Business Finance: Financial and Management Accounting Comparison

VerifiedAdded on 2023/01/11

|6

|1322

|71

Report

AI Summary

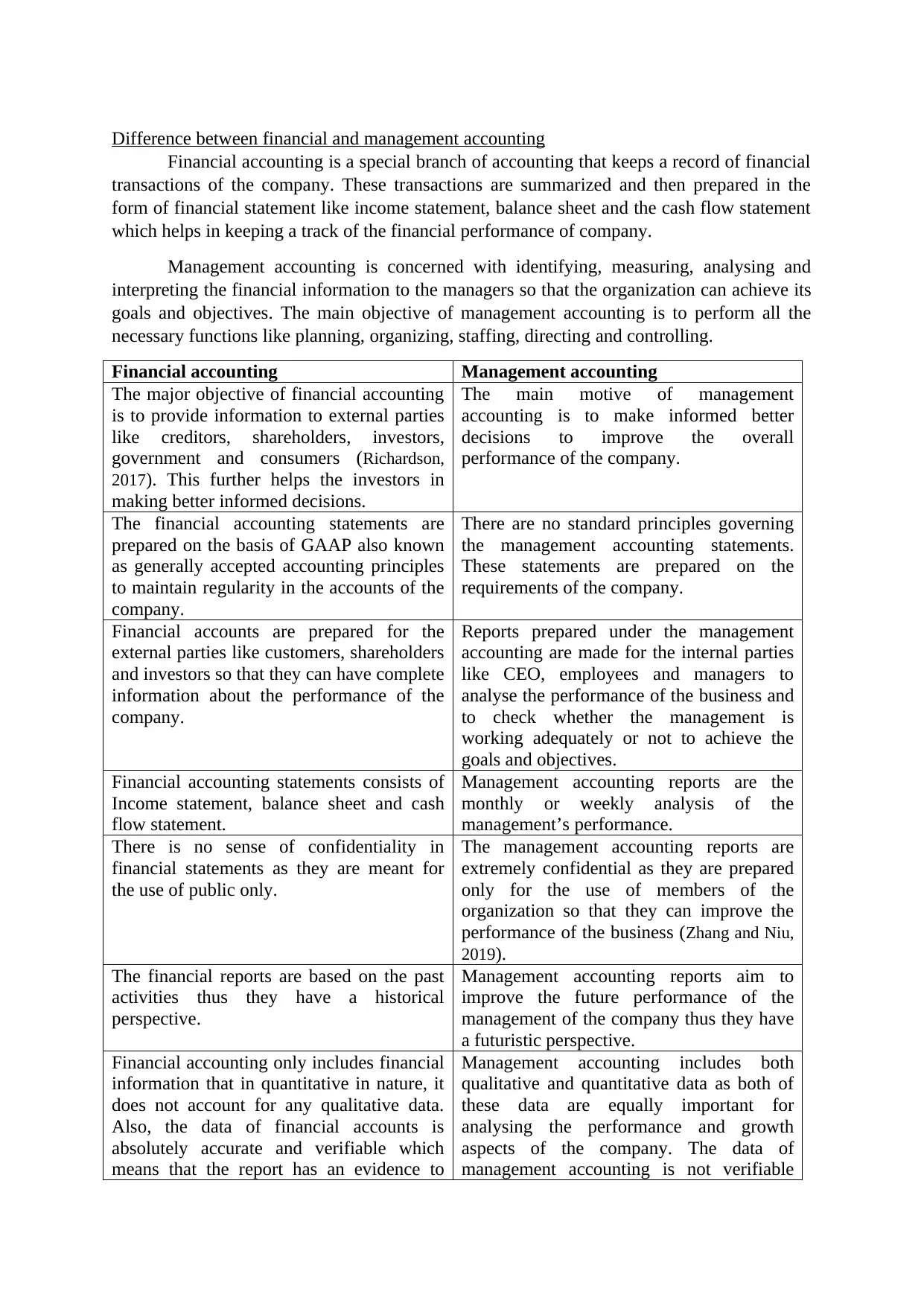

This report provides a comprehensive comparison between financial accounting and management accounting. It highlights the key distinctions in their objectives, users, principles, and the nature of the information they present. Financial accounting focuses on providing information to external parties like investors and creditors, adhering to GAAP and presenting historical, verifiable financial data through statements such as income statements, balance sheets, and cash flow statements. Management accounting, on the other hand, is geared towards internal users like managers, aiding in decision-making, planning, and control, using both qualitative and quantitative data, and offering a future-oriented perspective. The report further explores the usefulness of financial information to various stakeholders, including owners, creditors, employees, investors, the government, consumers, and stock exchanges, emphasizing how each group relies on financial data to assess business performance, make informed decisions, and ensure financial stability. The report also includes references to academic sources.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.