Financial Management Report: Financial Analysis and Recommendations

VerifiedAdded on 2023/01/12

|13

|3681

|20

Report

AI Summary

This financial management report analyzes key concepts related to corporate finance. The report begins with an introduction to financial management, emphasizing its role in business operations. The main body delves into two primary questions: the first question examines valuation models (Price Earnings Ratio, Dividend Valuation Model, and Discounted Cash Flow) and their application to a merger or takeover scenario involving Aztec and Trojan Plc, with a recommendation for the Aztec board. The second question focuses on investment appraisal techniques (Payback Period, Accounting Rate of Return, Net Present Value, and Internal Rate of Return) to evaluate potential investments. The report calculates and compares these metrics to assess the financial viability of different investment options. The conclusion summarizes the key findings and recommendations regarding valuation and investment decisions. References are provided to support the analysis.

Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................6

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

MAIN BODY..................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................6

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

INTRODUCTION

Financial management is the implementation of business management concepts to a firm's

resources available. Proper control of the finances of a company offers reliable energy and

routine operation to ensure effective running (Antonopoulos and Hall, 2018). If budgets are not

properly addressed, a company may face obstacles that can have significant consequences for its

growth and progress. It is an excellent method for monitoring an organization's financial

operations such as fund acquisition, fund use, billing, transfers, risk management and everything

else relevant to finance. This report based on two different questions that is related to merger or

takeover and investment appraisal techniques.

MAIN BODY

Question 2

Price Earnings Ratio: It is the ratio of the present share price of the company to its earnings

per share. It offers us an understanding of how the consumer is expected to pay for the profits

from the company (Dwiastanti, 2017). It also shows the current value of the stock. Generally

speaking, a high PE ratio indicates market analysts are positive on stock and expect the firm to

show faster growth in earnings going ahead. In certain instances, though, this can also be viewed

as an expensive stock. A low PE ratio may be viewed either as an underrated asset or market

investors are not too optimistic about potential earnings growth for the firm.

Formula:

Price Earnings Ratio of Aztec = Share price / Earnings per Share

= 3.89 / 0.21

= 18.52

Price Earnings Ratio of Trojan Plc = 40.4 / 147

= 27.48

Share price of Trojan Plc = 18.52 * 27.48

= 5.08

Market value = 147 * 5.08

= 746.76

Here it is believed that the market needs Aztec to generate a return on the resources of

Trojan on its own assets equivalent to that.

3

Financial management is the implementation of business management concepts to a firm's

resources available. Proper control of the finances of a company offers reliable energy and

routine operation to ensure effective running (Antonopoulos and Hall, 2018). If budgets are not

properly addressed, a company may face obstacles that can have significant consequences for its

growth and progress. It is an excellent method for monitoring an organization's financial

operations such as fund acquisition, fund use, billing, transfers, risk management and everything

else relevant to finance. This report based on two different questions that is related to merger or

takeover and investment appraisal techniques.

MAIN BODY

Question 2

Price Earnings Ratio: It is the ratio of the present share price of the company to its earnings

per share. It offers us an understanding of how the consumer is expected to pay for the profits

from the company (Dwiastanti, 2017). It also shows the current value of the stock. Generally

speaking, a high PE ratio indicates market analysts are positive on stock and expect the firm to

show faster growth in earnings going ahead. In certain instances, though, this can also be viewed

as an expensive stock. A low PE ratio may be viewed either as an underrated asset or market

investors are not too optimistic about potential earnings growth for the firm.

Formula:

Price Earnings Ratio of Aztec = Share price / Earnings per Share

= 3.89 / 0.21

= 18.52

Price Earnings Ratio of Trojan Plc = 40.4 / 147

= 27.48

Share price of Trojan Plc = 18.52 * 27.48

= 5.08

Market value = 147 * 5.08

= 746.76

Here it is believed that the market needs Aztec to generate a return on the resources of

Trojan on its own assets equivalent to that.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dividend valuation model: It is a way to evaluate the share price of a company based on

the belief that the equity is worthy all the possible dividend payout investment relative to its

interest (Brooke, 2016). That put it differently; shares were used to measure the possible

dividends depending on the capital costs. For dividend calculation, the payout model values for

both g and r are needed, such as:

G = growth rate

R = interest rate

G = (13 / 10) = 1.14 %

Then,

g = 4 √ (13 / 10)

= 1.14%

The cost of equity using CAPM

Ke = 5 + (1.10 * (11 – 5)) = 11.60%

Po = 0.116 – 0.114 = 0.002

Total market value = 147 * 0.002 = 294 million

Discount cash flow method: It is an tool for measuring the worth of an expenditure

based on the projected cash flows (Hoque, 2017). The DCF calculation is seeking to measure the

importance of current investment based on projections of how much revenue it will generate in

the present. It refers both to cash contributions from investors and to company owners willing to

make improvements to their businesses, such as acquiring new equipment.

Discount cash flow method by using WACC of Aztec

Present value of:

Earnings = 40.4 * 1.02 / (0.09 – 0.02)

= 588.68

Assets sale = 21 million / 1.09

= 19.27

Synergy = 5 / 0.09

= 55.56

Total present value of Trojan Plc = 588.68 + 19.27 + 55.56

= 663.51

4

the belief that the equity is worthy all the possible dividend payout investment relative to its

interest (Brooke, 2016). That put it differently; shares were used to measure the possible

dividends depending on the capital costs. For dividend calculation, the payout model values for

both g and r are needed, such as:

G = growth rate

R = interest rate

G = (13 / 10) = 1.14 %

Then,

g = 4 √ (13 / 10)

= 1.14%

The cost of equity using CAPM

Ke = 5 + (1.10 * (11 – 5)) = 11.60%

Po = 0.116 – 0.114 = 0.002

Total market value = 147 * 0.002 = 294 million

Discount cash flow method: It is an tool for measuring the worth of an expenditure

based on the projected cash flows (Hoque, 2017). The DCF calculation is seeking to measure the

importance of current investment based on projections of how much revenue it will generate in

the present. It refers both to cash contributions from investors and to company owners willing to

make improvements to their businesses, such as acquiring new equipment.

Discount cash flow method by using WACC of Aztec

Present value of:

Earnings = 40.4 * 1.02 / (0.09 – 0.02)

= 588.68

Assets sale = 21 million / 1.09

= 19.27

Synergy = 5 / 0.09

= 55.56

Total present value of Trojan Plc = 588.68 + 19.27 + 55.56

= 663.51

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Discusses the problem which associated with valuation model and recommend best one for

Aztec board:

Price earnings ratio:

Advantages: This ratio helps in evaluating opportunities for financial success by

assessing the conditions of the business and comparing them with previous performances. That

often determines what is generated for the shareholders. PE ratios help investors to determine

growth prospects before engaging in the company. The ratios indicate companies that could be

affected by dramatic price changes. High PE leads to the selloff of the plant while low PE

indicates the continued output of the plant. It a allow shareholders to decide how much each

dollar they want to pay for the stock. That information can be used to identify underrated

inventories.

Disadvantages: At the time of calculating Price earnings ratio, it cannot take into account

debt / capital structure. Common accounting standards come in the way of PE comparisons

between various firms and different countries. These interventions include the depletion,

depreciation and taxation methods. Competitive securities find it impossible to decide what

amount profits we are trying to deliver and possibly keep P / E intangible. The slowing or stock

buy-backs will boost the earnings of the business so this will lead to increased risk costs by

doing so. The loss-making companies are unable to use the PE ratio because they cannot measure

losses at the early stage of production.

Discounted cash flow model:

Advantages: This model has a significant advantage as it limits spending to a single

amount. If the NPV is positive, the investment is considered to be a source of revenue; if it is

negative, then the portfolio would be a loser. That helps to make up to date decisions about

specific investments (Baños-Caballero, García-Teruel and Martínez-Solano, 2016). In fact, the

strategy allows company to change between significantly different resources. Investment

judgments are the method which is both precise and effective. If the measurements of the metric

are relatively accurate, no other method can do the job of evaluating the assets yield maximum

value.

Disadvantages: The greatest drawback of DCF is the reality that it needs to make a lot of

predictions. In the immediate future, cash flows will rely on different variables, such as

expectations for the market, market conditions, unpredictable issues and much more. Measuring

5

Aztec board:

Price earnings ratio:

Advantages: This ratio helps in evaluating opportunities for financial success by

assessing the conditions of the business and comparing them with previous performances. That

often determines what is generated for the shareholders. PE ratios help investors to determine

growth prospects before engaging in the company. The ratios indicate companies that could be

affected by dramatic price changes. High PE leads to the selloff of the plant while low PE

indicates the continued output of the plant. It a allow shareholders to decide how much each

dollar they want to pay for the stock. That information can be used to identify underrated

inventories.

Disadvantages: At the time of calculating Price earnings ratio, it cannot take into account

debt / capital structure. Common accounting standards come in the way of PE comparisons

between various firms and different countries. These interventions include the depletion,

depreciation and taxation methods. Competitive securities find it impossible to decide what

amount profits we are trying to deliver and possibly keep P / E intangible. The slowing or stock

buy-backs will boost the earnings of the business so this will lead to increased risk costs by

doing so. The loss-making companies are unable to use the PE ratio because they cannot measure

losses at the early stage of production.

Discounted cash flow model:

Advantages: This model has a significant advantage as it limits spending to a single

amount. If the NPV is positive, the investment is considered to be a source of revenue; if it is

negative, then the portfolio would be a loser. That helps to make up to date decisions about

specific investments (Baños-Caballero, García-Teruel and Martínez-Solano, 2016). In fact, the

strategy allows company to change between significantly different resources. Investment

judgments are the method which is both precise and effective. If the measurements of the metric

are relatively accurate, no other method can do the job of evaluating the assets yield maximum

value.

Disadvantages: The greatest drawback of DCF is the reality that it needs to make a lot of

predictions. In the immediate future, cash flows will rely on different variables, such as

expectations for the market, market conditions, unpredictable issues and much more. Measuring

5

future optimistic cash flows will lead to assumptions about a project that will not profit off later,

damaging earnings. Earning capital moves too low, this may lead to missed opportunity to make

an asset seem valued high. It can be a risk to settle on a cost of returning for the version and

the version will need to be accurately estimated for reimbursement.

Dividend valuation model:

Advantage: It does not enable for the establishment of a wealth generation presumption. For

the securities measured, the rate of earnings growth must be greater than the rate of return;

otherwise the calculation does not work. It implies they use this formula to predict what future

dividends will be, based on what the current dividend looks to be. Determined the place to invest

is easier when using the valuation formula, since you should be able to maintain the investment

interest. Around the same time, they will earn money from either the dividends they collect, that

can help to increase the average value of investments, especially if individual have invested in

many dividends paying stocks from either a wide range of industries

Disadvantages: When matching tiny-cap stock with large-cap stocks, it is the smaller

businesses that have fared well over long time spans. Most small businesses are unable to

manage a dividend which means that this valuation model could not be used to measure their

value (Danes, Garbow and Jokela, 2016). This should be extended to securities paying by the

dividend. When shareholders concentrated solely on this specific example, they would lose a lot

of possibilities of generating value for the portfolio. There have been a variety of factors which

can influence the price of shares over the time. Customer retention, market awareness and even

the ownership of intangibles also have the power to increase the profitability of the business.

This is proposed from the preceding review that the company should adopt the P / E ratio as

a valuation of its securities. It lets the managers make their business decisions to improve the

productivity or competitiveness of the company.

Question 3

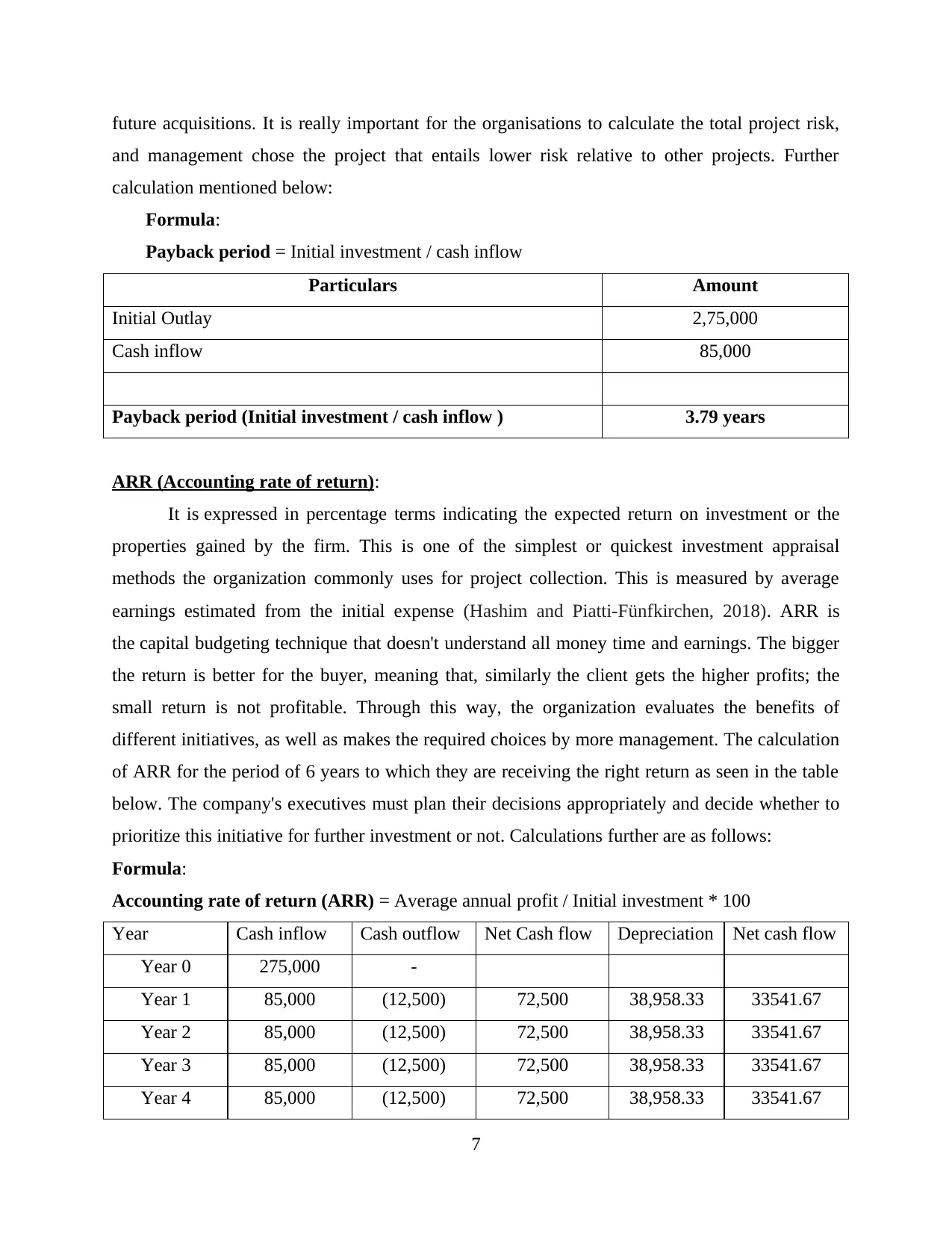

Payback period:

It is the methodology of capital budgeting which is used to assess more spending and to

allow the investors to consider or pick the right alternative. Payback period is the time on which

the organization will recover the money paid. Low payback time is beneficial for the client, as it

helps to recover the entire investment as well as to continue earning profits on it. It is guided by

the incorrigible appraisal plan executives at the organization who can render educated choices on

6

damaging earnings. Earning capital moves too low, this may lead to missed opportunity to make

an asset seem valued high. It can be a risk to settle on a cost of returning for the version and

the version will need to be accurately estimated for reimbursement.

Dividend valuation model:

Advantage: It does not enable for the establishment of a wealth generation presumption. For

the securities measured, the rate of earnings growth must be greater than the rate of return;

otherwise the calculation does not work. It implies they use this formula to predict what future

dividends will be, based on what the current dividend looks to be. Determined the place to invest

is easier when using the valuation formula, since you should be able to maintain the investment

interest. Around the same time, they will earn money from either the dividends they collect, that

can help to increase the average value of investments, especially if individual have invested in

many dividends paying stocks from either a wide range of industries

Disadvantages: When matching tiny-cap stock with large-cap stocks, it is the smaller

businesses that have fared well over long time spans. Most small businesses are unable to

manage a dividend which means that this valuation model could not be used to measure their

value (Danes, Garbow and Jokela, 2016). This should be extended to securities paying by the

dividend. When shareholders concentrated solely on this specific example, they would lose a lot

of possibilities of generating value for the portfolio. There have been a variety of factors which

can influence the price of shares over the time. Customer retention, market awareness and even

the ownership of intangibles also have the power to increase the profitability of the business.

This is proposed from the preceding review that the company should adopt the P / E ratio as

a valuation of its securities. It lets the managers make their business decisions to improve the

productivity or competitiveness of the company.

Question 3

Payback period:

It is the methodology of capital budgeting which is used to assess more spending and to

allow the investors to consider or pick the right alternative. Payback period is the time on which

the organization will recover the money paid. Low payback time is beneficial for the client, as it

helps to recover the entire investment as well as to continue earning profits on it. It is guided by

the incorrigible appraisal plan executives at the organization who can render educated choices on

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

future acquisitions. It is really important for the organisations to calculate the total project risk,

and management chose the project that entails lower risk relative to other projects. Further

calculation mentioned below:

Formula:

Payback period = Initial investment / cash inflow

Particulars Amount

Initial Outlay 2,75,000

Cash inflow 85,000

Payback period (Initial investment / cash inflow ) 3.79 years

ARR (Accounting rate of return):

It is expressed in percentage terms indicating the expected return on investment or the

properties gained by the firm. This is one of the simplest or quickest investment appraisal

methods the organization commonly uses for project collection. This is measured by average

earnings estimated from the initial expense (Hashim and Piatti-Fünfkirchen, 2018). ARR is

the capital budgeting technique that doesn't understand all money time and earnings. The bigger

the return is better for the buyer, meaning that, similarly the client gets the higher profits; the

small return is not profitable. Through this way, the organization evaluates the benefits of

different initiatives, as well as makes the required choices by more management. The calculation

of ARR for the period of 6 years to which they are receiving the right return as seen in the table

below. The company's executives must plan their decisions appropriately and decide whether to

prioritize this initiative for further investment or not. Calculations further are as follows:

Formula:

Accounting rate of return (ARR) = Average annual profit / Initial investment * 100

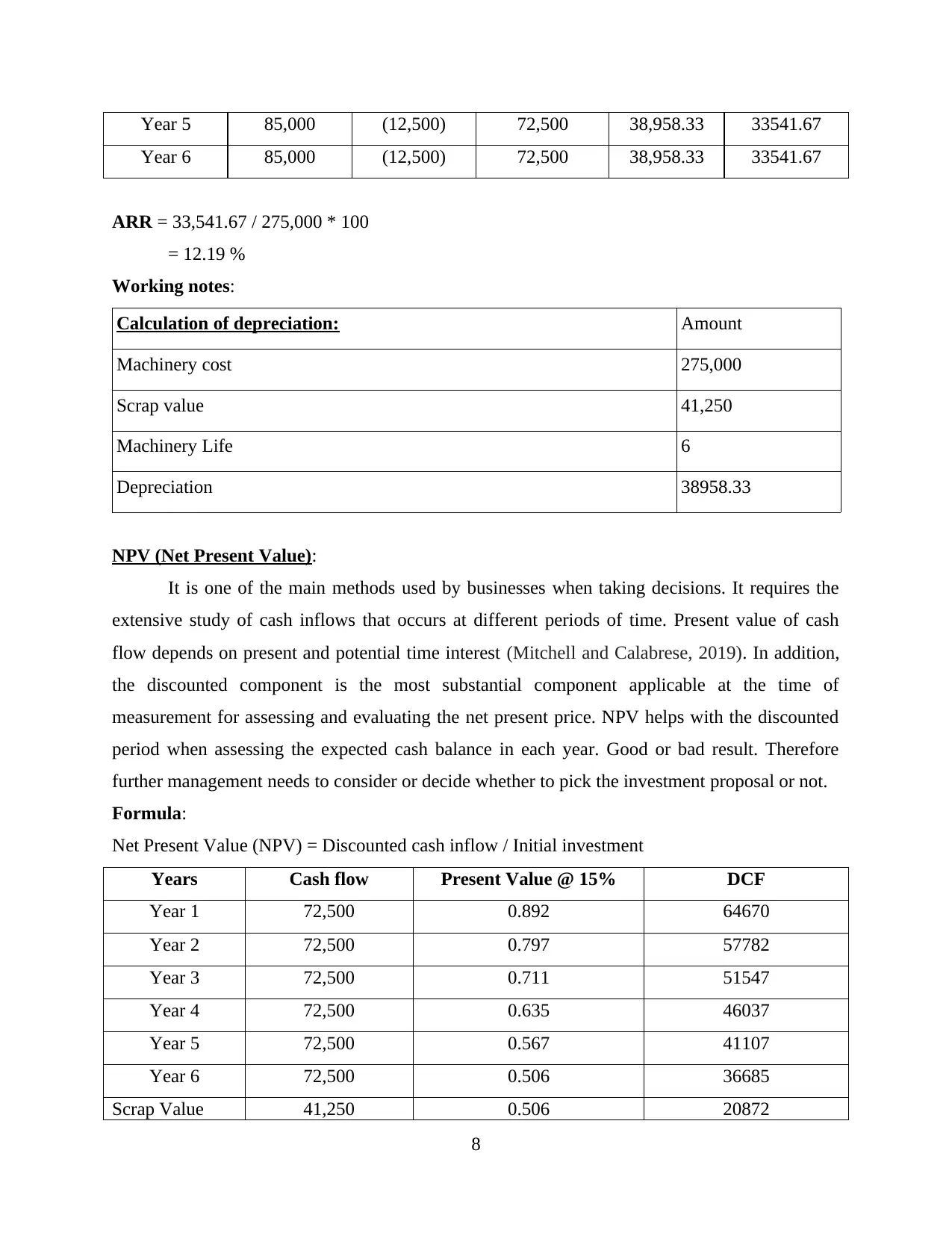

Year Cash inflow Cash outflow Net Cash flow Depreciation Net cash flow

Year 0 275,000 -

Year 1 85,000 (12,500) 72,500 38,958.33 33541.67

Year 2 85,000 (12,500) 72,500 38,958.33 33541.67

Year 3 85,000 (12,500) 72,500 38,958.33 33541.67

Year 4 85,000 (12,500) 72,500 38,958.33 33541.67

7

and management chose the project that entails lower risk relative to other projects. Further

calculation mentioned below:

Formula:

Payback period = Initial investment / cash inflow

Particulars Amount

Initial Outlay 2,75,000

Cash inflow 85,000

Payback period (Initial investment / cash inflow ) 3.79 years

ARR (Accounting rate of return):

It is expressed in percentage terms indicating the expected return on investment or the

properties gained by the firm. This is one of the simplest or quickest investment appraisal

methods the organization commonly uses for project collection. This is measured by average

earnings estimated from the initial expense (Hashim and Piatti-Fünfkirchen, 2018). ARR is

the capital budgeting technique that doesn't understand all money time and earnings. The bigger

the return is better for the buyer, meaning that, similarly the client gets the higher profits; the

small return is not profitable. Through this way, the organization evaluates the benefits of

different initiatives, as well as makes the required choices by more management. The calculation

of ARR for the period of 6 years to which they are receiving the right return as seen in the table

below. The company's executives must plan their decisions appropriately and decide whether to

prioritize this initiative for further investment or not. Calculations further are as follows:

Formula:

Accounting rate of return (ARR) = Average annual profit / Initial investment * 100

Year Cash inflow Cash outflow Net Cash flow Depreciation Net cash flow

Year 0 275,000 -

Year 1 85,000 (12,500) 72,500 38,958.33 33541.67

Year 2 85,000 (12,500) 72,500 38,958.33 33541.67

Year 3 85,000 (12,500) 72,500 38,958.33 33541.67

Year 4 85,000 (12,500) 72,500 38,958.33 33541.67

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year 5 85,000 (12,500) 72,500 38,958.33 33541.67

Year 6 85,000 (12,500) 72,500 38,958.33 33541.67

ARR = 33,541.67 / 275,000 * 100

= 12.19 %

Working notes:

Calculation of depreciation: Amount

Machinery cost 275,000

Scrap value 41,250

Machinery Life 6

Depreciation 38958.33

NPV (Net Present Value):

It is one of the main methods used by businesses when taking decisions. It requires the

extensive study of cash inflows that occurs at different periods of time. Present value of cash

flow depends on present and potential time interest (Mitchell and Calabrese, 2019). In addition,

the discounted component is the most substantial component applicable at the time of

measurement for assessing and evaluating the net present price. NPV helps with the discounted

period when assessing the expected cash balance in each year. Good or bad result. Therefore

further management needs to consider or decide whether to pick the investment proposal or not.

Formula:

Net Present Value (NPV) = Discounted cash inflow / Initial investment

Years Cash flow Present Value @ 15% DCF

Year 1 72,500 0.892 64670

Year 2 72,500 0.797 57782

Year 3 72,500 0.711 51547

Year 4 72,500 0.635 46037

Year 5 72,500 0.567 41107

Year 6 72,500 0.506 36685

Scrap Value 41,250 0.506 20872

8

Year 6 85,000 (12,500) 72,500 38,958.33 33541.67

ARR = 33,541.67 / 275,000 * 100

= 12.19 %

Working notes:

Calculation of depreciation: Amount

Machinery cost 275,000

Scrap value 41,250

Machinery Life 6

Depreciation 38958.33

NPV (Net Present Value):

It is one of the main methods used by businesses when taking decisions. It requires the

extensive study of cash inflows that occurs at different periods of time. Present value of cash

flow depends on present and potential time interest (Mitchell and Calabrese, 2019). In addition,

the discounted component is the most substantial component applicable at the time of

measurement for assessing and evaluating the net present price. NPV helps with the discounted

period when assessing the expected cash balance in each year. Good or bad result. Therefore

further management needs to consider or decide whether to pick the investment proposal or not.

Formula:

Net Present Value (NPV) = Discounted cash inflow / Initial investment

Years Cash flow Present Value @ 15% DCF

Year 1 72,500 0.892 64670

Year 2 72,500 0.797 57782

Year 3 72,500 0.711 51547

Year 4 72,500 0.635 46037

Year 5 72,500 0.567 41107

Year 6 72,500 0.506 36685

Scrap Value 41,250 0.506 20872

8

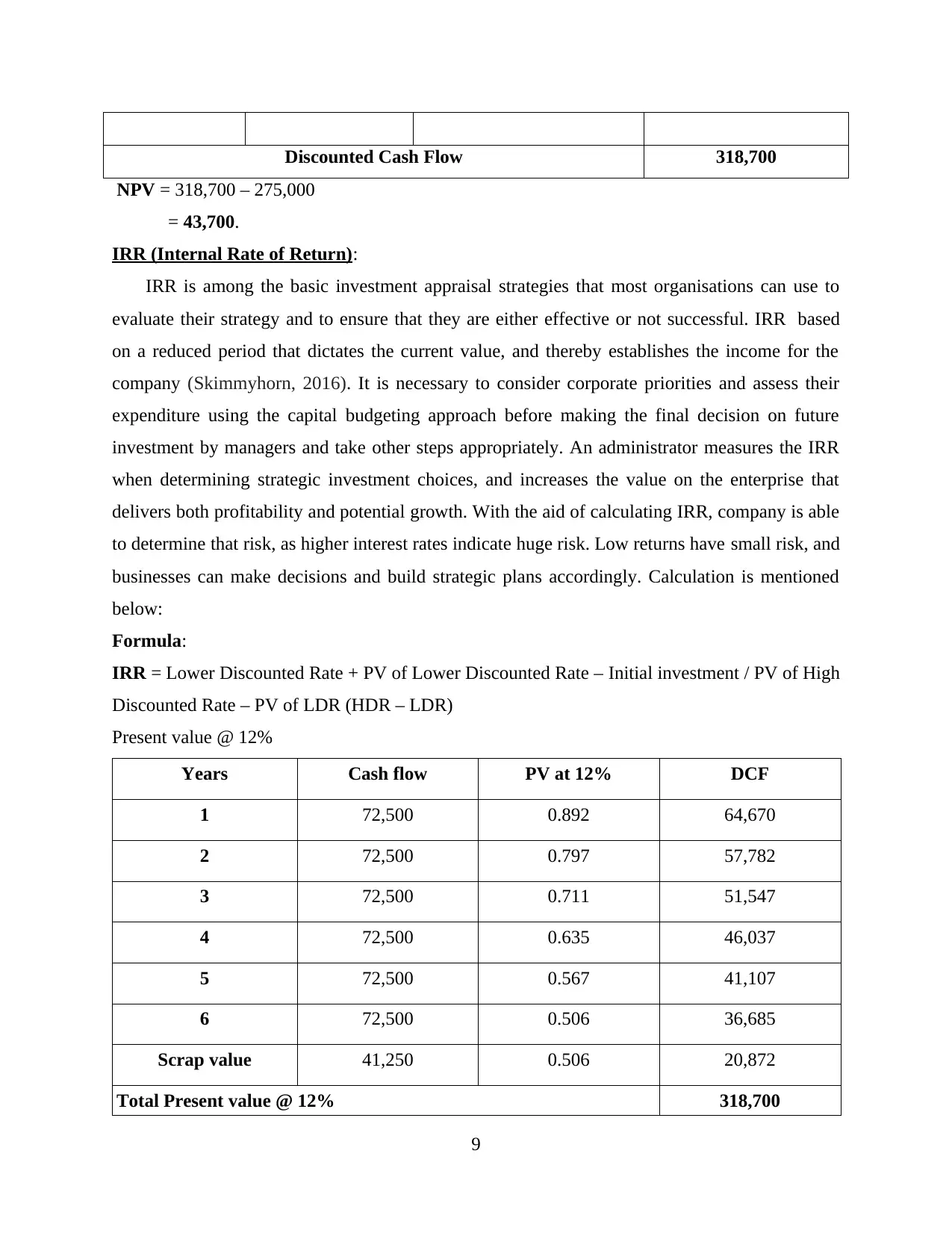

Discounted Cash Flow 318,700

NPV = 318,700 – 275,000

= 43,700.

IRR (Internal Rate of Return):

IRR is among the basic investment appraisal strategies that most organisations can use to

evaluate their strategy and to ensure that they are either effective or not successful. IRR based

on a reduced period that dictates the current value, and thereby establishes the income for the

company (Skimmyhorn, 2016). It is necessary to consider corporate priorities and assess their

expenditure using the capital budgeting approach before making the final decision on future

investment by managers and take other steps appropriately. An administrator measures the IRR

when determining strategic investment choices, and increases the value on the enterprise that

delivers both profitability and potential growth. With the aid of calculating IRR, company is able

to determine that risk, as higher interest rates indicate huge risk. Low returns have small risk, and

businesses can make decisions and build strategic plans accordingly. Calculation is mentioned

below:

Formula:

IRR = Lower Discounted Rate + PV of Lower Discounted Rate – Initial investment / PV of High

Discounted Rate – PV of LDR (HDR – LDR)

Present value @ 12%

Years Cash flow PV at 12% DCF

1 72,500 0.892 64,670

2 72,500 0.797 57,782

3 72,500 0.711 51,547

4 72,500 0.635 46,037

5 72,500 0.567 41,107

6 72,500 0.506 36,685

Scrap value 41,250 0.506 20,872

Total Present value @ 12% 318,700

9

NPV = 318,700 – 275,000

= 43,700.

IRR (Internal Rate of Return):

IRR is among the basic investment appraisal strategies that most organisations can use to

evaluate their strategy and to ensure that they are either effective or not successful. IRR based

on a reduced period that dictates the current value, and thereby establishes the income for the

company (Skimmyhorn, 2016). It is necessary to consider corporate priorities and assess their

expenditure using the capital budgeting approach before making the final decision on future

investment by managers and take other steps appropriately. An administrator measures the IRR

when determining strategic investment choices, and increases the value on the enterprise that

delivers both profitability and potential growth. With the aid of calculating IRR, company is able

to determine that risk, as higher interest rates indicate huge risk. Low returns have small risk, and

businesses can make decisions and build strategic plans accordingly. Calculation is mentioned

below:

Formula:

IRR = Lower Discounted Rate + PV of Lower Discounted Rate – Initial investment / PV of High

Discounted Rate – PV of LDR (HDR – LDR)

Present value @ 12%

Years Cash flow PV at 12% DCF

1 72,500 0.892 64,670

2 72,500 0.797 57,782

3 72,500 0.711 51,547

4 72,500 0.635 46,037

5 72,500 0.567 41,107

6 72,500 0.506 36,685

Scrap value 41,250 0.506 20,872

Total Present value @ 12% 318,700

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

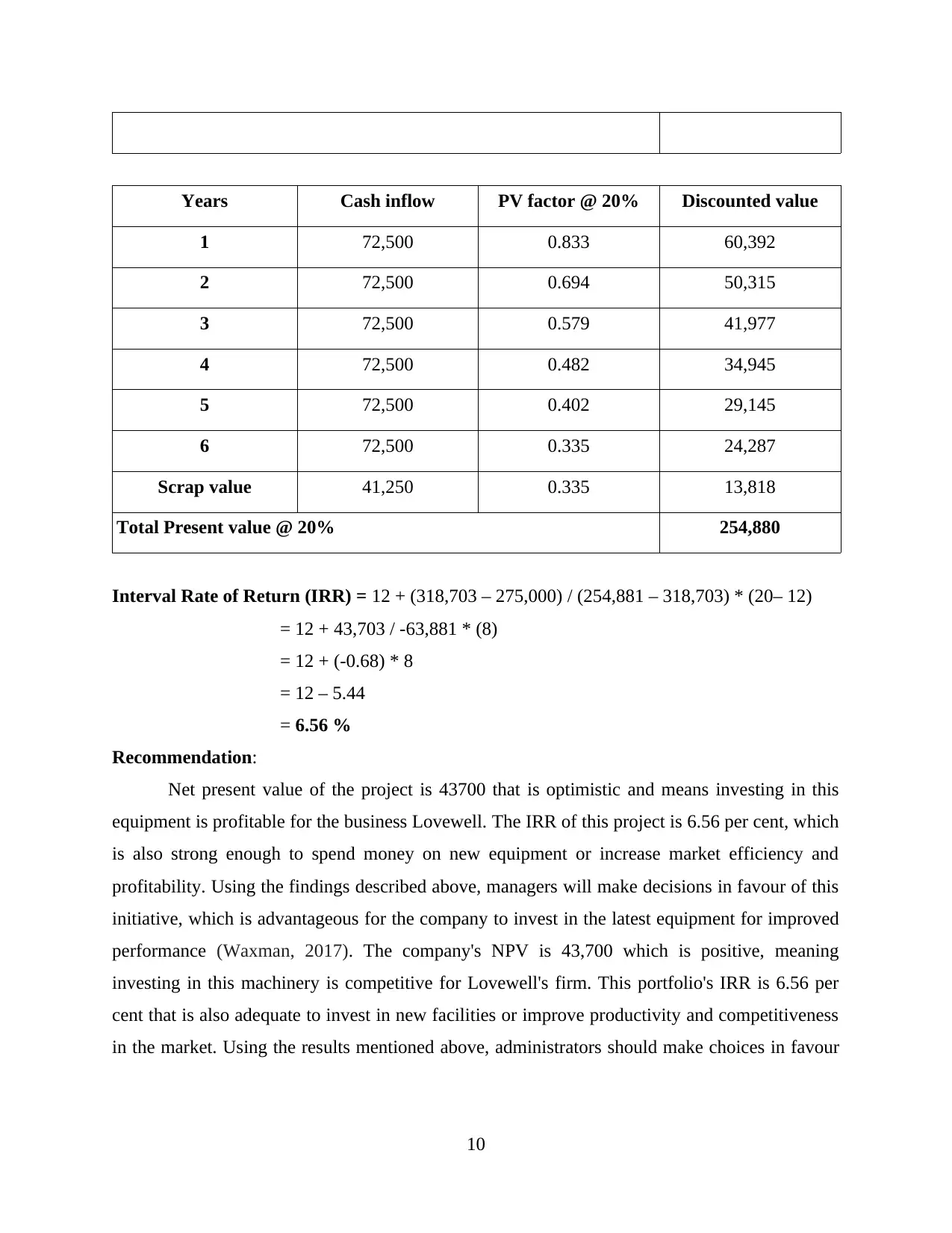

Years Cash inflow PV factor @ 20% Discounted value

1 72,500 0.833 60,392

2 72,500 0.694 50,315

3 72,500 0.579 41,977

4 72,500 0.482 34,945

5 72,500 0.402 29,145

6 72,500 0.335 24,287

Scrap value 41,250 0.335 13,818

Total Present value @ 20% 254,880

Interval Rate of Return (IRR) = 12 + (318,703 – 275,000) / (254,881 – 318,703) * (20– 12)

= 12 + 43,703 / -63,881 * (8)

= 12 + (-0.68) * 8

= 12 – 5.44

= 6.56 %

Recommendation:

Net present value of the project is 43700 that is optimistic and means investing in this

equipment is profitable for the business Lovewell. The IRR of this project is 6.56 per cent, which

is also strong enough to spend money on new equipment or increase market efficiency and

profitability. Using the findings described above, managers will make decisions in favour of this

initiative, which is advantageous for the company to invest in the latest equipment for improved

performance (Waxman, 2017). The company's NPV is 43,700 which is positive, meaning

investing in this machinery is competitive for Lovewell's firm. This portfolio's IRR is 6.56 per

cent that is also adequate to invest in new facilities or improve productivity and competitiveness

in the market. Using the results mentioned above, administrators should make choices in favour

10

1 72,500 0.833 60,392

2 72,500 0.694 50,315

3 72,500 0.579 41,977

4 72,500 0.482 34,945

5 72,500 0.402 29,145

6 72,500 0.335 24,287

Scrap value 41,250 0.335 13,818

Total Present value @ 20% 254,880

Interval Rate of Return (IRR) = 12 + (318,703 – 275,000) / (254,881 – 318,703) * (20– 12)

= 12 + 43,703 / -63,881 * (8)

= 12 + (-0.68) * 8

= 12 – 5.44

= 6.56 %

Recommendation:

Net present value of the project is 43700 that is optimistic and means investing in this

equipment is profitable for the business Lovewell. The IRR of this project is 6.56 per cent, which

is also strong enough to spend money on new equipment or increase market efficiency and

profitability. Using the findings described above, managers will make decisions in favour of this

initiative, which is advantageous for the company to invest in the latest equipment for improved

performance (Waxman, 2017). The company's NPV is 43,700 which is positive, meaning

investing in this machinery is competitive for Lovewell's firm. This portfolio's IRR is 6.56 per

cent that is also adequate to invest in new facilities or improve productivity and competitiveness

in the market. Using the results mentioned above, administrators should make choices in favour

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of this program which is beneficial for the organization to spend for successful performance in

the new equipment.

Critically evaluate the benefits or drawbacks of investment appraisal technique:

Payback period:

Benefits: Deciding if a project is chosen or not is one of the simplest ways of evaluating

the project, and it is beneficial for the customer. Using this method, managers can pick the right

percentage to spend. Such as a quick turnaround period should be preferred, because it allows the

company to rebound quicker from the initial investment.

Drawbacks: Managers will disregard negative NPV when taking critical choices,

because that would not be to any benefit. This strategy does not consider the time value of

resources and will rather be based on a fixed production period, because each investment had the

same cash flow as other decisions.

ARR (Accounting rate of return):

Benefits: ARR helps the firms to allow their investment decisions. Large returns are

successful and profitable for the company. Manager decides plan ARR by selecting the most

suitable one before making any decisions. This approach acknowledges the value of accounting,

which is always encountered by management in the policy making process.

Drawbacks: Average return expectations ignore the cash flow of the portfolio, which

depends on recorded sales and also estimates using average profit (Siminica, Motoi and Dumitru,

2017). This would further impact the different things that need to be dealt with. The consequence

as well as the overall result or viability of the project is neglected in these investment appraisal

techniques.

NPV (Net Present Value):

Benefits: In most businesses, NPV is used to evaluate their commitment and assess

whether or not organization should spend on this project. Positive NPV accepted

and unfavourable NPV's rejected because it is not beneficial for the company to invest with such

a project. This technique of investment valuation takes into account the time value of the

investments and provides further opportunities before companies. It is necessary for management

to make their decisions based on the involvement in the NPV.

11

the new equipment.

Critically evaluate the benefits or drawbacks of investment appraisal technique:

Payback period:

Benefits: Deciding if a project is chosen or not is one of the simplest ways of evaluating

the project, and it is beneficial for the customer. Using this method, managers can pick the right

percentage to spend. Such as a quick turnaround period should be preferred, because it allows the

company to rebound quicker from the initial investment.

Drawbacks: Managers will disregard negative NPV when taking critical choices,

because that would not be to any benefit. This strategy does not consider the time value of

resources and will rather be based on a fixed production period, because each investment had the

same cash flow as other decisions.

ARR (Accounting rate of return):

Benefits: ARR helps the firms to allow their investment decisions. Large returns are

successful and profitable for the company. Manager decides plan ARR by selecting the most

suitable one before making any decisions. This approach acknowledges the value of accounting,

which is always encountered by management in the policy making process.

Drawbacks: Average return expectations ignore the cash flow of the portfolio, which

depends on recorded sales and also estimates using average profit (Siminica, Motoi and Dumitru,

2017). This would further impact the different things that need to be dealt with. The consequence

as well as the overall result or viability of the project is neglected in these investment appraisal

techniques.

NPV (Net Present Value):

Benefits: In most businesses, NPV is used to evaluate their commitment and assess

whether or not organization should spend on this project. Positive NPV accepted

and unfavourable NPV's rejected because it is not beneficial for the company to invest with such

a project. This technique of investment valuation takes into account the time value of the

investments and provides further opportunities before companies. It is necessary for management

to make their decisions based on the involvement in the NPV.

11

Drawbacks: This instrument may be used by administrators to determine their viability

or to compare with other proposals, but it cannot be used even because all the cash capital flows

are the same (Valencia-Cárdenas and Restrepo-Morales, 2016). If the original outlay is specific,

otherwise there is no need to test or render predictions because it does not produce correct

findings. When it shifted, the net present value affected by the discounted rate and removes

macro considerations such as inflation.

IRR (Internal Rate of Return):

Benefits: It is primarily used to describe the gains that the business earns after particular

projects have been invested, and then to take necessary additional decisions. nThis should

promote strategic decision taking to pick the most successful option for the organization.

Managers make strong-return decisions, and decide which plan helps businesses maximize their

earnings.

Drawbacks: IRR does not consider efficiencies of scale affecting performance. It is

calculated using method of hit & test, which does not produce accurate results. That also impacts

the judgment-making processes of executives. There is also no such difference in credits or

borrowings. That initiative will see differing returns due to the change in reduced cost, so

investment choices are difficult for executives to make.

CONCLUSION

It has been mentioned in the above review that management is very important to the

financial condition of the organization. It is the framework that focuses on the product, and every

aspect or function of the business. Management build policy by highlighting organization and

operational efficiency. In order to make financial decisions, the organization adopts the

investment valuation method to measure the various considerations for the evaluation. It includes

payback time, accounting rate of return, IRR, NPV etc. These are the strategies to capital

budgeting which help manager make their choices about future spending for the growth of the

business.

12

or to compare with other proposals, but it cannot be used even because all the cash capital flows

are the same (Valencia-Cárdenas and Restrepo-Morales, 2016). If the original outlay is specific,

otherwise there is no need to test or render predictions because it does not produce correct

findings. When it shifted, the net present value affected by the discounted rate and removes

macro considerations such as inflation.

IRR (Internal Rate of Return):

Benefits: It is primarily used to describe the gains that the business earns after particular

projects have been invested, and then to take necessary additional decisions. nThis should

promote strategic decision taking to pick the most successful option for the organization.

Managers make strong-return decisions, and decide which plan helps businesses maximize their

earnings.

Drawbacks: IRR does not consider efficiencies of scale affecting performance. It is

calculated using method of hit & test, which does not produce accurate results. That also impacts

the judgment-making processes of executives. There is also no such difference in credits or

borrowings. That initiative will see differing returns due to the change in reduced cost, so

investment choices are difficult for executives to make.

CONCLUSION

It has been mentioned in the above review that management is very important to the

financial condition of the organization. It is the framework that focuses on the product, and every

aspect or function of the business. Management build policy by highlighting organization and

operational efficiency. In order to make financial decisions, the organization adopts the

investment valuation method to measure the various considerations for the evaluation. It includes

payback time, accounting rate of return, IRR, NPV etc. These are the strategies to capital

budgeting which help manager make their choices about future spending for the growth of the

business.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.