Financial Accounting Principles - Recording Transactions

VerifiedAdded on 2023/06/08

|13

|3410

|247

Homework Assignment

AI Summary

This assignment solution delves into fundamental financial accounting principles. It begins by defining bookkeeping and explaining how business transactions are maintained within the accounting system, emphasizing the double-entry system and the accounting equation. The solution then clarifies the roles of books of prime entry, journals, and ledgers. It proceeds to demonstrate the extraction of a trial balance using provided ledger balance data and prepares a bank reconciliation statement. Furthermore, the assignment defines the roles of suspense and control accounts, highlighting their differences. Finally, it constructs a control reconciliation statement for accounts receivables and payables, providing a comprehensive overview of key accounting concepts and practical applications.

Financial Accounting

Principles

Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Define book-keeping and how are the business transactions maintained in this system of

accounting...................................................................................................................................3

2. Define book-keeping, books of prime entry, journals and ledgers.........................................4

3. Extract the trial balance with the help of the data of ledger balances provided......................6

4. Prepare the Bank reconciliation statement with the help of data given. ................................7

5. Define the Role of suspense and control account. Also mention the difference between

them.............................................................................................................................................7

6. Prepare the control reconciliation statement for the accounts receivables and payables of the

business. .....................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Define book-keeping and how are the business transactions maintained in this system of

accounting...................................................................................................................................3

2. Define book-keeping, books of prime entry, journals and ledgers.........................................4

3. Extract the trial balance with the help of the data of ledger balances provided......................6

4. Prepare the Bank reconciliation statement with the help of data given. ................................7

5. Define the Role of suspense and control account. Also mention the difference between

them.............................................................................................................................................7

6. Prepare the control reconciliation statement for the accounts receivables and payables of the

business. .....................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

In this report it discuss about the concept of bookkeeping and the various of business

proceedings which are truly maintained in the accounting system of organization (Abdullah,

Stroulia and Nawaz, 2020). This is very significant to record the transactions in the debit and

credit side of the balance sheet because this statement show the company financial position and

ensure that total of both the assets and liability are similar if its not similar then its shows

irrelevancy in accounts. In another task it define the books of journals, ledgers and prime entry.

Afterwards it describe the meaning of trial balance and with the assistance of information it

provides the ledger balances and its important to create or put balance correctly in the trial

balance because the income statement of the firm also depends upon the accurate trial balance.

Also in another instance it prepare the bank reconciliation statement for the provided

information. Apart form this, it mainly explain the role and objective of suspense and control

account and show the comparison on them also. At last it create the control reconciliation

statement through the assistance of accounts receivable and payable.

MAIN BODY

1. Define book-keeping and how are the business transactions maintained in this system of

accounting.

Double entry book-keeping system is defined as a system which explains that there are

two parts to every transaction that occurs and affects two ledger accounts as a result. This

system deals in two or more than two accounts for each and every transaction or dealings that

takes place. The two effects are in the form of debit and credit (Cao, Jia and Manogaran, 2019).

Hence, there comes about two parts in the form of an equal and an opposite transaction affecting

two respective accounts. This system bases on the accounting equation Assets= Liability +

Equity. Hence any transaction that takes place, it has two respective effects. If it impacts the

asset side it needs to affect and change the amount of liability also so that the equation can be

balanced.

The respective principles that are required to be followed are:

Debit is recorded on the right and credit in the left.

Every debit constituent should have a comparable credit element.

Debit account gets the benefit and credit account provides the benefit.

In this report it discuss about the concept of bookkeeping and the various of business

proceedings which are truly maintained in the accounting system of organization (Abdullah,

Stroulia and Nawaz, 2020). This is very significant to record the transactions in the debit and

credit side of the balance sheet because this statement show the company financial position and

ensure that total of both the assets and liability are similar if its not similar then its shows

irrelevancy in accounts. In another task it define the books of journals, ledgers and prime entry.

Afterwards it describe the meaning of trial balance and with the assistance of information it

provides the ledger balances and its important to create or put balance correctly in the trial

balance because the income statement of the firm also depends upon the accurate trial balance.

Also in another instance it prepare the bank reconciliation statement for the provided

information. Apart form this, it mainly explain the role and objective of suspense and control

account and show the comparison on them also. At last it create the control reconciliation

statement through the assistance of accounts receivable and payable.

MAIN BODY

1. Define book-keeping and how are the business transactions maintained in this system of

accounting.

Double entry book-keeping system is defined as a system which explains that there are

two parts to every transaction that occurs and affects two ledger accounts as a result. This

system deals in two or more than two accounts for each and every transaction or dealings that

takes place. The two effects are in the form of debit and credit (Cao, Jia and Manogaran, 2019).

Hence, there comes about two parts in the form of an equal and an opposite transaction affecting

two respective accounts. This system bases on the accounting equation Assets= Liability +

Equity. Hence any transaction that takes place, it has two respective effects. If it impacts the

asset side it needs to affect and change the amount of liability also so that the equation can be

balanced.

The respective principles that are required to be followed are:

Debit is recorded on the right and credit in the left.

Every debit constituent should have a comparable credit element.

Debit account gets the benefit and credit account provides the benefit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The steps involving in double entry system of recording are:

1. Procurement of written documents: The first step in this system involves attainment of all

the documents that are proof of the business transactions that took place from the

accounting source document.

2. Recording in journal: The initial place where the transactions are recorded is in the books

of original entry as journal books of the company also referred as the day books

(Chandra and Siswanto, 2021). It gives an overview of the transaction and of the accounts

in ledger that are affected by the transaction.

3. Updating ledger accounts: The respective transactions are then written down in the

bookkeeping ledger accounts in a T structure. Each account represents a different ledger

and affects either of the two sides.

4. Debit or credit: The transactions are recorded in the ledger accounts through debit or

credit methods. With being recorded as a debit and then as a credit in the respective two

different ledger accounts. The bookkeeper should be well versed with the concepts to

make sure that the entries in the books are correct.

5. List in charts of accounts: All the different accounts in ledgers are all kept at a single

place named as chart of accounts with all the transactions in the ledger maintained,

recorded and created at a single place.

6. Support through mathematical formula: all the ledger accounts are then supported and

checked through the accounting equation formula to ensure the debits and credits

done in the entire book keeping are true and correct (Doron, Baker and Zucker, 2019).

This helps to then establish a trial balance.

7. Trial balance : If all the balances in ledger are matching and correct, the trial balance

shows up. With all the debits and credit sides match with the amount. If not, then

corrections need to be made so that a rectified trial balance could be generate.

8. Formulation of financial statements: After the completion of making of the trial balance,

then the financial statements are prepared such as income statement and balance sheet.

In the end, it also involves, making adjustment entries, rectifying if any mistakes and preparing a

modified trial balance and preparing for closing entries to ensure correct financial statements.

1. Procurement of written documents: The first step in this system involves attainment of all

the documents that are proof of the business transactions that took place from the

accounting source document.

2. Recording in journal: The initial place where the transactions are recorded is in the books

of original entry as journal books of the company also referred as the day books

(Chandra and Siswanto, 2021). It gives an overview of the transaction and of the accounts

in ledger that are affected by the transaction.

3. Updating ledger accounts: The respective transactions are then written down in the

bookkeeping ledger accounts in a T structure. Each account represents a different ledger

and affects either of the two sides.

4. Debit or credit: The transactions are recorded in the ledger accounts through debit or

credit methods. With being recorded as a debit and then as a credit in the respective two

different ledger accounts. The bookkeeper should be well versed with the concepts to

make sure that the entries in the books are correct.

5. List in charts of accounts: All the different accounts in ledgers are all kept at a single

place named as chart of accounts with all the transactions in the ledger maintained,

recorded and created at a single place.

6. Support through mathematical formula: all the ledger accounts are then supported and

checked through the accounting equation formula to ensure the debits and credits

done in the entire book keeping are true and correct (Doron, Baker and Zucker, 2019).

This helps to then establish a trial balance.

7. Trial balance : If all the balances in ledger are matching and correct, the trial balance

shows up. With all the debits and credit sides match with the amount. If not, then

corrections need to be made so that a rectified trial balance could be generate.

8. Formulation of financial statements: After the completion of making of the trial balance,

then the financial statements are prepared such as income statement and balance sheet.

In the end, it also involves, making adjustment entries, rectifying if any mistakes and preparing a

modified trial balance and preparing for closing entries to ensure correct financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Define book-keeping, books of prime entry, journals and ledgers. Double entry book-keeping: It states that each and business transaction which is recorded

in the books of accounts has two effects, equal and opposite. It affects two or more than

two accounts with each transaction that takes place. It is established on the basis of an

equation: Assets= Liabilities + Equity. The transactions are recorded in terms of debit

and credit. This establishes a system of accuracy in the preparation of financial

statements.

Books of prime entry: It refers to the original source of document where the transactions

are recorded that occur in a business organisation at the first place before being entered in

any separate journals or ledgers. These are of a great help to the accountants when they

required re-checking of any of the business transactions as ledgers might be of

complication when the requirement is just re checking all the transactions of the business

(Faber and Jonker, 2019). There are 6 books of prime entry refereed as:

1. Sales Journal

2. Purchase Journal

3. Purchase Return Journal

4. Sales Return Journal

5. Cash Journal

6. General Journal

Journal: A journal is also termed as a book of original entry or a day book. It has the

collections of all the business transactions recorded in a chronological manner. The

details and informations put in the journal while recording the transactions are termed as

journal entry. The documents on which the journal is base includes the business

vouchers, invoices and transaction receipts and cards.

Ledgers: A ledger is a collection of many different accounts that record the accounting

transactions. Each and every account in ledger has some opening carry forward balance

and it mentions each and every transaction taking it from journal and record it as either as

debit or credit (Feng, Conrad and Hussein, 2022). This is also termed as second book of

entry. It provides the individual balances of each and every account that the company has

in their books of accounts.

in the books of accounts has two effects, equal and opposite. It affects two or more than

two accounts with each transaction that takes place. It is established on the basis of an

equation: Assets= Liabilities + Equity. The transactions are recorded in terms of debit

and credit. This establishes a system of accuracy in the preparation of financial

statements.

Books of prime entry: It refers to the original source of document where the transactions

are recorded that occur in a business organisation at the first place before being entered in

any separate journals or ledgers. These are of a great help to the accountants when they

required re-checking of any of the business transactions as ledgers might be of

complication when the requirement is just re checking all the transactions of the business

(Faber and Jonker, 2019). There are 6 books of prime entry refereed as:

1. Sales Journal

2. Purchase Journal

3. Purchase Return Journal

4. Sales Return Journal

5. Cash Journal

6. General Journal

Journal: A journal is also termed as a book of original entry or a day book. It has the

collections of all the business transactions recorded in a chronological manner. The

details and informations put in the journal while recording the transactions are termed as

journal entry. The documents on which the journal is base includes the business

vouchers, invoices and transaction receipts and cards.

Ledgers: A ledger is a collection of many different accounts that record the accounting

transactions. Each and every account in ledger has some opening carry forward balance

and it mentions each and every transaction taking it from journal and record it as either as

debit or credit (Feng, Conrad and Hussein, 2022). This is also termed as second book of

entry. It provides the individual balances of each and every account that the company has

in their books of accounts.

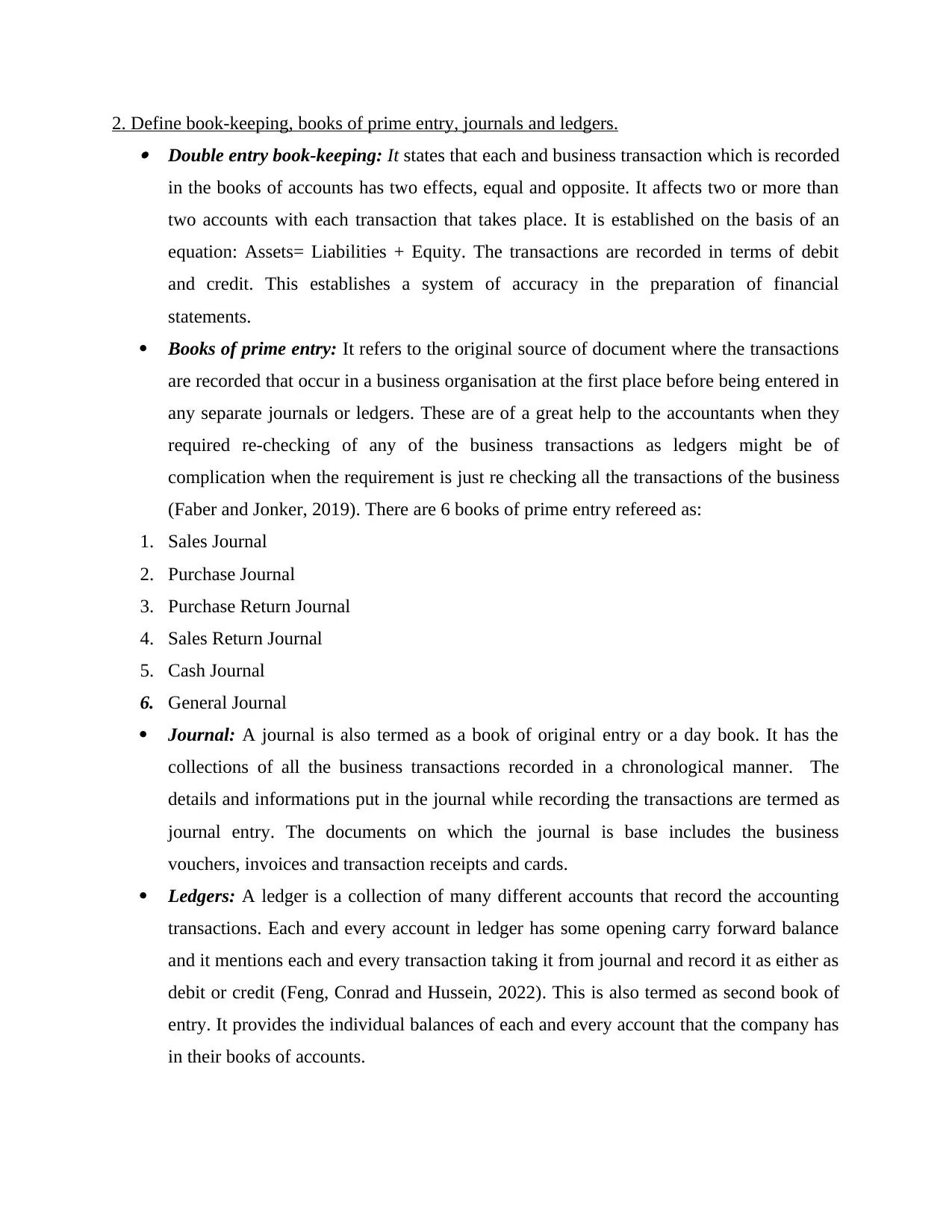

3. Extract the trial balance with the help of the data of ledger balances provided.

Trial Balance

This statement is the report of accounting that records the last balance in each and every generic

account of ledger (Frank, 2018). It basically means that it explain the total side of asset and

liability, sales revenue, equity, costa and the account of profit and loss.

Trial balance is mainly run as a portion of closing month procedure. This is significantly utilized

to confirm the complete total of all debits side similar to the total of all credits side. Which

means there are no unequal entries of journal in the system of accounting that would create it

unfeasible to make adequate financial documents.

Trial Balance

This statement is the report of accounting that records the last balance in each and every generic

account of ledger (Frank, 2018). It basically means that it explain the total side of asset and

liability, sales revenue, equity, costa and the account of profit and loss.

Trial balance is mainly run as a portion of closing month procedure. This is significantly utilized

to confirm the complete total of all debits side similar to the total of all credits side. Which

means there are no unequal entries of journal in the system of accounting that would create it

unfeasible to make adequate financial documents.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

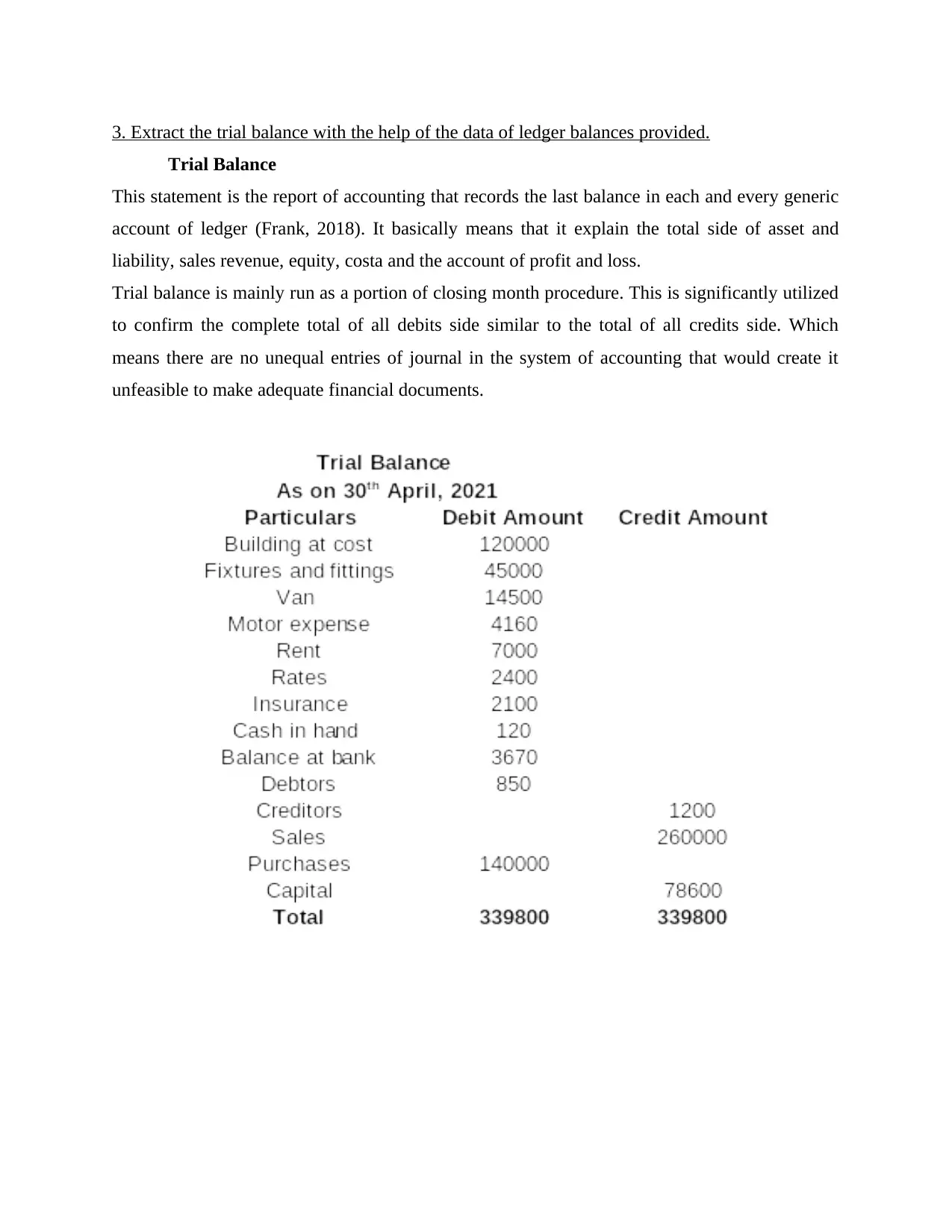

4. Prepare the Bank reconciliation statement with the help of data given.

Bank Reconciliation statement

It can be defined as a statement that relates the balance of cash through the balance sheet of

organization to the comparable value on its bank document. Accommodation of two accounts

mainly assist to determine that there is any requirement to show variations in accounting. This

statement of bank are done at daily intervals to confirm that the lists of firm's cash are adequate

or not. It also assist to identify any fraud and impact on cash (vanček, 2022). It also identify the

service of bank which includes fees, penalties and NSF checks. It will come and get tuned

through the balance of firm cash.

Bank reconciliation A/C

5. Define the Role of suspense and control account. Also mention the difference between them.

Control Account: It is also called adjustment account. In this A/C, general ledger keeps

clean all the details and it includes all the balances correct which is used in making financial

statements of an organisation (Laila and Puspitasari, 2021). It records the data and items in

several subsidiary ledgers and concise into the proportionate adjustment A/C.

For a small business establishment, all the accounts are together kept in a single ledger and the

balances for making trial balance can be extracted from that ledger account. But for a big

business enterprise, that deals in a massive number of transactions and dealings and where a

Bank Reconciliation statement

It can be defined as a statement that relates the balance of cash through the balance sheet of

organization to the comparable value on its bank document. Accommodation of two accounts

mainly assist to determine that there is any requirement to show variations in accounting. This

statement of bank are done at daily intervals to confirm that the lists of firm's cash are adequate

or not. It also assist to identify any fraud and impact on cash (vanček, 2022). It also identify the

service of bank which includes fees, penalties and NSF checks. It will come and get tuned

through the balance of firm cash.

Bank reconciliation A/C

5. Define the Role of suspense and control account. Also mention the difference between them.

Control Account: It is also called adjustment account. In this A/C, general ledger keeps

clean all the details and it includes all the balances correct which is used in making financial

statements of an organisation (Laila and Puspitasari, 2021). It records the data and items in

several subsidiary ledgers and concise into the proportionate adjustment A/C.

For a small business establishment, all the accounts are together kept in a single ledger and the

balances for making trial balance can be extracted from that ledger account. But for a big

business enterprise, that deals in a massive number of transactions and dealings and where a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

whole set of accounts are maintained. Few subsidiary ledger accounts are opened such as sales

ledger, purchase ledger which then become a part of double entry system. To make a trial

balance for such big organisations, it is necessary to extract the numbers from these subsidiary

ledgers. But to sometimes avoid such situations, business keep a control account maintained for

all the subsidiary ledgers for collecting the amount of balances.

There are two ways to keep control accounts under double-entry system.

In case the business maintains the accounts for sales ledger and purchase ledger as part of

the double entry system, the use of control accounts in that case only remains to provide

information regarding the balances and is not a part of double entry system (Patra and

Rath, 2022).

In case the organisation keeps the control accounts and treats them as a part of double-

entry system, then the subsidiary ledgers are not its part and are only to provide analysis

for the balances.

The purpose of keeping control accounts is to summarise and make records of large number of

massive transaction at one point of time and of the same kind. They assist in various transactions

reconciliation and in identification and findings of respective errors in the recordings.

Roles Of Control Account:

It aids in verifying the numerical rightness of items uploaded in the particular ledger

accounts.

It helps to prevent all kind of errors and frauds in the accounts because it maintains the

particular ledger account transactions. It assists to checking out the accuracy of the balance of the purchase and sales ledgers.

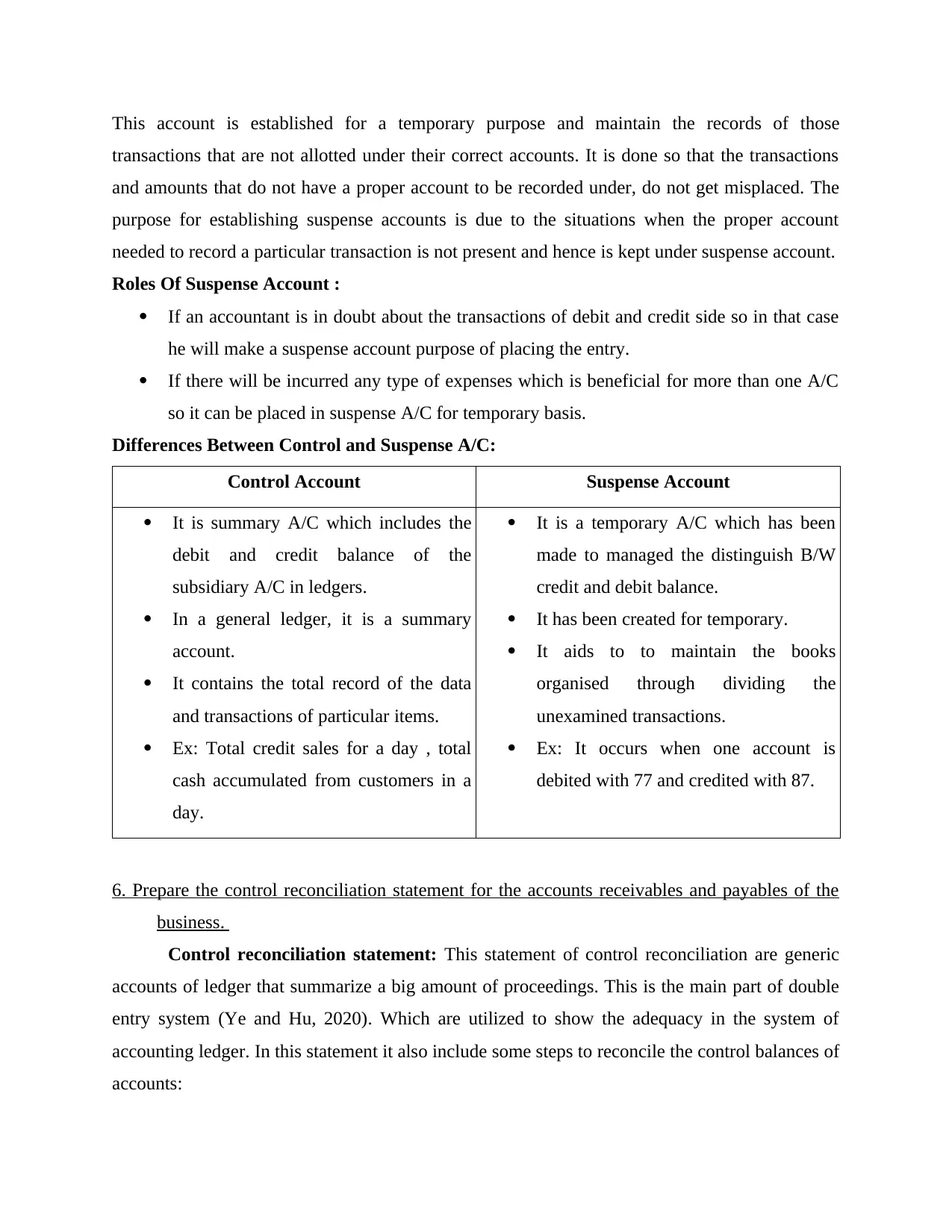

Suspense Account: It is a temporary account which collect and store the transactions and it has

been created for modify the variation between debit and credit side. It is made for short time

period. Suspense account is an account that is established for a temporary purpose and maintain

the records of those transactions that are not allotted under their correct accounts. It is done so

that the transactions and amounts that do not have a proper account to be recorded under, do not

get misplaced (Sharma, 2019). The purpose for establishing suspense accounts is due to the

situations when the proper account needed to record a particular transaction is not present and

hence is kept under suspense account.

ledger, purchase ledger which then become a part of double entry system. To make a trial

balance for such big organisations, it is necessary to extract the numbers from these subsidiary

ledgers. But to sometimes avoid such situations, business keep a control account maintained for

all the subsidiary ledgers for collecting the amount of balances.

There are two ways to keep control accounts under double-entry system.

In case the business maintains the accounts for sales ledger and purchase ledger as part of

the double entry system, the use of control accounts in that case only remains to provide

information regarding the balances and is not a part of double entry system (Patra and

Rath, 2022).

In case the organisation keeps the control accounts and treats them as a part of double-

entry system, then the subsidiary ledgers are not its part and are only to provide analysis

for the balances.

The purpose of keeping control accounts is to summarise and make records of large number of

massive transaction at one point of time and of the same kind. They assist in various transactions

reconciliation and in identification and findings of respective errors in the recordings.

Roles Of Control Account:

It aids in verifying the numerical rightness of items uploaded in the particular ledger

accounts.

It helps to prevent all kind of errors and frauds in the accounts because it maintains the

particular ledger account transactions. It assists to checking out the accuracy of the balance of the purchase and sales ledgers.

Suspense Account: It is a temporary account which collect and store the transactions and it has

been created for modify the variation between debit and credit side. It is made for short time

period. Suspense account is an account that is established for a temporary purpose and maintain

the records of those transactions that are not allotted under their correct accounts. It is done so

that the transactions and amounts that do not have a proper account to be recorded under, do not

get misplaced (Sharma, 2019). The purpose for establishing suspense accounts is due to the

situations when the proper account needed to record a particular transaction is not present and

hence is kept under suspense account.

This account is established for a temporary purpose and maintain the records of those

transactions that are not allotted under their correct accounts. It is done so that the transactions

and amounts that do not have a proper account to be recorded under, do not get misplaced. The

purpose for establishing suspense accounts is due to the situations when the proper account

needed to record a particular transaction is not present and hence is kept under suspense account.

Roles Of Suspense Account :

If an accountant is in doubt about the transactions of debit and credit side so in that case

he will make a suspense account purpose of placing the entry.

If there will be incurred any type of expenses which is beneficial for more than one A/C

so it can be placed in suspense A/C for temporary basis.

Differences Between Control and Suspense A/C:

Control Account Suspense Account

It is summary A/C which includes the

debit and credit balance of the

subsidiary A/C in ledgers.

In a general ledger, it is a summary

account.

It contains the total record of the data

and transactions of particular items.

Ex: Total credit sales for a day , total

cash accumulated from customers in a

day.

It is a temporary A/C which has been

made to managed the distinguish B/W

credit and debit balance.

It has been created for temporary.

It aids to to maintain the books

organised through dividing the

unexamined transactions.

Ex: It occurs when one account is

debited with 77 and credited with 87.

6. Prepare the control reconciliation statement for the accounts receivables and payables of the

business.

Control reconciliation statement: This statement of control reconciliation are generic

accounts of ledger that summarize a big amount of proceedings. This is the main part of double

entry system (Ye and Hu, 2020). Which are utilized to show the adequacy in the system of

accounting ledger. In this statement it also include some steps to reconcile the control balances of

accounts:

transactions that are not allotted under their correct accounts. It is done so that the transactions

and amounts that do not have a proper account to be recorded under, do not get misplaced. The

purpose for establishing suspense accounts is due to the situations when the proper account

needed to record a particular transaction is not present and hence is kept under suspense account.

Roles Of Suspense Account :

If an accountant is in doubt about the transactions of debit and credit side so in that case

he will make a suspense account purpose of placing the entry.

If there will be incurred any type of expenses which is beneficial for more than one A/C

so it can be placed in suspense A/C for temporary basis.

Differences Between Control and Suspense A/C:

Control Account Suspense Account

It is summary A/C which includes the

debit and credit balance of the

subsidiary A/C in ledgers.

In a general ledger, it is a summary

account.

It contains the total record of the data

and transactions of particular items.

Ex: Total credit sales for a day , total

cash accumulated from customers in a

day.

It is a temporary A/C which has been

made to managed the distinguish B/W

credit and debit balance.

It has been created for temporary.

It aids to to maintain the books

organised through dividing the

unexamined transactions.

Ex: It occurs when one account is

debited with 77 and credited with 87.

6. Prepare the control reconciliation statement for the accounts receivables and payables of the

business.

Control reconciliation statement: This statement of control reconciliation are generic

accounts of ledger that summarize a big amount of proceedings. This is the main part of double

entry system (Ye and Hu, 2020). Which are utilized to show the adequacy in the system of

accounting ledger. In this statement it also include some steps to reconcile the control balances of

accounts:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

They Fix the faults of control account in both the receivable or payable account of control

by listing the debits or credits.

They also fix the mistakes receivable or payable ledger in the register of ledger balances

such as receivable or payable by adding and subtracting.

Accounts receivable: This is the type of transaction or payment in which the firm will receive

for their customers who buy their products and services in a form of credit. Basically the period

of credit is having a small range start for some days and end with in a months or in other case it

stretch the time duration for a year. In simple words in this firm must have to exceed a line of

credit to their customers. In which firm can sell their products and services in both cash and

credit form. This trade receivable is also activated as current assets on the firm's balance sheet.

Accounts payable: The type of payable belongs to the account in which the generic ledger

shows a firm's duty to pay off the liability of short time duration to their creditors or providers.

One another important use of accounts payable in context for the department of business or

sections that is mainly answerable for creating the payments which are self-owed by the

organization to distributors and some other creditors.

by listing the debits or credits.

They also fix the mistakes receivable or payable ledger in the register of ledger balances

such as receivable or payable by adding and subtracting.

Accounts receivable: This is the type of transaction or payment in which the firm will receive

for their customers who buy their products and services in a form of credit. Basically the period

of credit is having a small range start for some days and end with in a months or in other case it

stretch the time duration for a year. In simple words in this firm must have to exceed a line of

credit to their customers. In which firm can sell their products and services in both cash and

credit form. This trade receivable is also activated as current assets on the firm's balance sheet.

Accounts payable: The type of payable belongs to the account in which the generic ledger

shows a firm's duty to pay off the liability of short time duration to their creditors or providers.

One another important use of accounts payable in context for the department of business or

sections that is mainly answerable for creating the payments which are self-owed by the

organization to distributors and some other creditors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

The above report concluded that double entry bookkeeping is important to maintain

because it shows the firm transactions in both the asset and credit side which is important to

record in an appropriate manner because it helps the company to understand the firm's financial

position in long run. If it discuss about the trial balance its necessary to prepare because without

the trial balance company can't create an income statement and not appropriately recognize the

profits in their business. Also in bank reconciliation statement its important to check the similar

transactions of cash. On that basis firm prepare the bank reconciliation statement and check the

incorrect transaction in bank statement.

The above report concluded that double entry bookkeeping is important to maintain

because it shows the firm transactions in both the asset and credit side which is important to

record in an appropriate manner because it helps the company to understand the firm's financial

position in long run. If it discuss about the trial balance its necessary to prepare because without

the trial balance company can't create an income statement and not appropriately recognize the

profits in their business. Also in bank reconciliation statement its important to check the similar

transactions of cash. On that basis firm prepare the bank reconciliation statement and check the

incorrect transaction in bank statement.

REFERENCES

Books and Journals

Abdullah, A., Stroulia, E. and Nawaz, F., 2020, August. Efficiency optimization in supply chain

using RFID technology. In 2020 IEEE Intl Conf on Dependable, Autonomic and Secure

Computing, Intl Conf on Pervasive Intelligence and Computing, Intl Conf on Cloud and

Big Data Computing, Intl Conf on Cyber Science and Technology Congress

(DASC/PiCom/CBDCom/CyberSciTech). (pp. 1-6). IEEE.

Cao, Y., Jia, F. and Manogaran, G., 2019. Efficient traceability systems of steel products using

blockchain-based industrial Internet of Things. IEEE Transactions on Industrial

Informatics. 16(9), pp.6004-6012.

Chandra, S.M. and Siswanto, S., 2021. PENINGKATAN KAPASITAS PENGURUS DALAM

PENGELOLAAN ADMINISTRASI PONDOK PESANTREN API SYUBBANUL

WATHON METESEH. Khidmatan. 1(1), pp.42-50.

Doron, M., Baker, C.R. and Zucker, K.D., 2019. Bookkeeper-controller-CFO: the rise of the

chief financial and chief accounting officer. Accounting Historians Journal. 46(2), pp.1-

8.

Faber, N. and Jonker, J., 2019. At your service: How can blockchain be used to address societal

challenges?. In Business transformation through blockchain (pp. 209-231). Palgrave

Macmillan, Cham.

Feng, X., Conrad, M. and Hussein, K., 2022. NHS Big Data Intelligence on Blockchain

Applications. In Big Data Intelligence for Smart Applications. (pp. 191-208). Springer,

Cham.

Frank, R.M., 2018. The Forgotten Tribe: Newscoverage Unlimited: How an International

Tragedy Spurred an Initiative to Help Newspeople Who Must Cover Grisly Stories.

In Sharing the Front Line and the Back Hills. (pp. 331-335). Routledge.

Hossain, M., 2021. Air. In Global Sustainability in Energy, Building, Infrastructure,

Transportation, and Water Technology. (pp. 381-394). Springer, Cham.

Ivanček, J., 2022. SPECIFIČNOSTI VOĐENJA POSLOVNIH KNJIGA OBRTNIKA U

SUSTAVU POREZA NA DOHODAK (Doctoral dissertation, University of Zagreb.

Faculty of Economics and Business. Department of Accounting).

Laila, A. and Puspitasari, D., 2021. PEMANFAATAN MEDIA SOSIAL SEBAGAI SARANA

MEMPERLUAS STRATEGI PEMASARAN PADA UMKM ABON KEPALA

SAPI. Khidmatan. 1(1), pp.51-61.

Patra, S. and Rath, J.P., 2022. A Study on Impact of Digital Accounting on the Small and

Medium Scale Business in Odisha.

Sharma, A., 2019. The Influence of Financial Literacy on the Performance of Small and

Medium-Scale Enterprises. IUP Journal of Accounting Research & Audit

Practices. 18(2).

Ye, Z. and Hu, J., 2020, February. Internal control of enterprise computer accounting

information system in the age of big data. In The International Conference on Cyber

Security Intelligence and Analytics (pp. 315-321). Springer, Cham.

Books and Journals

Abdullah, A., Stroulia, E. and Nawaz, F., 2020, August. Efficiency optimization in supply chain

using RFID technology. In 2020 IEEE Intl Conf on Dependable, Autonomic and Secure

Computing, Intl Conf on Pervasive Intelligence and Computing, Intl Conf on Cloud and

Big Data Computing, Intl Conf on Cyber Science and Technology Congress

(DASC/PiCom/CBDCom/CyberSciTech). (pp. 1-6). IEEE.

Cao, Y., Jia, F. and Manogaran, G., 2019. Efficient traceability systems of steel products using

blockchain-based industrial Internet of Things. IEEE Transactions on Industrial

Informatics. 16(9), pp.6004-6012.

Chandra, S.M. and Siswanto, S., 2021. PENINGKATAN KAPASITAS PENGURUS DALAM

PENGELOLAAN ADMINISTRASI PONDOK PESANTREN API SYUBBANUL

WATHON METESEH. Khidmatan. 1(1), pp.42-50.

Doron, M., Baker, C.R. and Zucker, K.D., 2019. Bookkeeper-controller-CFO: the rise of the

chief financial and chief accounting officer. Accounting Historians Journal. 46(2), pp.1-

8.

Faber, N. and Jonker, J., 2019. At your service: How can blockchain be used to address societal

challenges?. In Business transformation through blockchain (pp. 209-231). Palgrave

Macmillan, Cham.

Feng, X., Conrad, M. and Hussein, K., 2022. NHS Big Data Intelligence on Blockchain

Applications. In Big Data Intelligence for Smart Applications. (pp. 191-208). Springer,

Cham.

Frank, R.M., 2018. The Forgotten Tribe: Newscoverage Unlimited: How an International

Tragedy Spurred an Initiative to Help Newspeople Who Must Cover Grisly Stories.

In Sharing the Front Line and the Back Hills. (pp. 331-335). Routledge.

Hossain, M., 2021. Air. In Global Sustainability in Energy, Building, Infrastructure,

Transportation, and Water Technology. (pp. 381-394). Springer, Cham.

Ivanček, J., 2022. SPECIFIČNOSTI VOĐENJA POSLOVNIH KNJIGA OBRTNIKA U

SUSTAVU POREZA NA DOHODAK (Doctoral dissertation, University of Zagreb.

Faculty of Economics and Business. Department of Accounting).

Laila, A. and Puspitasari, D., 2021. PEMANFAATAN MEDIA SOSIAL SEBAGAI SARANA

MEMPERLUAS STRATEGI PEMASARAN PADA UMKM ABON KEPALA

SAPI. Khidmatan. 1(1), pp.51-61.

Patra, S. and Rath, J.P., 2022. A Study on Impact of Digital Accounting on the Small and

Medium Scale Business in Odisha.

Sharma, A., 2019. The Influence of Financial Literacy on the Performance of Small and

Medium-Scale Enterprises. IUP Journal of Accounting Research & Audit

Practices. 18(2).

Ye, Z. and Hu, J., 2020, February. Internal control of enterprise computer accounting

information system in the age of big data. In The International Conference on Cyber

Security Intelligence and Analytics (pp. 315-321). Springer, Cham.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.