Detailed Project: Valuation, Hedging, and Option Strategies in Finance

VerifiedAdded on 2020/12/18

|22

|4401

|91

Project

AI Summary

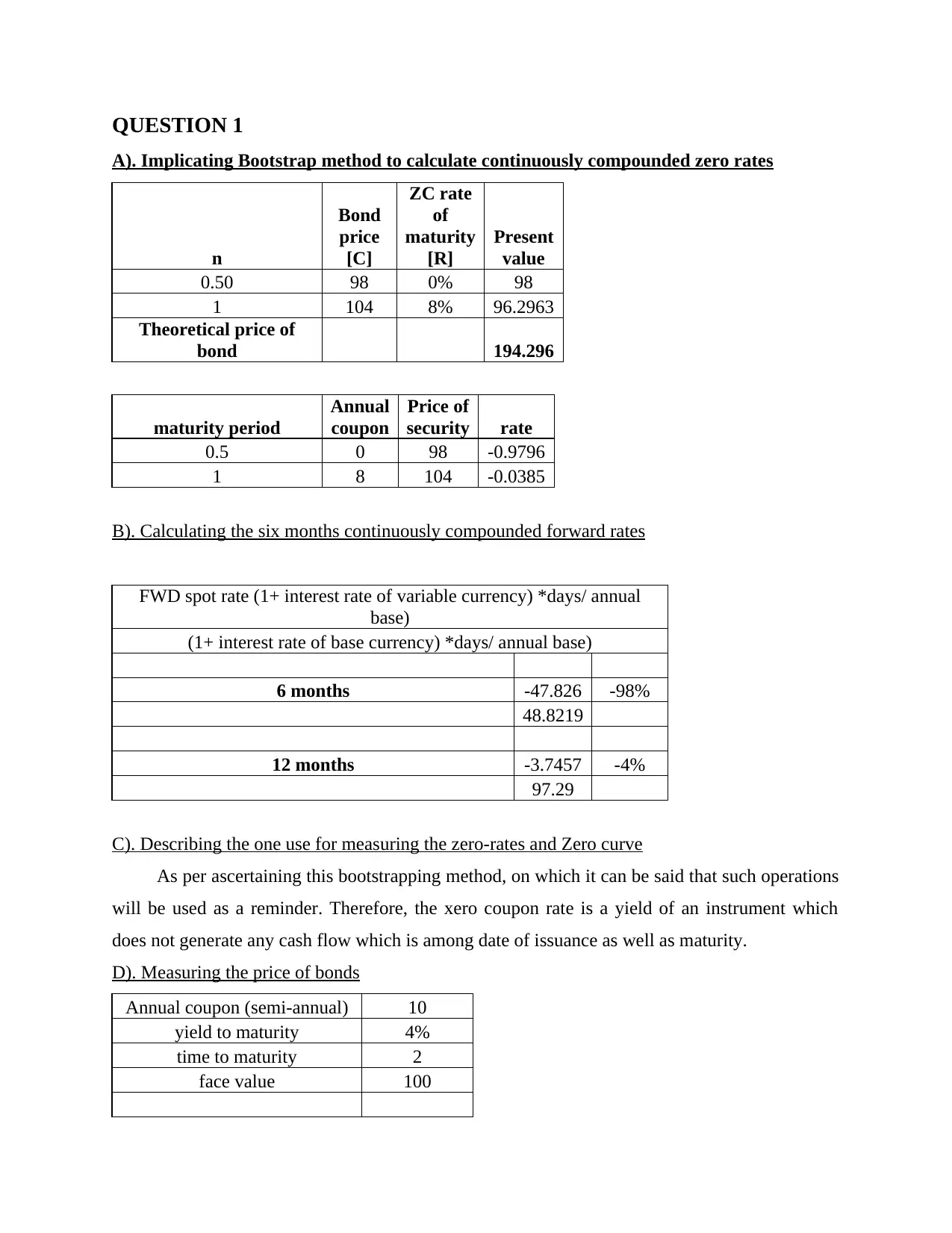

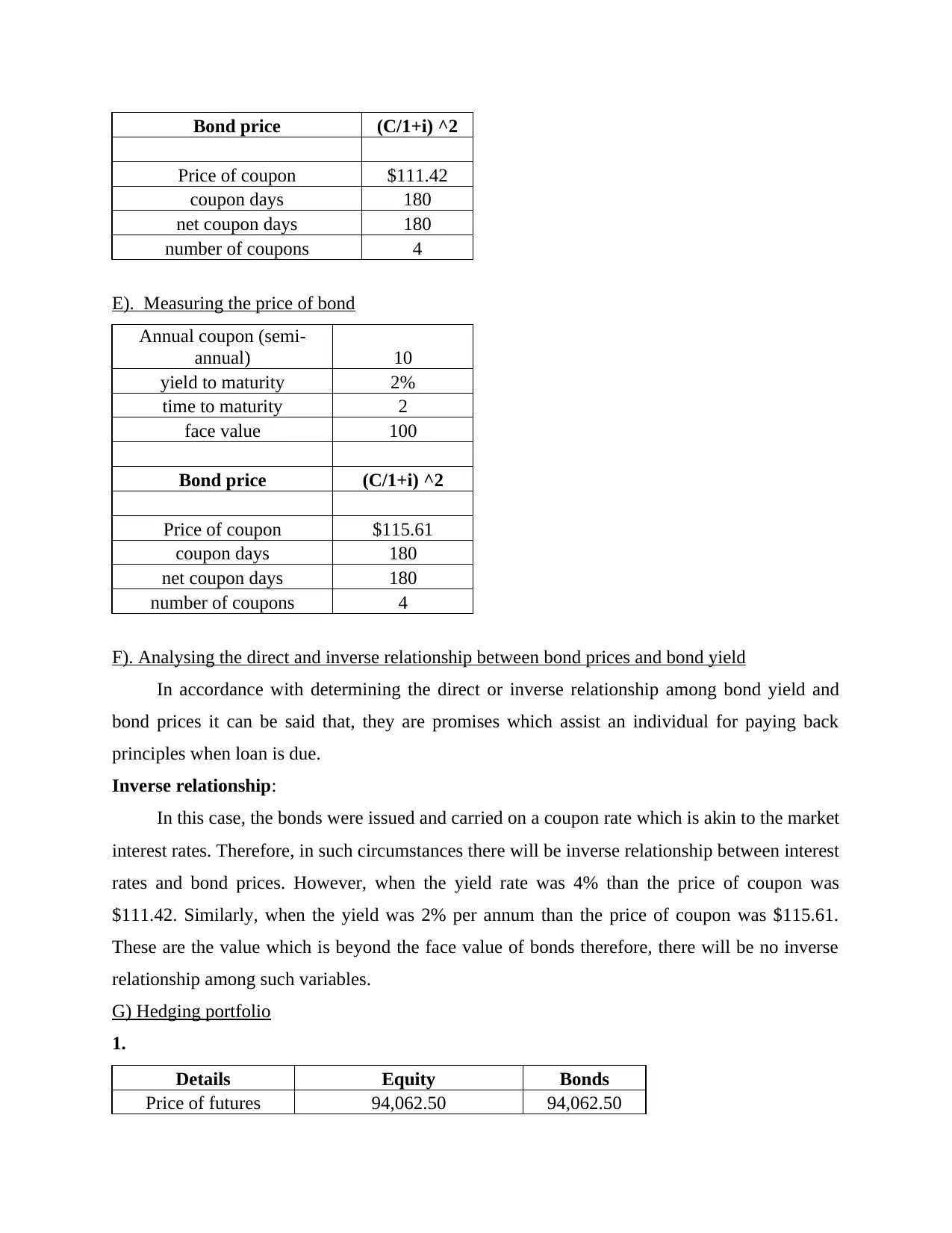

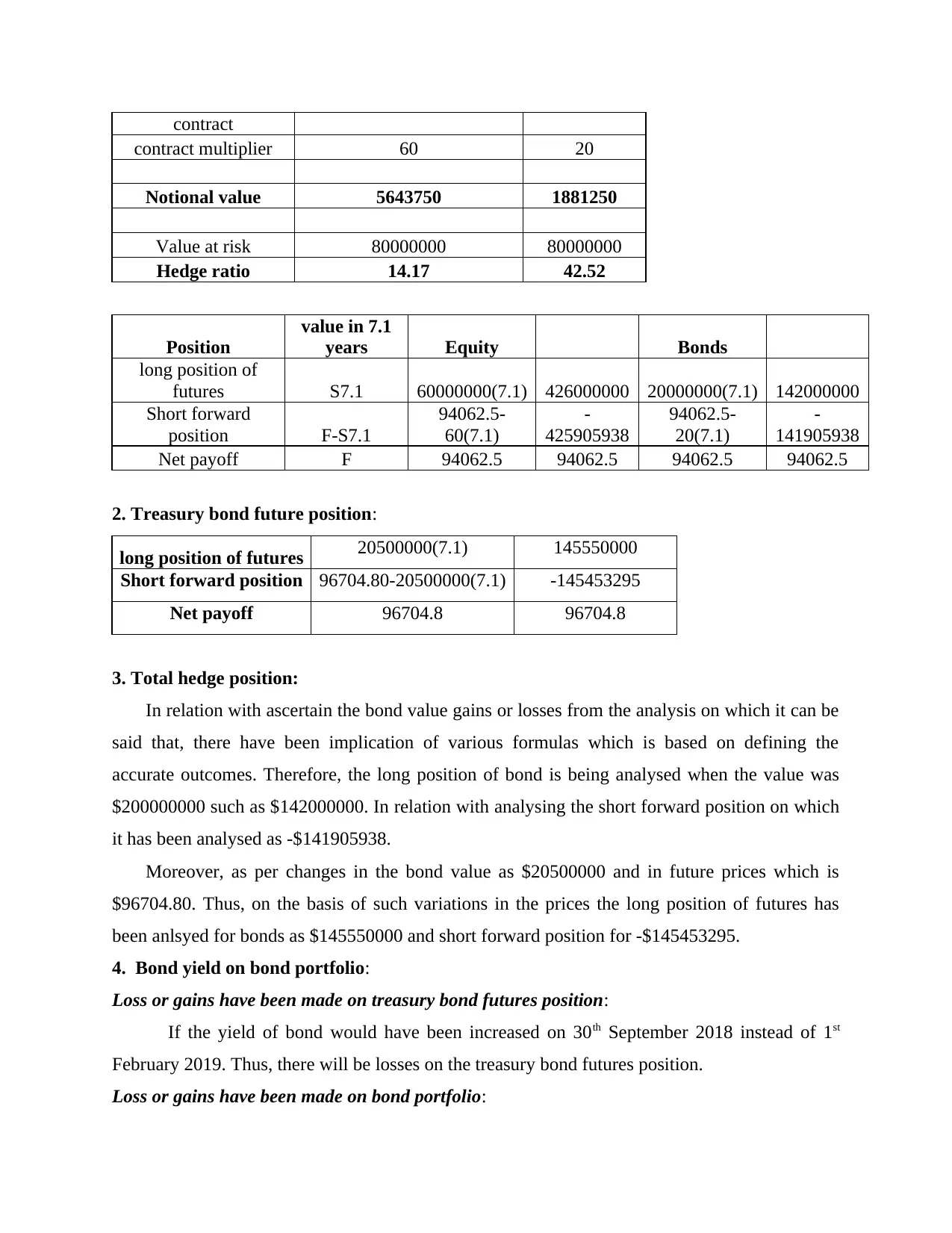

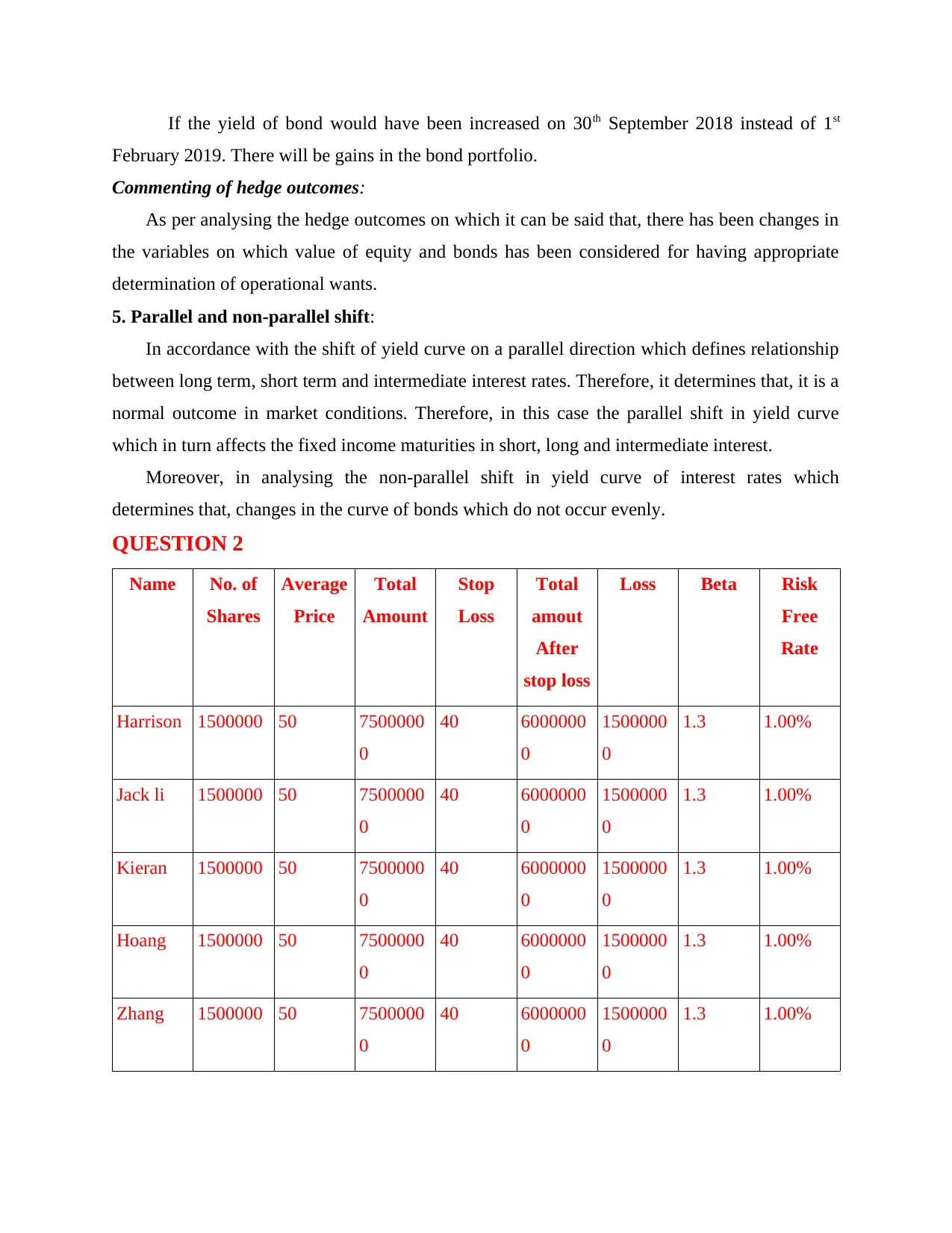

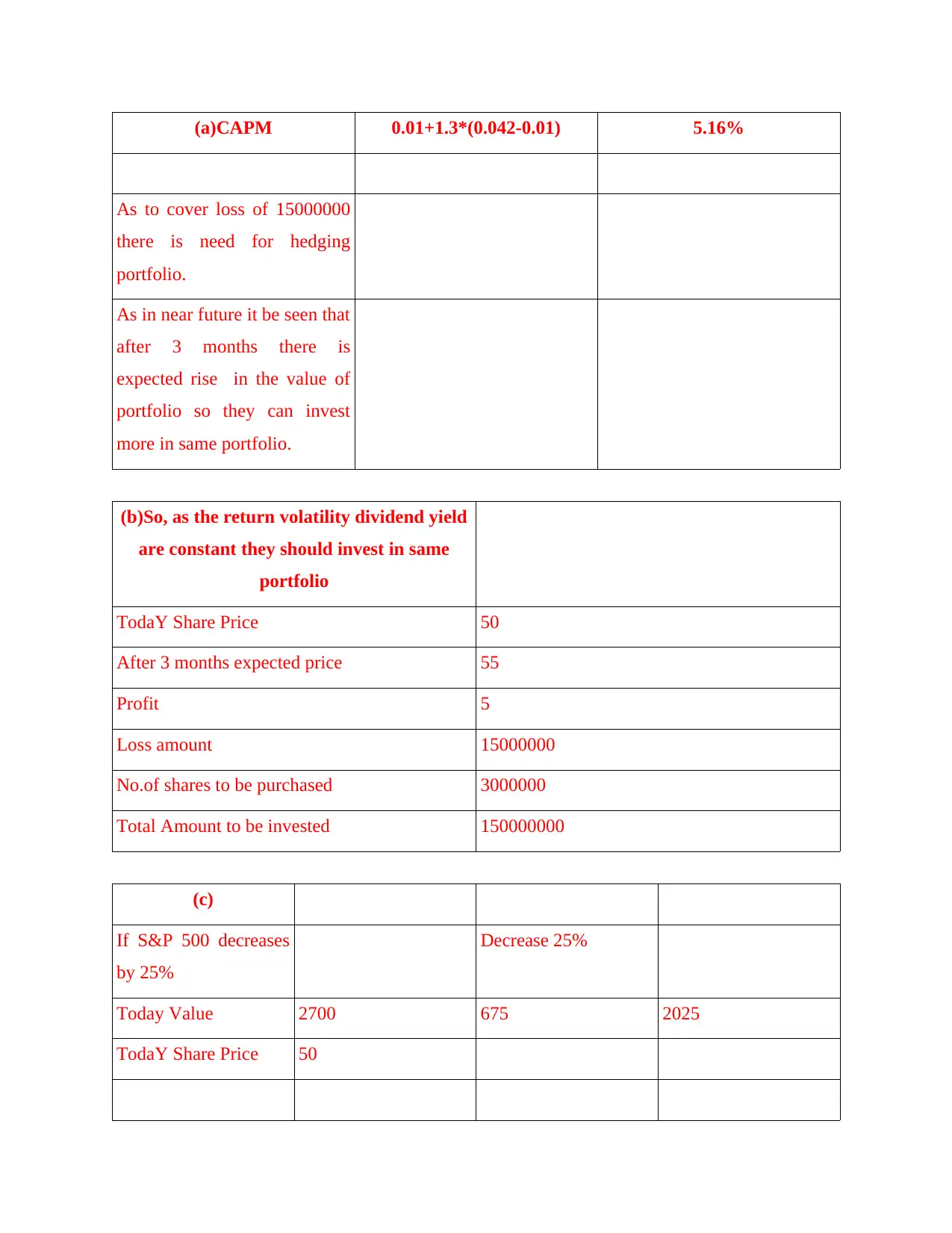

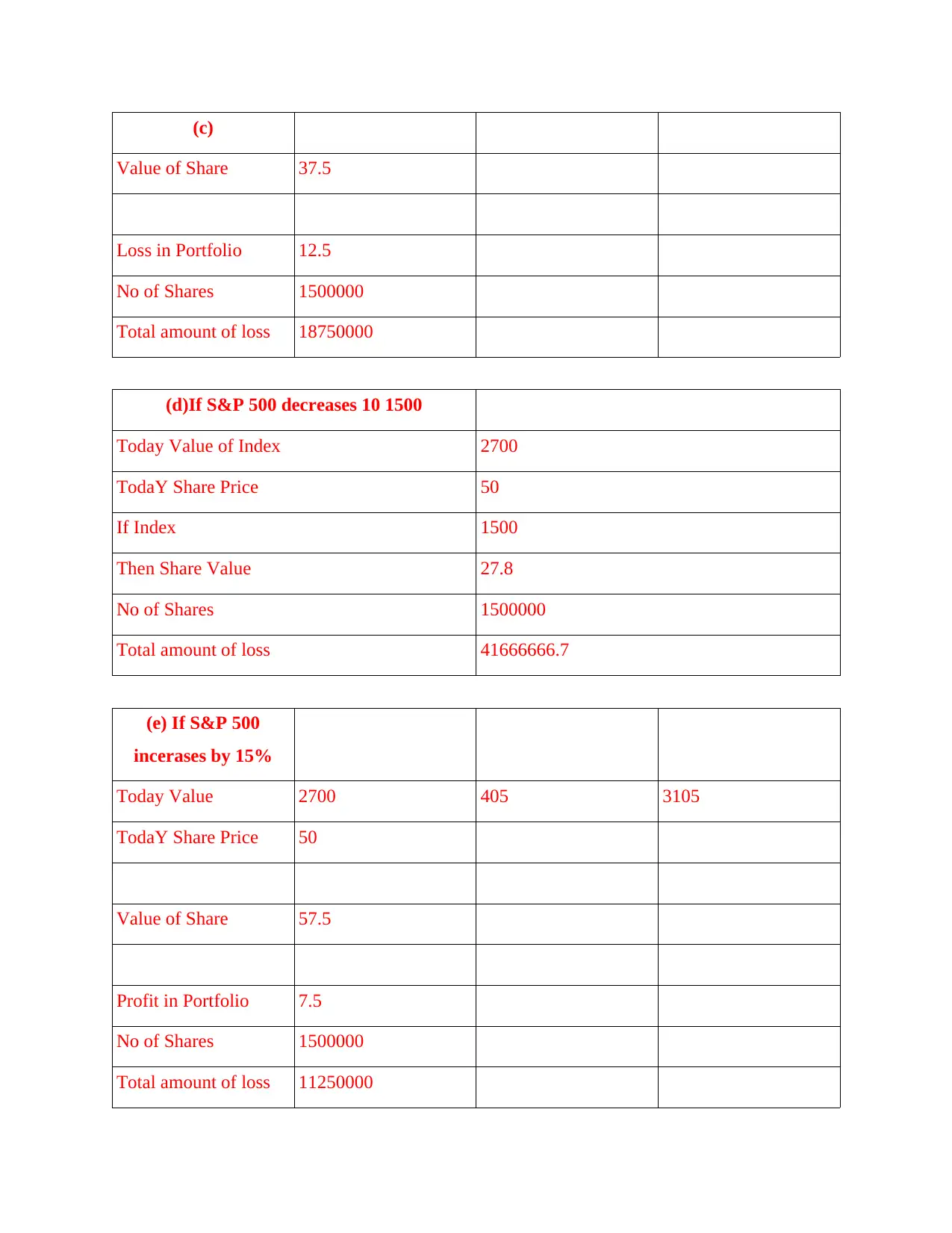

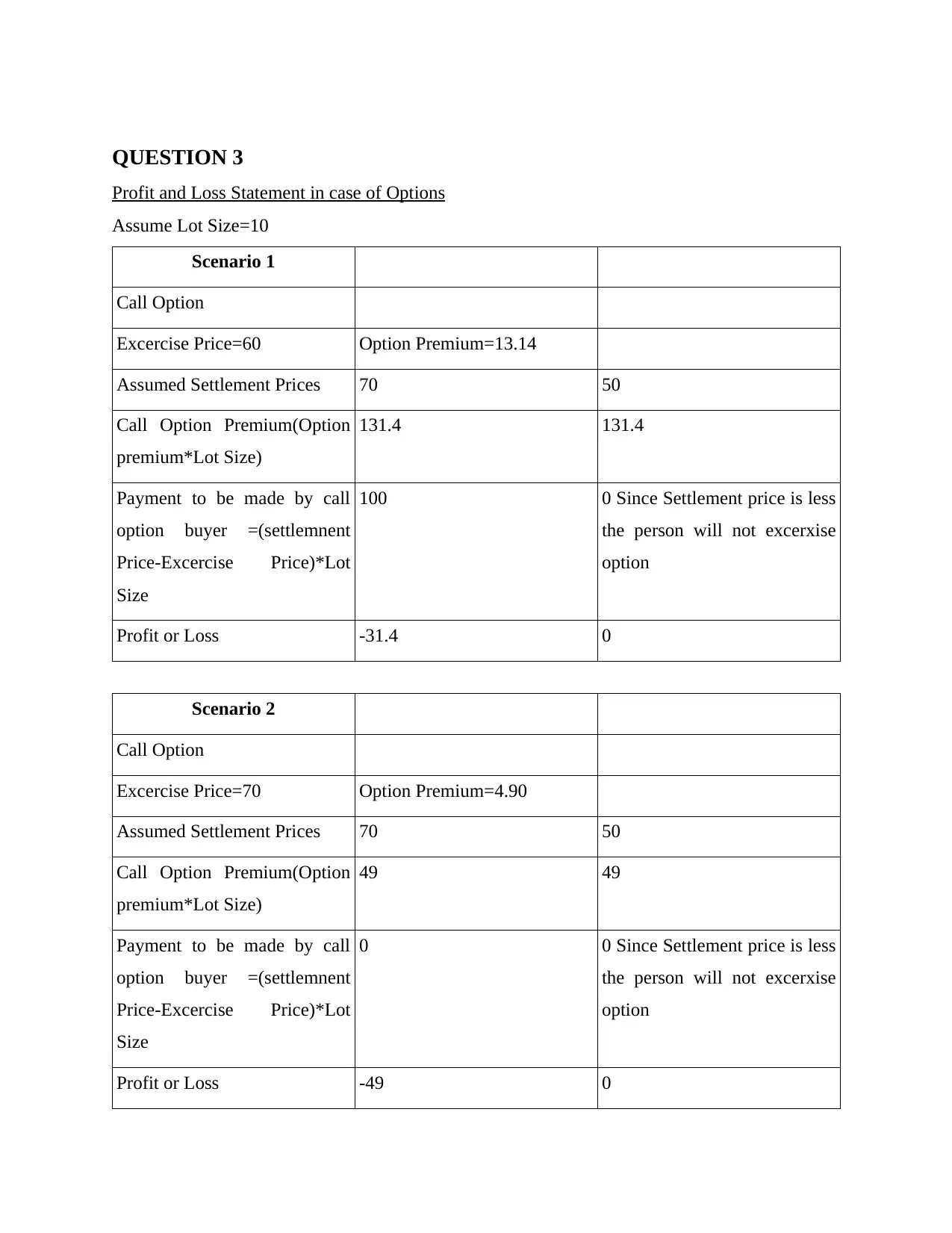

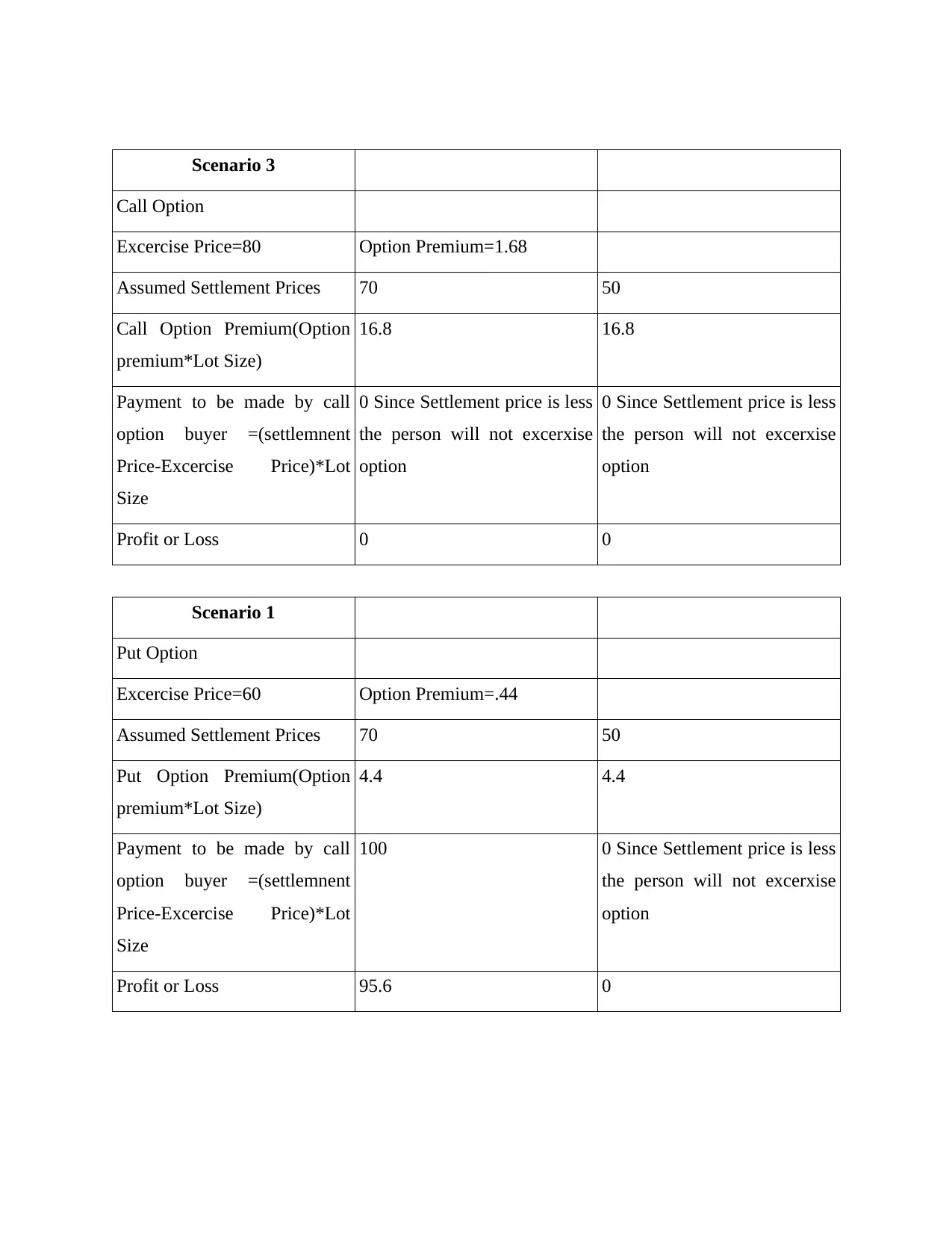

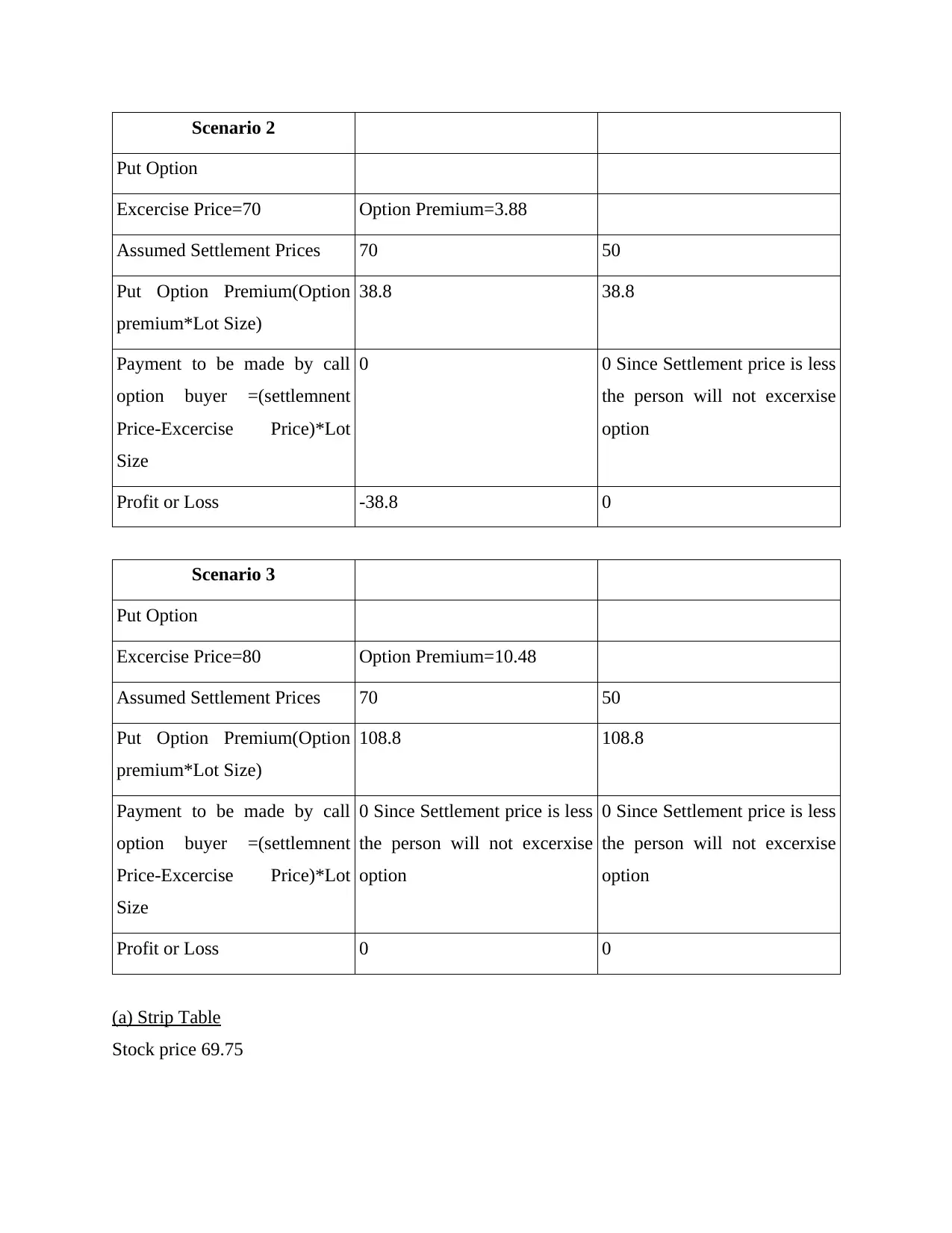

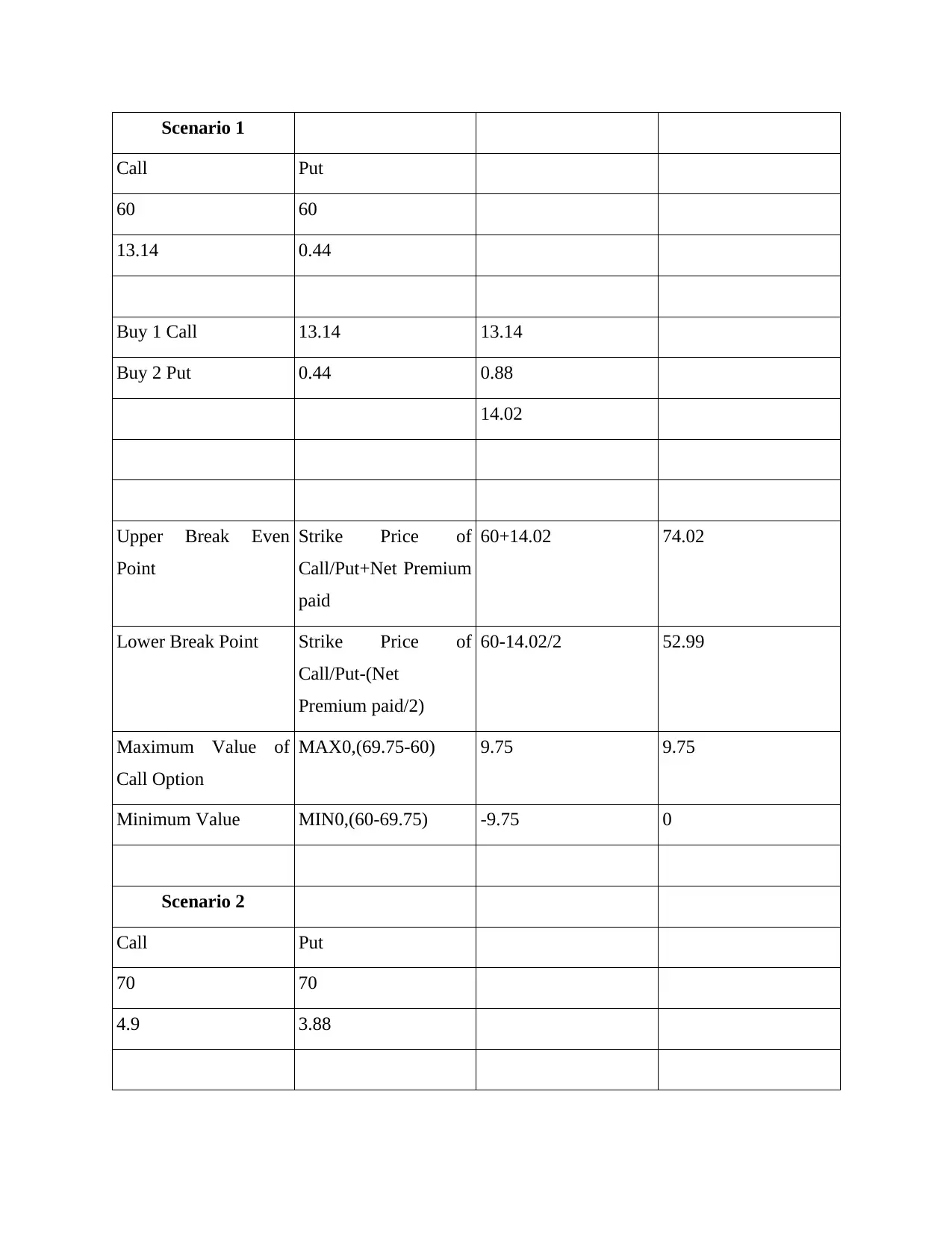

This finance project delves into various aspects of financial instruments and their applications. It begins with the calculation of continuously compounded zero rates using the bootstrap method and the determination of six-month forward rates. The project explores the use of zero rates and zero curves, bond pricing methodologies, and the analysis of the relationship between bond prices and yields, including hedging strategies. Furthermore, it includes a detailed analysis of option strategies, such as profit and loss statements for different scenarios. The project also covers the valuation of European put options using a four-step binomial tree and the Black-Scholes model, along with an explanation of the differences between American and European options. Finally, it explores the calculation of implied volatility and the hedging of a portfolio, including parallel and non-parallel shifts in the yield curve. The project also addresses the impacts of market movements on a portfolio and various option strategies like strip tables, reverse butterflies, straddles, and straps.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.