FIN 400 Financial Theory & Analysis Test 2, University of Botswana

VerifiedAdded on 2023/01/05

|4

|954

|53

Quiz and Exam

AI Summary

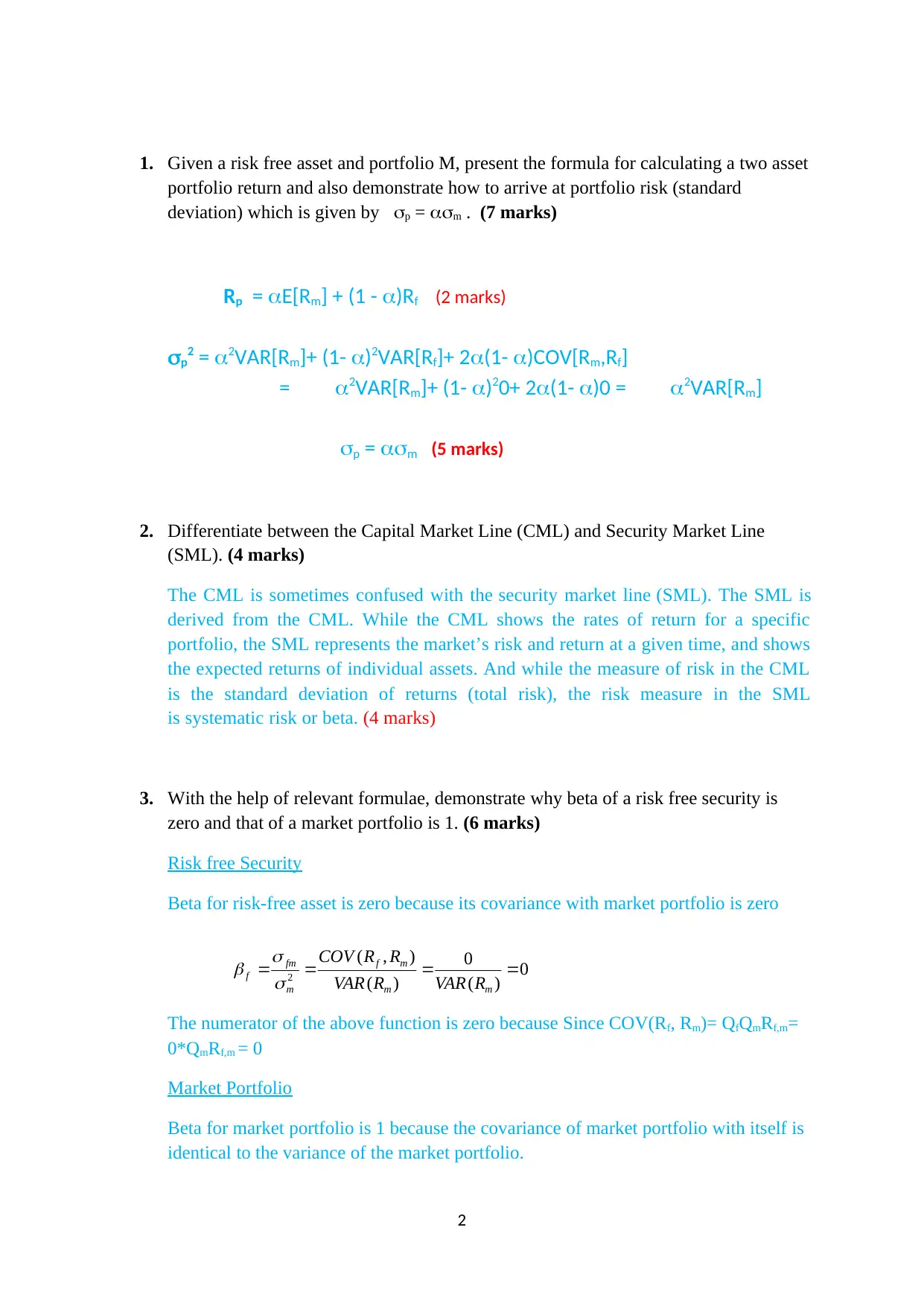

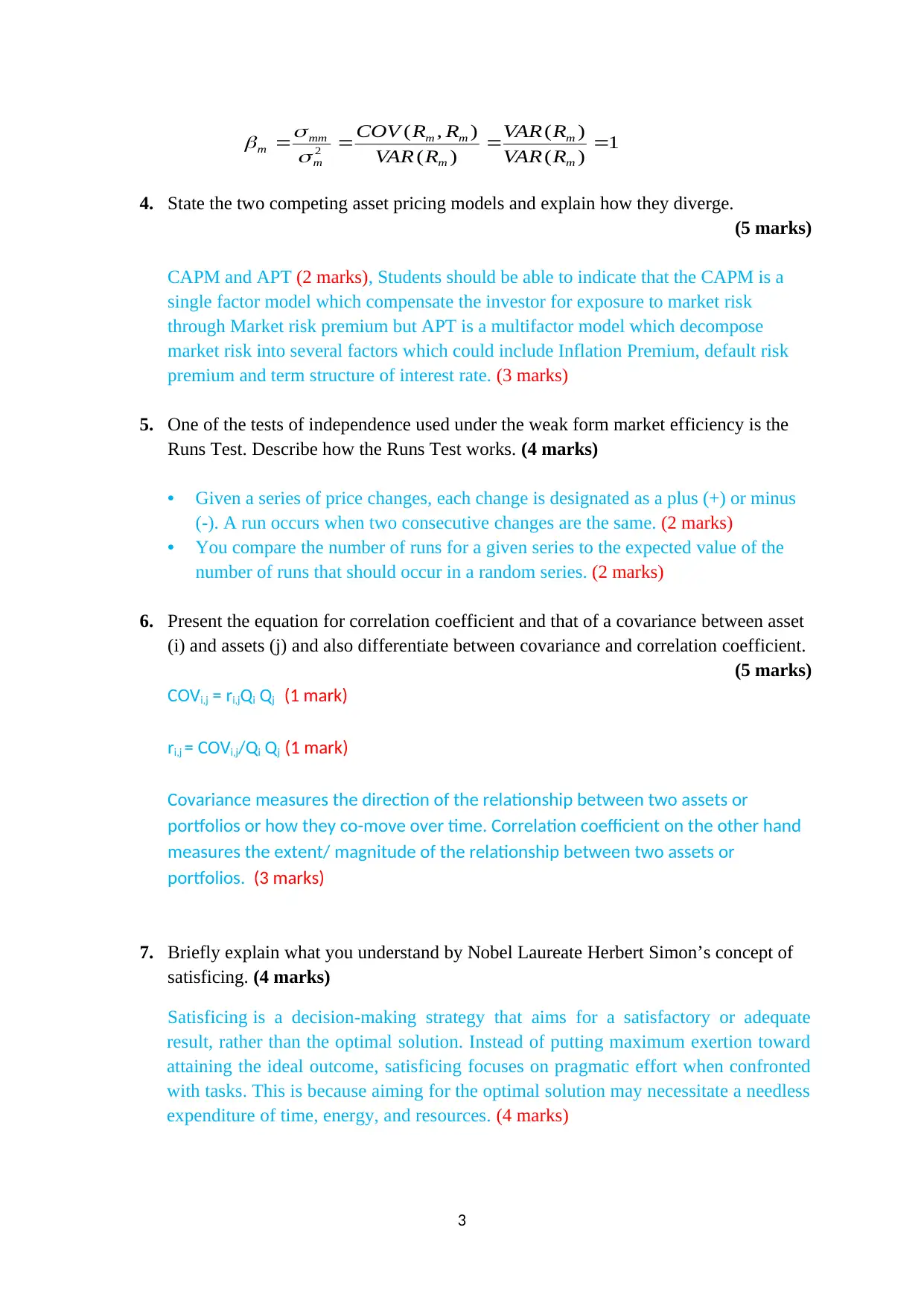

This document is a solution to the FIN 400 Financial Theory & Analysis Test 2 from the University of Botswana, conducted in November 2021. The exam covers key concepts in financial theory and analysis, including portfolio return and risk calculation, differentiation between Capital Market Line (CML) and Security Market Line (SML), and the demonstration of beta for risk-free assets and market portfolios. It explores asset pricing models like CAPM and APT, explains the Runs Test for market efficiency, and presents equations for correlation and covariance, along with their distinctions. The solution also touches on Herbert Simon's concept of satisficing and the components of total variance, including systematic and unsystematic risks. The solutions are presented with formulas, explanations, and point-form answers to provide a comprehensive understanding of the topics.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.