Accounting Report: Users of Financial Statements and Their Purposes

VerifiedAdded on 2021/02/20

|12

|3011

|57

Report

AI Summary

This report provides a comprehensive comparison of financial and management accounting, detailing their key differences in terms of definition, purpose, objective, users, and reporting focus. The report also explores the various users of financial statements, including internal users such as management and employees, and external users such as investors, trade creditors, lenders, and the government. It explains the specific purposes for which each user group utilizes financial information, highlighting how they assess a company's financial performance and make informed decisions. The report covers aspects like the differences in mandatory compliance, format of preparation, scope, and the nature of information considered in both types of accounting. Furthermore, it explains how financial accounting focuses on evaluating the overall financial position and profitability, while management accounting is more concerned with operational reports and internal decision-making within the company. The report is available on Desklib, a platform offering resources for students.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

a.) Difference between financial and management accounting..................................................1

(b) Different users of the Financial Statements of the company and their purpose of using

Financial Statements of the company-........................................................................................4

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

a.) Difference between financial and management accounting..................................................1

(b) Different users of the Financial Statements of the company and their purpose of using

Financial Statements of the company-........................................................................................4

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Accounting is the process where all the financial transactions of the company are

analysed, recorded, summarised and on the basis of the reports various interpretation are made

for the company (Accounting, 2019). Accounting is the stream under which various different

reports related to cost accounting, management accounting, Financial accounting etc. are

prepared. These reports are than used by the various users of the company who are interested in

knowing the company's financial position in order to evaluate the performance of the company.

Accounting is the vast concept which includes double entry systems and uses Generally

Accepted Accounting Principles (GAAP) to prepare financial statements for the various

companies. Accounting prepares the financial statements for the company which consists of

Trading and Profit & Loss account, Balance Sheet and Cash Flow Statement (Hoyle, 2015). The

report consists of difference between financial accounting and management accounting. It also

consists of the various users of the financial statements and purpose that why users use this

information.

MAIN BODY

a.) Difference between financial and management accounting.

PARTICULARS FINANCIAL

ACCOUNTING

MANAGEMENT

ACCOUNTING

1

Accounting is the process where all the financial transactions of the company are

analysed, recorded, summarised and on the basis of the reports various interpretation are made

for the company (Accounting, 2019). Accounting is the stream under which various different

reports related to cost accounting, management accounting, Financial accounting etc. are

prepared. These reports are than used by the various users of the company who are interested in

knowing the company's financial position in order to evaluate the performance of the company.

Accounting is the vast concept which includes double entry systems and uses Generally

Accepted Accounting Principles (GAAP) to prepare financial statements for the various

companies. Accounting prepares the financial statements for the company which consists of

Trading and Profit & Loss account, Balance Sheet and Cash Flow Statement (Hoyle, 2015). The

report consists of difference between financial accounting and management accounting. It also

consists of the various users of the financial statements and purpose that why users use this

information.

MAIN BODY

a.) Difference between financial and management accounting.

PARTICULARS FINANCIAL

ACCOUNTING

MANAGEMENT

ACCOUNTING

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

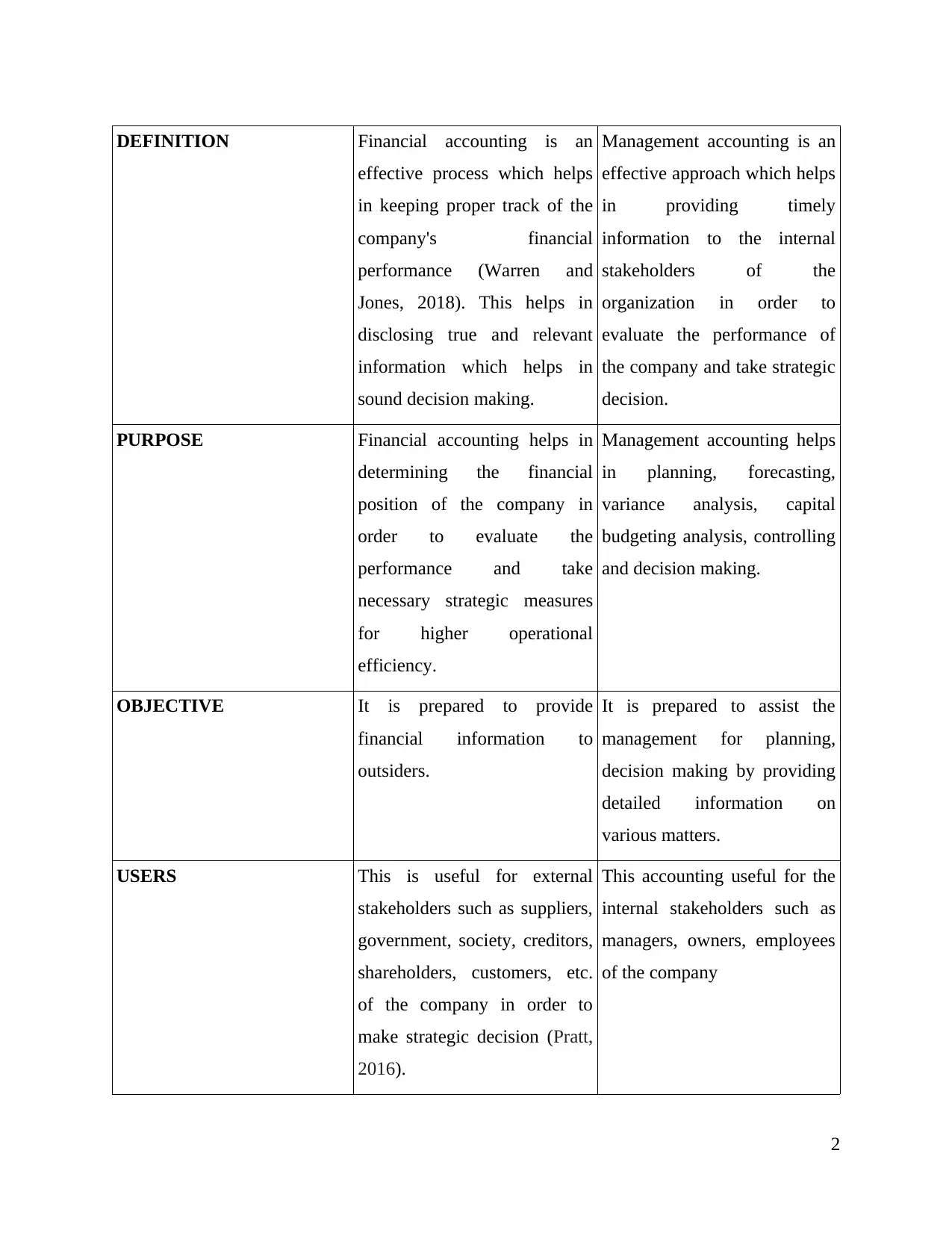

DEFINITION Financial accounting is an

effective process which helps

in keeping proper track of the

company's financial

performance (Warren and

Jones, 2018). This helps in

disclosing true and relevant

information which helps in

sound decision making.

Management accounting is an

effective approach which helps

in providing timely

information to the internal

stakeholders of the

organization in order to

evaluate the performance of

the company and take strategic

decision.

PURPOSE Financial accounting helps in

determining the financial

position of the company in

order to evaluate the

performance and take

necessary strategic measures

for higher operational

efficiency.

Management accounting helps

in planning, forecasting,

variance analysis, capital

budgeting analysis, controlling

and decision making.

OBJECTIVE It is prepared to provide

financial information to

outsiders.

It is prepared to assist the

management for planning,

decision making by providing

detailed information on

various matters.

USERS This is useful for external

stakeholders such as suppliers,

government, society, creditors,

shareholders, customers, etc.

of the company in order to

make strategic decision (Pratt,

2016).

This accounting useful for the

internal stakeholders such as

managers, owners, employees

of the company

2

effective process which helps

in keeping proper track of the

company's financial

performance (Warren and

Jones, 2018). This helps in

disclosing true and relevant

information which helps in

sound decision making.

Management accounting is an

effective approach which helps

in providing timely

information to the internal

stakeholders of the

organization in order to

evaluate the performance of

the company and take strategic

decision.

PURPOSE Financial accounting helps in

determining the financial

position of the company in

order to evaluate the

performance and take

necessary strategic measures

for higher operational

efficiency.

Management accounting helps

in planning, forecasting,

variance analysis, capital

budgeting analysis, controlling

and decision making.

OBJECTIVE It is prepared to provide

financial information to

outsiders.

It is prepared to assist the

management for planning,

decision making by providing

detailed information on

various matters.

USERS This is useful for external

stakeholders such as suppliers,

government, society, creditors,

shareholders, customers, etc.

of the company in order to

make strategic decision (Pratt,

2016).

This accounting useful for the

internal stakeholders such as

managers, owners, employees

of the company

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

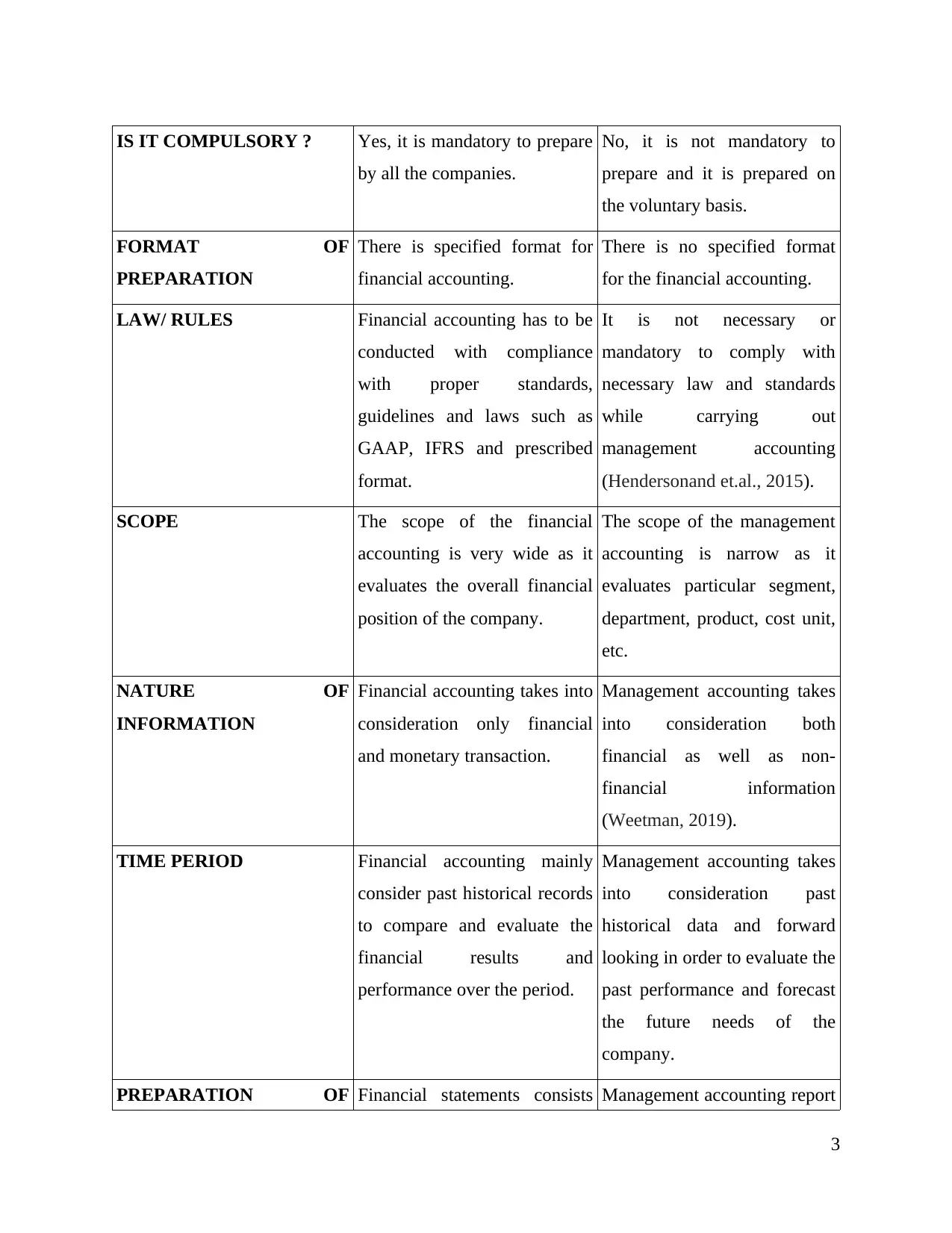

IS IT COMPULSORY ? Yes, it is mandatory to prepare

by all the companies.

No, it is not mandatory to

prepare and it is prepared on

the voluntary basis.

FORMAT OF

PREPARATION

There is specified format for

financial accounting.

There is no specified format

for the financial accounting.

LAW/ RULES Financial accounting has to be

conducted with compliance

with proper standards,

guidelines and laws such as

GAAP, IFRS and prescribed

format.

It is not necessary or

mandatory to comply with

necessary law and standards

while carrying out

management accounting

(Hendersonand et.al., 2015).

SCOPE The scope of the financial

accounting is very wide as it

evaluates the overall financial

position of the company.

The scope of the management

accounting is narrow as it

evaluates particular segment,

department, product, cost unit,

etc.

NATURE OF

INFORMATION

Financial accounting takes into

consideration only financial

and monetary transaction.

Management accounting takes

into consideration both

financial as well as non-

financial information

(Weetman, 2019).

TIME PERIOD Financial accounting mainly

consider past historical records

to compare and evaluate the

financial results and

performance over the period.

Management accounting takes

into consideration past

historical data and forward

looking in order to evaluate the

past performance and forecast

the future needs of the

company.

PREPARATION OF Financial statements consists Management accounting report

3

by all the companies.

No, it is not mandatory to

prepare and it is prepared on

the voluntary basis.

FORMAT OF

PREPARATION

There is specified format for

financial accounting.

There is no specified format

for the financial accounting.

LAW/ RULES Financial accounting has to be

conducted with compliance

with proper standards,

guidelines and laws such as

GAAP, IFRS and prescribed

format.

It is not necessary or

mandatory to comply with

necessary law and standards

while carrying out

management accounting

(Hendersonand et.al., 2015).

SCOPE The scope of the financial

accounting is very wide as it

evaluates the overall financial

position of the company.

The scope of the management

accounting is narrow as it

evaluates particular segment,

department, product, cost unit,

etc.

NATURE OF

INFORMATION

Financial accounting takes into

consideration only financial

and monetary transaction.

Management accounting takes

into consideration both

financial as well as non-

financial information

(Weetman, 2019).

TIME PERIOD Financial accounting mainly

consider past historical records

to compare and evaluate the

financial results and

performance over the period.

Management accounting takes

into consideration past

historical data and forward

looking in order to evaluate the

past performance and forecast

the future needs of the

company.

PREPARATION OF Financial statements consists Management accounting report

3

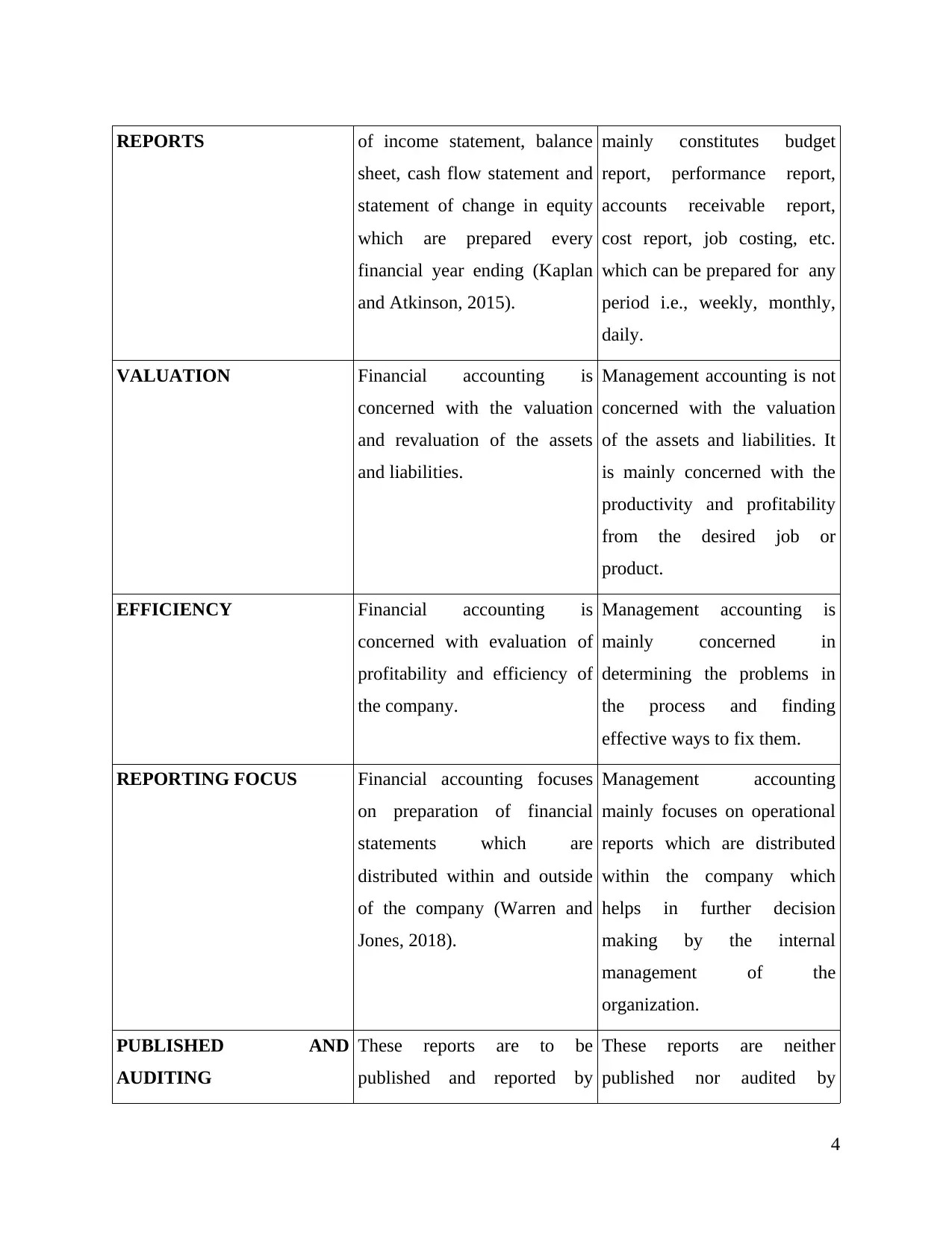

REPORTS of income statement, balance

sheet, cash flow statement and

statement of change in equity

which are prepared every

financial year ending (Kaplan

and Atkinson, 2015).

mainly constitutes budget

report, performance report,

accounts receivable report,

cost report, job costing, etc.

which can be prepared for any

period i.e., weekly, monthly,

daily.

VALUATION Financial accounting is

concerned with the valuation

and revaluation of the assets

and liabilities.

Management accounting is not

concerned with the valuation

of the assets and liabilities. It

is mainly concerned with the

productivity and profitability

from the desired job or

product.

EFFICIENCY Financial accounting is

concerned with evaluation of

profitability and efficiency of

the company.

Management accounting is

mainly concerned in

determining the problems in

the process and finding

effective ways to fix them.

REPORTING FOCUS Financial accounting focuses

on preparation of financial

statements which are

distributed within and outside

of the company (Warren and

Jones, 2018).

Management accounting

mainly focuses on operational

reports which are distributed

within the company which

helps in further decision

making by the internal

management of the

organization.

PUBLISHED AND

AUDITING

These reports are to be

published and reported by

These reports are neither

published nor audited by

4

sheet, cash flow statement and

statement of change in equity

which are prepared every

financial year ending (Kaplan

and Atkinson, 2015).

mainly constitutes budget

report, performance report,

accounts receivable report,

cost report, job costing, etc.

which can be prepared for any

period i.e., weekly, monthly,

daily.

VALUATION Financial accounting is

concerned with the valuation

and revaluation of the assets

and liabilities.

Management accounting is not

concerned with the valuation

of the assets and liabilities. It

is mainly concerned with the

productivity and profitability

from the desired job or

product.

EFFICIENCY Financial accounting is

concerned with evaluation of

profitability and efficiency of

the company.

Management accounting is

mainly concerned in

determining the problems in

the process and finding

effective ways to fix them.

REPORTING FOCUS Financial accounting focuses

on preparation of financial

statements which are

distributed within and outside

of the company (Warren and

Jones, 2018).

Management accounting

mainly focuses on operational

reports which are distributed

within the company which

helps in further decision

making by the internal

management of the

organization.

PUBLISHED AND

AUDITING

These reports are to be

published and reported by

These reports are neither

published nor audited by

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statutory auditors. statutory auditors (Kaplan and

Atkinson, 2015).

(b) Different users of the Financial Statements of the company and their purpose of using

Financial Statements of the company-

Financial Statements are used by the person who are interested in knowing the financial

position of the company in order to know the performance of the company (Hoque, 2018). These

users are either having existing business with the company or either they want to enter into new

business with the company in near future. There are two types of users of the company i.e.

Internal users and External users. Internal users of the financial statements are within the

organisation only. Internal users of the company are those who uses company's financial

statements in order to take certain decisions for the company. For example, Management, etc.

External users of the company are those who are not involved in taking the decisions for the

company but have some financial interest in the company. External users are outside the

organisation and does not work within the organisation. For example, Government, Customers,

Trade Creditors, Investors etc. The different types of users of Financial Statements of the

company are-

Internal users of the financial statements of the company-

Management-

The main user of the financial statement of the company are Management. Management

is the internal user of the financial statements of the company. They are the one who are highly

interested in the Financial Statements of the company. They consist of Board of Directors,

managers and other officers of the business (Hawn, 2016). They are interested in the company's

financial statements because they are the one who evaluate the performance of the business and

take certain decisions related to the company. They are interested in knowing the profits of the

company and by evaluating performance of the company using ratio analysis techniques. These

techniques helps managers in knowing that whether the company will be meeting all its

obligations on time or not. These ratio helps them to know the liquidity, profitability and

5

Atkinson, 2015).

(b) Different users of the Financial Statements of the company and their purpose of using

Financial Statements of the company-

Financial Statements are used by the person who are interested in knowing the financial

position of the company in order to know the performance of the company (Hoque, 2018). These

users are either having existing business with the company or either they want to enter into new

business with the company in near future. There are two types of users of the company i.e.

Internal users and External users. Internal users of the financial statements are within the

organisation only. Internal users of the company are those who uses company's financial

statements in order to take certain decisions for the company. For example, Management, etc.

External users of the company are those who are not involved in taking the decisions for the

company but have some financial interest in the company. External users are outside the

organisation and does not work within the organisation. For example, Government, Customers,

Trade Creditors, Investors etc. The different types of users of Financial Statements of the

company are-

Internal users of the financial statements of the company-

Management-

The main user of the financial statement of the company are Management. Management

is the internal user of the financial statements of the company. They are the one who are highly

interested in the Financial Statements of the company. They consist of Board of Directors,

managers and other officers of the business (Hawn, 2016). They are interested in the company's

financial statements because they are the one who evaluate the performance of the business and

take certain decisions related to the company. They are interested in knowing the profits of the

company and by evaluating performance of the company using ratio analysis techniques. These

techniques helps managers in knowing that whether the company will be meeting all its

obligations on time or not. These ratio helps them to know the liquidity, profitability and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

solvency position of the company. The main purpose of using financial statements by

management is to take the decisions for the company based on their profits or losses.

Employees-

Employees are the internal users of Financial Information of the company. They are the

individuals who are within the organisation and work for the organisation. The main purpose of

employees to use the Financial Information is to know the profitability of the company in order

to know the growth of the company (Watson, and et.al., 2018). Based on the growth of the

company employees decide whether to leave the company or retain in the company. Any

employee who wants to grow faster will always be ensuring that the company in which they are

working should also be growing company. This helps the employees to also grow faster and

ensures that the company is growing in positive direction.

External users of Financial Statements of the company-

Investors or potential Investors-

Investors are the external user of the financial statements of the company. They are the

one who wants to invest in the company in order to maximize their profits. Investors are

generally interested in the past financial statements of the company for knowing the future

potential of the company. The main purpose of using company's financial statements is to know

that whether there investments in the company will be profitable or not. Current investors uses

this information to know whether the company will be giving all the returns to investors for

which they have promised or not. Potential Investors uses company's financial statements in

order to know that whether to invest in the company or not (Herremans, 2016). Financial

statements helps the potential investors in assessing profitable investments. They are generally

interested in the profitability, turnover ratios of the company.

Trade Creditors or Suppliers-

Trade creditors or suppliers are external users of financial statements of the company.

Trade creditors are those persons who give the goods on credit to the company. The main

purpose of trade creditors to use the financial information of the company is to know whether the

company will be paying its debt on time or not. They are interested in knowing the company's

6

management is to take the decisions for the company based on their profits or losses.

Employees-

Employees are the internal users of Financial Information of the company. They are the

individuals who are within the organisation and work for the organisation. The main purpose of

employees to use the Financial Information is to know the profitability of the company in order

to know the growth of the company (Watson, and et.al., 2018). Based on the growth of the

company employees decide whether to leave the company or retain in the company. Any

employee who wants to grow faster will always be ensuring that the company in which they are

working should also be growing company. This helps the employees to also grow faster and

ensures that the company is growing in positive direction.

External users of Financial Statements of the company-

Investors or potential Investors-

Investors are the external user of the financial statements of the company. They are the

one who wants to invest in the company in order to maximize their profits. Investors are

generally interested in the past financial statements of the company for knowing the future

potential of the company. The main purpose of using company's financial statements is to know

that whether there investments in the company will be profitable or not. Current investors uses

this information to know whether the company will be giving all the returns to investors for

which they have promised or not. Potential Investors uses company's financial statements in

order to know that whether to invest in the company or not (Herremans, 2016). Financial

statements helps the potential investors in assessing profitable investments. They are generally

interested in the profitability, turnover ratios of the company.

Trade Creditors or Suppliers-

Trade creditors or suppliers are external users of financial statements of the company.

Trade creditors are those persons who give the goods on credit to the company. The main

purpose of trade creditors to use the financial information of the company is to know whether the

company will be paying its debt on time or not. They are interested in knowing the company's

6

liquidity position to check whether they have the ability to pay short term obligations or not

(Ramus, 2017). Also, they check the cash inflows and outflows of the company. Financial

Information also helps creditors in knowing the extent of amount of credit to be allowed, credit

period and application of other credit policies. This information also helps knowing the

creditworthiness of the company and decide whether to continue providing goods or not.

Lenders-

Lenders are the external users of financial statements of the company. Lenders are the

individuals or financial institutions who lend the money to the company in the form of loans

(Hameed, And et.al., 2016). The main purpose of lenders to use the financial information is to

know the profitability of the company. The main decision of the lenders are based on knowing

whether lenders can pay back their loans or not. Financial information helps lenders in knowing

the financial performance of the company and whether they can pay principal and interest

amount back to lenders or not. They check the short term as well as long term solvency of the

company through various solvency ratios. In this way lenders uses the financial statements of the

company.

Government-

Government is the external user of financial statements of the company. They keep close

watch on the performance of every firm that whether they yield good amount of profits or not.

The main purpose of Government in using financial statements is to know the earnings of the

company for the purpose of taxation (Leonidou, And et.al., 2017). Government is interested in

knowing that whether the company is paying taxes are according their taxes or not. Government

also ensures that the management of the business are also profitable or not and to safeguard them

from any problem. Both the Government i.e. State and Central Government are interested in

knowing the profits of the company in order to know whether the company is paying full taxes

based on their income.

Customers-

Customers are also external user of financial statements of the company. Customers are

the individuals who buy the products from the company. They are less interested in the financial

statements of the company. The main purpose of customers to use financial statements of the

7

(Ramus, 2017). Also, they check the cash inflows and outflows of the company. Financial

Information also helps creditors in knowing the extent of amount of credit to be allowed, credit

period and application of other credit policies. This information also helps knowing the

creditworthiness of the company and decide whether to continue providing goods or not.

Lenders-

Lenders are the external users of financial statements of the company. Lenders are the

individuals or financial institutions who lend the money to the company in the form of loans

(Hameed, And et.al., 2016). The main purpose of lenders to use the financial information is to

know the profitability of the company. The main decision of the lenders are based on knowing

whether lenders can pay back their loans or not. Financial information helps lenders in knowing

the financial performance of the company and whether they can pay principal and interest

amount back to lenders or not. They check the short term as well as long term solvency of the

company through various solvency ratios. In this way lenders uses the financial statements of the

company.

Government-

Government is the external user of financial statements of the company. They keep close

watch on the performance of every firm that whether they yield good amount of profits or not.

The main purpose of Government in using financial statements is to know the earnings of the

company for the purpose of taxation (Leonidou, And et.al., 2017). Government is interested in

knowing that whether the company is paying taxes are according their taxes or not. Government

also ensures that the management of the business are also profitable or not and to safeguard them

from any problem. Both the Government i.e. State and Central Government are interested in

knowing the profits of the company in order to know whether the company is paying full taxes

based on their income.

Customers-

Customers are also external user of financial statements of the company. Customers are

the individuals who buy the products from the company. They are less interested in the financial

statements of the company. The main purpose of customers to use financial statements of the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company is to know the establishment of proper accounting control because that leads to the

reduction in the cost of production (Watson, and et.al., 2018). It leads to the reduction in the

price of the goods paid by the customers to the company. They are interested in knowing that the

goods are sold at reduced price or not. Customers are also interested in knowing whether the

company will be surviving for the longer period to honour their product warranties or not. The

main purpose of the customers is to know whether the company is selling its products at fair

price or not.

CONCLUSION

The report consists of knowing what are the parts or types of accounting and what are the

various users of the financial statements of the company. Accounting helps in the preparation of

financial statements by preparing various reports for the company. These reports helps in taking

certain decisions for the company by the management. There are various differences between the

financial accounting and management accounting (Hueske, 2015). Financial Accounting takes

only monetary transactions into the account whereas management accounting is to evaluate the

performance of the company. Financial Information of the company are used by internal and

external stakeholders. These stakeholders use the financial statements in order to take certain

decisions for the company. Few uses this information in order to know the liquidity, profitability

and solvency ratios of the company. These ratios help in the evaluation of performance of the

company using ratio analysis techniques. There are various purpose of users for using the

financial information of the company. Some uses the financial information for lending loans,

some for tax purpose, some for decision taking for the company.

8

reduction in the cost of production (Watson, and et.al., 2018). It leads to the reduction in the

price of the goods paid by the customers to the company. They are interested in knowing that the

goods are sold at reduced price or not. Customers are also interested in knowing whether the

company will be surviving for the longer period to honour their product warranties or not. The

main purpose of the customers is to know whether the company is selling its products at fair

price or not.

CONCLUSION

The report consists of knowing what are the parts or types of accounting and what are the

various users of the financial statements of the company. Accounting helps in the preparation of

financial statements by preparing various reports for the company. These reports helps in taking

certain decisions for the company by the management. There are various differences between the

financial accounting and management accounting (Hueske, 2015). Financial Accounting takes

only monetary transactions into the account whereas management accounting is to evaluate the

performance of the company. Financial Information of the company are used by internal and

external stakeholders. These stakeholders use the financial statements in order to take certain

decisions for the company. Few uses this information in order to know the liquidity, profitability

and solvency ratios of the company. These ratios help in the evaluation of performance of the

company using ratio analysis techniques. There are various purpose of users for using the

financial information of the company. Some uses the financial information for lending loans,

some for tax purpose, some for decision taking for the company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Hameed, I. and et.al., 2016. How do internal and external CSR affect employees' organizational

identification? A perspective from the group engagement model. Frontiers in

psychology. 7. p.788.

Hawn, O. and Ioannou, I., 2016. Mind the gap: The interplay between external and internal

actions in the case of corporate social responsibility. Strategic Management

Journal. 37(13). pp.2569-2588.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Herremans, I. M., Nazari, J. A. and Mahmoudian, F. 2016. Stakeholder relationships,

engagement, and sustainability reporting. Journal of Business Ethics. 138(3). pp.417-435.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Hoyle, J. B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Hueske, A. K. and Guenther, E., 2015. What hampers innovation? External stakeholders, the

organization, groups and individuals: a systematic review of empirical barrier

research. Management Review Quarterly. 65(2). pp.113-148.

Leonidou, L. C. and et.al., 2017. Internal drivers and performance consequences of small firm

green business strategy: The moderating role of external forces. Journal of Business

Ethics. 140(3). pp.585-606.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Ramus, T. and Vaccaro, A. 2017. Stakeholders matter: How social enterprises address mission

drift. Journal of Business Ethics. 143(2). pp.307-322.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, R. and et.al., 2018. Harnessing difference: a capability‐based framework for stakeholder

engagement in environmental innovation. Journal of Product Innovation

Management. 35(2). pp.254-279.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

9

Books and Journals

Hameed, I. and et.al., 2016. How do internal and external CSR affect employees' organizational

identification? A perspective from the group engagement model. Frontiers in

psychology. 7. p.788.

Hawn, O. and Ioannou, I., 2016. Mind the gap: The interplay between external and internal

actions in the case of corporate social responsibility. Strategic Management

Journal. 37(13). pp.2569-2588.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Herremans, I. M., Nazari, J. A. and Mahmoudian, F. 2016. Stakeholder relationships,

engagement, and sustainability reporting. Journal of Business Ethics. 138(3). pp.417-435.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Hoyle, J. B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Hueske, A. K. and Guenther, E., 2015. What hampers innovation? External stakeholders, the

organization, groups and individuals: a systematic review of empirical barrier

research. Management Review Quarterly. 65(2). pp.113-148.

Leonidou, L. C. and et.al., 2017. Internal drivers and performance consequences of small firm

green business strategy: The moderating role of external forces. Journal of Business

Ethics. 140(3). pp.585-606.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Ramus, T. and Vaccaro, A. 2017. Stakeholders matter: How social enterprises address mission

drift. Journal of Business Ethics. 143(2). pp.307-322.

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, R. and et.al., 2018. Harnessing difference: a capability‐based framework for stakeholder

engagement in environmental innovation. Journal of Product Innovation

Management. 35(2). pp.254-279.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

9

Online

Accounting. 2019. (Online). Available through <https://www.accountingcoach.com/accounting-

basics/explanation>

10

Accounting. 2019. (Online). Available through <https://www.accountingcoach.com/accounting-

basics/explanation>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.