which

they can easily detect the fraud. Business entity can prevent the fraud by observing the activities

and functions of the employees. In addition to this, by communicating the fraud risk policies to

their employees’ owner can also restricts the undesirable activities of their employees.

Organization needs to include the type of frauds along with their consequences in fraud risk

policy. When employees are aware from such policies then they are hesitate to make fraud within

the business organization.

Furthermore, by creating the positive working environment business unit can prevent

employee fraud and theft. Thus, management needs to introduce open door policy within an

organization. It provides opportunity to share their ideas, views and suggestion with the

management of the firm. It is also the most effective of fraud prevention (Philippon, 2014).

Besides this, auditing is the best tool which helps organization in detecting the errors which are

present in the financial statements of an organization. Through this, company is able to present

the fair picture of their financial health and performance in front of the stakeholders. All the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

above mentioned ways provides assistance in manager in detecting fraud in the more effectively

and efficiently.

TASK 3

3.1 Planning an audit with reference to scope, materiality and risk

In auditing, scope, materiality and risks are the main factors which have high level of

influence upon the business organization. Scope of auditing consists of the level to which

organization can involve the financial transaction records or documents to assess and detect the

fraudulent activities. Whereas materiality refers to the impact which mistake and omission will

place upon the incomes statement, balance sheet as well as cash flow statement of the company

(Qi and Hu, 2014). For instance: FA Jet Ltd. is facing the major risk of fraud in the area of

purchasing department. This department in the subject to high risk because accounting personnel

records additional extra expenses as compared to the actual expenses which are incurred by

them. Thus, FA Jet Ltd. needs to be undertaking all the documents or records which are highly

associated with the purchasing activities of the firm.

In this condition, auditor needs to undertake all the purchasing documents such as

purchase order, file and manual. Through this, company is able to assess the actual price at

which material is purchased by them (Trompeter and et.al, 2014). Besides this, it also provides

assistance to an organization about the actual purchasing order which is made during the

accounting year. Along with it, auditor also needed to make evaluation of previous purchasing

record, order, manual and voucher of the firm.

Through this, auditor is able to assess the purchasing pattern of an organization. This

aspect facilitates easy detection of fraud which takes place purchasing record of FA Jet ltd.

Besides this, there is several risk or problems which auditor might face during their auditing

program. For instance: Auditor faces difficulty in getting the purchasing record or invoices from

the organization for the orders which are placed by them during the accounting year. Due to this

aspect, auditor will face difficulty in verifying the purchasing operation and functions of the firm

on the basis of vouchers or bills. In addition to this, auditor also requires support from the

employees of an organization in relation to collection of the entire document which are needed

for the auditing process. Thus, employee support also affects the success of auditing program.

8

and efficiently.

TASK 3

3.1 Planning an audit with reference to scope, materiality and risk

In auditing, scope, materiality and risks are the main factors which have high level of

influence upon the business organization. Scope of auditing consists of the level to which

organization can involve the financial transaction records or documents to assess and detect the

fraudulent activities. Whereas materiality refers to the impact which mistake and omission will

place upon the incomes statement, balance sheet as well as cash flow statement of the company

(Qi and Hu, 2014). For instance: FA Jet Ltd. is facing the major risk of fraud in the area of

purchasing department. This department in the subject to high risk because accounting personnel

records additional extra expenses as compared to the actual expenses which are incurred by

them. Thus, FA Jet Ltd. needs to be undertaking all the documents or records which are highly

associated with the purchasing activities of the firm.

In this condition, auditor needs to undertake all the purchasing documents such as

purchase order, file and manual. Through this, company is able to assess the actual price at

which material is purchased by them (Trompeter and et.al, 2014). Besides this, it also provides

assistance to an organization about the actual purchasing order which is made during the

accounting year. Along with it, auditor also needed to make evaluation of previous purchasing

record, order, manual and voucher of the firm.

Through this, auditor is able to assess the purchasing pattern of an organization. This

aspect facilitates easy detection of fraud which takes place purchasing record of FA Jet ltd.

Besides this, there is several risk or problems which auditor might face during their auditing

program. For instance: Auditor faces difficulty in getting the purchasing record or invoices from

the organization for the orders which are placed by them during the accounting year. Due to this

aspect, auditor will face difficulty in verifying the purchasing operation and functions of the firm

on the basis of vouchers or bills. In addition to this, auditor also requires support from the

employees of an organization in relation to collection of the entire document which are needed

for the auditing process. Thus, employee support also affects the success of auditing program.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.2 Identifying and use appropriate audit tests

Audit test refers to the substantive procedure which is undertaken by an auditor to collect

the efficient amount of evidence. With the help of audit test auditor can assure the organization

that financial statements are free from detection or material misstatement to the large extent. It

enables auditor to present the clear picture of financial performance of an organization with the

help of supporting evidence. There are various types of audit test are available to an auditor

which they can use in detecting the fraud (Sikka, 2015). It includes risk assessment procedure,

test of control, substantive test of transaction and analytical procedures (5 types of Audit test,

2016). Auditor of an FA Jet Ltd. undertakes substantive and analytical produce to detect the

errors which are present in the financial statements of an enterprise. In this test, auditor compares

actual records with their expectation. It enables auditor to identify each and every misstatements

and there by helps in detecting the omissions which are present in the financial statements of the

firm.

3.3 Analysis of the stages of the audit process

Auditing is termed as systematic process in which inspection and evaluation of the

different books of accounts of an organization is carried out by the independent or statutory body

with reference to certain auditing rules and regulation of auditing. In this context, stages of

auditing process are explained below which are considered by Auditors of FA Jet Ltd. while

handling auditing operations: Planning or requesting the documents: It is the first section of auditing process in which

auditor demands for all the documents and books of accounts in which audit is required.

It includes several documents related to purchasing records like purchase order, invoices,

vouchers, etc. In addition to that auditors are also carried out detail evaluation of previous

auditing report, bank statements along with ledgers accounts in order to assess in-depth

information of company's transactions (Ho and Mallick, 2015). This approach has found

very effective for organization in assessment of deviations that have been addressed in

different records and accounting transaction so as management of business entity will be

able to take appropriate measures in order to remove deviations. Preparation of an audit plan: It is second stage of auditing process in which auditor

develops an appropriate audit plan after collection of all kind of documents and reports. It

is also termed as an outline of whole auditing process. This outline provides significant

9

Audit test refers to the substantive procedure which is undertaken by an auditor to collect

the efficient amount of evidence. With the help of audit test auditor can assure the organization

that financial statements are free from detection or material misstatement to the large extent. It

enables auditor to present the clear picture of financial performance of an organization with the

help of supporting evidence. There are various types of audit test are available to an auditor

which they can use in detecting the fraud (Sikka, 2015). It includes risk assessment procedure,

test of control, substantive test of transaction and analytical procedures (5 types of Audit test,

2016). Auditor of an FA Jet Ltd. undertakes substantive and analytical produce to detect the

errors which are present in the financial statements of an enterprise. In this test, auditor compares

actual records with their expectation. It enables auditor to identify each and every misstatements

and there by helps in detecting the omissions which are present in the financial statements of the

firm.

3.3 Analysis of the stages of the audit process

Auditing is termed as systematic process in which inspection and evaluation of the

different books of accounts of an organization is carried out by the independent or statutory body

with reference to certain auditing rules and regulation of auditing. In this context, stages of

auditing process are explained below which are considered by Auditors of FA Jet Ltd. while

handling auditing operations: Planning or requesting the documents: It is the first section of auditing process in which

auditor demands for all the documents and books of accounts in which audit is required.

It includes several documents related to purchasing records like purchase order, invoices,

vouchers, etc. In addition to that auditors are also carried out detail evaluation of previous

auditing report, bank statements along with ledgers accounts in order to assess in-depth

information of company's transactions (Ho and Mallick, 2015). This approach has found

very effective for organization in assessment of deviations that have been addressed in

different records and accounting transaction so as management of business entity will be

able to take appropriate measures in order to remove deviations. Preparation of an audit plan: It is second stage of auditing process in which auditor

develops an appropriate audit plan after collection of all kind of documents and reports. It

is also termed as an outline of whole auditing process. This outline provides significant

9

assistance to auditor in order to conduct the audit in an effective manner without any

issues. Auditor makes wide range of plans and policies associated with the purchasing

manual, purchase orders, purchasing file, list of suppliers or vendors and receiving

documents etc. In addition to that an appropriate audit plan provides significant support

to auditor for managing different activities and operations as per the predetermined

schedule. Scheduling of a meeting: It is third section of auditing process which is implemented after

the preparation of an appropriate audit plan with the size and nature of business. In this

section, auditor organizes an appropriate meeting with senior management of FA Jet Ltd.

In this meeting, auditor carries out detail discussion with the management and

administration staff who is involved in auditing process about the whole audit program

(Fedele, 2015). Apart from that they also discuss the time issue that could be face during

the auditing process. In addition to that detail evaluation of various other issues is also

carried out with reference to views and suggestions of managers. Conducting the fieldwork: According to this stage, auditor implements the audit plan with

reference to different suggestions and views of managers that have been gained in open

meeting. In this section, auditor carries out verification and evaluation of the all the kinds

of accounting transaction such as purchasing records and sales records which are

disclosed in the different books of accounts. This assessment has found very effective for

identification of different deficiencies that have been occurred in the different record due

to improper management of accounting transactions and business records. Drafting the report: It is most important stage of an auditing program in which auditor

provides valuable information to the management of an organization. Draft contains

information about the stock which is not recorded in the books of accounts. In addition to

this, auditor also communicates the deficiencies to the management which are present in

income and expenditure aspect of the firm (CAI and Feng, 2015). Along with it, auditor

also includes suggestion which they want to give the management in relation to the

detection or prevention of fraudulent activities.

Setting up the closing meeting: At the last stage, auditor arranges meeting with the senior

management of an organization. Through this, auditor is able to identify the views of

10

issues. Auditor makes wide range of plans and policies associated with the purchasing

manual, purchase orders, purchasing file, list of suppliers or vendors and receiving

documents etc. In addition to that an appropriate audit plan provides significant support

to auditor for managing different activities and operations as per the predetermined

schedule. Scheduling of a meeting: It is third section of auditing process which is implemented after

the preparation of an appropriate audit plan with the size and nature of business. In this

section, auditor organizes an appropriate meeting with senior management of FA Jet Ltd.

In this meeting, auditor carries out detail discussion with the management and

administration staff who is involved in auditing process about the whole audit program

(Fedele, 2015). Apart from that they also discuss the time issue that could be face during

the auditing process. In addition to that detail evaluation of various other issues is also

carried out with reference to views and suggestions of managers. Conducting the fieldwork: According to this stage, auditor implements the audit plan with

reference to different suggestions and views of managers that have been gained in open

meeting. In this section, auditor carries out verification and evaluation of the all the kinds

of accounting transaction such as purchasing records and sales records which are

disclosed in the different books of accounts. This assessment has found very effective for

identification of different deficiencies that have been occurred in the different record due

to improper management of accounting transactions and business records. Drafting the report: It is most important stage of an auditing program in which auditor

provides valuable information to the management of an organization. Draft contains

information about the stock which is not recorded in the books of accounts. In addition to

this, auditor also communicates the deficiencies to the management which are present in

income and expenditure aspect of the firm (CAI and Feng, 2015). Along with it, auditor

also includes suggestion which they want to give the management in relation to the

detection or prevention of fraudulent activities.

Setting up the closing meeting: At the last stage, auditor arranges meeting with the senior

management of an organization. Through this, auditor is able to identify the views of

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.