Financial Econometrics Report: Time Series Analysis and Forecasting

VerifiedAdded on 2020/10/05

|23

|4558

|137

Report

AI Summary

This report delves into financial econometrics, applying statistical methods to financial market data. It identifies and estimates time series models, evaluates sub-sample forecasts, and analyzes the characteristics of returns. The report examines the impact of oil price shocks on financial variables, including market volatility and equity returns, along with the influence of Economic Policy Uncertainty (EPU) on bond spreads and volatility. Furthermore, it tests hypotheses concerning private consumption expenditure, its relationship with financial wealth and labor income, and its predictive power for future consumption and equity returns. The analysis employs VAR models and Granger causality tests to establish relationships between variables and assess the effects of shocks. The report provides a comprehensive analysis of financial market dynamics.

FINANCIAL

ECONOMETRICS

ECONOMETRICS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Identifying and estimating time series model........................................................................1

(b) Using sub sample obtained in and out of sample forecasts and evaluating chosen models..4

QUESTION 3...................................................................................................................................7

(a) Calculating effect of shocks of oil prices on financial variables...........................................7

(b) Establishing that development in equity market impact volatility......................................12

(c) Impact of EPU on bond spread and volatility index............................................................13

QUESTION 4.................................................................................................................................16

(a) Testing the hypothesis that private consumption expenditure is related to financial wealth

and labour income.....................................................................................................................16

(b) Forecasting future private consumption expenditure.........................................................18

(c) Testing the hypothesis that ‘excess’ private consumption expenditure is a useful predictor

of excess equity returns.............................................................................................................20

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

(a) Identifying and estimating time series model........................................................................1

(b) Using sub sample obtained in and out of sample forecasts and evaluating chosen models..4

QUESTION 3...................................................................................................................................7

(a) Calculating effect of shocks of oil prices on financial variables...........................................7

(b) Establishing that development in equity market impact volatility......................................12

(c) Impact of EPU on bond spread and volatility index............................................................13

QUESTION 4.................................................................................................................................16

(a) Testing the hypothesis that private consumption expenditure is related to financial wealth

and labour income.....................................................................................................................16

(b) Forecasting future private consumption expenditure.........................................................18

(c) Testing the hypothesis that ‘excess’ private consumption expenditure is a useful predictor

of excess equity returns.............................................................................................................20

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

INTRODUCTION

Financial econometrics is known as application of statistical method to data of financial

market. It is considered as branch of financial economics and helps in studying quantitative

problems arise through management. The present report would identify and estimate time series

model and sub sample obtained in and out of forecasts of sample. It will consider series of

returns and examined about normality with important characteristic of distributions of returns. In

the same series, it will estimate model of conditional variance and motivation with use along

with incorporation of specification both sign and relative size of shock with impact in condition

volatility (Li and et.al., 2019). Moreover, it will extract impact of shocks to prices of oil on

particular financial variables and development in equity markets which impact volatility.

Simultaneously, it will show impact of EPU on spread of bond and affected through volatility

index. This report will test hypothesis that private consumption expenditure is related to two of

sources and way to predict future private consumption expenditure. Lastly, hypothesis would be

testes about excess private consumption expenditure as useful predictor of excess returns of

equity.

QUESTION 1

(a) Identifying and estimating time series model

On basis of identifying and determining time series model, there is evaluation of the least

square model which is form of mathematical regression that extracts line of best fit for particular

set of data, giving visual demonstration of relationship among different data points. Every point

of data is replicated as representative of relationship within independent variable and unknown

dependent variable. It gives overall rationale for placement of the line of appropriate fit within

data points being elaborated (Nguyen, 2019). The very common application of method of the

least squares which is replicated as linear or ordinary with objective of creating a straight line

that reduces sum of squares of errors produced by outcomes of associated equations like

associated equations like squared residuals from variations in observed value and anticipated on

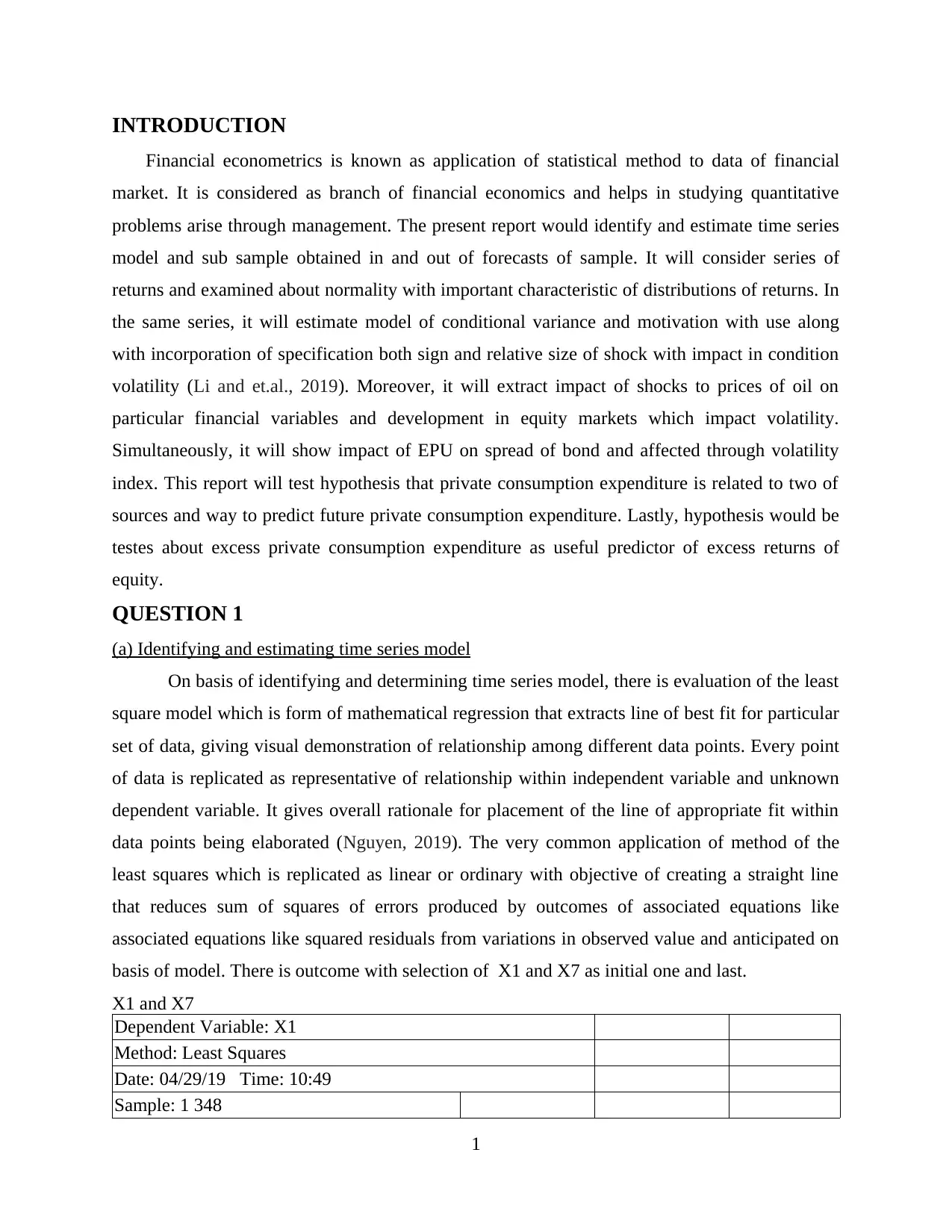

basis of model. There is outcome with selection of X1 and X7 as initial one and last.

X1 and X7

Dependent Variable: X1

Method: Least Squares

Date: 04/29/19 Time: 10:49

Sample: 1 348

1

Financial econometrics is known as application of statistical method to data of financial

market. It is considered as branch of financial economics and helps in studying quantitative

problems arise through management. The present report would identify and estimate time series

model and sub sample obtained in and out of forecasts of sample. It will consider series of

returns and examined about normality with important characteristic of distributions of returns. In

the same series, it will estimate model of conditional variance and motivation with use along

with incorporation of specification both sign and relative size of shock with impact in condition

volatility (Li and et.al., 2019). Moreover, it will extract impact of shocks to prices of oil on

particular financial variables and development in equity markets which impact volatility.

Simultaneously, it will show impact of EPU on spread of bond and affected through volatility

index. This report will test hypothesis that private consumption expenditure is related to two of

sources and way to predict future private consumption expenditure. Lastly, hypothesis would be

testes about excess private consumption expenditure as useful predictor of excess returns of

equity.

QUESTION 1

(a) Identifying and estimating time series model

On basis of identifying and determining time series model, there is evaluation of the least

square model which is form of mathematical regression that extracts line of best fit for particular

set of data, giving visual demonstration of relationship among different data points. Every point

of data is replicated as representative of relationship within independent variable and unknown

dependent variable. It gives overall rationale for placement of the line of appropriate fit within

data points being elaborated (Nguyen, 2019). The very common application of method of the

least squares which is replicated as linear or ordinary with objective of creating a straight line

that reduces sum of squares of errors produced by outcomes of associated equations like

associated equations like squared residuals from variations in observed value and anticipated on

basis of model. There is outcome with selection of X1 and X7 as initial one and last.

X1 and X7

Dependent Variable: X1

Method: Least Squares

Date: 04/29/19 Time: 10:49

Sample: 1 348

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Included observations: 348

Variable Coefficient Std. Error t-Statistic Prob.

C 0.300250 0.033813 8.879709 0.0000

X7 1.053131 0.033399 31.53165 0.0000

R-squared 0.741838 Mean dependent var 0.245242

Adjusted R-squared 0.741092 S.D. dependent var 1.238003

S.E. of regression 0.629933 Akaike info criterion 1.919324

Sum squared resid 137.2983 Schwarz criterion 1.941464

Log likelihood -331.9625 Hannan-Quinn criter. 1.928138

F-statistic 994.2452 Durbin-Watson stat 1.948666

Prob(F-statistic) 0.000000

2

Variable Coefficient Std. Error t-Statistic Prob.

C 0.300250 0.033813 8.879709 0.0000

X7 1.053131 0.033399 31.53165 0.0000

R-squared 0.741838 Mean dependent var 0.245242

Adjusted R-squared 0.741092 S.D. dependent var 1.238003

S.E. of regression 0.629933 Akaike info criterion 1.919324

Sum squared resid 137.2983 Schwarz criterion 1.941464

Log likelihood -331.9625 Hannan-Quinn criter. 1.928138

F-statistic 994.2452 Durbin-Watson stat 1.948666

Prob(F-statistic) 0.000000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3

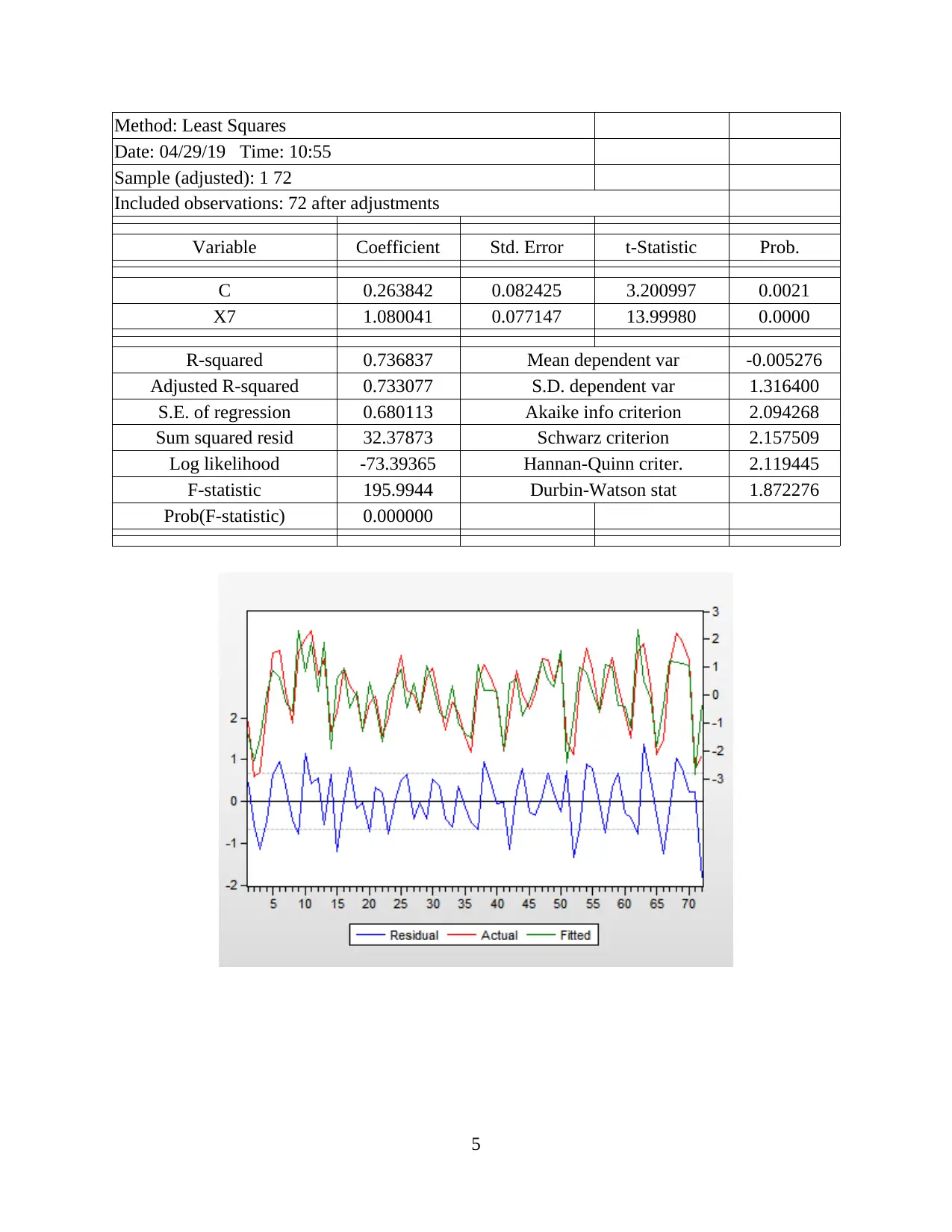

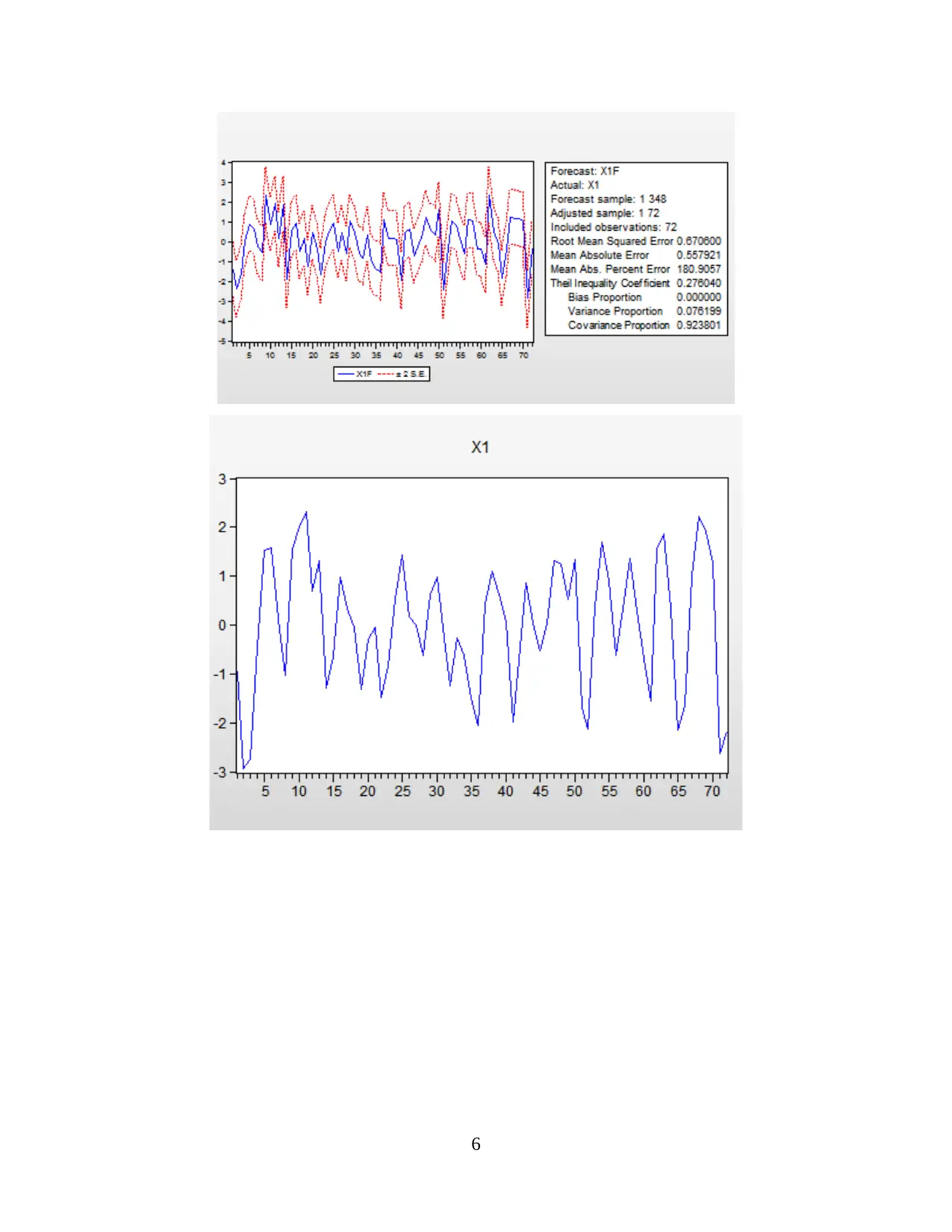

(b) Using sub sample obtained in and out of sample forecasts and evaluating chosen models

The sub sample obtained in and out of forecasts of sample with evaluation of the least

squares model with its advantages and disadvantages such as”

It has placed itself as initial tool for modeling of process due to completeness and

effectiveness. The types of data are described better with functions which are non linear in

parameters due to either processes are inherently linear or due to short ranges any process could

be approximated through linear model. Moreover, estimate of non parameters obtained through

linear least square are optimal estimate through broad class of estimates of possible parameter

with usual assumptions for process modeling. This undertakes efficient application of data and

good outcome could be obtained with very small data sets.

On the contrary, it could be assumed with long ranges with poor extrapolation properties

along with sensitivity to outliers (Luo and Chen, 2019). It is becoming difficult for extracting

particular linear model which fits data as range of data raises. The explanatory variables are very

extreme along with output of linear model. In simpler terms, linear models might be not very

effective to extrapolate the outcome of process for which data could not be gathered in region of

interest.

Dependent Variable: X1

4

The sub sample obtained in and out of forecasts of sample with evaluation of the least

squares model with its advantages and disadvantages such as”

It has placed itself as initial tool for modeling of process due to completeness and

effectiveness. The types of data are described better with functions which are non linear in

parameters due to either processes are inherently linear or due to short ranges any process could

be approximated through linear model. Moreover, estimate of non parameters obtained through

linear least square are optimal estimate through broad class of estimates of possible parameter

with usual assumptions for process modeling. This undertakes efficient application of data and

good outcome could be obtained with very small data sets.

On the contrary, it could be assumed with long ranges with poor extrapolation properties

along with sensitivity to outliers (Luo and Chen, 2019). It is becoming difficult for extracting

particular linear model which fits data as range of data raises. The explanatory variables are very

extreme along with output of linear model. In simpler terms, linear models might be not very

effective to extrapolate the outcome of process for which data could not be gathered in region of

interest.

Dependent Variable: X1

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Method: Least Squares

Date: 04/29/19 Time: 10:55

Sample (adjusted): 1 72

Included observations: 72 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C 0.263842 0.082425 3.200997 0.0021

X7 1.080041 0.077147 13.99980 0.0000

R-squared 0.736837 Mean dependent var -0.005276

Adjusted R-squared 0.733077 S.D. dependent var 1.316400

S.E. of regression 0.680113 Akaike info criterion 2.094268

Sum squared resid 32.37873 Schwarz criterion 2.157509

Log likelihood -73.39365 Hannan-Quinn criter. 2.119445

F-statistic 195.9944 Durbin-Watson stat 1.872276

Prob(F-statistic) 0.000000

5

Date: 04/29/19 Time: 10:55

Sample (adjusted): 1 72

Included observations: 72 after adjustments

Variable Coefficient Std. Error t-Statistic Prob.

C 0.263842 0.082425 3.200997 0.0021

X7 1.080041 0.077147 13.99980 0.0000

R-squared 0.736837 Mean dependent var -0.005276

Adjusted R-squared 0.733077 S.D. dependent var 1.316400

S.E. of regression 0.680113 Akaike info criterion 2.094268

Sum squared resid 32.37873 Schwarz criterion 2.157509

Log likelihood -73.39365 Hannan-Quinn criter. 2.119445

F-statistic 195.9944 Durbin-Watson stat 1.872276

Prob(F-statistic) 0.000000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

QUESTION 3

(a) Calculating effect of shocks of oil prices on financial variables

In the scenario, there is requirement of extracting impact of shocks to oil price on

particular financial variables comprises financial market volatility index and stock market returns

along with interest rate among government and corporate bonds along with Economic Policy

Uncertainty there is selection of VAR model to calculating it. VAR has numerous advantages as

compared to OLS model. The users must have to test that variable are exogenous and

endogenous because every variables are endogenous. Secondly, then VAR model as value of a

particular variable depends on more than associations of white noise terms as per own lags which

is very flexible compared to models to AR model (Goel and Mehra, 2019). Thus, comparison

with traditional models with accuracy of predict with VAR is very better. On basis of data and

variables, it could be written with statistical model with equation :

Spread=+Oil_r)

EPU = +Oil_r)

Vix = +Oil_r)

Nasdaq_r = +Oil_r)

The first step is required for testing that every variables as stationery or non stationery

with application Dickey-Fuller unit root test. It could be observed that prob* which is less than

5%. Moreover, P value could be reject that hypothesis and nasdaq_q is stationery.

7

(a) Calculating effect of shocks of oil prices on financial variables

In the scenario, there is requirement of extracting impact of shocks to oil price on

particular financial variables comprises financial market volatility index and stock market returns

along with interest rate among government and corporate bonds along with Economic Policy

Uncertainty there is selection of VAR model to calculating it. VAR has numerous advantages as

compared to OLS model. The users must have to test that variable are exogenous and

endogenous because every variables are endogenous. Secondly, then VAR model as value of a

particular variable depends on more than associations of white noise terms as per own lags which

is very flexible compared to models to AR model (Goel and Mehra, 2019). Thus, comparison

with traditional models with accuracy of predict with VAR is very better. On basis of data and

variables, it could be written with statistical model with equation :

Spread=+Oil_r)

EPU = +Oil_r)

Vix = +Oil_r)

Nasdaq_r = +Oil_r)

The first step is required for testing that every variables as stationery or non stationery

with application Dickey-Fuller unit root test. It could be observed that prob* which is less than

5%. Moreover, P value could be reject that hypothesis and nasdaq_q is stationery.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

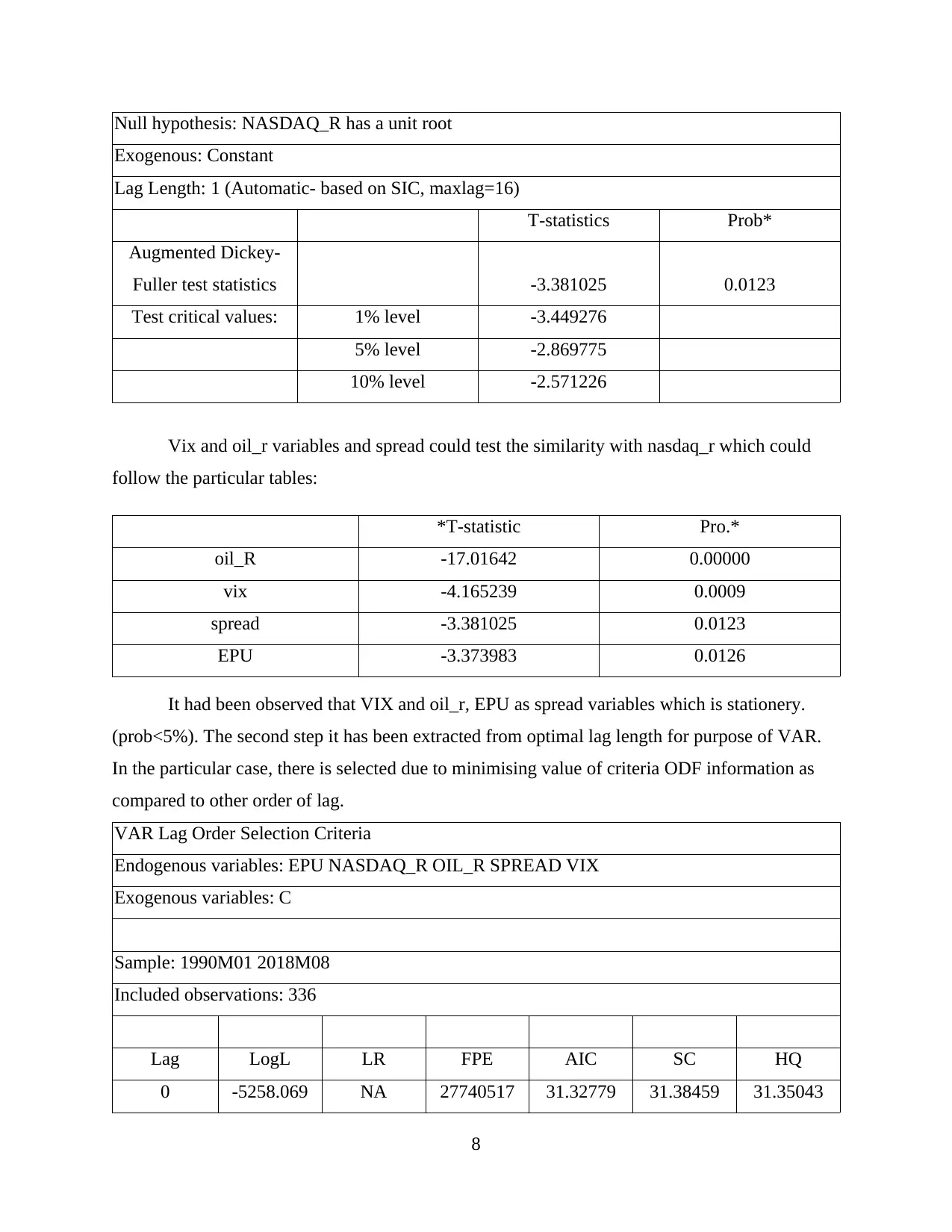

Null hypothesis: NASDAQ_R has a unit root

Exogenous: Constant

Lag Length: 1 (Automatic- based on SIC, maxlag=16)

T-statistics Prob*

Augmented Dickey-

Fuller test statistics -3.381025 0.0123

Test critical values: 1% level -3.449276

5% level -2.869775

10% level -2.571226

Vix and oil_r variables and spread could test the similarity with nasdaq_r which could

follow the particular tables:

*T-statistic Pro.*

oil_R -17.01642 0.00000

vix -4.165239 0.0009

spread -3.381025 0.0123

EPU -3.373983 0.0126

It had been observed that VIX and oil_r, EPU as spread variables which is stationery.

(prob<5%). The second step it has been extracted from optimal lag length for purpose of VAR.

In the particular case, there is selected due to minimising value of criteria ODF information as

compared to other order of lag.

VAR Lag Order Selection Criteria

Endogenous variables: EPU NASDAQ_R OIL_R SPREAD VIX

Exogenous variables: C

Sample: 1990M01 2018M08

Included observations: 336

Lag LogL LR FPE AIC SC HQ

0 -5258.069 NA 27740517 31.32779 31.38459 31.35043

8

Exogenous: Constant

Lag Length: 1 (Automatic- based on SIC, maxlag=16)

T-statistics Prob*

Augmented Dickey-

Fuller test statistics -3.381025 0.0123

Test critical values: 1% level -3.449276

5% level -2.869775

10% level -2.571226

Vix and oil_r variables and spread could test the similarity with nasdaq_r which could

follow the particular tables:

*T-statistic Pro.*

oil_R -17.01642 0.00000

vix -4.165239 0.0009

spread -3.381025 0.0123

EPU -3.373983 0.0126

It had been observed that VIX and oil_r, EPU as spread variables which is stationery.

(prob<5%). The second step it has been extracted from optimal lag length for purpose of VAR.

In the particular case, there is selected due to minimising value of criteria ODF information as

compared to other order of lag.

VAR Lag Order Selection Criteria

Endogenous variables: EPU NASDAQ_R OIL_R SPREAD VIX

Exogenous variables: C

Sample: 1990M01 2018M08

Included observations: 336

Lag LogL LR FPE AIC SC HQ

0 -5258.069 NA 27740517 31.32779 31.38459 31.35043

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

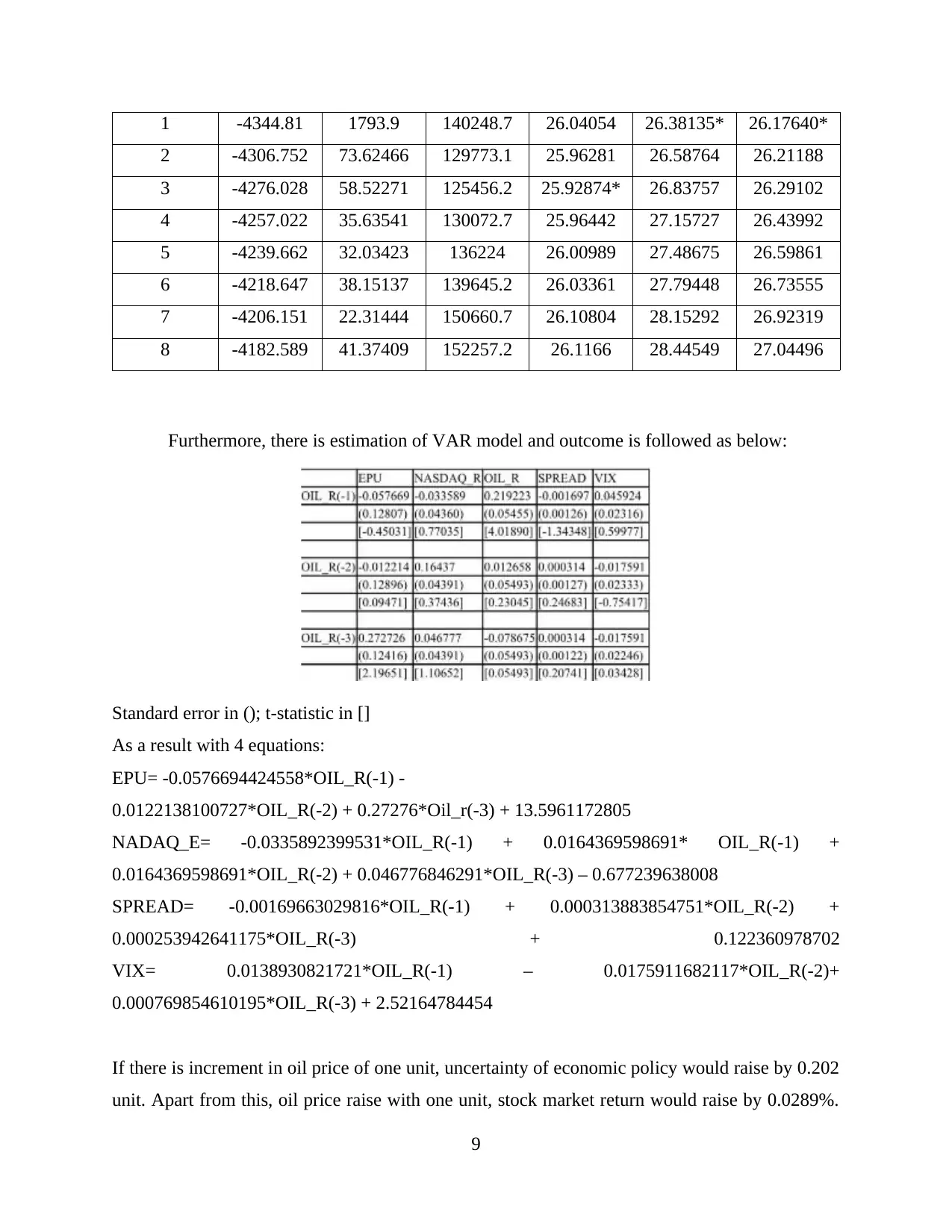

1 -4344.81 1793.9 140248.7 26.04054 26.38135* 26.17640*

2 -4306.752 73.62466 129773.1 25.96281 26.58764 26.21188

3 -4276.028 58.52271 125456.2 25.92874* 26.83757 26.29102

4 -4257.022 35.63541 130072.7 25.96442 27.15727 26.43992

5 -4239.662 32.03423 136224 26.00989 27.48675 26.59861

6 -4218.647 38.15137 139645.2 26.03361 27.79448 26.73555

7 -4206.151 22.31444 150660.7 26.10804 28.15292 26.92319

8 -4182.589 41.37409 152257.2 26.1166 28.44549 27.04496

Furthermore, there is estimation of VAR model and outcome is followed as below:

Standard error in (); t-statistic in []

As a result with 4 equations:

EPU= -0.0576694424558*OIL_R(-1) -

0.0122138100727*OIL_R(-2) + 0.27276*Oil_r(-3) + 13.5961172805

NADAQ_E= -0.0335892399531*OIL_R(-1) + 0.0164369598691* OIL_R(-1) +

0.0164369598691*OIL_R(-2) + 0.046776846291*OIL_R(-3) – 0.677239638008

SPREAD= -0.00169663029816*OIL_R(-1) + 0.000313883854751*OIL_R(-2) +

0.000253942641175*OIL_R(-3) + 0.122360978702

VIX= 0.0138930821721*OIL_R(-1) – 0.0175911682117*OIL_R(-2)+

0.000769854610195*OIL_R(-3) + 2.52164784454

If there is increment in oil price of one unit, uncertainty of economic policy would raise by 0.202

unit. Apart from this, oil price raise with one unit, stock market return would raise by 0.0289%.

9

2 -4306.752 73.62466 129773.1 25.96281 26.58764 26.21188

3 -4276.028 58.52271 125456.2 25.92874* 26.83757 26.29102

4 -4257.022 35.63541 130072.7 25.96442 27.15727 26.43992

5 -4239.662 32.03423 136224 26.00989 27.48675 26.59861

6 -4218.647 38.15137 139645.2 26.03361 27.79448 26.73555

7 -4206.151 22.31444 150660.7 26.10804 28.15292 26.92319

8 -4182.589 41.37409 152257.2 26.1166 28.44549 27.04496

Furthermore, there is estimation of VAR model and outcome is followed as below:

Standard error in (); t-statistic in []

As a result with 4 equations:

EPU= -0.0576694424558*OIL_R(-1) -

0.0122138100727*OIL_R(-2) + 0.27276*Oil_r(-3) + 13.5961172805

NADAQ_E= -0.0335892399531*OIL_R(-1) + 0.0164369598691* OIL_R(-1) +

0.0164369598691*OIL_R(-2) + 0.046776846291*OIL_R(-3) – 0.677239638008

SPREAD= -0.00169663029816*OIL_R(-1) + 0.000313883854751*OIL_R(-2) +

0.000253942641175*OIL_R(-3) + 0.122360978702

VIX= 0.0138930821721*OIL_R(-1) – 0.0175911682117*OIL_R(-2)+

0.000769854610195*OIL_R(-3) + 2.52164784454

If there is increment in oil price of one unit, uncertainty of economic policy would raise by 0.202

unit. Apart from this, oil price raise with one unit, stock market return would raise by 0.0289%.

9

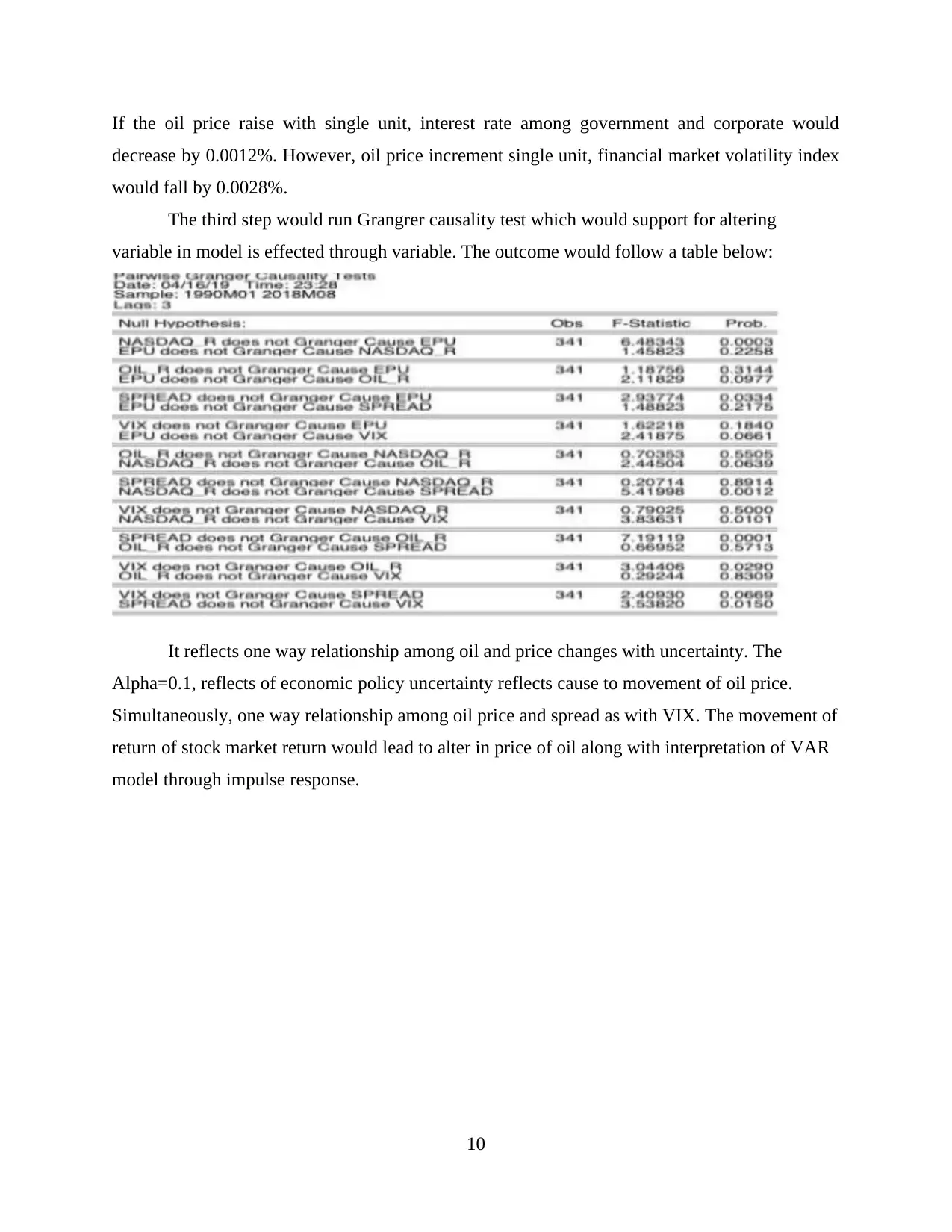

If the oil price raise with single unit, interest rate among government and corporate would

decrease by 0.0012%. However, oil price increment single unit, financial market volatility index

would fall by 0.0028%.

The third step would run Grangrer causality test which would support for altering

variable in model is effected through variable. The outcome would follow a table below:

It reflects one way relationship among oil and price changes with uncertainty. The

Alpha=0.1, reflects of economic policy uncertainty reflects cause to movement of oil price.

Simultaneously, one way relationship among oil price and spread as with VIX. The movement of

return of stock market return would lead to alter in price of oil along with interpretation of VAR

model through impulse response.

10

decrease by 0.0012%. However, oil price increment single unit, financial market volatility index

would fall by 0.0028%.

The third step would run Grangrer causality test which would support for altering

variable in model is effected through variable. The outcome would follow a table below:

It reflects one way relationship among oil and price changes with uncertainty. The

Alpha=0.1, reflects of economic policy uncertainty reflects cause to movement of oil price.

Simultaneously, one way relationship among oil price and spread as with VIX. The movement of

return of stock market return would lead to alter in price of oil along with interpretation of VAR

model through impulse response.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.