International Business Finance: Project Financial Viability Analysis

VerifiedAdded on 2021/04/21

|11

|2234

|95

Report

AI Summary

This report provides a detailed financial analysis of a new project to be conducted in Brazil by a US company, focusing on its financial viability and performance. The analysis includes calculating free cash flow, evaluating hedging strategies for currency risk, and assessing the implications of using debt from both Brazilian and US sources. The report also examines the factors driving differences between financial options and the potential impact of a financial crisis on the project. The findings suggest that hedging currency risk and utilizing debt from the Brazilian subsidiary, rather than the US parent company, are the most financially sound strategies. The report concludes with a recommendation to proceed with the project under specific conditions and emphasizes the importance of currency risk management to maximize returns on investment. The analysis uses NPV calculations to support its recommendations.

[AIB subject title and subject AQF Level]

[Student name]

[Student number]

[International Business Finance]

Word count: [.. insert word count here ..]

1

[Student name]

[Student number]

[International Business Finance]

Word count: [.. insert word count here ..]

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The assessment mainly evaluates the financial performance of the new project, which could

help in addressing the financial viability of the new project. In addition, relevant financial

performance is evaluated on the basis of difference circumstance and scenarios, which could

help in identifying the financial viability of the new project. Moreover, from the scenario

analysis financial stability and profitability generated from the project could be identified.

Hence, it is recommended for the company to conduct the project with the identified

measures, which might help the US parent company to increase their returns from

investment.

2

The assessment mainly evaluates the financial performance of the new project, which could

help in addressing the financial viability of the new project. In addition, relevant financial

performance is evaluated on the basis of difference circumstance and scenarios, which could

help in identifying the financial viability of the new project. Moreover, from the scenario

analysis financial stability and profitability generated from the project could be identified.

Hence, it is recommended for the company to conduct the project with the identified

measures, which might help the US parent company to increase their returns from

investment.

2

Table of contents

a. Calculating the Free cash flow of the project:....................................................................4

b.(i) Hedging $2 million:........................................................................................................5

b.(ii) Not hedging $2 million..............................................................................................5

c.(i) Using the debt option from BRL:...................................................................................6

c.(ii) Using the debt option from US:.................................................................................7

d. Factors driving the difference between two factors:..........................................................7

e. Impact of financial crisis on the project:............................................................................8

Conclusion and recommendation:..........................................................................................9

Reference and Bibliography list...........................................................................................10

3

a. Calculating the Free cash flow of the project:....................................................................4

b.(i) Hedging $2 million:........................................................................................................5

b.(ii) Not hedging $2 million..............................................................................................5

c.(i) Using the debt option from BRL:...................................................................................6

c.(ii) Using the debt option from US:.................................................................................7

d. Factors driving the difference between two factors:..........................................................7

e. Impact of financial crisis on the project:............................................................................8

Conclusion and recommendation:..........................................................................................9

Reference and Bibliography list...........................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

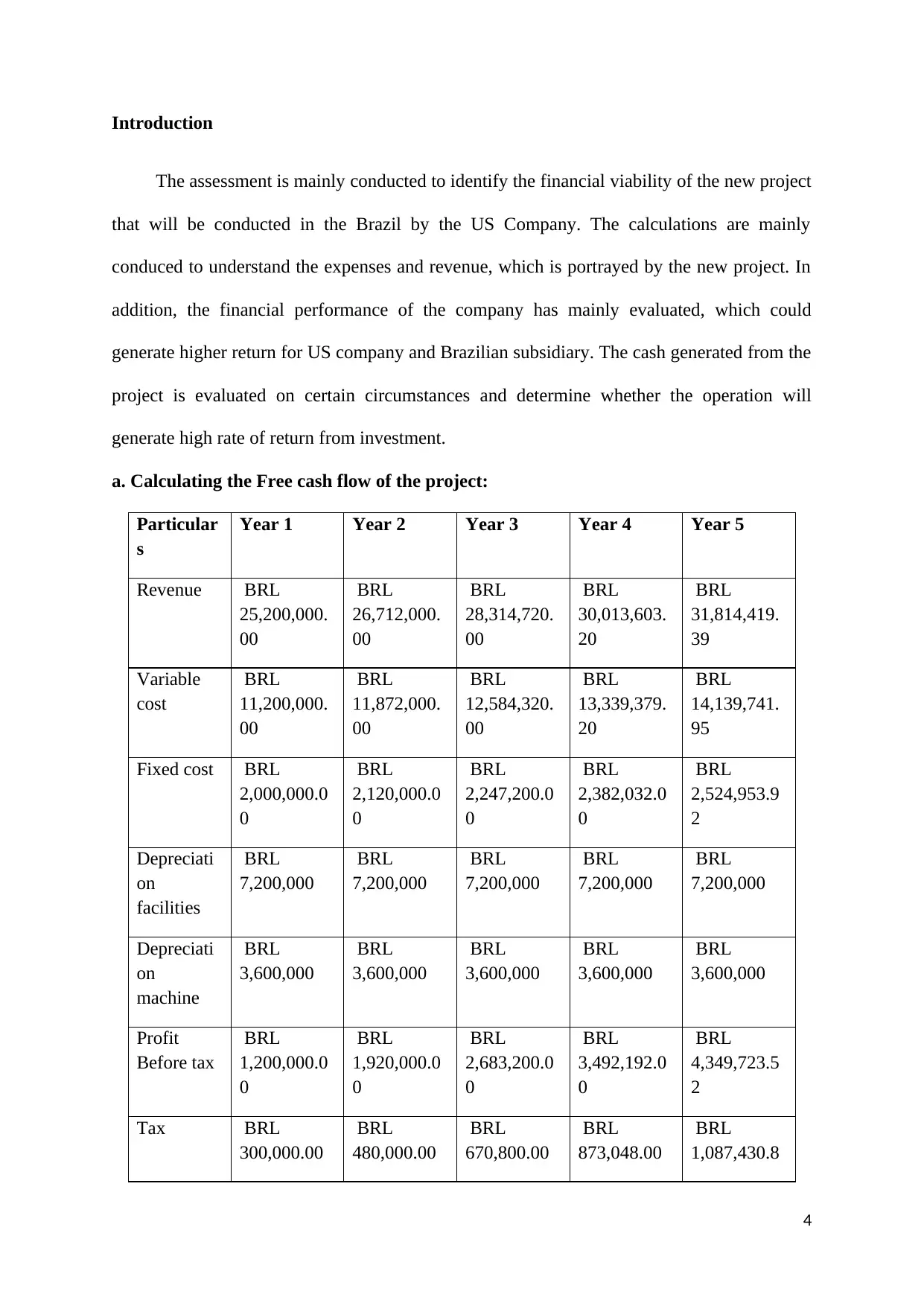

Introduction

The assessment is mainly conducted to identify the financial viability of the new project

that will be conducted in the Brazil by the US Company. The calculations are mainly

conduced to understand the expenses and revenue, which is portrayed by the new project. In

addition, the financial performance of the company has mainly evaluated, which could

generate higher return for US company and Brazilian subsidiary. The cash generated from the

project is evaluated on certain circumstances and determine whether the operation will

generate high rate of return from investment.

a. Calculating the Free cash flow of the project:

Particular

s

Year 1 Year 2 Year 3 Year 4 Year 5

Revenue BRL

25,200,000.

00

BRL

26,712,000.

00

BRL

28,314,720.

00

BRL

30,013,603.

20

BRL

31,814,419.

39

Variable

cost

BRL

11,200,000.

00

BRL

11,872,000.

00

BRL

12,584,320.

00

BRL

13,339,379.

20

BRL

14,139,741.

95

Fixed cost BRL

2,000,000.0

0

BRL

2,120,000.0

0

BRL

2,247,200.0

0

BRL

2,382,032.0

0

BRL

2,524,953.9

2

Depreciati

on

facilities

BRL

7,200,000

BRL

7,200,000

BRL

7,200,000

BRL

7,200,000

BRL

7,200,000

Depreciati

on

machine

BRL

3,600,000

BRL

3,600,000

BRL

3,600,000

BRL

3,600,000

BRL

3,600,000

Profit

Before tax

BRL

1,200,000.0

0

BRL

1,920,000.0

0

BRL

2,683,200.0

0

BRL

3,492,192.0

0

BRL

4,349,723.5

2

Tax BRL

300,000.00

BRL

480,000.00

BRL

670,800.00

BRL

873,048.00

BRL

1,087,430.8

4

The assessment is mainly conducted to identify the financial viability of the new project

that will be conducted in the Brazil by the US Company. The calculations are mainly

conduced to understand the expenses and revenue, which is portrayed by the new project. In

addition, the financial performance of the company has mainly evaluated, which could

generate higher return for US company and Brazilian subsidiary. The cash generated from the

project is evaluated on certain circumstances and determine whether the operation will

generate high rate of return from investment.

a. Calculating the Free cash flow of the project:

Particular

s

Year 1 Year 2 Year 3 Year 4 Year 5

Revenue BRL

25,200,000.

00

BRL

26,712,000.

00

BRL

28,314,720.

00

BRL

30,013,603.

20

BRL

31,814,419.

39

Variable

cost

BRL

11,200,000.

00

BRL

11,872,000.

00

BRL

12,584,320.

00

BRL

13,339,379.

20

BRL

14,139,741.

95

Fixed cost BRL

2,000,000.0

0

BRL

2,120,000.0

0

BRL

2,247,200.0

0

BRL

2,382,032.0

0

BRL

2,524,953.9

2

Depreciati

on

facilities

BRL

7,200,000

BRL

7,200,000

BRL

7,200,000

BRL

7,200,000

BRL

7,200,000

Depreciati

on

machine

BRL

3,600,000

BRL

3,600,000

BRL

3,600,000

BRL

3,600,000

BRL

3,600,000

Profit

Before tax

BRL

1,200,000.0

0

BRL

1,920,000.0

0

BRL

2,683,200.0

0

BRL

3,492,192.0

0

BRL

4,349,723.5

2

Tax BRL

300,000.00

BRL

480,000.00

BRL

670,800.00

BRL

873,048.00

BRL

1,087,430.8

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Profit

After tax

BRL

900,000.00

BRL

1,440,000.0

0

BRL

2,012,400.0

0

BRL

2,619,144.0

0

BRL

3,262,292.6

4

Working

capital

BRL

6,000,000.0

0

Salvage

value

facilities

BRL

43,200,000

Cash Flow BRL

11,700,000.

00

BRL

12,240,000.

00

BRL

12,812,400.

00

BRL

13,419,144.

00

BRL

63,262,292.

64

b.(i) Hedging $2 million:

Particulars 0 1 2 3 4 5

PV of

parent cash

flows

2,900,000.

00

3,012,962.

96

2,496,114.

20

2,590,700.

82

4,039,639.

38

Initial

investment

by parent

-

12,600,000.

00

Cumulative

NPV

-

12,600,000.

00

-

9,700,000.

00

-

6,687,037.

04

-

4,190,922.

84

-

1,600,222.

02

2,439,417.

37

NPV 2,439,417.37

b.(ii) Not hedging $2 million

Particular 0 1 2 3 4 5

5

Profit

After tax

BRL

900,000.00

BRL

1,440,000.0

0

BRL

2,012,400.0

0

BRL

2,619,144.0

0

BRL

3,262,292.6

4

Working

capital

BRL

6,000,000.0

0

Salvage

value

facilities

BRL

43,200,000

Cash Flow BRL

11,700,000.

00

BRL

12,240,000.

00

BRL

12,812,400.

00

BRL

13,419,144.

00

BRL

63,262,292.

64

b.(i) Hedging $2 million:

Particulars 0 1 2 3 4 5

PV of

parent cash

flows

2,900,000.

00

3,012,962.

96

2,496,114.

20

2,590,700.

82

4,039,639.

38

Initial

investment

by parent

-

12,600,000.

00

Cumulative

NPV

-

12,600,000.

00

-

9,700,000.

00

-

6,687,037.

04

-

4,190,922.

84

-

1,600,222.

02

2,439,417.

37

NPV 2,439,417.37

b.(ii) Not hedging $2 million

Particular 0 1 2 3 4 5

5

s

PV of

parent

cash flows

2,900,000.

00

2,635,185.

19

2,396,032.

58

2,179,891.

18

3,132,148.

59

Initial

investment

by parent

-

12,600,000.

00

Cumulativ

e NPV

-

12,600,000.

00

-

9,700,000.

00

-

7,064,814.

81

-

4,668,782.

24

-

2,488,891.

05

643,257.54

NPV 643,257.54

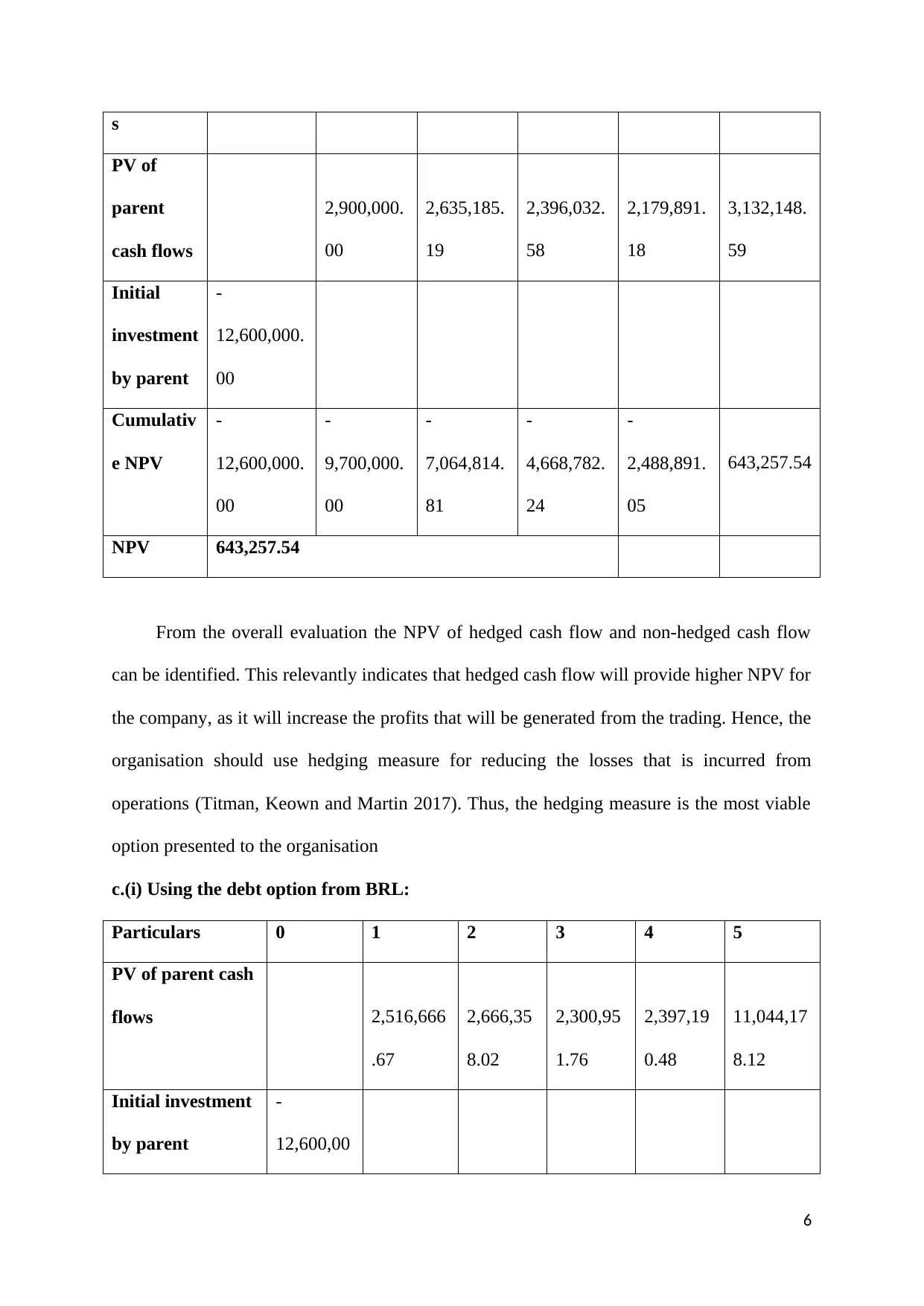

From the overall evaluation the NPV of hedged cash flow and non-hedged cash flow

can be identified. This relevantly indicates that hedged cash flow will provide higher NPV for

the company, as it will increase the profits that will be generated from the trading. Hence, the

organisation should use hedging measure for reducing the losses that is incurred from

operations (Titman, Keown and Martin 2017). Thus, the hedging measure is the most viable

option presented to the organisation

c.(i) Using the debt option from BRL:

Particulars 0 1 2 3 4 5

PV of parent cash

flows 2,516,666

.67

2,666,35

8.02

2,300,95

1.76

2,397,19

0.48

11,044,17

8.12

Initial investment

by parent

-

12,600,00

6

PV of

parent

cash flows

2,900,000.

00

2,635,185.

19

2,396,032.

58

2,179,891.

18

3,132,148.

59

Initial

investment

by parent

-

12,600,000.

00

Cumulativ

e NPV

-

12,600,000.

00

-

9,700,000.

00

-

7,064,814.

81

-

4,668,782.

24

-

2,488,891.

05

643,257.54

NPV 643,257.54

From the overall evaluation the NPV of hedged cash flow and non-hedged cash flow

can be identified. This relevantly indicates that hedged cash flow will provide higher NPV for

the company, as it will increase the profits that will be generated from the trading. Hence, the

organisation should use hedging measure for reducing the losses that is incurred from

operations (Titman, Keown and Martin 2017). Thus, the hedging measure is the most viable

option presented to the organisation

c.(i) Using the debt option from BRL:

Particulars 0 1 2 3 4 5

PV of parent cash

flows 2,516,666

.67

2,666,35

8.02

2,300,95

1.76

2,397,19

0.48

11,044,17

8.12

Initial investment

by parent

-

12,600,00

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0.00

Cumulative NPV -

12,600,00

0.00

-

10,083,33

3.33

-

7,416,97

5.31

-

5,116,02

3.55

-

2,718,83

3.07

8,325,345

.06

NPV

8,325,345

.06

c.(ii) Using the debt option from US:

Particulars 0 1 2 3 4 5

PV of

parent cash

flows

2,900,000.

00

3,012,962.

96

2,496,114.

20

2,590,700.

82

4,039,639.

38

Initial

investment

by parent

-

12,600,000.

00

Cumulative

NPV

-

12,600,000.

00

-

9,700,000.

00

-

6,687,037.

04

-

4,190,922.

84

-

1,600,222.

02

2,439,417.

37

NPV 2,439,417.37

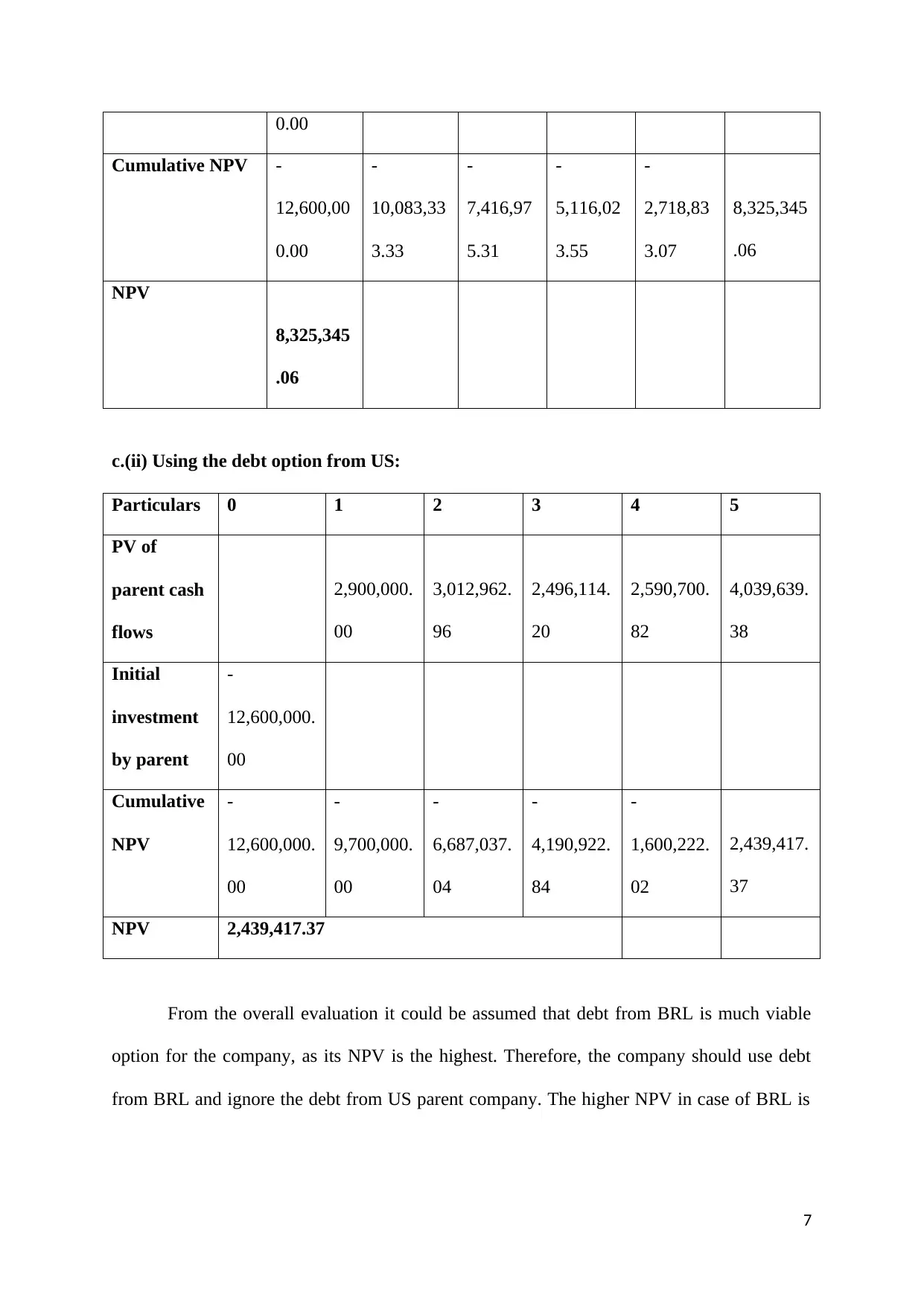

From the overall evaluation it could be assumed that debt from BRL is much viable

option for the company, as its NPV is the highest. Therefore, the company should use debt

from BRL and ignore the debt from US parent company. The higher NPV in case of BRL is

7

Cumulative NPV -

12,600,00

0.00

-

10,083,33

3.33

-

7,416,97

5.31

-

5,116,02

3.55

-

2,718,83

3.07

8,325,345

.06

NPV

8,325,345

.06

c.(ii) Using the debt option from US:

Particulars 0 1 2 3 4 5

PV of

parent cash

flows

2,900,000.

00

3,012,962.

96

2,496,114.

20

2,590,700.

82

4,039,639.

38

Initial

investment

by parent

-

12,600,000.

00

Cumulative

NPV

-

12,600,000.

00

-

9,700,000.

00

-

6,687,037.

04

-

4,190,922.

84

-

1,600,222.

02

2,439,417.

37

NPV 2,439,417.37

From the overall evaluation it could be assumed that debt from BRL is much viable

option for the company, as its NPV is the highest. Therefore, the company should use debt

from BRL and ignore the debt from US parent company. The higher NPV in case of BRL is

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

only obtained due to the low tax paid by the subsidiary in their home country for conducting

operating of the project (Hamilton and Webster 2015).

d. Factors driving the difference between two factors:

The use of stock issue can be conducted by the form in US and Brazil for raising the

required level of capital, which could support the financial requirements of the project. In

addition, conducting a share issue in Brazil the company needs to register in the stock market

and there is a long process, where the stock would receive the required capital from the issue.

Moreover, the second factor that is involved in the share issue is listing the parent company

in the Brazil without which the adequate capital from the stock market cannot be raised by

the company. The factor such as risk-free rate, market return and risk of the company also

needs to be evaluated before the listing and issue that could be conducted by the parent

company in Brazil. However, the issue could be conducted in US, where the parent company

actually exists, which might help in generating the required level capital from the issue

(Meyer and Peng 2016). The beta of the company is well determined, as it is present in US,

which might help in generating the required level of capital for the proposed project.

Therefore, the capital issue in US might help in generating the required money without

incurring extra cost of listing in Brazilian market. The conversion rate might also be an

adequate factor, which night help in supporting the project. The risk-free interest rate of US is

mainly at the level of 3%, while the interest rate of Brazil is detected at 7%, which relatively

reduces the expected return of stocks listed in US. Hence, the issue conducted by the parent

company in US might help in reducing the cost of equity and improve Weighted average cost

of capital (Shenkar, Luo and Chi 2014). Therefore, the difference in factors relevantly

indicates that the parent company should issue shares in US, as it might help in generating

adequate capital for the project.

8

operating of the project (Hamilton and Webster 2015).

d. Factors driving the difference between two factors:

The use of stock issue can be conducted by the form in US and Brazil for raising the

required level of capital, which could support the financial requirements of the project. In

addition, conducting a share issue in Brazil the company needs to register in the stock market

and there is a long process, where the stock would receive the required capital from the issue.

Moreover, the second factor that is involved in the share issue is listing the parent company

in the Brazil without which the adequate capital from the stock market cannot be raised by

the company. The factor such as risk-free rate, market return and risk of the company also

needs to be evaluated before the listing and issue that could be conducted by the parent

company in Brazil. However, the issue could be conducted in US, where the parent company

actually exists, which might help in generating the required level capital from the issue

(Meyer and Peng 2016). The beta of the company is well determined, as it is present in US,

which might help in generating the required level of capital for the proposed project.

Therefore, the capital issue in US might help in generating the required money without

incurring extra cost of listing in Brazilian market. The conversion rate might also be an

adequate factor, which night help in supporting the project. The risk-free interest rate of US is

mainly at the level of 3%, while the interest rate of Brazil is detected at 7%, which relatively

reduces the expected return of stocks listed in US. Hence, the issue conducted by the parent

company in US might help in reducing the cost of equity and improve Weighted average cost

of capital (Shenkar, Luo and Chi 2014). Therefore, the difference in factors relevantly

indicates that the parent company should issue shares in US, as it might help in generating

adequate capital for the project.

8

e. Impact of financial crisis on the project:

The negative impact of financial crisis will directly affect the operational capability of

the project and reduce the demand from customers. In addition, the crisis would also have a

negative impact on exchange currency of USD and Brazil, which might directly affect the

revenue received by parent company in US. Moreover, the financial performance might

directly have a negative impact on currency valuation, as the volatility in the capital market

could erode the revenue and capability of the company to operate in the competitive market

(Yugendhar and Ali 2017). The decline in demand of sunscreens could increase due to the

negative impact of the financial crisis, as it might hamper consumer power all around the

world, which reduces their ability to spend money in luxury market. The negative impact of

the crisis will directly affect currency valuation of USD and BRL, where it might hamper the

revenue collected by the US parent.

Moreover, the shortage of funds at the subsidiary could be overcome by reducing the

expense conducted on operations. The declining demand of sunscreens in Brazil could be

supported by reducing the production level of the company (Antras and Foley 2015). In

addition, the financial performance of the company could be reduced by ongoing financial

crisis, which could be supported by decreasing its financial expenses. The reduction in

expenses and laying down the number of employees would eventually help in reducing the

overhead cost incurred by the company. This measure could eventually help the company to

support the shortfall in relevant funds that is needed for the company’s survival during the

financial crisis (Perlmutter 2017).

Conclusion and recommendation:

The assessment mainly indicates the financial viability of the proposed project, which

will be stared in Brazil by the US parent. In addition, the calculation relevantly indicates the

financial stability of the project in generating high returns from investment, which is detected

9

The negative impact of financial crisis will directly affect the operational capability of

the project and reduce the demand from customers. In addition, the crisis would also have a

negative impact on exchange currency of USD and Brazil, which might directly affect the

revenue received by parent company in US. Moreover, the financial performance might

directly have a negative impact on currency valuation, as the volatility in the capital market

could erode the revenue and capability of the company to operate in the competitive market

(Yugendhar and Ali 2017). The decline in demand of sunscreens could increase due to the

negative impact of the financial crisis, as it might hamper consumer power all around the

world, which reduces their ability to spend money in luxury market. The negative impact of

the crisis will directly affect currency valuation of USD and BRL, where it might hamper the

revenue collected by the US parent.

Moreover, the shortage of funds at the subsidiary could be overcome by reducing the

expense conducted on operations. The declining demand of sunscreens in Brazil could be

supported by reducing the production level of the company (Antras and Foley 2015). In

addition, the financial performance of the company could be reduced by ongoing financial

crisis, which could be supported by decreasing its financial expenses. The reduction in

expenses and laying down the number of employees would eventually help in reducing the

overhead cost incurred by the company. This measure could eventually help the company to

support the shortfall in relevant funds that is needed for the company’s survival during the

financial crisis (Perlmutter 2017).

Conclusion and recommendation:

The assessment mainly indicates the financial viability of the proposed project, which

will be stared in Brazil by the US parent. In addition, the calculation relevantly indicates the

financial stability of the project in generating high returns from investment, which is detected

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the calculation NPV. Moreover, the evaluation of the project conducted under difference

circumstance and currency rate also depict the financial viability of the project. Hence, it is

recommended for the management to approve the project on certain circumstance. The debt

finance will be conducted by the Brazilian subsidiary and not the US parent. Furthermore, the

forward rate and hedging process also needs to be conducted by the company to minimise the

negative impact from currency volatility and generate high returns from investment.

Reference and Bibliography list

Allen, F., Armour, J., Balling, M., Belchambers, A., Danielsson, J., Gnan, E., Grant, C.,

Haben, P., Jackson, P., Macrae, R. and Micheler, E., 2017. Central banking and monetary

policy: Which will be the post-crisis new normal?. SUERF Studies.

Antras, P. and Foley, C.F., 2015. Poultry in motion: a study of international trade finance

practices. Journal of Political Economy, 123(4), pp.853-901.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Buckley, P., 2017. International business. Routledge.

Cavusgil, S.T., Knight, G., Riesenberger, J.R., Rammal, H.G. and Rose, E.L.,

2014. International business. Pearson Australia.

Cravino, J. and Levchenko, A.A., 2016. Multinational firms and international business cycle

transmission. The Quarterly Journal of Economics, 132(2), pp.921-962.

Cumming, D., Filatotchev, I., Knill, A., Reeb, D.M. and Senbet, L., 2017. Law, finance, and

the international mobility of corporate governance.

Demirovic, A., Tucker, J. and Guermat, C., 2015. Research in International Business and

Finance.

Disch, L., 2016. Representation. In The Oxford Handbook of Feminist Theory.

10

circumstance and currency rate also depict the financial viability of the project. Hence, it is

recommended for the management to approve the project on certain circumstance. The debt

finance will be conducted by the Brazilian subsidiary and not the US parent. Furthermore, the

forward rate and hedging process also needs to be conducted by the company to minimise the

negative impact from currency volatility and generate high returns from investment.

Reference and Bibliography list

Allen, F., Armour, J., Balling, M., Belchambers, A., Danielsson, J., Gnan, E., Grant, C.,

Haben, P., Jackson, P., Macrae, R. and Micheler, E., 2017. Central banking and monetary

policy: Which will be the post-crisis new normal?. SUERF Studies.

Antras, P. and Foley, C.F., 2015. Poultry in motion: a study of international trade finance

practices. Journal of Political Economy, 123(4), pp.853-901.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Buckley, P., 2017. International business. Routledge.

Cavusgil, S.T., Knight, G., Riesenberger, J.R., Rammal, H.G. and Rose, E.L.,

2014. International business. Pearson Australia.

Cravino, J. and Levchenko, A.A., 2016. Multinational firms and international business cycle

transmission. The Quarterly Journal of Economics, 132(2), pp.921-962.

Cumming, D., Filatotchev, I., Knill, A., Reeb, D.M. and Senbet, L., 2017. Law, finance, and

the international mobility of corporate governance.

Demirovic, A., Tucker, J. and Guermat, C., 2015. Research in International Business and

Finance.

Disch, L., 2016. Representation. In The Oxford Handbook of Feminist Theory.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ferreira, M.P., Santos, J.C., de Almeida, M.I.R. and Reis, N.R., 2014. Mergers & acquisitions

research: A bibliometric study of top strategy and international business journals, 1980–

2010. Journal of Business Research, 67(12), pp.2550-2558.

Forsgren, M. and Johanson, J., 2014. Managing networks in international business.

Routledge.

Hamilton, L. and Webster, P., 2015. The international business environment. Oxford

University Press, USA.

Kraemer-Eis, H., Botsari, A., Gvetadze, S., Lang, F. and Torfs, W., 2017. European Small

Business Finance Outlook: December 2017 (No. 2017/46). EIF Working Paper.

Li, X., 2015. Accounting conservatism and the cost of capital: An international

analysis. Journal of Business Finance & Accounting, 42(5-6), pp.555-582.

Meyer, K. and Peng, M.W., 2016. International business. Cengage Learning.

Montinari, L. and Stracca, L., 2016. Trade, finance or policies: What drives the cross-border

spill-over of business cycles?. Journal of Macroeconomics, 49, pp.131-148.

Perlmutter, H.V., 2017. The tortuous evolution of the multinational corporation.

In International Business (pp. 117-126). Routledge.

Rothonis, S., Tran, D. and Wu, E., 2015. Research in International Business and Finance.

Shenkar, O., Luo, Y. and Chi, T., 2014. International business. Routledge.

Tian, X., 2016. Managing international business in China. Cambridge University Press.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Yugendhar, A. and Ali, S.M., 2017. International Business, Finance and Accounting A

Comprehensive Study on Corporate Governance in an International Context. International

Journal of Engineering and Management Research (IJEMR), 7(5), pp.172-177.

11

research: A bibliometric study of top strategy and international business journals, 1980–

2010. Journal of Business Research, 67(12), pp.2550-2558.

Forsgren, M. and Johanson, J., 2014. Managing networks in international business.

Routledge.

Hamilton, L. and Webster, P., 2015. The international business environment. Oxford

University Press, USA.

Kraemer-Eis, H., Botsari, A., Gvetadze, S., Lang, F. and Torfs, W., 2017. European Small

Business Finance Outlook: December 2017 (No. 2017/46). EIF Working Paper.

Li, X., 2015. Accounting conservatism and the cost of capital: An international

analysis. Journal of Business Finance & Accounting, 42(5-6), pp.555-582.

Meyer, K. and Peng, M.W., 2016. International business. Cengage Learning.

Montinari, L. and Stracca, L., 2016. Trade, finance or policies: What drives the cross-border

spill-over of business cycles?. Journal of Macroeconomics, 49, pp.131-148.

Perlmutter, H.V., 2017. The tortuous evolution of the multinational corporation.

In International Business (pp. 117-126). Routledge.

Rothonis, S., Tran, D. and Wu, E., 2015. Research in International Business and Finance.

Shenkar, O., Luo, Y. and Chi, T., 2014. International business. Routledge.

Tian, X., 2016. Managing international business in China. Cambridge University Press.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Yugendhar, A. and Ali, S.M., 2017. International Business, Finance and Accounting A

Comprehensive Study on Corporate Governance in an International Context. International

Journal of Engineering and Management Research (IJEMR), 7(5), pp.172-177.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.