Financial Accounting Report: An Phat Sole Trader - Financial Accounts

VerifiedAdded on 2021/06/07

|23

|5224

|103

Report

AI Summary

This comprehensive financial accounting report, prepared by a junior accountant for Bach Viet Accounting and Auditing Consultancy Corporation, meticulously examines the financial practices of An Phat Furniture. The report begins by defining accounting and its different branches, including management and financial accounting, and then delves into the foundational rules, conventions, and principles of accounting. It explains the benefits of accounting rules and provides a detailed overview of the golden rules of accounting, including personal, real, and nominal accounts. The report further explores the accounting conventions of disclosure, consistency, conservatism, and materiality. It then proceeds to analyze the source documents, general journal, ledgers, and trial balance of An Phat, providing examples and explanations of each. The report includes adjustments for prepaid expenses, accruals, and bad debts, and explains their impact on financial statements. Finally, the report presents the final accounts for An Phat, including the general journal, trial balance, balance sheet, and income statement, providing a complete overview of the company's financial position and performance.

Financial Accounting

A1: Record business transactions and prepare final accounts for An Phat Sole

Trader Lecture’s name: Nguyen Thi Tuong Tam

Student’s name: Huynh Quang Long

Student’s ID: B180049

Class: B1902.

Number of pages: 22 pages

1

A1: Record business transactions and prepare final accounts for An Phat Sole

Trader Lecture’s name: Nguyen Thi Tuong Tam

Student’s name: Huynh Quang Long

Student’s ID: B180049

Class: B1902.

Number of pages: 22 pages

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

1. What is accounting? 1. Managenment accounting:............................................................................3

2.The rules of accounting:.....................................................................................................................4

Benefits of Accounting Rules:...........................................................................................................4

Accounting Rules of Debit and Credit:..............................................................................................4

Golden Rules of Accounting (Traditional Approach):.......................................................................4

Personal Account:..........................................................................................................................4

Real Account:................................................................................................................................4

Nominal Account:..........................................................................................................................5

3. The conventions of accounting:.........................................................................................................5

1.Convention of Disclosure:...............................................................................................................5

2.Convention of Consistency:............................................................................................................5

3. Convention of Conservatism:.........................................................................................................6

4. Convention of Materiality:.............................................................................................................6

4.The principles of accounting:.............................................................................................................6

Source document, General Journal, Ledgers, and Trial balance:...........................................................7

1.General Journal:.............................................................................................................................8

2. Ledgers:.......................................................................................................................................10

4.Trial balance:................................................................................................................................14

Prepaid expenses, Accruals and Bad debts Adjustments:....................................................................15

Source document:...........................................................................................................................15

Explanation of influences of bad debts written off to the balance sheet and the Income

Statement:...................................................................................................................................16

Prepayments:......................................................................................................................................17

Source document:...........................................................................................................................17

Final Accounts for An Phat:.................................................................................................................18

Source document:...........................................................................................................................18

1.General Journal:...........................................................................................................................19

2. Trial balance:...............................................................................................................................20

4. Balance sheet and Income statement......................................................................................20

Bibliography.........................................................................................................................................22

2

1. What is accounting? 1. Managenment accounting:............................................................................3

2.The rules of accounting:.....................................................................................................................4

Benefits of Accounting Rules:...........................................................................................................4

Accounting Rules of Debit and Credit:..............................................................................................4

Golden Rules of Accounting (Traditional Approach):.......................................................................4

Personal Account:..........................................................................................................................4

Real Account:................................................................................................................................4

Nominal Account:..........................................................................................................................5

3. The conventions of accounting:.........................................................................................................5

1.Convention of Disclosure:...............................................................................................................5

2.Convention of Consistency:............................................................................................................5

3. Convention of Conservatism:.........................................................................................................6

4. Convention of Materiality:.............................................................................................................6

4.The principles of accounting:.............................................................................................................6

Source document, General Journal, Ledgers, and Trial balance:...........................................................7

1.General Journal:.............................................................................................................................8

2. Ledgers:.......................................................................................................................................10

4.Trial balance:................................................................................................................................14

Prepaid expenses, Accruals and Bad debts Adjustments:....................................................................15

Source document:...........................................................................................................................15

Explanation of influences of bad debts written off to the balance sheet and the Income

Statement:...................................................................................................................................16

Prepayments:......................................................................................................................................17

Source document:...........................................................................................................................17

Final Accounts for An Phat:.................................................................................................................18

Source document:...........................................................................................................................18

1.General Journal:...........................................................................................................................19

2. Trial balance:...............................................................................................................................20

4. Balance sheet and Income statement......................................................................................20

Bibliography.........................................................................................................................................22

2

LO1: Record business transactions using double entry book-keeping,

and be able to extract a trial balance

I am a Junior Accountant in Bach Viet Accounting and Auditing Consultancy Corporation. I have

been asked by my line manager to prepare a 1,000-word report on its client An Phat Furniture as

evidence that An Phat is aware of regulations relating to accountancy, as well as the rules, principles,

and conventions relating to accountancy.

1. What is accounting?

1. Managenment accounting:

Management accounting (MA) is used by the internal environment (inside organization) likes

managers, shareholders, employees, etc.

MA is used to providing the information about activities in last year that helps manager,

shareholder, employees, etc to making-decision plans for the future.

2. Financial accounting:

Financial accounting (FA) is used by the external environment (outside organization) likes

customers, future investors, government, etc.

FA is used by people who need information from it such as shareholders, banks,

government, suppliers, etc.

+ Shareholder: decide to invest or not invest.

+ Bank: decide to lend or not lend.

+ Government: tax information.

+ Supplier: an ability payment money back (have enough cash or not).

+ Customer: buy its products or not buy (it tells the number of people to buy or use its

product/ service).

3

and be able to extract a trial balance

I am a Junior Accountant in Bach Viet Accounting and Auditing Consultancy Corporation. I have

been asked by my line manager to prepare a 1,000-word report on its client An Phat Furniture as

evidence that An Phat is aware of regulations relating to accountancy, as well as the rules, principles,

and conventions relating to accountancy.

1. What is accounting?

1. Managenment accounting:

Management accounting (MA) is used by the internal environment (inside organization) likes

managers, shareholders, employees, etc.

MA is used to providing the information about activities in last year that helps manager,

shareholder, employees, etc to making-decision plans for the future.

2. Financial accounting:

Financial accounting (FA) is used by the external environment (outside organization) likes

customers, future investors, government, etc.

FA is used by people who need information from it such as shareholders, banks,

government, suppliers, etc.

+ Shareholder: decide to invest or not invest.

+ Bank: decide to lend or not lend.

+ Government: tax information.

+ Supplier: an ability payment money back (have enough cash or not).

+ Customer: buy its products or not buy (it tells the number of people to buy or use its

product/ service).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.The rules of accounting:

Benefits of Accounting Rules:

Accounting rules works as a base for any accounting framework. Before applying accounting

principles a person is required to know the basic accounting rules that in a transaction which account

should be debited and which account should be credited.

Accounting rules are used uniformly by all entities and thus using it results in consistent and

comparable financial reports. (taxmann, 2020)

Accounting Rules of Debit and Credit:

There are rules of debit and credit to record transactions, one is traditional approach and the

other is modern approach, both the approaches have been defined in detail below: (taxmann,

2020)

Golden Rules of Accounting (Traditional Approach):

Golden rules of accounting are the basic accounting rules on the basis of which accounting

entries are recorded.

Personal Account:

The rule related to Personal account states debit the receiver and credit the giver. In other words, if a

person receives something, receiver’s account shall be debited and if a person gives something,

giver’s account shall be credited.

For example, if Mr. X receives cash of Rs. 10,000 from Mr. Y then in the books of Mr. Y, Mr. X will

be receiver so account of Mr. X will be debited with an amount of Rs. 10,000.

(taxmann, 2020)

Real Account:

The rule related to real account states debit what comes in, credit what goes out. In other words, if

something comes into business, it shall be debited and if something goes out of business, it shall be

credited.

For example: An asset purchased for cash would be accounted as per rules of real account wherein

asset is what came into business, so asset account will be debited and cash is something that got out of

business, so cash account will be credited. (taxmann, 2020)

4

Benefits of Accounting Rules:

Accounting rules works as a base for any accounting framework. Before applying accounting

principles a person is required to know the basic accounting rules that in a transaction which account

should be debited and which account should be credited.

Accounting rules are used uniformly by all entities and thus using it results in consistent and

comparable financial reports. (taxmann, 2020)

Accounting Rules of Debit and Credit:

There are rules of debit and credit to record transactions, one is traditional approach and the

other is modern approach, both the approaches have been defined in detail below: (taxmann,

2020)

Golden Rules of Accounting (Traditional Approach):

Golden rules of accounting are the basic accounting rules on the basis of which accounting

entries are recorded.

Personal Account:

The rule related to Personal account states debit the receiver and credit the giver. In other words, if a

person receives something, receiver’s account shall be debited and if a person gives something,

giver’s account shall be credited.

For example, if Mr. X receives cash of Rs. 10,000 from Mr. Y then in the books of Mr. Y, Mr. X will

be receiver so account of Mr. X will be debited with an amount of Rs. 10,000.

(taxmann, 2020)

Real Account:

The rule related to real account states debit what comes in, credit what goes out. In other words, if

something comes into business, it shall be debited and if something goes out of business, it shall be

credited.

For example: An asset purchased for cash would be accounted as per rules of real account wherein

asset is what came into business, so asset account will be debited and cash is something that got out of

business, so cash account will be credited. (taxmann, 2020)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nominal Account:

The rule related to nominal account states that debit all expenses and losses, credit all

incomes and gains. In other words, if any expense or loss is incurred for the business,

expense or loss account shall be debited and if any income or gain is earned in business,

income account or gain/profit account shall be credited.

For example: If salaries are paid to employees then salary is an expense and hence salary

account shall be debited. Likewise any rent received shall be credited to rent account as it is

an income. (taxmann, 2020)

3. The conventions of accounting:

4 Conventions of Accounting Principles | Accounting Principles:

1.Convention of Disclosure:

The disclosure of all significant information is one of the important accounting conventions.

It implies that accounts should be prepared in such a way that all material information is

clearly disclosed to the reader.

This information should not only include figures given in the final accounts but also

information which occurs after the preparation of balance sheet but before the presentation of

financial statements. The idea behind this convention is that anybody who wants to study the

financial statements should not be prejudiced by concealing any facts He should be able to

make a free judgment. (Mishra, 2020)

2.Convention of Consistency:

The convention of consistency means that same accounting principles should be used for

preparing financial statements for different periods. It enables the management to draw

important conclusions regarding the working of the concern over a longer period. It allows a

comparison in the performance of different periods.

If different accounting procedures and processes are used for preparing financial statements

of different years then the result will not be comparable because these will be based on

different postulates.

If possible, net monetary effect of these changes should also be given. Consistencies may be of three

types:

5

The rule related to nominal account states that debit all expenses and losses, credit all

incomes and gains. In other words, if any expense or loss is incurred for the business,

expense or loss account shall be debited and if any income or gain is earned in business,

income account or gain/profit account shall be credited.

For example: If salaries are paid to employees then salary is an expense and hence salary

account shall be debited. Likewise any rent received shall be credited to rent account as it is

an income. (taxmann, 2020)

3. The conventions of accounting:

4 Conventions of Accounting Principles | Accounting Principles:

1.Convention of Disclosure:

The disclosure of all significant information is one of the important accounting conventions.

It implies that accounts should be prepared in such a way that all material information is

clearly disclosed to the reader.

This information should not only include figures given in the final accounts but also

information which occurs after the preparation of balance sheet but before the presentation of

financial statements. The idea behind this convention is that anybody who wants to study the

financial statements should not be prejudiced by concealing any facts He should be able to

make a free judgment. (Mishra, 2020)

2.Convention of Consistency:

The convention of consistency means that same accounting principles should be used for

preparing financial statements for different periods. It enables the management to draw

important conclusions regarding the working of the concern over a longer period. It allows a

comparison in the performance of different periods.

If different accounting procedures and processes are used for preparing financial statements

of different years then the result will not be comparable because these will be based on

different postulates.

If possible, net monetary effect of these changes should also be given. Consistencies may be of three

types:

5

(a) Vertical consistency

(b) Horizontal consistency

(c) Third dimensional consistency.

The vertical consistency is maintained within inter-related financial statements of the same

period. If a change has been made in dealing with two aspects of the same statement then it

will be vertical inconsistency. For example, if one method of depreciation is used while

preparing profit and loss account and another method is followed while preparing balance

sheet, it will be a case of vertical inconsistency. When figures of one financial year are

compared with the figures of another financial year of the same organisation it will be a case

of horizontal consistency. Third dimensional consistency will arise when financial statements

of two different organisations, in the same industry, are compared. (Mishra, 2020)

3. Convention of Conservatism:

The convention of conservatism means a cautious approach or policy of ‘play safe’. This

convention ensures that uncertainties and risks inherent in business transactions should be

given a proper consideration. If there is a possibility of loss, it should be taken into account at

the earliest. On the other hand, a prospect of profit should be ignored up to the time it does

not materialize. (Mishra, 2020)

4. Convention of Materiality:

According to this convention only those events should be recorded which have a significant

bearing and insignificant things should be ignored. The avoidance of insignificant things will

not materially affect the records of the business.

It should be seen that the efforts involved in recording the events should be worth the labour

involved in it. There is no formula in making a distinction between material and immaterial

events. It is a matter of judgment and it is left to the accountant to take a decision.

(Mishra, 2020)

4.The principles of accounting:

There are general rules and concepts that govern the field of accounting. These general rules–

referred to as basic accounting principles and guidelines–form the groundwork on which

more detailed, complicated, and legalistic accounting rules are based. For example,

6

(b) Horizontal consistency

(c) Third dimensional consistency.

The vertical consistency is maintained within inter-related financial statements of the same

period. If a change has been made in dealing with two aspects of the same statement then it

will be vertical inconsistency. For example, if one method of depreciation is used while

preparing profit and loss account and another method is followed while preparing balance

sheet, it will be a case of vertical inconsistency. When figures of one financial year are

compared with the figures of another financial year of the same organisation it will be a case

of horizontal consistency. Third dimensional consistency will arise when financial statements

of two different organisations, in the same industry, are compared. (Mishra, 2020)

3. Convention of Conservatism:

The convention of conservatism means a cautious approach or policy of ‘play safe’. This

convention ensures that uncertainties and risks inherent in business transactions should be

given a proper consideration. If there is a possibility of loss, it should be taken into account at

the earliest. On the other hand, a prospect of profit should be ignored up to the time it does

not materialize. (Mishra, 2020)

4. Convention of Materiality:

According to this convention only those events should be recorded which have a significant

bearing and insignificant things should be ignored. The avoidance of insignificant things will

not materially affect the records of the business.

It should be seen that the efforts involved in recording the events should be worth the labour

involved in it. There is no formula in making a distinction between material and immaterial

events. It is a matter of judgment and it is left to the accountant to take a decision.

(Mishra, 2020)

4.The principles of accounting:

There are general rules and concepts that govern the field of accounting. These general rules–

referred to as basic accounting principles and guidelines–form the groundwork on which

more detailed, complicated, and legalistic accounting rules are based. For example,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the Financial Accounting Standards Board (FASB) uses the basic accounting principles and

guidelines as a basis for their own detailed and comprehensive set of accounting rules and

standards.

The phrase "generally accepted accounting principles" (or "GAAP") consists of three

important sets of rules: (1) the basic accounting principles and guidelines, (2) the detailed

rules and standards issued by FASB and its predecessor the Accounting Principles Board

(APB), and (3) the generally accepted industry practices.

Basic Accounting Principles and Guidelines

Since GAAP is founded on the basic accounting principles and guidelines, we can better

understand GAAP if we understand those accounting principles. The following is a list of the

ten main accounting principles and guidelines together with a highly condensed explanation

of each.

Economic Entity Assumption

Monetary Unit Assumption

Time Period Assumption

Cost Principle

Full Disclosure Principle

Going Concern Principle

Matching Principle

Revenue Recognition Principle

Materiality

Conservatism. (Averkamp, 2020)

When financial reports are generated by professional accountants, we have certain

expectations of the information they present to us:

1. We expect the accounting information to be reliable, verifiable, and objective.

2. We expect consistency in the accounting information.

3. We expect comparability in the accounting information. (Averkamp, 2020)

Source document, General Journal, Ledgers, and Trial

balance:

The source document of An Phat:

7

guidelines as a basis for their own detailed and comprehensive set of accounting rules and

standards.

The phrase "generally accepted accounting principles" (or "GAAP") consists of three

important sets of rules: (1) the basic accounting principles and guidelines, (2) the detailed

rules and standards issued by FASB and its predecessor the Accounting Principles Board

(APB), and (3) the generally accepted industry practices.

Basic Accounting Principles and Guidelines

Since GAAP is founded on the basic accounting principles and guidelines, we can better

understand GAAP if we understand those accounting principles. The following is a list of the

ten main accounting principles and guidelines together with a highly condensed explanation

of each.

Economic Entity Assumption

Monetary Unit Assumption

Time Period Assumption

Cost Principle

Full Disclosure Principle

Going Concern Principle

Matching Principle

Revenue Recognition Principle

Materiality

Conservatism. (Averkamp, 2020)

When financial reports are generated by professional accountants, we have certain

expectations of the information they present to us:

1. We expect the accounting information to be reliable, verifiable, and objective.

2. We expect consistency in the accounting information.

3. We expect comparability in the accounting information. (Averkamp, 2020)

Source document, General Journal, Ledgers, and Trial

balance:

The source document of An Phat:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

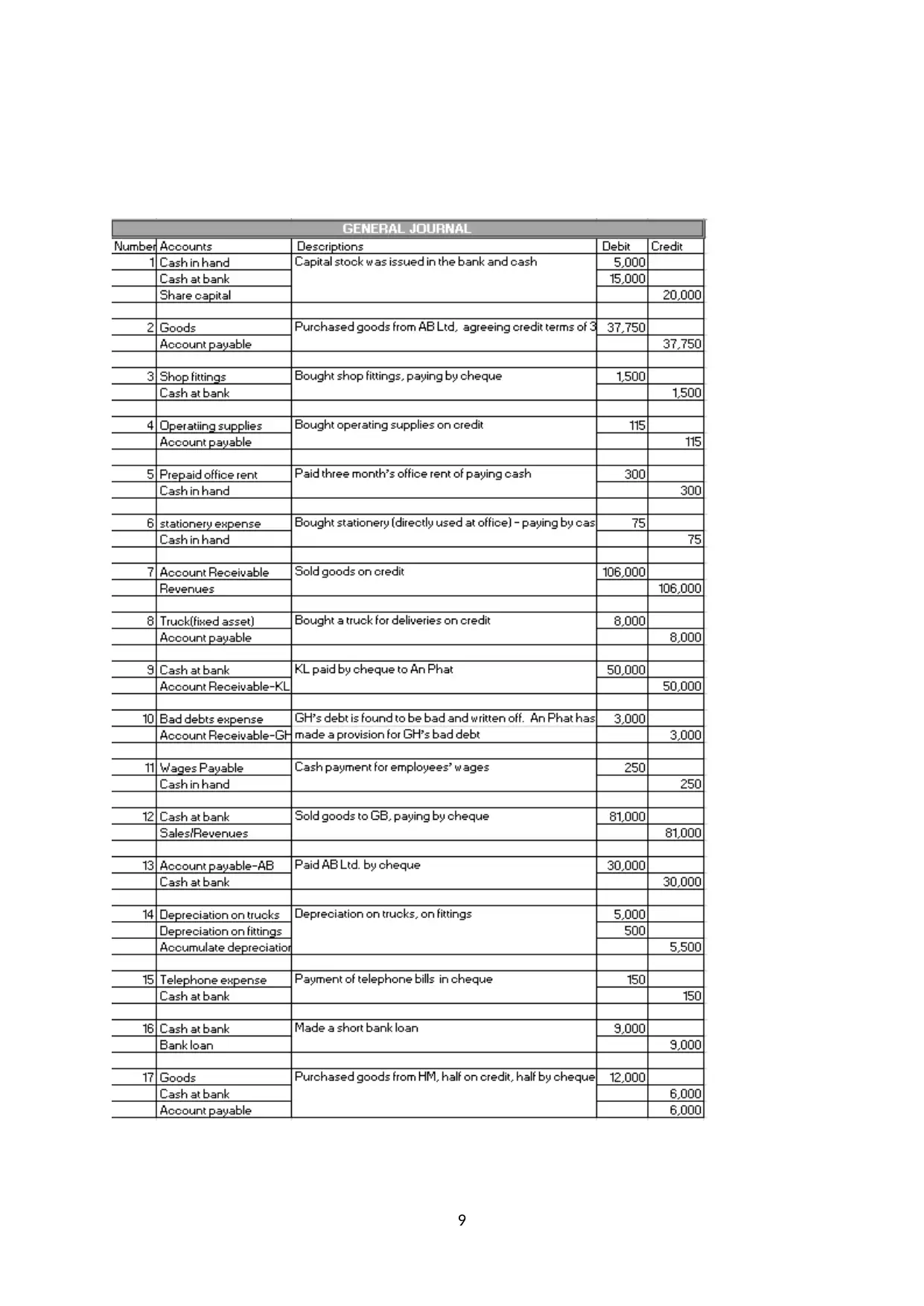

At 1 January 20X9, An Phat had the following balances on its ledger accounts: £

Cash in hand 2,000 Trucks at cost 17,500

Cash at bank 10,000 Accumulated Depreciation 5,000

Account Receivables (Dr) 26,000 Account Payable (Cr) 12,000

Goods 100,000 Bank loan 4,000

Operating supplies 22,000 Wages payables 1,000

Stationery 1,000 Telephone payables 200

Shop fittings at cost 28,000 Capital 184,300

1. An additional capital stock was issued £15,000 in the bank and £5,000 for cash.

2. Purchased goods to the value of £37,750 from AB Ltd., agreeing credit terms of 30 days

3. Bought shop fittings for £1,500, paying by cheque

4. Bought operating supplies on credit for £115

5. Paid three month’s office rent of £300 paying cash

6. Bought stationery (directly used at office) for £75 – paying by cash

7. Sold goods on credit to: GH £34,000; KL £72,000

8. Bought a truck for deliveries for £8,000 on credit

9. KL paid £50,000 by cheque to An Phat.

10. GH’s debt of £3,000 is found to be bad and written off. An Phat has not made a provision for

GH’s bad debt.

11. Cash payment of £250 for employees’ wages

12. Sold goods to GB £81,000, paying by cheque

13. Paid AB Ltd. £30,000 by cheque.

14. Depreciation on trucks at £5,000, on fittings at £500

15. Payment of telephone bills is £150 in cheque

16. Made a short bank loan of £9,000.

17. Purchased goods from HM for £12,000, half on credit, half by cheque.

1.General Journal:

General journal is a daybook or journal which is used to record transactions relating to

adjustment entries, opening stock, accounting errors etc. The source documents of this prime

entry book are journal voucher, copy of management reports and invoices.

It is where double entry bookkeeping entries are recorded by debiting one or more accounts

and crediting another one or more accounts with the same total amount. The total amount

debited and the total amount credited should always be equal, thereby ensuring

the accounting equation is maintained. In accounting and bookkeeping, a journal is a record

of financial transactions in order by date. (wikipedia, 2020)

The table of An Phat’s general journal :

8

Cash in hand 2,000 Trucks at cost 17,500

Cash at bank 10,000 Accumulated Depreciation 5,000

Account Receivables (Dr) 26,000 Account Payable (Cr) 12,000

Goods 100,000 Bank loan 4,000

Operating supplies 22,000 Wages payables 1,000

Stationery 1,000 Telephone payables 200

Shop fittings at cost 28,000 Capital 184,300

1. An additional capital stock was issued £15,000 in the bank and £5,000 for cash.

2. Purchased goods to the value of £37,750 from AB Ltd., agreeing credit terms of 30 days

3. Bought shop fittings for £1,500, paying by cheque

4. Bought operating supplies on credit for £115

5. Paid three month’s office rent of £300 paying cash

6. Bought stationery (directly used at office) for £75 – paying by cash

7. Sold goods on credit to: GH £34,000; KL £72,000

8. Bought a truck for deliveries for £8,000 on credit

9. KL paid £50,000 by cheque to An Phat.

10. GH’s debt of £3,000 is found to be bad and written off. An Phat has not made a provision for

GH’s bad debt.

11. Cash payment of £250 for employees’ wages

12. Sold goods to GB £81,000, paying by cheque

13. Paid AB Ltd. £30,000 by cheque.

14. Depreciation on trucks at £5,000, on fittings at £500

15. Payment of telephone bills is £150 in cheque

16. Made a short bank loan of £9,000.

17. Purchased goods from HM for £12,000, half on credit, half by cheque.

1.General Journal:

General journal is a daybook or journal which is used to record transactions relating to

adjustment entries, opening stock, accounting errors etc. The source documents of this prime

entry book are journal voucher, copy of management reports and invoices.

It is where double entry bookkeeping entries are recorded by debiting one or more accounts

and crediting another one or more accounts with the same total amount. The total amount

debited and the total amount credited should always be equal, thereby ensuring

the accounting equation is maintained. In accounting and bookkeeping, a journal is a record

of financial transactions in order by date. (wikipedia, 2020)

The table of An Phat’s general journal :

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

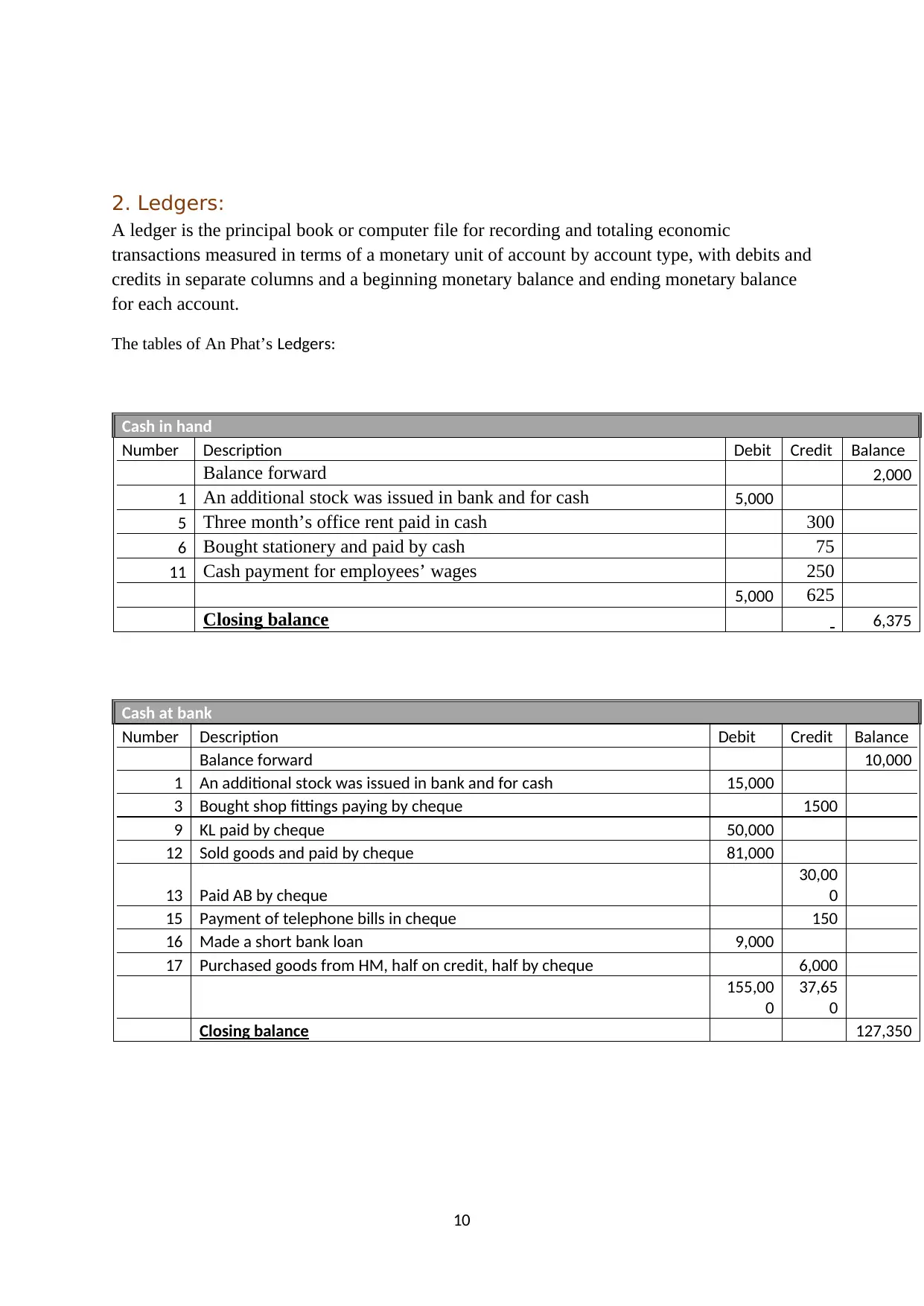

2. Ledgers:

A ledger is the principal book or computer file for recording and totaling economic

transactions measured in terms of a monetary unit of account by account type, with debits and

credits in separate columns and a beginning monetary balance and ending monetary balance

for each account.

The tables of An Phat’s Ledgers:

Cash in hand

Number Description Debit Credit Balance

Balance forward 2,000

1 An additional stock was issued in bank and for cash 5,000

5 Three month’s office rent paid in cash 300

6 Bought stationery and paid by cash 75

11 Cash payment for employees’ wages 250

5,000 625

Closing balance 6,375

Cash at bank

Number Description Debit Credit Balance

Balance forward 10,000

1 An additional stock was issued in bank and for cash 15,000

3 Bought shop fittings paying by cheque 1500

9 KL paid by cheque 50,000

12 Sold goods and paid by cheque 81,000

13 Paid AB by cheque

30,00

0

15 Payment of telephone bills in cheque 150

16 Made a short bank loan 9,000

17 Purchased goods from HM, half on credit, half by cheque 6,000

155,00

0

37,65

0

Closing balance 127,350

10

A ledger is the principal book or computer file for recording and totaling economic

transactions measured in terms of a monetary unit of account by account type, with debits and

credits in separate columns and a beginning monetary balance and ending monetary balance

for each account.

The tables of An Phat’s Ledgers:

Cash in hand

Number Description Debit Credit Balance

Balance forward 2,000

1 An additional stock was issued in bank and for cash 5,000

5 Three month’s office rent paid in cash 300

6 Bought stationery and paid by cash 75

11 Cash payment for employees’ wages 250

5,000 625

Closing balance 6,375

Cash at bank

Number Description Debit Credit Balance

Balance forward 10,000

1 An additional stock was issued in bank and for cash 15,000

3 Bought shop fittings paying by cheque 1500

9 KL paid by cheque 50,000

12 Sold goods and paid by cheque 81,000

13 Paid AB by cheque

30,00

0

15 Payment of telephone bills in cheque 150

16 Made a short bank loan 9,000

17 Purchased goods from HM, half on credit, half by cheque 6,000

155,00

0

37,65

0

Closing balance 127,350

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

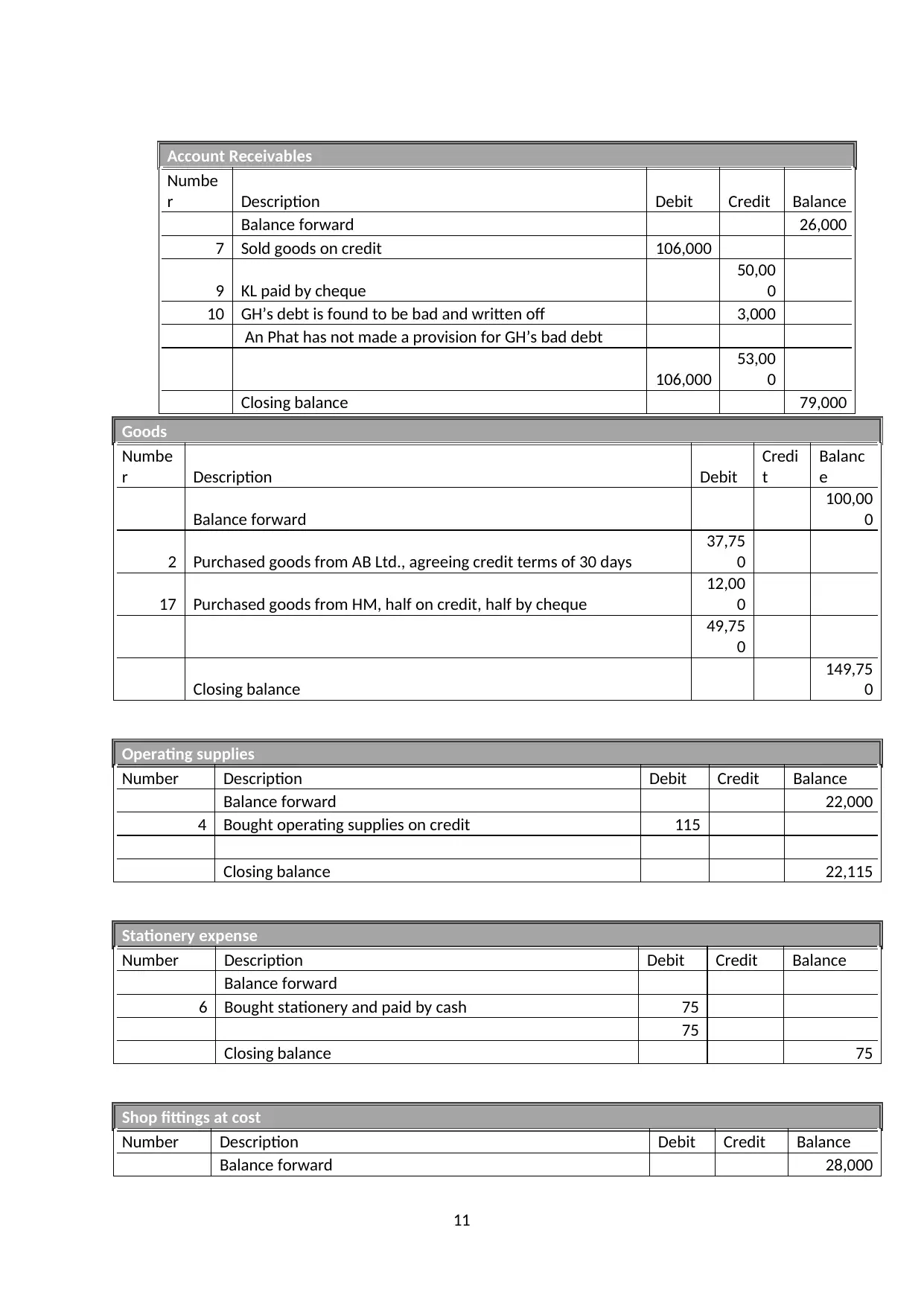

Goods

Numbe

r Description Debit

Credi

t

Balanc

e

Balance forward

100,00

0

2 Purchased goods from AB Ltd., agreeing credit terms of 30 days

37,75

0

17 Purchased goods from HM, half on credit, half by cheque

12,00

0

49,75

0

Closing balance

149,75

0

Operating supplies

Number Description Debit Credit Balance

Balance forward 22,000

4 Bought operating supplies on credit 115

Closing balance 22,115

Stationery expense

Number Description Debit Credit Balance

Balance forward

6 Bought stationery and paid by cash 75

75

Closing balance 75

Shop fittings at cost

Number Description Debit Credit Balance

Balance forward 28,000

11

Account Receivables

Numbe

r Description Debit Credit Balance

Balance forward 26,000

7 Sold goods on credit 106,000

9 KL paid by cheque

50,00

0

10 GH’s debt is found to be bad and written off 3,000

An Phat has not made a provision for GH’s bad debt

106,000

53,00

0

Closing balance 79,000

Numbe

r Description Debit

Credi

t

Balanc

e

Balance forward

100,00

0

2 Purchased goods from AB Ltd., agreeing credit terms of 30 days

37,75

0

17 Purchased goods from HM, half on credit, half by cheque

12,00

0

49,75

0

Closing balance

149,75

0

Operating supplies

Number Description Debit Credit Balance

Balance forward 22,000

4 Bought operating supplies on credit 115

Closing balance 22,115

Stationery expense

Number Description Debit Credit Balance

Balance forward

6 Bought stationery and paid by cash 75

75

Closing balance 75

Shop fittings at cost

Number Description Debit Credit Balance

Balance forward 28,000

11

Account Receivables

Numbe

r Description Debit Credit Balance

Balance forward 26,000

7 Sold goods on credit 106,000

9 KL paid by cheque

50,00

0

10 GH’s debt is found to be bad and written off 3,000

An Phat has not made a provision for GH’s bad debt

106,000

53,00

0

Closing balance 79,000

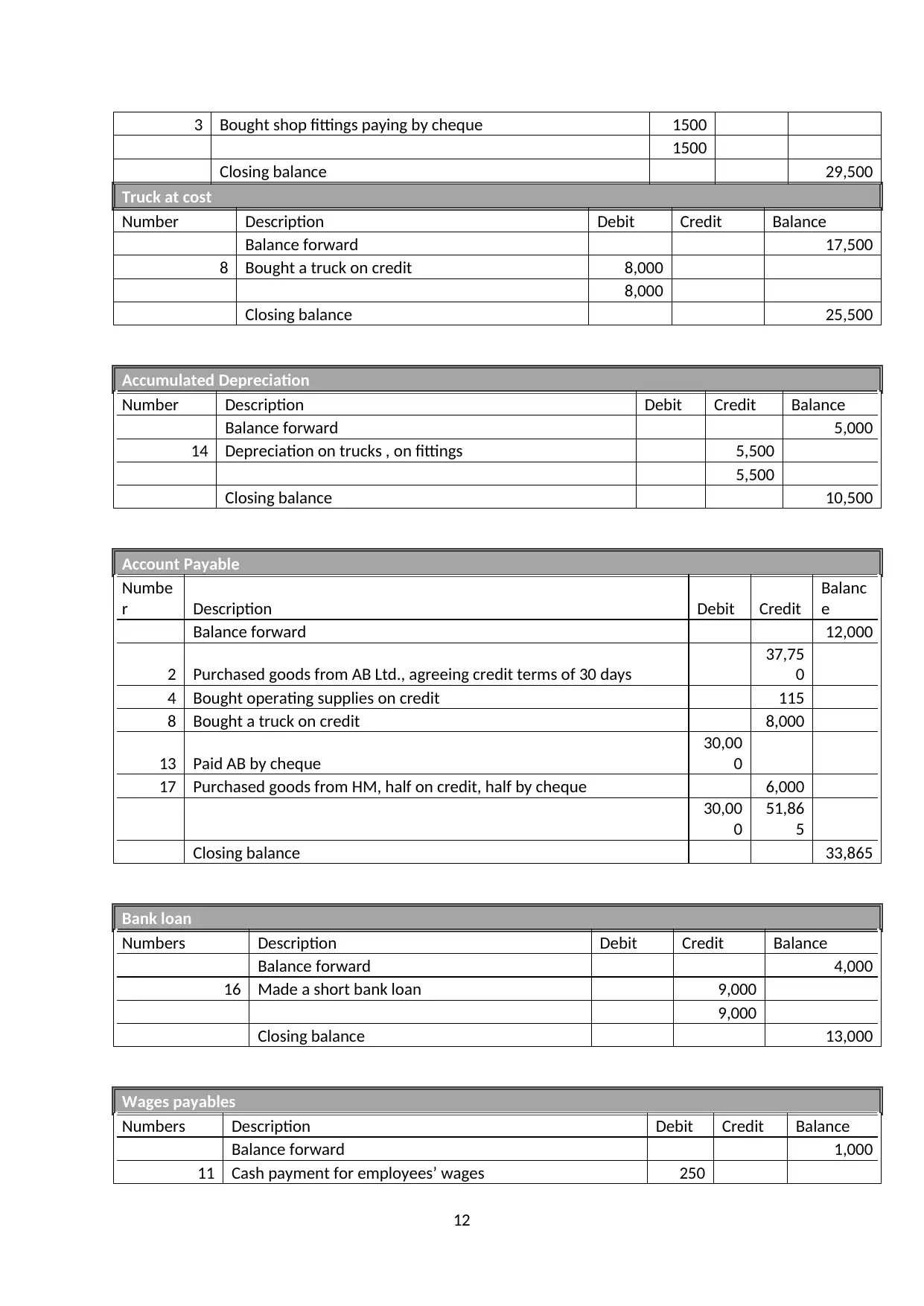

3 Bought shop fittings paying by cheque 1500

1500

Closing balance 29,500

Truck at cost

Number Description Debit Credit Balance

Balance forward 17,500

8 Bought a truck on credit 8,000

8,000

Closing balance 25,500

Accumulated Depreciation

Number Description Debit Credit Balance

Balance forward 5,000

14 Depreciation on trucks , on fittings 5,500

5,500

Closing balance 10,500

Account Payable

Numbe

r Description Debit Credit

Balanc

e

Balance forward 12,000

2 Purchased goods from AB Ltd., agreeing credit terms of 30 days

37,75

0

4 Bought operating supplies on credit 115

8 Bought a truck on credit 8,000

13 Paid AB by cheque

30,00

0

17 Purchased goods from HM, half on credit, half by cheque 6,000

30,00

0

51,86

5

Closing balance 33,865

Bank loan

Numbers Description Debit Credit Balance

Balance forward 4,000

16 Made a short bank loan 9,000

9,000

Closing balance 13,000

Wages payables

Numbers Description Debit Credit Balance

Balance forward 1,000

11 Cash payment for employees’ wages 250

12

1500

Closing balance 29,500

Truck at cost

Number Description Debit Credit Balance

Balance forward 17,500

8 Bought a truck on credit 8,000

8,000

Closing balance 25,500

Accumulated Depreciation

Number Description Debit Credit Balance

Balance forward 5,000

14 Depreciation on trucks , on fittings 5,500

5,500

Closing balance 10,500

Account Payable

Numbe

r Description Debit Credit

Balanc

e

Balance forward 12,000

2 Purchased goods from AB Ltd., agreeing credit terms of 30 days

37,75

0

4 Bought operating supplies on credit 115

8 Bought a truck on credit 8,000

13 Paid AB by cheque

30,00

0

17 Purchased goods from HM, half on credit, half by cheque 6,000

30,00

0

51,86

5

Closing balance 33,865

Bank loan

Numbers Description Debit Credit Balance

Balance forward 4,000

16 Made a short bank loan 9,000

9,000

Closing balance 13,000

Wages payables

Numbers Description Debit Credit Balance

Balance forward 1,000

11 Cash payment for employees’ wages 250

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.