Financial Management in Organisation: Cost and Valuation

VerifiedAdded on 2020/12/09

|11

|3395

|276

Report

AI Summary

This report provides a comprehensive analysis of financial management within an organization, specifically focusing on Vodafone plc. It delves into various methods for estimating the cost of capital, including cost of debt, cost of preference share capital, cost of equity capital (dividend yield, dividend yield plus growth rate, and earning yield methods), and the weighted average cost of capital (WACC). The report also explores different business valuation methods such as cost approach, market approach, income approach, and market capitalization, applying these methods to Vodafone's financial data. Furthermore, it addresses foreign exchange issues related to the company's financing, particularly concerning bonds and their implications. The analysis incorporates financial data and formulas to illustrate the practical application of these concepts within the telecommunications industry.

FINANCIAL

MANAGEMENT

IN

ORGANISATION

MANAGEMENT

IN

ORGANISATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

(a) Methods of estimating cost of capital....................................................................................1

(b) Business Valuation methods..................................................................................................3

(c) Foreign exchange issues related to the finance......................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

(a) Methods of estimating cost of capital....................................................................................1

(b) Business Valuation methods..................................................................................................3

(c) Foreign exchange issues related to the finance......................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Finance is the lifeline of any organisation which needs to a continuous flow of funds in

and out in a business enterprises (Ogiela, 2015) . Financial management is an important in any

business which is related to marketing and production because it is broad activity of an

organization. It is the process of planning, organizing, controlling and motivating financial

resources to achieve required goals and objectives of a company. In the particular report taken

company Vodafone plc, it is a business based in UK, which can operate in many countries. It is a

British multinational telecommunication company and they have owned network in 25 countries

and their partner network in 47 further countries. In the report focused on various methods of

cost of capital and estimate of the cost of capital of Vodafone investors. Apart from discuss

possible business valuation methods and applying in Vodafone to identify issues of each

estimated values. In addition determine the foreign exchange issues related to the financial raised

from bonds in different countries.

TASK

(a) Methods of estimating cost of capital

Cost of capital is the required return which is important for company as opportunity cost

and making a specific investment. The particular rate of return that could have been earned by

putting the same money into a different investment with equal risk. In hence, the cost of capital

is the rate of return essential to influence the investor to make a give investment. There is

mentioned different methods of estimation of cost of capital -

Cost of Debt

Cost of debt capital states to the total cost or rate of interest paid by an organization in

raising debt capital. In present time total interest paid by company on raising debt capital is not

reasoned as cost of debt because the total interest is activated as cost of debt because the total

interest is treated as an expenses and it is deducted from tax (Cho and et.al, 2012). There is

applied formula to calculate cost of debt -

Kd = (1-T) * R* 100 (It is applied after tax adjustment)

When company issues debentures on premium and discount after then calculating cost of

debt and principal amount will be adjusted with these amount after adjust amount will be

net proceed -

1

Finance is the lifeline of any organisation which needs to a continuous flow of funds in

and out in a business enterprises (Ogiela, 2015) . Financial management is an important in any

business which is related to marketing and production because it is broad activity of an

organization. It is the process of planning, organizing, controlling and motivating financial

resources to achieve required goals and objectives of a company. In the particular report taken

company Vodafone plc, it is a business based in UK, which can operate in many countries. It is a

British multinational telecommunication company and they have owned network in 25 countries

and their partner network in 47 further countries. In the report focused on various methods of

cost of capital and estimate of the cost of capital of Vodafone investors. Apart from discuss

possible business valuation methods and applying in Vodafone to identify issues of each

estimated values. In addition determine the foreign exchange issues related to the financial raised

from bonds in different countries.

TASK

(a) Methods of estimating cost of capital

Cost of capital is the required return which is important for company as opportunity cost

and making a specific investment. The particular rate of return that could have been earned by

putting the same money into a different investment with equal risk. In hence, the cost of capital

is the rate of return essential to influence the investor to make a give investment. There is

mentioned different methods of estimation of cost of capital -

Cost of Debt

Cost of debt capital states to the total cost or rate of interest paid by an organization in

raising debt capital. In present time total interest paid by company on raising debt capital is not

reasoned as cost of debt because the total interest is activated as cost of debt because the total

interest is treated as an expenses and it is deducted from tax (Cho and et.al, 2012). There is

applied formula to calculate cost of debt -

Kd = (1-T) * R* 100 (It is applied after tax adjustment)

When company issues debentures on premium and discount after then calculating cost of

debt and principal amount will be adjusted with these amount after adjust amount will be

net proceed -

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Kd = I / N.P. (after adjusting premium or discount of floating cost)

Cost of debt after tax adjustment

Kd = IX (1-t) /N.P.

Cost of preference share capital

According to this method total of amount of dividend paid and expenses acquisition for

increasing preference shares. The dividend paid on preference shares is not less from tax, as

dividend is an acquiring of profit and not well-advised as an expenses (Zimmerman and Roberts,

2012) . Cost of preference shares can be calculated by using the following formula -

Kpc = Dividend / net proceed of preference share capital

Cost of Equity capital

This method is little difficult as compare with cost of debt and cost of preference capital.

There is main reason of this method that the equity shareholders do not receive fixed interest or

dividend. The dividend on equity share change which is depended on profit because it is earned

by a company. This method is very important and there is risk factor plays an important role to

decide rate of dividend to be paid on equity capital. In this method adopted different method to

calculate cost of equity - Dividend Yield method = Ke = Dividend per share / Net proceed per share Dividend yield plus growth rate of dividend method = Ke = Dividend per share /Net

proceed per share + growth rate

Earning yield method = Ke = Earning per share / Net proceed per share

Cost of retained earnings

Retained earnings are known as profit reserve of a company which are not distributed as

dividend. Retained earnings kept by company for finance long term as well as short term

projects. The investors expect that the company should invest the retained earnings on those

projects which is profitable for company. In addition the investors require that the organization

should divided the profit earned by investing retained earnings in the form of dividend

(Sweeting, 2017).

Ke = Kr Approach

Weighted average cost of capital

According to this method whole cost which is obtained from several source of capital

and calculate of firm's cost of capital. In the category of capital includes all sources and they are

2

Cost of debt after tax adjustment

Kd = IX (1-t) /N.P.

Cost of preference share capital

According to this method total of amount of dividend paid and expenses acquisition for

increasing preference shares. The dividend paid on preference shares is not less from tax, as

dividend is an acquiring of profit and not well-advised as an expenses (Zimmerman and Roberts,

2012) . Cost of preference shares can be calculated by using the following formula -

Kpc = Dividend / net proceed of preference share capital

Cost of Equity capital

This method is little difficult as compare with cost of debt and cost of preference capital.

There is main reason of this method that the equity shareholders do not receive fixed interest or

dividend. The dividend on equity share change which is depended on profit because it is earned

by a company. This method is very important and there is risk factor plays an important role to

decide rate of dividend to be paid on equity capital. In this method adopted different method to

calculate cost of equity - Dividend Yield method = Ke = Dividend per share / Net proceed per share Dividend yield plus growth rate of dividend method = Ke = Dividend per share /Net

proceed per share + growth rate

Earning yield method = Ke = Earning per share / Net proceed per share

Cost of retained earnings

Retained earnings are known as profit reserve of a company which are not distributed as

dividend. Retained earnings kept by company for finance long term as well as short term

projects. The investors expect that the company should invest the retained earnings on those

projects which is profitable for company. In addition the investors require that the organization

should divided the profit earned by investing retained earnings in the form of dividend

(Sweeting, 2017).

Ke = Kr Approach

Weighted average cost of capital

According to this method whole cost which is obtained from several source of capital

and calculate of firm's cost of capital. In the category of capital includes all sources and they are

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

proportionately weighted such as common stock, bonds, preferred stock and any other long term

debt which is included in WASS calculation. There is company has followed particular formula -

WACC = E/V * Re + D/v * Rd * (1 Tc)

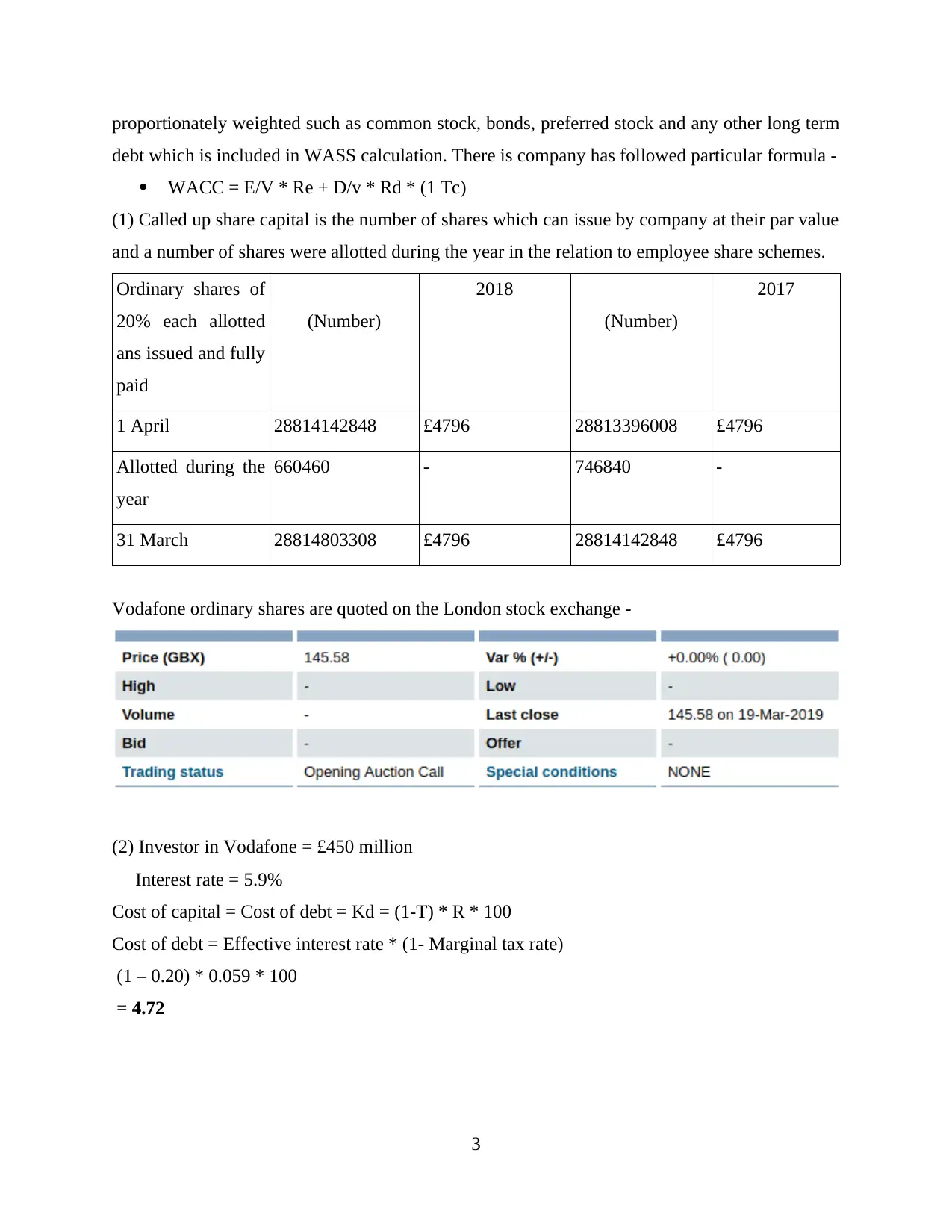

(1) Called up share capital is the number of shares which can issue by company at their par value

and a number of shares were allotted during the year in the relation to employee share schemes.

Ordinary shares of

20% each allotted

ans issued and fully

paid

(Number)

2018

(Number)

2017

1 April 28814142848 £4796 28813396008 £4796

Allotted during the

year

660460 - 746840 -

31 March 28814803308 £4796 28814142848 £4796

Vodafone ordinary shares are quoted on the London stock exchange -

(2) Investor in Vodafone = £450 million

Interest rate = 5.9%

Cost of capital = Cost of debt = Kd = (1-T) * R * 100

Cost of debt = Effective interest rate * (1- Marginal tax rate)

(1 – 0.20) * 0.059 * 100

= 4.72

3

debt which is included in WASS calculation. There is company has followed particular formula -

WACC = E/V * Re + D/v * Rd * (1 Tc)

(1) Called up share capital is the number of shares which can issue by company at their par value

and a number of shares were allotted during the year in the relation to employee share schemes.

Ordinary shares of

20% each allotted

ans issued and fully

paid

(Number)

2018

(Number)

2017

1 April 28814142848 £4796 28813396008 £4796

Allotted during the

year

660460 - 746840 -

31 March 28814803308 £4796 28814142848 £4796

Vodafone ordinary shares are quoted on the London stock exchange -

(2) Investor in Vodafone = £450 million

Interest rate = 5.9%

Cost of capital = Cost of debt = Kd = (1-T) * R * 100

Cost of debt = Effective interest rate * (1- Marginal tax rate)

(1 – 0.20) * 0.059 * 100

= 4.72

3

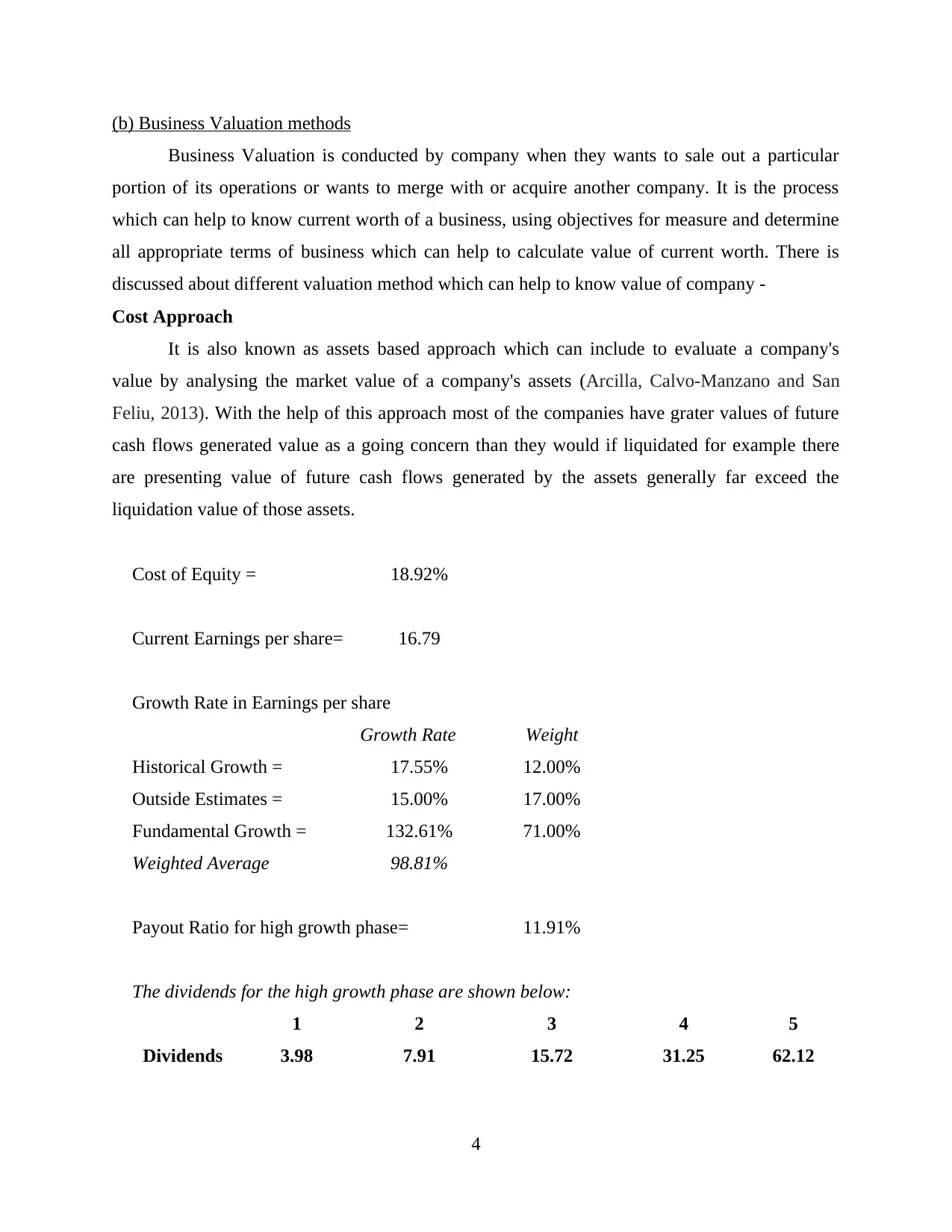

(b) Business Valuation methods

Business Valuation is conducted by company when they wants to sale out a particular

portion of its operations or wants to merge with or acquire another company. It is the process

which can help to know current worth of a business, using objectives for measure and determine

all appropriate terms of business which can help to calculate value of current worth. There is

discussed about different valuation method which can help to know value of company -

Cost Approach

It is also known as assets based approach which can include to evaluate a company's

value by analysing the market value of a company's assets (Arcilla, Calvo-Manzano and San

Feliu, 2013). With the help of this approach most of the companies have grater values of future

cash flows generated value as a going concern than they would if liquidated for example there

are presenting value of future cash flows generated by the assets generally far exceed the

liquidation value of those assets.

Cost of Equity = 18.92%

Current Earnings per share= 16.79

Growth Rate in Earnings per share

Growth Rate Weight

Historical Growth = 17.55% 12.00%

Outside Estimates = 15.00% 17.00%

Fundamental Growth = 132.61% 71.00%

Weighted Average 98.81%

Payout Ratio for high growth phase= 11.91%

The dividends for the high growth phase are shown below:

1 2 3 4 5

Dividends 3.98 7.91 15.72 31.25 62.12

4

Business Valuation is conducted by company when they wants to sale out a particular

portion of its operations or wants to merge with or acquire another company. It is the process

which can help to know current worth of a business, using objectives for measure and determine

all appropriate terms of business which can help to calculate value of current worth. There is

discussed about different valuation method which can help to know value of company -

Cost Approach

It is also known as assets based approach which can include to evaluate a company's

value by analysing the market value of a company's assets (Arcilla, Calvo-Manzano and San

Feliu, 2013). With the help of this approach most of the companies have grater values of future

cash flows generated value as a going concern than they would if liquidated for example there

are presenting value of future cash flows generated by the assets generally far exceed the

liquidation value of those assets.

Cost of Equity = 18.92%

Current Earnings per share= 16.79

Growth Rate in Earnings per share

Growth Rate Weight

Historical Growth = 17.55% 12.00%

Outside Estimates = 15.00% 17.00%

Fundamental Growth = 132.61% 71.00%

Weighted Average 98.81%

Payout Ratio for high growth phase= 11.91%

The dividends for the high growth phase are shown below:

1 2 3 4 5

Dividends 3.98 7.91 15.72 31.25 62.12

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

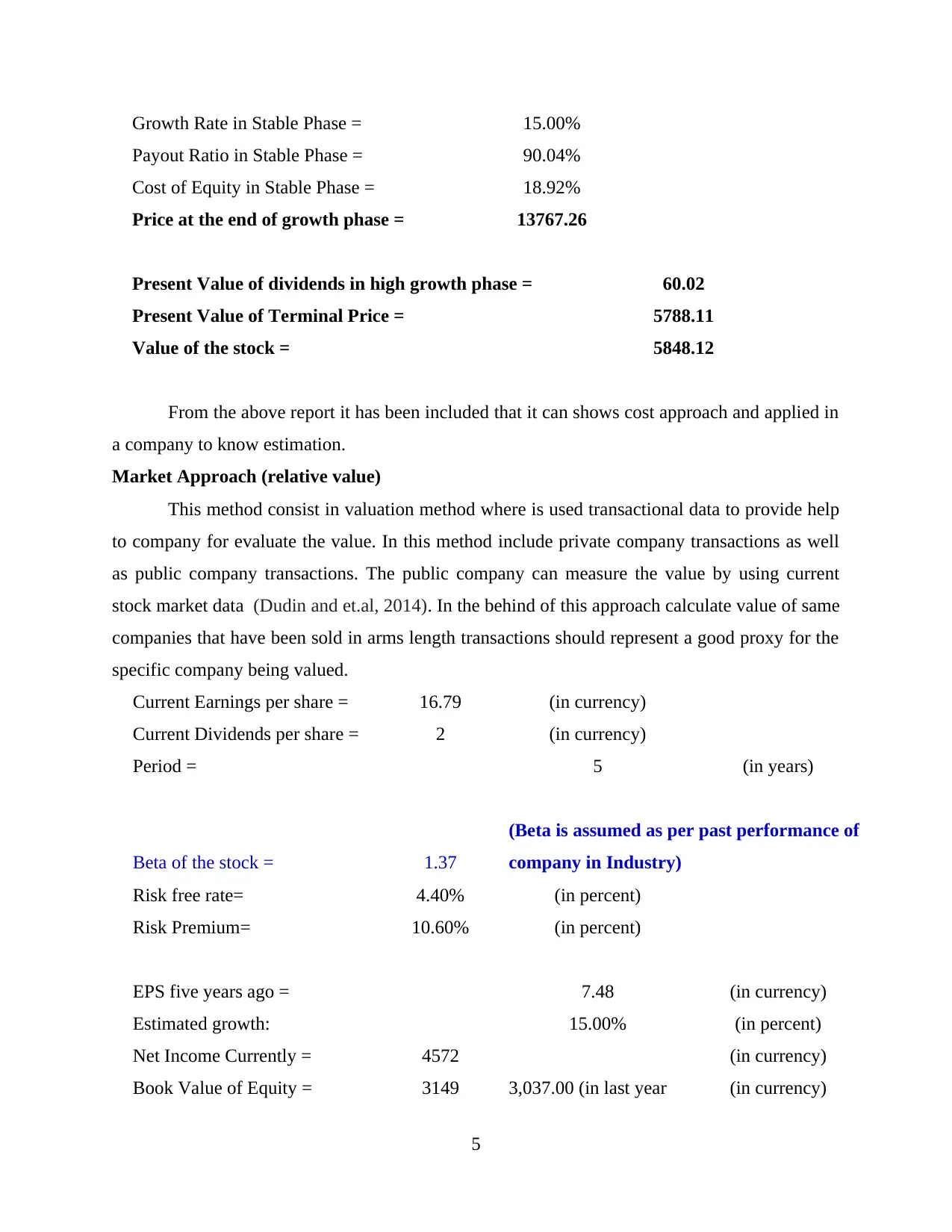

Growth Rate in Stable Phase = 15.00%

Payout Ratio in Stable Phase = 90.04%

Cost of Equity in Stable Phase = 18.92%

Price at the end of growth phase = 13767.26

Present Value of dividends in high growth phase = 60.02

Present Value of Terminal Price = 5788.11

Value of the stock = 5848.12

From the above report it has been included that it can shows cost approach and applied in

a company to know estimation.

Market Approach (relative value)

This method consist in valuation method where is used transactional data to provide help

to company for evaluate the value. In this method include private company transactions as well

as public company transactions. The public company can measure the value by using current

stock market data (Dudin and et.al, 2014). In the behind of this approach calculate value of same

companies that have been sold in arms length transactions should represent a good proxy for the

specific company being valued.

Current Earnings per share = 16.79 (in currency)

Current Dividends per share = 2 (in currency)

Period = 5 (in years)

Beta of the stock = 1.37

(Beta is assumed as per past performance of

company in Industry)

Risk free rate= 4.40% (in percent)

Risk Premium= 10.60% (in percent)

EPS five years ago = 7.48 (in currency)

Estimated growth: 15.00% (in percent)

Net Income Currently = 4572 (in currency)

Book Value of Equity = 3149 3,037.00 (in last year (in currency)

5

Payout Ratio in Stable Phase = 90.04%

Cost of Equity in Stable Phase = 18.92%

Price at the end of growth phase = 13767.26

Present Value of dividends in high growth phase = 60.02

Present Value of Terminal Price = 5788.11

Value of the stock = 5848.12

From the above report it has been included that it can shows cost approach and applied in

a company to know estimation.

Market Approach (relative value)

This method consist in valuation method where is used transactional data to provide help

to company for evaluate the value. In this method include private company transactions as well

as public company transactions. The public company can measure the value by using current

stock market data (Dudin and et.al, 2014). In the behind of this approach calculate value of same

companies that have been sold in arms length transactions should represent a good proxy for the

specific company being valued.

Current Earnings per share = 16.79 (in currency)

Current Dividends per share = 2 (in currency)

Period = 5 (in years)

Beta of the stock = 1.37

(Beta is assumed as per past performance of

company in Industry)

Risk free rate= 4.40% (in percent)

Risk Premium= 10.60% (in percent)

EPS five years ago = 7.48 (in currency)

Estimated growth: 15.00% (in percent)

Net Income Currently = 4572 (in currency)

Book Value of Equity = 3149 3,037.00 (in last year (in currency)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017)

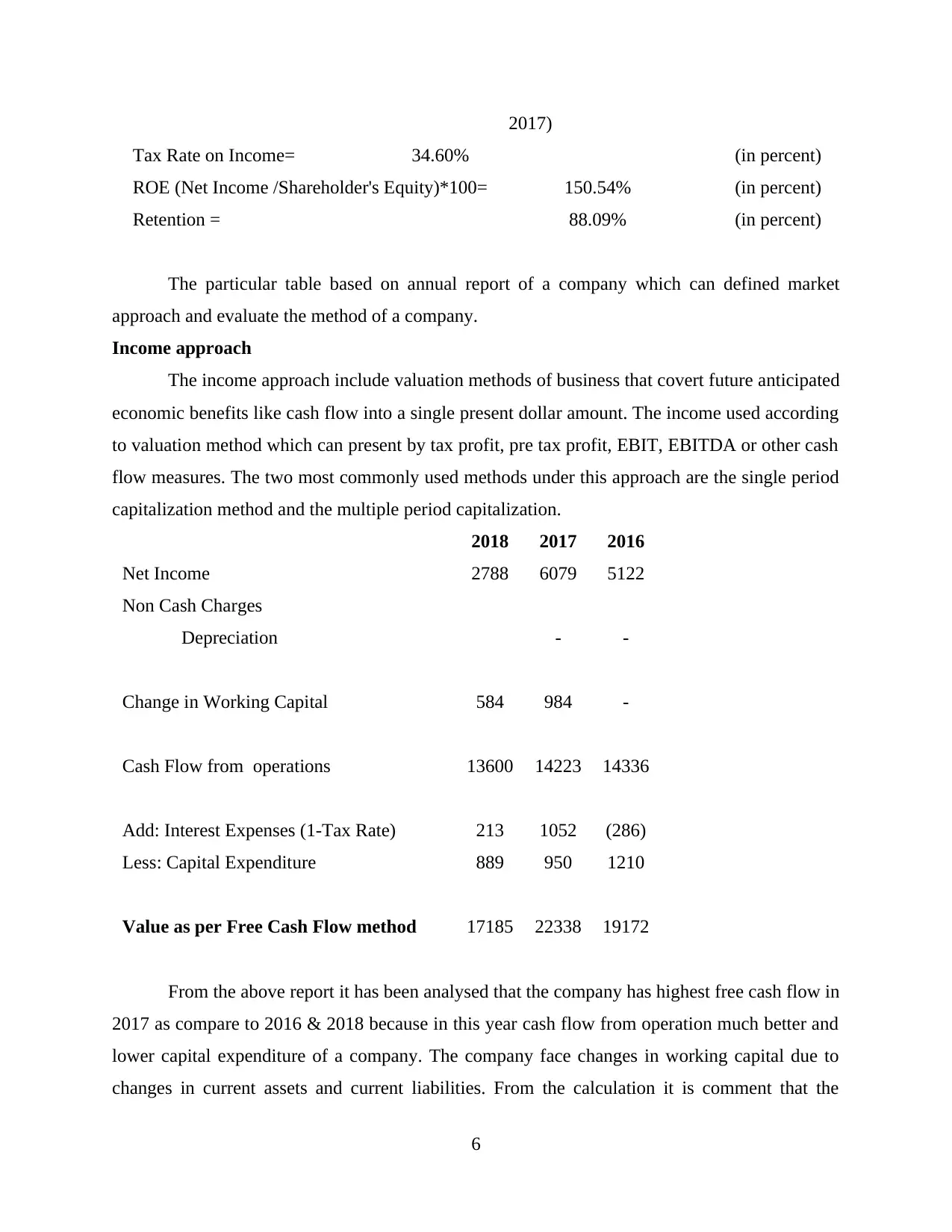

Tax Rate on Income= 34.60% (in percent)

ROE (Net Income /Shareholder's Equity)*100= 150.54% (in percent)

Retention = 88.09% (in percent)

The particular table based on annual report of a company which can defined market

approach and evaluate the method of a company.

Income approach

The income approach include valuation methods of business that covert future anticipated

economic benefits like cash flow into a single present dollar amount. The income used according

to valuation method which can present by tax profit, pre tax profit, EBIT, EBITDA or other cash

flow measures. The two most commonly used methods under this approach are the single period

capitalization method and the multiple period capitalization.

2018 2017 2016

Net Income 2788 6079 5122

Non Cash Charges

Depreciation - -

Change in Working Capital 584 984 -

Cash Flow from operations 13600 14223 14336

Add: Interest Expenses (1-Tax Rate) 213 1052 (286)

Less: Capital Expenditure 889 950 1210

Value as per Free Cash Flow method 17185 22338 19172

From the above report it has been analysed that the company has highest free cash flow in

2017 as compare to 2016 & 2018 because in this year cash flow from operation much better and

lower capital expenditure of a company. The company face changes in working capital due to

changes in current assets and current liabilities. From the calculation it is comment that the

6

Tax Rate on Income= 34.60% (in percent)

ROE (Net Income /Shareholder's Equity)*100= 150.54% (in percent)

Retention = 88.09% (in percent)

The particular table based on annual report of a company which can defined market

approach and evaluate the method of a company.

Income approach

The income approach include valuation methods of business that covert future anticipated

economic benefits like cash flow into a single present dollar amount. The income used according

to valuation method which can present by tax profit, pre tax profit, EBIT, EBITDA or other cash

flow measures. The two most commonly used methods under this approach are the single period

capitalization method and the multiple period capitalization.

2018 2017 2016

Net Income 2788 6079 5122

Non Cash Charges

Depreciation - -

Change in Working Capital 584 984 -

Cash Flow from operations 13600 14223 14336

Add: Interest Expenses (1-Tax Rate) 213 1052 (286)

Less: Capital Expenditure 889 950 1210

Value as per Free Cash Flow method 17185 22338 19172

From the above report it has been analysed that the company has highest free cash flow in

2017 as compare to 2016 & 2018 because in this year cash flow from operation much better and

lower capital expenditure of a company. The company face changes in working capital due to

changes in current assets and current liabilities. From the calculation it is comment that the

6

company has valued free cash flow in different year in respectively in 2016, £17185 in 2017,

£22338 and in 2018, £19172.

Market Capitalization

It is the simplest method of business valuation which is calculated through multiplying

the company's share price by its total number of shares outstanding.

(c) Foreign exchange issues related to the finance

In the context of Vodafone Plc, the bonds which have been undertake by the company

mandatory convertible bonds + high debt security. The MCB related to short term bonds because

the term period of particular bonds is 3 years which is buy back after 3 years. The company has

adopted this policy because of avoiding equity dilution and economical impact of share

movements. The company has gone with hedging strategy which can profitable for a company

because of economical impact does not affect to the strategy (Filip and Raffournier 2014). The

advantage of this strategy when situation in the favour of selling so company will go with selling

point of view and when situation favour in buying so company has following busying strategy.

The company has purchased mandatory convertible bonds on 25 august 2017 to £729.1 million

shares which can be convert of treasury shares at a conversion price which is £1.9751. The

company has reflected the conversion price at issue £2.1730 adjusted for the pound sterling

equivalents of aggregate dividends paid in August 2016, February 2017 and August 2017. The

bonds amounts difference shows because of accountable regarding change in currency rate. The

company has carrying value of the bonds in 2017, £660 and in 2018, £3062 which can relate to

short term borrowings. The interest rate on this of particular bond 0.0% to 8.125%. In long term

the carrying value £19345 in 2017 and £18804 in 2018 and there is same interest rate provided

by company to bond holders. The fair value will be change of a company in short term and long

term which is

Fair value 2017 2018

Short term borrowings £667 £3057

Long term borrowings £19286 £18714

The company has faced many issues related to the finance raised from bonds in different

currencies -

7

£22338 and in 2018, £19172.

Market Capitalization

It is the simplest method of business valuation which is calculated through multiplying

the company's share price by its total number of shares outstanding.

(c) Foreign exchange issues related to the finance

In the context of Vodafone Plc, the bonds which have been undertake by the company

mandatory convertible bonds + high debt security. The MCB related to short term bonds because

the term period of particular bonds is 3 years which is buy back after 3 years. The company has

adopted this policy because of avoiding equity dilution and economical impact of share

movements. The company has gone with hedging strategy which can profitable for a company

because of economical impact does not affect to the strategy (Filip and Raffournier 2014). The

advantage of this strategy when situation in the favour of selling so company will go with selling

point of view and when situation favour in buying so company has following busying strategy.

The company has purchased mandatory convertible bonds on 25 august 2017 to £729.1 million

shares which can be convert of treasury shares at a conversion price which is £1.9751. The

company has reflected the conversion price at issue £2.1730 adjusted for the pound sterling

equivalents of aggregate dividends paid in August 2016, February 2017 and August 2017. The

bonds amounts difference shows because of accountable regarding change in currency rate. The

company has carrying value of the bonds in 2017, £660 and in 2018, £3062 which can relate to

short term borrowings. The interest rate on this of particular bond 0.0% to 8.125%. In long term

the carrying value £19345 in 2017 and £18804 in 2018 and there is same interest rate provided

by company to bond holders. The fair value will be change of a company in short term and long

term which is

Fair value 2017 2018

Short term borrowings £667 £3057

Long term borrowings £19286 £18714

The company has faced many issues related to the finance raised from bonds in different

currencies -

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Credit or Default risk – This risk is a borrower will be unable to pay the contractual

interest or principal on its debt facultative. Credit risk is particular related to investor who

can hold bonds in their portfolios. In this type risk consist of government bonds which is

issued by federal government (Habib, Uddin Bhuiyan and Islam, 2013). They have the

least amount of default risk like the lowest returns. On the other hand Vodafone company

tend to have the highest amount of default risk because of lower interest rate on their

bonds.

Country risk – The particular risk states that a country won't be able to honour its

financial commitments. When a country defaults on its obligation so it will harm to the

performance of financial instruments of particular country as well as other countries it

has relationship with. Country risk happen in Vodafone when they are bought bonds from

another country and on the particular country defaults on its obligations. It is mostly

related to emerging market or countries that have a serve deficit.

Foreign exchange risk -

Interest Rate risk – In the risk that an investment's value will change due to change in

the absolute level of interest rates the spread between two rates, in the shape of the yield

curve or in any other interest rate relationship. In the context of Vodafone company it has

been affected to value of bonds more directly than stocks and is a significant risks to all

bond holders (Cohen and et.al, 2014).

Market risk – In this risk that an investment will face fluctuations and decline in value

because of economic developments and other events that impact the whole market. It is

also known as systematic risk which can affect to all securities in the same manner.

Specifically market risk can consist of inflation risk, currency risk, liquidity risk, interest

rate risk and socio-political risk. It is also consider in Vodafone plc because market risk

impossible to avoid in completely way. These above risks can be relieved to some extent

by diversification.

Political risk – In these type risk an investment's returns could sustain due to political

changes and instability. This type of risk can related to change in government, legislative

bodies, other foreign policy makers or military control. This type of risk origin in

Vodafone plc when other countries politics will be change and affect to companies

8

interest or principal on its debt facultative. Credit risk is particular related to investor who

can hold bonds in their portfolios. In this type risk consist of government bonds which is

issued by federal government (Habib, Uddin Bhuiyan and Islam, 2013). They have the

least amount of default risk like the lowest returns. On the other hand Vodafone company

tend to have the highest amount of default risk because of lower interest rate on their

bonds.

Country risk – The particular risk states that a country won't be able to honour its

financial commitments. When a country defaults on its obligation so it will harm to the

performance of financial instruments of particular country as well as other countries it

has relationship with. Country risk happen in Vodafone when they are bought bonds from

another country and on the particular country defaults on its obligations. It is mostly

related to emerging market or countries that have a serve deficit.

Foreign exchange risk -

Interest Rate risk – In the risk that an investment's value will change due to change in

the absolute level of interest rates the spread between two rates, in the shape of the yield

curve or in any other interest rate relationship. In the context of Vodafone company it has

been affected to value of bonds more directly than stocks and is a significant risks to all

bond holders (Cohen and et.al, 2014).

Market risk – In this risk that an investment will face fluctuations and decline in value

because of economic developments and other events that impact the whole market. It is

also known as systematic risk which can affect to all securities in the same manner.

Specifically market risk can consist of inflation risk, currency risk, liquidity risk, interest

rate risk and socio-political risk. It is also consider in Vodafone plc because market risk

impossible to avoid in completely way. These above risks can be relieved to some extent

by diversification.

Political risk – In these type risk an investment's returns could sustain due to political

changes and instability. This type of risk can related to change in government, legislative

bodies, other foreign policy makers or military control. This type of risk origin in

Vodafone plc when other countries politics will be change and affect to companies

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

policies. It is also called as geopolitical risk because it becomes more of a factors as an

investment's time horizon gets longer (Bandy, 2014).

CONCLUSION

As per the above discussion it has been concluded that financial management is very

important for any company because it is lifeline for any organisation. In any company manage

finance and survive business for long time is important to manage. There company has applied

different valuation method to know about current worth of a company such as market approach,

cost approach and income approach. There are company has purchased MCB from other

company which is redeemable in 3 years and company will buy back again. Various issues are

origin in foreign exchange which is origin in company and which is solve by company.

9

investment's time horizon gets longer (Bandy, 2014).

CONCLUSION

As per the above discussion it has been concluded that financial management is very

important for any company because it is lifeline for any organisation. In any company manage

finance and survive business for long time is important to manage. There company has applied

different valuation method to know about current worth of a company such as market approach,

cost approach and income approach. There are company has purchased MCB from other

company which is redeemable in 3 years and company will buy back again. Various issues are

origin in foreign exchange which is origin in company and which is solve by company.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.