Management Accounting (ACC202) Report: Flying Airline Analysis

VerifiedAdded on 2020/05/16

|12

|2948

|100

Report

AI Summary

This management accounting report (ACC202) analyzes the financial viability of Flying Airline Company, evaluating three key situations. The first situation assesses the cost implications of replacing an old loader truck with a new one, using differential cost analysis to determine the financial benefits. The second situation compares the profitability of non-stop and one-stop flight routes, considering revenue, costs, and differential costs. The report highlights the importance of economic and operational factors in decision-making. The third situation examines the financial viability of a special tourist charter flight proposal, calculating profitability under both normal circumstances and when spare capacity is available. The report uses calculations to determine the best course of action for the airline, emphasizing cost reduction and profit maximization strategies. The report provides comprehensive financial analysis to aid in management decisions, using relevant calculations and citing academic sources.

Running head: MANAGEMENT ACCOUNTING (ACC 202)

Management Accounting (ACC 202)

Name of the Student:

Name of the University:

Authors Note:

Management Accounting (ACC 202)

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING (ACC 202)

1

Table of Contents

Situation 1 (Identifying the financial viability of replacing old loader truck with new loader

truck):.........................................................................................................................................2

Detecting the financial viability of old and new loader truck with relevant calculations

conducted for Flying Airline Company:....................................................................................2

Situation 2 (Calculating financial viability of flight route for Flying Airline Company):.........4

A) Detecting non-stop route and one-stop route financial viability by conducting adequate

calculation:.................................................................................................................................4

B) Evaluating other factors, which needs to be evaluated before conducting any decision for

Flying Airline Company:...........................................................................................................7

Situation 3 (Stating viability of the new special tourist charter flight proposal presented to

Flying Airline Company):..........................................................................................................8

A) Stating the calculations needed by Flying Airline Compony to accept the special tourist

charter proposal when adequate spare capacity is present:........................................................8

B) Mentioning the viability of the new proposal with adequate calculation when there is no

space available to Flying Airline Company:............................................................................10

Reference and Bibliography:....................................................................................................12

1

Table of Contents

Situation 1 (Identifying the financial viability of replacing old loader truck with new loader

truck):.........................................................................................................................................2

Detecting the financial viability of old and new loader truck with relevant calculations

conducted for Flying Airline Company:....................................................................................2

Situation 2 (Calculating financial viability of flight route for Flying Airline Company):.........4

A) Detecting non-stop route and one-stop route financial viability by conducting adequate

calculation:.................................................................................................................................4

B) Evaluating other factors, which needs to be evaluated before conducting any decision for

Flying Airline Company:...........................................................................................................7

Situation 3 (Stating viability of the new special tourist charter flight proposal presented to

Flying Airline Company):..........................................................................................................8

A) Stating the calculations needed by Flying Airline Compony to accept the special tourist

charter proposal when adequate spare capacity is present:........................................................8

B) Mentioning the viability of the new proposal with adequate calculation when there is no

space available to Flying Airline Company:............................................................................10

Reference and Bibliography:....................................................................................................12

MANAGEMENT ACCOUNTING (ACC 202)

2

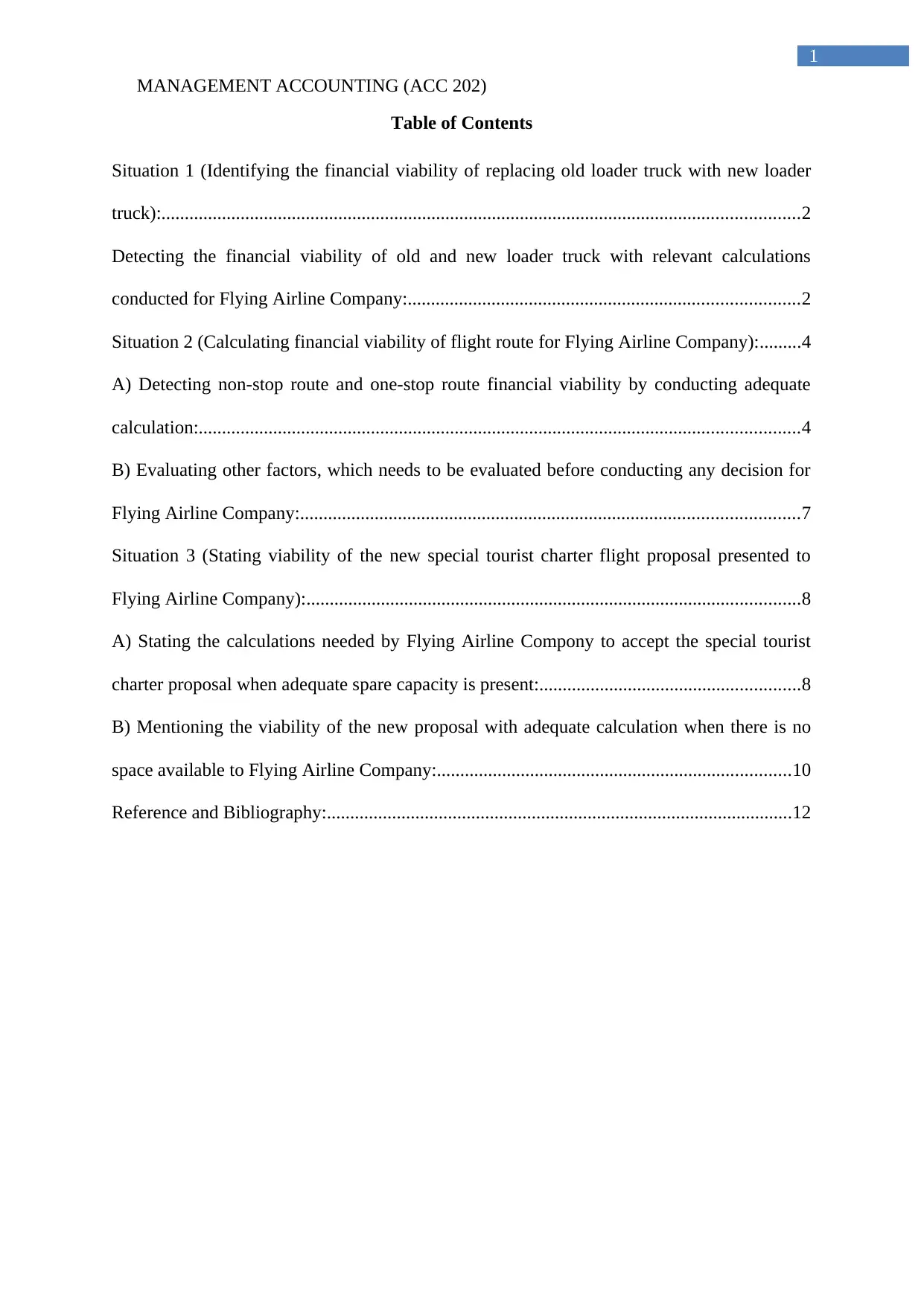

Situation 1 (Identifying the financial viability of replacing old loader truck with new

loader truck):

Detecting the financial viability of old and new loader truck with relevant calculations

conducted for Flying Airline Company:

Situation 1 (Not replacing Old loader)

Particulars Amount

Depreciation for old loader $ 25,000.00

Write off for old loader $ 0.00

Proceeds from sale of old loader $ 0.00

Depreciation for new loader $ 0.00

Operating costs involved for old loader $ 80,000.00

Total Operating cost $ 105,000.00

The calculation that is conducted in the above table mainly helps in identifying the

overall operating cost incurred by Flying Airline Compony, when old loader truck is used in

its operations. The total operating cost mainly amounts to $105,000, which includes

depreciation and operating cost involved for the old loader. This relevant calculation of cost

incurred from equipment allows the management to take adequate decision for cutting its cost

and increase their profitability. Cannon (2014) mentioned that with the evaluation of cost

analysis management can detect actual cost incurred by its operations, which helps in making

adequate management decision.

Situation 1 (Replacing Old loader)

Particulars Amount

Depreciation for old loader $ 0.00

2

Situation 1 (Identifying the financial viability of replacing old loader truck with new

loader truck):

Detecting the financial viability of old and new loader truck with relevant calculations

conducted for Flying Airline Company:

Situation 1 (Not replacing Old loader)

Particulars Amount

Depreciation for old loader $ 25,000.00

Write off for old loader $ 0.00

Proceeds from sale of old loader $ 0.00

Depreciation for new loader $ 0.00

Operating costs involved for old loader $ 80,000.00

Total Operating cost $ 105,000.00

The calculation that is conducted in the above table mainly helps in identifying the

overall operating cost incurred by Flying Airline Compony, when old loader truck is used in

its operations. The total operating cost mainly amounts to $105,000, which includes

depreciation and operating cost involved for the old loader. This relevant calculation of cost

incurred from equipment allows the management to take adequate decision for cutting its cost

and increase their profitability. Cannon (2014) mentioned that with the evaluation of cost

analysis management can detect actual cost incurred by its operations, which helps in making

adequate management decision.

Situation 1 (Replacing Old loader)

Particulars Amount

Depreciation for old loader $ 0.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING (ACC 202)

3

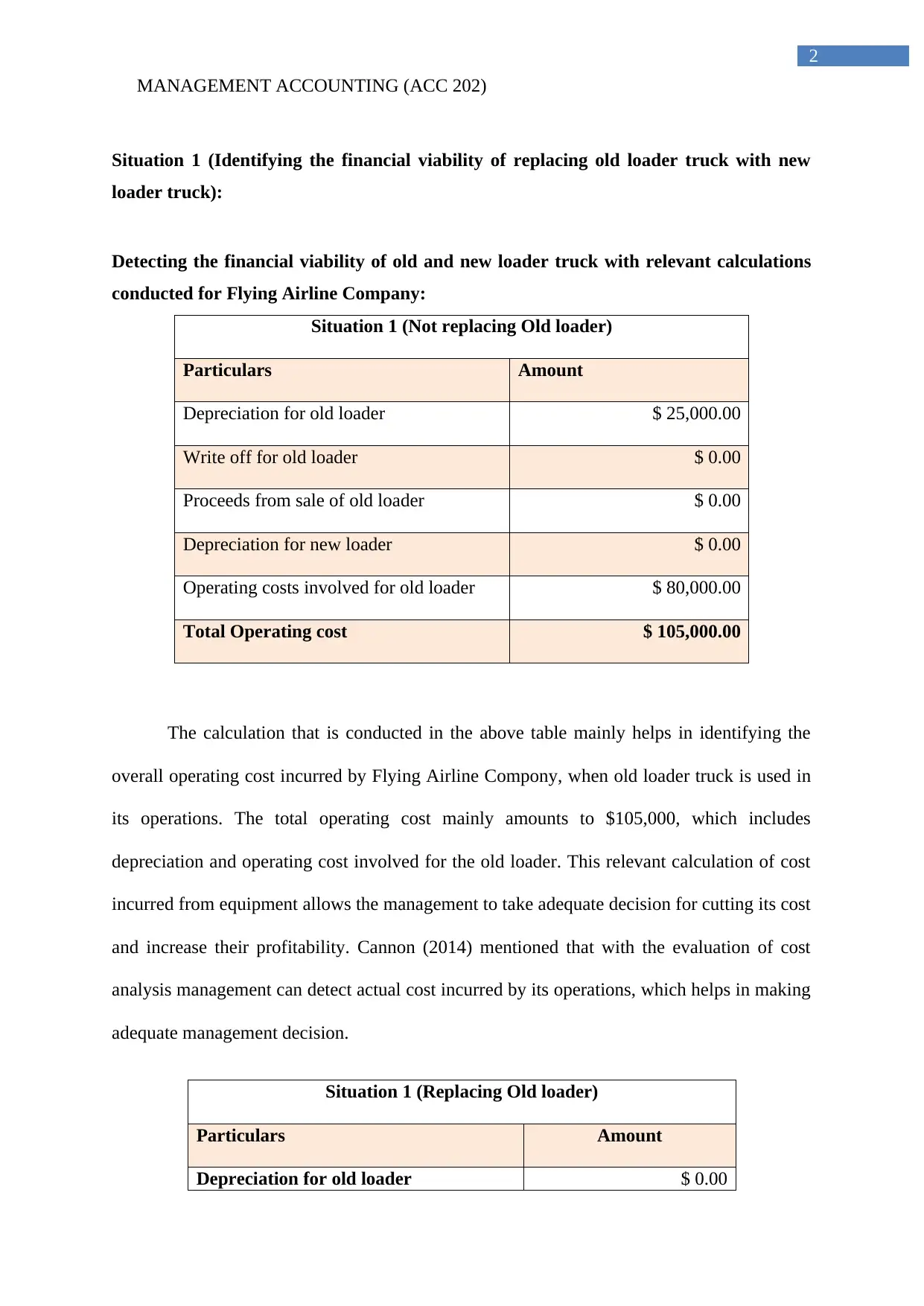

Write off for old loader $ 25,000.00

Proceeds from sale of old loader $ (5,000.00)

Depreciation for new loader $ 20,000.00

Operating costs involved for old loader $ 50,000.00

Total Operating cost $ 90,000.00

The table mainly represent the overall cost if the old loader is replaced with the new

loader truck. Relevant reduction in operating cost is detected from operations, which could

eventually help the management of Flying Airline Company to take adequate cost decision.

The decline operation cost mainly declined from the value of $105,000 to $90,000, which is

relevantly a profit of $15,000 identified from the implementation of new loader truck. The

company with the help of cost analysis can detect financial enhancement, which is attained

from the implementation of the new loader. On the other hand, Collier (2015) argued that

viability of cost analysis mainly reduces when adequate research is not conducted by the

management on cost. The relevant reduction of cost is detected from the sale proceeds of the

old loader, which cannot continue in next year. Hence, from second year the overall operation

cost will be at the level of $95,000, which is relatively lower from the current expenses

incurred by the company.

Situation 1 (Differential cost)

Particulars Amount

Depreciation for old loader $ 0.00

Write off for old loader $ 0.00

Proceeds from sale of old loader $ 5,000.00

3

Write off for old loader $ 25,000.00

Proceeds from sale of old loader $ (5,000.00)

Depreciation for new loader $ 20,000.00

Operating costs involved for old loader $ 50,000.00

Total Operating cost $ 90,000.00

The table mainly represent the overall cost if the old loader is replaced with the new

loader truck. Relevant reduction in operating cost is detected from operations, which could

eventually help the management of Flying Airline Company to take adequate cost decision.

The decline operation cost mainly declined from the value of $105,000 to $90,000, which is

relevantly a profit of $15,000 identified from the implementation of new loader truck. The

company with the help of cost analysis can detect financial enhancement, which is attained

from the implementation of the new loader. On the other hand, Collier (2015) argued that

viability of cost analysis mainly reduces when adequate research is not conducted by the

management on cost. The relevant reduction of cost is detected from the sale proceeds of the

old loader, which cannot continue in next year. Hence, from second year the overall operation

cost will be at the level of $95,000, which is relatively lower from the current expenses

incurred by the company.

Situation 1 (Differential cost)

Particulars Amount

Depreciation for old loader $ 0.00

Write off for old loader $ 0.00

Proceeds from sale of old loader $ 5,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING (ACC 202)

4

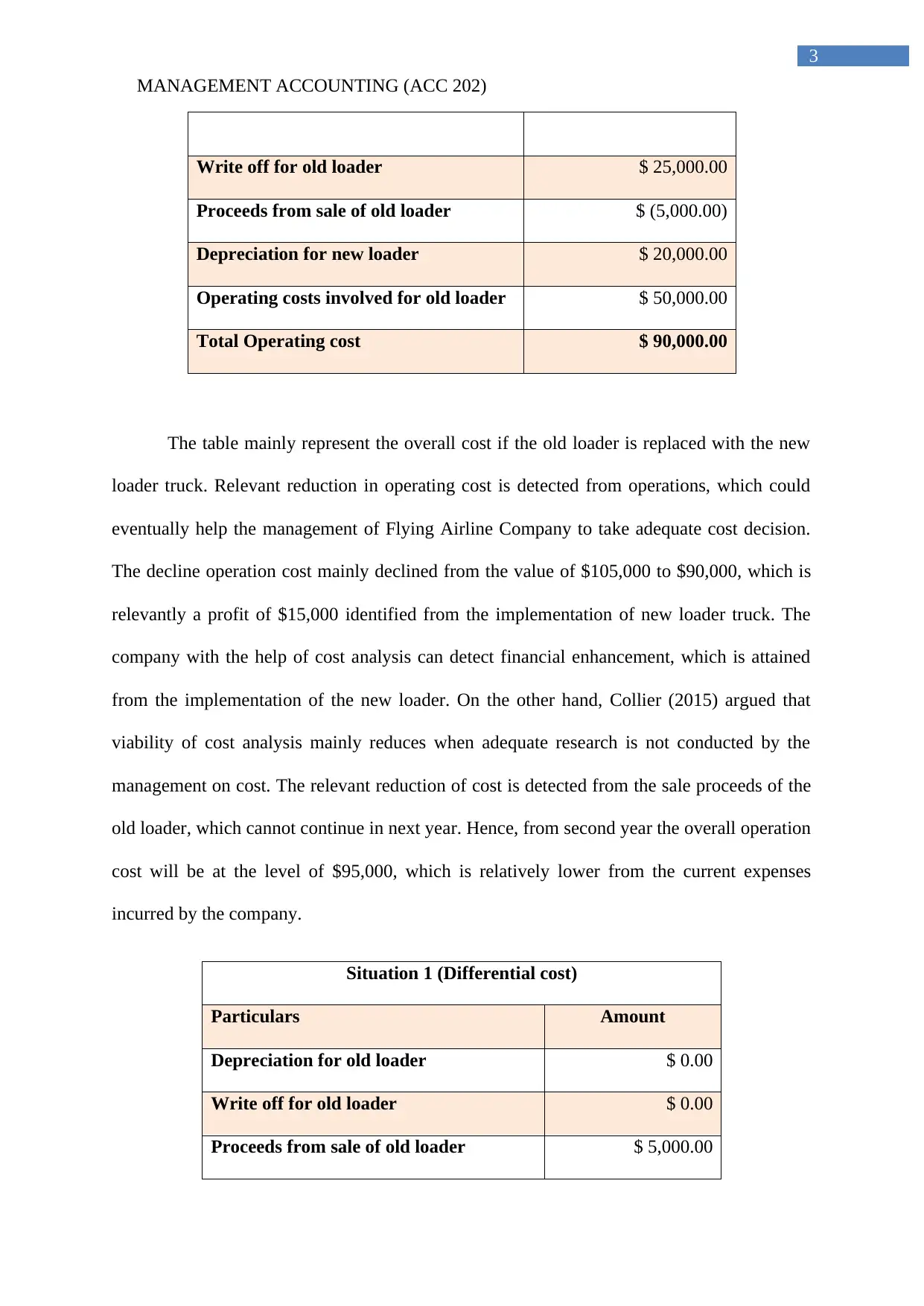

Depreciation for new loader $ (20,000.00)

Operating costs involved for old loader $ 30,000.00

Total Operating cost $ 15,000.00

The differential calculation conducted in the above table mainly helps in

understanding the overall cost savings, which could be conducted by Flying Airline Company

after implementing the new loader truck in its operations. The overall differential cost

analysis mainly indicates total difference in operating cost by $15,000, which is obtained by

the company if new loader is implemented. The difference in actual operation cost between

old and new loader can be detected from the above calculation, which amounts to $30,000.

Hence, the implementation of new loader truck could eventually allow the company to attain

higher profits, due to reduction in its operating cost. In this context, D'Onza, Greco and

Allegrini (2016) mentioned that management with the evaluation of differential cost can

detect financial improvement, which could improve their cash inflow and reduce cash

outflow. Therefore, Flying Airline Company could adequately use the new loader truck, as it

helps in reducing operating cost, which in turn improves its profit generation capacity.

Situation 2 (Calculating financial viability of flight route for Flying Airline Company):

A) Detecting non-stop route and one-stop route financial viability by conducting

adequate calculation:

Situation 2 (Non-Stop Route)

Particulars Amount

Revenue from passenger $ 240,000.00

Revenue from Cargo $ 80,000.00

San Francisco (landing fees) $ 0.00

4

Depreciation for new loader $ (20,000.00)

Operating costs involved for old loader $ 30,000.00

Total Operating cost $ 15,000.00

The differential calculation conducted in the above table mainly helps in

understanding the overall cost savings, which could be conducted by Flying Airline Company

after implementing the new loader truck in its operations. The overall differential cost

analysis mainly indicates total difference in operating cost by $15,000, which is obtained by

the company if new loader is implemented. The difference in actual operation cost between

old and new loader can be detected from the above calculation, which amounts to $30,000.

Hence, the implementation of new loader truck could eventually allow the company to attain

higher profits, due to reduction in its operating cost. In this context, D'Onza, Greco and

Allegrini (2016) mentioned that management with the evaluation of differential cost can

detect financial improvement, which could improve their cash inflow and reduce cash

outflow. Therefore, Flying Airline Company could adequately use the new loader truck, as it

helps in reducing operating cost, which in turn improves its profit generation capacity.

Situation 2 (Calculating financial viability of flight route for Flying Airline Company):

A) Detecting non-stop route and one-stop route financial viability by conducting

adequate calculation:

Situation 2 (Non-Stop Route)

Particulars Amount

Revenue from passenger $ 240,000.00

Revenue from Cargo $ 80,000.00

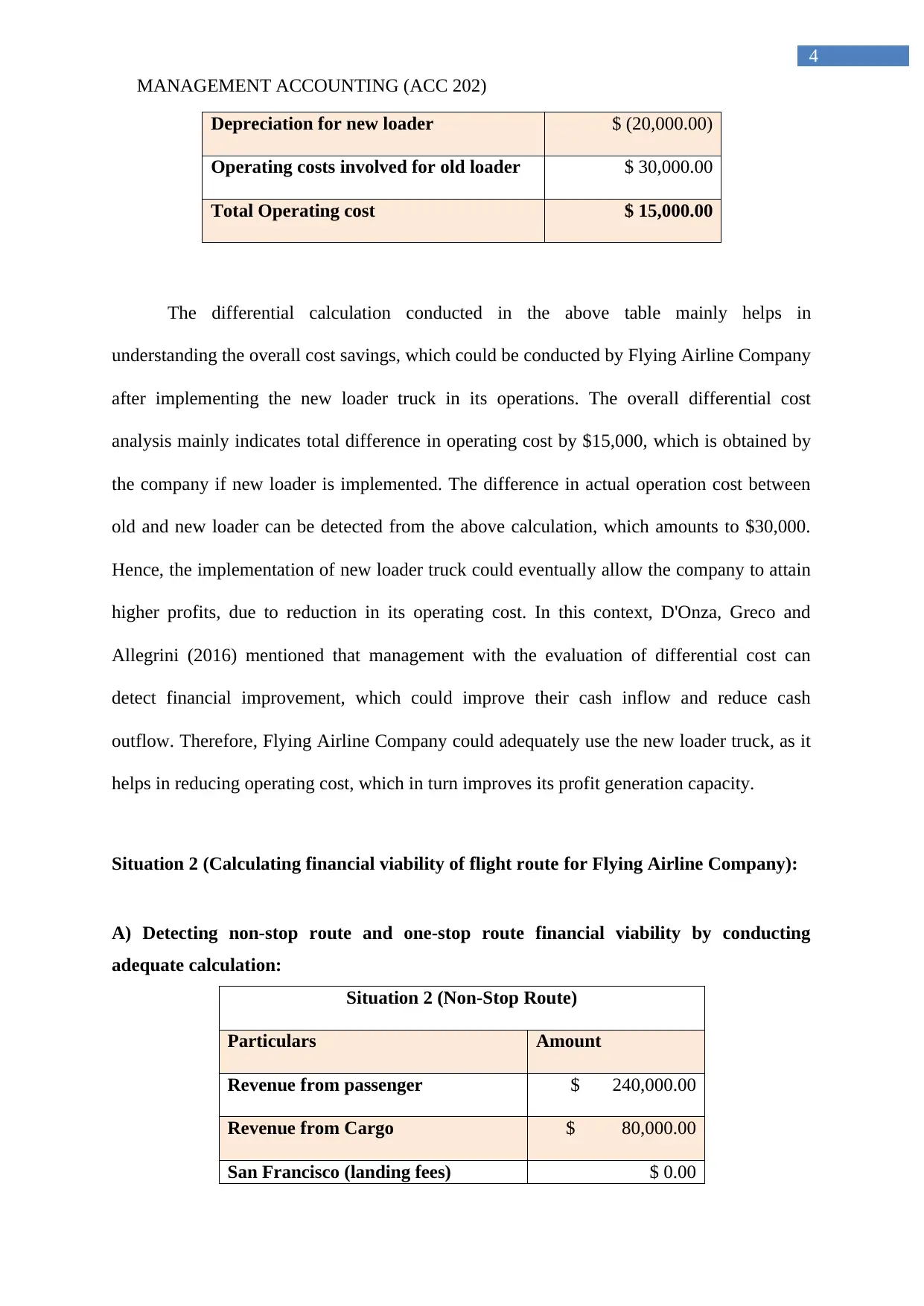

San Francisco (landing fees) $ 0.00

MANAGEMENT ACCOUNTING (ACC 202)

5

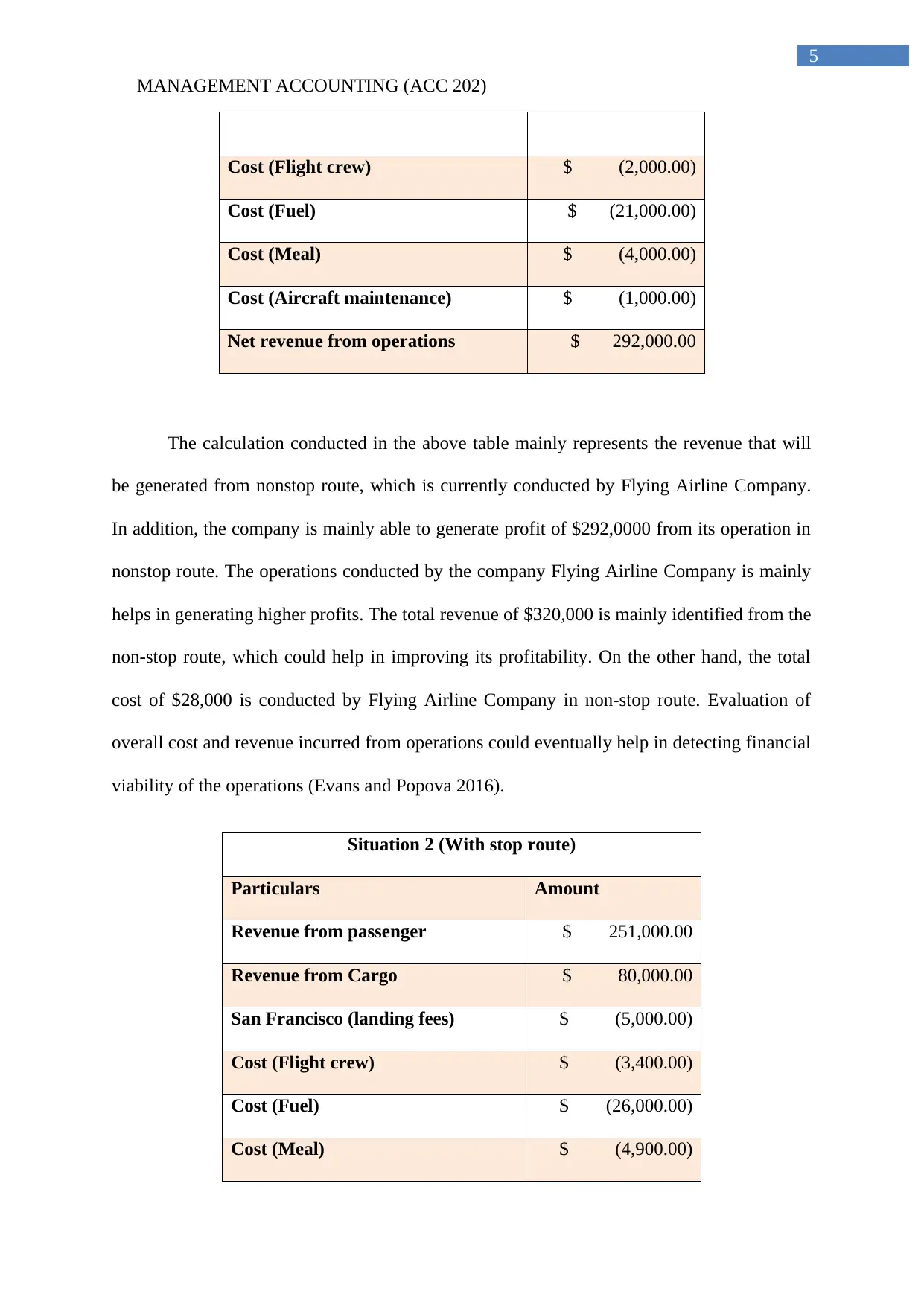

Cost (Flight crew) $ (2,000.00)

Cost (Fuel) $ (21,000.00)

Cost (Meal) $ (4,000.00)

Cost (Aircraft maintenance) $ (1,000.00)

Net revenue from operations $ 292,000.00

The calculation conducted in the above table mainly represents the revenue that will

be generated from nonstop route, which is currently conducted by Flying Airline Company.

In addition, the company is mainly able to generate profit of $292,0000 from its operation in

nonstop route. The operations conducted by the company Flying Airline Company is mainly

helps in generating higher profits. The total revenue of $320,000 is mainly identified from the

non-stop route, which could help in improving its profitability. On the other hand, the total

cost of $28,000 is conducted by Flying Airline Company in non-stop route. Evaluation of

overall cost and revenue incurred from operations could eventually help in detecting financial

viability of the operations (Evans and Popova 2016).

Situation 2 (With stop route)

Particulars Amount

Revenue from passenger $ 251,000.00

Revenue from Cargo $ 80,000.00

San Francisco (landing fees) $ (5,000.00)

Cost (Flight crew) $ (3,400.00)

Cost (Fuel) $ (26,000.00)

Cost (Meal) $ (4,900.00)

5

Cost (Flight crew) $ (2,000.00)

Cost (Fuel) $ (21,000.00)

Cost (Meal) $ (4,000.00)

Cost (Aircraft maintenance) $ (1,000.00)

Net revenue from operations $ 292,000.00

The calculation conducted in the above table mainly represents the revenue that will

be generated from nonstop route, which is currently conducted by Flying Airline Company.

In addition, the company is mainly able to generate profit of $292,0000 from its operation in

nonstop route. The operations conducted by the company Flying Airline Company is mainly

helps in generating higher profits. The total revenue of $320,000 is mainly identified from the

non-stop route, which could help in improving its profitability. On the other hand, the total

cost of $28,000 is conducted by Flying Airline Company in non-stop route. Evaluation of

overall cost and revenue incurred from operations could eventually help in detecting financial

viability of the operations (Evans and Popova 2016).

Situation 2 (With stop route)

Particulars Amount

Revenue from passenger $ 251,000.00

Revenue from Cargo $ 80,000.00

San Francisco (landing fees) $ (5,000.00)

Cost (Flight crew) $ (3,400.00)

Cost (Fuel) $ (26,000.00)

Cost (Meal) $ (4,900.00)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING (ACC 202)

6

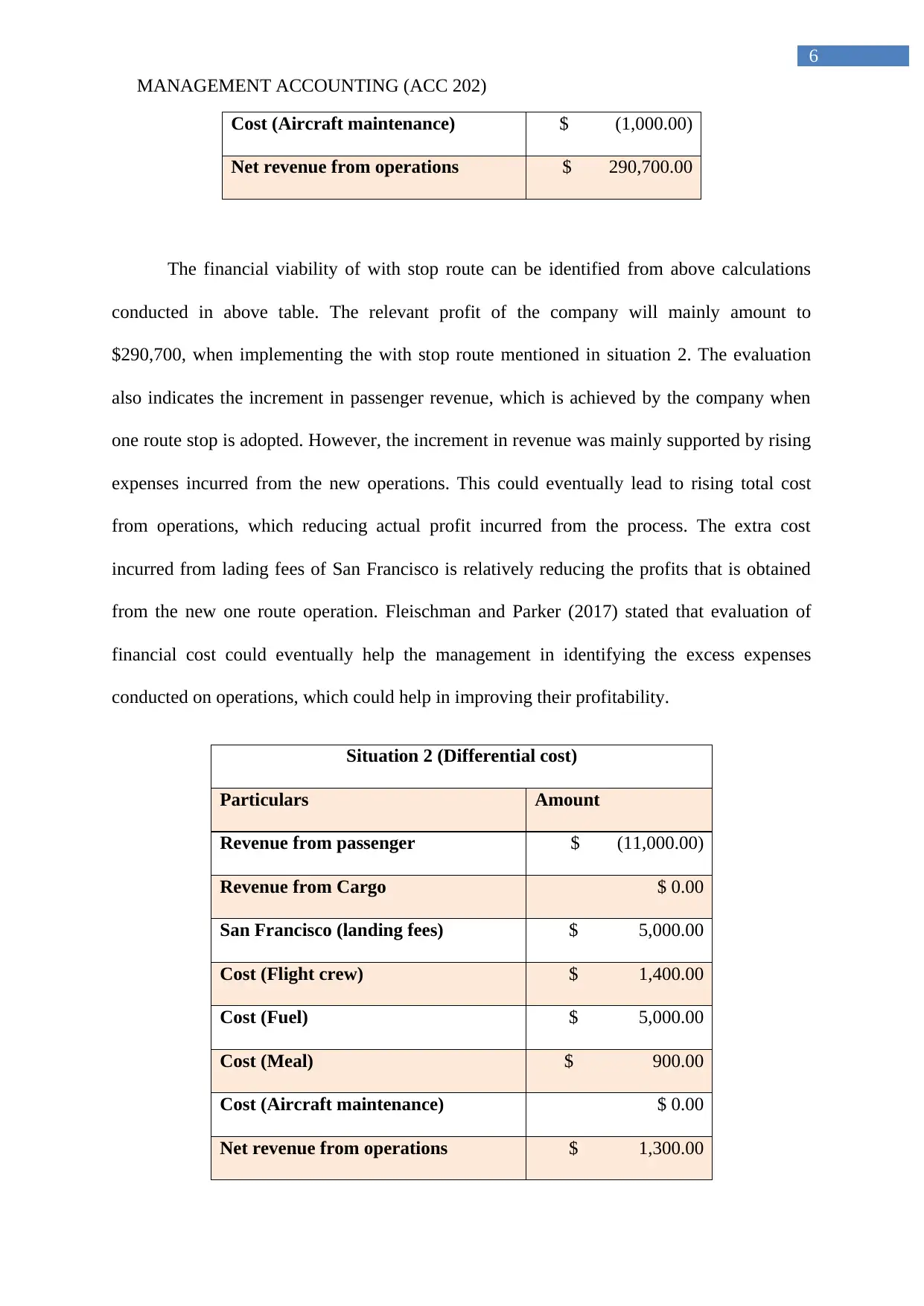

Cost (Aircraft maintenance) $ (1,000.00)

Net revenue from operations $ 290,700.00

The financial viability of with stop route can be identified from above calculations

conducted in above table. The relevant profit of the company will mainly amount to

$290,700, when implementing the with stop route mentioned in situation 2. The evaluation

also indicates the increment in passenger revenue, which is achieved by the company when

one route stop is adopted. However, the increment in revenue was mainly supported by rising

expenses incurred from the new operations. This could eventually lead to rising total cost

from operations, which reducing actual profit incurred from the process. The extra cost

incurred from lading fees of San Francisco is relatively reducing the profits that is obtained

from the new one route operation. Fleischman and Parker (2017) stated that evaluation of

financial cost could eventually help the management in identifying the excess expenses

conducted on operations, which could help in improving their profitability.

Situation 2 (Differential cost)

Particulars Amount

Revenue from passenger $ (11,000.00)

Revenue from Cargo $ 0.00

San Francisco (landing fees) $ 5,000.00

Cost (Flight crew) $ 1,400.00

Cost (Fuel) $ 5,000.00

Cost (Meal) $ 900.00

Cost (Aircraft maintenance) $ 0.00

Net revenue from operations $ 1,300.00

6

Cost (Aircraft maintenance) $ (1,000.00)

Net revenue from operations $ 290,700.00

The financial viability of with stop route can be identified from above calculations

conducted in above table. The relevant profit of the company will mainly amount to

$290,700, when implementing the with stop route mentioned in situation 2. The evaluation

also indicates the increment in passenger revenue, which is achieved by the company when

one route stop is adopted. However, the increment in revenue was mainly supported by rising

expenses incurred from the new operations. This could eventually lead to rising total cost

from operations, which reducing actual profit incurred from the process. The extra cost

incurred from lading fees of San Francisco is relatively reducing the profits that is obtained

from the new one route operation. Fleischman and Parker (2017) stated that evaluation of

financial cost could eventually help the management in identifying the excess expenses

conducted on operations, which could help in improving their profitability.

Situation 2 (Differential cost)

Particulars Amount

Revenue from passenger $ (11,000.00)

Revenue from Cargo $ 0.00

San Francisco (landing fees) $ 5,000.00

Cost (Flight crew) $ 1,400.00

Cost (Fuel) $ 5,000.00

Cost (Meal) $ 900.00

Cost (Aircraft maintenance) $ 0.00

Net revenue from operations $ 1,300.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING (ACC 202)

7

The calculation conducted on differential cost analysis is understood from the

operations, which might help in detecting financial viability of one stop route. From the

evaluation relevant loss can be identified by Flying Airline Company if one stop route is

adopted. This could eventually decline the actual profits obtained by $1,300, as expenses

from operations has increased relatively. Therefore, total revenue from implementing the one

stop route is could generate profit of $290,700, while the nonstop route could obtain

$292,000. Hence, the Flying Airline Company needs to reject the one stop route, as it will

reduce the actual revenue generated from operations. Gillion et al. (2016) mentioned that the

use of operational cost analysis could eventually help the companies in detecting financial

viability of each projects.

B) Evaluating other factors, which needs to be evaluated before conducting any decision

for Flying Airline Company:

The evaluation of overall condition presented in Situation II could help in detecting

other factors before reaching any decision. The economic factor needs to be evaluated by

Flying airline company, which could help in understating the purchasing power of

consumers. This detection of purchasing power could eventually help in understanding ability

of the consumer to pay relevant price for the services provided by Flying Airline Company.

In addition, operational increment of the company after implementing one stop route could be

identified, which might help in expanding its operations (Grant 2016). This expansion of the

operations could eventually help in generating higher revenue in long term. Both economic

and operational factor needs to be evaluated by Flying Airline Company before taking any

kind of decision based on financial perspective.

7

The calculation conducted on differential cost analysis is understood from the

operations, which might help in detecting financial viability of one stop route. From the

evaluation relevant loss can be identified by Flying Airline Company if one stop route is

adopted. This could eventually decline the actual profits obtained by $1,300, as expenses

from operations has increased relatively. Therefore, total revenue from implementing the one

stop route is could generate profit of $290,700, while the nonstop route could obtain

$292,000. Hence, the Flying Airline Company needs to reject the one stop route, as it will

reduce the actual revenue generated from operations. Gillion et al. (2016) mentioned that the

use of operational cost analysis could eventually help the companies in detecting financial

viability of each projects.

B) Evaluating other factors, which needs to be evaluated before conducting any decision

for Flying Airline Company:

The evaluation of overall condition presented in Situation II could help in detecting

other factors before reaching any decision. The economic factor needs to be evaluated by

Flying airline company, which could help in understating the purchasing power of

consumers. This detection of purchasing power could eventually help in understanding ability

of the consumer to pay relevant price for the services provided by Flying Airline Company.

In addition, operational increment of the company after implementing one stop route could be

identified, which might help in expanding its operations (Grant 2016). This expansion of the

operations could eventually help in generating higher revenue in long term. Both economic

and operational factor needs to be evaluated by Flying Airline Company before taking any

kind of decision based on financial perspective.

MANAGEMENT ACCOUNTING (ACC 202)

8

Situation 3 (Stating viability of the new special tourist charter flight proposal presented

to Flying Airline Company):

A) Stating the calculations needed by Flying Airline Compony to accept the special

tourist charter proposal when adequate spare capacity is present:

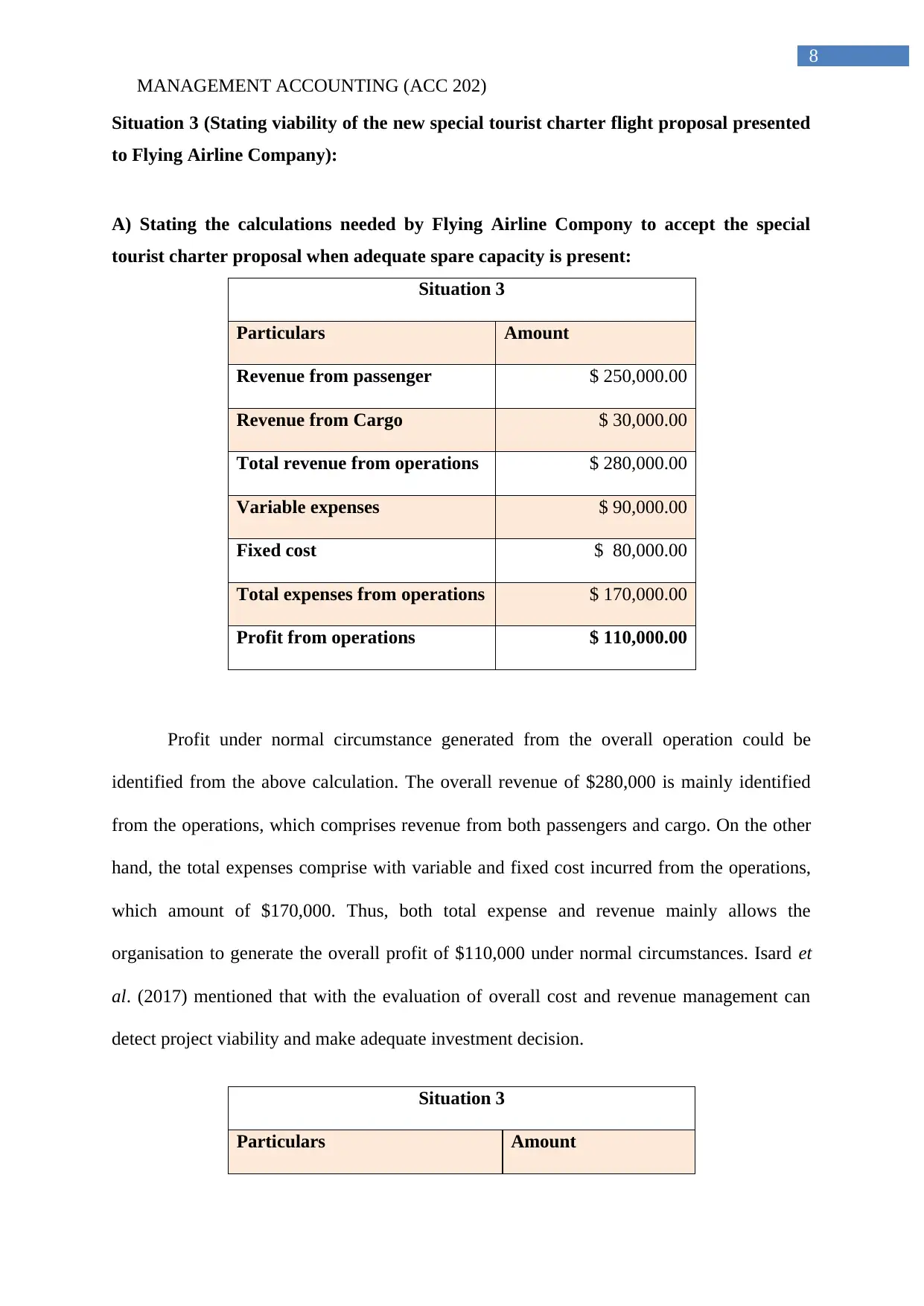

Situation 3

Particulars Amount

Revenue from passenger $ 250,000.00

Revenue from Cargo $ 30,000.00

Total revenue from operations $ 280,000.00

Variable expenses $ 90,000.00

Fixed cost $ 80,000.00

Total expenses from operations $ 170,000.00

Profit from operations $ 110,000.00

Profit under normal circumstance generated from the overall operation could be

identified from the above calculation. The overall revenue of $280,000 is mainly identified

from the operations, which comprises revenue from both passengers and cargo. On the other

hand, the total expenses comprise with variable and fixed cost incurred from the operations,

which amount of $170,000. Thus, both total expense and revenue mainly allows the

organisation to generate the overall profit of $110,000 under normal circumstances. Isard et

al. (2017) mentioned that with the evaluation of overall cost and revenue management can

detect project viability and make adequate investment decision.

Situation 3

Particulars Amount

8

Situation 3 (Stating viability of the new special tourist charter flight proposal presented

to Flying Airline Company):

A) Stating the calculations needed by Flying Airline Compony to accept the special

tourist charter proposal when adequate spare capacity is present:

Situation 3

Particulars Amount

Revenue from passenger $ 250,000.00

Revenue from Cargo $ 30,000.00

Total revenue from operations $ 280,000.00

Variable expenses $ 90,000.00

Fixed cost $ 80,000.00

Total expenses from operations $ 170,000.00

Profit from operations $ 110,000.00

Profit under normal circumstance generated from the overall operation could be

identified from the above calculation. The overall revenue of $280,000 is mainly identified

from the operations, which comprises revenue from both passengers and cargo. On the other

hand, the total expenses comprise with variable and fixed cost incurred from the operations,

which amount of $170,000. Thus, both total expense and revenue mainly allows the

organisation to generate the overall profit of $110,000 under normal circumstances. Isard et

al. (2017) mentioned that with the evaluation of overall cost and revenue management can

detect project viability and make adequate investment decision.

Situation 3

Particulars Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING (ACC 202)

9

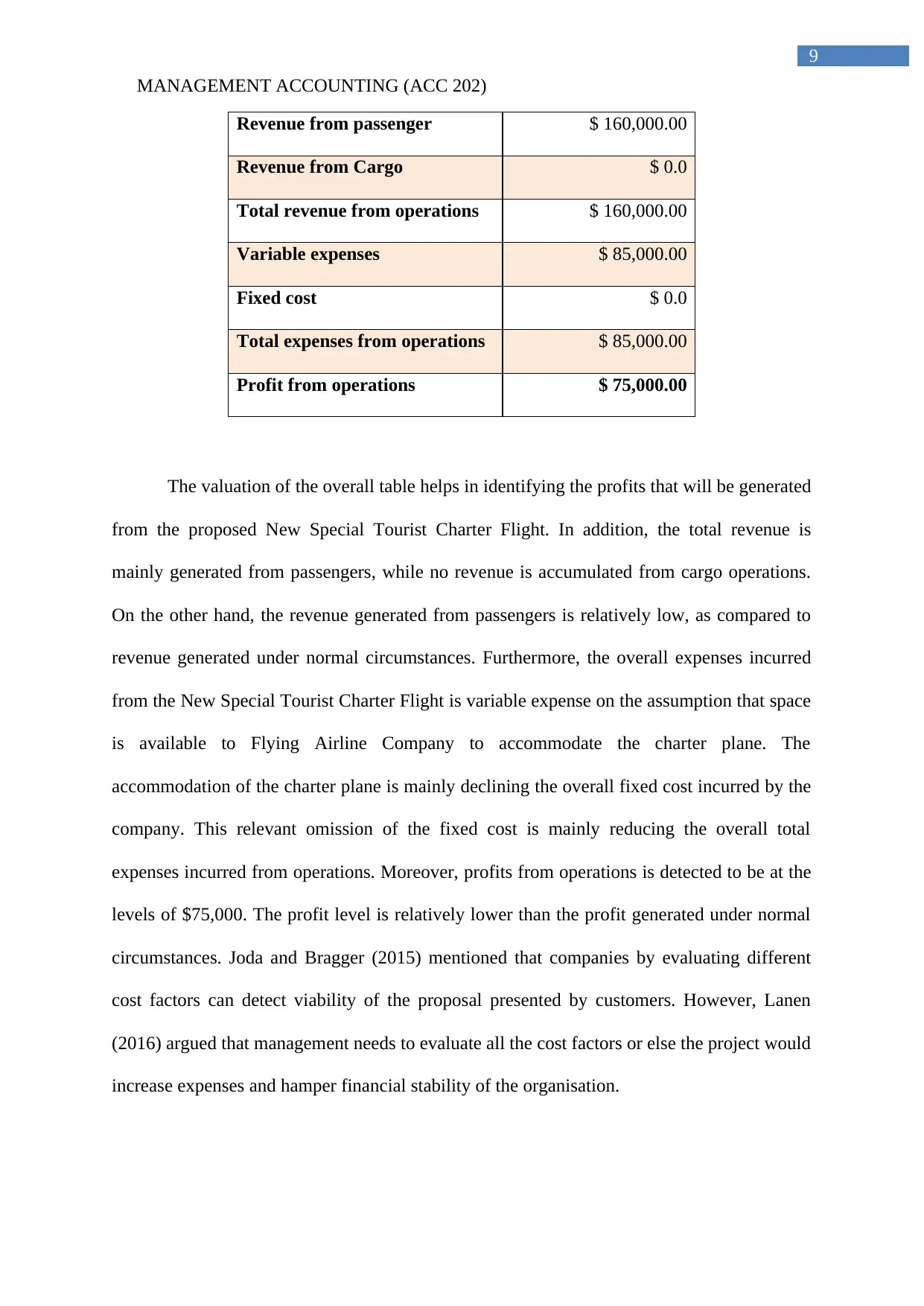

Revenue from passenger $ 160,000.00

Revenue from Cargo $ 0.0

Total revenue from operations $ 160,000.00

Variable expenses $ 85,000.00

Fixed cost $ 0.0

Total expenses from operations $ 85,000.00

Profit from operations $ 75,000.00

The valuation of the overall table helps in identifying the profits that will be generated

from the proposed New Special Tourist Charter Flight. In addition, the total revenue is

mainly generated from passengers, while no revenue is accumulated from cargo operations.

On the other hand, the revenue generated from passengers is relatively low, as compared to

revenue generated under normal circumstances. Furthermore, the overall expenses incurred

from the New Special Tourist Charter Flight is variable expense on the assumption that space

is available to Flying Airline Company to accommodate the charter plane. The

accommodation of the charter plane is mainly declining the overall fixed cost incurred by the

company. This relevant omission of the fixed cost is mainly reducing the overall total

expenses incurred from operations. Moreover, profits from operations is detected to be at the

levels of $75,000. The profit level is relatively lower than the profit generated under normal

circumstances. Joda and Bragger (2015) mentioned that companies by evaluating different

cost factors can detect viability of the proposal presented by customers. However, Lanen

(2016) argued that management needs to evaluate all the cost factors or else the project would

increase expenses and hamper financial stability of the organisation.

9

Revenue from passenger $ 160,000.00

Revenue from Cargo $ 0.0

Total revenue from operations $ 160,000.00

Variable expenses $ 85,000.00

Fixed cost $ 0.0

Total expenses from operations $ 85,000.00

Profit from operations $ 75,000.00

The valuation of the overall table helps in identifying the profits that will be generated

from the proposed New Special Tourist Charter Flight. In addition, the total revenue is

mainly generated from passengers, while no revenue is accumulated from cargo operations.

On the other hand, the revenue generated from passengers is relatively low, as compared to

revenue generated under normal circumstances. Furthermore, the overall expenses incurred

from the New Special Tourist Charter Flight is variable expense on the assumption that space

is available to Flying Airline Company to accommodate the charter plane. The

accommodation of the charter plane is mainly declining the overall fixed cost incurred by the

company. This relevant omission of the fixed cost is mainly reducing the overall total

expenses incurred from operations. Moreover, profits from operations is detected to be at the

levels of $75,000. The profit level is relatively lower than the profit generated under normal

circumstances. Joda and Bragger (2015) mentioned that companies by evaluating different

cost factors can detect viability of the proposal presented by customers. However, Lanen

(2016) argued that management needs to evaluate all the cost factors or else the project would

increase expenses and hamper financial stability of the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING (ACC 202)

10

From the overall evaluation, Flying Airline Company could eventually help in

generating higher revenue from its operations, as fixed income will be provided from the

touristy company. Hence, accepting the proposal of New Special Tourist Charter Flight could

eventually help Flying Airline Company to improves its profitability in long run. However,

under normal circumstance the company would attain higher profit, but constant orders

would not be provided. Therefore, accepting the proposal for New Special Tourist Charter

Flight could help in improving its financial viability. Li (2015) cited that cost analysis allow

the company to evaluate performance of its operations in different circumstance and detect

the minimum revenue requirement for achieving breakeven. The detection of breakeven value

and units allow the management to take operational decision for improving its current

financial capability.

B) Mentioning the viability of the new proposal with adequate calculation when there is

no space available to Flying Airline Company:

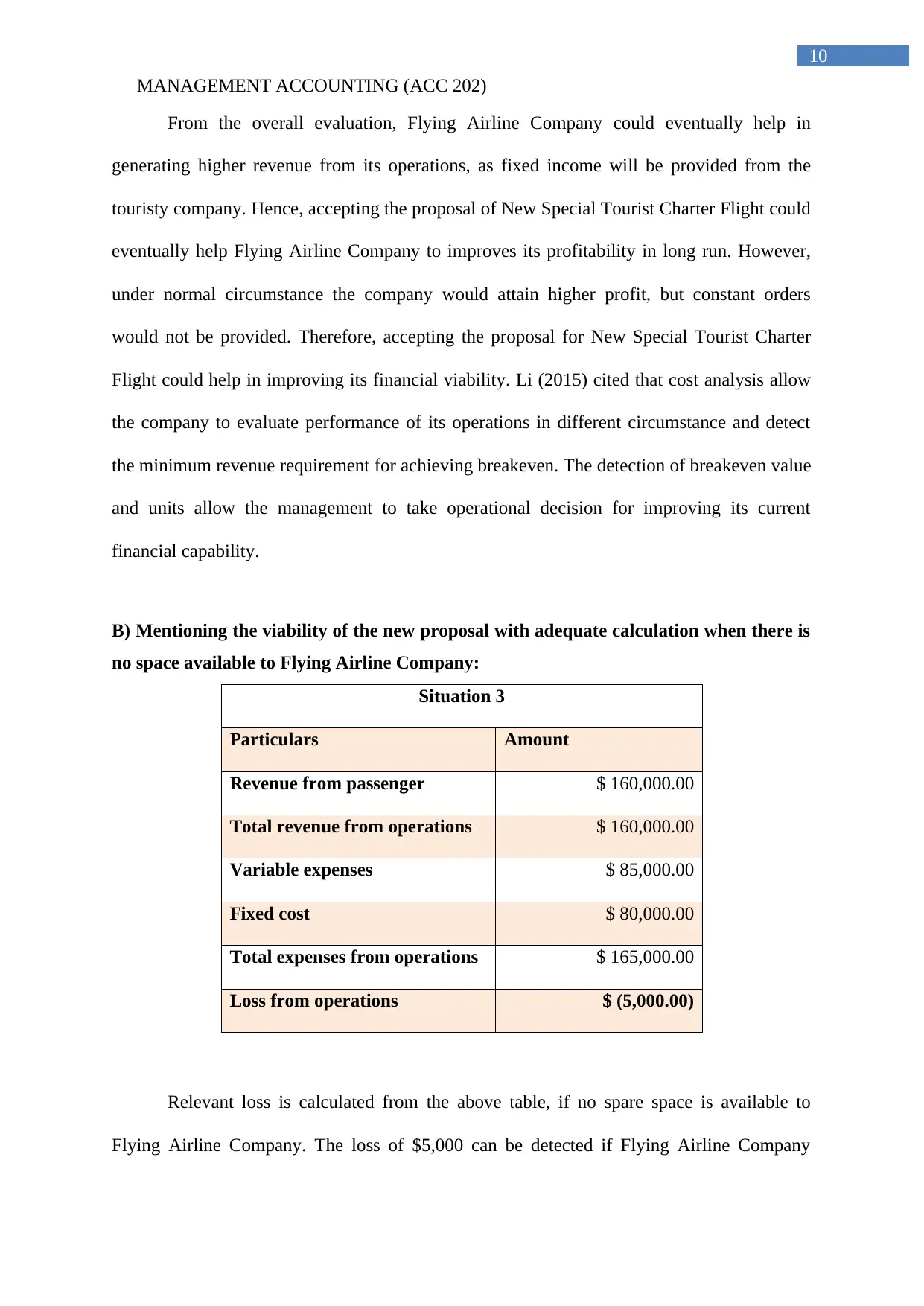

Situation 3

Particulars Amount

Revenue from passenger $ 160,000.00

Total revenue from operations $ 160,000.00

Variable expenses $ 85,000.00

Fixed cost $ 80,000.00

Total expenses from operations $ 165,000.00

Loss from operations $ (5,000.00)

Relevant loss is calculated from the above table, if no spare space is available to

Flying Airline Company. The loss of $5,000 can be detected if Flying Airline Company

10

From the overall evaluation, Flying Airline Company could eventually help in

generating higher revenue from its operations, as fixed income will be provided from the

touristy company. Hence, accepting the proposal of New Special Tourist Charter Flight could

eventually help Flying Airline Company to improves its profitability in long run. However,

under normal circumstance the company would attain higher profit, but constant orders

would not be provided. Therefore, accepting the proposal for New Special Tourist Charter

Flight could help in improving its financial viability. Li (2015) cited that cost analysis allow

the company to evaluate performance of its operations in different circumstance and detect

the minimum revenue requirement for achieving breakeven. The detection of breakeven value

and units allow the management to take operational decision for improving its current

financial capability.

B) Mentioning the viability of the new proposal with adequate calculation when there is

no space available to Flying Airline Company:

Situation 3

Particulars Amount

Revenue from passenger $ 160,000.00

Total revenue from operations $ 160,000.00

Variable expenses $ 85,000.00

Fixed cost $ 80,000.00

Total expenses from operations $ 165,000.00

Loss from operations $ (5,000.00)

Relevant loss is calculated from the above table, if no spare space is available to

Flying Airline Company. The loss of $5,000 can be detected if Flying Airline Company

MANAGEMENT ACCOUNTING (ACC 202)

11

accept the offer for New Special Tourist Charter Flight. The company will incur an extra

fixed cost of $80,000 for accommodating the new charter plane for supporting its activities.

This could eventually increase loss from operations, which will incur by Flying Airline

Company due to the increased total expenses (Marglin 2014). Hence, if no extra space is

available then the company needs to reject the proposal for New Special Tourist Charter

Flight, as it might hamper its future financial stability.

11

accept the offer for New Special Tourist Charter Flight. The company will incur an extra

fixed cost of $80,000 for accommodating the new charter plane for supporting its activities.

This could eventually increase loss from operations, which will incur by Flying Airline

Company due to the increased total expenses (Marglin 2014). Hence, if no extra space is

available then the company needs to reject the proposal for New Special Tourist Charter

Flight, as it might hamper its future financial stability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.