Financial Planning Report: SMSF, Taxation, and Investment

VerifiedAdded on 2020/02/24

|9

|1739

|31

Report

AI Summary

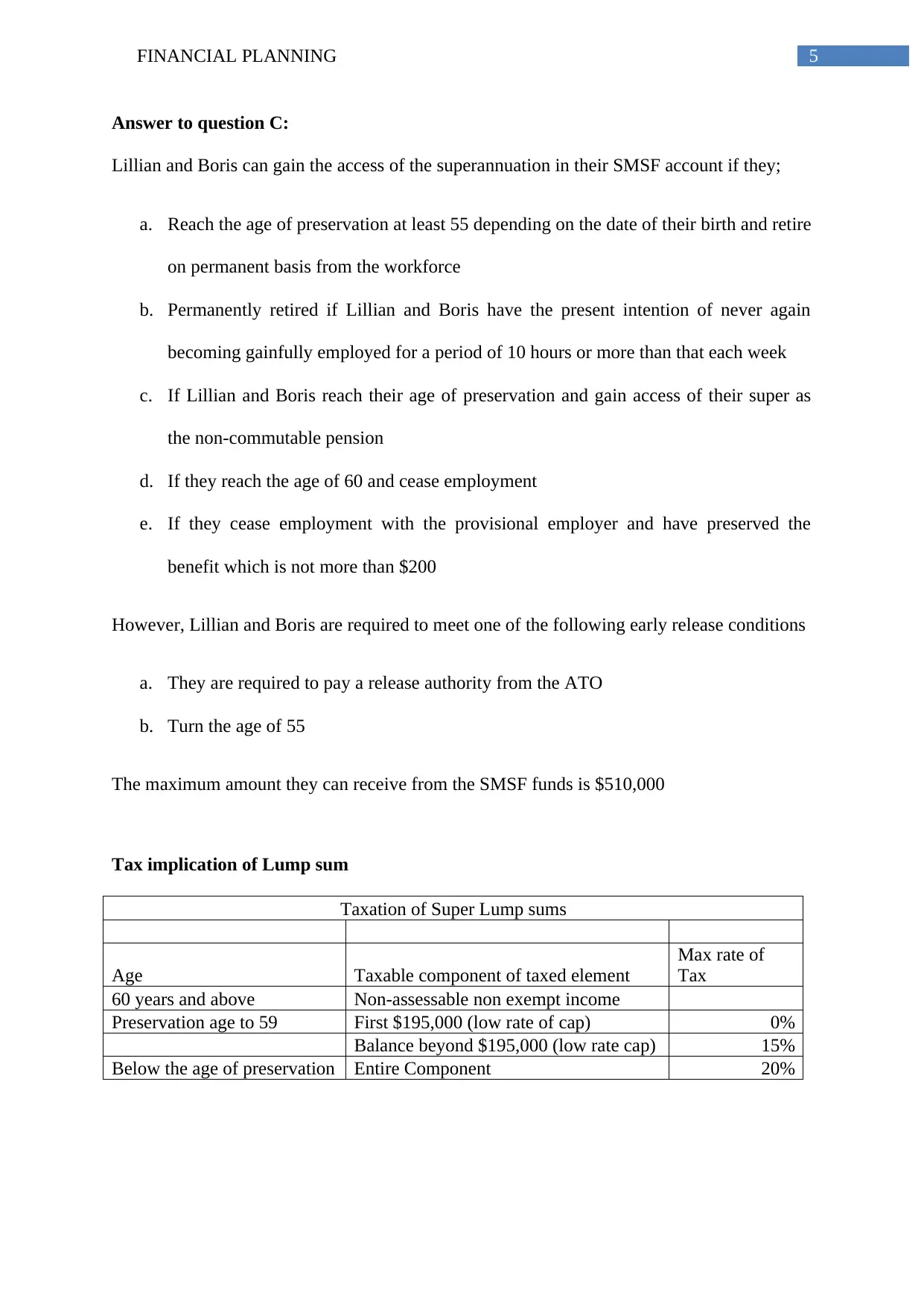

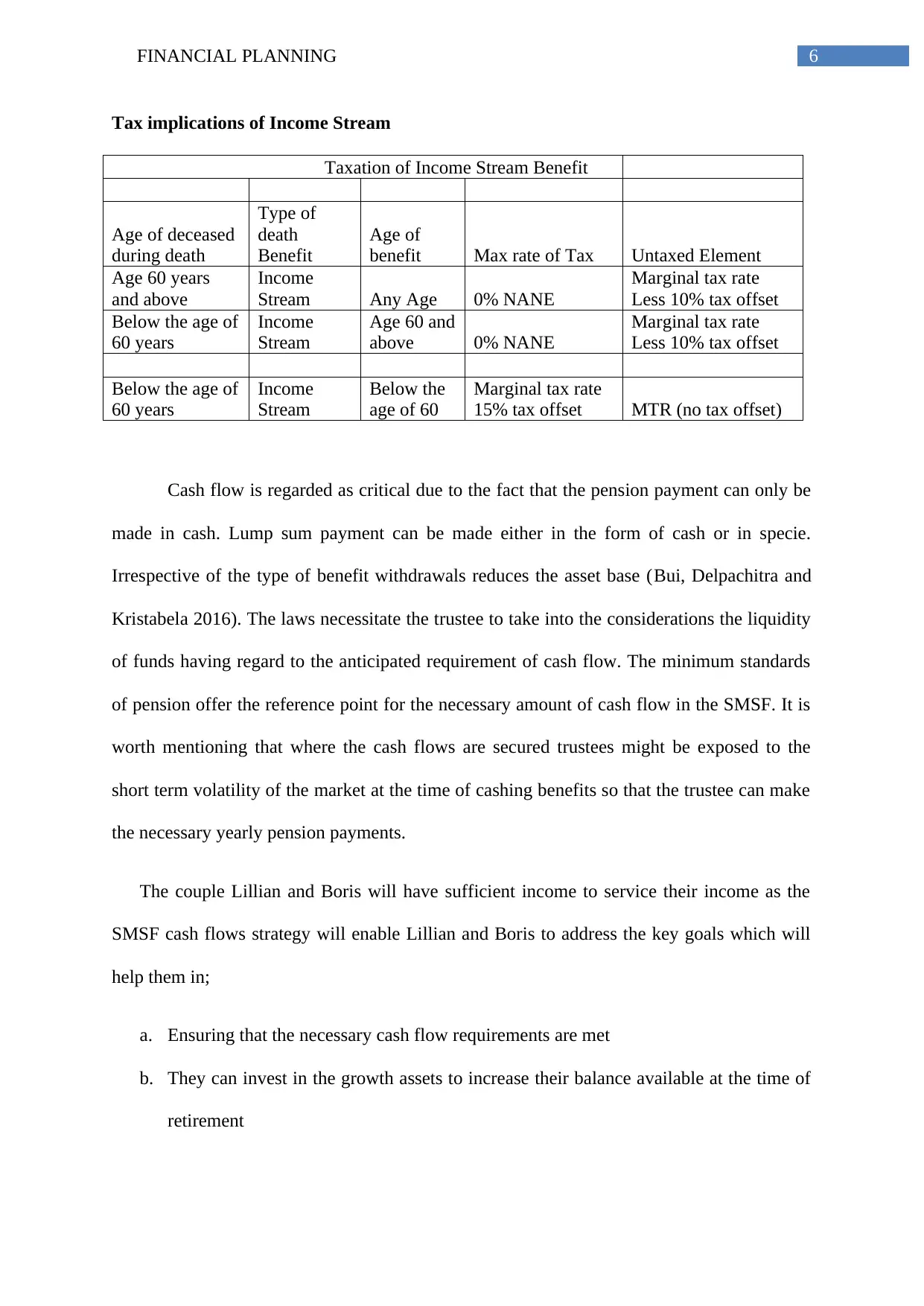

This report analyzes the financial planning strategies of Lillian and Boris, focusing on their self-managed superannuation fund (SMSF). It examines contribution splitting rules, including the maximum amount they can split. The report assesses the implications of investing in a rental property through their SMSF, considering costs, volatility, and tax offsets. It also outlines the conditions for accessing superannuation funds, along with the tax implications of lump sum payments and income streams. Furthermore, it discusses cash flow strategies and the importance of liquidity for SMSFs, ensuring the couple can meet their financial goals, maximize growth, and manage risks effectively. The report references several academic sources to support its findings and recommendations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.