APC308 Financial Management: Valuation and Investment Analysis

VerifiedAdded on 2023/01/12

|16

|3075

|61

Report

AI Summary

This report provides a comprehensive analysis of financial management principles, focusing on valuation techniques and investment appraisal methods. It begins with an introduction to financial management, emphasizing its role in achieving business goals. The report then delves into the intricacies of mergers and takeovers, exploring valuation techniques such as the Price Earnings Ratio, Dividend Valuation Method, and Discounted Cash Flow, critically discussing their benefits and limitations. The analysis extends to investment appraisal techniques, including Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR), providing detailed calculations and interpretations for a case study involving Lovewell Limited. The report concludes by summarizing the findings and emphasizing the importance of considering various factors when making financial decisions, offering valuable insights for financial management students and professionals.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................4

QUESTION 2.................................................................................................................................................4

Mergers and takeovers............................................................................................................................4

b. Critically discuss the problems related with the valuation techniques and provide recommendations

.................................................................................................................................................................6

QUESTION 3.................................................................................................................................................7

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV and IRR

.................................................................................................................................................................7

b. Limitations and benefits of different investment appraisal techniques............................................13

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................16

INTRODUCTION...........................................................................................................................................4

QUESTION 2.................................................................................................................................................4

Mergers and takeovers............................................................................................................................4

b. Critically discuss the problems related with the valuation techniques and provide recommendations

.................................................................................................................................................................6

QUESTION 3.................................................................................................................................................7

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV and IRR

.................................................................................................................................................................7

b. Limitations and benefits of different investment appraisal techniques............................................13

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management is the method of having to take care of all funding associated

operations that an entity conducts in order to achieve defined business goals. It's

concentrated primarily on applying operational concepts to all the investor's numerical resources.

Potential budget criteria for activities may be calculated with both the assistance of it. To ensure

that all the processes connected with it have been carried out consistently, it is very essential for

supervisors to thoroughly review final statements so that decisions can be made for the potential.

Questions two and three are chosen to complete this Analysis (Antonopoulos and Hall, 2018).

This report will address a number of subjects like market valuation of other takeover

organisation, possible changes in corporate and short-term impact on Aztech Company. In

addition, measurements are also performed in this plan with the aid of various portfolio

evaluation methods together with their benefits and drawbacks.

QUESTION 2

Mergers and takeovers

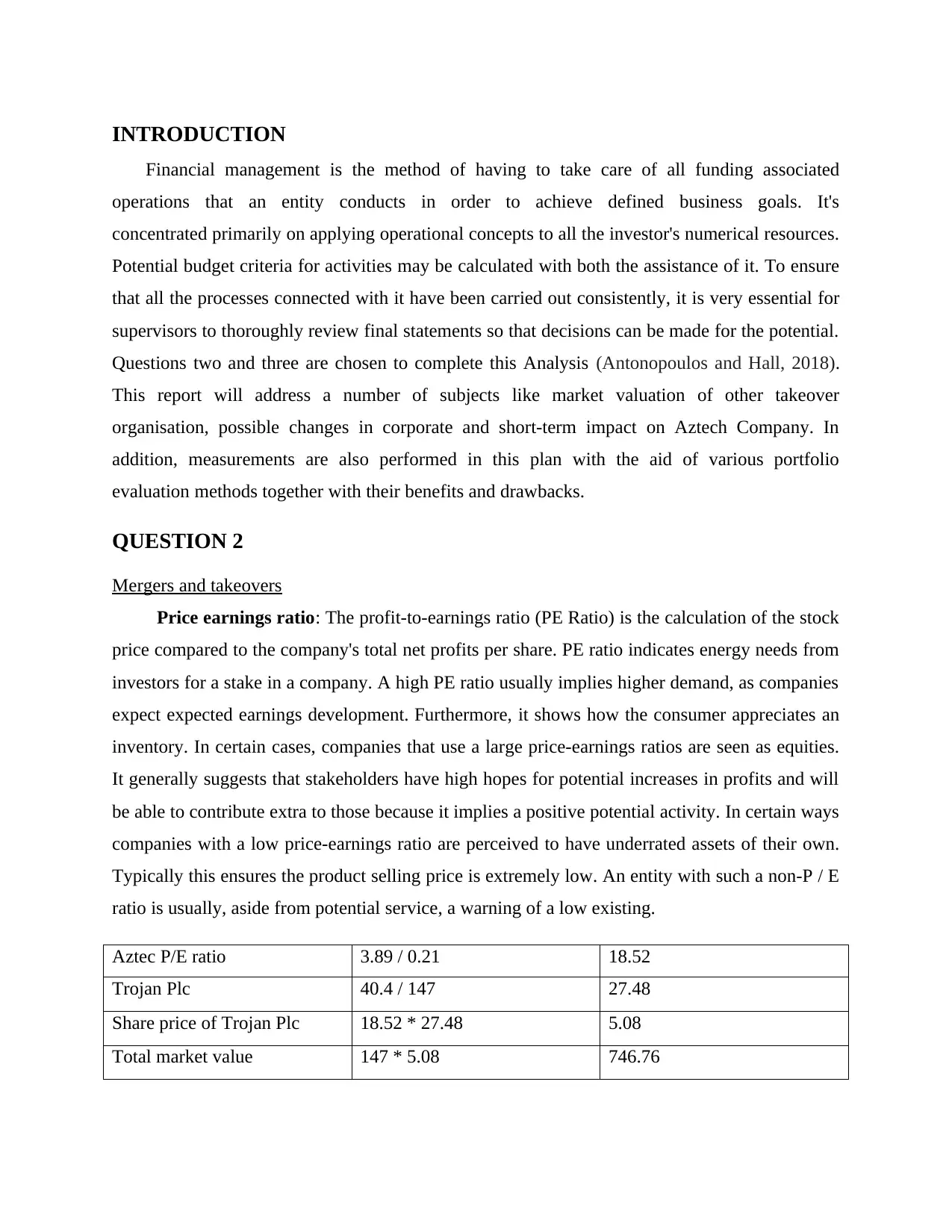

Price earnings ratio: The profit-to-earnings ratio (PE Ratio) is the calculation of the stock

price compared to the company's total net profits per share. PE ratio indicates energy needs from

investors for a stake in a company. A high PE ratio usually implies higher demand, as companies

expect expected earnings development. Furthermore, it shows how the consumer appreciates an

inventory. In certain cases, companies that use a large price-earnings ratios are seen as equities.

It generally suggests that stakeholders have high hopes for potential increases in profits and will

be able to contribute extra to those because it implies a positive potential activity. In certain ways

companies with a low price-earnings ratio are perceived to have underrated assets of their own.

Typically this ensures the product selling price is extremely low. An entity with such a non-P / E

ratio is usually, aside from potential service, a warning of a low existing.

Aztec P/E ratio 3.89 / 0.21 18.52

Trojan Plc 40.4 / 147 27.48

Share price of Trojan Plc 18.52 * 27.48 5.08

Total market value 147 * 5.08 746.76

Financial management is the method of having to take care of all funding associated

operations that an entity conducts in order to achieve defined business goals. It's

concentrated primarily on applying operational concepts to all the investor's numerical resources.

Potential budget criteria for activities may be calculated with both the assistance of it. To ensure

that all the processes connected with it have been carried out consistently, it is very essential for

supervisors to thoroughly review final statements so that decisions can be made for the potential.

Questions two and three are chosen to complete this Analysis (Antonopoulos and Hall, 2018).

This report will address a number of subjects like market valuation of other takeover

organisation, possible changes in corporate and short-term impact on Aztech Company. In

addition, measurements are also performed in this plan with the aid of various portfolio

evaluation methods together with their benefits and drawbacks.

QUESTION 2

Mergers and takeovers

Price earnings ratio: The profit-to-earnings ratio (PE Ratio) is the calculation of the stock

price compared to the company's total net profits per share. PE ratio indicates energy needs from

investors for a stake in a company. A high PE ratio usually implies higher demand, as companies

expect expected earnings development. Furthermore, it shows how the consumer appreciates an

inventory. In certain cases, companies that use a large price-earnings ratios are seen as equities.

It generally suggests that stakeholders have high hopes for potential increases in profits and will

be able to contribute extra to those because it implies a positive potential activity. In certain ways

companies with a low price-earnings ratio are perceived to have underrated assets of their own.

Typically this ensures the product selling price is extremely low. An entity with such a non-P / E

ratio is usually, aside from potential service, a warning of a low existing.

Aztec P/E ratio 3.89 / 0.21 18.52

Trojan Plc 40.4 / 147 27.48

Share price of Trojan Plc 18.52 * 27.48 5.08

Total market value 147 * 5.08 746.76

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

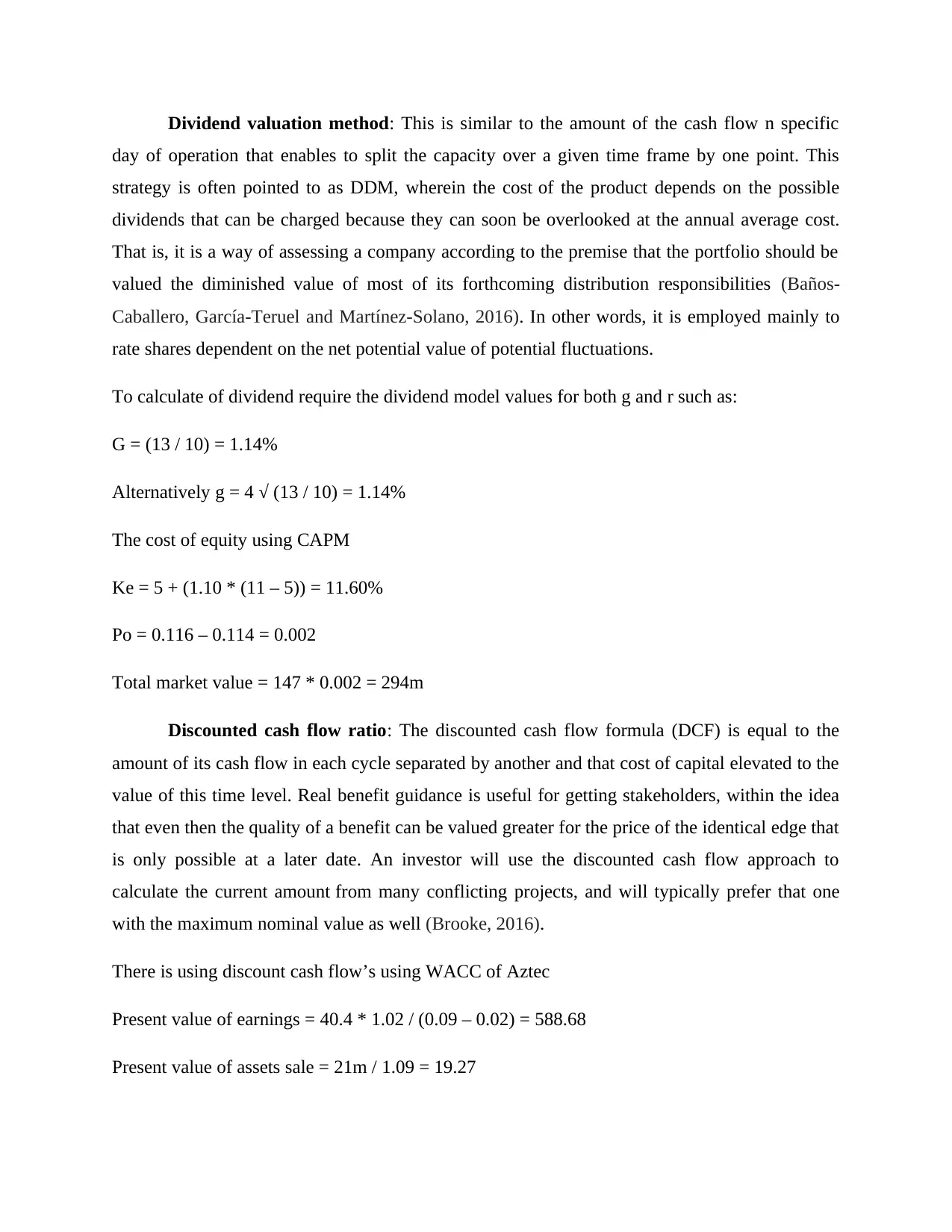

Dividend valuation method: This is similar to the amount of the cash flow n specific

day of operation that enables to split the capacity over a given time frame by one point. This

strategy is often pointed to as DDM, wherein the cost of the product depends on the possible

dividends that can be charged because they can soon be overlooked at the annual average cost.

That is, it is a way of assessing a company according to the premise that the portfolio should be

valued the diminished value of most of its forthcoming distribution responsibilities (Baños-

Caballero, García-Teruel and Martínez-Solano, 2016). In other words, it is employed mainly to

rate shares dependent on the net potential value of potential fluctuations.

To calculate of dividend require the dividend model values for both g and r such as:

G = (13 / 10) = 1.14%

Alternatively g = 4 √ (13 / 10) = 1.14%

The cost of equity using CAPM

Ke = 5 + (1.10 * (11 – 5)) = 11.60%

Po = 0.116 – 0.114 = 0.002

Total market value = 147 * 0.002 = 294m

Discounted cash flow ratio: The discounted cash flow formula (DCF) is equal to the

amount of its cash flow in each cycle separated by another and that cost of capital elevated to the

value of this time level. Real benefit guidance is useful for getting stakeholders, within the idea

that even then the quality of a benefit can be valued greater for the price of the identical edge that

is only possible at a later date. An investor will use the discounted cash flow approach to

calculate the current amount from many conflicting projects, and will typically prefer that one

with the maximum nominal value as well (Brooke, 2016).

There is using discount cash flow’s using WACC of Aztec

Present value of earnings = 40.4 * 1.02 / (0.09 – 0.02) = 588.68

Present value of assets sale = 21m / 1.09 = 19.27

day of operation that enables to split the capacity over a given time frame by one point. This

strategy is often pointed to as DDM, wherein the cost of the product depends on the possible

dividends that can be charged because they can soon be overlooked at the annual average cost.

That is, it is a way of assessing a company according to the premise that the portfolio should be

valued the diminished value of most of its forthcoming distribution responsibilities (Baños-

Caballero, García-Teruel and Martínez-Solano, 2016). In other words, it is employed mainly to

rate shares dependent on the net potential value of potential fluctuations.

To calculate of dividend require the dividend model values for both g and r such as:

G = (13 / 10) = 1.14%

Alternatively g = 4 √ (13 / 10) = 1.14%

The cost of equity using CAPM

Ke = 5 + (1.10 * (11 – 5)) = 11.60%

Po = 0.116 – 0.114 = 0.002

Total market value = 147 * 0.002 = 294m

Discounted cash flow ratio: The discounted cash flow formula (DCF) is equal to the

amount of its cash flow in each cycle separated by another and that cost of capital elevated to the

value of this time level. Real benefit guidance is useful for getting stakeholders, within the idea

that even then the quality of a benefit can be valued greater for the price of the identical edge that

is only possible at a later date. An investor will use the discounted cash flow approach to

calculate the current amount from many conflicting projects, and will typically prefer that one

with the maximum nominal value as well (Brooke, 2016).

There is using discount cash flow’s using WACC of Aztec

Present value of earnings = 40.4 * 1.02 / (0.09 – 0.02) = 588.68

Present value of assets sale = 21m / 1.09 = 19.27

Present value of synergy = 5 / 0.09 = 55.56

Total present value of Trojan Plc = 588.68 + 19.27 + 55.56 = 663.51

b. Critically discuss the problems related with the valuation techniques and provide

recommendations

Price earnings ratio

Benefits:

1. Assess growth potential: PE ratios enable stakeholders assess the potential growth of the

enterprise until they participate. The ratios indicate businesses that can be impacted by drastic

price change. High PE contributes to the company's selloff while low PE demonstrates the

organisation's continuous production.

2. Growth estimates: P/E tests a future growth potential by considering the current business

circumstances and contrasting it to past results. This also dictates what the investors are created

for business.

3. Comparison: PE will be used for comparing and valuing holdings of corporations with each

other rendering it a valuable quantitative device. This includes the organizational background

throughout a particular market area (Danes, Garbow and Jokela, 2016).

Limitations

1. Bad decisions: This can result in poor choices impacting the company to meet the planned

income.

2. Non appropriate for determining damages: Loss-making firms may not use PE ratio because it

cannot calculate liabilities at the early days of overall business.

3. Historical earnings: P/E expectations are depended on current records, so it is challenging to

forecast such profits as they can not accurately estimate profits.

Dividend valuation model

Total present value of Trojan Plc = 588.68 + 19.27 + 55.56 = 663.51

b. Critically discuss the problems related with the valuation techniques and provide

recommendations

Price earnings ratio

Benefits:

1. Assess growth potential: PE ratios enable stakeholders assess the potential growth of the

enterprise until they participate. The ratios indicate businesses that can be impacted by drastic

price change. High PE contributes to the company's selloff while low PE demonstrates the

organisation's continuous production.

2. Growth estimates: P/E tests a future growth potential by considering the current business

circumstances and contrasting it to past results. This also dictates what the investors are created

for business.

3. Comparison: PE will be used for comparing and valuing holdings of corporations with each

other rendering it a valuable quantitative device. This includes the organizational background

throughout a particular market area (Danes, Garbow and Jokela, 2016).

Limitations

1. Bad decisions: This can result in poor choices impacting the company to meet the planned

income.

2. Non appropriate for determining damages: Loss-making firms may not use PE ratio because it

cannot calculate liabilities at the early days of overall business.

3. Historical earnings: P/E expectations are depended on current records, so it is challenging to

forecast such profits as they can not accurately estimate profits.

Dividend valuation model

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefits: The model does not try to assume wild predictions in regard of inventory potential

increment, as the rate of dividend improvement cannot be higher than the rate of return for the

methodology to work. All it does is make a decision based about what the payout is being

charged through currently as well as on the expectation that throughout the forecast the dividends

will rise at an un-outrageous amount. If the inherent investment in the shape of investment

arrives back additional capital well that's just a side product of all of that.

Limitations: The main drawback of this model that for this require large number of assumptions

that cannot possible. A high level of details may outcomes in overconfidence and looks at the

organisation valuation of competitors. It is most challenging for the weighted average cost of

capital.

Discounted cash flow

Benefits: It is less affected by unpredictable external influences, as it is an in on itself-looking

mechanism that focuses too much on the company's core assumptions and strong value driver

forecasts (Dwiastanti, 2017). Unlike the proportional assessment approach, financial procedures

and expectations are less impacted as it focuses on producing cash flow.

Limitations: The estimation reliability calculated and uses the DCF approach depends heavily on

the consistency of the calculations about Free Cash Flows, Target Price, and Rate of return. The

extracted price is extremely vulnerable to the references provided, which results in radically

different appraisals by specific observers depending on the subjective view of the business's

compensatory picks.

QUESTION 3

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV

and IRR

Investment evaluation can be described as a mix of numerous kinds of approaches

applied by companies to evaluate the effectiveness of the selection of alternatives available for

them in order to make potential investment (Hashim and Piatti-Fünfkirchen, 2018). The main

aim is to assess the feasibility of the planned proposal or the alternatives to allocate resources in

the prospect chosen by a client. Lovewell Limited is thinking of buying a new computer to

increment, as the rate of dividend improvement cannot be higher than the rate of return for the

methodology to work. All it does is make a decision based about what the payout is being

charged through currently as well as on the expectation that throughout the forecast the dividends

will rise at an un-outrageous amount. If the inherent investment in the shape of investment

arrives back additional capital well that's just a side product of all of that.

Limitations: The main drawback of this model that for this require large number of assumptions

that cannot possible. A high level of details may outcomes in overconfidence and looks at the

organisation valuation of competitors. It is most challenging for the weighted average cost of

capital.

Discounted cash flow

Benefits: It is less affected by unpredictable external influences, as it is an in on itself-looking

mechanism that focuses too much on the company's core assumptions and strong value driver

forecasts (Dwiastanti, 2017). Unlike the proportional assessment approach, financial procedures

and expectations are less impacted as it focuses on producing cash flow.

Limitations: The estimation reliability calculated and uses the DCF approach depends heavily on

the consistency of the calculations about Free Cash Flows, Target Price, and Rate of return. The

extracted price is extremely vulnerable to the references provided, which results in radically

different appraisals by specific observers depending on the subjective view of the business's

compensatory picks.

QUESTION 3

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV

and IRR

Investment evaluation can be described as a mix of numerous kinds of approaches

applied by companies to evaluate the effectiveness of the selection of alternatives available for

them in order to make potential investment (Hashim and Piatti-Fünfkirchen, 2018). The main

aim is to assess the feasibility of the planned proposal or the alternatives to allocate resources in

the prospect chosen by a client. Lovewell Limited is thinking of buying a new computer to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enhance company efficiency. The corporation may use investment evaluation for the intention of

assessing whether it would be able to support the business or not specific strategies. Each of

these definitions is as follows:

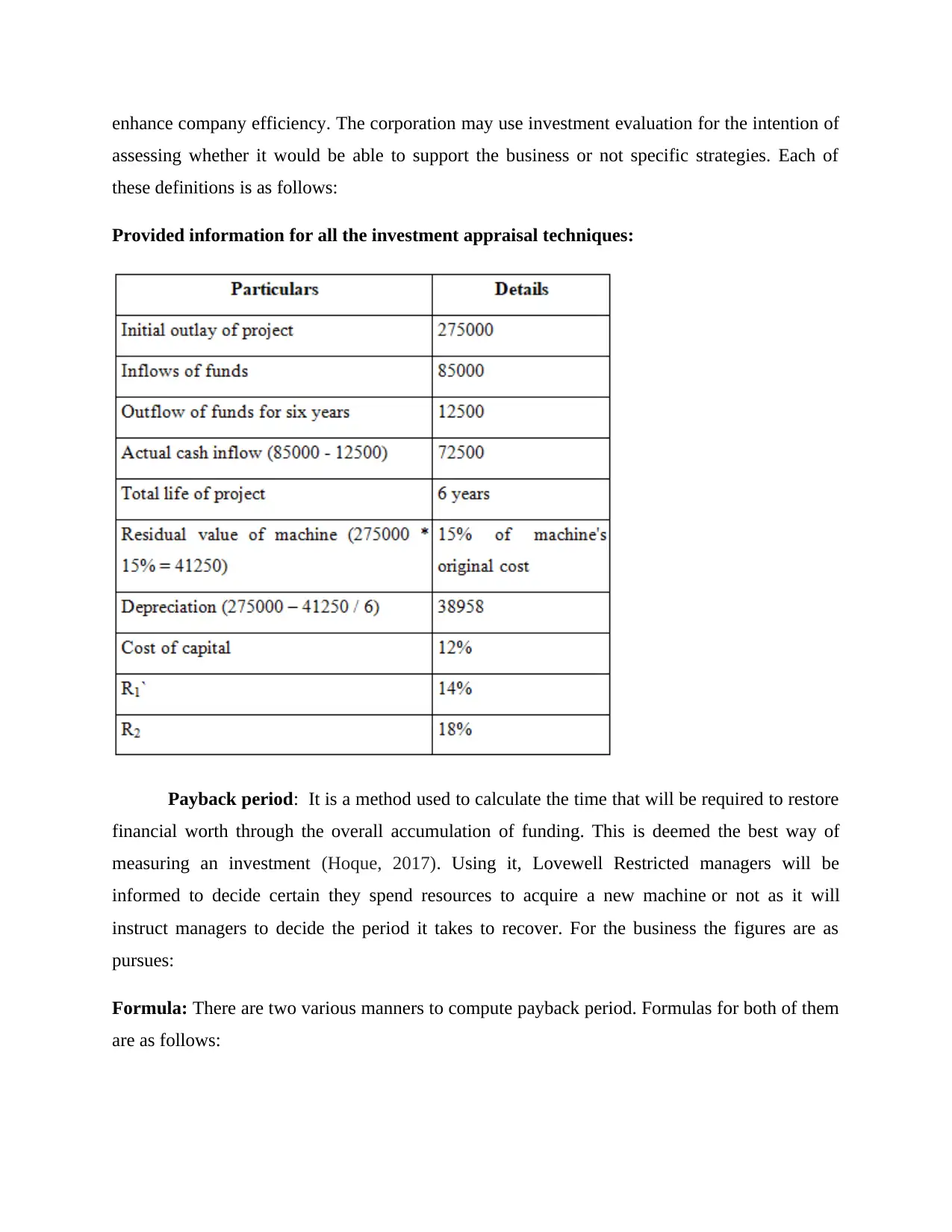

Provided information for all the investment appraisal techniques:

Payback period: It is a method used to calculate the time that will be required to restore

financial worth through the overall accumulation of funding. This is deemed the best way of

measuring an investment (Hoque, 2017). Using it, Lovewell Restricted managers will be

informed to decide certain they spend resources to acquire a new machine or not as it will

instruct managers to decide the period it takes to recover. For the business the figures are as

pursues:

Formula: There are two various manners to compute payback period. Formulas for both of them

are as follows:

assessing whether it would be able to support the business or not specific strategies. Each of

these definitions is as follows:

Provided information for all the investment appraisal techniques:

Payback period: It is a method used to calculate the time that will be required to restore

financial worth through the overall accumulation of funding. This is deemed the best way of

measuring an investment (Hoque, 2017). Using it, Lovewell Restricted managers will be

informed to decide certain they spend resources to acquire a new machine or not as it will

instruct managers to decide the period it takes to recover. For the business the figures are as

pursues:

Formula: There are two various manners to compute payback period. Formulas for both of them

are as follows:

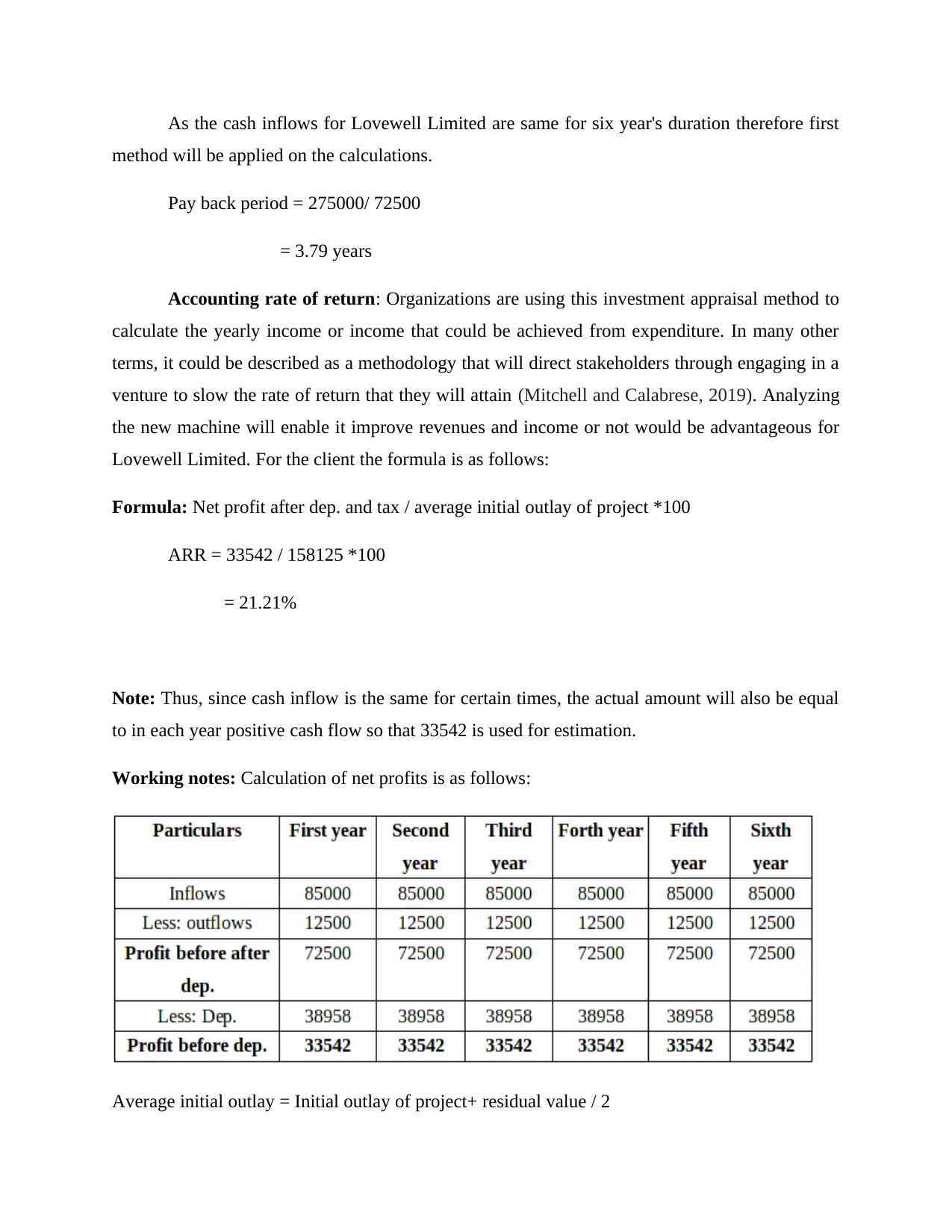

As the cash inflows for Lovewell Limited are same for six year's duration therefore first

method will be applied on the calculations.

Pay back period = 275000/ 72500

= 3.79 years

Accounting rate of return: Organizations are using this investment appraisal method to

calculate the yearly income or income that could be achieved from expenditure. In many other

terms, it could be described as a methodology that will direct stakeholders through engaging in a

venture to slow the rate of return that they will attain (Mitchell and Calabrese, 2019). Analyzing

the new machine will enable it improve revenues and income or not would be advantageous for

Lovewell Limited. For the client the formula is as follows:

Formula: Net profit after dep. and tax / average initial outlay of project *100

ARR = 33542 / 158125 *100

= 21.21%

Note: Thus, since cash inflow is the same for certain times, the actual amount will also be equal

to in each year positive cash flow so that 33542 is used for estimation.

Working notes: Calculation of net profits is as follows:

Average initial outlay = Initial outlay of project+ residual value / 2

method will be applied on the calculations.

Pay back period = 275000/ 72500

= 3.79 years

Accounting rate of return: Organizations are using this investment appraisal method to

calculate the yearly income or income that could be achieved from expenditure. In many other

terms, it could be described as a methodology that will direct stakeholders through engaging in a

venture to slow the rate of return that they will attain (Mitchell and Calabrese, 2019). Analyzing

the new machine will enable it improve revenues and income or not would be advantageous for

Lovewell Limited. For the client the formula is as follows:

Formula: Net profit after dep. and tax / average initial outlay of project *100

ARR = 33542 / 158125 *100

= 21.21%

Note: Thus, since cash inflow is the same for certain times, the actual amount will also be equal

to in each year positive cash flow so that 33542 is used for estimation.

Working notes: Calculation of net profits is as follows:

Average initial outlay = Initial outlay of project+ residual value / 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 275000 + 41250 / 2

= 158125

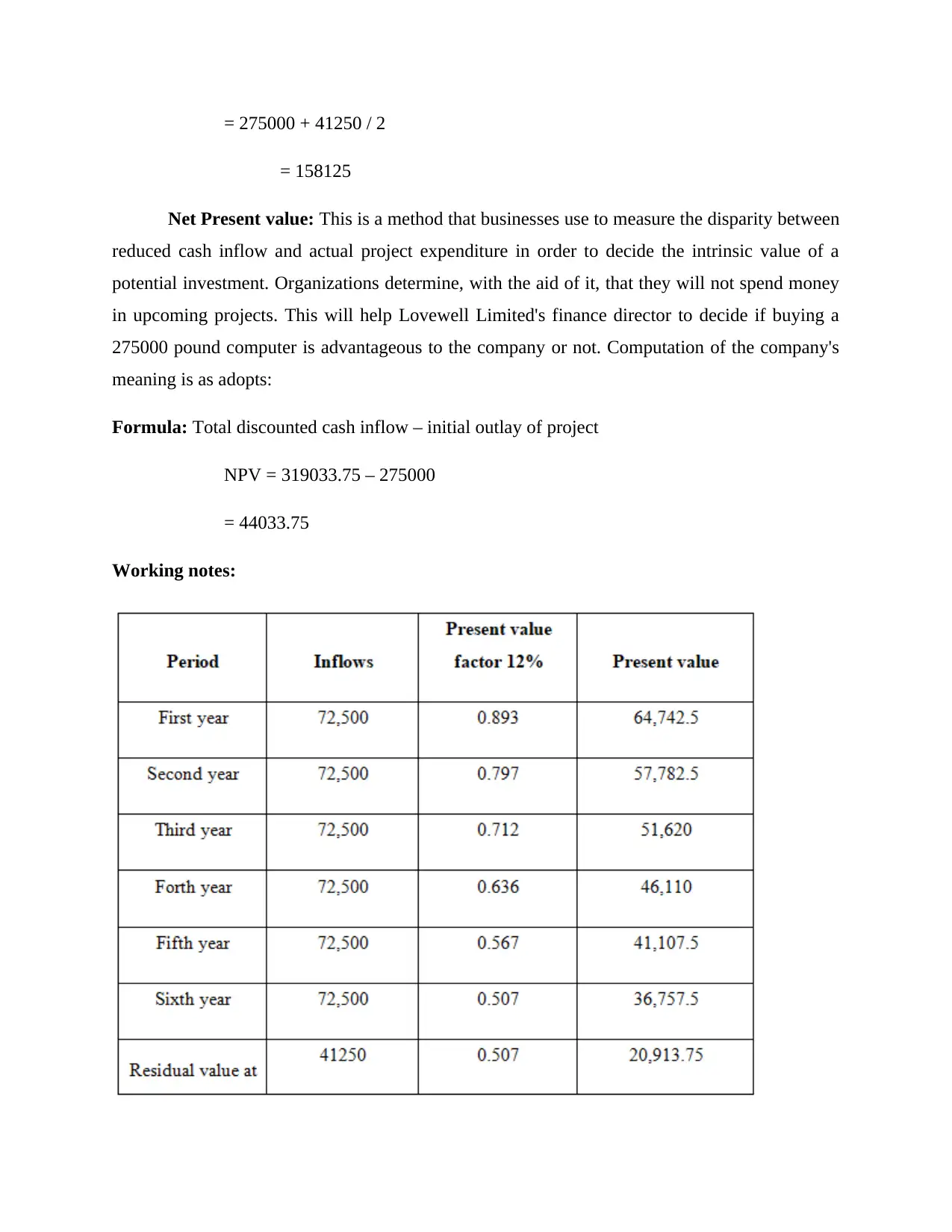

Net Present value: This is a method that businesses use to measure the disparity between

reduced cash inflow and actual project expenditure in order to decide the intrinsic value of a

potential investment. Organizations determine, with the aid of it, that they will not spend money

in upcoming projects. This will help Lovewell Limited's finance director to decide if buying a

275000 pound computer is advantageous to the company or not. Computation of the company's

meaning is as adopts:

Formula: Total discounted cash inflow – initial outlay of project

NPV = 319033.75 – 275000

= 44033.75

Working notes:

= 158125

Net Present value: This is a method that businesses use to measure the disparity between

reduced cash inflow and actual project expenditure in order to decide the intrinsic value of a

potential investment. Organizations determine, with the aid of it, that they will not spend money

in upcoming projects. This will help Lovewell Limited's finance director to decide if buying a

275000 pound computer is advantageous to the company or not. Computation of the company's

meaning is as adopts:

Formula: Total discounted cash inflow – initial outlay of project

NPV = 319033.75 – 275000

= 44033.75

Working notes:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

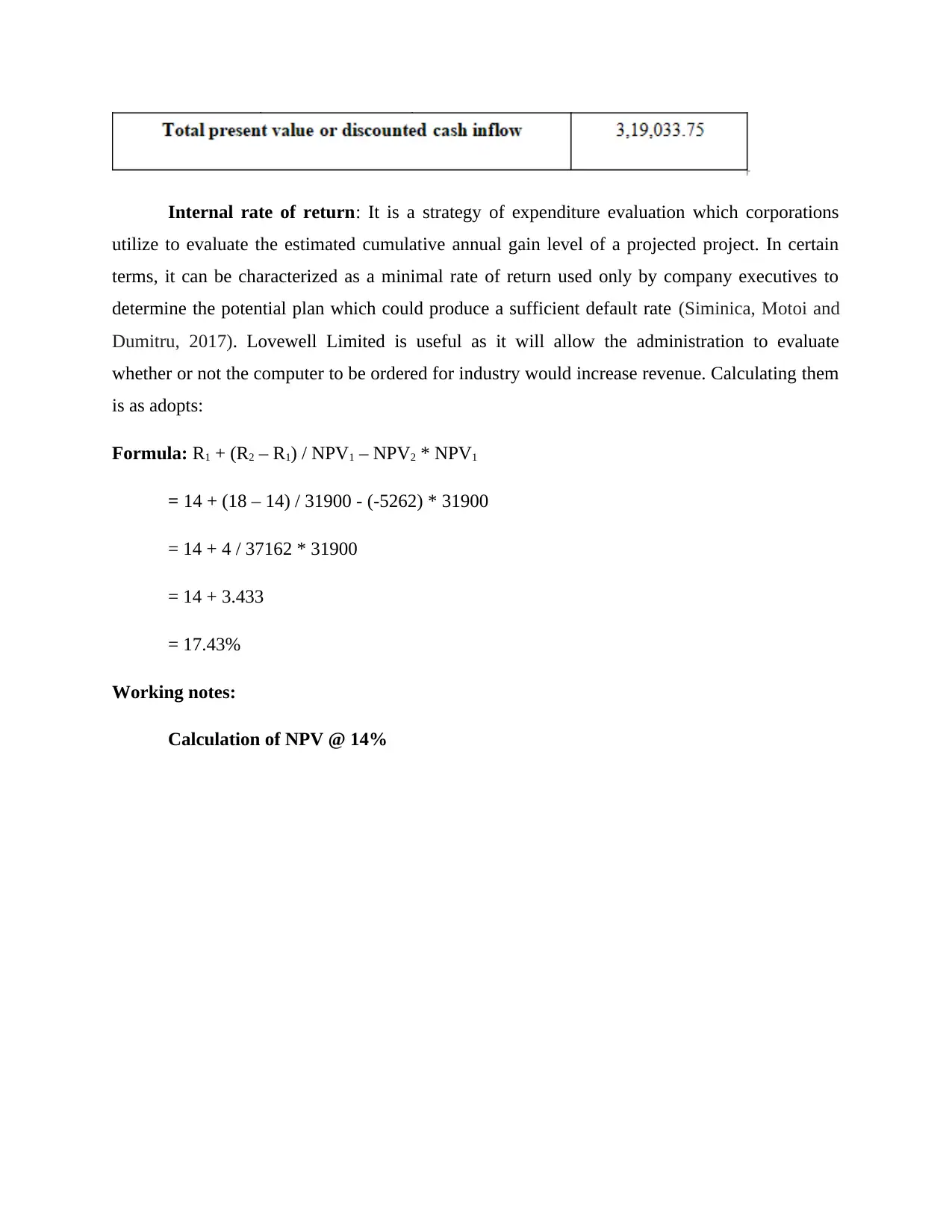

Internal rate of return: It is a strategy of expenditure evaluation which corporations

utilize to evaluate the estimated cumulative annual gain level of a projected project. In certain

terms, it can be characterized as a minimal rate of return used only by company executives to

determine the potential plan which could produce a sufficient default rate (Siminica, Motoi and

Dumitru, 2017). Lovewell Limited is useful as it will allow the administration to evaluate

whether or not the computer to be ordered for industry would increase revenue. Calculating them

is as adopts:

Formula: R1 + (R2 – R1) / NPV1 – NPV2 * NPV1

= 14 + (18 – 14) / 31900 - (-5262) * 31900

= 14 + 4 / 37162 * 31900

= 14 + 3.433

= 17.43%

Working notes:

Calculation of NPV @ 14%

utilize to evaluate the estimated cumulative annual gain level of a projected project. In certain

terms, it can be characterized as a minimal rate of return used only by company executives to

determine the potential plan which could produce a sufficient default rate (Siminica, Motoi and

Dumitru, 2017). Lovewell Limited is useful as it will allow the administration to evaluate

whether or not the computer to be ordered for industry would increase revenue. Calculating them

is as adopts:

Formula: R1 + (R2 – R1) / NPV1 – NPV2 * NPV1

= 14 + (18 – 14) / 31900 - (-5262) * 31900

= 14 + 4 / 37162 * 31900

= 14 + 3.433

= 17.43%

Working notes:

Calculation of NPV @ 14%

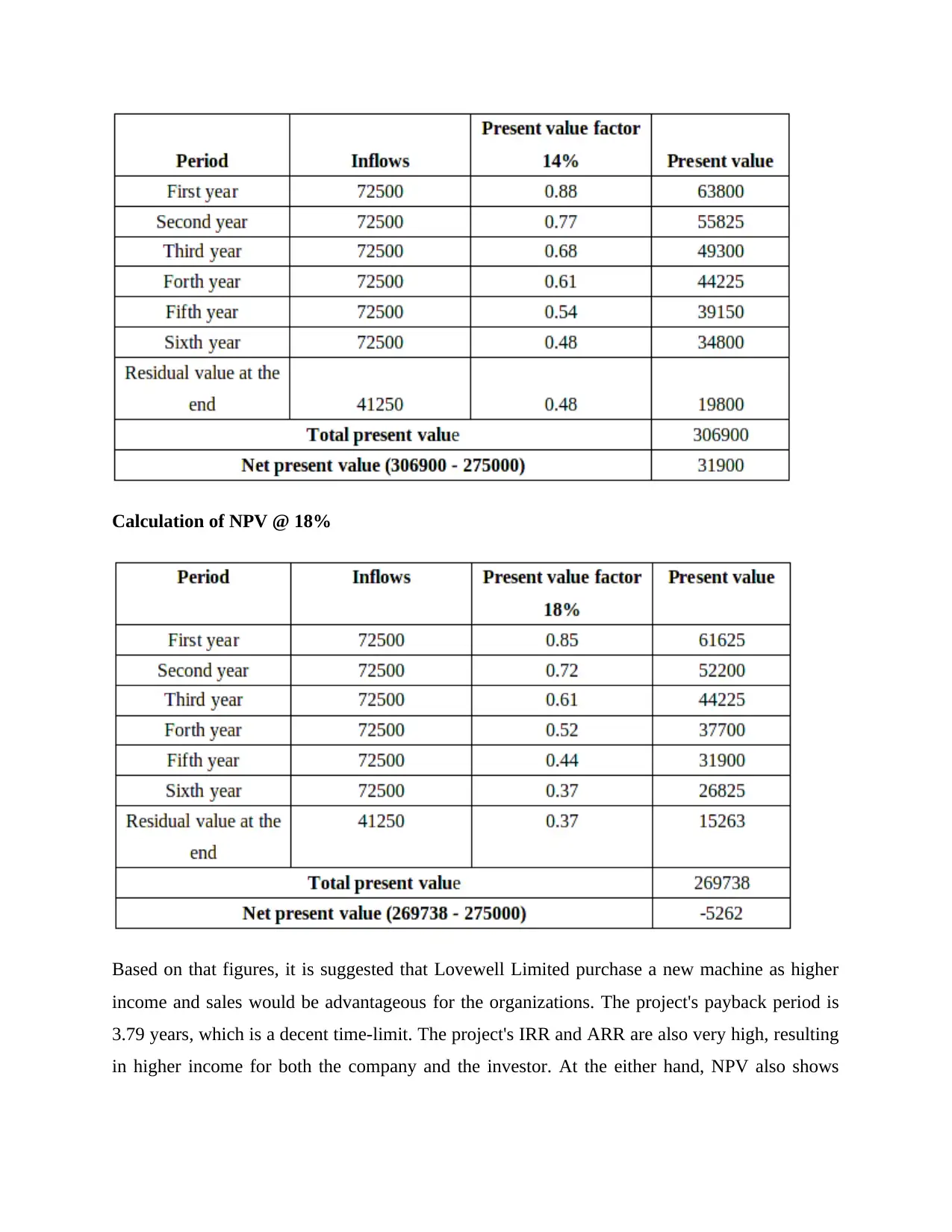

Calculation of NPV @ 18%

Based on that figures, it is suggested that Lovewell Limited purchase a new machine as higher

income and sales would be advantageous for the organizations. The project's payback period is

3.79 years, which is a decent time-limit. The project's IRR and ARR are also very high, resulting

in higher income for both the company and the investor. At the either hand, NPV also shows

Based on that figures, it is suggested that Lovewell Limited purchase a new machine as higher

income and sales would be advantageous for the organizations. The project's payback period is

3.79 years, which is a decent time-limit. The project's IRR and ARR are also very high, resulting

in higher income for both the company and the investor. At the either hand, NPV also shows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.