Analyzing Business Transactions: Financial Statements and Ratios

VerifiedAdded on 2022/12/29

|15

|2324

|56

Report

AI Summary

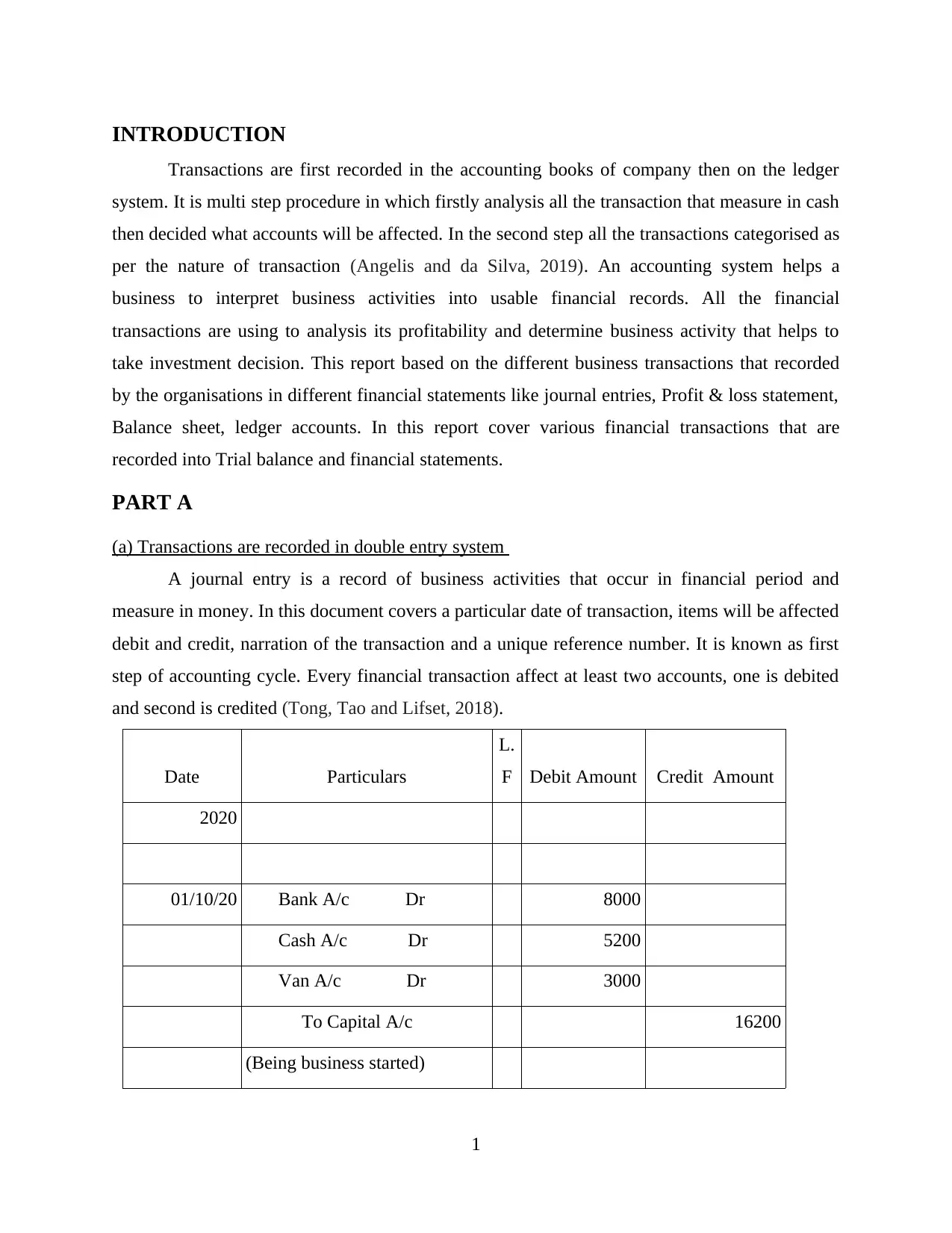

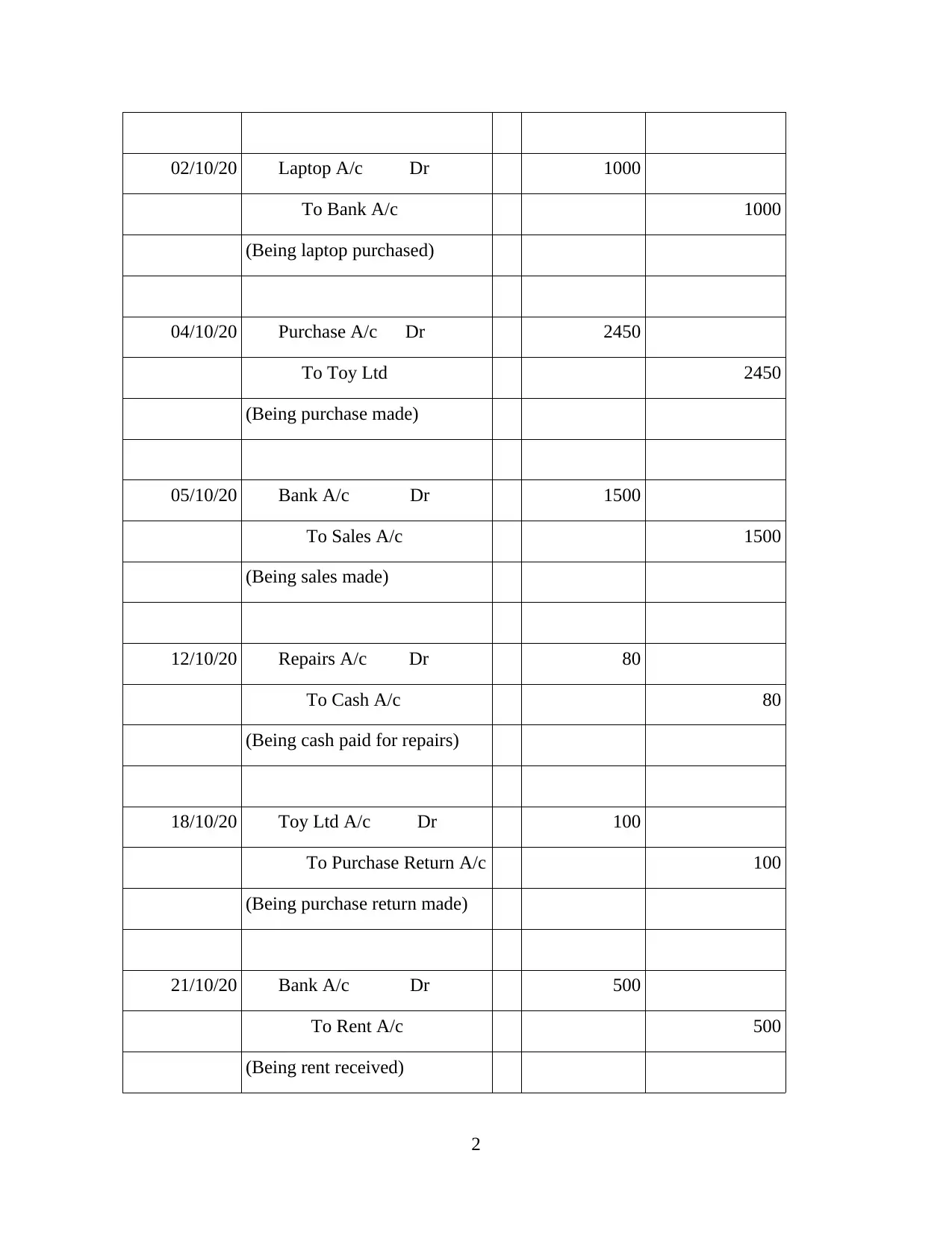

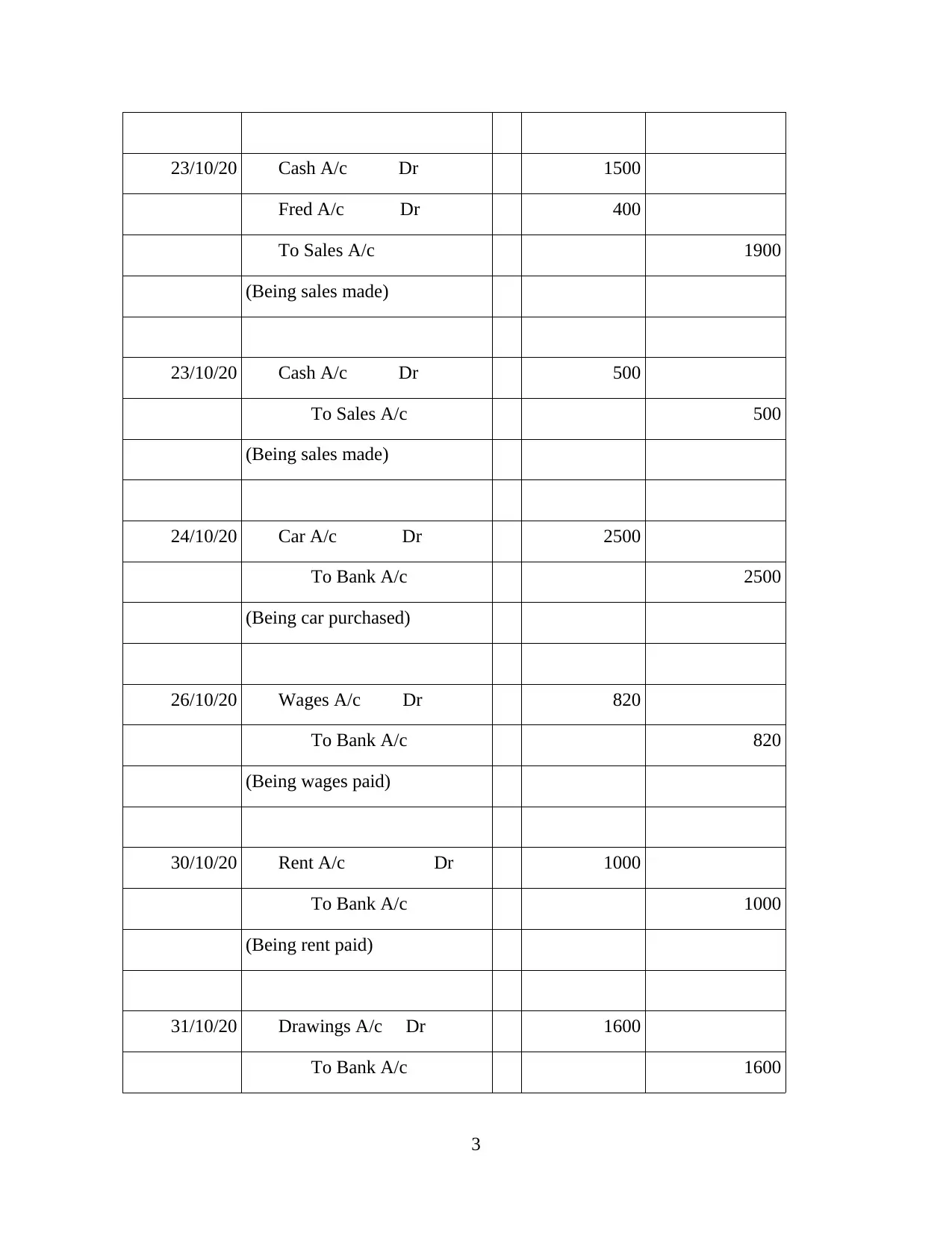

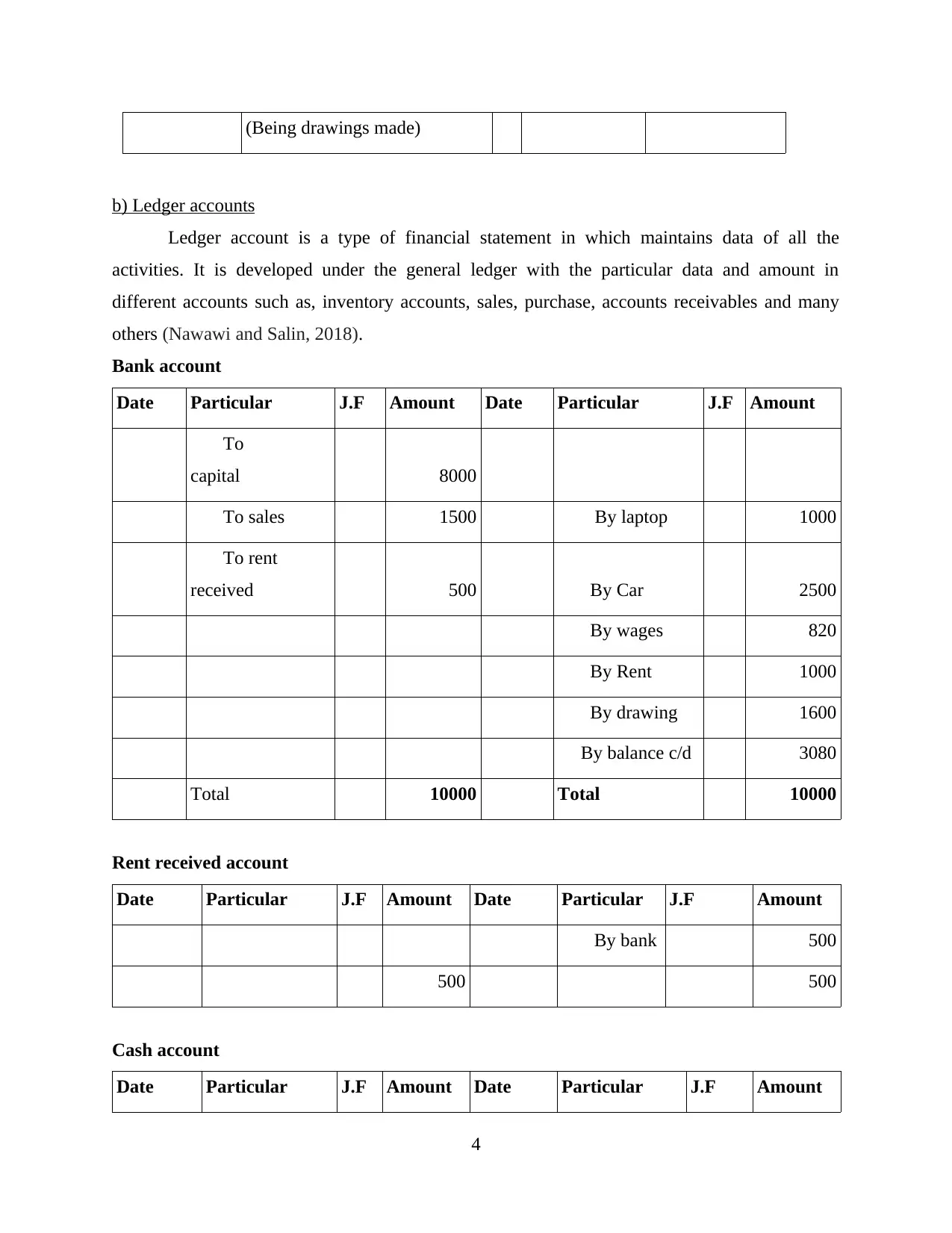

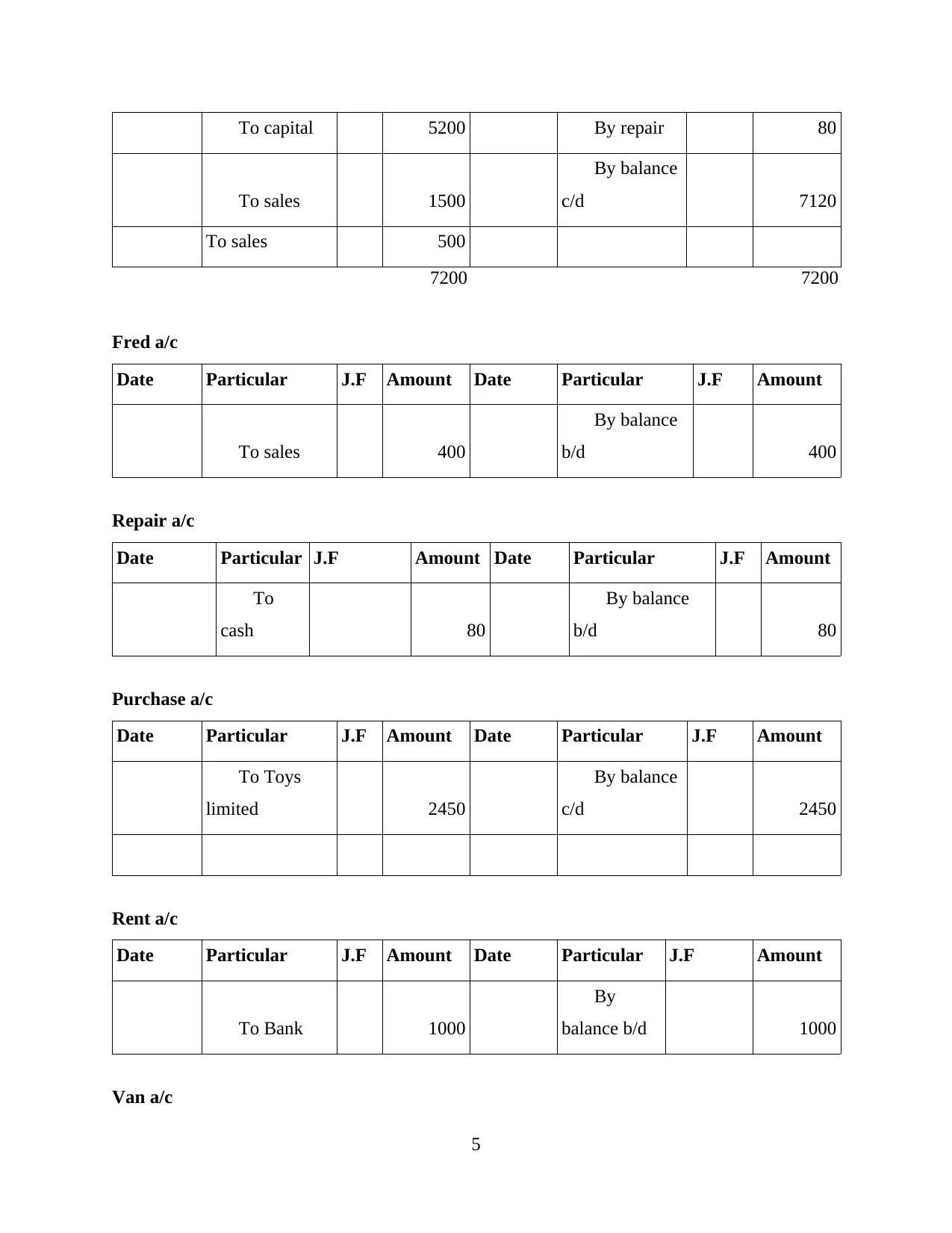

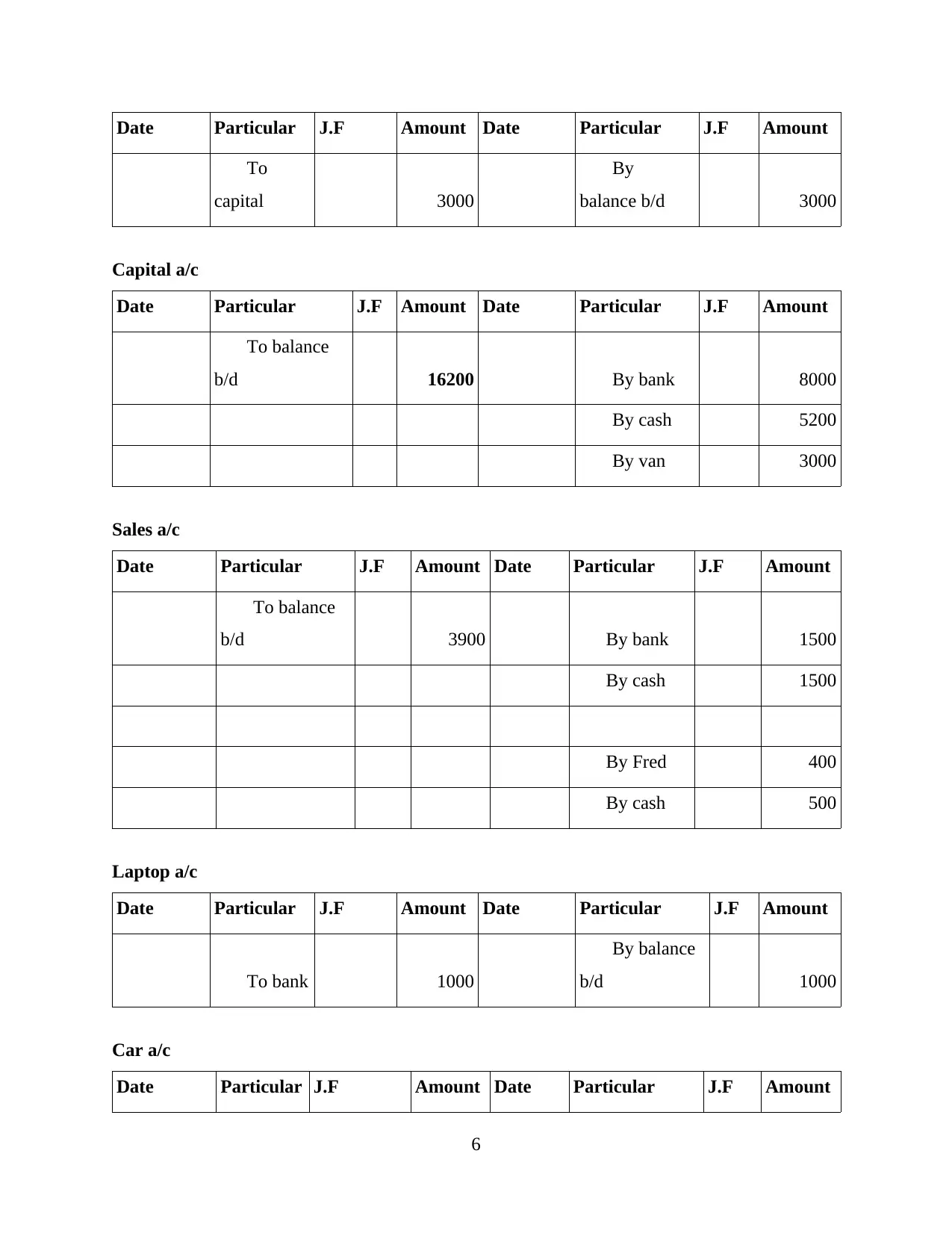

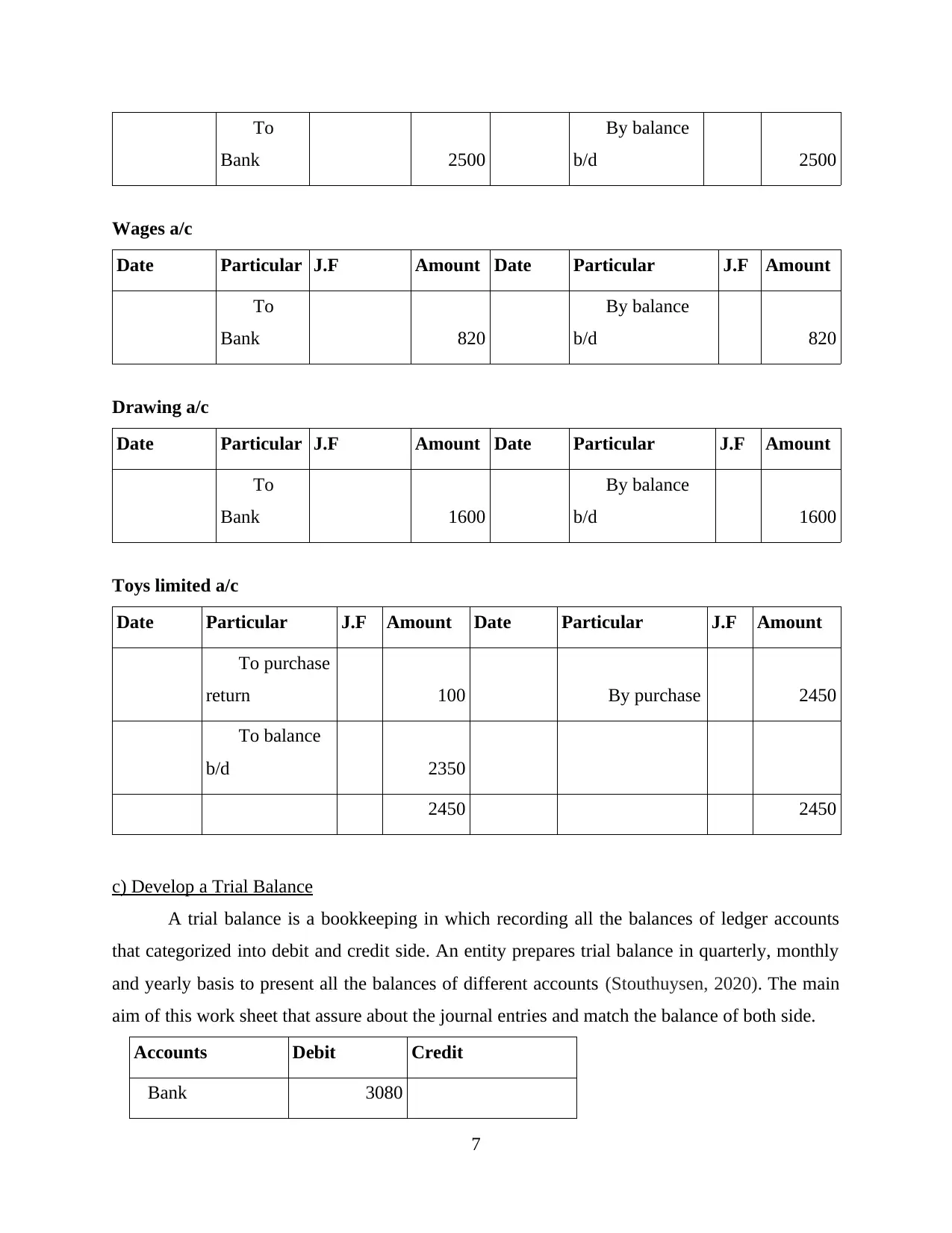

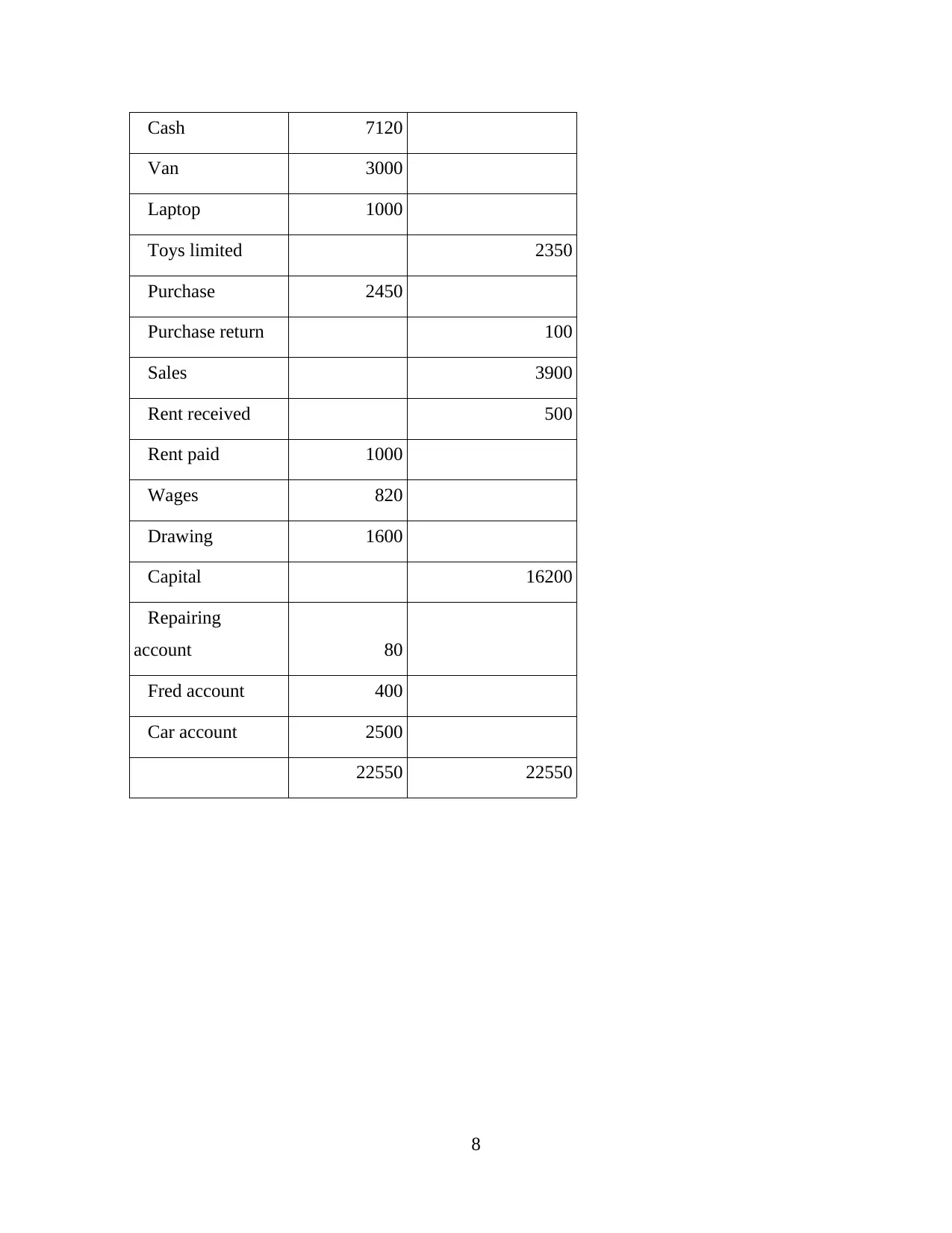

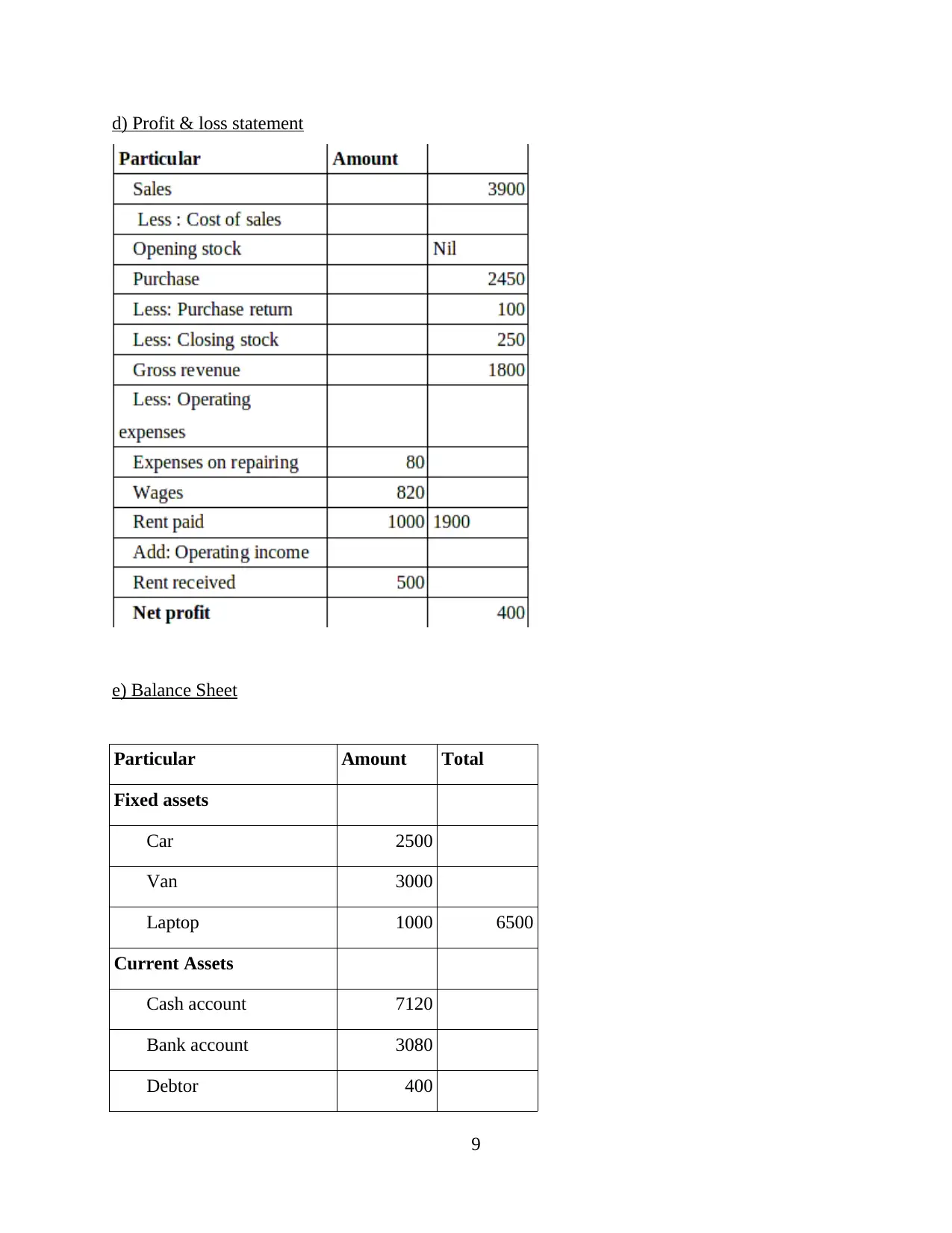

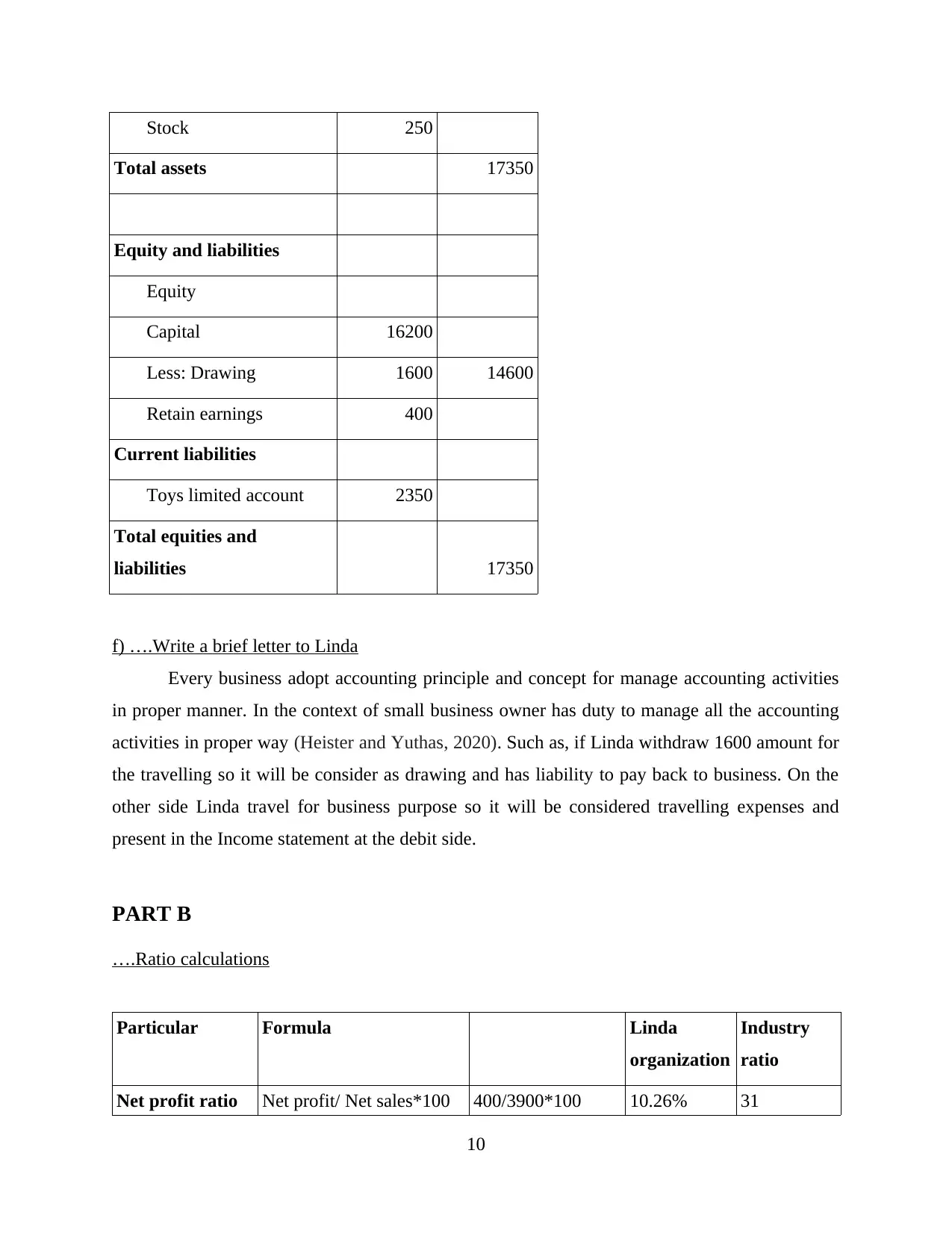

This report provides a comprehensive overview of recording business transactions and their impact on financial statements. It begins with an introduction to the double-entry system and the importance of accurate financial records. The report then details the process of recording transactions in journal entries and transferring them to ledger accounts, including examples of bank, cash, and capital accounts. A trial balance is developed to ensure the accuracy of the recorded transactions, followed by the creation of profit and loss statements and balance sheets. The report also includes a brief letter to Linda, addressing accounting principles for small businesses. Furthermore, the report delves into ratio calculations, including net profit, gross profit, current, quick, and accounts receivable and payable ratios, comparing Linda's business performance with industry benchmarks. The conclusion summarizes the key findings, emphasizing the importance of financial reporting and analysis in business decision-making.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.