Econometrics Analysis of Financial Time Series Assignment

VerifiedAdded on 2022/09/28

|6

|1445

|25

Homework Assignment

AI Summary

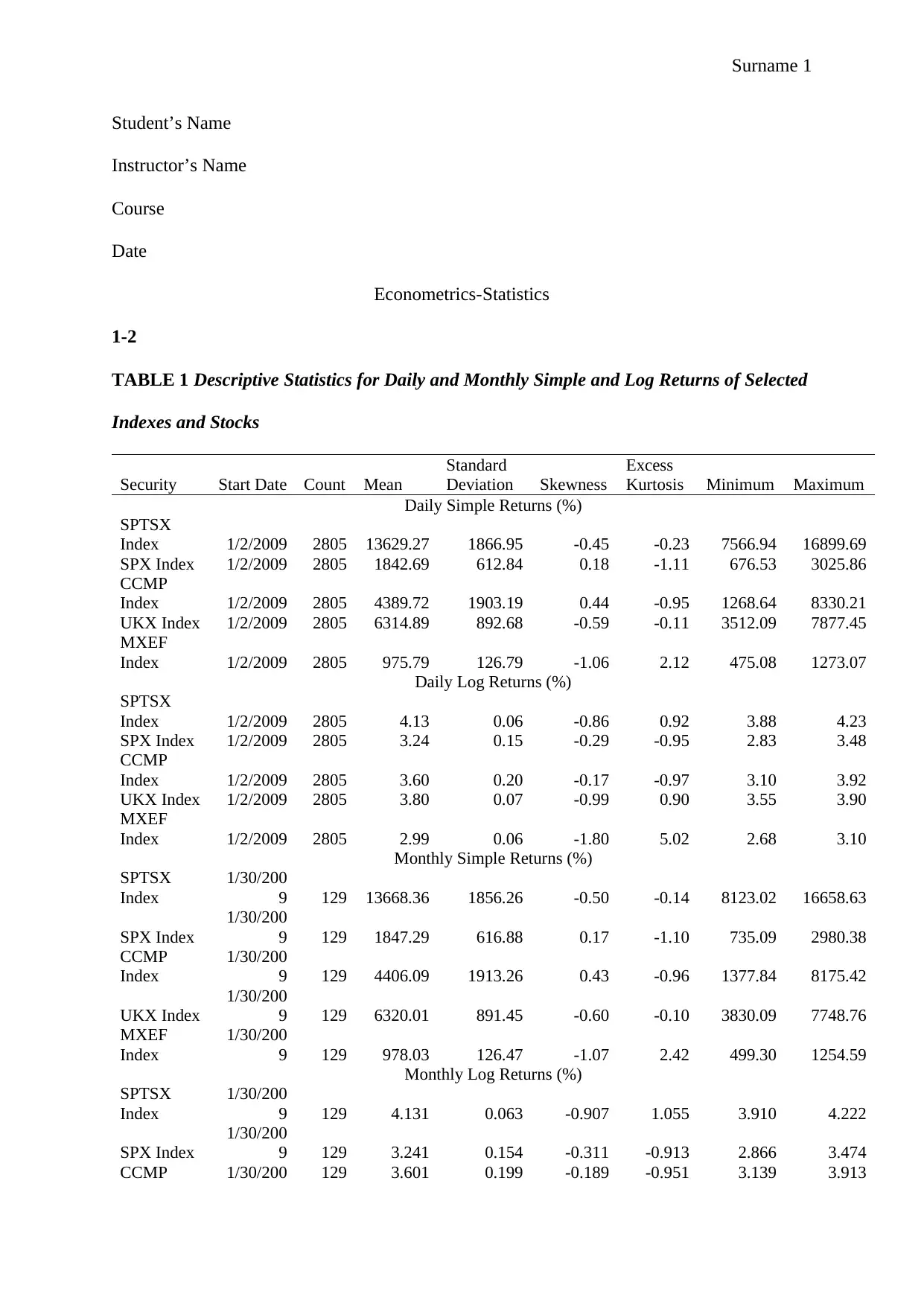

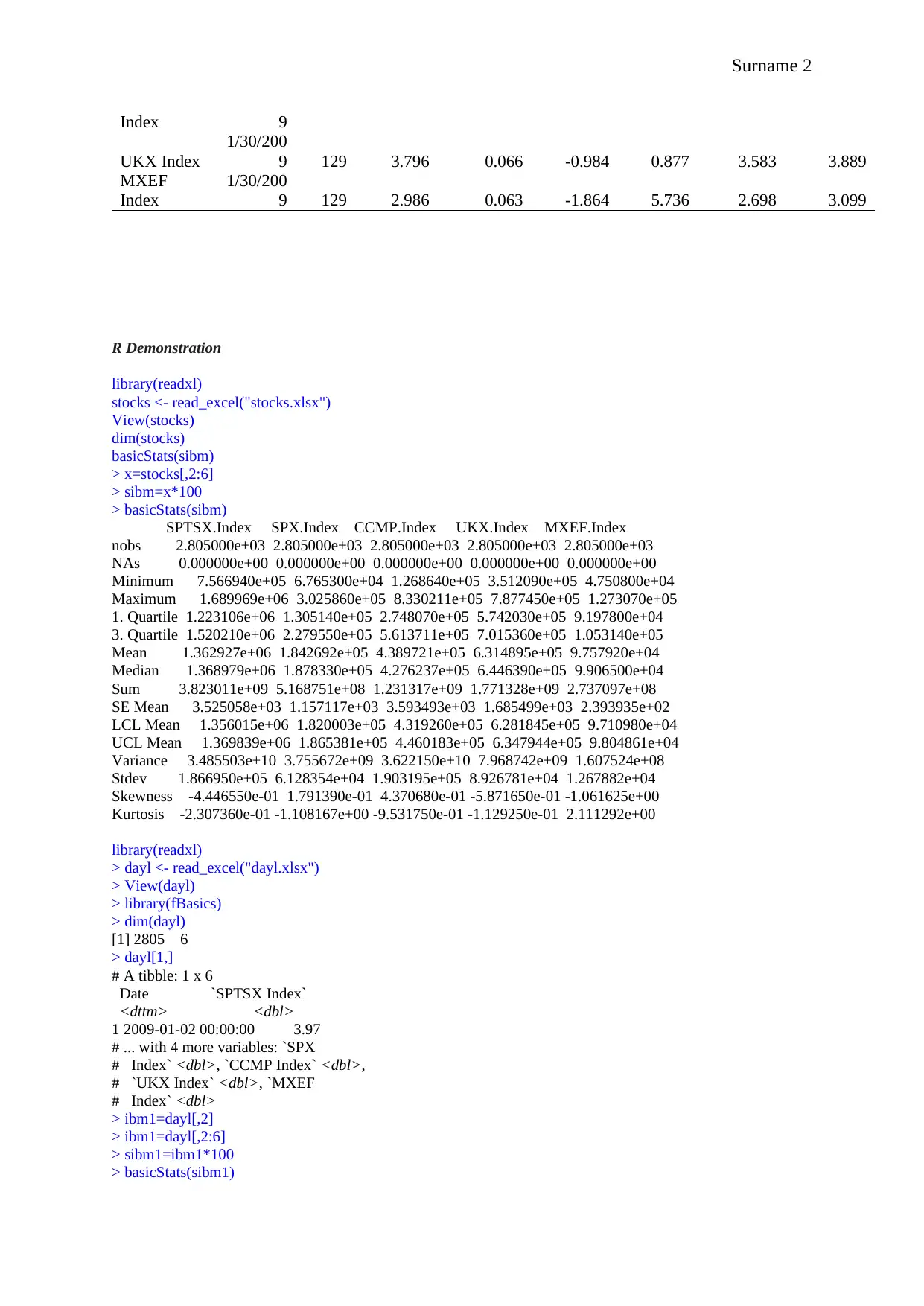

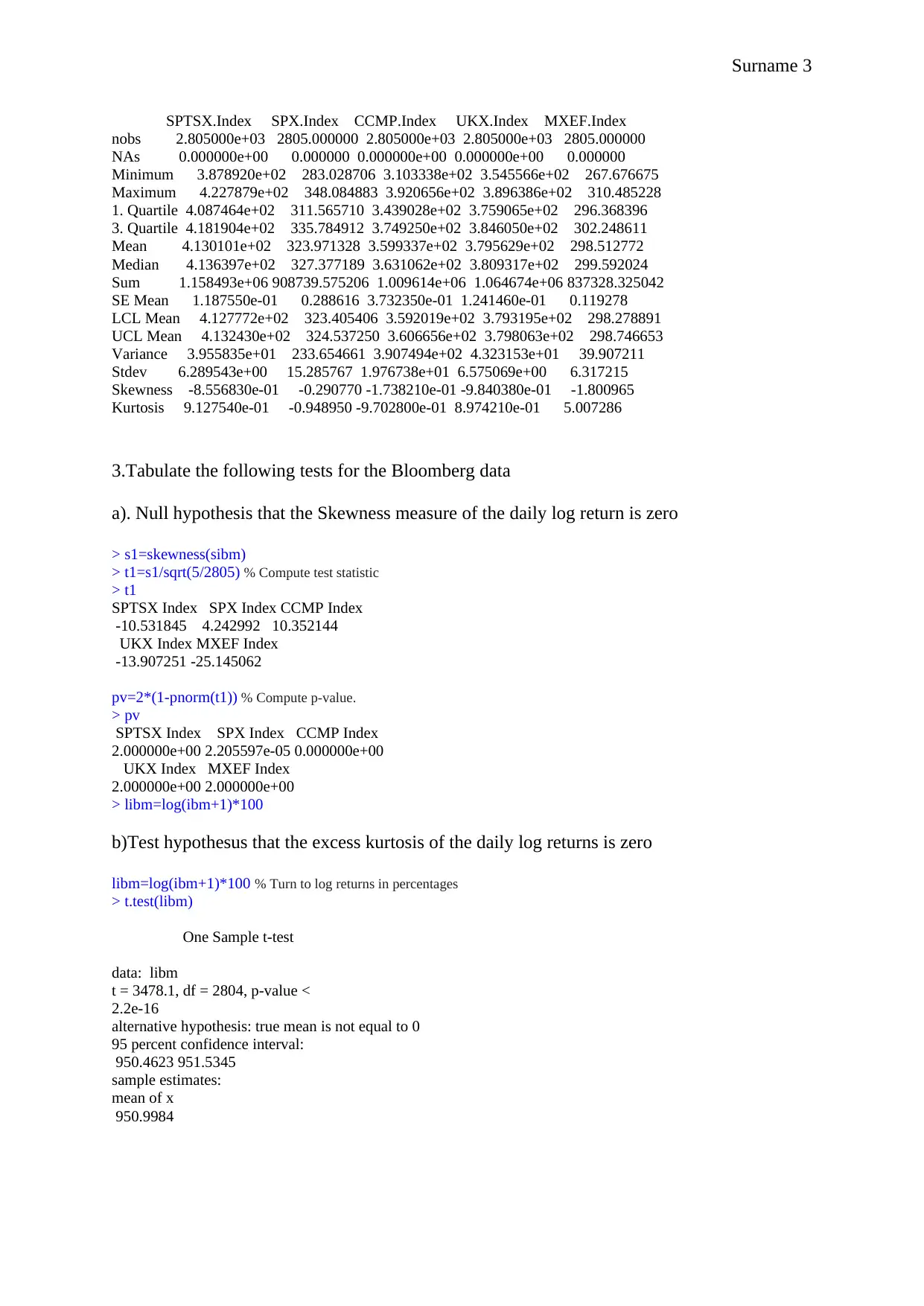

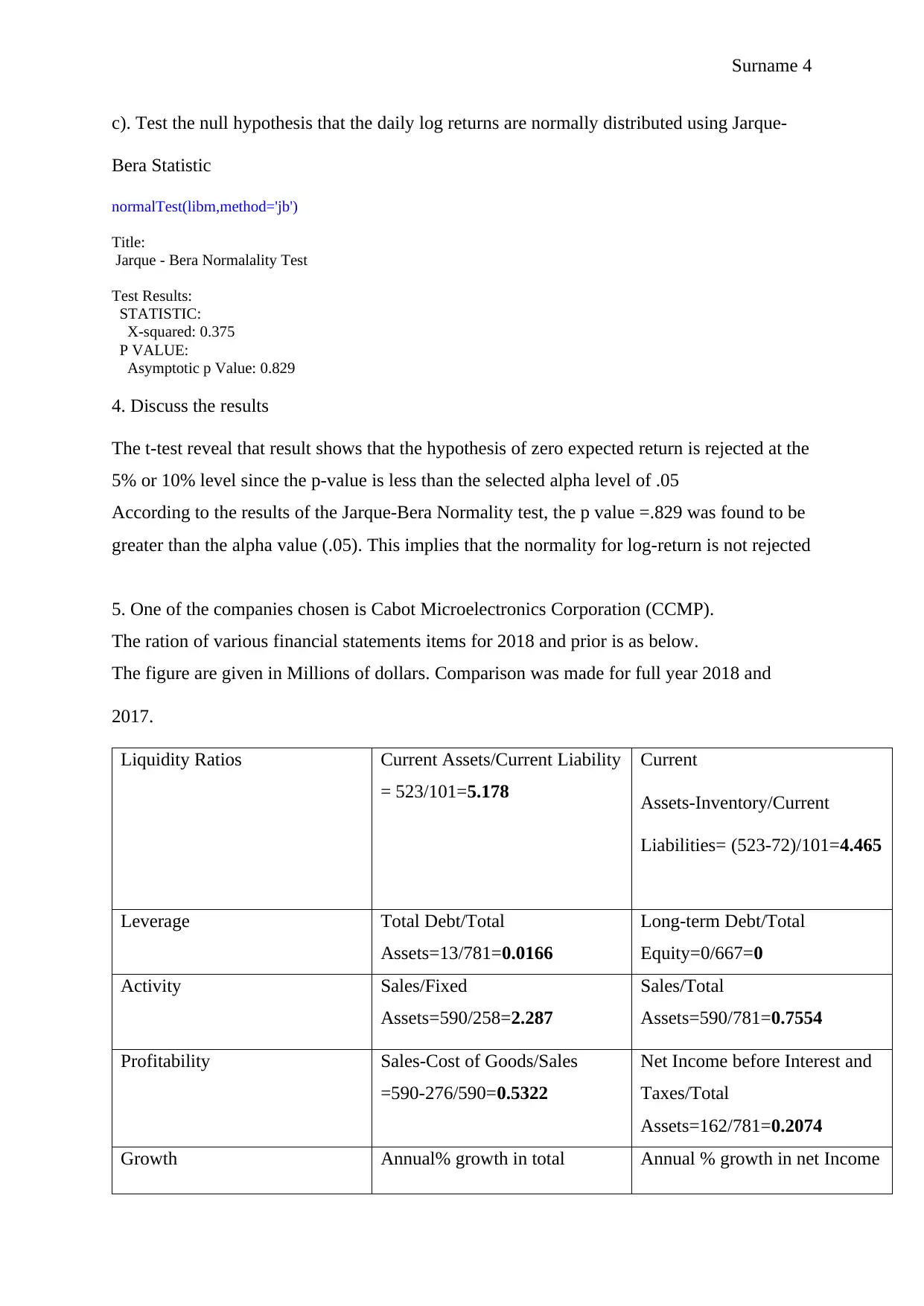

This assignment analyzes financial time series data using econometrics and R programming. It begins with descriptive statistics of daily and monthly simple and log returns for various indexes and stocks, including SPTSX, SPX, CCMP, UKX, and MXEF. The analysis involves calculating mean, standard deviation, skewness, and kurtosis. The assignment then uses R code to import data and calculate basic statistics using the 'fBasics' package. Further, the assignment involves performing hypothesis tests for skewness and excess kurtosis of daily log returns, including the computation of test statistics and p-values. The Jarque-Bera test is applied to assess the normality of the returns. The assignment includes a financial statement analysis of Cabot Microelectronics Corporation (CCMP), calculating liquidity, leverage, activity, profitability, and growth ratios for 2018 and 2017. Finally, it discusses concepts such as maximum likelihood estimation, the importance of delta in financial series, and whether the likelihood function can be considered a joint probability density function.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.